India Wealth Management Market Size, Share, Trends and Forecast by Business Model, Provider, End User, and Region, 2026-2034

India Wealth Management Market Summary:

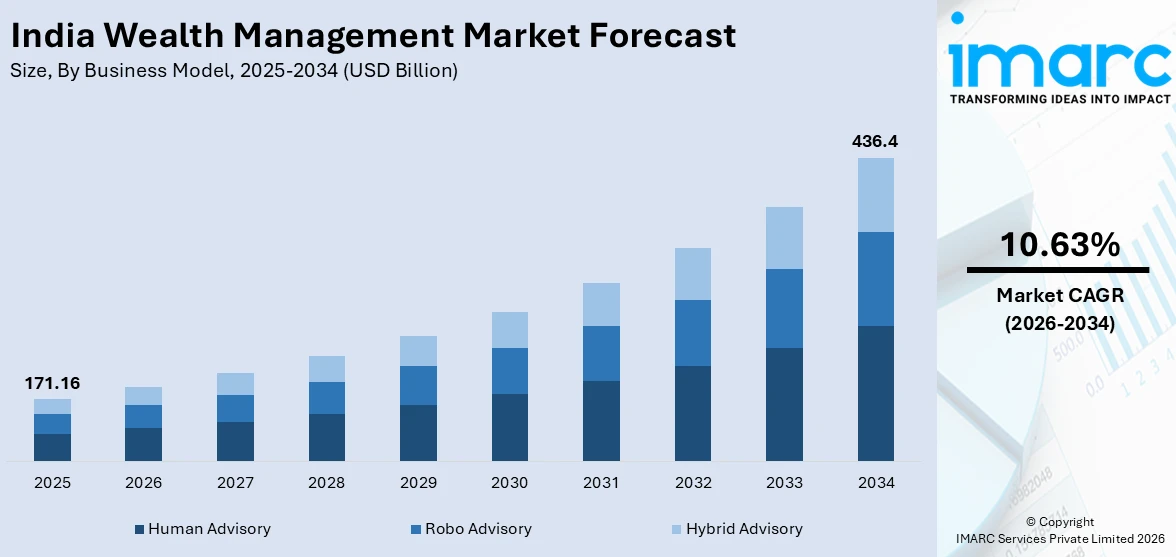

The India wealth management market size was valued at USD 171.16 Billion in 2025 and is projected to reach USD 436.4 Billion by 2034, growing at a compound annual growth rate of 10.63% from 2026-2034.

The India wealth management market is experiencing robust expansion, underpinned by rising affluence, increasing financialization of household savings, and growing demand for personalized advisory services. The shift from traditional physical asset investments toward diversified financial portfolios is accelerating adoption across investor segments. A younger, digitally savvy generation of investors is reshaping service expectations, while expanding wealth creation in tier-two and tier-three cities is broadening the addressable market for wealth management solutions across the India wealth management market share.

Key Takeaways and Insights:

-

By Business Model: Human advisory dominates the market with a share of 46.2% in 2025, driven by the enduring preference among affluent investors for personalized, relationship-driven financial guidance and tailored wealth planning services.

-

By Provider: Banks hold the largest market share of 41.7% in 2025, leveraging their extensive branch networks, established customer trust, diversified product portfolios, and integrated financial service ecosystems to capture the leading position.

-

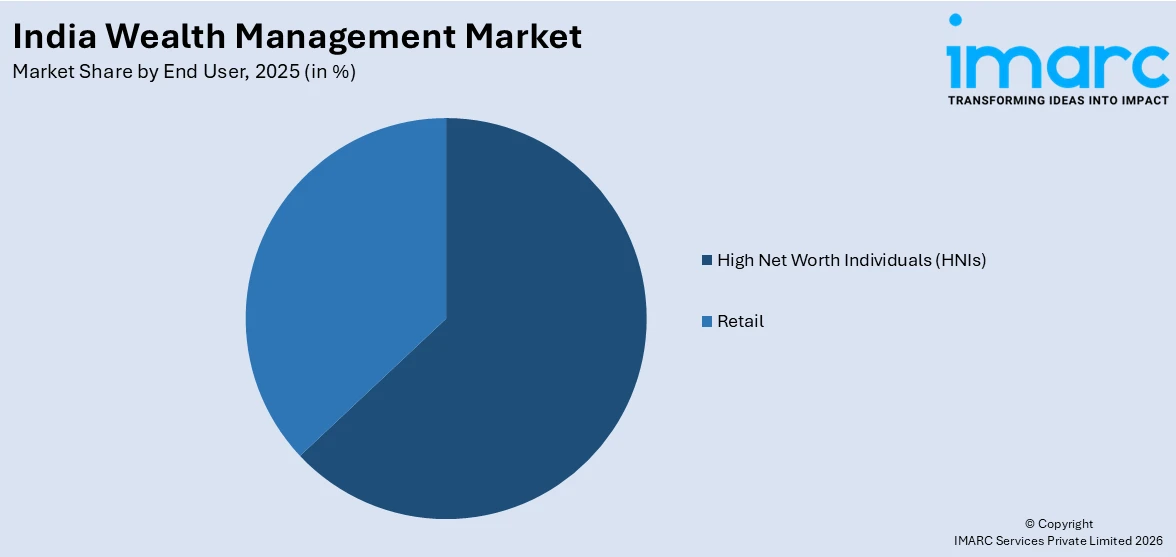

By End User: High net worth individuals (HNIs) dominate the market with a share of 62.8% in 2025, reflecting the growing population of affluent investors seeking sophisticated portfolio management, estate planning, and global diversification strategies.

-

By Region: West India leads the market with a share of 32.9% in 2025, supported by the concentration of financial institutions, corporate headquarters, and a high density of wealthy individuals in the region.

-

Key Players: The India wealth management market is highly competitive, with established financial institutions, independent advisory firms, and emerging fintech platforms competing through product innovation, digital capabilities, personalized service offerings, and strategic partnerships to strengthen market share and expand client reach.

To get more information on this market Request Sample

The India wealth management market is advancing as the country's economic growth trajectory accelerates wealth creation across diverse segments. Rising disposable incomes, increased financial literacy, and the growing sophistication of investment preferences are driving demand for comprehensive wealth management solutions. In November 2025, India’s alternative investment ecosystem, including Portfolio Management Services (PMS) and Alternative Investment Funds (AIFs) collectively surpassed ₹23.43 lakh crore in assets under management, underscoring affluent investors’ shift toward diversified, structured investment products. The transition from physical assets such as gold and real estate toward financial instruments including equities, mutual funds, and alternative investments is reshaping portfolio compositions. Regulatory reforms, digital transformation, and the emergence of hybrid advisory models that blend technology with human expertise are further strengthening the ecosystem. Additionally, the expansion of wealth creation to smaller cities beyond traditional metropolitan hubs is creating significant opportunities for service providers to penetrate underserved markets.

India Wealth Management Market Trends:

Rising Adoption of Digital and Hybrid Advisory Models

The wealth management industry is witnessing a significant shift toward digital platforms and hybrid advisory models that combine technology-driven insights with personalized human guidance. Robo-advisory services, artificial intelligence-powered portfolio management, and mobile-first investment platforms are gaining traction among younger and tech-savvy investors. In 2025, approximately 70% of wealth management firms in India adopted AI‑driven advisory or robo‑advisory tools, enabling real‑time insights and personalised portfolio suggestions for clients. This digital transformation is enabling wealth managers to deliver scalable, cost-effective advisory services while maintaining the personalized touch that affluent clients expect.

Growing Interest in Alternative and ESG-Focused Investments

Investors are increasingly diversifying portfolios beyond traditional asset classes, showing heightened interest in alternative investments such as private equity, venture capital, real estate investment trusts, and structured products. In June 2025, investments in Alternative Investment Funds (AIFs) by India’s high‑net‑worth individuals rose sharply to ₹5.38 trillion, up 32 % year‑on‑year, reflecting growing demand for diversified, non‑traditional strategies. Simultaneously, environmental, social, and governance factors are becoming integral to investment decision-making, with wealth managers incorporating sustainable investment frameworks and impact-driven strategies to meet evolving client expectations and align portfolios with responsible investing principles.

Expansion of Wealth Services to Emerging Cities and Younger Demographics

Wealth creation is no longer confined to major metropolitan centers, with tier-two and tier-three cities emerging as significant growth corridors for wealth management services. In September 2025, Mercedes‑Benz Hurun India Wealth Report highlighted that seven Tier‑II cities now rank among India’s top 10 millionaire makers, reflecting rapid wealth expansion beyond metros. Simultaneously, a younger generation of first-generation entrepreneurs, startup founders, and salaried professionals with equity-linked compensation are entering the wealth management ecosystem, compelling providers to develop tailored offerings, accessible entry points, and digitally enabled engagement models. The convergence of rising incomes in smaller cities and the digital fluency of younger investor cohorts is reshaping how wealth management firms design, distribute, and deliver their advisory solutions nationwide.

Market Outlook 2026-2034:

India's wealth management market is positioned for sustained expansion, supported by robust economic growth, favorable demographic shifts, and increasing financial sophistication among investors. The ongoing transition from physical assets to diversified financial portfolios, coupled with regulatory modernization and technological advancements, is expected to drive higher revenue streams across advisory and portfolio management services. The rising population of high net worth and ultra-high net worth individuals, combined with expanding wealth creation in emerging urban centers beyond traditional metropolitan hubs, will further fuel demand for comprehensive and customized wealth management solutions across the country. The market generated a revenue of USD 171.16 Billion in 2025 and is projected to reach a revenue of USD 436.4 Billion by 2034, growing at a compound annual growth rate of 10.63% from 2026-2034.

India Wealth Management Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Business Model |

Human Advisory |

46.2% |

|

Provider |

Banks |

41.7% |

|

End User |

High Net Worth Individuals (HNIs) |

62.8% |

|

Region |

West India |

32.9% |

Business Model Insights:

- Human Advisory

- Robo Advisory

- Hybrid Advisory

The human advisory dominates with a market share of 46.2% of the total India wealth management market in 2025.

Human advisory continues to be the preferred wealth management model in India, driven by the deeply personal nature of financial planning and the trust that affluent clients place in dedicated relationship managers. In June 2025, a CFA Institute survey found that 91% of Indian investors still preferred human financial advisors over purely automated advice, despite the rise of AI‑based tools, underscoring enduring trust in human guidance. High net worth individuals and ultra-high net worth families rely on personalized guidance for complex investment decisions, estate planning, tax optimization, and intergenerational wealth transfer.

The continued pre-eminence of human advisory is a testament to the sophistication of financial requirements of high net-worth individuals who demand a sophisticated understanding of their individual and business context, as well as their strategic vision. Relationship managers act as trusted advisors who provide holistic advice that goes beyond portfolio construction to include issues of succession, philanthropic structuring, and international wealth management. The capacity to deliver empathetic and adaptive advice in times of market turbulence further cements client loyalty to human advisory.

Provider Insights:

- FinTech Advisors

- Banks

- Traditional Wealth Managers

- Others

Banks led with a share of 41.7% of the total India wealth management market in 2025.

Banks maintain a commanding position in India's wealth management landscape, leveraging their extensive branch distribution networks, established customer relationships, and the ability to bundle wealth services with core banking products. In December 2025, Axis Bank announced plans to hire 50 senior private bankers and expand its Burgundy Private division across 52 cities, strengthening its advisory desks and private banking offerings to meet growing affluent client demand. The trust and credibility associated with regulated banking institutions make them the preferred choice for a large segment of affluent clients.

The competitive advantage of banks extends beyond distribution reach, encompassing comprehensive product ecosystems that integrate lending, treasury, insurance, and investment solutions under a unified platform. This integrated service model enables banks to capture a greater share of client wallet by addressing multiple financial needs through a single relationship. Additionally, banks are expanding their wealth management presence into emerging cities, deploying technology-driven engagement models, and enhancing advisory talent capabilities to maintain their leadership position amid intensifying competition from independent firms and fintech platforms.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Retail

- High Net Worth Individuals (HNIs)

High net worth individuals (HNIs) dominate with a market share of 62.8% of the total India wealth management market in 2025.

High net worth individuals (HNIs) represent the core client segment in India's wealth management market, driving demand for sophisticated portfolio management, global diversification, alternative investment access, and comprehensive financial planning services. In June 2025, India added over 33,000 new millionaires, bringing its total HNWI population to nearly 378,810, with strong interest in diversified portfolios and tailored advisory services, reflecting expanding wealth and evolving client expectations. The expanding population of affluent individuals, fueled by entrepreneurial success, equity-linked compensation, and intergenerational wealth transfer, is continuously increasing the addressable market.

The evolving expectations of high-net-worth individuals are reshaping the wealth management value proposition, as these clients increasingly demand institutional-quality research, access to exclusive investment opportunities, and seamless digital engagement alongside traditional relationship-driven advisory. A growing proportion of younger affluent investors are bringing forward-thinking approaches to wealth management, prioritizing global portfolio diversification, sustainable investment principles, and technology-enabled transparency. This demographic shift is compelling wealth managers to continuously innovate their service delivery models, product offerings, and advisory frameworks to retain and attract this influential client segment.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 32.9% share of the total India wealth management market in 2025.

West India commands the leading position in the country's wealth management market, driven by the concentration of major financial centers, corporate headquarters, and a high density of high net worth and ultra-high net worth individuals. The region's well-established financial services infrastructure, presence of leading wealth management firms, and a thriving entrepreneurial ecosystem contribute to robust demand for advisory and portfolio management services. Growing wealth creation in emerging commercial hubs across the region is further expanding the client base for wealth management providers.

The region has an established capital markets infrastructure, strong liquidity pools, and easy access to regulatory authorities, which makes it conducive for the efficient delivery of financial services. The presence of a thriving start-up and technology ecosystem is also constantly creating new sources of wealth, thereby creating first-generation affluent individuals who are eager to seek expert financial advice. Moreover, the cosmopolitan investor base in the region also shows greater openness to diversified asset allocation approaches, alternative investments, and global portfolio approaches.

Market Dynamics:

Growth Drivers:

Why is the India Wealth Management Market Growing?

Rapid Growth in India's High Net Worth Population and Wealth Accumulation

India is witnessing an unprecedented expansion in its affluent population, driven by sustained economic growth, a thriving entrepreneurial ecosystem, and the increasing financialization of household savings. In September 2025, India’s millionaire households reached 8.71 lakh, up nearly 90% since 2021, reflecting broad‑based wealth creation across states such as Maharashtra, Delhi, and Tamil Nadu. The country's strong macroeconomic fundamentals, including rising gross domestic product, expanding foreign direct investment, and a vibrant startup landscape, are accelerating wealth creation across multiple sectors and geographies. As disposable incomes rise, individuals are increasingly seeking professional guidance to manage, preserve, and grow their accumulated assets through diversified investment strategies.

Accelerating Shift from Physical Assets to Financial Instruments

Indian investors are undergoing a fundamental transition in their asset allocation preferences, moving away from traditional physical assets such as gold and real estate toward market-linked financial instruments including equities, mutual funds, alternative investment funds, and structured products. In December 2025, PhonePe Wealth launched a Daily SIP feature allowing users to invest as little as ₹10 per day in mutual funds, making disciplined market‑linked investing accessible for micro and new investors. This behavioral shift is being driven by improved financial awareness, attractive capital market returns, ease of digital investment platforms, and government-led initiatives promoting financial inclusion and education.

Digital Transformation and Technological Innovation in Advisory Services

The integration of advanced technologies into wealth management is fundamentally reshaping how advisory services are delivered and consumed in India. AI, ML, data analytics, and automation are enabling wealth managers to offer hyper-personalized investment recommendations, real-time portfolio monitoring, and predictive insights at scale. In November 2025, Bengaluru‑based wealth‑tech startup Wealthy raised ₹130 crore in funding to enhance its AI‑powered advisory and distributor tools, signalling investor confidence in tech‑enabled wealth solutions. Digital platforms are lowering barriers to entry, making professional wealth management accessible to a wider audience while improving operational efficiency and client engagement.

Market Restraints:

What Challenges the India Wealth Management Market is Facing?

Talent Shortage and Rising Advisory Workforce Costs

The rapid expansion of wealth management demand has significantly outpaced the supply of qualified relationship managers and experienced financial advisors. The scarcity of skilled professionals is intensifying hiring competition, driving up compensation packages, sign-on bonuses, and retention costs. This talent constraint limits the ability of wealth management firms to scale operations effectively, maintain service quality, and penetrate emerging markets, creating a structural bottleneck that may restrain overall market growth potential.

Evolving Regulatory Complexity and Compliance Burden

The wealth management industry in India operates within an increasingly complex regulatory framework, with frequent updates to investment advisory guidelines, disclosure requirements, digital accessibility standards, and anti-money laundering protocols. While regulatory oversight strengthens investor protection, the cumulative compliance burden raises operational costs, requires continuous investment in infrastructure and training, and can create barriers for smaller advisory firms, potentially limiting market participation and service innovation.

Low Financial Literacy and Trust Deficit Among Potential Investors

Despite improving financial awareness, a substantial portion of India’s affluent and emerging affluent population continues to rely on informal financial advice or self-directed investment approaches. Deep-rooted preferences for traditional savings instruments, limited understanding of sophisticated financial products, and skepticism toward advisory fees create reluctance in adopting professional wealth management services. Overcoming this trust deficit requires sustained investor education efforts and transparent fee-based advisory models.

Competitive Landscape:

The India wealth management market is characterized by a dynamic and increasingly competitive landscape, with a diverse mix of established financial institutions, independent advisory firms, fintech-driven platforms, and global entrants vying for market share. The industry is witnessing a convergence of traditional and digital business models, as providers invest in technology infrastructure, artificial intelligence-powered advisory tools, and hybrid service delivery frameworks to differentiate their offerings. Strategic partnerships, mergers, and acquisitions are reshaping the competitive dynamics, as firms seek to combine local market expertise with global investment capabilities. The growing demand for fee-based advisory models over commission-driven distribution is prompting a fundamental shift in business practices and revenue structures. Firms are competing on the strength of their product shelf breadth, advisory talent quality, digital user experience, and ability to deliver holistic financial planning solutions that encompass investment management, estate planning, tax optimization, and cross-border wealth structuring.

Recent Developments:

-

In February 2026, InvestValue Fintech launched its ‘India Winners’ multi-cap PMS under InvestValue Capital, targeting Rs500 crore AUM in the first year. The platform serves over 15,000 clients, with strong metro and Tier‑2 city presence, leveraging digital tools and a partner ecosystem to expand India’s wealth management offerings.

India Wealth Management Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Business Models Covered |

Human Advisory, Robo Advisory, Hybrid Advisory |

|

Providers Covered |

FinTech Advisors, Banks, Traditional Wealth Managers, Others |

|

End Users Covered |

Retail, High Net Worth Individuals (HNIs) |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Wealth Management Market Report

The India wealth management market size was valued at USD 171.16 Billion in 2025.

The India wealth management market is expected to grow at a compound annual growth rate of 10.63% from 2026-2034 to reach USD 436.4 Billion by 2034.

Human advisory, holding the largest share of 46.2%, leads the India wealth management market through its personalized financial guidance, relationship-driven engagement, and ability to deliver tailored investment strategies addressing the complex needs of affluent clients.

Key factors driving the India wealth management market include rapid growth in the high net worth population, accelerating transition from physical to financial assets, digital transformation in advisory services, rising financial literacy, and expanding wealth creation in emerging cities.

Major challenges include acute talent shortages among qualified financial advisors, evolving regulatory complexity and compliance burdens, low financial literacy among potential investors, trust deficits toward fee-based advisory models, and the high cost of technology infrastructure adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)