India Wedding Services Market Size, Share, Trends and Forecast by Type, Booking Type, Service Type, and Region, 2026-2034

India Wedding Services Market Size, Share, Trends & Forecast (2026-2034)

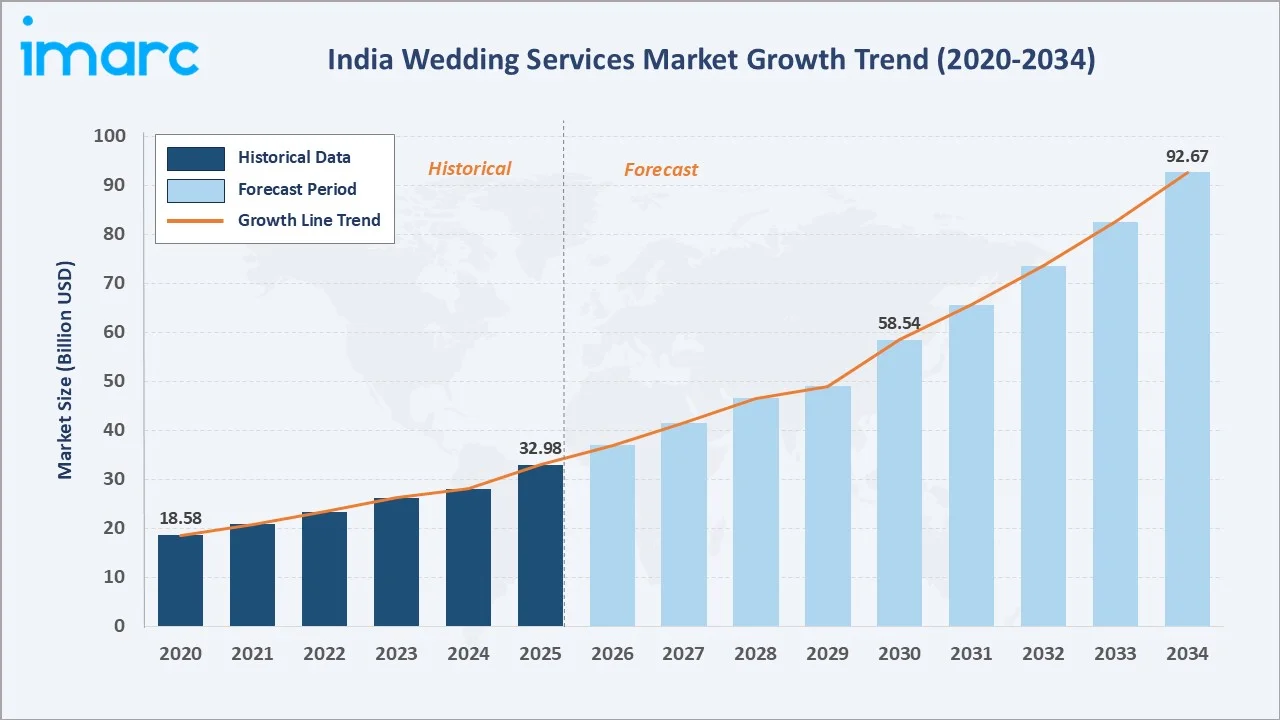

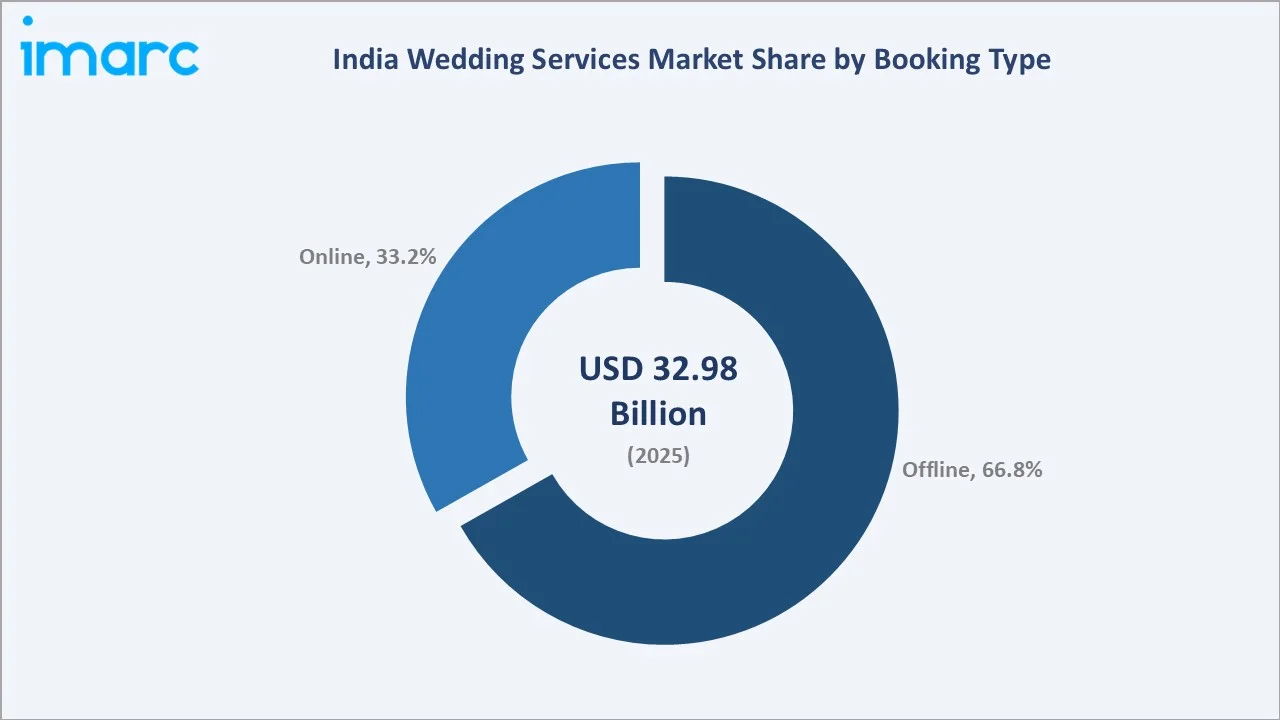

The India wedding services market reached USD 32.98 Billion in 2025 and is projected to reach USD 92.67 Billion by 2034, growing at a CAGR of 12.16% during 2026-2034. The market is driven by rising consumer aspirations, growing social media influence, increasing adoption of professional event management, and rapid expansion of online booking platforms.

Wedding expenditures continue to rise across urban and semi-urban India, with couples increasingly opting for multi-day, multi-event celebrations. The Local segment dominates at 82.3%, while the Offline booking channel retains 66.8% share as trust-based vendor relationships remain central to India wedding planning processes.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 32.98 Billion |

|

Forecast Market Size (2034) |

USD 92.67 Billion |

|

CAGR (2026-2034) |

12.16% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Local (82.3%, 2025) |

|

Dominant Booking Type |

Offline (66.8%, 2025) |

|

Leading Region |

West India (36.2%, 2025) |

To get more information on this market, Request Sample

The India wedding services market expanded from USD 18.58 Billion in 2020 to USD 32.98 Billion in 2025, nearly doubling in five years. Growth was briefly disrupted by COVID-19 in 2020-2021 before recovering sharply. The market is anchored at USD 58.54 Billion in 2030 and projected to reach USD 92.67 Billion by 2034.

Executive Summary

The India wedding services market reached USD 32.98 Billion in 2025, positioning it among the world's most vibrant wedding economy segments, underpinned by a vast young marriageable population, growing disposable incomes, and deep cultural significance of elaborate wedding ceremonies.

Local weddings dominate at 82.3%, commanding broad geographic coverage and lower cost structures, while destination weddings at 17.7% represent the fastest-growing premium sub-segment. Offline booking retains 66.8% share driven by trust-based vendor selection preferences across all income segments.

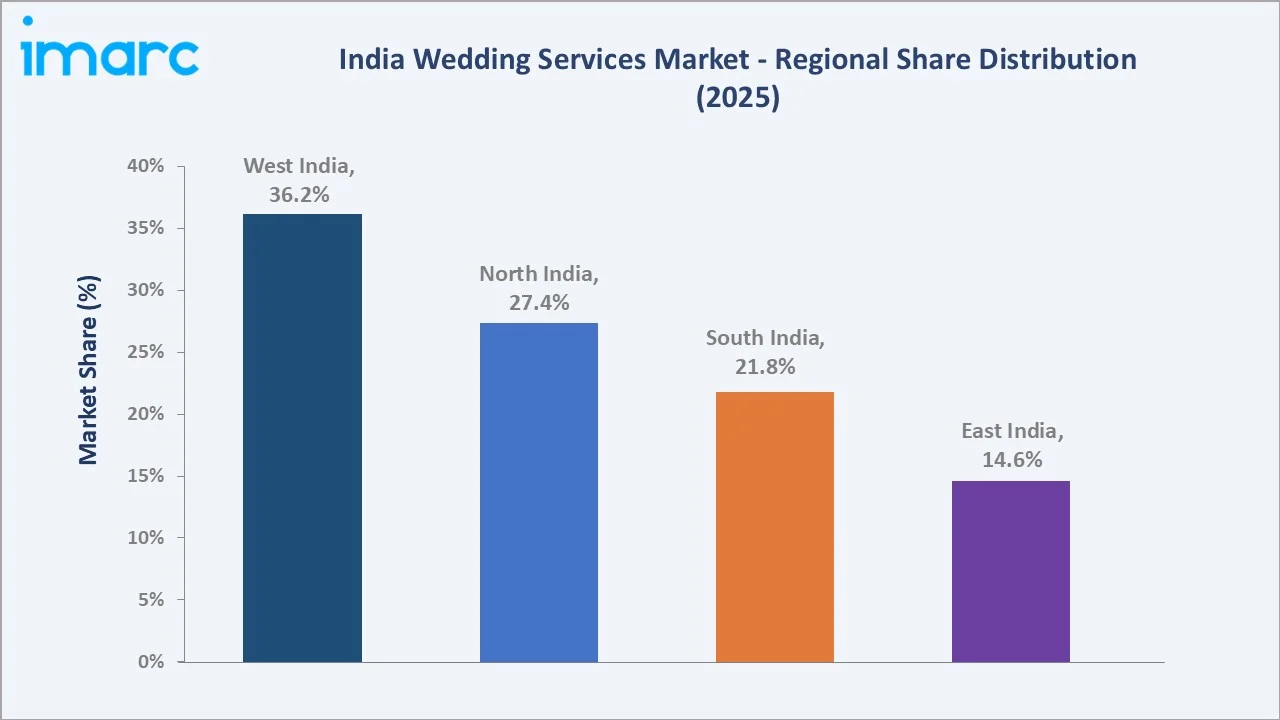

West India leads with a 36.2% regional share, anchored by Gujarat and Maharashtra's large wedding economies. North India at 27.4% reflects the prominence of large-scale Punjabi and Delhi NCR wedding formats commanding some of the highest per-event budgets nationally.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Local – 82.3% share (2025) |

|

Fastest Growing Type |

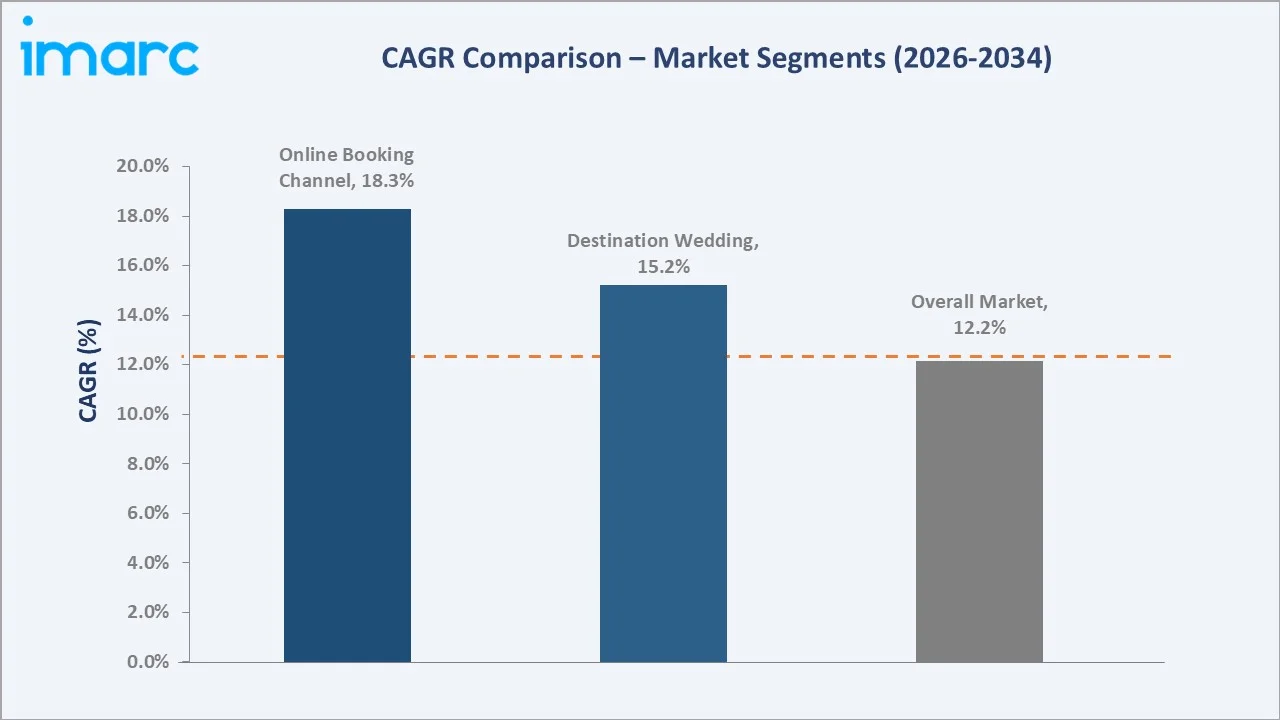

Destination – ~15.2% CAGR (2026-2034) |

|

Dominant Booking Type |

Offline – 66.8% market share (2025) |

|

Fastest Growing Booking |

Online – ~18.3% CAGR (2026-2034) |

|

Leading Region |

West India – 36.2% share (2025) |

|

Market Opportunity |

Tier-2/3 City Formalisation; AI Planning; Destination Wedding Infrastructure |

India Wedding Services Market Overview

The India wedding services market encompasses venue booking, catering, decoration, photography, videography, wedding planning coordination, transport, and all associated services across all wedding formats from intimate local ceremonies to grand multi-day destination celebrations.

The ecosystem integrates venue operators, catering companies, decor specialists, photography and media studios, professional wedding planners, digital booking platforms, bridal fashion retailers, and ancillary hospitality services. Macroeconomic drivers include rising household income, urbanisation, expanding middle class, and social media-driven aspirations.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

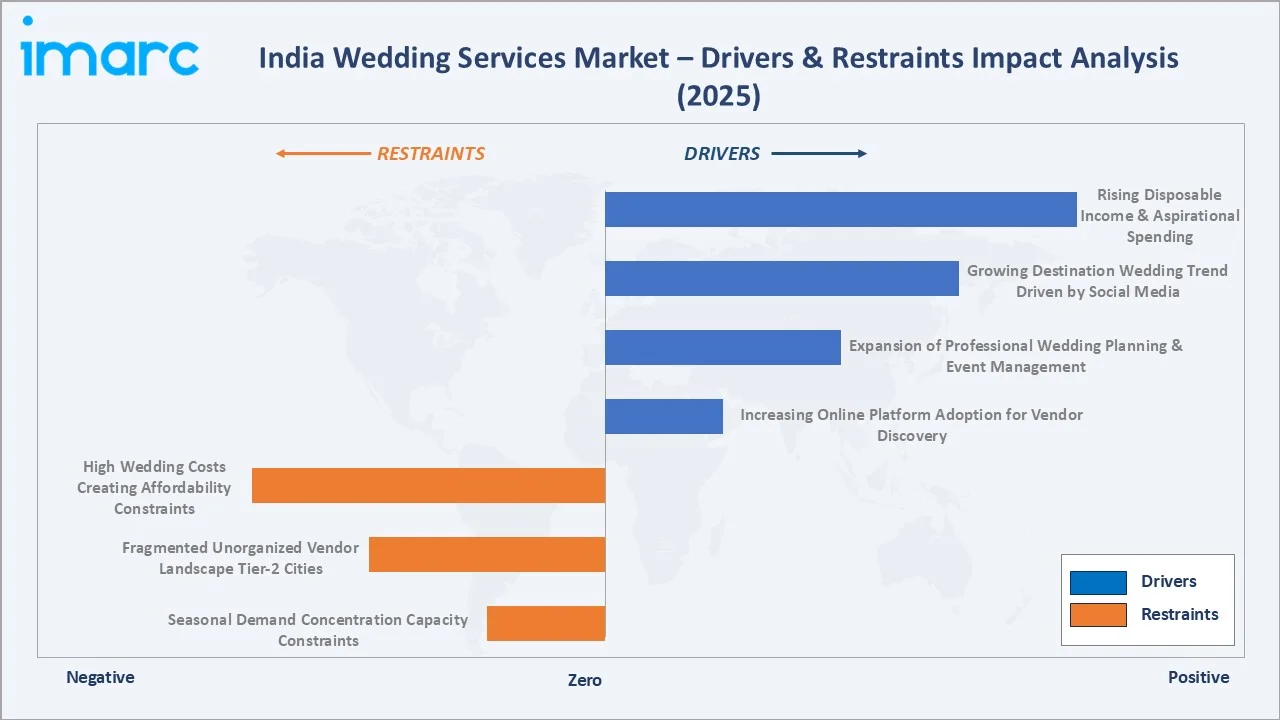

- Rising Disposable Income & Aspirational Spending: Growing household incomes across urban and tier-2 cities are enabling higher wedding budgets, with couples investing in premium venues, professional photography, and multi-event ceremonies. Rising aspirational consumption is directly expanding average per-wedding expenditure across all income segments.

- Growing Destination Wedding Trend Driven by Social Media: Platforms like Instagram are driving aspirational wedding formats. WeddingWire India reported 13% year-on-year growth in destination weddings, driven by high-profile celebrity events. This trend is expanding per-wedding spend and attracting international hospitality brands to the India market.

- Expansion of Professional Wedding Planning & Event Management: Rising complexity of multi-day wedding formats and cross-vendor coordination is accelerating demand for professional wedding planners and full-service event management companies across India's metropolitan and tier-1 cities.

- Increasing Online Platform Adoption for Vendor Discovery: Digital platforms such as WedMeGood and Weddingz enable couples to discover, compare, and book vendors efficiently, expanding the addressable market by integrating previously fragmented local vendor ecosystems into structured digital discovery channels.

Market Restraints

- High Wedding Costs Creating Affordability Constraints: Escalating costs across venues, catering, and decor services are limiting market accessibility for lower-income segments, constraining overall volume growth despite strong aspirational demand across broader consumer demographics in India.

- Fragmented & Unorganized Vendor Landscape in Tier-2/Tier-3 Cities: The dominance of informal, unregistered vendors in smaller cities creates quality inconsistency, pricing opacity, and trust barriers, significantly inhibiting market formalisation and digital platform penetration into high-volume Tier-2 and Tier-3 markets.

- Seasonal Demand Concentration Creating Capacity Constraints: Indian weddings are heavily concentrated around auspicious dates, creating acute venue and vendor shortages during peak seasons and reducing service quality, client satisfaction, and sustainable revenue distribution across the calendar year.

Market Opportunities

- Micro & Intimate Wedding Segment Growth: Post-pandemic consumer preference for smaller, personalised ceremonies is creating an emerging micro-wedding segment, enabling premium per-guest spending and new service packaging opportunities for boutique wedding planners targeting quality-conscious urban couples.

- Technology Integration in Wedding Planning: AI-powered planning tools, AR-based decor visualisation, and virtual venue tours are creating differentiated service offerings and expanding the addressable digital market, particularly within the rapidly growing online booking channel across metro India.

Market Challenges

- Vendor Quality Standardisation Across Geographies: Ensuring consistent service quality across a vast, geographically dispersed vendor base remains a significant challenge for platforms and aggregators, creating customer satisfaction risks across both local and destination wedding service segments.

- GST Compliance & Pricing Transparency: The multi-rate GST structure applied to various wedding services, ranging from catering to venue rental, creates pricing complexity and compliance burden for small operators, impeding market formalisation and transparent consumer pricing across India.

Emerging Market Trends

1. Destination Wedding Premiumisation Driven by Aspirational Demand

Destination weddings in India are evolving from a niche luxury format into a mainstream aspiration, with Goa, Udaipur, and other cities as leading venues. High-profile celebrity weddings and social media amplification are expanding per-wedding spend and attracting international hospitality brands to India's wedding market.

2. Digital Platform Maturation & Vendor Ecosystem Aggregation

Wedding planning platforms are consolidating vendor ecosystems by offering end-to-end booking, verified reviews, and package comparison. Digital discovery is reducing friction, improving price transparency, and accelerating vendor formalisation, particularly in metro and tier-1 cities across India.

3. Experiential & Themed Wedding Formats Driving Premium Spend

Couples are investing in highly personalised, experiential wedding formats featuring custom decor themes, live entertainment, and curated culinary experiences. This trend expands average revenue per wedding and creates high-margin service categories for professional wedding planners across premium segments.

4. Technology-Enabled Wedding Services Transforming Vendor Discovery

AI-powered planning tools, AR-based decor previews, and digital invitation platforms are being adopted by leading wedding planning companies, enhancing client experience and opening new digital revenue streams across India's expanding wedding services value chain.

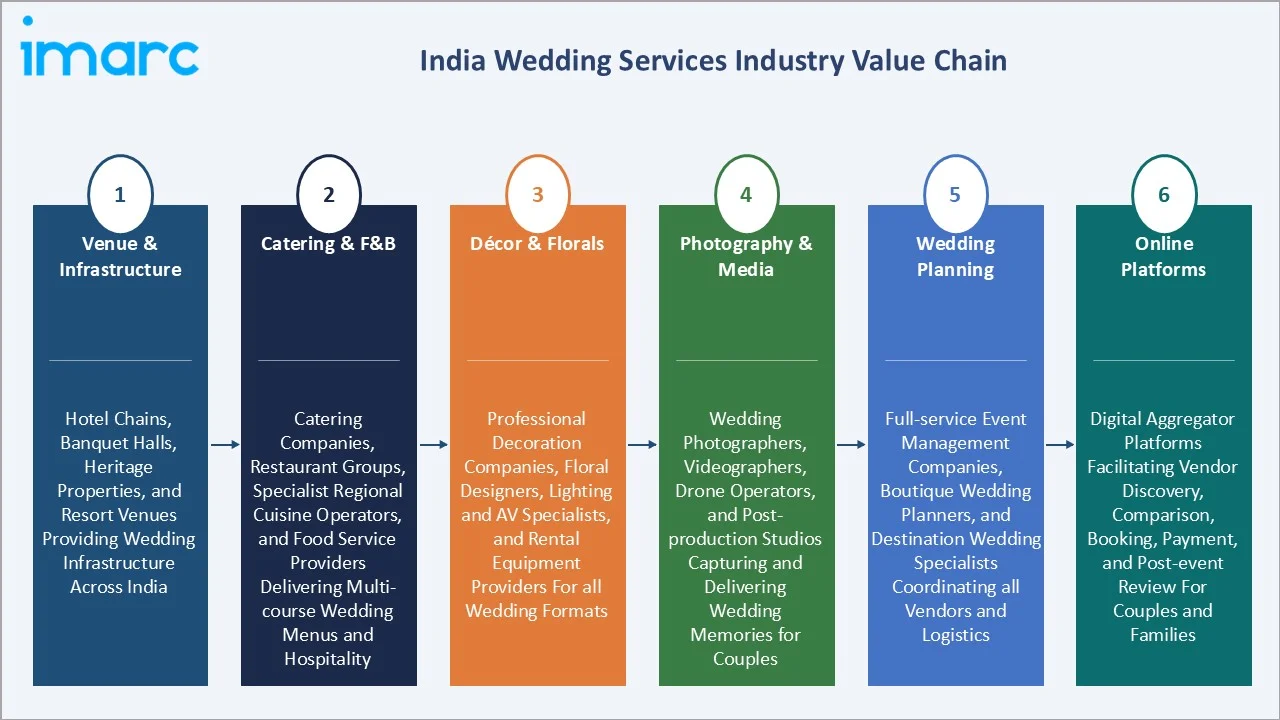

Industry Value Chain Analysis

The India wedding services value chain integrates venue infrastructure providers, catering and F&B specialists, decor and floral vendors, photography and media studios, professional wedding planning agencies, and digital booking platforms, connecting all participants to the end consumer couple and family.

|

Stage |

Key Participants |

|

Venue & Infrastructure |

Hotel chains, banquet halls, heritage properties, resort venues, and open-air event spaces provide wedding venue infrastructure across India |

|

Catering & F&B |

Catering companies, restaurant groups, specialist regional cuisine operators, and food service providers delivering multi-course wedding menus and hospitality |

|

Decor & Florals |

Professional decoration companies, floral designers, lighting and AV specialists, and rental equipment providers for all wedding formats |

|

Photography & Media |

Wedding photographers, videographers, drone operators, and post-production studios capturing and delivering wedding memories for couples |

|

Wedding Planning |

Full-service event management companies, boutique wedding planners, and destination wedding specialists coordinating all vendors and logistics |

|

Online Platforms |

Digital aggregator platforms facilitating vendor discovery, comparison, booking, payment, and post-event review for couples and families |

The online platform tier represents the India wedding services value chain's most transformative commercial stage, as digital aggregators progressively integrate previously fragmented vendor ecosystems, creating scalable discovery and booking infrastructure across geographic markets.

Technology Landscape in the India Wedding Services Industry

Digital Booking & Vendor Discovery Platforms

Digital booking platforms offer comprehensive vendor discovery, price comparison, verified reviews, and seamless payment integration. These platforms reduce information asymmetry between couples and vendors, enabling efficient market discovery and improving service quality accountability across India's fragmented vendor base.

AI-Powered Wedding Planning Tools

AI-powered planning tools enable personalised vendor recommendations, budget optimisation, and timeline management for couples. These tools are being integrated into leading wedding platforms, creating differentiated digital experiences and expanding premium service revenues through technology-driven personalisation capabilities.

Augmented Reality Decor Visualisation

AR-based decor visualisation enables couples to preview venue decor themes, floral arrangements, and lighting setups in real time before confirming bookings. This technology reduces decision uncertainty, accelerates vendor selection, and creates high-value service differentiation for premium wedding planning companies.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Local |

82.3% |

2025 |

|

Booking Type |

Offline |

66.8% |

2025 |

|

Service Type |

Catering Services |

34.9% |

2025 |

|

Region |

West India |

36.2% |

2025 |

By Type

The Local segment dominates at 82.3% in 2025, encompassing the vast majority of Indian weddings conducted within proximity of the couple's home city or region. Local weddings benefit from lower cost structures, established vendor relationships, and family network coordination across all income segments.

To access detailed market analysis, Request Sample

The Destination segment at 17.7% commands significantly higher per-wedding spend, with average event budgets 3-5x that of local weddings. This segment is growing at approximately 15.2% CAGR during 2026-2034, driven by premium hospitality demand and rising aspirational consumer behaviour.

By Booking Type

The Offline segment leads at 66.8% in 2025, reflecting the deeply trust-based nature of Indian wedding vendor relationships. Couples prefer in-person consultations, vendor walk-throughs, and direct negotiations for high-value wedding services. Family referrals remain a primary vendor discovery channel.

The Online segment at 33.2% is the fastest-growing channel at approximately 18.3% CAGR, driven by platforms enabling digital vendor discovery, price comparison, and streamlined booking. Online penetration is highest among urban millennials and within the destination wedding segment.

Regional Market Insights

|

Region |

Share (2025) |

Key India Wedding Services Market Drivers & Characteristics |

|

West India |

36.2% |

Driven by Maharashtra and Gujarat's large-scale wedding economies; premium venue and catering markets in Mumbai and Ahmedabad; high multi-day event budgets |

|

North India |

27.4% |

Driven by Punjabi, Rajasthani, and Delhi NCR wedding formats; high-value multi-day ceremonies; largest destination wedding feeder market nationally |

|

South India |

21.8% |

Strong traditional wedding culture in Tamil Nadu, Karnataka, and Telangana; rising technology-driven vendor discovery; growing destination sub-segment |

|

East India |

14.6% |

Emerging market driven by West Bengal and Odisha; growing platform penetration; expanding formal wedding services adoption in Kolkata and tier-2 cities |

West India, at 36.2%, leads through the large and affluent wedding economies of Maharashtra and Gujarat. North India at 27.4% is anchored by high-value Punjabi and Delhi NCR wedding formats.

South India, at 21.8%, reflects a large-scale culturally distinct wedding market with growing digital adoption. East India, at 14.6%, represents the market's fastest-developing region by platform penetration, with expanding formal wedding services adoption in Kolkata and emerging cities.

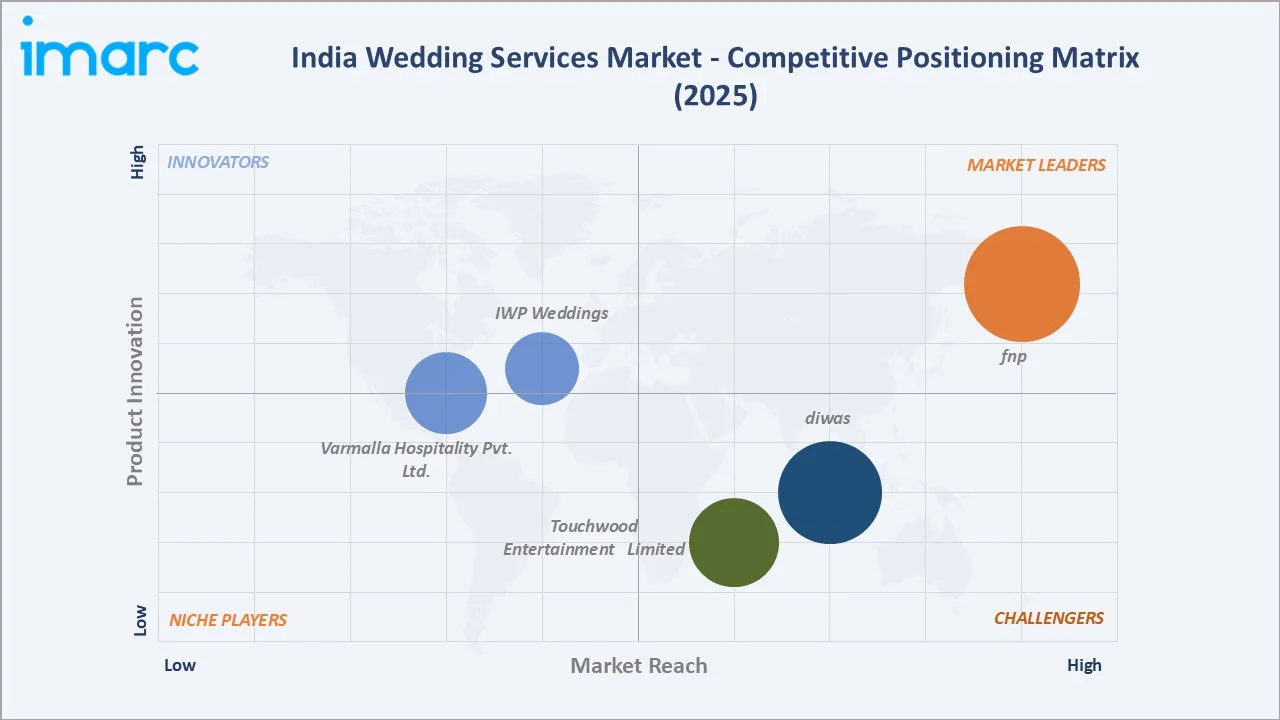

Competitive Landscape

The India wedding services market competitive landscape is highly fragmented, with a blend of national digital platforms, full-service luxury wedding planning companies, regional event management firms, and a vast base of local vendors operating across the wedding services value chain.

|

Company Name |

Key Services |

Market Position |

Core Strength |

|

fnp |

Decor, Floral, Gifting, Wedding Planning & Coordination |

Market Leader |

Nationwide retail and services network; integrated floral and decor offerings at scale |

|

diwas |

Budget wedding, Destination wedding, Luxury wedding Services |

Strong Challenger |

Boutique destination & luxury planner; pan-India + international execution |

|

Touchwood Entertainment Limited |

Full-Service Event Management, Destination Weddings |

Strong Challenger |

Specialised full-service wedding and event management with destination expertise |

|

Varmalla Hospitality Pvt. Ltd. |

Destination Weddings, Exquisite Hospitality, Luxurious Residential Celebrations |

Emerging Player |

Premium luxury destination wedding & hospitality management; bespoke weddings India + international |

|

IWP Weddings |

Destination Management, Experiential Events, Social Gatherings, Destination Wedding Planning |

Emerging Player |

Royal wedding & event design; Jaipur/Mumbai base |

Key players include fnp, diwas, Touchwood Entertainment Limited, Varmalla Hospitality Pvt. Ltd., IWP Weddings, and others

Key Company Profiles

fnp

fnp is India's largest gifting brand and services company with significant presence in the wedding decor, planning, and event management segment. Headquartered in New Delhi, FNP operates through a nationwide network of retail outlets and online delivery infrastructure.

- Key Services: Wedding floral design and decor, wedding planning and coordination, gifting, and corporate event management services.

- Strategic Focus: Deepening full-service wedding category integration by combining floral decor, gifting, and event planning services while expanding digital booking capabilities and tier-2 city market penetration.

Touchwood Entertainment Limited

Touchwood Entertainment Limited is a full-service event management and wedding planning company in India, specialised in large-scale corporate events, destination weddings, and luxury wedding ceremonies. The company operates across India's major metros and premium destination wedding locations.

- Key Services: Full-service destination wedding planning, corporate event management, entertainment programming, luxury wedding coordination, and themed event design services.

- Strategic Focus: Positioning as a premium full-service destination wedding company targeting high-net-worth clients, expanding international destination capabilities, and deepening relationships with luxury hotel chains and heritage venue operators.

Market Concentration Analysis

The India wedding services market is highly fragmented, with no single company commanding more than an estimated 5-8% of total market revenue. Digital platforms of the top two key players collectively represent the highest market influence in the online booking channel but compete in a vast, offline-dominated market.

The Local wedding segment's dominance at 82.3% ensures that fragmented local vendors — caterers, decorators, photographers — retain the majority of market revenue. Organised players are progressively capturing share in the premium and destination segments where per-event spend is significantly higher.

Investment & Growth Opportunities

Highest Growth Segments

- Destination Wedding Services (~15.2% CAGR): Premium per-event spend, international venue partnerships, and high-profile celebrity wedding influence are creating structural demand growth for destination-specialised planning companies and luxury hospitality venues through 2034.

- Online Booking Platforms (~18.3% CAGR): Digital vendor aggregation, AI-powered matching, and seamless payment integration are driving rapid growth in online wedding booking, creating significant market opportunity for platform operators and technology-enabled planning services.

- Photography & Videography Premium Services: Rising demand for cinematic wedding films, drone coverage, and digital photo albums is creating high-value service categories within the wedding media production segment across both local and destination formats.

Emerging Investment Opportunities

Technology-enabled wedding services represent the highest ROI investment vector, enabling premium pricing, higher client retention, and geographic expansion without proportional cost scaling. Platforms integrating AI planning, AR decor visualisation, and seamless multi-vendor booking will command growing share in the rapidly expanding online booking segment.

Investment Themes

- Tier-2 & Tier-3 City Market Formalisation: Expanding platform services and professional wedding planning into underserved cities where informal vendors dominate creates large addressable market expansion opportunities for digital platforms and franchise-model event management companies.

- Destination Wedding Infrastructure Investment: Partnership models with heritage properties, resorts, and international venues in India's premium wedding destinations offer high-margin revenue at significantly lower per-event cost than standalone planning operations.

Future Market Outlook (2026-2034)

The India wedding services market is projected to grow from USD 32.98 Billion in 2025 to USD 92.67 Billion by 2034, delivering a 12.16% CAGR. Market growth will be driven by rising middle-class aspirations, platform-led vendor ecosystem formalisation, and expanding destination wedding adoption.

The online booking segment will continue gaining share, approaching 45-50% of total bookings by 2034 as digital-native millennials form the dominant wedding age cohort. The destination wedding segment will outpace overall market growth as premium experiences become the defining aspiration for higher-income segments.

By 2030, the market is projected to reach USD 58.54 Billion, with organised players capturing a rising share of the previously fragmented local wedding services ecosystem through brand building, technology integration, and expansion into tier-2 and tier-3 cities across India.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders, including professional wedding planners, venue operators, catering company executives, photography studio owners, and digital platform representatives across India's major metropolitan and tier-2 wedding markets.

Secondary Research

Secondary research encompassed Annual Wedding Industry Report 2024-2025, WeddingWire India destination wedding surveys, Ministry of Tourism data on domestic destination tourism, industry event management reports, and company annual disclosures. Over 50 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using bottom-up and top-down modelling: (i) total annual wedding volumes segmented by type and booking mode; (ii) average revenue per wedding by segment; (iii) platform take-rate and vendor service revenue blended estimates; (iv) regional growth adjustment factors applied.

India Wedding Services Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Destination, Local |

|

Booking Types Covered |

Online, Offline |

|

Service Types Covered |

Catering Services, Decoration Services, Transport Services, Videography & Photography Services, Wedding Planning Services, Other Services |

|

Regions Covered |

North India, South India, East India, West India |

| Companies Covered | fnp, diwas, Touchwood Entertainment Limited, Varmalla Hospitality Pvt. Ltd., IWP Weddings, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Wedding Services Market Report

The India wedding services market reached USD 32.98 Billion in 2025, driven by Local weddings dominating at 82.3%, Offline booking leading at 66.8%, and West India commanding 36.2% regional share through the large-scale Gujarat and Maharashtra wedding economies.

The market grows at 12.16% CAGR during 2026-2034, reaching USD 92.67 Billion by 2034. This reflects rising consumer aspirations, digital platform expansion, and growing destination wedding premiumisation across India.

Local weddings account for 82.3% of the market share in 2025, capturing the vast majority of India's annual wedding volume across all income segments and geographies nationwide.

Offline booking leads at 66.8% in 2025, reflecting trust-based vendor relationships and family network coordination that remain central to Indian wedding planning processes across all regions.

West India leads at 36.2% through the large and affluent wedding economies of Maharashtra and Gujarat, anchored by Mumbai and Ahmedabad's premium venue and catering markets.

Leading companies include fnp, diwas, Touchwood Entertainment Limited, Varmalla Hospitality Pvt. Ltd., IWP Weddings, and others.

The market is projected to reach approximately USD 58.54 Billion by 2030, driven by online platform maturation, rising destination wedding adoption, and tier-2 city market formalisation across India.

Three priority opportunities: online platform expansion into tier-2 and tier-3 cities, destination wedding infrastructure partnerships with premium venue operators, and AI-powered technology integration for personalised wedding planning services.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade