India Welding Consumables Market Size, Share, Trends and Forecast by Product, Welding Technique, End Use Industries, and Region, 2026-2034

India Welding Consumables Market Summary:

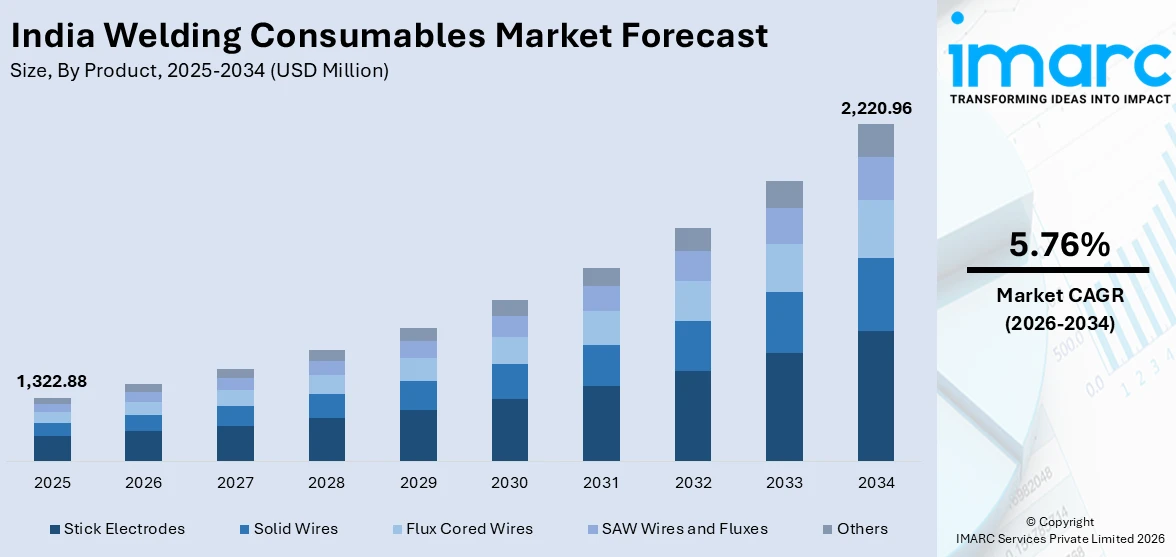

The India welding consumables market size was valued at USD 1,322.88 Million in 2025 and is projected to reach USD 2,220.96 Million by 2034, growing at a compound annual growth rate of 5.76% from 2026-2034.

India's welding consumables market is experiencing robust expansion underpinned by the country's sweeping infrastructure modernization, the rapid scaling of automotive manufacturing, and the accelerating transition toward renewable energy. The government's flagship PM Gati Shakti National Master Plan, integrating multimodal connectivity initiatives across roads, railways, ports, and airports, is generating sustained demand for electrodes, filler metals, and fluxes across construction and fabrication applications. Simultaneously, the Production-Linked Incentive scheme across multiple industrial sectors is strengthening domestic manufacturing capacity, reinforcing the need for high-performance welding consumables. The expanding clean energy segment, particularly solar and wind energy infrastructure, further broadens the addressable base for the India welding consumables market share.

Key Takeaways and Insights:

- By Product: Stick electrodes dominate the market with a share of 34.5% in 2025, owing to their wide applicability across construction and general fabrication sectors, ease of operation under diverse field conditions, and lower equipment cost requirements making them the preferred choice for small and medium enterprises throughout India.

- By Welding Technique: Arc welding leads the market with the largest share of 48.5% in 2025, driven by its versatility across heavy-duty applications in construction, shipbuilding, and industrial manufacturing, as well as widespread adoption among MSME-scale fabricators who rely on its cost-efficiency and relatively simple operational requirements.

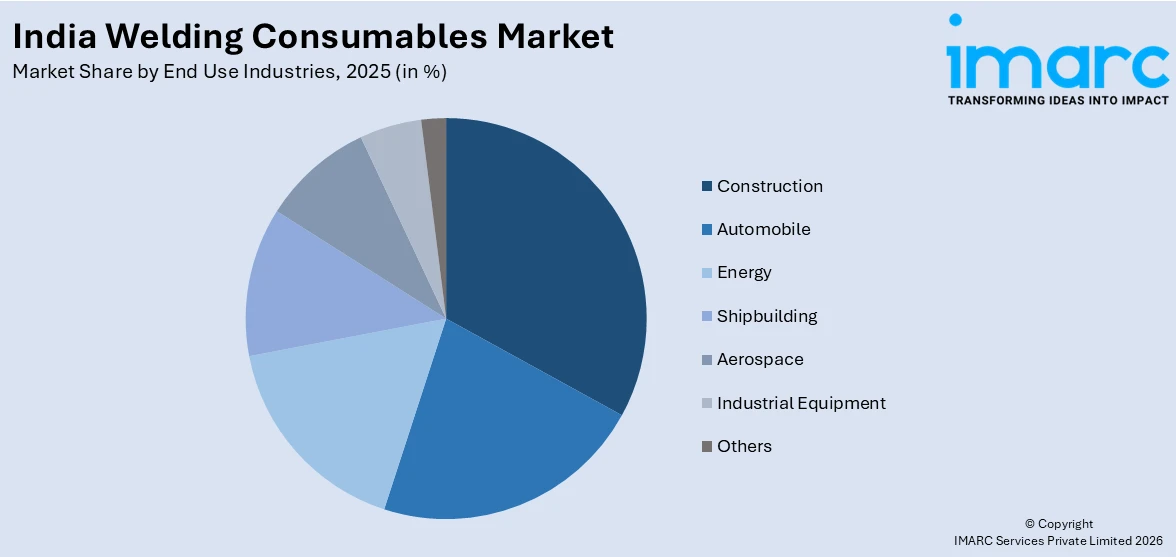

- By End Use Industries: Construction represents the largest segment with a market share of 32.5% in 2025, supported by India's massive infrastructure pipeline including highways, bridges, metro rail corridors, and smart city developments generating continuous, high-volume consumption of welding electrodes and filler materials.

- By Region: West and Central India dominate the market with a share of 32.5% in 2025, reflecting the high concentration of automotive OEMs, engineering clusters, and shipbuilding facilities across Maharashtra and Gujarat, along with large-scale infrastructure projects such as the Mumbai Trans Harbour Link and Pune Metro that sustain consistent demand.

- Key Players: The India welding consumables market exhibits a competitive landscape with both established multinational companies and strong domestic players operating across product segments and geographies, competing through product quality, distribution network depth, and technology innovation.

To get more information on this market Request Sample

The India welding consumables market is deeply intertwined with the country's broader industrial and infrastructural growth narrative. India's Union Budget 2025-26 allocated a capital investment outlay of Rs. 11.21 lakh crore (USD 128.64 billion) for infrastructure, representing 3.1% of GDP, which directly underpins sustained demand for welding materials across construction and fabrication. The construction sector alone, supported by programs such as Bharatmala Pariyojana for highways, Smart Cities Mission, and Sagarmala for ports, consumes large volumes of stick electrodes and solid wires for structural steelwork. In parallel, India's automotive sector, benefiting from PLI incentives for advanced automotive technology, is integrating precision MIG and TIG welding consumables into body panel, chassis, and exhaust system fabrication. The country's renewable energy additions of 29.52 GW in FY 2024-25, including 23.83 GW of solar capacity, have expanded the downstream welding requirement for panel structures, wind turbine towers, and related infrastructure.

India Welding Consumables Market Trends:

Rising Adoption of Automated and Robotic Welding Systems

India's manufacturing sector is progressively integrating robotic welding systems to enhance throughput consistency and reduce dependence on skilled manual labor. The automation wave, driven by the Make in India initiative and PLI-linked investments in automotive and electronics manufacturing, is increasing demand for precision-formulated wires and flux-cored consumables optimized for automated torch delivery. By March 2025, PLI-supported manufacturing investments across 14 sectors realized over Rs. 1.76 lakh crore, accelerating factory modernization and driving the shift toward automation-compatible welding consumable grades in facilities across Pune, Chennai, and Manesar.

Expanding Renewable Energy Infrastructure Creating New Demand

The rapid expansion of renewable energy infrastructure in India is creating a new and sustained demand base for welding consumables. Projects involving solar panel mounting structures, wind turbine towers, substations, and grid transmission systems require extensive metal fabrication, which relies heavily on specialized electrodes and filler materials. As the country continues to prioritize clean energy development, large-scale installations and supporting infrastructure are expected to increase. This ongoing shift toward renewable power generation will drive consistent demand for welding consumables used in fabrication, assembly, and maintenance activities across energy projects.

Growing Demand for Low-Fume and Eco-Friendly Welding Consumables

Environmental and workplace safety concerns are increasingly influencing product development in the India welding consumables market. Manufacturers are focusing on producing low-spatter and low-fume electrodes and wires to improve air quality and enhance worker safety during welding operations. Growing awareness about occupational health, along with stricter industrial safety regulations, is encouraging industries such as construction, automotive, and heavy engineering to adopt more environmentally responsible consumables. In response, companies are prioritizing energy-efficient and eco-friendly welding solutions, reflecting a broader industry shift toward sustainable manufacturing practices and compliance with evolving environmental standards.

Market Outlook 2026-2034:

The India welding consumables market is positioned for consistent and broad-based growth throughout the forecast period, supported by sustained government investment in physical infrastructure, expanding industrial manufacturing, and growing clean energy fabrication requirements. Ongoing programs such as PM Gati Shakti, Bharatmala Pariyojana, and the National Infrastructure Pipeline will continue to provide a high-volume demand base for construction-segment consumables, while PLI-backed automotive and electronic manufacturing facilities deepen the requirement for precision welding materials. The market generated a revenue of USD 1,322.88 Million in 2025 and is projected to reach a revenue of USD 2,220.96 Million by 2034, growing at a compound annual growth rate of 5.76% from 2026-2034.

India Welding Consumables Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Stick Electrodes |

34.5% |

|

Welding Technique |

Arc Welding |

48.5% |

|

End Use Industries |

Construction |

32.5% |

|

Region |

West and Central India |

32.5% |

Product Insights:

- Stick Electrodes

- Solid Wires

- Flux Cored Wires

- SAW Wires and Fluxes

- Others

Stick electrodes dominate the India welding consumables market with a share of 34.5% of the total market in 2025.

Stick electrodes, also referred to as shielded metal arc welding (SMAW) electrodes, represent the dominant product category in the India welding consumables market due to their unmatched versatility, affordability, and suitability across diverse field conditions. Comprising a core wire rod coated in a protective flux compound, these electrodes generate a shielding gas upon combustion that protects the weld pool from atmospheric contamination. Their portability and minimal equipment requirements make them the preferred choice for construction-site fabrication, bridge building, structural steelwork, and repair applications across India's widespread infrastructure corridor.

The dominance of stick electrodes in India is reinforced by the price-conscious buying behavior of small and medium enterprises and independent contractors who constitute a large share of welding demand. Industries such as construction, general engineering, and pipeline maintenance continue to rely heavily on these electrodes for their ability to weld through rust, dirt, and coated surfaces without requiring controlled environments. The extensive distribution network built by domestic manufacturers further ensures availability in Tier 2 and Tier 3 cities, maintaining high consumption volumes across the country's decentralized manufacturing and fabrication ecosystem.

Welding Technique Insights:

- Arc Welding

- Resistance Welding

- Oxyfuel Welding

- Ultrasonic Welding

- Others

Arc welding leads with a share of 48.5% of the total India welding consumables market in 2025.

Arc welding leads the India welding consumables market primarily due to its widespread use across major industrial sectors such as construction, automotive, shipbuilding, and heavy engineering. The process is highly versatile and compatible with various metals and thicknesses, making it suitable for a wide range of fabrication and repair applications. Industries rely on arc welding for structural steel fabrication, pipelines, and machinery manufacturing, where strong and durable joints are essential. Its relatively simple equipment requirements and adaptability to different working environments further support its extensive use across both large industrial facilities and smaller workshops.

Another key reason for arc welding’s dominance is the continuous demand for consumables such as electrodes, flux-cored wires, and filler metals used in processes like shielded metal arc welding and gas metal arc welding. These consumables are essential for maintaining welding quality and productivity in large-scale manufacturing and infrastructure projects. The technique is also favored for its reliability, cost-effectiveness, and ability to perform efficiently in outdoor and on-site conditions. As industrial production and fabrication activities expand, arc welding continues to generate consistent demand for welding consumables across multiple end-use sectors.

End Use Industries Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Automobile

- Energy

- Shipbuilding

- Aerospace

- Industrial Equipment

- Others

Construction represent the highest revenue with a 32.5% share of the total India welding consumables market in 2025.

The construction sector represents the largest end-use industry for welding consumables in India, supported by extensive infrastructure development across the country. Large steel-based projects such as highways, bridges, metro rail networks, airports, ports, and commercial buildings require significant fabrication and structural joining activities. These operations depend heavily on welding consumables including stick electrodes, solid wires, and submerged arc welding wires. Continuous investments in transportation networks, urban infrastructure, and large-scale public projects are strengthening construction activity, thereby generating consistent and high-volume demand for welding consumables used in structural fabrication and assembly.

India’s construction industry continues to expand steadily, driven by growing urbanization, residential development, and the transformation of urban infrastructure. Welding plays a crucial role in manufacturing structural components, joining reinforcement bars, assembling prefabricated structures, and supporting industrial plant installations. Beyond construction, the automobile industry represents another significant end-use sector, where precision welding consumables are required for vehicle body frames, chassis, and exhaust systems. Additional demand comes from sectors such as energy, shipbuilding, aerospace, and industrial machinery, contributing to a diversified consumption base for welding consumables across various manufacturing and infrastructure activities.

Regional Insights:

- North India

- West and Central India

- South India

- East India

West and Central India exhibits clear dominance with a 32.5% share of the total India welding consumables market in 2025.

West and Central India leads the regional segmentation of the India welding consumables market, anchored by Maharashtra and Gujarat's extensive industrial base. In Maharashtra, which supplies around 18 percent of the national welding consumable demand, major automotive OEMs and tier-1 suppliers are in Pune, Nashik and Mumbai and there is a major shipbuilding and heavy engineering presence as well. The mega infrastructure projects in the state, such as the Mumbai Trans Harbour Link and the growing metro rail networks, are guaranteed to provide the state with an unending supply of welding demand. Gujarat's industrial clusters across Surat, Ahmedabad, and Rajkot, serving textiles, chemicals, and engineering sectors, further reinforce the region's market leadership.

North India represents the second-largest regional market, with demand concentrated in Delhi-NCR's manufacturing belt, Haryana's automotive fabrication clusters, and Rajasthan's emerging industrial corridors. The region has the advantage of the big highway and expressway initiatives like the Bharatmala and the Delhi-Mumbai Industrial Corridor. South India, which is being led by Tamil Nadu, Karnataka, and Andhra Pradesh, is experiencing fast growth due to automotive production in Chennai and electronics in Bengaluru. The East India zone, West Bengal, Jharkhand, and Odisha are the states that attract the demand mostly by steel, shipbuilding, and heavy engineering industries and the Sagarmala port development program contributes to the industrial development along the coastal areas.

Market Dynamics:

Growth Drivers:

Why is the India Welding Consumables Market Growing?

Massive Government-Backed Infrastructure Investment

Government-led infrastructure expansion in India is a major structural driver of demand for welding consumables. Large-scale national development initiatives are accelerating the construction of transportation networks, including roads, railways, ports, airports, and inland waterways. These coordinated infrastructure programs encourage integrated planning and faster project execution across multiple regions and sectors. Steel-intensive projects such as highways, bridges, flyovers, metro rail systems, and port facilities require extensive structural fabrication and metal joining. As welding plays a crucial role in assembling and reinforcing these structures, the ongoing development of infrastructure continues to generate steady and high-volume demand for welding electrodes, filler metals, and related consumables.

Expanding Automotive and Manufacturing Sector Under PLI Incentives

India’s manufacturing sector is experiencing a structural shift supported by government initiatives aimed at strengthening domestic production across multiple industries. Programs designed to encourage industrial investment are accelerating growth in sectors such as automotive, electronics, white goods, and specialty steel. This expansion is increasing the need for precision welding consumables used in manufacturing processes. In the automotive industry, welding materials such as MIG wires, TIG filler rods, and flux-cored wires are essential for assembling vehicle components, including lightweight structures and advanced systems. As manufacturing capacity expands and production technologies evolve, demand for reliable welding consumables continues to grow across diverse industrial applications.

Accelerating Renewable Energy and Power Sector Development

India’s transition toward clean energy is creating a rapidly expanding demand segment for welding consumables. The construction of renewable energy infrastructure, including solar panel mounting systems, wind turbine towers and components, substations, and grid connection facilities, requires extensive welding and metal fabrication. These projects rely on structural electrodes, solid wires, and flux-cored materials to ensure strong and reliable joints in large steel structures. As the country continues to prioritize renewable power generation and modernize its energy infrastructure, the scale of construction and installation activities is increasing. This shift is generating sustained demand for welding consumables across renewable energy projects.

Market Restraints:

What Challenges the India Welding Consumables Market is Facing?

Volatility in Raw Material Prices

Welding consumables are manufactured from steel wire, flux compounds, and various alloy materials whose prices are subject to global commodity market fluctuations. Volatility in iron ore, coking coal, manganese, and nickel prices directly impacts production costs and margin compression for consumable manufacturers. India's reliance on imported raw materials and specialty alloys exposes the supply chain to currency depreciation risk and global supply disruptions, creating pricing uncertainty that affects procurement planning for end users across construction and fabrication sectors.

Competition from Low-Cost Imported Consumables

Local Indian manufacturers face sustained competitive pressure from low-cost imported welding consumables, particularly from China, which has historically offered aggressive pricing in the electrode and wire segments. The import competitiveness has negatively impacted the market share of domestic players in specialized segments including shipbuilding, automotive, and white goods applications. Anti-dumping regulations and Bureau of Indian Standards certification requirements offer some protection, but enforcement gaps and import diversion through third-country routing continue to constrain domestic industry growth and pricing power.

Shortage of Skilled Welding Workforce

Despite high demand across construction, manufacturing, and energy sectors, India faces a significant deficit of certified and technically trained welders, limiting the pace of project execution and quality outcomes. The mismatch between the vocational training output and industry requirements for welding proficiency, particularly for specialized techniques such as TIG, plasma arc, and robotic welding, creates bottlenecks in deploying high-performance consumables effectively. Without adequate skilled welders, industries default to simpler, lower-specification consumables, constraining the premiumization trajectory of the market.

Competitive Landscape:

The India welding consumables market exhibits moderate competitive intensity, characterized by the coexistence of established multinational companies with strong technology portfolios and well-entrenched domestic manufacturers with deep distribution reach. The competitive field spans a broad product range including stick electrodes, solid wires, flux-cored wires, and submerged arc welding materials, with players differentiating through application-specific product formulations, certification credentials, and nationwide dealer and distributor networks. The market has witnessed growing emphasis on digital welding solutions and sustainability-compliant product lines, reflecting the broader industry evolution toward energy-efficient and low-emission consumable technologies. Local manufacturers are gaining market share by offering competitive pricing and benefiting from shorter, more efficient supply chains. In contrast, multinational companies rely on their advanced metallurgical capabilities and strong global research and development networks to serve high-specification applications in sectors such as automotive, aerospace, and energy infrastructure.

India Welding Consumables Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Stick Electrodes, Solid Wires, Flux Cored Wires, SAW Wires and Fluxes, Others |

| Welding Techniques Covered | Arc Welding, Resistance Welding, Oxyfuel Welding, Ultrasonic Welding, Others |

| End use Industries Covered | Construction, Automobile, Energy, Shipbuilding, Aerospace, Industrial Equipment, Others |

| Regions Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Welding Consumables Market Report

The India welding consumables market size was valued at USD 1,322.88 Million in 2025.

The India welding consumables market is expected to grow at a compound annual growth rate of 5.76% from 2026-2034 to reach USD 2,220.96 Million by 2034.

Stick electrodes held the largest product share of 34.5% in 2025, driven by their versatility, affordability, and suitability across construction, general fabrication, and repair applications under diverse field conditions, making them the preferred choice for small and medium enterprises and contractors across India.

Key factors driving the India welding consumables market include massive government-backed infrastructure investment under PM Gati Shakti and Bharatmala Pariyojana, expanding automotive and manufacturing output driven by PLI scheme incentives, rapid scale-up of renewable energy infrastructure, and growing adoption of automation and robotic welding in industrial facilities.

Major challenges include volatility in raw material prices impacting production costs, competitive pressure from low-cost imported consumables particularly from China, shortage of skilled and certified welders limiting quality-intensive applications, and environmental compliance costs associated with transitioning to low-fume and eco-friendly consumable formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)