India Wind Energy Market Size, Share, Trends and Forecast by Component, Rating, Installation, Turbine Type, Application, and Region, 2026-2034

India Wind Energy Market Size & Forecast 2026-2034

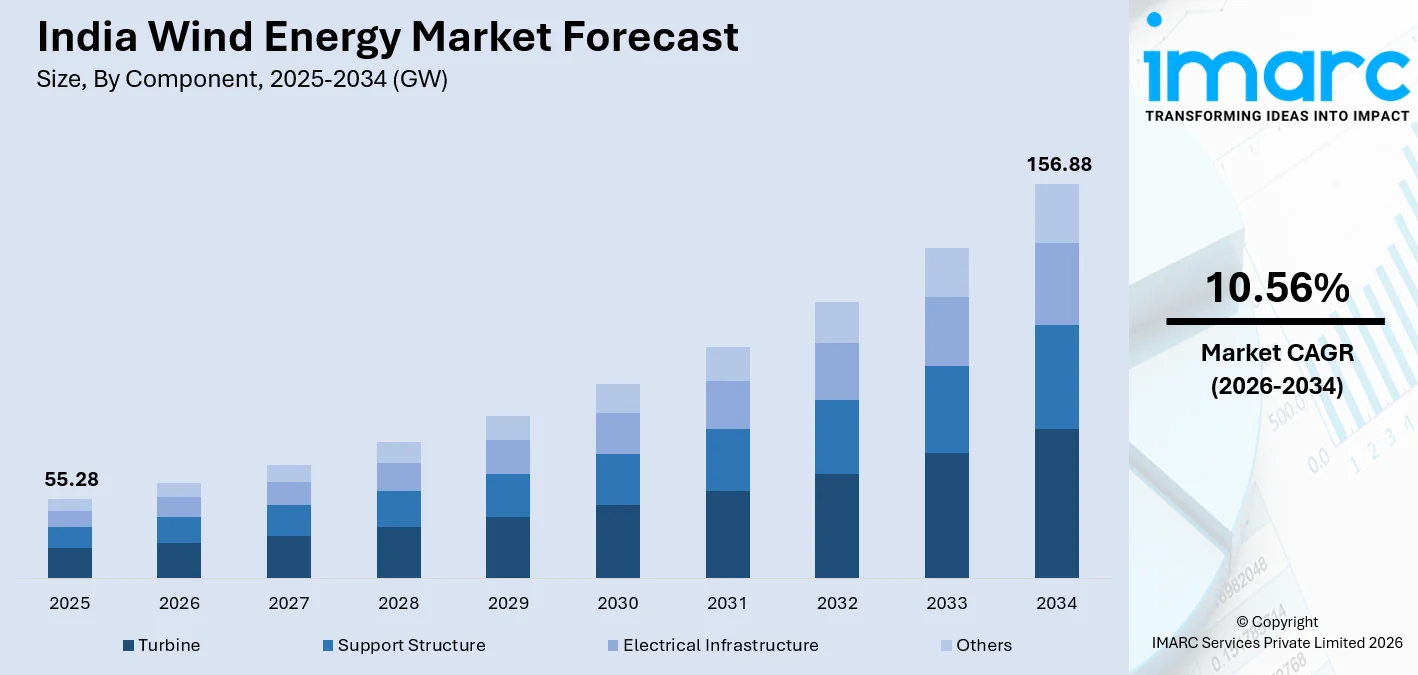

India wind energy market size reached at 55.28 GW in 2025, and it is projected to reach 156.88 GW by 2034, with a CAGR of 10.56% during 2026-2034. The market is witnessing accelerating momentum, driven by the national target of achieving 100 GW of wind energy installed capacity by the year 2030, along with the domestic production of wind turbine equipment. The wind energy installed capacity of India exceeded the 50 GW mark in March 2025, and as of November 2025, it has reached 53.99 GW, a year-over-year growth rate of 12.5%. This is due to India's fourth position in the world with regard to total installed wind energy capacity.

To get more information on this market Request Sample

India Wind Energy Industry Analysis - Key Insights

- Turbine commands 45.3% of component share in 2025 - the single highest-cost element in any wind installation, representing 40–50% of project capital expenditure. All 13 ALMM-enlisted manufacturers, including Suzlon, Inox Wind, and new entrant Adani Wind, anchor supply to this segment.

- >2 ≤ 5 MW leads rating at 38.7% in 2025 - the commercial sweet spot for India's onshore conditions, with Suzlon's 3.15 MW S144 dominating 92% of current order books.

- Onshore holds 98.2% of the installation share in 2025 - near-total dominance reflecting the absence of any commissioned offshore project. SECI cancelled 4.5 GW of offshore tenders in August 2025 due to developer disinterest, confirming that all commercial expansion is land-based through the near term.

- Horizontal axis dominates turbine type at 97.5% in 2025 - an almost exclusive structural share, as HAWT technology is the only commercially viable format for utility-scale generation at India's wind sites.

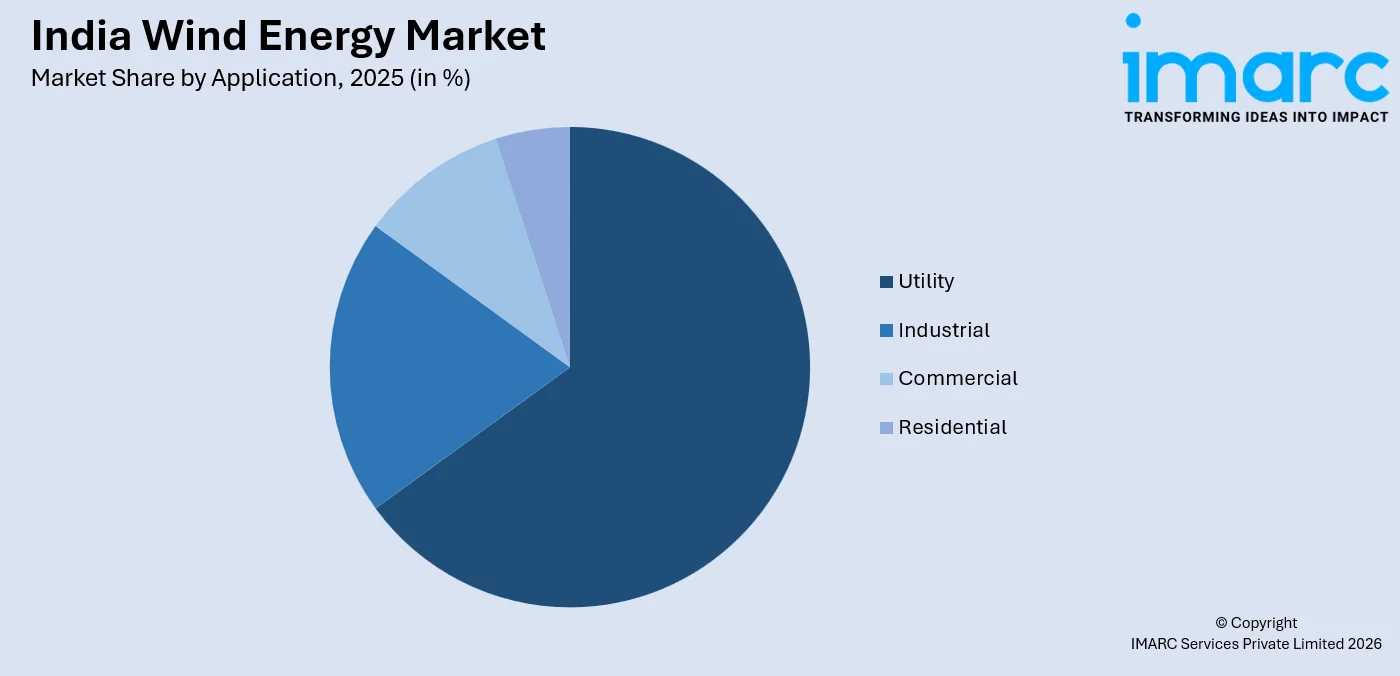

- Utility leads application at 64.8% in 2025 - PSU procurement by NTPC and SECI-tendered capacity drives the bulk of additions. Suzlon's 1,166 MW NTPC Green order in September 2024, India's largest-ever single wind award, exemplifies the utility segment's structural primacy over C&I off-takers.

- South India leads regionally at 38.4% in 2025 - Tamil Nadu, Karnataka, and Andhra Pradesh, together accounting for nearly half of India’s total wind energy capacity, which currently stands at about 54 GW.

India Wind Energy Market Trends and Dynamic 2026

Market Trends

Acceleration of Higher-Capacity 3–5 MW Turbine Deployments

India's wind market is at a technological turning point as it is moving to higher-rated wind turbines to achieve more power per site and reduce the levelized cost of energy. MNRE's ALMM (Wind) approved 13 wind turbine manufacturers with ratings from sub-2 MW to 5.3 MW. In December 2025, Envision Energy commissioned India's first 5 MW wind turbine at CleanMax's project site in Mudugal, Karnataka, marking a commercial milestone in next-generation turbine deployment.

Domestic Manufacturing Expansion and Supply-Chain Localization

India's wind turbine manufacturing capacity grew from 12 GW per annum in 2022 to 20 GW per annum in 2024, positioning domestic OEMs to potentially capture 10% of global supply by 2030. MNRE's ALMM (Wind) and ALMM Wind Turbine Components mandates now require that listed components, including blades, towers, generators, gearboxes, and special bearings, be sourced only from approved domestic producers, accelerating supply-chain localization across the turbine manufacturing value chain.

- Corporate Open-Access Wind Procurement: Energy-intensive industrial and commercial consumers are increasingly entering into wind power procurement through open-access routes, with wind developers like CleanMax and Serentica spearheading industrial and commercial wind capacity addition in states like Karnataka, Tamil Nadu, and Maharashtra.

- Green Hydrogen Integration: Wind capacity is now being integrated with electroliers for green hydrogen production. This is a new trend that enables renewable electricity to be directly converted into hydrogen form for large-scale decarbonization.

- Offshore Wind Development Restart: In October 2025, MNRE planned to launch a tender for offshore wind power development along the coast of Tamil Nadu by early 2026, after 4.5 GW of offshore tenders were cancelled in August 2025 due to concerns over commercial viability.

Growth Drivers

Government's 100 GW Wind Target and Supporting Policy Architecture

India's target of 100 GW from wind energy by 2030 is underpinned by its policy framework that requires 10 GW of onshore wind bids to be made every year, wind energy-specific RPOs, and an announcement of INR 74,000 crores under the Prime Minister's COP26 announcement for renewable projects. The Union Budget 2026 allocated INR 600 crores to the Green Energy Corridor for 6,000 km of intra-state transmission to directly support grid evacuation for wind projects.

Record Turbine Order Activity and New Entrant Manufacturing Investment

India's turbine order pipeline is rising, with domestic companies Suzlon and Inox Wind dominating the annual volumes of new contracts. Adani Wind won orders worth 304 MW of external turbine orders in August 2025 for its 3.3 MW model at four locations in Gujarat and Tamil Nadu. New entrants in the wind industry, namely, Envision Energy and SANY, have increased the competitive landscape of the industry, leading to a faster technology transfer and a wider variety of turbine models available in the Indian market.

- State-Level Wind Targets and Auction Pipelines: Andhra Pradesh, Rajasthan, and Telangana have set ambitious wind targets with active state-level auction programs, expanding the national tendering pipeline beyond SECI.

- Industrial and Corporate RE Procurement: Energy-intensive manufacturers are signing long-term wind power purchase agreements under captive and group captive models, providing wind developers with revenue certainty outside DISCOM procurement and enabling capacity additions in states with strong C&I demand.

- Advances in Turbine Technology and Cost Reduction: Improvements in turbine efficiency, taller hybrid lattice towers, and larger rotor diameters are raising capacity utilization factors across India's wind sites, reducing the levelized cost of energy and strengthening the competitive position of onshore wind against alternative generation technologies.

Market Restraints

Transmission Infrastructure Gaps and Grid Evacuation Bottlenecks: The growth of wind energy in India is being impeded by gaps in inter-state and intra-state transmission infrastructure, especially in states with high wind energy potential. Project commissioning is being delayed due to grid connectivity challenges, right-of-way issues, and the pace of transmission corridor upgradation lagging behind the pace of tendering and awarding renewable energy projects.

Land Acquisition Complexity and Environmental Clearance Delays: Onshore wind energy projects involve large tracts of land acquisition and are associated with long regulatory approval cycles from state and central governments. The conversion of agricultural and forest lands to accommodate onshore wind projects, along with opposition from local populations to tall modern wind turbine installations, is causing delays in project commissioning.

Offshore Wind Commercial Viability Challenges: India's offshore wind ambitions face structural barriers, including high capital intensity, the absence of a mature domestic offshore supply chain, inadequate port infrastructure for marine installation, and insufficient viability gap funding to bridge the gap between project economics and commercially acceptable tariff levels, deterring developer participation across successive offshore tender rounds.

India Wind Energy Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Turbine | 45.3% | 2025 |

| Rating | >2 ≤ 5 MW | 38.7% | 2025 |

| Installation | Onshore | 98.2% | 2025 |

| Turbine Type | Horizontal Axis | 97.5% | 2025 |

| Application | Utility | 64.8% | 2025 |

| Region | South India | 38.4% | 2025 |

Component Insights

Turbine - 45.3% Market Share (2025) | Leading Component

Wind turbines represent the dominant cost item in any wind installation, comprising around 50% of project capital expenditure. The major components of wind turbines, which are considered to be costly, are blades, nacelles, and towers. Further, changes in larger turbine sizes and more efficient components are significantly influencing the procurement scenario and are improving project economics in India’s wind energy market.

|

Segment Breakdown Turbine (45.3%) · Support Structure · Electrical Infrastructure · Others |

Rating Insights

>2 ≤ 5 MW - 38.7% Market Share (2025) | Leading Rating

The >2-5 MW class is India’s largest commercial class, matching India’s main onshore wind resource characteristics and MNRE’s ALMM Program. The most widely procured machine in this class is Suzlon’s 3.15 MW S144. In August 2025, Adani Wind was awarded 304 MW of external turbine orders for its 3.3 MW class from independent power producers in Gujarat and Tamil Nadu. This reiterates the commercial supremacy of this class in both domestic OEM and captive developer procurement segments.

|

Segment Breakdown >2 ≤ 5 MW (38.7%) · ≤ 2 MW · >5 ≤ 8 MW · >8 ≤ 10 MW · >10 ≤ 12 MW · >12 MW |

Installation Insights

Onshore - 98.2% Market Share (2025) | Leading Installation

India’s entire commercial wind energy portfolio is comprised of onshore capacity, a reflection of the lack of commissioned offshore capacity up to 2025. India’s strategy is to develop large onshore wind corridors in states such as Tamil Nadu, Gujarat, and Karnataka, where there is a conducive wind regime and grid connectivity. Offshore wind is still in the planning stages, with pilot projects to be developed off Gujarat and Tamil Nadu.

|

Segment Breakdown Onshore (98.2%) · Offshore |

Turbine Type Insights

Horizontal Axis - 97.5% Market Share (2025) | Leading Turbine Type

Horizontal Axis Wind Turbines are the universally adopted norm for wind energy generation on a utility scale in India, providing the highest level of aerodynamic efficiency and suitability for the rotor diameters and tower heights applicable to India's primary onshore wind energy sites. All commercially available wind turbines included in the MNRE's ALMM (Wind) list are horizontal-axis wind turbines, and contemporary rotor diameters for wind turbines rated for the highest capacity are over 170 meters.

|

Segment Breakdown Horizontal Axis (97.5%) · Vertical Axis |

Application Insights

Access the comprehensive market breakdown Request Sample

Utility - 64.8% Market Share (2025) | Leading Application

Utility is the leading category for wind energy applications in India, driven by high-capacity power purchase agreements and PSU-led procurement through NTPC and SECI mechanisms. These comprise multi-megawatt wind farms that supply power directly to the grid, providing long-term revenue assurance for wind energy investors. Moreover, the ongoing implementation of competitive bidding and hybrid renewable tendering is also enhancing the growth trajectory for utility wind energy in India.

|

Segment Breakdown Utility (64.8%) · Industrial · Commercial · Residential |

Regional Insights

South India - 38.4% Market Share (2025) | Leading Region

The South Indian market dominates the Indian market in terms of wind power, anchored by Tamil Nadu (11,830.36 MW) and Karnataka (7,714.74 MW). The Muppandal Wind Farm in the Kanyakumari district of Tamil Nadu is the biggest onshore wind farm in India, producing 1,500 MW of power. Andhra Pradesh is fast emerging as the third leader in the South Indian market. It targets 35 GW of installed wind power by 2029.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

38.4%

|

|

Key States

|

Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala |

|

Major Growth Drivers

|

Highest national wind resource concentration, established manufacturing ecosystem, Tamil Nadu repowering policy |

|

Outlook

|

Dominant region with offshore wind as long-term upside |

North India:

North India's wind development is concentrated in Rajasthan, which set a target of 25 GW of wind and hybrid energy by 2030 under its Integrated Clean Energy Policy 2024. Madhya Pradesh contributed 351 MW of new wind capacity in Q1 2025, a significant resurgence after negligible prior-quarter additions, reflecting improving transmission access and developer interest.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Rajasthan, Madhya Pradesh, Himachal Pradesh, Uttarakhand |

|

Major Growth Drivers

|

25 GW Rajasthan wind and hybrid target, green hydrogen nexus, ISTS transmission waiver, flat terrain enabling large turbine logistics |

|

Outlook

|

Emerging as a major wind-solar-hydrogen supply corridor by 2030 |

East India:

East India remains the least-developed wind region, constrained by lower average wind speeds and infrastructure gaps. In April 2025, Assam set a 200 MW wind target under its Integrated Clean Energy Policy, its first wind-specific commitment. This move signals the region’s increasing focus on renewable energy, aiming to tap into its wind energy potential and contribute to India's green energy transition.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Odisha, West Bengal, Assam, Jharkhand |

|

Major Growth Drivers

|

Policy activation in Assam, industrial electricity demand growth, Green Energy Corridor transmission expansion, RPO compliance obligations |

|

Outlook

|

Nascent stage; long-term upside as transmission and policy frameworks mature |

West India:

West India is led by Gujarat, India's largest wind state with 13,816.68 MW of installed capacity, supported by 7.5 m/s average wind speeds at 120-metre hub heights and a single-window clearance process. In January 2025, Suzlon and Torrent Power signed a 486 MW hybrid order in Gujarat's Bhogat region, bringing their cumulative collaboration to 1 GW across Gujarat and Karnataka.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Gujarat, Rajasthan, Maharashtra, Madhya Pradesh |

|

Major Growth Drivers

|

Gujarat coastal wind resource and clearance efficiency, Rajasthan 25 GW hybrid energy target, Maharashtra industrial power demand |

|

Outlook

|

Gujarat retains cumulative leadership; Rajasthan expanding as wind-solar-hydrogen nexus |

Market Outlook 2026-2034

What is the future outlook of India wind energy market?

India wind energy market is expected to sustain steady capacity growth through 2034.

India wind energy market is positioned for sustained expansion through 2034, underpinned by the government's 100 GW wind target, record domestic turbine manufacturing capacity of 20 GW per annum, and a deepening project pipeline under construction. Turbine technology advancement toward the 3–5 MW class, accelerating PSU and C&I offtake, wind-solar hybrid integration, and the progressive development of offshore wind infrastructure will collectively drive capacity additions. India's third-place global ranking and its ambition to supply 10% of global turbine demand by 2030 reinforce the India wind energy market forecast.

India Wind Energy Market - Leading Key Players

India wind energy market is shaped by a competitive landscape encompassing domestic OEMs with deep manufacturing roots, large-scale independent power producers, and PSU-backed developers. Domestic turbine manufacturers hold a structural cost advantage through local component sourcing, while large IPPs and PSUs drive demand through long-term PPAs and utility auction participation. New entrants from China, including Envision Energy and SANY, are intensifying competition at the higher capacity bands and accelerating technology transfer within the country's wind manufacturing ecosystem.

| Company | Leading Brands | Highlights |

|---|---|---|

| Suzlon Energy Limited | S120 (2.1 MW), S133 (2.6–3 MW), S144 (up to 3.15 MW) | India's No. 1 wind energy company managing ~15 GW of assets; secured India's largest single wind order of 1,166 MW from NTPC Green Energy in September 2024; net debt-free with over 5 GW in active order book as of September 2024 |

| Inox Wind Limited | 2 MW and 3 MW turbine series; upcoming 4. X MW platform | Captured a significant share of annual contract volumes alongside Suzlon, with both firms holding over 50% of India's annual turbine contract volumes for three consecutive years; preparing to launch 4 MW-class turbines |

| ReNew Energy Global | Wind power generation projects/renewable energy portfolio | Commissioned 250 MW wind project in Maharashtra in Q3 2025: one of India's largest IPP wind developers with an extensive portfolio across SECI ISTS and state-level auction tenders |

Some of the existing key players in the market are Envision Energy India, SANY Renewable Energy, NTPC Renewable Energy Limited, Vayona Energy, Greenko Group, Torrent Power, Sembcorp Green Infra, Juniper Green Energy, etc.

Latest Development & News

- In October 2025, Envision Energy India secured a 501.6 MW wind turbine generator order from renewable developer Evren, agreeing to supply about 152 units of its EN156/3.3 MW smart wind turbines for projects in Andhra Pradesh. The turbines feature a 156-meter rotor diameter and 140-meter hub height and are optimized for Indian wind conditions.

- In January 2025, Suzlon Energy secured a 486 MW wind-solar hybrid order from Torrent Power in Gujarat's Bhogat region, involving 162 S144 wind turbine generators rated at 3 MW each on Hybrid Lattice Towers. The order brought the companies' cumulative collaboration to 1 GW across Gujarat and Karnataka, designed to deliver power to approximately one million households and exemplifying the growing wind-solar hybrid procurement model.

India Wind Energy Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Turbine, Support Structure, Electrical Infrastructure, Others |

| Ratings Covered | ≤ 2 MW, >2 ≤ 5 MW, >5 ≤ 8 MW, >8 ≤ 10 MW, >10 ≤ 12 MW, > 12 MW |

| Installations Covered | Offshore, Onshore |

| Turbine Types Covered | Horizontal Axis, Vertical Axis |

| Applications Covered | Utility, Industrial, Commercial, Residential |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Wind Energy Market Report

India wind energy market stood at 55.28 GW in 2025.

The market is anticipated to reach 156.88 GW by 2034.

Turbine dominates the market with a share of 45.3% in 2025, representing 40–50% of total wind project capital expenditure. All 13 ALMM-enlisted manufacturers supply turbines as the core component, making it the most competitively contested segment in India's wind supply chain.

>2 ≤ 5 MW dominates the market with a share of 38.7% in 2025, driven by the growing deployment of 3.3–5.2 MW models from Adani Wind and Envision across onshore project sites in Gujarat and Karnataka.

Onshore dominates the market with a share of 98.2% in 2025, reflecting that all commercial wind capacity additions in India remain land-based through the near term.

Horizontal axis dominates the market with a share of 97.5% in 2025, as HAWT technology is the universal standard for utility-scale wind generation in India.

Utility dominates the market with a share of 64.8% in 2025, driven by PSU procurement from NTPC and SECI-tendered capacity. Suzlon's 1,166 MW NTPC Green order further exemplifies the scale of institutional utility procurement underpinning this segment's leadership.

South India dominates the market with a share of 38.4% in 2025, anchored by Tamil Nadu, Karnataka, and Andhra Pradesh’s growing installed wind capacity.

Key growth drivers include India's 100 GW wind target backed by 10 GW annual onshore auction mandates, PSU-led utility procurement by NTPC and SECI, domestic turbine manufacturing capacity of 20 GW per annum, wind-solar hybrid procurement frameworks, and state-level targets from Andhra Pradesh (35 GW), Rajasthan (25 GW), and Karnataka, driving incremental additions.

Some of the major players in the market are Suzlon Energy Limited, Inox Wind Limited, ReNew Energy Global, Adani Green Energy Limited, JSW Energy Limited, Envision Energy India, SANY Renewable Energy, NTPC Renewable Energy Limited, Vayona Energy, and Greenko Group.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)