Indian Agricultural Implements Market Size, Share, Trends and Forecast by Product Type, Type, Distribution Channel, and Region, 2026-2034

Indian Agricultural Implements Market Summary:

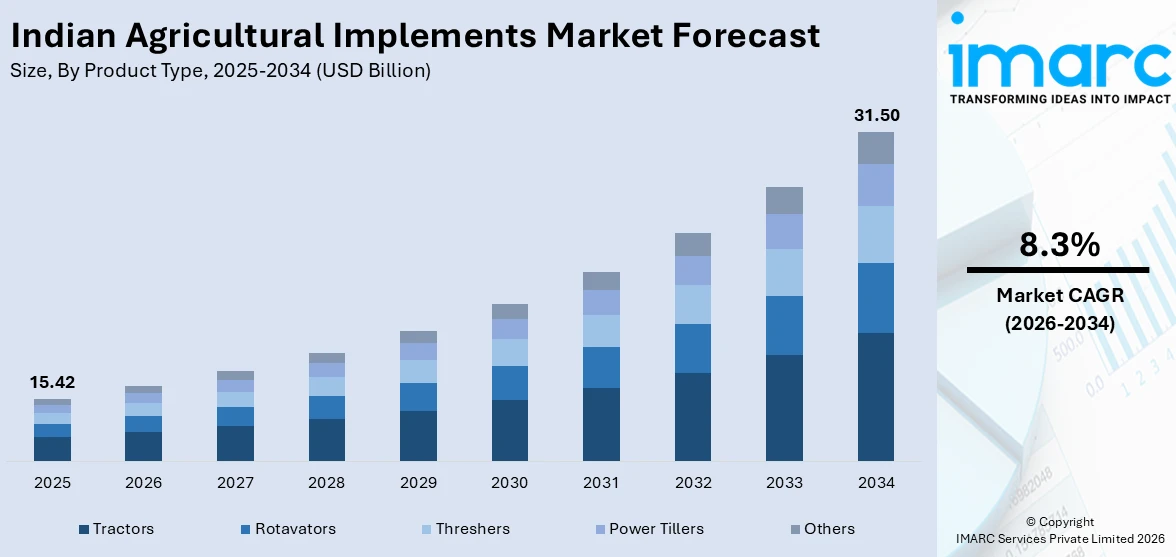

The Indian agricultural implements market size was valued at USD 15.42 Billion in 2025 and is projected to reach USD 31.50 Billion by 2034, growing at a compound annual growth rate of 8.3% from 2026-2034.

India's agricultural implements sector is undergoing a structural transformation driven by large-scale farm mechanization, evolving cropping patterns, and supportive government policies that are making modern implements more accessible. The widespread adoption of tractors, rotavators, and power tillers is enabling farmers to enhance productivity, reduce input costs, and manage labor shortages more effectively. Continued investment in rural infrastructure, expanding custom-hiring networks, and favorable rural credit conditions are collectively reinforcing growth across the Indian agricultural implements market share.

Key Takeaways and Insights:

- By Product Type: Tractors dominate the market with a share of 35% in 2025, driven by their unmatched versatility across tillage, sowing, haulage, and a range of other farm operations that make them indispensable across all agro-climatic zones in India.

- By Type: Mechanized lead the market with a share of 70% in 2025, reflecting the strong nationwide shift away from manual and animal-drawn tools toward engine-powered and tractor-operated equipment, accelerated by rising rural wages and labor shortages.

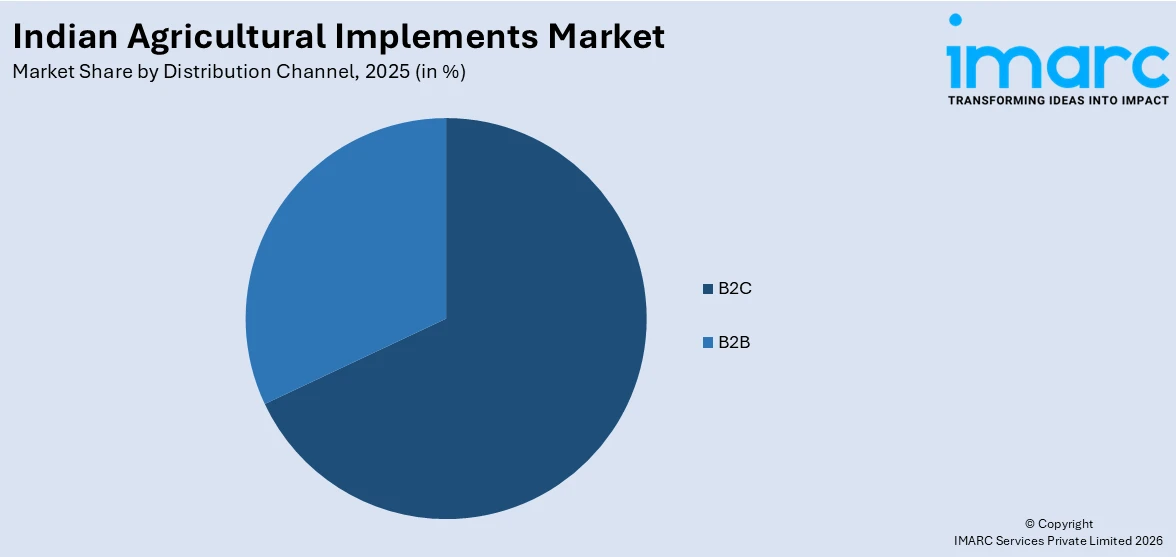

- By Distribution Channel: B2C represents the largest share of 68% in 2025, as individual farmers continue to purchase implements directly through authorized dealerships, tractor showrooms, and agri-equipment retail outlets across urban and semi-urban markets.

- Key Players: The Indian agricultural implements market is characterized by intense competition among domestic and multinational manufacturers. Some of the major market players include Mahindra & Mahindra Limited, Tractors and Farm Equipment Limited, Sonalika International Tractors Limited, Escorts Group, and Deere & Company.

To get more information of this market Request Sample

India has consistently ranked among the world's largest agricultural equipment markets, underpinned by the fact that over half its population depends on farming for livelihood. The Green Revolution laid the foundation for mechanization, and successive policy interventions have deepened its reach. The Sub-Mission on Agricultural Mechanization (SMAM), which provides financial assistance of 40–50% on machinery purchases, has been particularly transformative in enabling smallholder farmers to access modern equipment. The establishment of thousands of Custom Hiring Centres (CHCs) and Farm Machinery Banks (FMBs) across low-mechanization states has addressed the economics of small land holdings, which otherwise make individual ownership cost-prohibitive. The India tractor market size reached USD 9.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 15.9 Billion by 2034, exhibiting a growth rate (CAGR) of 6.05% during 2026-2034, with monthly figures regularly surging during sowing and harvesting seasons, underscoring the deepening integration of mechanized implements into the agricultural workflow.

Indian Agricultural Implements Market Trends:

Rising Adoption of Precision Farming Technologies and Smart Implements

A defining trend reshaping the Indian agricultural implements market is the gradual but accelerating integration of precision farming technologies into conventional equipment. GPS-enabled tractors, sensor-based soil monitoring systems, and telematics platforms are being embedded into new implement models, allowing farmers to optimize field operations with data-driven accuracy. The Government of India's Digital Agriculture Mission, which aims to create a unified farmer registry and geotagged crop database, is creating the institutional infrastructure to support precision equipment deployment at scale. For instance, Mahindra Tractors launched its OJA platform with a dedicated MYOJA telematics pack and PROJA productivity automation system, enabling real-time farm monitoring and reduced operator fatigue across compact field conditions in India.

Surge in Demand for Alternate-Fuel and Sustainable Agricultural Implements

Growing awareness of carbon emissions and rising diesel costs are prompting both manufacturers and farmers to explore alternate-fuel implement technologies. CNG, compressed biogas (CBG), and ethanol flex-fuel tractors are transitioning from prototypes to commercially viable products. This trend aligns closely with India's national ambition of achieving net-zero emissions by 2070, with the agricultural machinery sector identified as a key contributor. For instance, in November 2025, Mahindra & Mahindra showcased its full lineup of alternate-fuel tractors, including CNG/CBG dual-fuel models and an ethanol flex-fuel engine based on the Yuvo Tech+ platform, at Agrovision 2025 in Nagpur, underscoring an industry-wide commitment to sustainable mechanization.

Expansion of Custom Hiring Centres Driving Implement Access for Smallholder Farmers

India’s fragmented landholding pattern, where many farmers operate small plots, has traditionally limited the ability to purchase expensive agricultural machinery. Custom Hiring Centres (CHCs) are helping address this challenge by enabling farmers to rent equipment based on usage rather than owning it outright. Supported by government initiatives that provide financial assistance for establishing such centers, CHCs are expanding across regions with relatively low mechanization levels. This model significantly improves access to modern agricultural implements for small and marginal farmers, allowing them to benefit from mechanization without the burden of high upfront capital investment.

Market Outlook 2026-2034:

The Indian agricultural implements market is poised for sustained expansion through the forecast period, supported by the continued policy push toward farm mechanization, rising agricultural productivity targets, and the growing penetration of mechanized solutions in historically underserved regions such as East India and the northeastern states. Improved rural road connectivity, the expansion of dealer and service networks, and growing farmer awareness of the long-term economic benefits of mechanization are expected to support stronger demand for agricultural equipment. At the same time, supportive policy measures aimed at lowering the cost of machinery ownership can further encourage adoption, making modern farm equipment more accessible and financially viable for farmers across rural regions. The market generated a revenue of USD 15.42 Billion in 2025 and is projected to reach a revenue of USD 31.50 Billion by 2034, growing at a compound annual growth rate of 8.3% from 2026-2034.

Indian Agricultural Implements Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Tractors |

35% |

|

Type |

Mechanized |

70% |

|

Distribution Channel |

B2C |

68% |

Product Type Insights:

- Tractors

- Rotavators

- Threshers

- Power Tillers

- Others

Tractors dominate the Indian agricultural implements market with a share of 35% in 2025.

Tractors represent the backbone of mechanized farming in India, functioning as the primary power source for an extensive range of tractor-operated implements, including rotavators, seed drills, cultivators, and sprayers. Their dominance in the market stems from their unmatched operational versatility; a single tractor can support tillage preparation, inter-cultivation, sowing, plant protection, and post-harvest haulage across a full crop calendar. India is the world's largest tractor market by volume, and the segment has benefited enormously from government subsidies under SMAM, easy rural credit access, and a deeply established pan-India dealership and service network. The 30–50 HP range remains the highest-volume category, catering to the diverse field requirements of medium-sized farms across North India, Maharashtra, and the Deccan plateau.

Manufacturers are increasingly broadening their tractor product portfolios to cater to specialized and emerging agricultural applications. New models are being developed to address specific farming requirements such as orchard cultivation, haulage, and operations in diverse crop environments, reflecting the industry’s focus on greater functionality and user comfort. At the same time, companies are investing in new manufacturing facilities to expand production capacity and strengthen their presence in the domestic market. The combination of product diversification, evolving farmer expectations, and supportive government initiatives is expected to maintain tractors as the leading segment within the agricultural implements industry over the coming years.

Type Insights:

- Manual

- Mechanized

Mechanized represent the leading position with a share of 70% of the total Indian agricultural implements market in 2025.

Mechanized agricultural implements include a wide range of engine-powered and tractor-operated equipment such as combine harvesters, rotavators, seed drills, cultivators, and power weeders. Their growing prominence reflects a long-term transformation in Indian agriculture, where farmers are gradually shifting from labor-intensive practices to mechanized solutions. Rising rural labor costs, the challenges associated with an aging agricultural workforce, and the need to enhance farm productivity are encouraging greater adoption of modern equipment. Government programs that provide financial support for power tillers, rotavators, and other engine-driven implements have further improved affordability, enabling even smallholder farmers to adopt mechanized farming tools.

The mechanized implements segment continues to gain momentum as farmers become increasingly aware of the productivity and efficiency advantages offered by modern equipment. Research conducted by agricultural institutions and government bodies highlights the potential of mechanization to improve crop yields while reducing cultivation costs over time. In addition, the expansion of Custom Hiring Centres has made mechanized tools accessible to farmers who may not be able to purchase equipment outright. The integration of emerging technologies such as drones and precision agriculture solutions is further strengthening the role of mechanized systems, supporting their continued prominence within India’s agricultural equipment landscape.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- B2C

- B2B

B2C represent the highest revenue share with 68% of the total Indian agricultural implements market in 2025.

Business-to-consumer (B2C) distribution channels dominate India’s agricultural implements market due to the large number of individual farming households that purchase equipment directly from authorized dealers, agri-equipment retailers, and tractor showrooms. Large dealer systems in rural areas are significant in facilitating this channel because of the availability and accessibility of the products. What makes these outlets, in addition to being points of sale, is the fact that they provide services of maintaining their equipment and provision of spares, which builds the confidence of the farmers whenever it comes to owning their equipment. The availability of localized service support also enhances customer relationships and induces repeat purchases.

The growth of B2C distribution has also been supported by the increasing availability of rural financing options that help farmers manage the cost of agricultural machinery. Financial institutions, cooperative banks, and microfinance organizations are expanding their presence in rural areas, offering credit solutions tailored to farm equipment purchases. These financing arrangements make it easier for individual farmers to acquire modern implements without significant upfront capital. Although business-to-business channels serving agribusiness firms and institutional buyers are gradually expanding, the B2C segment is expected to remain dominant due to the country’s largely smallholder farming structure.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India, anchored by Punjab, Haryana, and Uttar Pradesh, has historically been the most mechanized agricultural region in the country and continues to generate the highest demand for tractors, combine harvesters, and precision tillage implements. Its large farm sizes, wheat-rice double-cropping systems, and well-established rural credit markets create ideal conditions for high-value implement adoption.

West and Central India, encompassing Maharashtra, Gujarat, Madhya Pradesh, and Rajasthan, represents a dynamic growth market where soybean, cotton, and sugarcane cultivation is driving demand for specialized equipment such as rotavators, seed drills, and sugarcane harvesters. State governments in this region have been active in disbursing SMAM funds to support CHC establishment.

South India, covering Karnataka, Andhra Pradesh, Telangana, and Tamil Nadu, is witnessing increased adoption of compact tractors, paddy transplanters, and power weeders, reflecting the region's diverse cropping systems including paddy, horticultural crops, and plantation agriculture. Escorts Kubota has noted a strengthening presence in southern India as a factor supporting its market share growth.

East India, comprising Bihar, West Bengal, Odisha, and Jharkhand, remains underpenetrated relative to its agricultural potential, with low farm power availability per hectare. However, targeted government programs, including SMAM's dedicated North-Eastern Region component offering up to 95% subsidized Farm Machinery Bank establishment, are beginning to unlock latent demand in this region.

Market Dynamics:

Growth Drivers:

Why is the Indian Agricultural Implements Market Growing?

Government Subsidies and Policy Support Under SMAM and Allied Schemes

Government initiatives promoting farm mechanization have emerged as a major catalyst for the growth of the agricultural implements sector in India. Under national agricultural development programs, farmers receive financial assistance to purchase a wide range of farm machinery, with additional support often extended to smallholders, women farmers, and socially disadvantaged groups. These initiatives also encourage the establishment of Custom Hiring Centres and Farm Machinery Banks, which enable farmers to access equipment on a shared or rental basis. Various state-level schemes further complement these efforts by supporting the adoption of modern tools such as planters, transplanters, and harvesting equipment. In addition, supportive policy measures, including incentives for emerging technologies and favorable tax policies on agricultural machinery, are improving affordability and encouraging farmers to transition toward mechanized farming practices.

Intensifying Rural Labor Shortage Driving Mechanization Imperative

A structural and accelerating labor shortage in rural India is emerging as one of the most powerful long-term drivers of agricultural implements demand. Large-scale migration of rural youth to urban centers in search of industrial and service-sector employment has dramatically reduced the availability of agricultural laborers, particularly during the time-critical sowing and harvesting windows. The National Rural Employment Guarantee Act (NREGA) has compounded this dynamic by providing year-round rural employment alternatives, significantly reducing the seasonal inflow of migrant laborers to major farming states such as Punjab and Haryana during the kharif transplantation season. As a result, demand for tractors, power tillers, rotavators, and harvesting equipment has surged in these states, where farmers face acute labor constraints during peak periods. The fundamental economics of mechanization, where machines replace scarce and increasingly expensive labor while improving timeliness of operations, ensures that this driver will remain durable across the forecast period, even as agricultural wages continue to rise in response to competing employment opportunities.

Rising Agricultural Incomes and Expanding Rural Credit Penetration

India’s steady economic growth and periodic revisions in agricultural support pricing have gradually strengthened rural household incomes, allowing more farmers to invest in modern agricultural implements. Favorable climatic conditions that support strong crop output also improve farm cash flows, encouraging farmers to allocate greater resources toward machinery purchases. As agricultural productivity and income stability improve, the willingness to adopt mechanized solutions continues to rise across farming communities. In addition, the expansion of formal rural banking infrastructure has significantly improved access to equipment financing in many agricultural regions. Cooperative banks, regional rural banks, and microfinance institutions are increasingly offering credit products tailored for farm machinery purchases. Equipment manufacturers are also collaborating with financial institutions to develop specialized lending programs that make machinery more accessible to farmers. These financing initiatives, combined with rising rural incomes, are helping accelerate the adoption of agricultural implements across diverse farming segments.

Market Restraints:

What Challenges the Indian Agricultural Implements Market is Facing?

High Initial Capital Cost for Small and Marginal Farmers

Despite government subsidies, the absolute purchase price of mechanized agricultural implements remains prohibitive for a significant proportion of small and marginal farmers who cultivate fewer than two hectares. Tractors, combine harvesters, and other high-value implements involve substantial upfront capital expenditure that may be difficult to recoup on small landholdings where the economics of individual ownership are unfavorable. Inadequate awareness of financing options and subsidy schemes further limits access among the most economically vulnerable farming households.

Fragmented Land Holdings Limiting Operational Efficiency

India's average farm size remains very small due to generations of land subdivision, making it economically inefficient for individual farmers to deploy large machinery across fragmented plots. Irregular field shapes, narrow access lanes, and non-contiguous holdings further reduce the productivity gains achievable through mechanization. While custom-hiring models partially address this constraint, logistical challenges in coordinating machinery movement across dispersed smallholdings remain a persistent structural restraint on the market's growth potential.

Inadequate After-Sales Service Infrastructure in Remote Areas

The availability of qualified service technicians, genuine spare parts, and maintenance facilities is unevenly distributed across India's vast rural geography. Farmers in remote areas of East India, Jharkhand, Chhattisgarh, and the northeastern states frequently face prolonged equipment downtime due to the absence of nearby service centers and the high cost of transporting machines to urban repair facilities. This service gap increases the total cost of ownership and reduces farmer confidence in purchasing high-value implements, particularly from brands with limited rural dealer density.

Competitive Landscape:

The Indian agricultural implements market exhibits a relatively concentrated yet highly competitive structure, with a small group of major manufacturers accounting for a significant share of the tractor and power equipment segment. Market leadership is largely supported by extensive dealer networks, broad product portfolios spanning multiple horsepower categories, and strong brand recognition developed through long-term presence in rural markets. Companies are increasingly differentiating themselves through technological advancements, international collaborations, and the expansion of manufacturing capabilities. At the same time, ongoing investments in production facilities and the introduction of technologically enhanced models are enabling manufacturers to strengthen their presence across key horsepower segments while addressing evolving farmer requirements. Some of the major market players include:

- Mahindra & Mahindra Limited

- Tractors and Farm Equipment Limited

- Sonalika International Tractors Limited

- Escorts Group

- Deere & Company

Recent Developments:

- August 2025: The Yamuna Expressway Industrial Development Authority (YEIDA) allotted approximately 200 acres of land to Escorts Kubota Limited in Sector-10 of YEIDA for establishing a Rs 4,500 crore integrated tractor and commercial equipment manufacturing plant. The facility, to be developed in phases starting with a Rs 2,000 crore initial investment, is expected to create employment for 4,000 people and significantly expand Escorts Kubota's production capacity.

- October 2025: Gromax Agri Equipment Limited, a joint venture between Mahindra & Mahindra and the Government of Gujarat, launched eight new Trakstar tractor models in a single event, spanning the 25–50 HP range in both 2WD and 4WD configurations. The launch included India's first sub-50 HP factory-fitted cabin tractor in the Trakstar Kavach Series, designed for haulage and agricultural tasks across diverse cropping environments.

Indian Agricultural Implements Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Tractors, Rotavators, Threshers, Power Tillers, Others |

| Types Covered | Manual, Mechanized |

| Distribution Channels Covered | B2C, B2B |

| Region Covered | North India, West and Central India, South India, East India |

| Companies Covered | Mahindra & Mahindra Limited, Tractors and Farm Equipment Limited, Sonalika International Tractors Limited, Escorts Group, Deere & Company |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Agricultural Implements Market Report

The Indian agricultural implements market size was valued at USD 15.42 Billion in 2025.

The Indian agricultural implements market is expected to grow at a compound annual growth rate of 8.3% from 2026-2034 to reach USD 31.50 Billion by 2034.

Tractors held the largest share in the Indian agricultural implements market, accounting for 35% of total market revenue in 2025. Their dominance is driven by operational versatility across multiple farm activities including tillage, sowing, haulage, and the operation of tractor-mounted implements, making them essential equipment across all agro-climatic regions.

Key factors driving the Indian agricultural implements market include government subsidies under SMAM that lower the effective cost of machinery ownership, acute rural labor shortages compelling farmers to adopt mechanized solutions, rising farm incomes and improving rural credit access, and a favorable policy environment including the recent GST reduction on tractors and agricultural equipment.

Major challenges include high initial capital costs for small and marginal farmers, fragmented and sub-optimal land holdings that limit the operational efficiency of large machinery, inadequate after-sales service infrastructure in remote rural areas, and uneven awareness of subsidy programs and financing options among the country's diverse farming population.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)