Indian Aluminium Powder Market Size, Share, Trends and Forecast by End-Use, Technology, Raw Material, Furnace Type, and Region, 2026-2034

Indian Aluminium Powder Market Size, Share, Trends & Forecast (2026-2034)

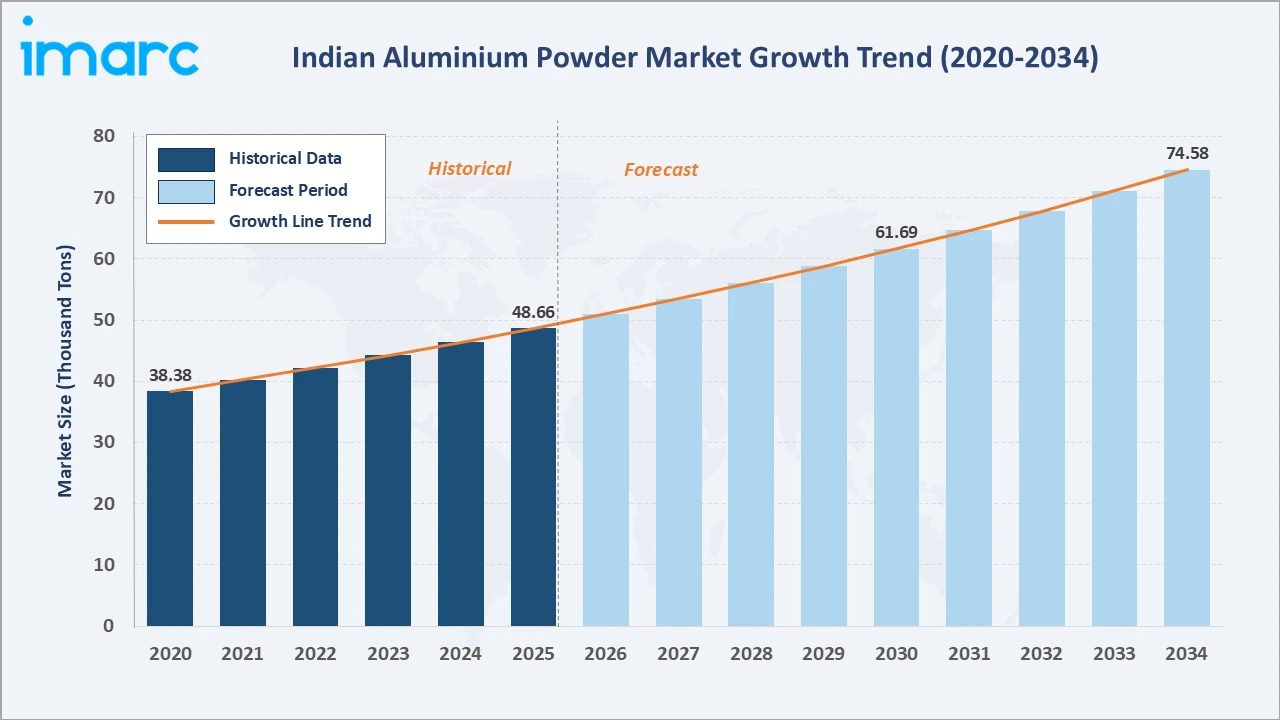

The Indian aluminium powder market reached a volume of 48.66 Thousand Tons in 2025 and is projected to reach 74.58 Thousand Tons by 2034, exhibiting a CAGR of 4.86% during 2026-2034. Rising demand from the pyrotechnics industry, increasing use of aluminium pastes in paints and coatings, and expanding construction activity are the primary drivers shaping the market growth.

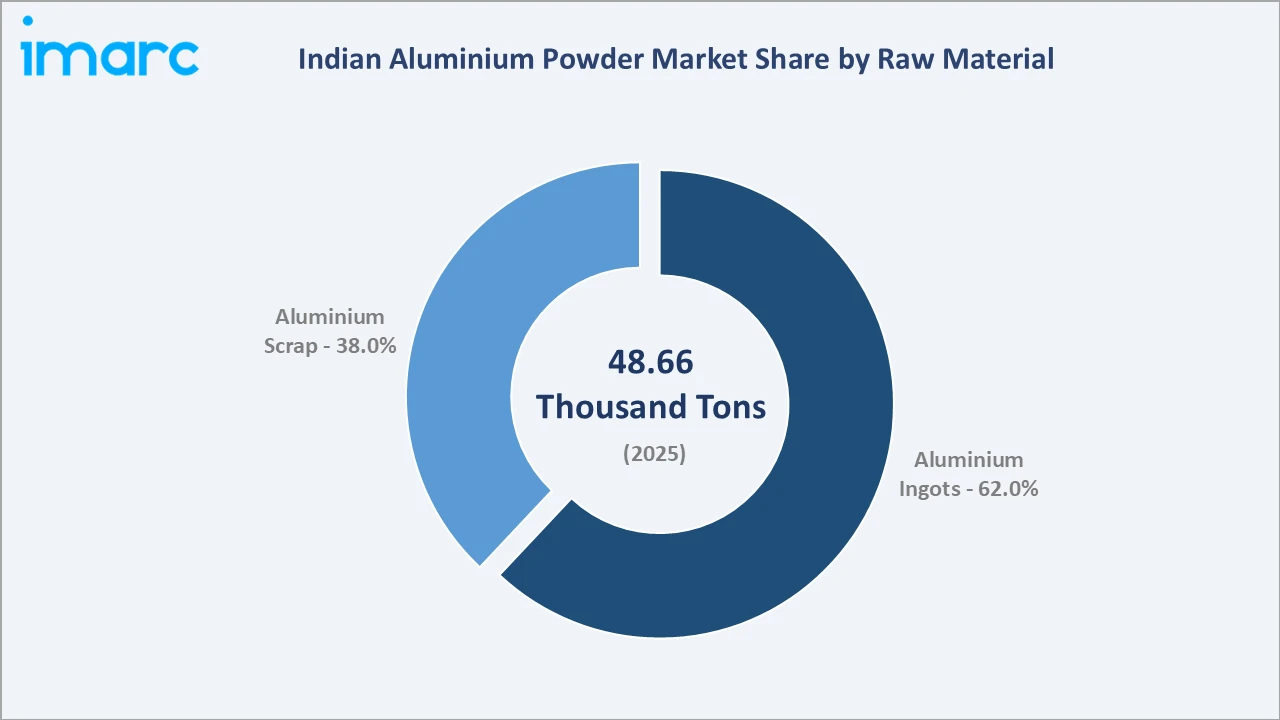

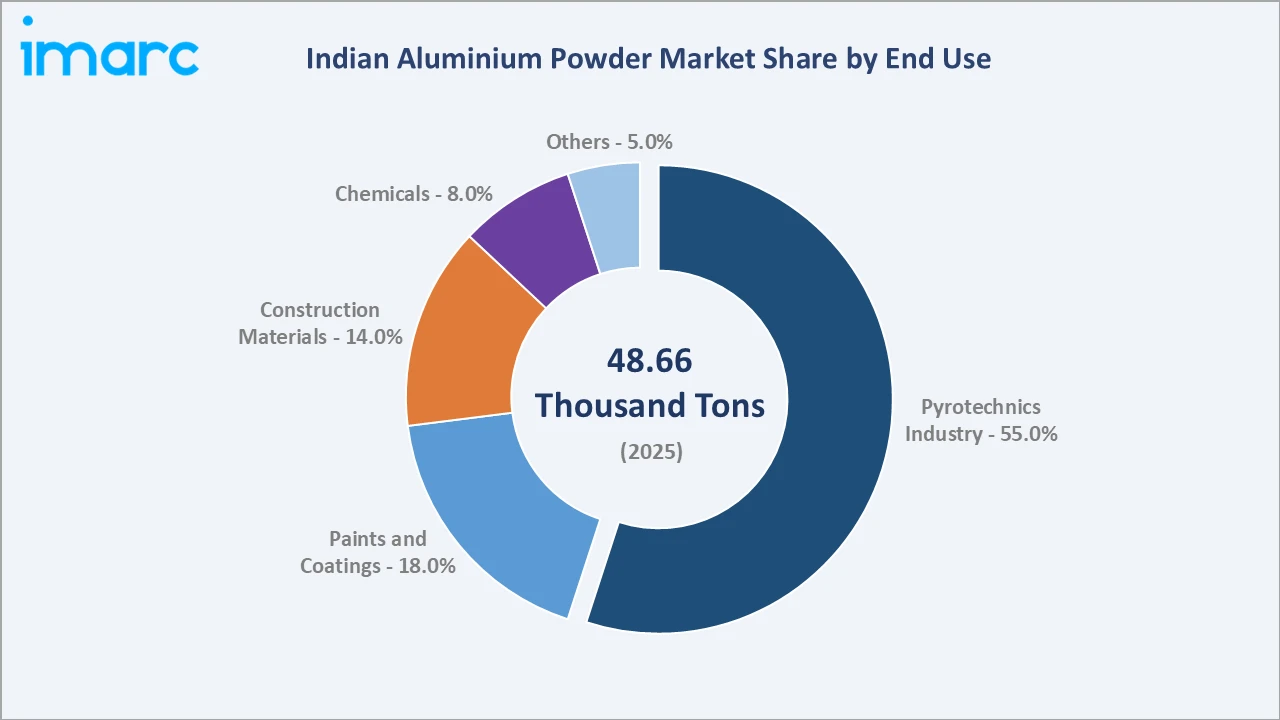

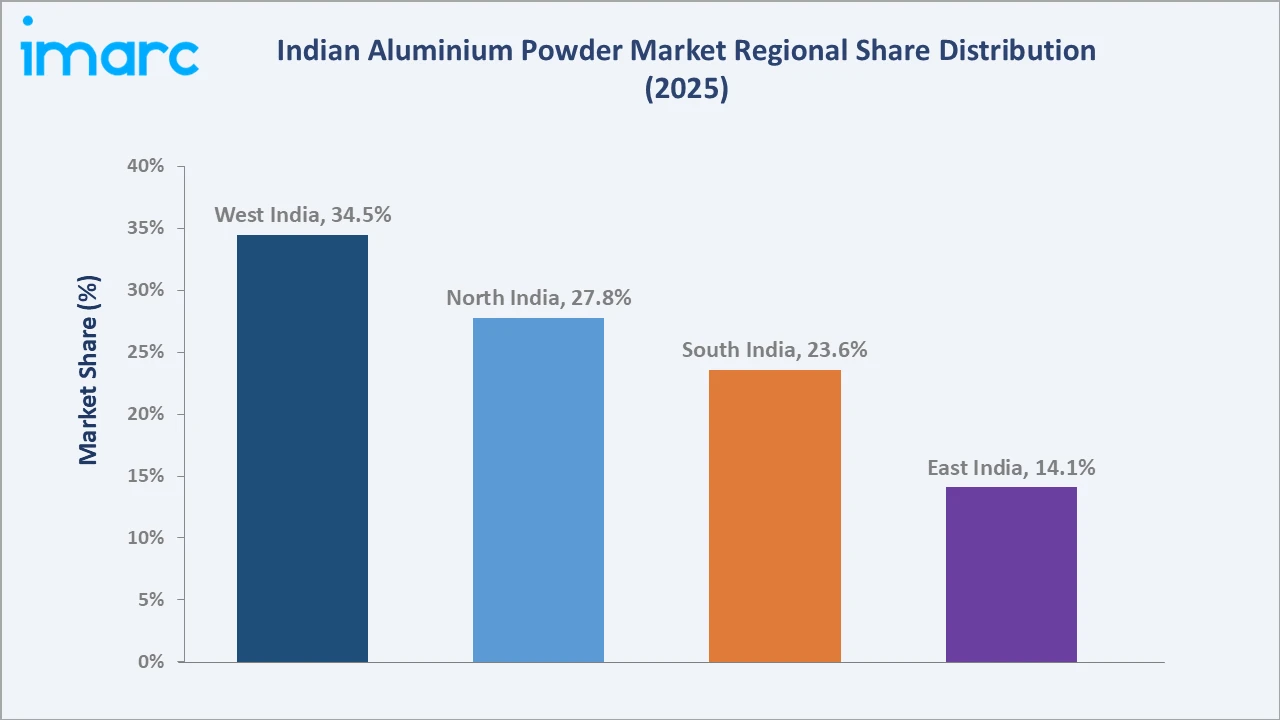

Aluminium ingots lead the raw material segment at 62.0% share, pyrotechnics industry dominates the end use segment with a 55.0% share, and West India commands the largest regional share at 34.5% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

48.66 Thousand Tons |

|

Forecast Market Size (2034) |

74.58 Thousand Tons |

|

CAGR (2026-2034) |

4.86% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (34.5%, 2025) |

|

Second Largest Region |

North India (27.8%, 2025) |

|

Leading Raw Material |

Aluminium Ingots (62.0%, 2025) |

|

Leading End Use |

Pyrotechnics Industry (55.0%, 2025) |

The Indian aluminium powder market expanded from 38.38 Thousand Tons in 2020 to 48.66 Thousand Tons in 2025, driven by rising consumption across pyrotechnics, construction, and paints applications. Anchored at 61.69 Thousand Tons in 2030, the market is forecast to reach 74.58 Thousand Tons by 2034, supported by growing scrap utilization and rising demand for pigment-grade powders.

To get more information on this market, Request Sample

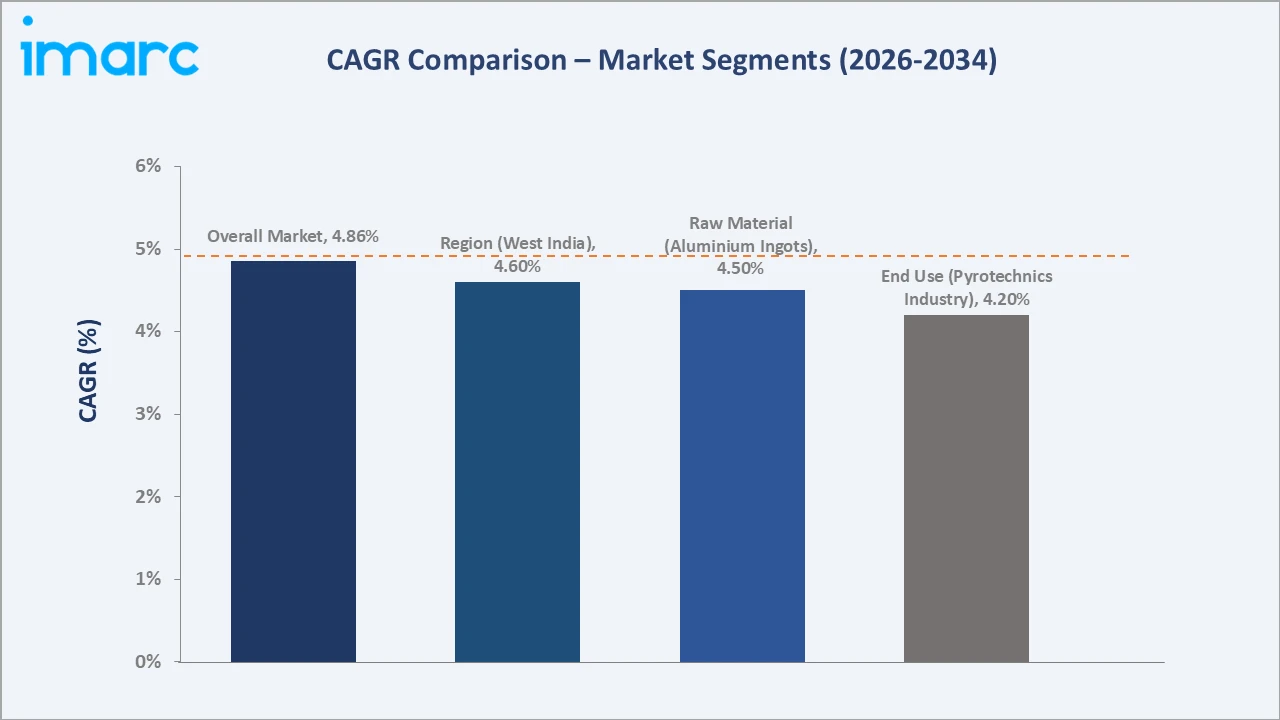

CAGR trajectories across raw material and end use sub-segments show paints and coatings and construction materials expanding faster than the overall 4.86% market CAGR, driven by rising infrastructure investment, growing automotive coatings demand, and increasing adoption of aluminium scrap as a cost-efficient feedstock.

Executive Summary

The Indian aluminium powder market is on a steady growth path, rising from 38.38 Thousand Tons in 2020 to 74.58 Thousand Tons by 2034. The market has shifted from small, regionally fragmented supply toward organized manufacturing supported by air atomization and ball-milling technologies serving pyrotechnics, paints, construction, and chemical applications.

Aluminium ingots lead the raw material segment at 62.0% in 2025, owing to their high purity, consistent quality, and widespread availability for producing aluminium powder through atomization and other manufacturing processes. Pyrotechnics industry remains the largest end use category at 55.0%, supported by strong demand for fireworks, explosives, and other pyrotechnic formulations. West India commands 34.5% of regional share through established powder manufacturing clusters.

Key Market Insights

|

Insight |

Data |

|

Leading Raw Material |

Aluminium Ingots - 62.0% share (2025) |

|

Second Largest Raw Material |

Aluminium Scrap - 38.0% share (2025) |

|

Leading End Use |

Pyrotechnics Industry - 55.0% share (2025) |

|

Second Largest End Use |

Paints and Coatings - 18.0% share (2025) |

|

Leading Region |

West India - 34.5% share (2025) |

|

Second Largest Region |

North India - 27.8% share (2025) |

|

Top Companies |

MMP Industries Limited., MEPCO, Sri Kaliswari Metal Powders Pvt. Ltd., Deva Metal Powders Pvt. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Aluminium ingots dominance at 62.0% is supported by consistent primary aluminium supply from domestic smelters, ensuring stable feedstock availability for atomization-based powder manufacturing across the country.

- Aluminium scrap utilization at 38.0% is expanding as secondary aluminium becomes a cost-efficient feedstock for powder producers.

- Pyrotechnics industry leadership at 55.0% is anchored by strong demand for aluminium powder in fireworks, explosives, and other pyrotechnic formulations, supported by its high energy output and consistent combustion characteristics.

- Paints and coatings share at 18.0% is supported by rising use of leafing and non-leafing aluminium pastes as metallic pigments in automotive and industrial coating formulations.

- West India at 34.5% dominates regional share, anchored by established powder manufacturing clusters in Maharashtra and Gujarat and proximity to primary aluminium smelting and ingot supply.

Indian Aluminium Powder Market Overview

Aluminium powder refers to finely divided aluminium metal produced primarily through air atomization, or through stamping and milling of aluminium ingots and scrap, resulting in atomized, flake, or pyrotechnic grades used across explosives, pigments, and construction chemicals. The market spans industrial, technical, and pyrotechnic grades tailored to specific industrial applications.

The Indian ecosystem integrates primary aluminium producers, scrap recyclers, powder and paste manufacturers, and downstream industries including pyrotechnics, paints and coatings, construction, and chemicals, supported by distributors and regulators overseeing explosive-grade material handling.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

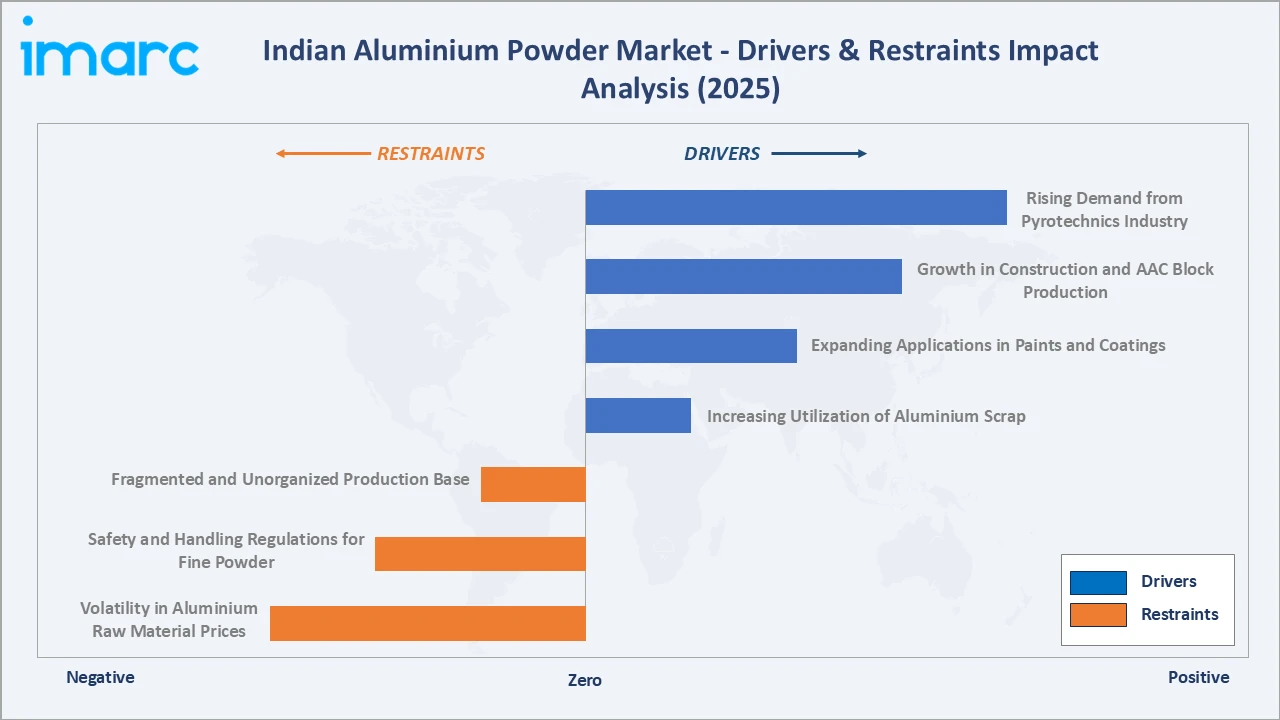

- Rising Demand from Pyrotechnics Industry: India's concentrated fireworks manufacturing base in Sivakasi and Melamathur continues to generate consistent bulk demand for pyrotechnic-grade flake aluminium powder, supporting steady offtake for regional producers.

- Growth in Construction and AAC Block Production: Rising infrastructure spending is expanding demand for aluminium powder as an expansion agent in AAC blocks. The Union Government allocated INR 11,11,111 Crore (3.4% of GDP) toward FY2024-25 capital expenditure, supporting construction-linked aluminium powder demand.

- Expanding Applications in Paints and Coatings: Rising use of leafing and non-leafing aluminium pastes as metallic pigments in automotive and industrial coatings is broadening the addressable market beyond traditional explosive and pyrotechnic applications.

- Increasing Utilization of Aluminium Scrap: Growing availability of secondary aluminium and rising cost-efficiency of scrap-based feedstock are supporting capacity additions among powder manufacturers focused on non-pyrotechnic grades.

Market Restraints

- Volatility in Aluminium Raw Material Prices: Fluctuations in aluminium prices driven by global supply and demand dynamics increase raw material costs and put pressure on the profit margins of aluminium powder manufacturers, particularly small and medium-sized producers.

- Safety and Handling Regulations for Fine Powder: Aluminium powder requires strict handling, storage, and transportation practices due to its flammable nature, increasing compliance requirements and operational costs for manufacturers.

- Fragmented and Unorganized Production Base: A large share of domestic capacity is concentrated among small and medium enterprises with limited technology upgradation, constraining consistent quality standards across the industry.

Market Opportunities

- Export Potential in Pyrotechnic-Grade Powder: Growing global demand for fireworks and rising competitiveness of Indian manufacturers present opportunities to expand pyrotechnic powder exports alongside finished firecracker shipments.

- Growth in Green and Aerated Construction Materials: Rising adoption of AAC blocks as a lightweight, energy-efficient construction material is expanding demand for construction-grade aluminium powder used as a foaming agent.

Market Challenges

- Import Competition from Low-Cost Ingots: Rising imports of cheaper aluminium alloyed ingots increase feedstock competition for domestic powder manufacturers reliant on locally sourced primary metal.

- Energy-Intensive Production Process: Atomization and milling processes are energy-intensive, and rising industrial power costs continue to weigh on production economics for smaller manufacturers.

Emerging Market Trends

1. Rising Adoption of Air Atomization Technology

Manufacturers are increasingly shifting from traditional stamp-milling processes to air atomization technology, which offers finer particle control and improved yield consistency across atomized aluminium powder grades used in coatings and specialty applications.

2. Shift Toward Recycled Aluminium Scrap Feedstock

Producers are increasingly incorporating aluminium scrap as a cost-efficient feedstock alternative to primary ingots. India's secondary aluminium capacity stood at around 2.2 Million Tons in FY2025-26, supporting greater availability of recycled feedstock for aluminium powder production and reducing dependence on primary metal.

3. Growth of Construction-Grade Powder for AAC Blocks

Expanding use of AAC in residential and commercial construction is driving demand for fine, uniformly sized aluminium powder used as a foaming and expansion agent in block manufacturing.

4. Expansion of Export-Oriented Pyrotechnic Powder Capacity

Producers around Sivakasi are expanding capacity to serve both domestic fireworks demand and growing export opportunities, as Tamil Nadu's fireworks industry pursues greater international market participation.

Industry Value Chain Analysis

The Indian aluminium powder value chain spans six stages, from raw material supply through end-use consumption. Powder manufacturing and processing capture the highest value-add, while sourcing and distribution increasingly determine cost competitiveness.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Primary aluminium smelters, ingot suppliers, and aluminium scrap recyclers and traders |

|

Smelting & Ingot Production |

Integrated aluminium producers and secondary smelters supplying ingots to powder manufacturers |

|

Powder Manufacturing |

Atomized and flake aluminium powder producers using air atomization, stamping, and ball-milling processes |

|

Processing & Grading |

Powder classification, sieving, and quality-grading facilities producing application-specific grades |

|

Distribution & Warehousing |

Regional distributors, stockists, and sales depots supplying industrial and regional customers |

|

End-Use Industries |

Pyrotechnics manufacturers, paints and coatings companies, construction material producers, and chemical industries |

Vertically integrated players with in-house atomization technology and direct access to primary aluminium feedstock are positioned to capture greater value than smaller producers reliant on third-party ingot supply.

Technology Landscape in the Indian Aluminium Powder Industry

Air Atomization and Particle Engineering

Modern producers are deploying air atomization systems that offer finer control over particle size, enabling consistent quality across atomized grades used in coatings, pigments, and specialty applications.

Materials Innovation in Pastes and Pigments

Continued innovation in leafing and non-leafing paste formulations is improving metallic finish, corrosion resistance, and compatibility with water- and solvent-based coating systems for automotive customers.

Process Automation and Quality Control

Manufacturers are gradually adopting automated milling, sieving, and packaging systems alongside in-house quality labs to meet defense, export, and industrial specification standards consistently.

Safety and Emission Control Technology

Given the flammable nature of fine aluminium powder, producers are investing in dust-control, inert atmosphere handling, and explosion-prevention systems to comply with explosives-handling regulations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End Use |

Pyrotechnics Industry |

55.0% |

2025 |

|

Technology |

Air Atomization |

64.0% |

2025 |

|

Raw Material |

Aluminium Ingots |

62.0% |

2025 |

|

Furnace Type |

Oil-Fired Furnace |

36.0% |

2025 |

|

Region |

West India |

34.5% |

2025 |

By Raw Material

Aluminium ingots command a 62.0% majority share in 2025, driven by consistent primary aluminium availability and the need for high-purity feedstock in pyrotechnic and pigment-grade powder production. The segment benefits from established supply relationships with domestic smelters and reliable input quality.

To access detailed market analysis, Request Sample

Aluminium scrap accounts for 38.0% share in 2025, driven by its cost efficiency, improving availability, and increasing adoption as a sustainable feedstock for aluminium powder production.

By End Use

Pyrotechnics industry leads the end use segment with 55.0% share in 2025, reflecting concentrated demand from Sivakasi's firecracker manufacturing cluster, which accounts for the large majority of India's fireworks production.

Paints and coatings represent 18.0% share, supported by the growing use of aluminium powder as a metallic pigment to enhance the appearance, durability, and protective properties of industrial and automotive coatings.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

34.5% |

Established powder manufacturing clusters, proximity to primary aluminium smelting capacity, and strong industrial and construction demand |

|

North India |

27.8% |

Growing construction activity, expanding industrial base, and rising demand from paints and coatings manufacturers |

|

South India |

23.6% |

Concentrated pyrotechnics manufacturing cluster in Tamil Nadu, rising industrial diversification, and expanding export-oriented production |

|

East India |

14.1% |

Emerging industrial development, growing construction sector, and gradual expansion of regional distribution networks |

West India at 34.5% in 2025 leads the regional landscape, anchored by established powder and paste manufacturing clusters in Maharashtra and Gujarat. Proximity to primary aluminium smelting capacity supports sustained leadership across pyrotechnic and industrial powder grades.

South India at 23.6% is the fastest-growing region, anchored by Tamil Nadu's dense cluster of pyrotechnic aluminium powder producers around Sivakasi and Melamathur. Rising export orientation and continued expansion of fireworks manufacturing capacity are accelerating regional growth through 2034.

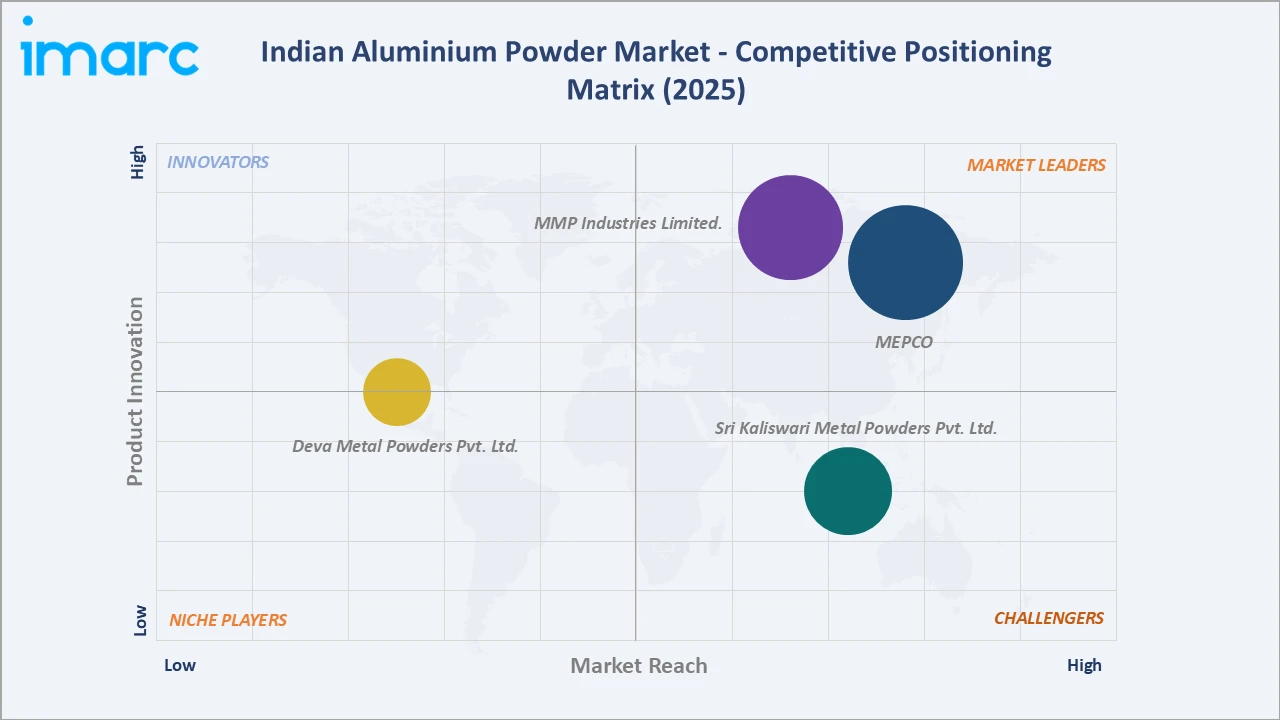

Competitive Landscape

The Indian aluminium powder market is moderately fragmented, with established manufacturers concentrated around Nagpur, Sivakasi, and other regional industrial clusters competing alongside smaller regional producers. Production technology, feedstock access, and application-specific quality certifications form the key competitive differentiators across the industry.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

MMP Industries Limited. |

MMP Aluminium Powder |

Leader |

Diversified powder and paste portfolio supported by technical collaborations |

|

MEPCO |

MEPCO Aluminium Powder & Pastes |

Leader |

Export-oriented growth and R&D-led product innovation |

|

Sri Kaliswari Metal Powders Pvt. Ltd. |

Air Atomized Aluminium Powders |

Challenger |

Regional focus on pyrotechnic and construction-grade powder |

|

Deva Metal Powders Pvt. Ltd. |

Deva Atomized and Flake Aluminium Powder |

Emerging |

Technology-led production supported by consultancy services |

Key players include MMP Industries Limited., MEPCO, Sri Kaliswari Metal Powders Pvt. Ltd., and Deva Metal Powders Pvt. Ltd., among others.

Key Company Profiles

MMP Industries Limited.

MMP Industries Limited. is a Nagpur-headquartered manufacturer of aluminium powders, pastes, foils, and conductors, with a multi-decade manufacturing history and a diversified presence across central India.

- Product Portfolio: Aluminium powders and pastes, along with aluminium foils and conductors serving construction, defense, coatings, and industrial applications.

- Recent Developments: MMP Industries Limited. has expanded its aluminium powder and paste production capabilities while strengthening its product portfolio to serve growing demand from coatings, defense, construction, and industrial applications.

- Strategic Focus: Broadening its reach across the powder and paste business by drawing on established technical partnerships.

MEPCO

MEPCO is a long-established Indian manufacturer of non-ferrous metal powders and pastes, with a multi-decade presence in the aluminium powder industry and a broad domestic and export footprint.

- Product Portfolio: Aluminium powders and pastes, along with a wider range of non-ferrous metal powders serving industrial, coatings, and pyrotechnic applications.

- Recent Developments: The company continues to invest in product development and manufacturing capacity to support its export-oriented operations.

- Strategic Focus: Pursuing international market expansion underpinned by continuous research and product development.

Sri Kaliswari Metal Powders Pvt. Ltd.

Sri Kaliswari Metal Powders Pvt. Ltd. is a Tamil Nadu-based manufacturer of aluminium powders serving India's pyrotechnics and construction industries.

- Product Portfolio: Air atomized aluminium powders, along with pyrotechnic and construction-grade powder products.

- Recent Developments: The company continues to align its manufacturing operations with regional demand across the pyrotechnics and construction sectors.

- Strategic Focus: Concentrating on serving the pyrotechnics and construction sectors within its home region.

Market Concentration Analysis

The Indian aluminium powder market is moderately fragmented, with leading manufacturers such as MMP Industries Limited. and MEPCO accounting for a meaningful share of organized production, while numerous small and medium enterprises serve regional and application-specific demand.

Barriers to entry include the need for specialized atomization technology, consistent feedstock access, and compliance with explosives-handling and safety regulations, which favor established players with integrated supply relationships and diversified product portfolios.

Consolidation is gradual, with larger manufacturers expanding capacity and forward-integrating into paste and pigment production, while smaller regional producers continue serving localized pyrotechnic and construction-grade demand.

Investment & Growth Opportunities

Fastest-Growing Segments

Paints and coatings are forecast to grow the fastest among end use segments, driven by rising automotive coatings demand and increasing use of aluminium pigment pastes. Construction materials follow closely, supported by expanding AAC block manufacturing.

Emerging Markets

South India is the fastest-growing region, anchored by Tamil Nadu's dense pyrotechnic powder manufacturing cluster and rising export-oriented capacity. The region represents meaningful opportunity for producers able to expand application-specific and export-grade powder offerings.

Venture & Investment Trends

Investment is concentrated in air atomization capacity expansion, scrap-processing infrastructure, and paste and pigment production lines that align with growing paints, coatings, and construction-grade demand beyond traditional pyrotechnic applications.

Future Market Outlook (2026-2034)

The Indian aluminium powder market is forecast to expand from 48.66 Thousand Tons in 2025 to 74.58 Thousand Tons by 2034 at a CAGR of 4.86%, adding roughly 25.92 Thousand Tons in incremental volume over the forecast period.

Three forces will shape the market through 2034: rising infrastructure-linked demand for aerated concrete applications, growing adoption of aluminium scrap as a cost-efficient feedstock, and continued expansion of pyrotechnic-grade powder capacity supporting Sivakasi's fireworks manufacturing base.

By 2034, the market is expected to be defined by a more diversified end use base, with paints and coatings and construction materials accounting for a higher share of demand alongside sustained pyrotechnics consumption, supported by expanding scrap-processing infrastructure and technology upgradation.

Research Methodology

Primary Research

Primary research included structured interactions with aluminium powder manufacturers, raw material suppliers, and industry associations, validating market sizing, segment shares, and regional demand patterns across raw material and end use categories.

Secondary Research

Secondary sources included Ministry of Mines publications, Ministry of Finance budget documents, industry association data, and company disclosures from listed and unlisted aluminium powder and primary aluminium producers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining historical volume trends, end-use industry growth rates, feedstock availability, and regional industrial activity. Scenario analysis addressed feedstock price volatility and regulatory considerations affecting explosive-grade material handling.

Indian Aluminium Powder Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Tons, '000 USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| End-Uses Covered | Pyrotechnics Industry |

| Technologies Covered | Air Atomization |

| Raw Materials Covered | Aluminum Ingots, Aluminum Scrap |

| Furnace Types Covered | Oil-Fired Furnace, Gas-Fired Furnace, Electric Furnace |

| Region Covered | North India, South India, East India, West India |

| Companies Covered | MMP Industries Limited., MEPCO, Sri Kaliswari Metal Powders Pvt. Ltd., Deva Metal Powders Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Aluminium Powder Market Report

The Indian aluminium powder market reached a volume of 48.66 Thousand Tons in 2025, driven by demand from the pyrotechnics, paints and coatings, and construction industries.

The market is projected to grow at a CAGR of 4.86% from 2026-2034, reaching 74.58 Thousand Tons, supported by rising construction and coatings demand.

Aluminium ingots lead at 62.0% share in 2025, driven by consistent primary aluminium supply, ensuring reliable feedstock availability and uniform powder quality for industrial applications.

Pyrotechnics industry dominates at 55.0% share in 2025, anchored by Sivakasi's concentrated fireworks manufacturing base in Tamil Nadu.

West India commands 34.5% share in 2025, led by established powder manufacturing clusters in Maharashtra and Gujarat.

South India, with 23.6% share in 2025, is the fastest-growing region, supported by Tamil Nadu's dense pyrotechnic powder manufacturing cluster.

Leading players include MMP Industries Limited., MEPCO, Sri Kaliswari Metal Powders Pvt. Ltd., and Deva Metal Powders Pvt. Ltd., among others.

The market is expected to grow steadily through 2034, supported by diversifying end use demand across construction, coatings, and pyrotechnics, alongside expanding scrap-based feedstock utilization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)