Indian Feed Additives Market Size, Share, Trends and Forecast by Source, Product Type, Livestock, Form, and Region, 2026-2034

Indian Feed Additives Market Size, Share, Trends & Forecast (2026-2034)

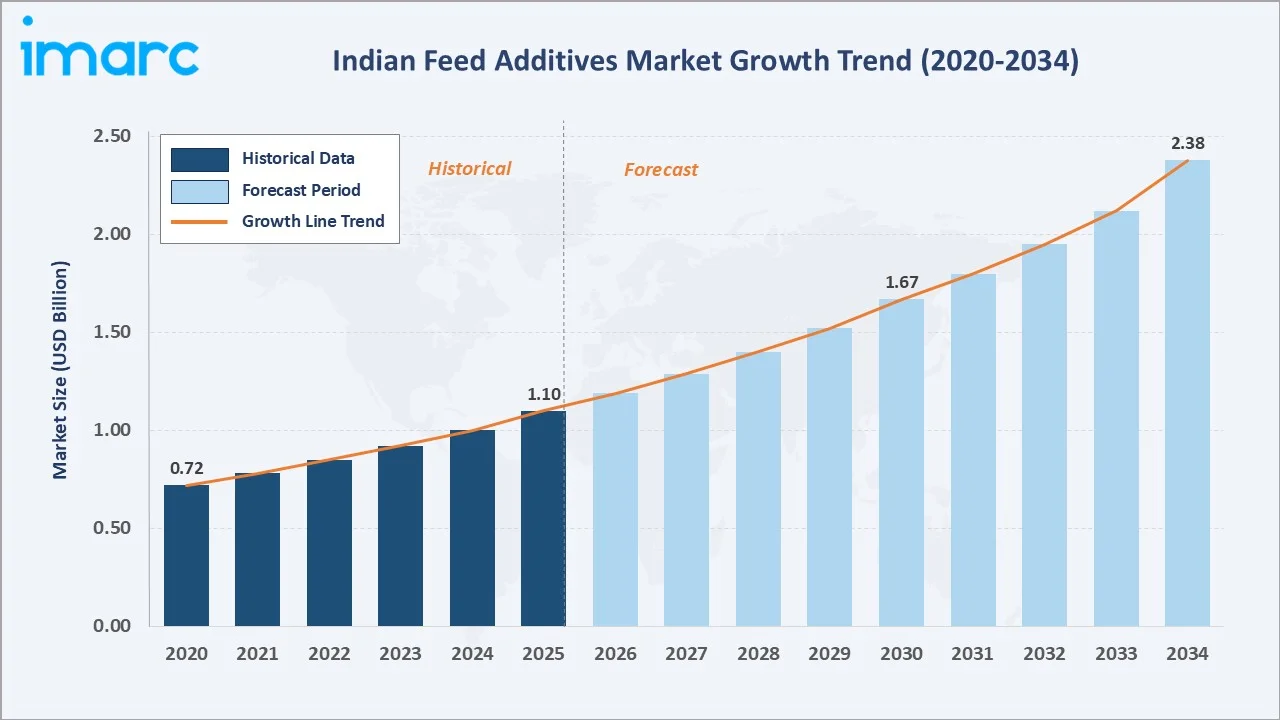

The Indian feed additives market reached USD 1.10 Billion in 2025 and is projected to reach USD 2.38 Billion by 2034, growing at a CAGR of 8.68% during 2026-2034. Growing awareness about animal nutrition, emerging technological advancements in feed additive formulations, the rising adoption of modern animal husbandry practices, and the implementation of favorable government initiatives to support livestock development are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.10 Billion |

|

Forecast Market Size (2034) |

USD 2.38 Billion |

|

CAGR (2026-2034) |

8.68% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

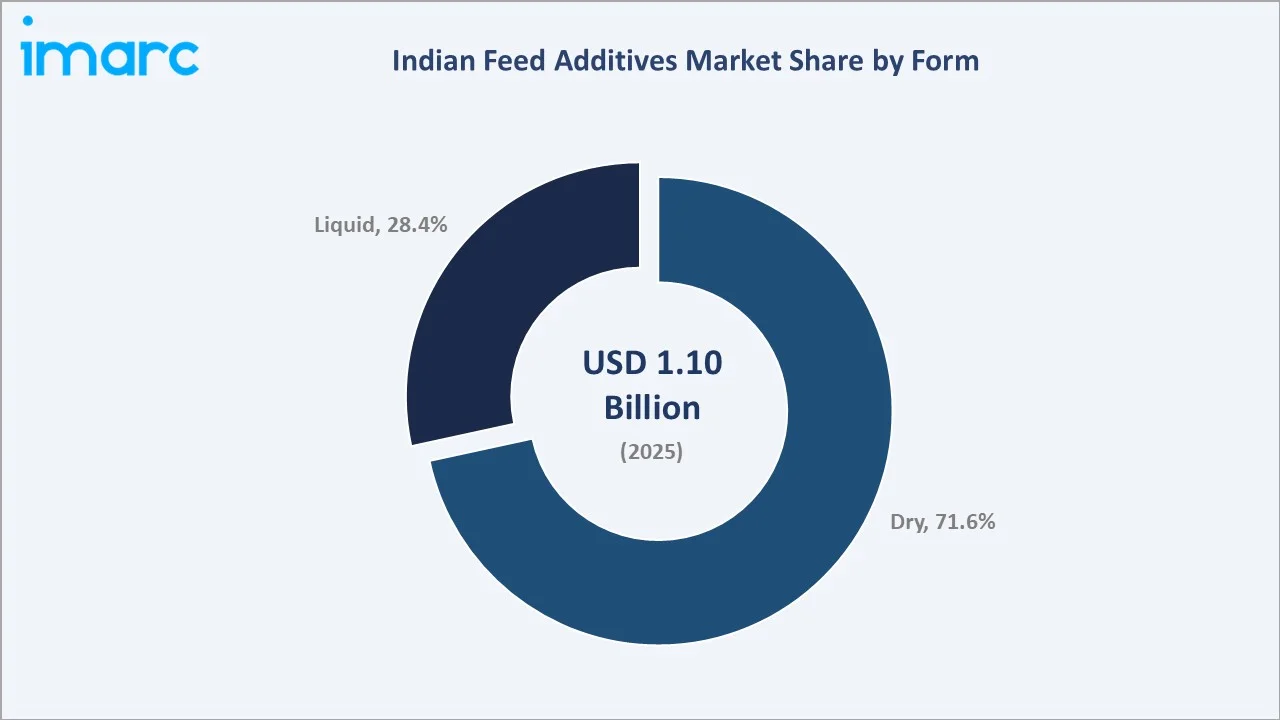

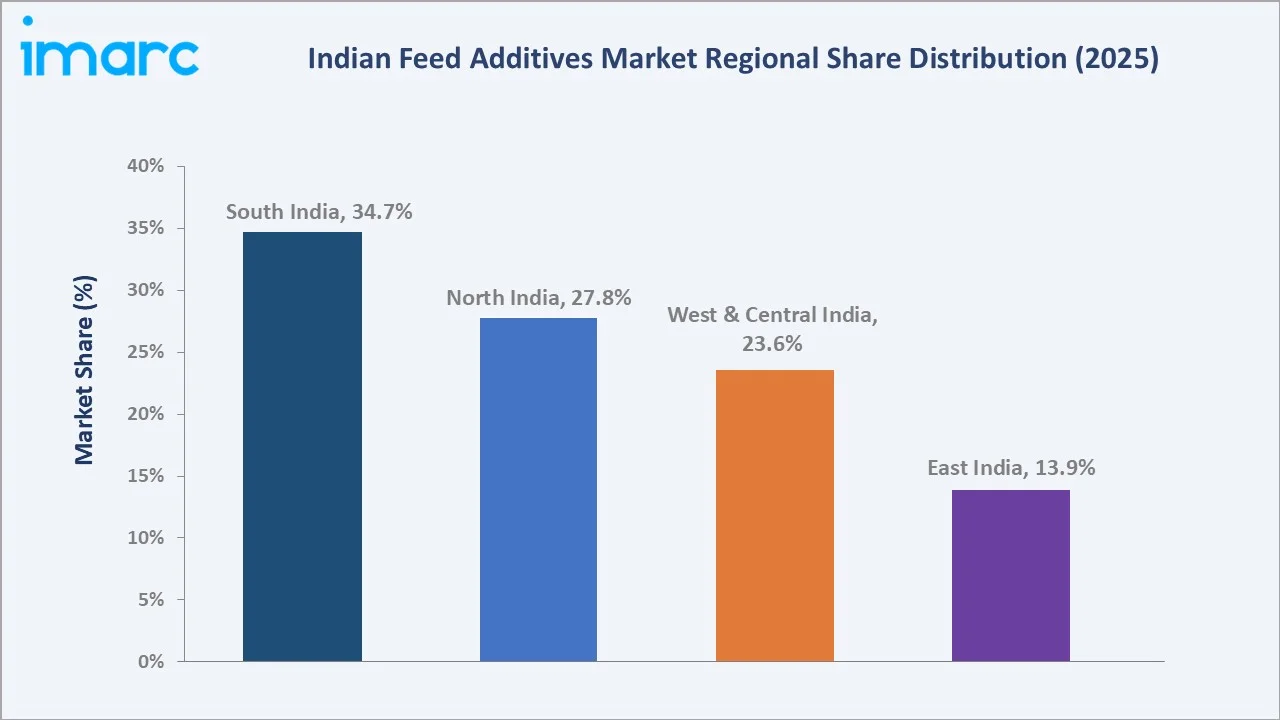

South India leads regionally, holding a 34.7% market share in 2025, underpinned by the region’s large and expanding poultry sector, particularly in Andhra Pradesh and Telangana. Dry-form feed additives command the dominant 71.6% share, reflecting the ease of handling, blending, and storage that powdered and granular formats offer for large-scale commercial feed mill operations.

To get more information on this market, Request Sample

India’s feed additives market is underpinned by three structural forces: rising per-capita animal protein consumption, the government’s livestock development programs, and technological advancements in additive formulations including probiotics, enzymes, and microencapsulation. Each force independently drives adoption across multiple additive categories, collectively sustaining near double-digit CAGR through 2034.

Executive Summary

The Indian feed additives market is experiencing robust, broad-based expansion driven by the convergence of rising animal protein demand, industrialization of livestock farming, and government-backed initiatives. The market was valued at USD 1.10 Billion in 2025 and is forecast to reach USD 2.38 Billion by 2034, growing at a CAGR of 8.68%. This trajectory is anchored by India’s rapidly expanding poultry, dairy, and aquaculture sectors, which collectively drive over 75% of feed additive demand.

Dry-form additives dominate with a 71.6% share in 2025, while synthetic sources account for 58.6%. South India leads regionally at 34.7%, driven by its large poultry belt. Key global and domestic players, including Cargill, Incorporated, Evonik Industries AG, BASF, dsm-firmenich, Kemin Industries, Inc., collectively shape the market’s competitive landscape through continuous innovation and strategic manufacturing partnerships.

Key Market Insights

|

Insight |

Data |

|

Largest Form Segment |

Dry – 71.6% share (2025) |

|

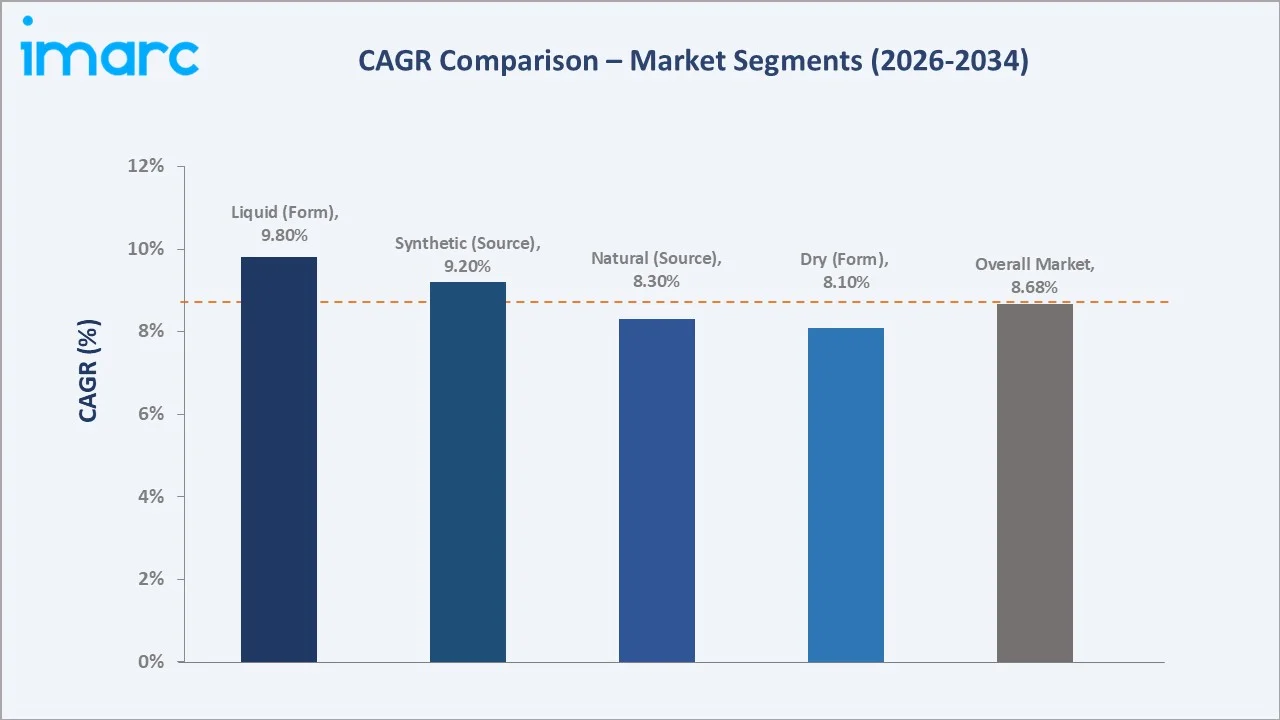

Fastest Growing Form Segment |

Liquid – ~9.8% CAGR (2026-2034) |

|

Largest Source Segment |

Synthetic – 58.6% share (2025) |

|

Fastest Growing Source Segment |

Synthetic – ~9.2% CAGR (2026-2034) |

|

Leading Region |

South India – 34.7% share (2025) |

|

Top Companies |

Cargill, Incorporated, Evonik Industries AG, BASF, dsm-firmenich, Kemin Industries, Inc. |

Key Analytical Observations Supporting the Above Data:

- Dry-form additives’ 71.6% share (2025) reflects their operational advantages in large-scale feed mill production: consistent particle size distribution, superior shelf stability, and compatibility with high-capacity pelleting and extrusion systems.

- Synthetic source at 58.6% (2025) remains dominant due to the superior consistency, predictable bioavailability, and cost-competitiveness of chemically synthesized vitamins, amino acids, and trace minerals relative to natural alternatives, particularly for high-volume poultry and swine feed production.

- South India led with a 34.7% share (2025), as Andhra Pradesh leads in total egg production, accounting for 18.37% of the national output, followed by Tamil Nadu with 15.63% and Telangana with 12.98%.

- Liquid-form additives’ fastest-growth trajectory (~9.8% CAGR) is driven by increasing aquaculture feed formulation needs, the rising use of liquid acidifiers and enzyme cocktails in broiler and dairy rations, and the growing preference for precision dosing systems in large-scale integrated farming operations.

Indian Feed Additives Market Overview

Feed additives are substances incorporated into animal diets to improve health, growth, and performance. These additives include vitamins, minerals, amino acids, probiotics, prebiotics, enzymes, acidifiers, antioxidants, and growth promoters. They complement the nutritional content of animal feed, address specific deficiencies, and enhance physiological functions. In India, the feed additives market encompasses both synthetic and natural origin additives supplied in dry and liquid forms to poultry, ruminant, swine, aquaculture, and pet animal sectors.

Macroeconomic drivers include India’s per capita annual consumption of poultry meat of about 3.4 kg, government capital expenditure through the National Livestock Mission (NLM), and the Animal Husbandry Infrastructure Development Fund (AHIDF) offering INR 15,000 Crore to incentivize modern livestock infrastructure. As of December 2024, banks have approved 363 projects under the AHIDF, with animal feed manufacturing capacity reaching approximately 84.52 lakh MTPA across 128 projects. This creates a large and growing base market for feed additives.

Market Dynamics

To evaluate market opportunities, Request Sample

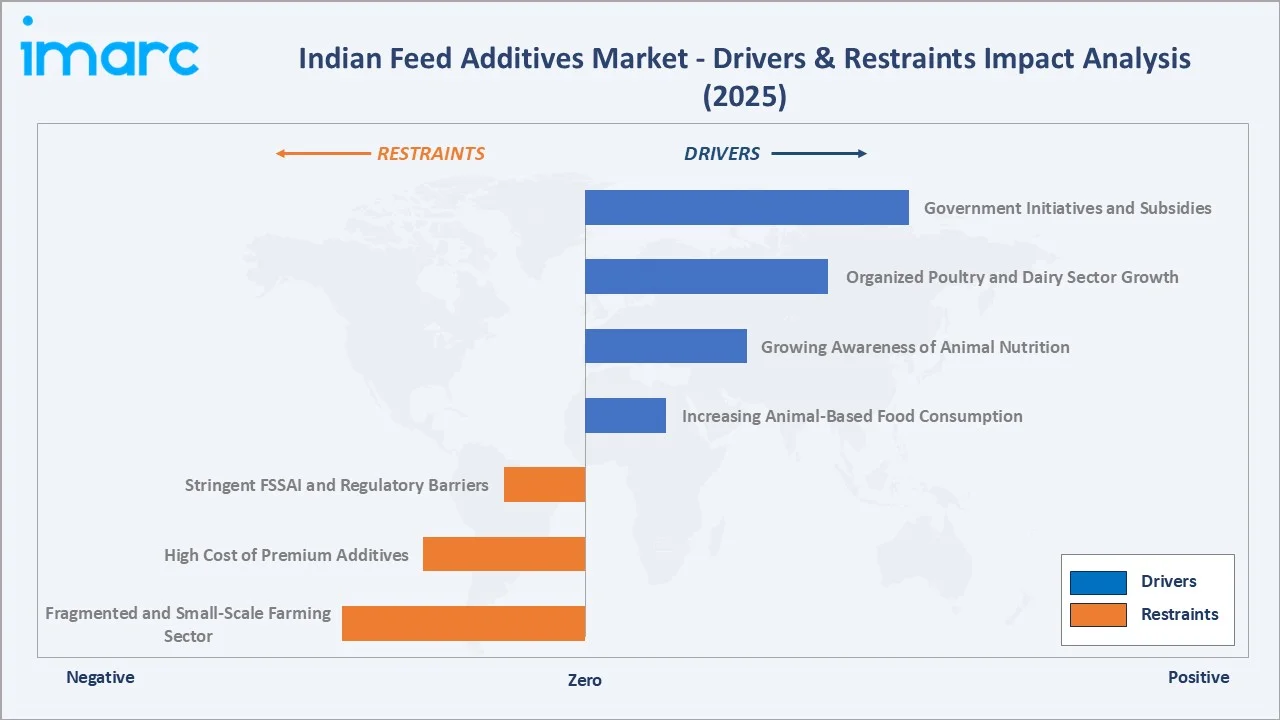

Market Drivers

- Increasing Animal-Based Food Consumption: Per capita egg availability has increased from 79 to 106 eggs annually, reflecting a 34% rise in individual consumption from 2018-19 to 2024-25. As per the Basic Animal Husbandry Statistics 2024, milk production amounted to 239.30 million tons in FY 2024–25.

- Growing Awareness of Animal Nutrition: Indian farmers and livestock producers increasingly understand the link between feed quality, animal health, and productivity. Krishi Vigyan Kendra (KVK) extension services, veterinary outreach programs, and digital agri-platforms are accelerating the adoption of precision nutrition practices.

- Organized Poultry and Dairy Sector Growth: India’s organized poultry sector, comprising vertically integrated broiler integrators such as Suguna Foods, Venkateshwara Hatcheries, and Srinivasa Farms, accounts for approximately 50–55% of poultry output and drives disproportionately high feed additive adoption.

- Government Initiatives and Subsidies: The National Livestock Mission (NLM), Animal Husbandry Infrastructure Development Fund (AHIDF), and PM Matsya Sampada Yojana (PMMSY) collectively provide subsidies and credit guarantees to livestock and aquaculture producers, enabling investments in modern feed formulation and higher-quality additive inputs that improve productivity.

Market Restraints

- Fragmented and Small-Scale Farming Sector: Marginal, small, and semi-medium farmers, with average operational holdings of less than 4 hectares, own approximately 87.7% of the livestock in India. These farmers lack the financial capacity and technical knowledge to adopt sophisticated feed additive programs, limiting total addressable market penetration relative to the size of India’s livestock population.

- High Cost of Premium Additives: Specialty additives, including protected amino acids, encapsulated butyrates, phytogenics, and multi-strain probiotic complexes, command significant price premiums over commodity supplements. Price sensitivity among Indian feed manufacturers constrains rapid adoption of higher-value additive categories despite demonstrated productivity benefits.

- Stringent FSSAI and Regulatory Barriers: The FSSAI’s Food Safety and Standards (Animal Feed and Feed Additives) Regulations 2022 require comprehensive safety dossiers, clinical data, and local manufacturing registration for new additive approvals. Multi-year regulatory timelines increase the cost and complexity of introducing novel additive products into the Indian market.

Market Opportunities

- Aquaculture Feed Additive Expansion: Fish production has surged by 106%, rising from 95.79 lakh tons in FY 2013-14 to 197.75 lakh tons in FY 2024-25. A total of INR 38,572 crore has been approved or announced across various schemes, including the Blue Revolution and the Fisheries and Aquaculture Infrastructure Development Fund (FIDF).

- Natural and Phytogenic Additives Growth: Consumer demand for antibiotic-free and residue-free animal products is driving the substitution of antibiotic growth promoters (AGPs) with natural alternatives, including phytogenics, essential oil blends, and botanical extracts. India’s government has progressively restricted AGP use, creating a structural opportunity for natural additive suppliers.

Market Challenges

- Cold Chain and Storage Infrastructure Gaps: Liquid feed additives and temperature-sensitive probiotic preparations require cold-chain distribution infrastructure that remains underdeveloped across India’s rural livestock hubs. Thermal degradation during transport and storage reduces product efficacy and creates liability risks, slowing adoption of liquid and biological additive categories.

- Counterfeit and Substandard Products: The feed additives market faces significant challenges from counterfeit and adulterated products, particularly in the vitamin and mineral premix segment. Substandard additives not only fail to deliver nutritional benefits but can also harm animal health, eroding trust in the broader category and creating regulatory enforcement challenges.

Emerging Market Trends

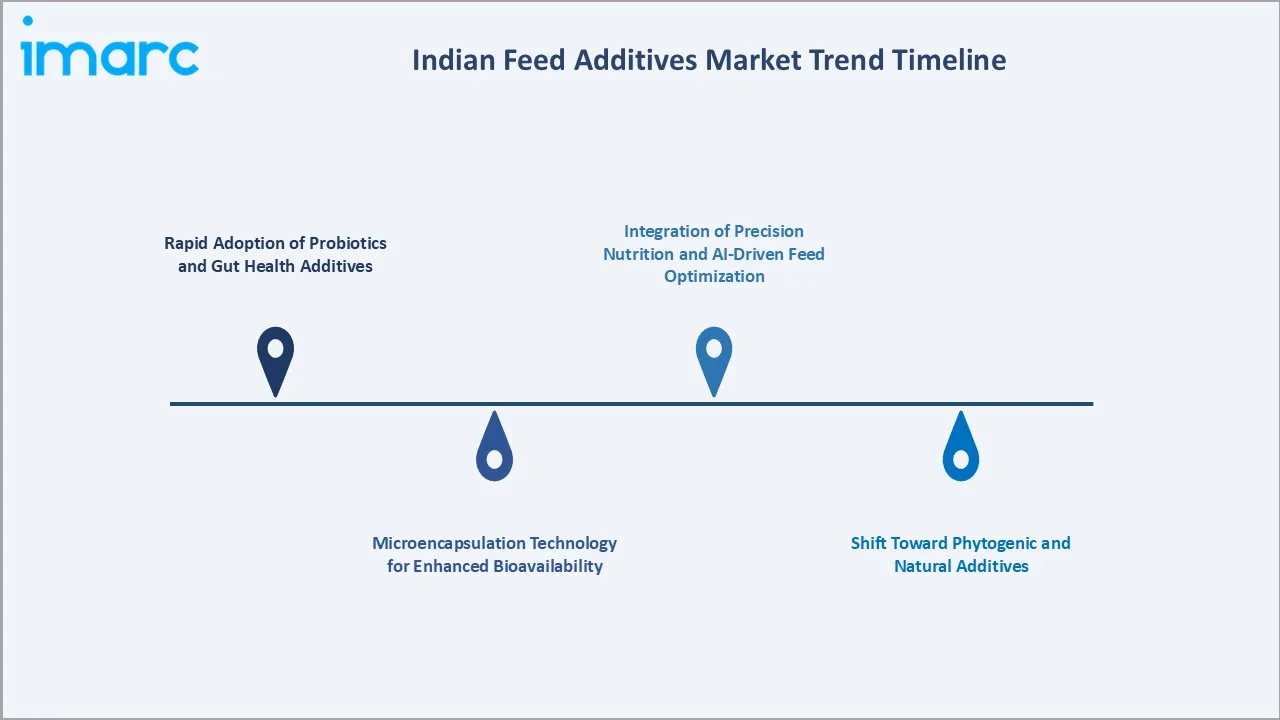

1. Rapid Adoption of Probiotics and Gut Health Additives

In response to the progressive restriction on antibiotic growth promoters, Indian poultry and aquaculture producers are rapidly adopting multi-strain probiotic, prebiotic, and synbiotic formulations. Kemin Industries’ launch of Pathorol for shrimp hepatopancreas health in 2023, available to Indian customers, exemplifies the tailoring of global probiotic technology for Indian aquaculture conditions. The gut health additives sub-segment is growing at an estimated 12–15% CAGR within the broader Indian market.

2. Microencapsulation Technology for Enhanced Bioavailability

Microencapsulation, the process of encapsulating sensitive feed additive molecules in protective matrices, is gaining rapid adoption in Indian feed mills for vitamins, amino acids, and organic acids. The technology protects additives from thermal degradation during pelleting (85–95°C) and improves targeted release in specific digestive tract segments versus unprotected forms, improving the cost-effectiveness calculation for Indian feed manufacturers.

3. Shift Toward Phytogenic and Natural Additives

India's prohibition on several antibiotic growth promoters under the Drugs and Cosmetics Act, combined with growing retailer and consumer pressure for antibiotic-free meat and dairy, is driving rapid substitution of AGPs with phytogenic additives (plant extracts, essential oils) and organic acids. The natural additives segment is projected to grow from a 41.4% share in 2025 to approximately 48–50% by 2034.

4. Integration of Precision Nutrition and AI-Driven Feed Optimization

Large integrated poultry and dairy operators in India are adopting AI-driven ration formulation platforms that dynamically adjust additive inclusion rates based on real-time animal performance data, ambient temperature, and feed raw material quality. This digital transformation elevates the strategic role of feed additive suppliers from commodity input providers to precision nutrition partners, enabling value-based pricing and long-term supply contracts.

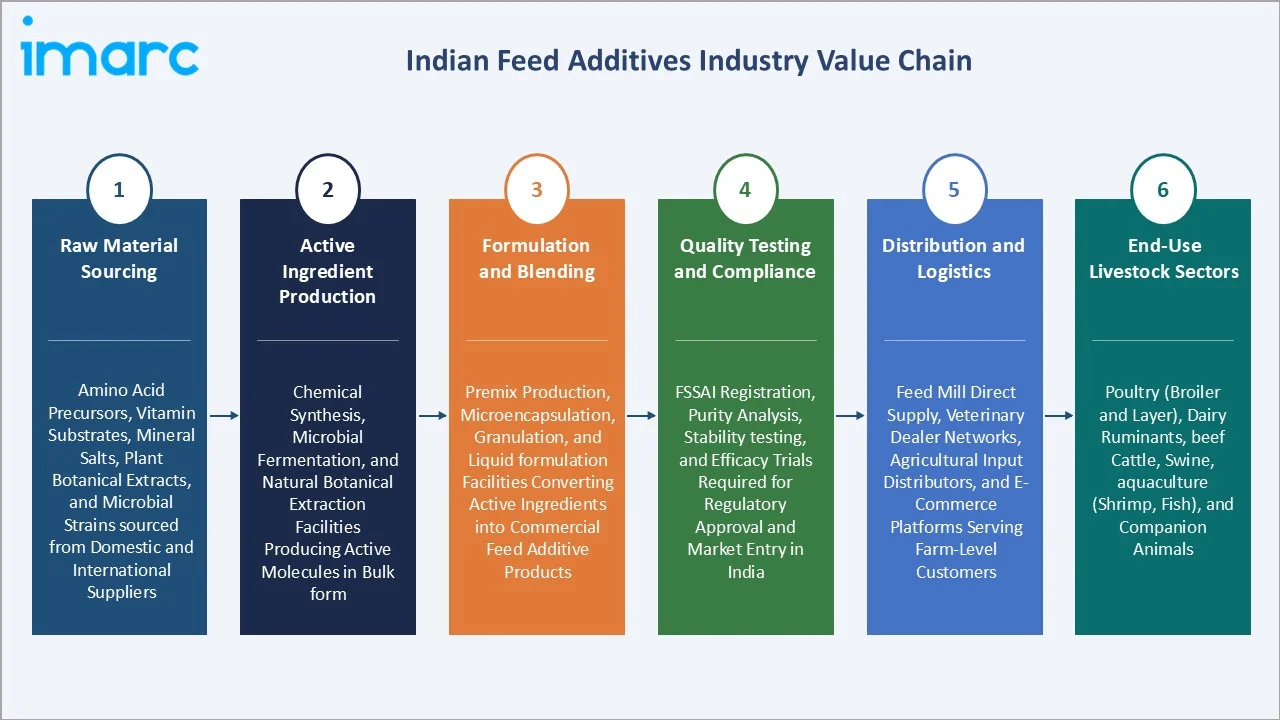

Industry Value Chain Analysis

The Indian feed additives value chain spans raw material sourcing through end-use livestock application, with each stage characterized by specific competitive dynamics and regulatory requirements.

|

Stage |

Description |

|

Raw Material Sourcing |

Amino acid precursors, vitamin substrates, mineral salts, plant botanical extracts, and microbial strains sourced from domestic and international suppliers |

|

Active Ingredient Production |

Chemical synthesis, microbial fermentation, and natural botanical extraction facilities producing active molecules in bulk form |

|

Formulation and Blending |

Premix production, microencapsulation, granulation, and liquid formulation facilities converting active ingredients into commercial feed additive products |

|

Quality Testing and Compliance |

FSSAI registration, purity analysis, stability testing, and efficacy trials required for regulatory approval and market entry in India |

|

Distribution and Logistics |

Feed mill direct supply, veterinary dealer networks, agricultural input distributors, and e-commerce platforms serving farm-level customers. |

|

End-Use Livestock Sectors |

Poultry (broiler and layer), dairy ruminants, beef cattle, swine, aquaculture (shrimp, fish), and companion animals |

Technology Landscape in the Indian Feed Additives Industry

Amino Acid Production and Delivery Technologies

Amino acids, particularly DL-methionine, L-lysine, L-threonine, and L-tryptophan, represent the largest product category in the Indian feed additives market by value. Evonik Industries’ MetAMINO (DL-methionine) and BASF’s Natugrain/Natuphos are produced through industrial fermentation and chemical synthesis processes optimized for consistent purity above 99%.

Enzyme Technology for Feed Efficiency

Multi-enzyme complexes incorporating phytases, xylanases, beta-glucanases, and proteases are widely used in Indian poultry and swine feed to improve nutrient digestibility and reduce feed cost. Phytase supplementation (releasing phosphorus from phytate-bound plant sources) reduces the need for inorganic phosphate supplementation by 60–80%, directly lowering feed formulation costs.

Probiotic and Prebiotic Formulation Platforms

Direct-fed microbial (DFM) technologies, incorporating Bacillus subtilis, Lactobacillus acidophilus, Enterococcus faecium, and Saccharomyces cerevisiae strains, are increasingly used in Indian poultry, dairy, and aquaculture feeds as antibiotic alternatives. Shelf-stable spore-forming Bacillus-based probiotics, capable of surviving feed pelleting at 85–90°C, are the fastest-growing probiotic format in the Indian market.

Natural Antioxidants and Preservation Technologies

Rosemary extract (rosmarinic acid), tocopherol blends, and mixed carotenoid antioxidant systems are increasingly replacing synthetic antioxidants (BHA, BHT) in premium poultry and aquafeed formulations, driven by consumer demand for cleaner-label animal products. Antioxidant technology ensures feed fat stability, prevents rancidity during storage, and protects vitamin A and E activity, improving overall nutrient delivery to the animal.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Form |

Dry |

71.6% |

2025 |

|

Source |

Synthetic |

58.6% |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Livestock |

🔒 |

🔒 |

2025 |

|

Region |

South India |

34.7% |

2025 |

By Form

Dry form feed additives dominate the Indian market with a 71.6% share in 2025. This segment encompasses powders, granules, pellets, and micro-granules, and covers virtually all vitamin premixes, amino acid supplements, mineral blends, and enzyme preparations. The dry format’s dominance reflects its logistical advantages, ambient temperature storage, longer shelf life, and compatibility with automated feed mill mixing and pelleting equipment.

To access detailed market analysis, Request Sample

Liquid form additives, at 28.4%, are the fastest-growing form segment, driven by the growing use of liquid acidifiers (formic acid, propionic acid blends), liquid enzymes for aquafeed, and liquid probiotic cultures for intensive poultry operations. Liquid formats offer superior homogeneity and can be applied post-pelleting via liquid coating systems, making them particularly attractive for heat-sensitive additives.

By Source

Synthetic source additives account for 58.6% of the Indian feed additives market in 2025. Synthetic production guarantees high purity, consistent potency, and predictable bioavailability, making synthetic vitamins, mineral chelates, and chemically synthesized amino acids the preferred choice for formulating balanced, commercially specified feed rations.

Natural-source additives, at 41.4%, encompass plant-derived vitamins (vitamin E from soya, vitamin C from acerola), fermentation-derived amino acids, botanical phytogenics, and bio-fermented probiotics. The natural segment is the fastest-growing from a source perspective, driven by the progressive restriction of antibiotic growth promoters and growing consumer demand for antibiotic-free meat and dairy.

Regional Market Insights

South India’s market leadership (34.7%, 2025) is firmly anchored by Andhra Pradesh and Telangana’s dominant position in India’s broiler poultry industry. These two states account for approximately 45% of India’s broiler production, creating the country’s highest concentration of large-scale integrated feed mill and poultry farm operations that are the primary consumers of scientifically formulated feed additives.

The industry is witnessing increasing investments in product innovations, especially in areas like probiotics, enzymes, and organic acids, to meet the growing demand for high-quality feed additives in the livestock and poultry sectors.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

34.7% |

Dominant broiler poultry belt in Andhra Pradesh and Telangana, large-scale feed mill concentration, growing aquaculture sector in coastal states, and high adoption of scientifically formulated premix programs |

|

North India |

27.8% |

Large dairy ruminant population in Uttar Pradesh, Punjab, and Haryana, significant poultry sector in Haryana, and growing demand for mineral and vitamin supplements for cattle and buffalo herds |

|

West & Central India |

23.6% |

Significant dairy cattle and buffalo population in Maharashtra, Gujarat, and Madhya Pradesh, organized poultry farms in Maharashtra, and expanding aquaculture in Gujarat coastal districts |

|

East India |

13.9% |

Growing poultry and aquaculture sectors in West Bengal and Odisha, rising freshwater fish aquaculture in Bihar and Jharkhand, and increasing government extension support for modern livestock feeding practices |

North India at 27.8% is driven by its large dairy ruminant population; Uttar Pradesh has the largest livestock population in India, with 68 million animals. The rising adoption of balanced mineral-vitamin supplementation and rumen bypass nutrients among progressive dairy farmers in the Indo-Gangetic Plain represents a high-growth opportunity for specialty ruminant additive suppliers.

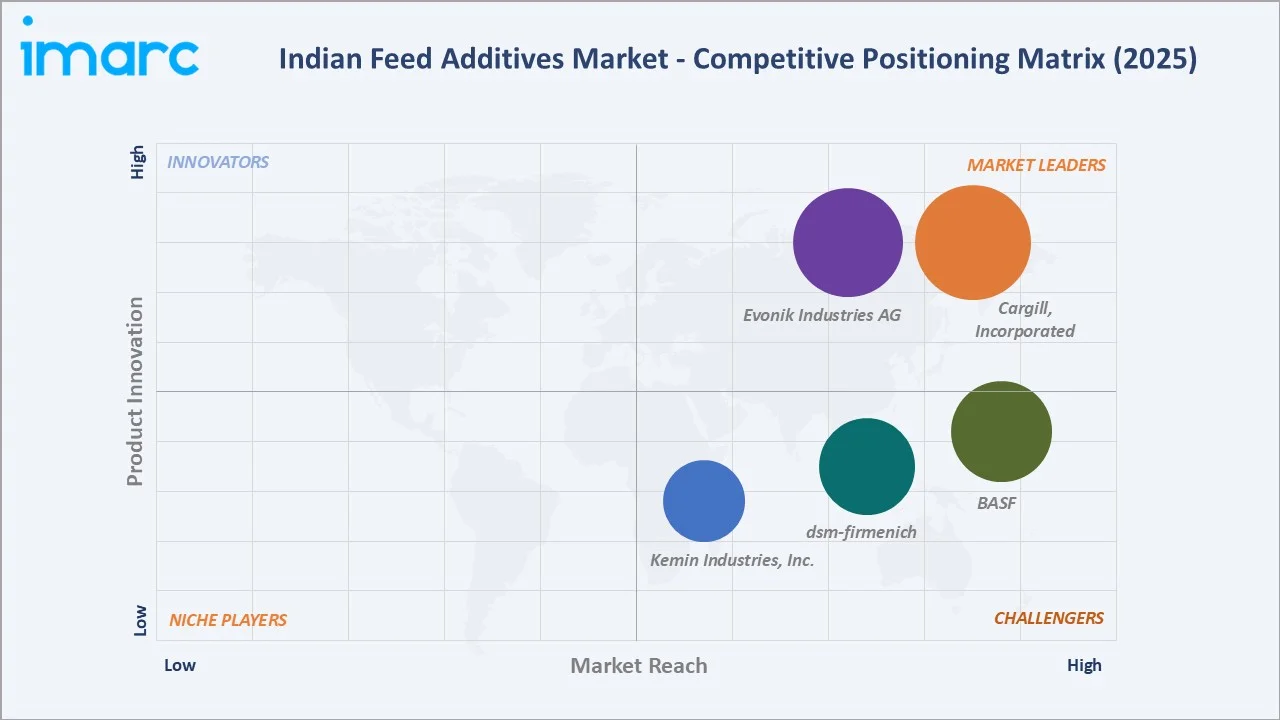

Competitive Landscape

India’s feed additives market exhibits moderate fragmentation, with global majors dominating the premium amino acid and enzyme segments while a growing domestic industry serves mid-market vitamin-mineral premix and natural additive categories.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Cargill, Incorporated |

Purina, EWOS, Provimi |

Market Leader |

Integrated animal nutrition; broad premix, amino acid, and mycotoxin binder portfolio; strong Indian distribution network |

|

Evonik Industries AG |

MetAMINO, Mepron, Ecobiol |

Market Leader |

Global leader in DL-methionine and essential amino acids; precision nutrition expertise; manufacturing in 100+ countries |

|

BASF |

Natugrain TS, Natuphos E, Lutavit, Lucantin, Lucarotin |

Strong Challenger |

Comprehensive vitamin and carotenoid portfolio; microencapsulated forms; Luprosil expansion |

|

dsm-firmenich |

RONOZYME, ROVIMIX, CAROPHYLL, CYLACTIN, CRINA, and Hy-D, among others

|

Strong Challenger |

Broad vitamin premix, enzyme, and probiotic portfolio; OVN precision nutrition programs; sustainability focus |

|

Kemin Industries, Inc. |

CLOSTAT, LYSOFORTE EXTEND, ButiPEARL, EnerFAT PLUS, TOXFIN, Kemin AquaScience |

Challenger |

Specialty gut health additives, protected butyrates, and antimicrobial agents; India-specific product development |

Key Company Profiles

Cargill, Incorporated

Cargill, Incorporated, headquartered in Wayzata, Minnesota, USA, is one of the world’s largest privately held food and agriculture corporations. Through its animal nutrition divisions, Cargill offers a comprehensive portfolio of feed additives, premixes, and complete feed solutions for poultry, swine, ruminants, and aquaculture operations across India.

- Product Portfolio: Provimi premix programs for poultry and swine, Purina, and EWOS.

- Recent Developments: In February 2026, Cargill India opened its second dairy feed manufacturing plant in Punjab with an investment of around INR 300 crore, with an annual capacity of about 4 lakh tons.

- Strategic Focus: Integrated supply chain advantages combined with regional manufacturing investment in high-growth markets, emphasizing sustainability-linked additive solutions as major livestock producers require partners with demonstrable carbon reduction credentials.

Evonik Industries AG

Evonik Industries AG, headquartered in Essen, Germany, is a leading specialty chemicals company and the global leader in essential amino acids for animal nutrition. Evonik’s Animal Nutrition division is a major supplier to the Indian market through its methionine, lysine, threonine, and tryptophan product lines.

- Product Portfolio: MetAMINO (DL-methionine), Mepron (rumen-protected methionine for dairy), and Ecobiol.

- Recent Developments: In November 2025, Evonik showcased its updated Ecobiol probiotic at Poultry India 2025 in Hyderabad, featuring an optimized outgrowth profile that enables faster probiotic activity for poultry gut health and feed efficiency.

- Strategic Focus: Precision amino acid nutrition programs; sustainability through renewable fermentation feedstocks; digital precision nutrition advisory services to reduce total amino acid inclusion and improve FCR.

BASF

BASF, headquartered in Ludwigshafen, Germany, is the world’s largest chemical company and a significant player in the Indian feed additives market through its Animal Nutrition segment. BASF supplies vitamins, carotenoids, organic acids, and micronutrient solutions to Indian feed manufacturers and premix producers.

- Product Portfolio: Lutavit (vitamin E, A, D3 range), Lucantin (carotenoid pigments for poultry and aquaculture). Natugrain TS, Natuphos E, and Lucarotin.

- Recent Developments: In October 2025, BASF introduced Lutavit A/D3 1000/200 NXT, a next-generation vitamin A and D3 feed additive designed to deliver improved stability and consistent nutrient supply in animal nutrition applications.

- Strategic Focus: Microencapsulation technology leadership for vitamin stability; Luprosil expansion in Indian poultry amid AGP restriction; sustainability focus through low-carbon vitamin synthesis processes.

Market Concentration Analysis

The Indian feed additives market exhibits moderate fragmentation, with the top five global players (Cargill, Evonik, BASF, dsm-firmenich, and Kemin) collectively holding approximately 35–42% of market revenue in 2025. A growing domestic segment, comprising companies in premix blending, herbal additive manufacturing, and regional distribution, competes effectively in the mid-market vitamin-mineral and natural additive categories.

Consolidation is occurring in the specialty additive segment, with global companies acquiring or partnering with regional Indian distributors to strengthen last-mile connectivity. The domestic natural additive segment is simultaneously fragmenting, with biotechnology-native start-ups capturing niche positions in phytogenics and probiotic cultures using proprietary strain libraries unavailable to large commodity players.

Investment & Growth Opportunities

Fastest Growing Segments

Liquid acidifiers and enzyme cocktails (~9.8% CAGR), probiotic and prebiotic complexes (~11–13% CAGR), natural phytogenic additives (~12% CAGR), and rumen bypass nutrients for dairy (~10% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 600–700 Million within the Indian feed additives ecosystem by 2034.

Emerging Market Expansion

Aquaculture feed additive demand from Andhra Pradesh’s shrimp belt, Odisha’s inland fisheries, and Gujarat’s marine aquaculture sector represents an incremental USD 200–250 Million opportunity beyond the established poultry and dairy markets by 2034. Entry strategies include partnerships with local shrimp hatcheries, PMMSY-linked government tender participation, and field trial demonstration programs.

Venture and Institutional Investment Trends

- India’s AHIDF provides an INR 15,000 Crore government-backed credit guarantee scheme for investment in animal husbandry infrastructure, indirectly enabling feed additive demand growth by accelerating modernization of feed mills, dairy processing, and poultry integration capacity across underserved states.

- The PLI scheme for food processing creates downstream demand pull for higher-quality animal-derived products, incentivizing livestock producers to invest in performance-enhancing feed additive programs to meet export-grade quality standards for meat, dairy, and seafood.

- Natural and clean-label additive segments are attracting venture investment as consumer-facing brands in egg, poultry meat, and dairy products build marketing differentiation around antibiotic-free and additive-natural production practices, creating a premium market pull for biological feed additive suppliers.

Future Market Outlook (2026-2034)

India’s feed additives market is positioned for near double-digit sustained growth through 2034. From a base of USD 1.10 Billion in 2025, the market is projected to reach USD 2.38 Billion by 2034, representing incremental value creation of USD 1.28 Billion at a CAGR of 8.68%. This trajectory is structurally supported by India’s irreversible move toward organized and industrial livestock farming, rising per-capita animal protein consumption, and the government’s sustained commitment to livestock sector development.

The technology transition from conventional feed supplementation to precision nutrition, enabled by AI-driven ration optimization, IoT-based animal health monitoring, and microencapsulated targeted delivery systems, will define the market’s composition by 2034. Additive suppliers positioning as precision nutrition partners rather than commodity input providers will capture disproportionate value from India’s expanding animal agriculture sector.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 120 industry participants in 2024–2025, including feed additive manufacturers, premix producers, commercial feed mill operators, poultry and dairy integrators, veterinary nutritionists, and institutional investors across India and key exporting countries.

Secondary Research

Secondary research encompassed company annual reports, DAHD (Department of Animal Husbandry & Dairying) livestock census and feed data, FSSAI-approved additive registrations, DGFT import-export data for feed additives (HS Codes 2309, 3824), and trade publications including Feed Navigator, Feed International, and Poultry India.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating compound feed production volumes, additive inclusion rate trends, average selling price trajectories by additive category, and livestock population growth rates by state. A base-case CAGR of 8.68% reflects consensus estimates validated against compound feed production projections and additive demand indicators from FY 2020 to FY 2025.

Indian Feed Additives Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Sources Covered | Synthetic, Natural |

| Product Types Covered |

|

| Livestocks Covered |

|

| Forms Covered | Dry, Liquid |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Cargill, Incorporated, Evonik Industries AG, BASF, dsm-firmenich, Kemin Industries, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Indian feed additives market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Indian feed additives market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Indian feed additives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Feed Additives Market Report

The Indian feed additives market reached USD 1.10 Billion in 2025 and is projected to reach USD 2.38 Billion by 2034.

The market is expected to grow at a CAGR of 8.68% during 2026-2034, driven by rising animal protein demand, modernization of livestock farming, and the shift from antibiotic growth promoters to natural additive alternatives.

South India leads with a 34.7% share in 2025, anchored by Andhra Pradesh and Telangana’s dominant position in India’s broiler poultry industry and the region’s large concentration of organized feed mills.

Dry-form additives dominate with a 71.6% share in 2025, encompassing powders, granules, and pellets that are compatible with standard commercial feed mill mixing and pelleting equipment.

Synthetic-source additives hold the largest share at 58.6%, driven by their consistent purity, predictable bioavailability, and cost-competitiveness for high-volume poultry and aquaculture feed formulation.

Key players include Cargill, Incorporated, Evonik Industries AG, BASF, dsm-firmenich, Kemin Industries, Inc.

Liquid-form additives are growing at approximately 9.8% CAGR because of their superior post-pelleting application capability for heat-sensitive enzymes and probiotics, and the expansion of Indian aquafeed formulation requiring liquid acidifiers.

Key challenges include the fragmented smallholder farming structure limiting premium additive adoption, high costs of specialty additive categories, stringent FSSAI regulatory approval timelines, and cold chain infrastructure gaps for liquid and biological additives.

Aquaculture feed additives, natural phytogenic and probiotic products, rumen bypass nutrients for dairy, liquid acidifiers and enzyme complexes, and digital precision nutrition advisory platforms represent the highest-growth investment opportunities through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade