Indian Fish Market Size, Share, Trends and Forecast by Fish Type, Product Type, Distribution Channel, Sector, and State, 2026-2034

Indian Fish Market Size, Share, Trends & Forecast (2026-2034)

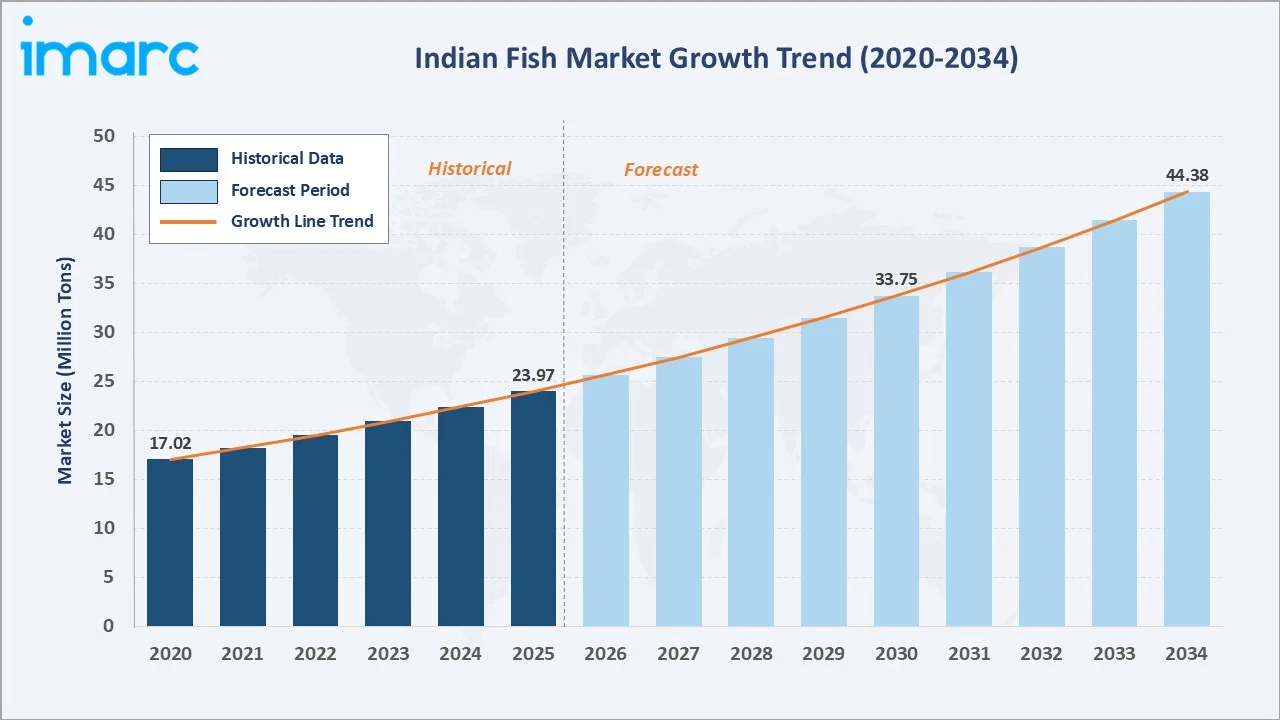

The Indian fish market reached a volume of 23.97 Million Tons in 2025 and is projected to reach 44.38 Million Tons by 2034, exhibiting a CAGR of 7.08% during 2026-2034. Rising protein consumption, expanding aquaculture output, and broadening cold-chain infrastructure are primary drivers of market growth. In FY 2024-25, India became the second-largest fish producer globally, accounting for 8% of global fish production.

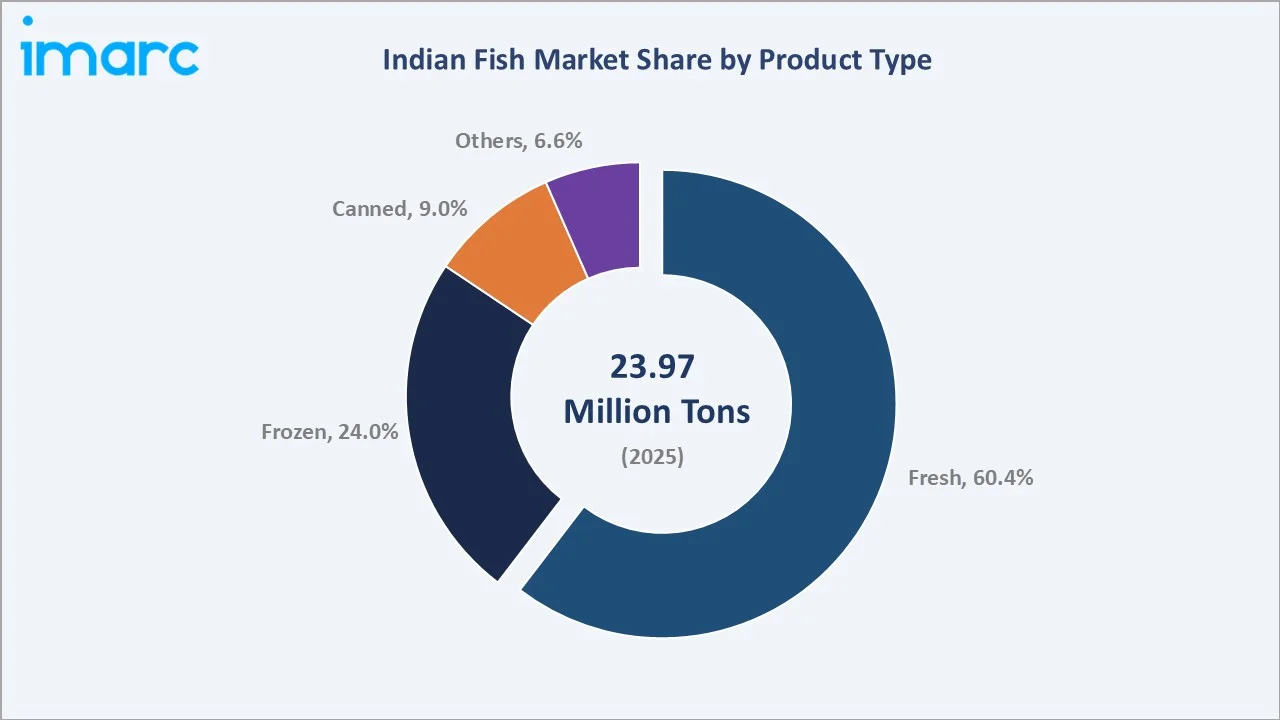

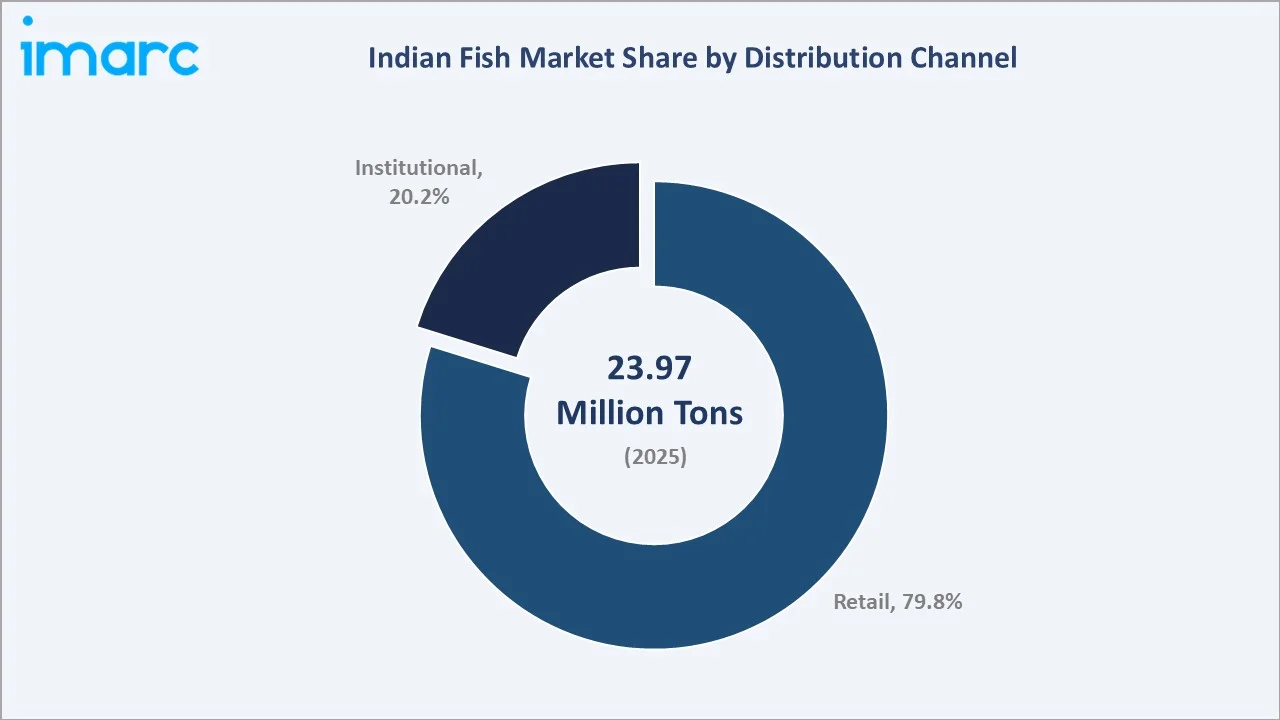

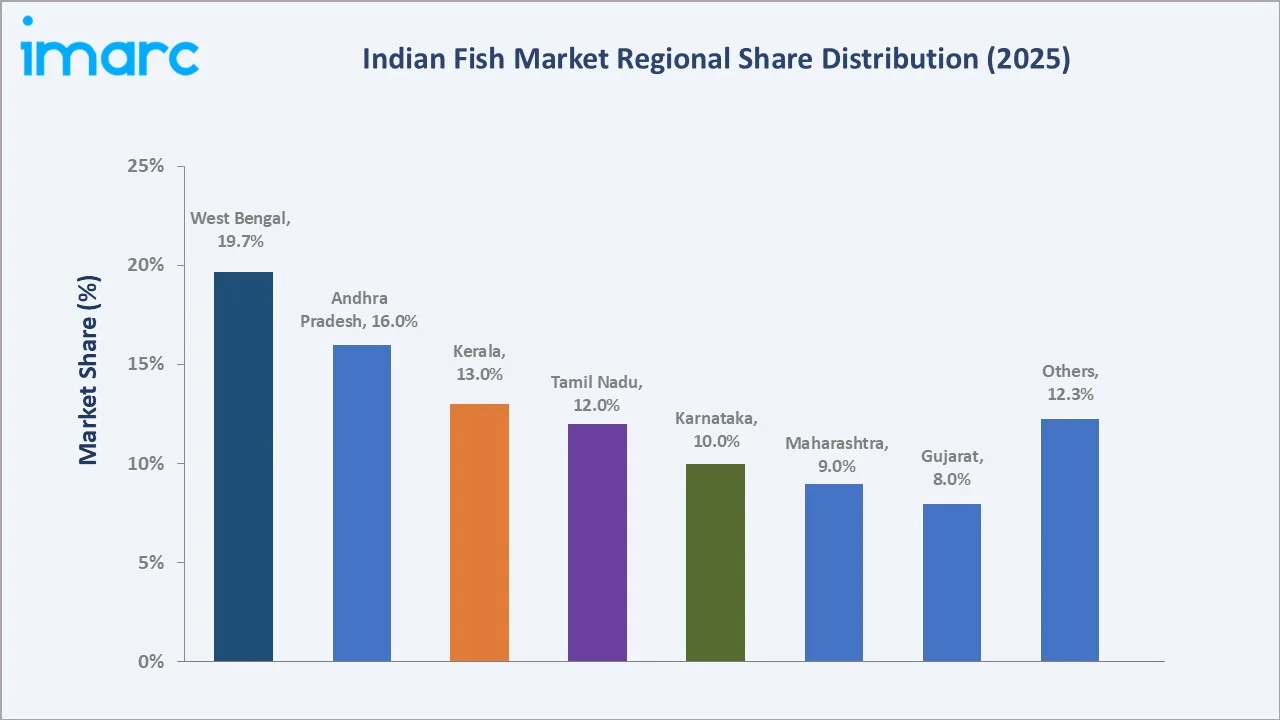

Fresh leads product type share at 60.4%, retail dominates distribution channel at 79.8%, and West Bengal commands the highest state-level share at 19.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

23.97 Million Tons |

|

Forecast Market Size (2034) |

44.38 Million Tons |

|

CAGR (2026-2034) |

7.08% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest State |

West Bengal (19.7%, 2025) |

|

Second Largest State |

Andhra Pradesh (16.0%, 2025) |

|

Leading Product Type |

Fresh (60.4%, 2025) |

|

Leading Distribution Channel |

Retail (79.8%, 2025) |

To get more information on this market, Request Sample

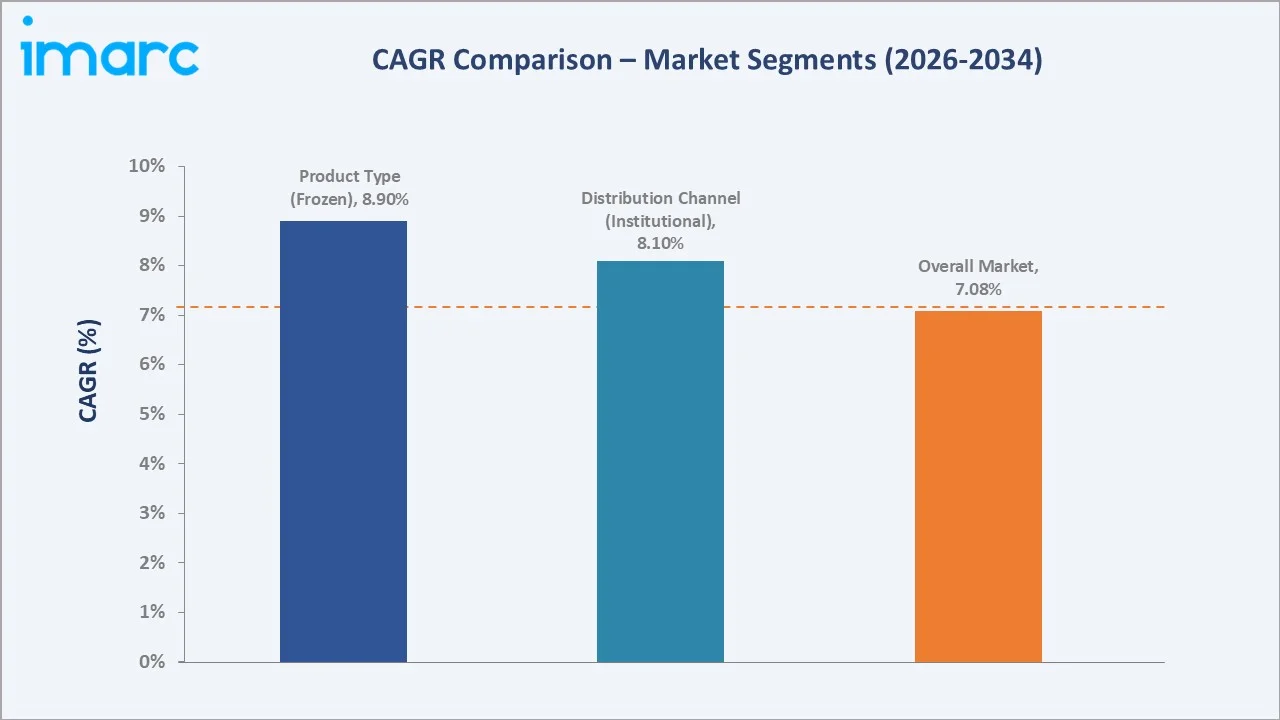

CAGR trajectories across product type and distribution channel sub-segments show frozen and canned growing faster than the overall 7.08% market CAGR, driven by improving cold-chain logistics, expanding modern retail penetration, and rising institutional buyer demand.

Executive Summary

The Indian fish market is on a sustained growth trajectory, expanding from 17.02 Million Tons in 2020 to 23.97 Million Tons in 2025, and forecast to reach 44.38 Million Tons by 2034. This growth reflects a structural shift from fragmented, informal supply chains toward organized, technology-enabled distribution systems spanning marine capture fisheries, inland aquaculture, and cold-storage-linked retail networks.

Fresh dominates product type share at 60.4% in 2025, driven by deep-rooted consumer preferences, widespread wet-market presence, and the absence of cold-chain requirements at the retail end. Retail leads distribution channel at 79.8%, anchored by traditional wet markets, supermarkets, and online grocery platforms. West Bengal commands the largest state-level share at 19.7%, supported by strong fish consumption habits, extensive inland aquaculture activity, and a well-established seafood distribution ecosystem.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Fresh – 60.4% share (2025) |

|

Second Largest Product Type |

Frozen – 24.0% share (2025) |

|

Leading Distribution Channel |

Retail – 79.8% share (2025) |

|

Second Largest Distribution Channel |

Institutional – 20.2% share (2025) |

|

Leading State |

West Bengal – 19.7% share (2025) |

|

Second Largest State |

Andhra Pradesh – 16.0% share (2025) |

|

Top Companies |

IFB Agro Industries Limited, Avanti Feeds Limited, Nekkanti SeaFoods, Falcon Marine Exports |

Key Analytical Observations Expanding on the Data Above:

- Fresh dominance at 60.4% in 2025 reflects the strength of traditional consumption patterns across coastal and inland states, the widespread reach of unorganized wet markets, and consumer preference for perceived freshness over convenience formats.

- Frozen at 24.0% is expanding rapidly, driven by modern trade growth, export-oriented aquaculture in Andhra Pradesh and Gujarat, and the penetration of organized cold-chain logistics into tier-2 and tier-3 cities. As per IMARC Group, the India cold chain logistics market size reached USD 12.6 Billion in 2025.

- Retail at 79.8% continues to dominate, combining traditional wet market networks, supermarkets, and rapidly growing online fish delivery platforms that have emerged across metro and urban India.

- Institutional share at 20.2% is supported by consistent demand from hotels, restaurants, catering services, educational institutions, hospitals, and food processing companies, which rely on bulk seafood procurement to meet large-scale consumption requirements throughout the year.

- West Bengal at 19.7% leads state-level share, anchored by the country's high per-capita fish consumption, the culturally central role of hilsa and rohu in Bengali cuisine, and large inland fisheries supported by the Ganges-Brahmaputra river system.

Indian Fish Market Overview

The Indian fish market encompasses the production, processing, distribution, and sale of marine and freshwater fish across capture fisheries and aquaculture systems. It covers fresh, frozen, canned, and other value-added fish products marketed through retail and institutional channels. The ecosystem integrates fishing communities, aquaculture enterprises, processing units, cold-chain operators, wholesale traders, cooperatives, and organized retail and online platforms.

Macroeconomic factors, including rising disposable incomes, growing protein awareness, government subsidy programs, infrastructure investment under PMMSY, and expanding organized retail penetration, are reshaping demand and supply dynamics. The market spans all coastal and major inland states, with West Bengal, Andhra Pradesh, Kerala, Tamil Nadu, Karnataka, Maharashtra, and Gujarat forming the production and consumption core.

Market Dynamics

To evaluate market opportunities, Request Sample

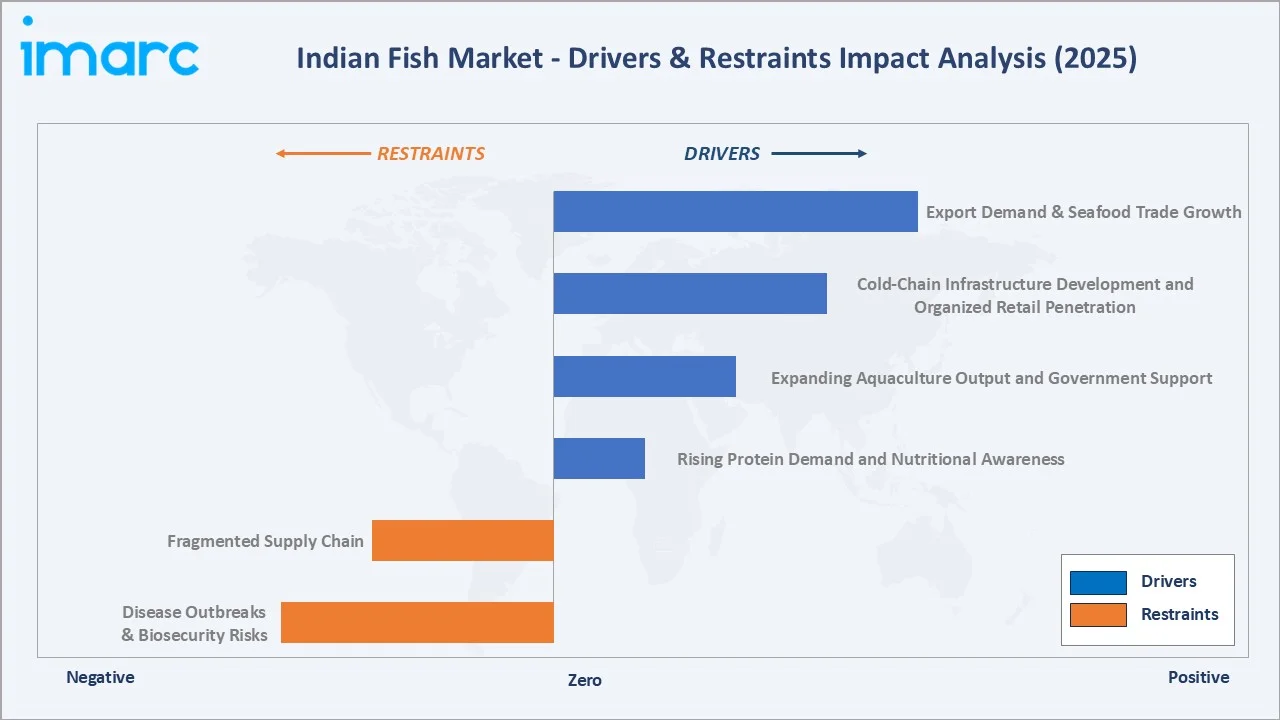

Market Drivers

- Rising Protein Demand and Nutritional Awareness: Growing health consciousness, nutritional education, and the shift toward protein-rich diets across urban and semi-urban India are driving consistent volume growth in fish consumption across all age groups and income segments.

- Expanding Aquaculture Output and Government Support: India's aquaculture sector has grown rapidly through PMMSY investments in hatcheries, feed production, and post-harvest infrastructure. Launched in the Union Budget 2025-26, the Prime Minister Dhan-Dhaanya Krishi Yojana (PMDDKY) aims to stimulate development in 100 Agri Aspirational districts. The program guarantees saturation-centered convergence of 36 initiatives from 11 ministries, directly aiding 1.7 Crore farmers, including the Department of Fisheries initiatives like PMMSY, PMMKSSY, and Kisan Credit Card for the Fisheries Sector.

- Cold-Chain Infrastructure Development and Organized Retail Penetration: Investments in refrigerated transport, cold storage, and modern retail formats are extending the freshness window for fish, enabling broader geographic distribution and supporting the growth of frozen and processed segments beyond coastal proximity markets.

- Export Demand and Global Seafood Trade Growth: India's seafood exports are supporting higher-quality aquaculture production and creating backward linkages that improve overall fish supply quality and domestic market availability.

Market Restraints

- Fragmented Supply Chain and Unorganized Market Structure: The dominance of small-scale fishers, lack of price transparency, multiple intermediaries, and the absence of standardized grading systems increase transaction costs, limit quality consistency, and reduce value captured by producers and formal processors.

- Disease Outbreaks and Biosecurity Risks: Recurring disease outbreaks in aquaculture systems, including viral and bacterial infections, can result in significant stock losses, lower productivity, and increased operational costs for farmers. These risks create supply uncertainty and discourage investment in intensive aquaculture expansion projects.

Market Opportunities

- Value-Added and Processed Fish Products: Growing urban demand for ready-to-cook and ready-to-eat fish products presents opportunities for processors to move up the value chain into marinated, breaded, smoked, and convenience-format offerings targeting modern retail and food service.

- Online Fish Delivery and Direct-to-Consumer Models: The rapid growth of online grocery and fresh food delivery platforms is enabling fish sellers to bypass traditional intermediaries, improve freshness assurance, expand geographic reach, and capture premium urban consumer segments.

Market Challenges

- Climate Change and Fisheries Resource Depletion: Overfishing in coastal zones, changing monsoon patterns, sea-surface temperature rise, and habitat degradation are creating resource pressure on marine capture fisheries, increasing supply volatility and affecting fishing community livelihoods.

- Quality and Food Safety Compliance: Meeting domestic and export food safety standards, including antibiotic residue limits, hygiene protocols, and traceability requirements, remains a persistent challenge for fragmented small-scale producers competing in organized retail and export channels.

Emerging Market Trends

1. Rapid Expansion of Aquaculture and Shift Toward Farmed Fish

India's aquaculture output has grown significantly faster than marine capture over the past decade, with farmed fish accounting for a majority of total production. Species diversification into pangasius, tilapia, and high-value shrimp is expanding the supply base.

2. Digital Transformation and Online Fish Retail Growth

Online fish delivery platforms have transformed urban fish retail by offering cleaned, portioned, and marinated products with same-day delivery. These platforms are bypassing traditional intermediaries, improving cold-chain compliance, and enabling premium pricing for quality-assured fresh and processed fish, supporting the Indian fish market growth through higher value-per-unit capture and expanded geographic reach.

3. Premiumization and Value-Added Seafood Development

Rising urban incomes and evolving food habits are driving demand for marinated, ready-to-cook, and ethnically flavored fish preparations in organized retail formats. Processors are investing in branded value-added fish lines targeting supermarkets and quick-commerce platforms, shifting competition from commodity volume to differentiated product positioning.

4. Export Orientation and International Certification Compliance

Export demand from the United States, European Union, Japan, and Southeast Asia is prompting Indian processors to upgrade facilities, achieve BRC, HACCP, and BAP certifications, and invest in traceability systems. This export-driven quality improvement is creating positive spillovers into the domestic market by raising overall processing standards and enabling branded domestic retail entry.

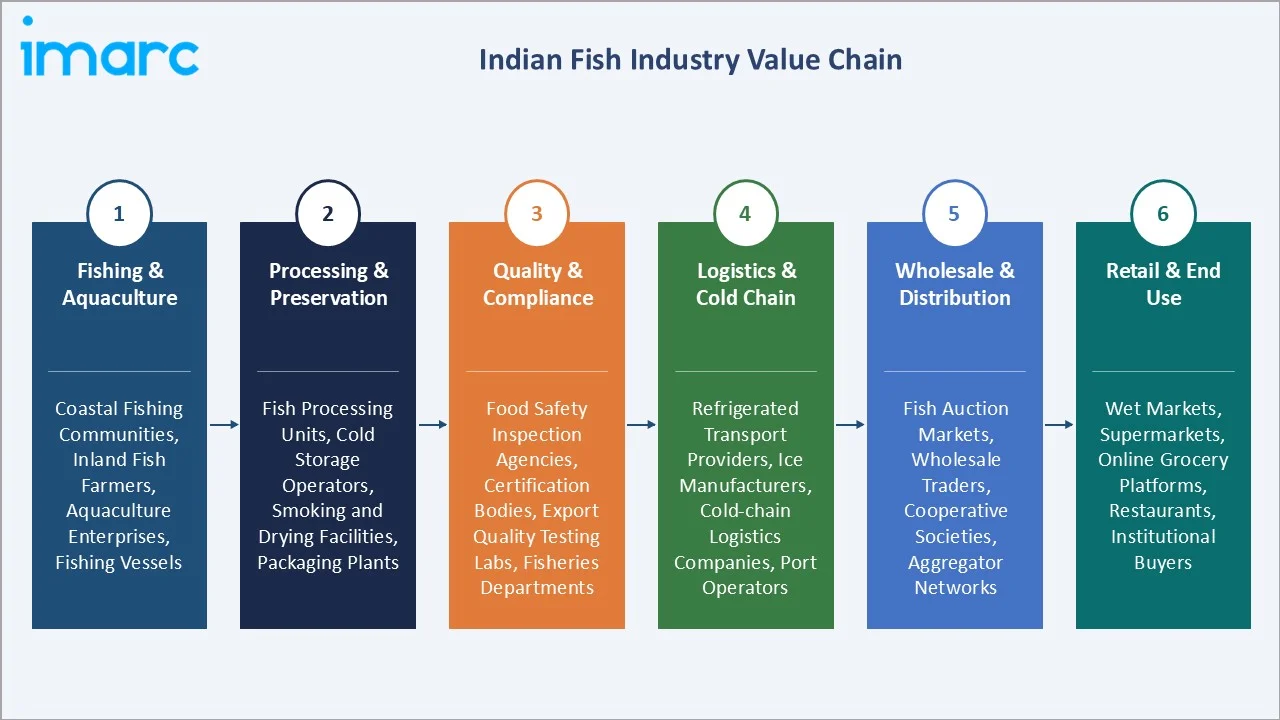

Industry Value Chain Analysis

The Indian fish market value chain spans six stages from primary production through end use consumption and lifecycle management. Processing, cold-chain logistics, and retail distribution capture the highest value-add, while post-harvest handling and quality compliance infrastructure increasingly determine sustainable competitive position across the market.

|

Stage |

Key Players / Examples |

|

Fishing & Aquaculture |

Coastal fishing communities, inland fish farmers, aquaculture enterprises, marine and freshwater fishing vessels |

|

Processing & Preservation |

Fish processing units, cold storage operators, smoking and drying facilities, canning and packaging plants |

|

Quality & Compliance |

Food safety inspection agencies, certification bodies, export quality testing labs, state fisheries departments |

|

Logistics & Cold Chain |

Refrigerated transport providers, ice manufacturers, cold-chain logistics companies, port and terminal operators |

|

Wholesale & Distribution |

Fish auction markets, wholesale traders, cooperative societies, aggregator networks, institutional procurement agents |

|

Retail & End Use |

Wet markets, supermarkets and hypermarkets, online grocery platforms, restaurants, institutional buyers such as hotels and canteens |

Vertically integrated players, particularly those combining aquaculture production, processing, and branded retail or export sales, are positioned to capture greater value than fragmented intermediary-dependent operators reliant on spot market transactions.

Technology Landscape in the India Fish Industry

Aquaculture Technology and Feed Innovation

Advanced recirculating aquaculture systems (RAS), biofloc technology, and precision feeding systems are improving fish yield per unit area and reducing disease incidence. Feed manufacturers are deploying formulation technology to optimize protein efficiency, reduce fishmeal dependency, and improve feed conversion ratios for major farmed species, including shrimp, rohu, and tilapia.

Cold-Chain and Post-Harvest Technology

Improved ice-making equipment, insulated fish landing centers, blast-freezing technology, and GPS-tracked refrigerated transport are extending shelf life and reducing losses across the supply chain. Government-funded fish landing centers equipped with ice plants and cold rooms are improving primary-level handling in major coastal states.

Digital Platforms and Traceability Systems

Blockchain-based traceability platforms, QR-coded packaging, and mobile-enabled auction systems are improving price discovery, transaction efficiency, and end-to-end quality documentation. State fisheries portals and digital catch reporting tools are modernizing fleet management and enabling better resource monitoring across marine fishing zones.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Fish Type |

Inland Fishes |

70.3% |

2025 |

|

Product Type |

Fresh |

60.4% |

2025 |

|

Distribution Channel |

Retail |

79.8% |

2025 |

|

Sector |

🔒 |

🔒 |

2025 |

|

State |

West Bengal |

19.7% |

2025 |

By Product Type

Fresh commands the largest product type share at 60.4% in 2025, driven by deeply embedded consumer preferences for live and freshly caught fish, the ubiquitous presence of wet markets and roadside fish vendors across urban and rural India, and lower consumer willingness to pay premiums for processed formats at the mass market level. The segment benefits from the perishable, high-turnover nature of fish supply, which maintains vendor economics even in low-infrastructure environments.

To access detailed market analysis, Request Sample

Frozen at 24.0% is the second largest product type, supported by modern trade expansion, organized aquaculture supply chains, and institutional buyer procurement. Its longer shelf life and suitability for long-distance transportation further enhance its appeal across urban retail and foodservice channels.

By Distribution Channel

Retail commands 79.8% of distribution channel in 2025, encompassing traditional wet fish markets, neighborhood fishmongers, supermarkets and hypermarkets, and online fish delivery platforms. The segment benefits from direct consumer access, high purchase frequency, and the widespread availability of seafood across both urban and rural markets.

Institutional at 20.2% serves hotels, restaurants, caterers, hospitals, defense canteens, and institutional processors. This segment is expanding as foodservice formalizes and organized restaurant chains build direct procurement relationships with approved aquaculture suppliers and certified processing units.

Regional Market Insights

|

State |

Share (2025) |

Key Growth Drivers |

|

West Bengal |

19.7% |

Large inland fisheries, strong hilsa culture, dense river networks, and high per-capita fish consumption |

|

Andhra Pradesh |

16.0% |

Extensive coastal access, export-oriented shrimp farming, and well-developed cold-chain infrastructure |

|

Kerala |

13.0% |

Deep-sea marine fishing tradition, strong export linkages, robust processing industry, and high domestic seafood consumption |

|

Tamil Nadu |

12.0% |

Established marine fishing fleet, growing aquaculture base, strong institutional procurement, and extensive coastline |

|

Karnataka |

10.0% |

Expanding aquaculture activity, growing urban demand, improving cold-chain logistics, and state-supported fisheries programs |

|

Maharashtra |

9.0% |

Large urban consumer base in Mumbai, well-connected distribution networks, expanding organized retail penetration |

|

Gujarat |

8.0% |

Major marine fishing hub, significant export orientation, strong industrial fishing fleet, and large processing zone infrastructure |

|

Others |

12.3% |

Emerging inland fisheries, rising urban middle-class demand, improving cold-chain access, and state-level aquaculture development programs |

West Bengal at 19.7% in 2025 leads state-level market share, reflecting high per-capita fish consumption in India, deep cultural significance of fish, extensive inland water bodies, and large-scale hilsa and rohu fisheries. A well-developed network of fish markets, aquaculture farms, and distribution channels further strengthens the state's position as a key seafood production and consumption hub.

Andhra Pradesh at 16.0% represents the second largest state-level market, anchoring export-oriented shrimp and fish supply to both domestic processors and international buyers. Its well-established hatchery infrastructure and access to major port facilities further support the state's leadership in seafood production and trade.

Competitive Landscape

The Indian fish market is moderately fragmented, with a large informal sector of small-scale fishers and traders alongside a growing organized layer of aquaculture producers, processors, and branded retail operators. Brand strength, processing capacity, cold-chain control, export certifications, and digital platform presence form the key competitive differentiators in the organized segment.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

IFB Agro Industries Limited |

IFB Fresh Catch |

Leader |

Integrated aquaculture and seafood processing with strong export and domestic market presence |

|

Avanti Feeds Limited |

Avanti Frozen Foods |

Leader |

Large-scale shrimp feed and processing with vertically integrated aquaculture supply chain |

|

Nekkanti SeaFoods |

Nekkanti SeaFoods |

Leader |

Export-oriented marine seafood processing with focus on quality-certified frozen fish products |

|

Falcon Marine Exports |

Falcon Fresh |

Emerging |

Marine seafood export specialist with focus on certified processing and international market compliance |

Key players include IFB Agro Industries Limited, Avanti Feeds Limited, Nekkanti SeaFoods, and Falcon Marine Exports, among others.

Key Company Profiles

IFB Agro Industries Limited

IFB Agro Industries Limited is a Kolkata-based integrated company with diversified operations in aquaculture, seafood processing, and allied segments. The company markets its domestic retail seafood range under the IFB Fresh Catch brand, offering frozen and ready-to-cook products across modern trade, e-commerce platforms, and the hospitality sector.

- Product Portfolio: Frozen prawns, fish fillets, and ready-to-cook and ready-to-fry seafood products marketed under the IFB Fresh Catch brand through organized retail, hospitality, and export channels.

- Recent Development: The company has been actively expanding its aquaculture feed distribution network and strengthening its cold-chain-linked processing capacity to support growing domestic retail and export demand for branded frozen seafood products.

- Strategic Focus: Strengthening integrated aquaculture and processing capabilities, expanding the IFB Fresh Catch retail brand footprint, and growing export volumes through certified processing infrastructure.

Avanti Feeds Limited

Avanti Feeds Limited is one of India's leading aquaculture companies, engaged in shrimp feed manufacturing and seafood processing and export. The company operates through its wholly-owned subsidiary Avanti Frozen Foods, which manages shrimp processing and export operations serving global markets.

- Product Portfolio: Shrimp aquafeeds and processed frozen shrimp products, including value-added and ready-to-cook shrimp formats, marketed through institutional and export channels to buyers in the United States, Europe, Japan, and the Middle East.

- Recent Development: The company has been investing in capacity expansion across its shrimp processing facilities and diversifying its export market reach, while continuing to strengthen its position as the leading shrimp feed supplier in India.

- Strategic Focus: Scaling shrimp feed and processing capacity, deepening integration across the aquaculture value chain, and expanding access to high-value international markets through quality-certified processing.

Nekkanti SeaFoods

Nekkanti SeaFoods is one of India's largest seafood processing and export companies, with fully integrated operations spanning hatcheries, aquaculture farms, and state-of-the-art processing facilities. The company serves institutional buyers and retail importers across major global seafood markets.

- Product Portfolio: Processed and frozen shrimp and fish products, including head-on shell-on, headless shell-on, peeled and deveined, breaded, and cooked formats, distributed to buyers in the United States, Europe, Japan, and other international markets.

- Recent Development: The company has been expanding its processing infrastructure and deepening buyer relationships in key international markets, reinforcing its position among India's top seafood exporters by volume and product quality.

- Strategic Focus: Maintaining export quality certifications, expanding processing capacity, and growing the value-added product range targeting international organized retail and food service segments.

Market Concentration Analysis

The Indian fish market is highly fragmented at the production and primary distribution level, with millions of small-scale marine fishers and inland aquaculture farmers operating across thousands of landing centers, fish ponds, and local markets. Organized players account for a relatively small share of total market volume, with concentration increasing significantly in export-oriented processing and branded domestic retail segments.

Barriers to entry in the organized segment include export certification and quality compliance costs, cold-chain infrastructure investment, working capital requirements for perishable inventory management, and the need for established buyer relationships in export markets. These factors favor well-capitalized integrated producers with established supply chains and quality management systems.

Consolidation is emerging in the aquaculture feed, processing, and export segments, where scale economies and quality consistency demands are favoring integrated producers. Online fish retail is also consolidating around a few well-funded platforms building brand equity and supply chain control in urban markets.

Investment & Growth Opportunities

Fastest-Growing Segments

Frozen is the fastest-growing product type, expanding at a CAGR of approximately 8.90%, driven by modern retail expansion, export-oriented aquaculture, and institutional buyer demand for standardized, shelf-stable supply. Canned at 9.0% presents premium growth opportunity in export, urban snacking, and defense procurement channels.

Emerging Markets

Karnataka, Maharashtra, and Gujarat represent significant untapped opportunity for organized distribution expansion, with growing urban middle-class demand, improving cold-chain logistics, and underserved modern retail fish supply. Institutional at 20.2% is expanding as foodservice formalizes and organized procurement displaces spot buying.

Venture & Investment Trends

Investment is flowing into online fish delivery platforms, cold-chain logistics providers, branded aquaculture producers, and value-added seafood processors. Government PMMSY allocations are stimulating co-investment in landing infrastructure, fish processing clusters, and aquaculture technology, creating favorable conditions for private capital deployment in the organized market segment.

Future Market Outlook (2026-2034)

The Indian fish market is forecast to expand from 23.97 Million Tons in 2025 to 44.38 Million Tons by 2034 at a CAGR of 7.08%, adding approximately 20.41 Million Tons in incremental annual volume over the forecast period. The market is projected to reach 33.75 Million Tons in 2030 as aquaculture productivity gains, cold-chain investment, and organized retail penetration compound across the forecast period.

Four forces will shape the market through 2034: continued aquaculture intensification and species diversification; the modernization of post-harvest and cold-chain infrastructure; the expansion of organized retail and online delivery channels; and the deepening integration of Indian seafood producers into global export value chains.

By 2034, the Indian fish market is expected to be defined by a greater balance between capture fisheries and aquaculture supply, significantly higher penetration of frozen and value-added products, and a growing share of organized retail and digital distribution in total market volume. Policy continuity under PMMSY and successor schemes is expected to support sustained above-average growth through the forecast period.

Research Methodology

Primary Research

Primary research included structured interviews with fish traders, aquaculture producers, cold-chain logistics operators, organized retail buyers, export processors, and government fisheries officials, validating market sizing, production volumes, segment shares, and regional demand dynamics.

Secondary Research

Secondary sources included Ministry of Fisheries, Animal Husbandry & Dairying publications, National Fisheries Development Board data, Marine Products Export Development Authority (MPEDA) trade statistics, FAO fishery reports, and annual reports, investor presentations, and press releases from leading seafood processors and aquafeed companies.

Forecasting Models

Market forecasts employed top-down and bottom-up models combining aquaculture production data, marine capture landing statistics, consumption surveys, cold-chain capacity projections, and macroeconomic growth variables. Scenario analysis addressed aquaculture productivity, cold-chain investment pacing, and export market evolution through 2034.

Indian Fish Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fish Types Covered |

|

| Product Types Covered | Fresh, Frozen, Canned, Others |

| Distribution Channels Covered | Retail, Institutional |

| Sectors Covered | Organised, Unorganised |

| States Covered | West Bengal, Andhra Pradesh, Karnataka, Kerala, Gujarat, Tamil Nadu, Maharashtra, Others |

| Companies Covered | IFB Agro Industries Limited, Avanti Feeds Limited, Nekkanti SeaFoods, Falcon Marine Exports, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Fish Market Report

The Indian fish market reached a volume of 23.97 Million Tons in 2025, driven by rising protein demand, expanding aquaculture output, and improving cold-chain distribution infrastructure.

The market is projected to grow at 7.08% CAGR from 2026-2034, reaching 44.38 Million Tons, supported by aquaculture expansion, frozen segment growth, and organized retail penetration.

Fresh leads at 60.4% in 2025, driven by traditional consumer preferences, wet-market distribution, and the widespread availability of freshly caught fish across coastal and inland states.

Retail commands 79.8% in 2025, encompassing wet markets, supermarkets, and online delivery platforms, with institutional at 20.2% growing through foodservice formalization.

West Bengal leads at 19.7% in 2025, reflecting high per-capita fish consumption, strong inland fisheries, and the cultural centrality of fish in Bengali cuisine.

Key players include IFB Agro Industries Limited, Avanti Feeds Limited, Nekkanti SeaFoods, and Falcon Marine Exports, among others.

Aquaculture has become the primary growth engine, with farmed fish output growing rapidly through shrimp, rohu, catla, and tilapia farming across coastal and inland states.

Growth is driven by rising protein awareness, aquaculture output expansion, government fisheries investment under PMMSY, cold-chain modernization, and online fish retail platform growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)