Indian LED Lighting Market Size, Share, Trends and Forecast by Product Type and Application, 2026-2034

Indian LED Lighting Market Size, Share, Trends & Forecast (2026-2034)

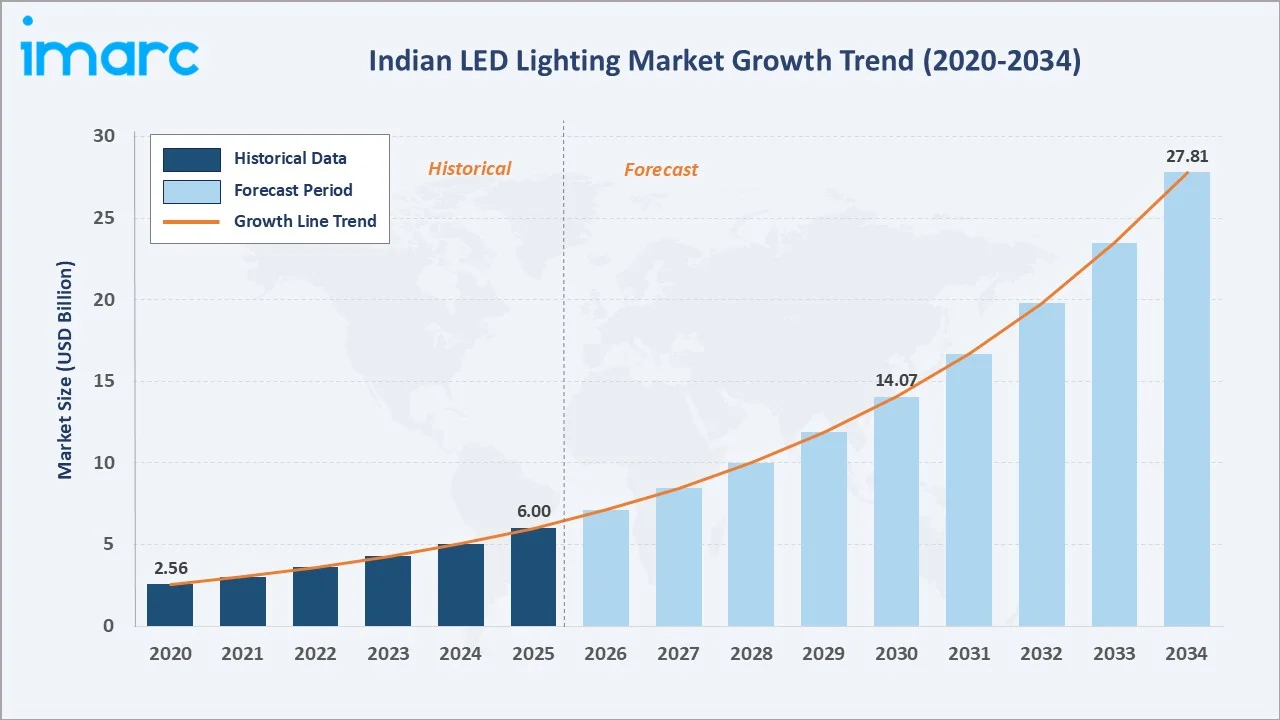

The Indian LED lighting market size was valued at USD 6.00 Billion in 2025 and is projected to reach USD 27.81 Billion by 2034, growing at a CAGR of 18.58% during 2026-2034. Smart city infrastructure development, government energy efficiency programs, and rising consumer demand for sustainable, technologically advanced lighting solutions are the primary catalysts driving India's LED lighting industry.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.00 Billion |

|

Forecast Market Size (2034) |

USD 27.81 Billion |

|

CAGR (2026-2034) |

18.58% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

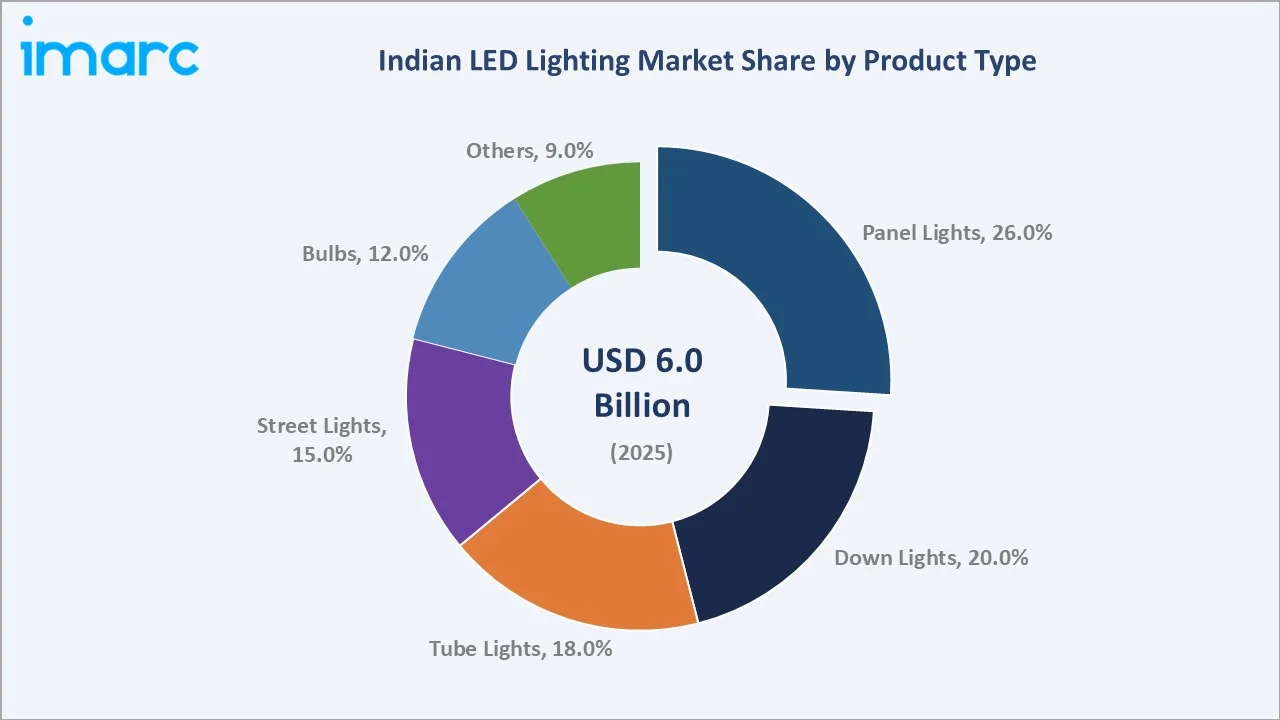

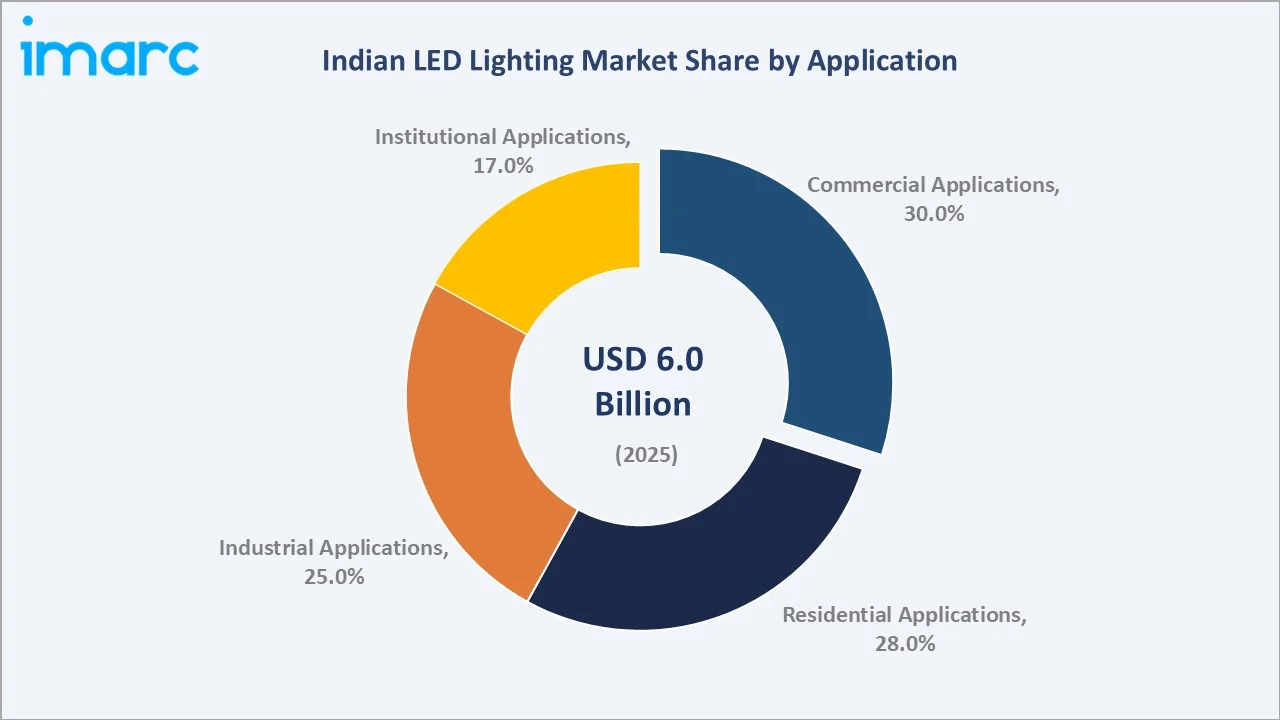

Panel lights dominate with a 26.0% product-type share in 2025, while commercial applications lead at 30.0%. North India holds the largest regional share, supported by extensive Smart City Mission deployments in Delhi-NCR and Uttar Pradesh. The UJALA scheme has distributed over 36 crore LED units nationally, and Energy Efficiency Services Limited has installed over 1.34 crore LED streetlights, delivering annual energy savings exceeding 9,001 million units, demonstrating the transformative impact of government-led programs on India's LED adoption trajectory.

To get more information on this market, Request Sample

With applications spanning commercial, residential, industrial, and institutional segments, and a rapidly growing smart lighting ecosystem supported by IoT integration, the Indian LED lighting market forecast reflects one of the strongest growth trajectories among global emerging market lighting sectors through 2034.

Executive Summary

The Indian LED lighting market is on an exceptional growth path, driven by convergent forces of urbanization, government infrastructure investment, and rapid technological advancement in smart and connected lighting systems. The market reached USD 6.00 Billion in 2025 and is forecast to reach USD 27.81 Billion by 2034, reflecting a robust CAGR of 18.58%, one of the highest growth rates in global lighting markets.

Panel lights command the largest product share at 26.0%, reflecting extensive adoption across modern commercial offices, retail spaces, and institutional buildings. Commercial applications lead demand at 30.0%, driven by rapid expansion of office complexes, healthcare facilities, and hospitality venues. Key players, Signify Holding, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Bajaj Electricals India, Surya Roshni Ltd., and Halonix Technologies Private Limited, are investing in smart lighting platforms, domestic manufacturing under PLI incentives, and IoT-enabled product portfolios to capture the market's high-growth trajectory.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Panel Lights – 26.0% share (2025) |

|

Largest Segment (Application) |

Commercial Applications – 30.0% share (2025) |

|

Fastest Growing Product |

Street Lights (CAGR ~21.2%, 2026-2034) |

|

Fastest Growing Application |

Commercial Applications (CAGR ~20.3%) |

|

Key Government Program |

UJALA: 36.87 Cr units; 1.34 Cr streetlights installed (2025) |

|

Manufacturing Catalyst |

Signify-Dixon JV (March 2025); PLI INR 444.54 Cr (FY 2025–26) |

Key Analytical Observations Supporting the Above Data:

- Panel lights account for 26.0% of the Indian LED lighting market in 2025, preferred in contemporary retail spaces, commercial offices, and institutional buildings for their elegant design, uniform light distribution, and superior energy efficiency compared to traditional fluorescent fixtures.

- Commercial applications dominate at 30.0% in 2025, driven by rapid expansion of office complexes, retail chains, healthcare facilities, and hospitality venues implementing Energy Conservation Building Code mandates that require high-efficiency LED installations in new and renovated structures.

- North India holds approximately 34.0% of the market in 2025, underpinned by large-scale Smart Cities Mission deployments across Delhi, Lucknow, and Agra, alongside high commercial real estate activity and extensive LED streetlight replacement programs in Uttar Pradesh and Haryana.

- South India at 28.0% is the fastest-growing region, led by Bengaluru's booming technology park and commercial office sector, the Karnataka government's INR 684-crore LED streetlight program in Bengaluru approved in August 2024, and expanding hospitality infrastructure.

- Street lights represent 15.0% of product demand in 2025 and exhibit the strongest segment CAGR at approximately 21.2%, supported by sustained government procurement through the Street Lighting National Programme and state-level smart streetlight initiatives.

Indian LED Lighting Market Overview

The Indian LED lighting market encompasses the design, manufacture, distribution, and installation of light-emitting diode-based illumination products across indoor and outdoor applications spanning residential, commercial, institutional, industrial, and public infrastructure segments. India has emerged as the world's largest LED distribution market by unit volume, driven by government bulk-procurement programs that reduced LED bulb prices by approximately 80% since 2014 through demand aggregation.

Structural growth drivers include India's 100 Smart Cities Mission, catalyzing intelligent streetlight and building automation deployments, the Production-Linked Incentive (PLI) Scheme for White Goods, covering LED lights, with a total outlay of INR 6,238 crore, to be implemented from FY 2021–22 to FY 2028–29, and India's expanding commercial real estate market generating consistent high-specification architectural lighting demand.

Lighting accounts for approximately 15% of India's national electricity consumption, making each incremental percentage point of LED penetration a measurable contributor to national energy security objectives and carbon reduction commitments under the Paris Agreement.

Market Dynamics

To evaluate market opportunities, Request Sample

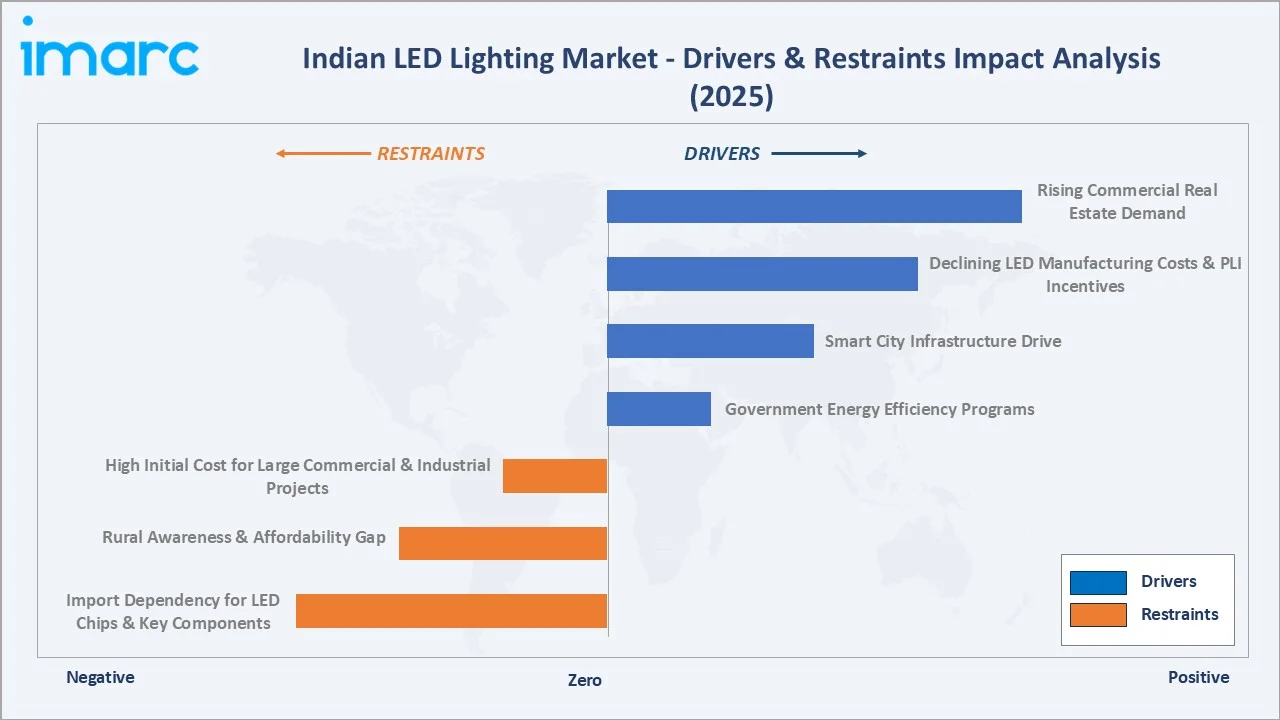

Market Drivers

- Government Energy Efficiency Programs: Energy Efficiency Services Limited installed over 1.34 crore LED streetlights across Urban Local Bodies and Gram Panchayats by January 2025, generating annual energy savings exceeding 9,001 million units and proving the economic case for large-scale LED conversion.

- Smart City Infrastructure Drive: India's 100 Smart Cities Mission has triggered large-scale LED deployments integrated with IoT sensors, adaptive controls, and remote management platforms across participating cities.

- Declining LED Manufacturing Costs and PLI Incentives: LED component costs have fallen dramatically, with the PLI scheme for White Goods allocating INR 444.54 crore for FY 2025–26 to incentivize domestic driver and PCB assembly.

- Rising Commercial Real Estate Demand: Energy Conservation Building Code standards require high-efficiency LED installations in new commercial and institutional buildings, creating a mandatory compliance-driven demand base that sustains commercial segment growth through the forecast period.

These drivers reinforce a self-sustaining adoption cycle, government programs build consumer familiarity, declining costs expand affordability, rising real estate creates mandatory compliance demand, and smart city initiatives drive premium product segment growth across India's rapidly urbanizing economy.

Market Restraints

- High Initial Cost for Large Commercial and Industrial Projects: Despite falling consumer LED prices, large-scale commercial and industrial LED lighting system installations require significant upfront capital investment.

- Rural Awareness and Affordability Gap: Despite the UJALA scheme's success in urban and peri-urban areas, rural household LED adoption remains constrained by awareness gaps, limited retail distribution reach, and preference for lowest-cost alternatives.

- Import Dependency for LED Chips and Key Components: India imports a significant proportion of LED chips and specialized semiconductor components, creating supply chain vulnerability to geopolitical disruptions, logistics cost inflation, and foreign exchange rate movements. While PLI incentives are progressively building domestic manufacturing capabilities, complete supply chain localization will require sustained multi-year investment.

Market Opportunities

- Domestic Manufacturing Expansion Through PLI and JV Partnerships: The March 2025 Signify-Dixon Technologies 50:50 joint venture to manufacture LED solutions, bulbs, battens, downlights, and accessories exemplifies the strategic opportunity for technology-manufacturing partnerships.

- Smart Lighting and IoT Integration Premium Segment: India's smart lighting market is a high-growth adjacent opportunity, with occupancy sensors, daylight harvesting, app-based controls, and building management system integration commanding significant price premiums over commodity LED.

- Horticulture and Specialty Lighting Applications: India's expanding controlled environment agriculture, cold storage infrastructure, and pharmaceutical facility segment is creating demand for specialized spectrum-tuned LED grow lights and hygiene-compliant cleanroom luminaires.

Market Challenges

- Quality and Standards Compliance: Bureau of Indian Standards Quality Control Orders have made IS certification compulsory, raising entry barriers for grey-market imports. Enforcing compliance across the long tail of unorganized distributors and regional assemblers continues to challenge established players whose products compete against non-compliant lower-priced alternatives in price-sensitive segments.

- Talent for Smart Lighting Systems Integration: Deploying IoT-enabled LED systems requires electrical engineering expertise combined with software integration capabilities that remain scarce in Tier-2 and Tier-3 city installation contractor ecosystems. Workforce capability development for commissioning and maintaining intelligent lighting infrastructure represents a structural challenge for market-wide smart lighting adoption.

Emerging Market Trends

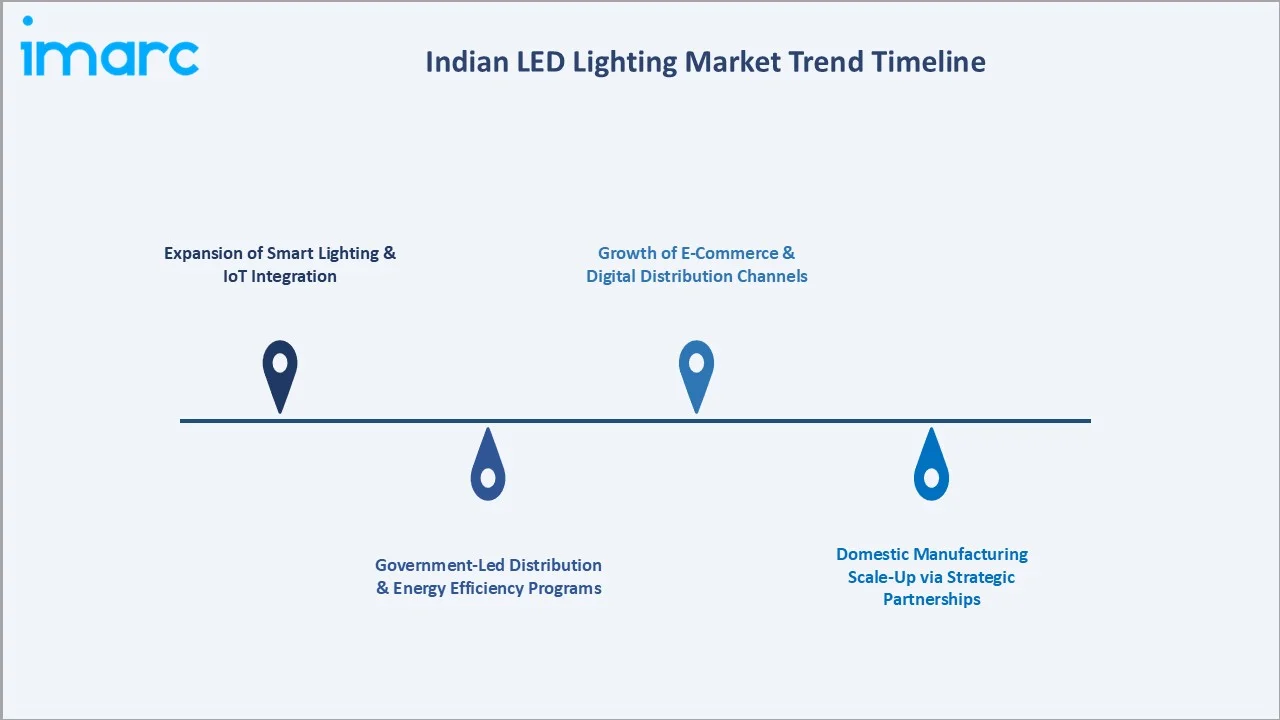

1. Expansion of Smart Lighting and IoT Integration

Companies are developing human-centric lighting solutions that adjust color temperature and intensity to support occupant wellbeing and workplace productivity. The convergence of smart lighting with 5G infrastructure, exemplified by smart poles combining LED luminaires with small cells and environmental sensors, is creating data-rich urban infrastructure assets that extend far beyond basic illumination functionality.

2. Government-Led Distribution and Energy Efficiency Programs

UJALA scheme reduced LED bulb prices from INR 310 to INR 38.45 through demand aggregation, distributing over 36.87 crore LED units nationally. Energy Efficiency Services Limited had installed over 1.34 crore LED streetlights across Urban Local Bodies and Gram Panchayats by January 2025, achieving annual energy savings exceeding 9,001 million units.

3. Domestic Manufacturing Scale-Up Through Strategic Partnerships

In March 2025, Signify and Dixon Technologies announced a proposed 50:50 joint venture to build domestic LED manufacturing capacity for bulbs, battens, downlights, strips, and accessories, pairing Signify's global lighting IP with Dixon's manufacturing scale under the Make in India policy alignment. The September 2024 PLI outlay increase to INR 444.54 crore for FY 2025–26 reinforces incentives for LED component localization.

4. Growth of E-Commerce and Digital Distribution Channels

Online platforms recorded a 9.2% CAGR between 2024 and 2025, fueled by smartphone penetration and cashless payment adoption. E-commerce channels prove particularly effective for smart bulbs and IoT-enabled lighting kits that require consumer education and comparison shopping before purchase.

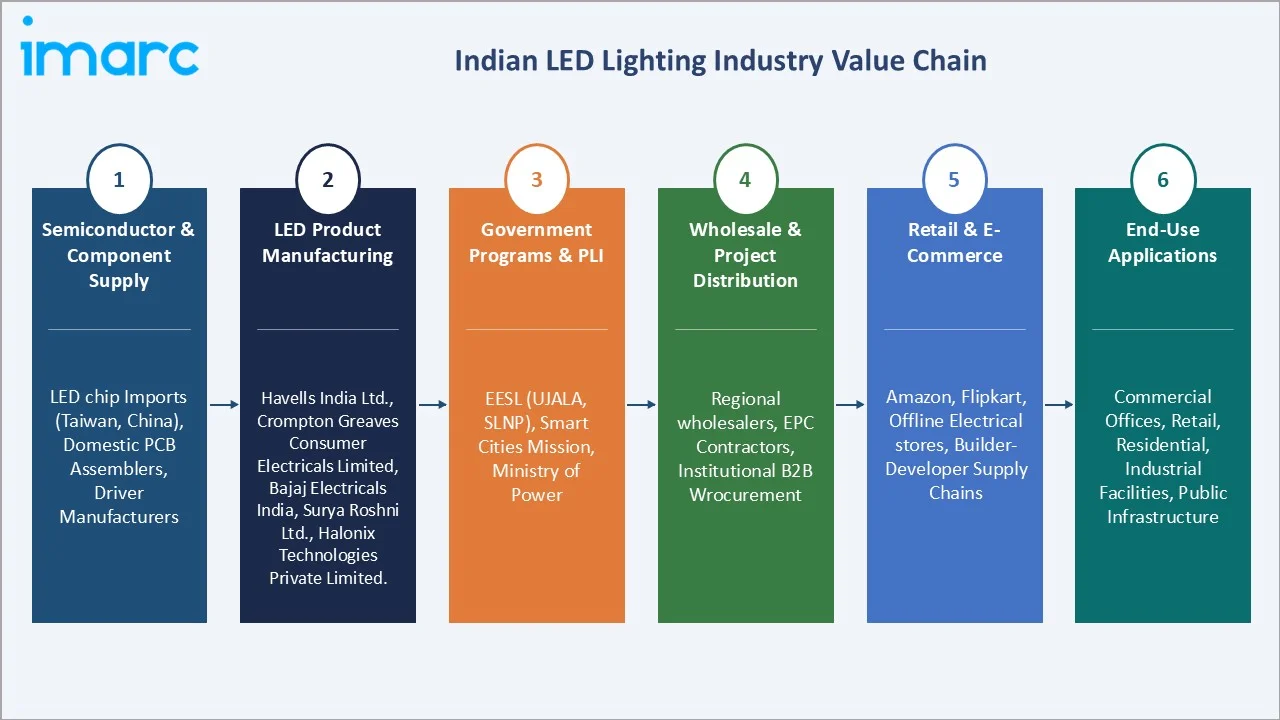

Industry Value Chain Analysis

The Indian LED lighting value chain spans semiconductor component supply through end-user application, with each stage influenced by government policy, import economics, and the competitive dynamics between domestic manufacturers and international technology leaders.

|

Stage |

Key Players / Examples |

|

Semiconductor & Component Supply |

LED chip imports (Taiwan, China), domestic PCB assemblers, driver manufacturers |

|

LED Product Manufacturing |

Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Bajaj Electricals India, Surya Roshni Ltd., Halonix Technologies Private Limited. |

|

Government Programs & PLI |

EESL (UJALA, SLNP), Smart Cities Mission, Ministry of Power |

|

Wholesale & Project Distribution |

Regional electrical wholesalers, EPC contractors, and institutional B2B procurement |

|

Retail & E-Commerce |

Amazon, Flipkart, offline electrical stores, and builder-developer supply chains |

|

End-Use Applications |

Commercial offices, retail, residential, industrial facilities, and public infrastructure |

Technology Landscape in the Indian LED Lighting Industry

Smart Lighting and IoT-Connected Systems

Signify introduced its SpaceSense Wi-Fi sensing technology through the WiZ lighting system, enabling lights to automatically detect motion and operate without the need for additional sensors or hardware. Building management system integration enables energy optimization, occupancy analytics, and predictive maintenance for large commercial facilities. Smart poles combining LED, 5G small cells, and EV charging points represent an emerging high-value urban infrastructure category attracting telecom co-financing.

Human-Centric Lighting Technology

Human-centric lighting systems that adjust color temperature (from 2700K warm white to 6500K daylight) and intensity based on time of day and circadian rhythm requirements are gaining adoption in premium office, healthcare, and educational facilities. Research demonstrating measurable improvements in occupant alertness, sleep quality, and productivity is accelerating adoption among corporate real estate developers and hospital design consultants.

High-Efficiency LED Technology and Energy Standards

In August 2022, Signify introduced an A-class LED tube consuming 60% less energy than standard Philips LED through technological innovation, meeting EU A-grade eco-design criteria. Bureau of Indian Standards Quality Control Orders (IS 16103-2 certification) are raising minimum performance thresholds for market-eligible products, progressively eliminating sub-standard imports and driving the installed base toward higher-efficiency luminaires.

Advanced Manufacturing Technology

PLI-incentivized facilities in Gujarat and Tamil Nadu are deploying automated SMT assembly lines, robotic soldering systems, and integrated optical testing equipment that match global quality standards while achieving cost structures competitive with imports. This manufacturing capability development positions India as an emerging export base for LED products targeting Southeast Asian and African markets.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Panel Lights |

26.0% |

2025 |

|

Application |

Commercial Applications |

30.0% |

2025 |

By Product Type

Panel lights dominate the product-type segment with a 26.0% share in 2025. Their dominance reflects extensive adoption across contemporary commercial offices, retail establishments, healthcare facilities, and institutional buildings seeking uniform, glare-free illumination with high energy efficiency. Panel lights offer aesthetic integration with modern false-ceiling architectures while delivering luminous efficacy that significantly outperforms fluorescent alternatives.

To access detailed market analysis, Request Sample

Down lights hold a 20.0% share, widely used in residential, hotel, and premium retail applications for accent and ambient lighting. Tube lights at 18.0% remain significant in industrial and institutional retrofits, replacing fluorescent battens. Street lights at 15.0% represent the fastest-growing product category, driven by sustained government procurement.

By Application

Commercial applications lead the market with a 30.0% share in 2025, driven by the rapid expansion of office spaces, retail establishments, hospitality venues, and healthcare facilities across India's major metropolitan markets. The implementation of Energy Conservation Building Code standards creates mandatory compliance requirements for high-efficiency LED installations in new commercial construction.

Residential applications represent 28.0%, growing as household LED penetration deepens beyond bulb replacement into complete lighting refurbishment of living spaces and smart home integration. Industrial applications hold 25.0%, driven by high-bay LED upgrades in manufacturing plants, warehouses, and logistics facilities.

Competitive Landscape

The Indian LED lighting market exhibits a moderately fragmented competitive structure with multinational technology leaders competing alongside domestic manufacturers leveraging established distribution networks, government procurement relationships, and Make in India manufacturing incentives.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Signify Holding |

Philips / WiZ |

Market Leader |

Global LED IP; smart lighting technology; Signify-Dixon JV for India manufacturing |

|

Havells India Ltd. |

Havells |

Market Leader |

Pan-India distribution; diverse product portfolio; premium brand positioning |

|

Crompton Greaves Consumer Electricals Limited |

Crompton |

Strong Challenger |

Value-segment leadership; nationwide dealer network; strong tier-2/3 presence |

|

Bajaj Electricals India |

Bajaj Electricals |

Strong Challenger |

Brand equity; smart infrastructure partnerships; tunnel & specialty lighting focus |

|

Surya Roshni Ltd. |

Surya |

Challenger |

Cost-competitive manufacturing; strong North India distribution; street lighting |

|

Halonix Technologies Private Limited |

Halonix |

Challenger |

BIS-certified quality products; domestic manufacturing; institutional supply focus |

Signify and Havells collectively hold the leading market share positions, with Crompton Greaves, Bajaj Electricals, Surya Roshni, and Halonix comprising the strong challenger tier. The top six players collectively account for an estimated 50–55% of organized market revenue in 2025.

Key Company Profiles

Signify Holding

Signify Holding, headquartered in Eindhoven, Netherlands, is the world's largest LED lighting company and India's premium lighting market leader. Signify combines global R&D capabilities with growing domestic manufacturing through strategic partnerships.

- Product Portfolio: Philips LED bulbs, battens, downlights, panel lights; WiZ smart lighting ecosystem; specialty horticulture and human-centric lighting solutions.

- Recent Developments: In March 2025, Signify and Dixon Technologies announced a proposed 50:50 joint venture for domestic manufacturing of LED solutions, bulbs, battens, downlights, strips, and accessories.

- Strategic Focus: Smart and connected lighting leadership; domestic manufacturing scale-up through Dixon JV; IoT platform development; premium institutional and smart city project capture.

Havells India Ltd.

Havells India Ltd., headquartered in Noida, is one of India's largest and most diversified fast-moving electrical goods manufacturers, with a comprehensive LED lighting portfolio spanning consumer, commercial, and industrial segments.

- Product Portfolio: LED bulbs, panel lights, downlights, battens, street lights, smart lighting, high-bay luminaires, and decorative LED fixtures across price tiers from value to premium segments.

- Recent Developments: Havells India reported a 7.9% year‑on‑year increase in consolidated net profit to INR 300.05 crore for the quarter ended December 31, 2025, up from INR 277.96 crore a year ago.

- Strategic Focus: Premium brand positioning; backward integration for margin protection; smart home ecosystem expansion; PLI-incentivized manufacturing capacity enhancement; export market development.

Crompton Greaves Consumer Electricals Limited

Crompton Greaves Consumer Electricals, headquartered in Mumbai, is a leading Indian consumer electricals brand with a strong value-to-mid-tier LED lighting portfolio. The company leverages digital storefronts and Tier-2/3 distribution expansion to deepen market reach beyond metropolitan markets.

- Product Portfolio: LED bulbs, tube lights, panel lights, downlights, streetlights, battens, and smart LED products under the Crompton brand across consumer, commercial, and institutional segments.

- Recent Developments: Installed over 2,000 high‑efficiency LED streetlights on more than 1,300 poles along a 42 km stretch of Bengaluru’s Satellite Town Ring Road, cutting energy use by up to 50% while improving road visibility and safety.

- Strategic Focus: Tier-2 and Tier-3 geographic expansion; digital omnichannel capability; value segment leadership; institutional and government supply relationship strengthening.

Market Concentration Analysis

The Indian LED lighting market exhibits moderate fragmentation, with the top six organized-sector players collectively holding an estimated 50–55% of market revenue in 2025. The balance is accounted for by a large population of regional assemblers, unorganized manufacturers, and grey-market importers, particularly in lower-tier product categories. BIS Quality Control Orders are progressively raising entry barriers for non-compliant producers, gradually consolidating market share toward certified manufacturers.

The PLI-incentivized joint venture and manufacturing expansion cycle is creating capital investment momentum that will reshape competitive dynamics through 2030. The Signify-Dixon JV announced in March 2025 exemplifies a broader trend of global IP holders partnering with domestic manufacturers to secure PLI eligibility and tariff advantage, creating new competitive entities that combine international technology with local cost structures.

Investment & Growth Opportunities

Fastest Growing Segments

Smart lighting systems (CAGR ~25%), LED street lights (CAGR ~21.2%), and commercial panel lights (CAGR ~20.8%) represent the three highest-growth investment vectors through 2034. Together, these priority segments address a total addressable incremental opportunity of approximately USD 8–10 Billion by 2030, supported by sustained government infrastructure spending, Smart Cities Mission Phase 2 deployments, and rapid commercial real estate expansion.

Emerging Market Expansion

East India and Tier-3 city markets represent the most under-penetrated domestic geographies, with rising infrastructure investment in Bhubaneswar, Patna, and Ranchi creating market activation opportunities. The PLI scheme manufacturing clusters in Gujarat and Tamil Nadu create adjacent investment opportunities in LED driver, PCB, and optical component manufacturing.

Venture and Institutional Investment Trends

- Key investment themes include smart lighting IoT platform development, LED component manufacturing localization under PLI, energy-as-a-service models for commercial lighting retrofits, and agricultural spectrum-tuned grow-light applications for India's expanding controlled environment agriculture sector.

- Government-backed ESCO financing models through Energy Efficiency Services Limited create investable demand-side opportunities, enabling upfront capital deployment with structured government payment guarantee frameworks for large institutional LED retrofits.

Future Market Outlook (2026-2034)

The Indian LED lighting market is positioned for exceptional, sustained growth through 2034. From a base of USD 6.00 Billion in 2025, the market is projected to reach USD 27.81 Billion by 2034, representing total incremental value creation of approximately USD 21.81 Billion over the forecast decade.

Policy evolution, the Smart Cities Mission Phase 2 deployment, BIS quality compliance enforcement, eliminating sub-standard imports, PLI-driven domestic manufacturing scale-up, and progressive Energy Conservation Building Code tightening, will drive simultaneous volume growth and product mix premiumization.

Long-term, the Indian LED lighting market trends are tied to three structural macro-themes: India's urban infrastructure investment creating massive public lighting procurement volumes, the commercial real estate and Smart Cities Mission generating consistent high-specification building lighting demand, and the digital transformation of Indian households accelerating smart home IoT-enabled lighting adoption.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys conducted in 2024–2025 with LED lighting manufacturers, EPC contractors, government energy efficiency agency representatives, commercial real estate developers, institutional facility managers, and retail consumers across North, South, West, and East India.

Secondary Research

Secondary research encompassed review of Ministry of Power publications, Bureau of Energy Efficiency reports, Smart Cities Mission implementation data, Energy Efficiency Services Limited UJALA and SLNP program statistics, Bureau of Indian Standards quality order notifications, PLI scheme Ministry of Heavy Industries circulars, and industry association data from the Electric Lamp and Component Manufacturers' Association of India.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating urbanization rates, commercial construction activity indices, government LED procurement volumes, per-capita lighting consumption evolution, and historical segment-level revenue trajectories. A base-case CAGR of 18.58% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates and government program procurement data.

Indian LED Lighting Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Panel Lights, Down Lights, Street Lights, Tube Lights, Bulbs, Others |

| Applications Covered | Commercial Applications, Residential Applications, Institutional Applications, Industrial Applications |

| Companies Covered | Signify Holding, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Bajaj Electricals India, Surya Roshni Ltd., Halonix Technologies Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian LED Lighting Market Report

The Indian LED lighting market size was valued at USD 6.00 Billion in 2025. It is projected to reach USD 27.81 Billion by 2034, growing at a CAGR of 18.58% during the forecast period of 2026-2034.

The Indian LED lighting market is expected to grow at a CAGR of 18.58% during the forecast period from 2026-2034, driven by government energy efficiency programs, Smart Cities Mission deployments, PLI-incentivized domestic manufacturing, and rising demand for smart IoT-connected lighting solutions.

North India leads the market with approximately 34.0% revenue share in 2025, driven by large-scale Smart Cities Mission deployments in Delhi-NCR, extensive government institutional LED upgrades across Uttar Pradesh and Punjab, and high commercial real estate activity in Gurugram and Noida technology corridors.

Panel lights dominate the product-type segment with a 26.0% share in 2025, valued at approximately USD 1.56 Billion, reflecting extensive adoption in commercial offices, retail establishments, and institutional buildings.

Commercial applications lead the market at 30.0% in 2025, driven by rapid expansion of office spaces, retail chains, hospitality venues, and healthcare facilities implementing Energy Conservation Building Code mandates that require high-efficiency LED installations in new and renovated commercial structures.

Key drivers include UJALA scheme distributing 36.87 crore LED units nationally, EESL's 1.34 crore LED streetlight installations saving 9,001 MU annually, Smart Cities Mission IoT lighting deployments, PLI scheme allocating INR 444.54 crore for LED component manufacturing, Signify-Dixon JV domestic manufacturing expansion (March 2025), and Energy Conservation Building Code compliance mandates.

Key players in the Indian LED lighting market include Signify Holding, Havells India Ltd., Crompton Greaves Consumer Electricals Limited, Bajaj Electricals India, Surya Roshni Ltd., and Halonix Technologies Private Limited.

Key challenges include high upfront costs for large commercial and industrial LED installations, rural market awareness and affordability gaps constraining household penetration, and enforcement complexity for BIS quality compliance across the large unorganized sector.

Significant opportunities exist in smart IoT-connected lighting system development, PLI-incentivized LED component manufacturing localization, ESCO-financed commercial retrofit programs, and distribution network expansion into underserved Tier-3 and East India markets through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)