Indian Mobile Components Manufacturing and Assembly Market Size, Share, Trends and Forecast by Mobile Type, Mobile Components, Assembly and Domestic Manufacturing, and Region, 2026-2034

Indian Mobile Components Manufacturing and Assembly Market Size, Share, Trends & Forecast (2026-2034)

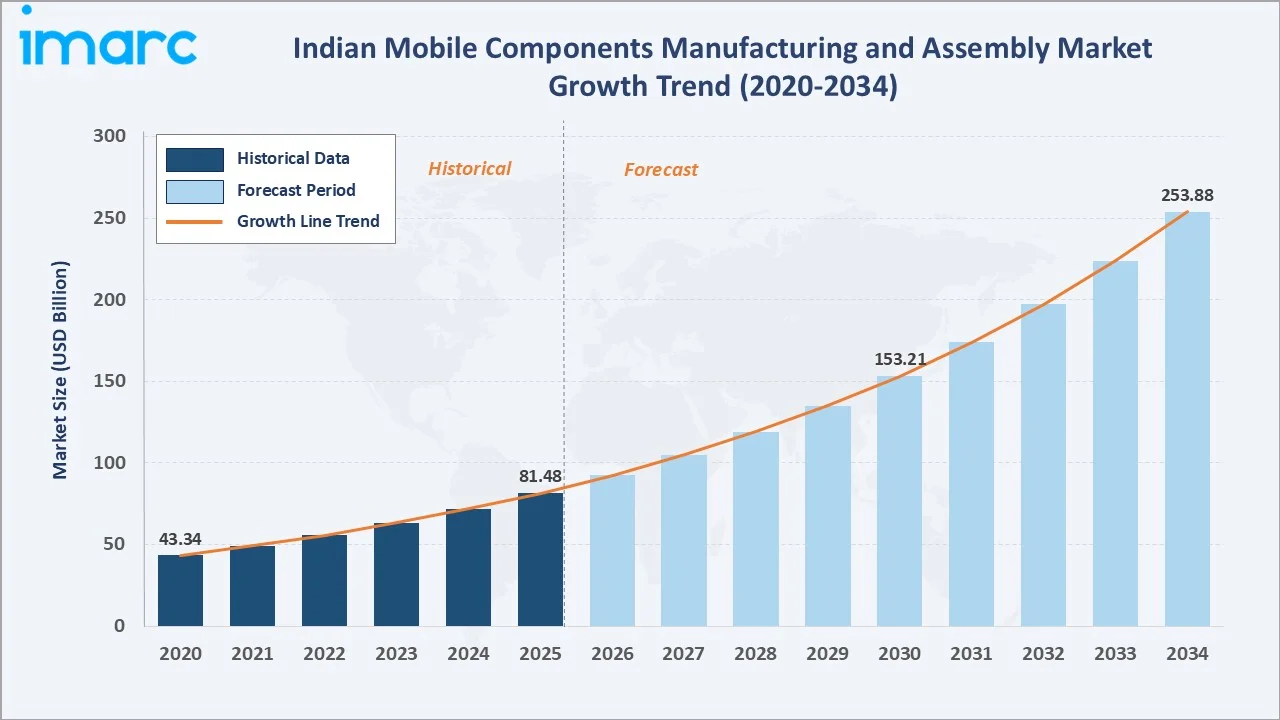

The Indian mobile components manufacturing and assembly market reached USD 81.48 Billion in 2025 and is projected to reach USD 253.88 Billion by 2034, growing at a CAGR of 13.46% during 2026-2034. Strong government support under the Production Linked Incentive (PLI) scheme, rising smartphone penetration exceeding 750 million subscribers, growing domestic consumption replacing imports, and India’s emergence as a global manufacturing hub for premium smartphones are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 81.48 Billion |

|

Forecast Market Size (2034) |

USD 253.88 Billion |

|

CAGR (2026-2034) |

13.46% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

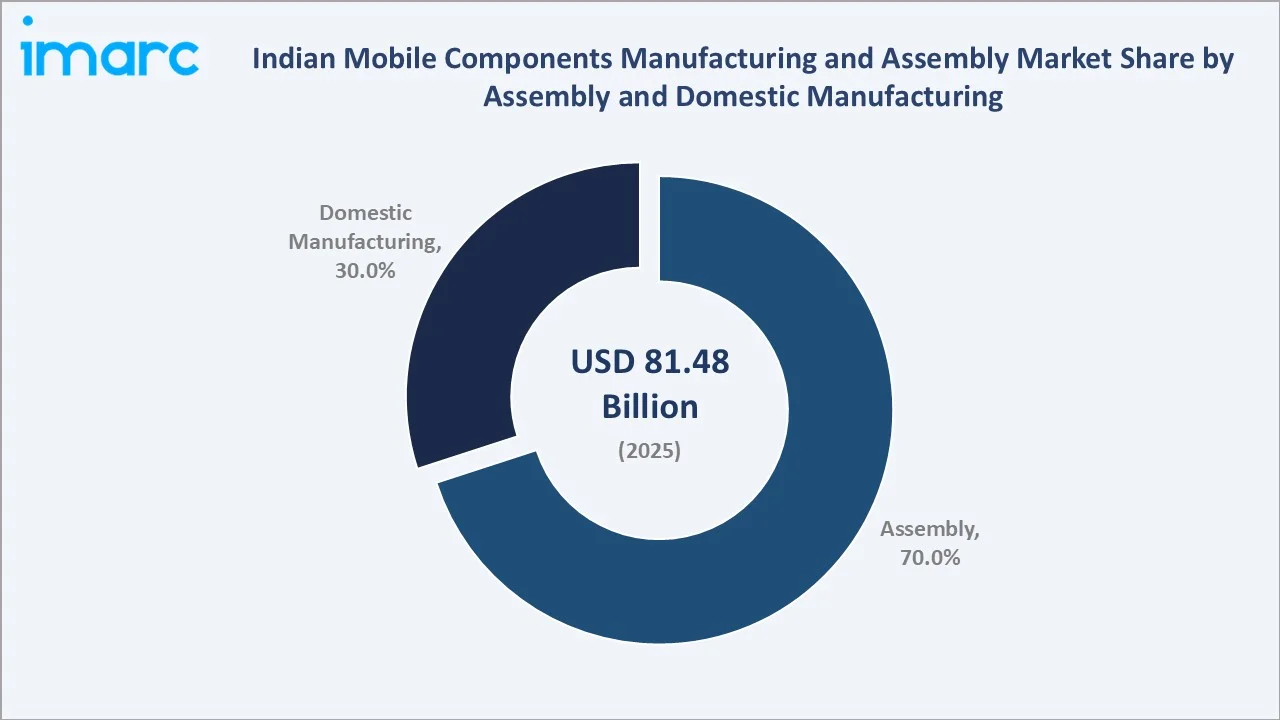

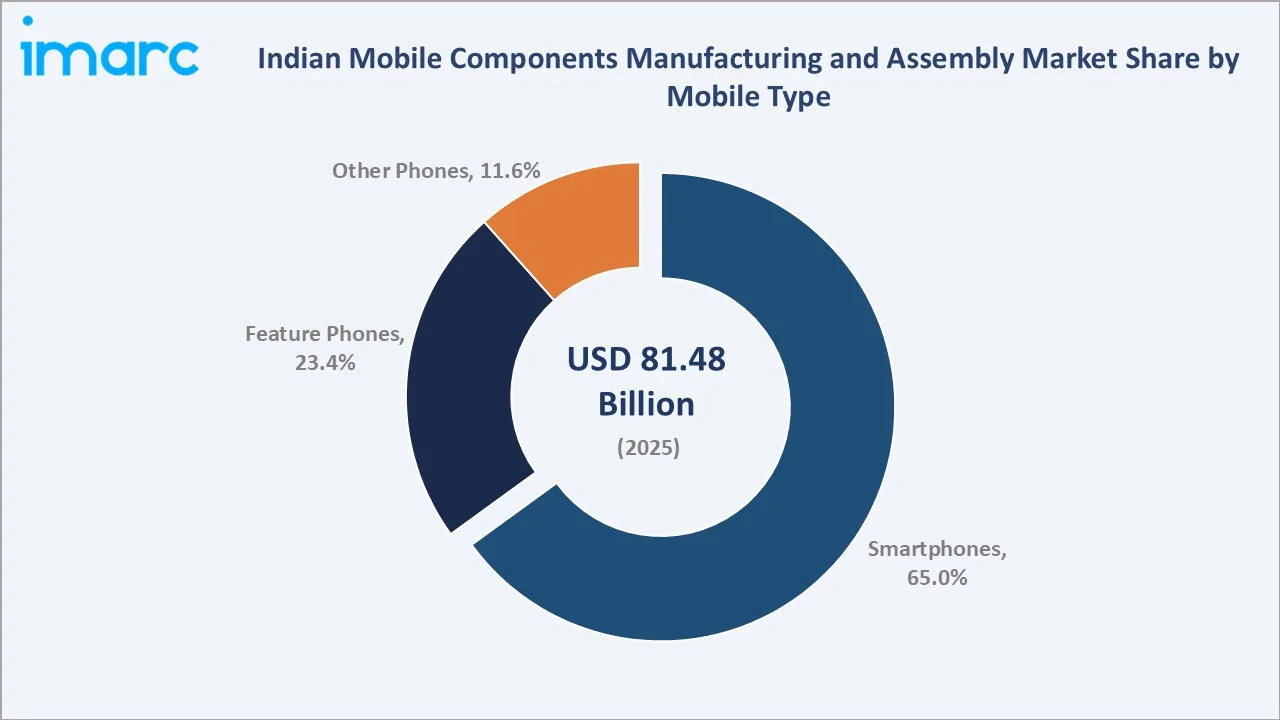

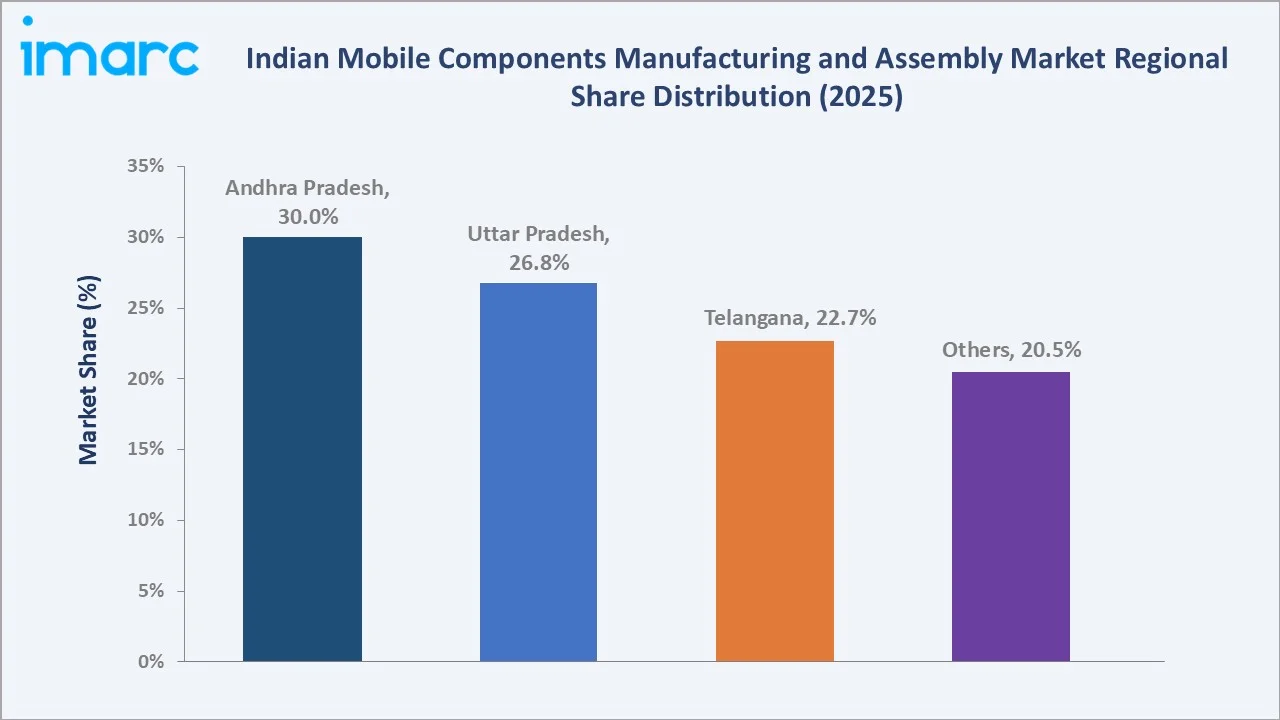

Andhra Pradesh leads regionally with a 30.0% market share in 2025, anchored by large-scale assembly facilities at Sri City SEZ and state-level incentives offering up to 25% capital subsidies. The assembly segment commands a dominant 70.0% share of the market, while smartphones retain the largest share among mobile types at 65.0% in 2025.

To get more information on this market, Request Sample

India’s mobile components market is underpinned by three structural forces: the PLI scheme accelerating domestic value addition, rising export orientation as Apple and Samsung scale India-based manufacturing, and deepening supply chain localization replacing Chinese imports across battery, display, and PCB segments.

Executive Summary

The Indian mobile components manufacturing and assembly market is experiencing robust, broad-based expansion driven by the convergence of policy-driven manufacturing incentives, surging domestic smartphone demand, and global supply chain realignment toward India. The market was valued at USD 81.48 Billion in 2025 and is forecast to reach USD 253.88 Billion by 2034, growing at a CAGR of 13.46%. This trajectory is anchored by India’s smartphone connections, which are projected to surpass 1.2 billion by 2030.

The assembly segment dominates with a 70.0% share in 2025, driven by large-scale contract manufacturers operating for Apple, Samsung, and Xiaomi. However, domestic manufacturing is growing fastest at an estimated 15.12% CAGR as value-added component production, spanning displays, batteries, camera modules, and PCBs, deepens in Andhra Pradesh, Uttar Pradesh, and Telangana.

Smartphones lead the mobile type segment at 65.0% of 2025 market value, benefiting from average selling price upgrades, 5G adoption accelerating to around 970 million subscriptions, and India’s premium segment growing at 18–22% annually. Key players, including Samsung, Xiaomi, Lenovo, Lava International Limited, and Micromax Informatics Ltd., collectively shape the competitive landscape through continuous supply chain investment and government partnership programs.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Assembly vs Manufacturing) |

Assembly – 70.0% share (2025) |

|

Fastest Growing Segment |

Domestic Manufacturing – ~15.12% CAGR (2026-2034) |

|

Largest Mobile Type |

Smartphones – 65.0% share (2025) |

|

Fastest Growing Mobile Type |

Smartphones – ~14.40% CAGR (2026-2034) |

|

Leading Region |

Andhra Pradesh – 30.0% share (2025) |

|

Top Companies |

Samsung, Xiaomi, Lenovo, Lava International Limited, and Micromax Informatics Ltd. |

Key Analytical Observations Supporting the Above Data:

- Assembly commands 70.0% of India’s mobile components market in 2025. This dominance reflects the PLI scheme’s initial phase focus on device assembly, with eligible manufacturers receiving incentives of 4–6% on incremental sales.

- Domestic manufacturing at 30.0% share (2025) is growing fastest because the government’s PMP imposes escalating import duties on sub-assemblies and components, compelling OEMs to localize production.

- Smartphones account for 65.0% of market value in 2025, driven by India’s premium smartphone shipments growing 11% year-on-year. Apple’s India production reached USD 22 Billion in FY2024–25, a 60% increase from the prior year, providing a structural demand anchor for the high-value assembly sub-chain.

- Andhra Pradesh’s 30.0% regional share reflects concentration of large-scale mobile assembly facilities in Sri City and Visakhapatnam SEZs, state capital subsidy programs offering up to 25% on fixed capital investment, and dedicated infrastructure with port connectivity for component imports and device exports.

Indian Mobile Components Manufacturing and Assembly Market Overview

Mobile components manufacturing and assembly encompasses design, fabrication, and final assembly of hardware components integrated into mobile devices, including smartphones, feature phones, and other mobile terminals. India’s market spans the complete value chain from raw component imports and domestic manufacturing of sub-assemblies (PCBs, displays, batteries, cameras, mechanical parts) through final device assembly, quality testing, and packaging for domestic sale and export.

India’s market is structurally supported by strong macroeconomic tailwinds. The 5G smartphone installed base crossed 750 million in 2028, with the 5G subscriber base expected to reach 970 million by 2030. The Indian government is expected to introduce a new production-linked incentive (PLI) scheme for mobile phones by May, with a proposed allocation exceeding USD 5 billion (around Rs 46,000 crore) to strengthen domestic manufacturing and increase mobile phone exports.

Market Dynamics

To evaluate market opportunities, Request Sample

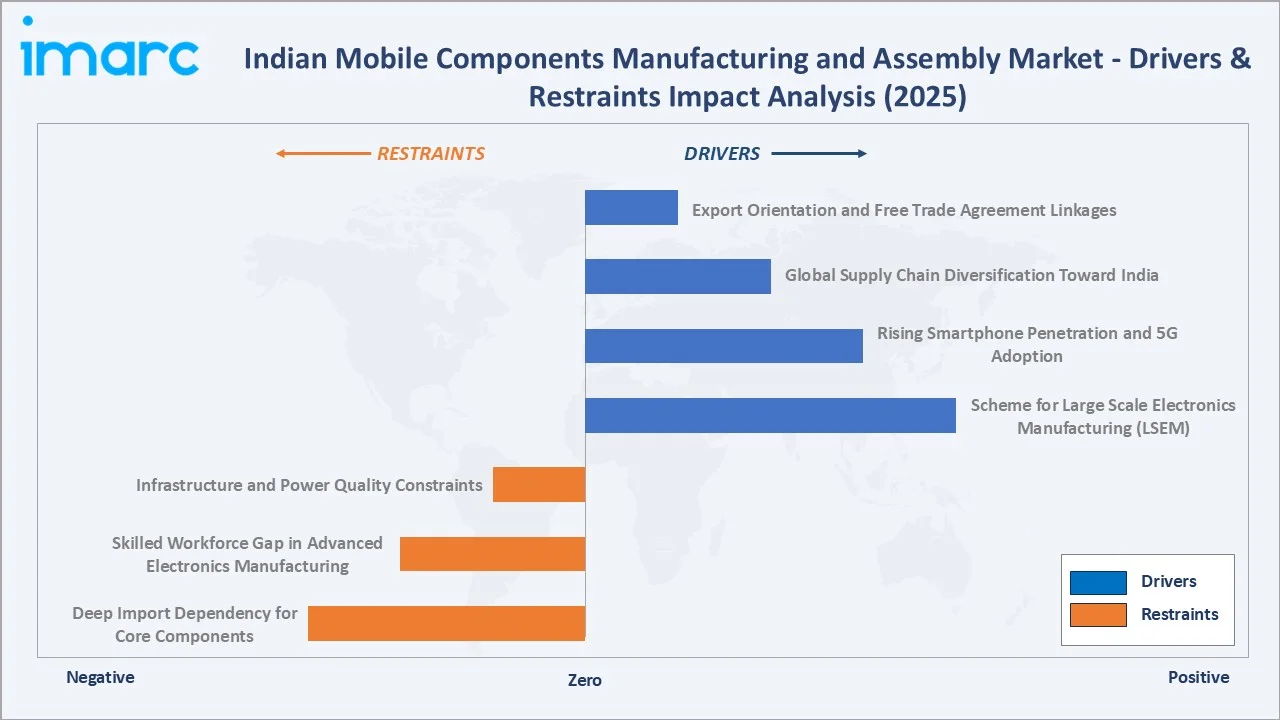

Market Drivers

- Scheme for Large Scale Electronics Manufacturing (LSEM): The Scheme for Large Scale Electronics Manufacturing (LSEM), introduced in 2020, aimed to strengthen domestic mobile phone manufacturing in India through an incentive outlay of INR 40,995 crore (~USD 5.7 billion) based on the prevailing exchange rates at the time.

- Rising Smartphone Penetration and 5G Adoption: According to a recent Ericsson report, India’s 5G subscriber base is expected to expand nearly threefold and reach 970 million by 2030, accounting for around 74% of the country’s total mobile subscribers. The 5G smartphone average selling price of USD 250–350 is 2.4× the feature phone equivalent, directly expanding total component value per device.

- Global Supply Chain Diversification Toward India: Apple’s India production surged to USD 22 Billion in FY2024–25 as Foxconn, Pegatron, and Tata Electronics expanded assembly capacity in Tamil Nadu and Karnataka. Samsung’s Noida plant increased premium smartphone production to 70 million units per annum in 2025. Google’s Pixel 9 India production and OnePlus’s Greater Noida facility signal accelerating global OEM commitment to India as a China-alternative manufacturing base.

- Export Orientation and Free Trade Agreement Linkages: India’s mobile phone exports crossed USD 25 Billion in FY2024–25. The UAE CEPA and UK FTA provide preferential access for Indian-manufactured devices in high-value markets. Export-oriented PLI beneficiaries must maintain a minimum export-to-production ratio of 60%, structurally linking India’s mobile component growth to global trade volumes.

Market Restraints

- Deep Import Dependency for Core Components: India currently imports approximately 65–70% of display panels and 70-80% of camera sensors by value from China, South Korea, and Taiwan. India’s smartphone average selling prices (ASPs) are anticipated to increase by 8–10% over 2026, with the most significant price hikes expected in devices priced below Rs 12,000.

- Skilled Workforce Gap in Advanced Electronics Manufacturing: India faces a deficit of approximately 10 million trained electronics manufacturing engineers by 2027. High-precision operations, including SMT, PCBA soldering, and optical bonding, require specialized technical training not yet delivered at sufficient scale by India’s ITI and polytechnic networks.

- Infrastructure and Power Quality Constraints: Mobile component manufacturing demands power supply reliability with below 2 minutes annual downtime for SMT lines. Tier-2 cities targeted for manufacturing diversification face average power reliability of 97–98%, below the 99.9%+ standard required for advanced electronics production.

Market Opportunities

- Semiconductor and Display Fab Investment: Backed by the India Semiconductor Mission and an investment outlay of INR 76,000 crore, the country has witnessed the establishment of multiple semiconductor fabrication and design facilities, strengthening its path toward technological self-reliance and lower import dependency.

- Camera and Optical Component Localization: India imports 80%+ of smartphone camera modules, representing a USD 6–8 Billion annual opportunity for domestic suppliers. Rising multi-camera configurations (3–5 cameras per premium smartphone) and periscope telephoto lens adoption create strong incentives for local optical assembly investment.

Market Challenges

- Counterfeit Components and Quality Enforcement: India’s rapid manufacturing scale-up has created gray market infiltration of counterfeit batteries, display assemblies, and PCB components estimated at 5–8% of after-market volume. Substandard components create safety hazards and inflate warranty costs for legitimate OEMs, while BIS quality control order enforcement remains inconsistent.

- Working Capital Intensity and Supply Chain Financing: Mobile component assembly operates on working capital cycles of 45–60 days. MSMEs comprising 70%+ of India’s component tier face financing rates of 12–14% versus 4–6% for their Chinese counterparts, creating a structural cost disadvantage at OEM negotiation stages.

Emerging Market Trends

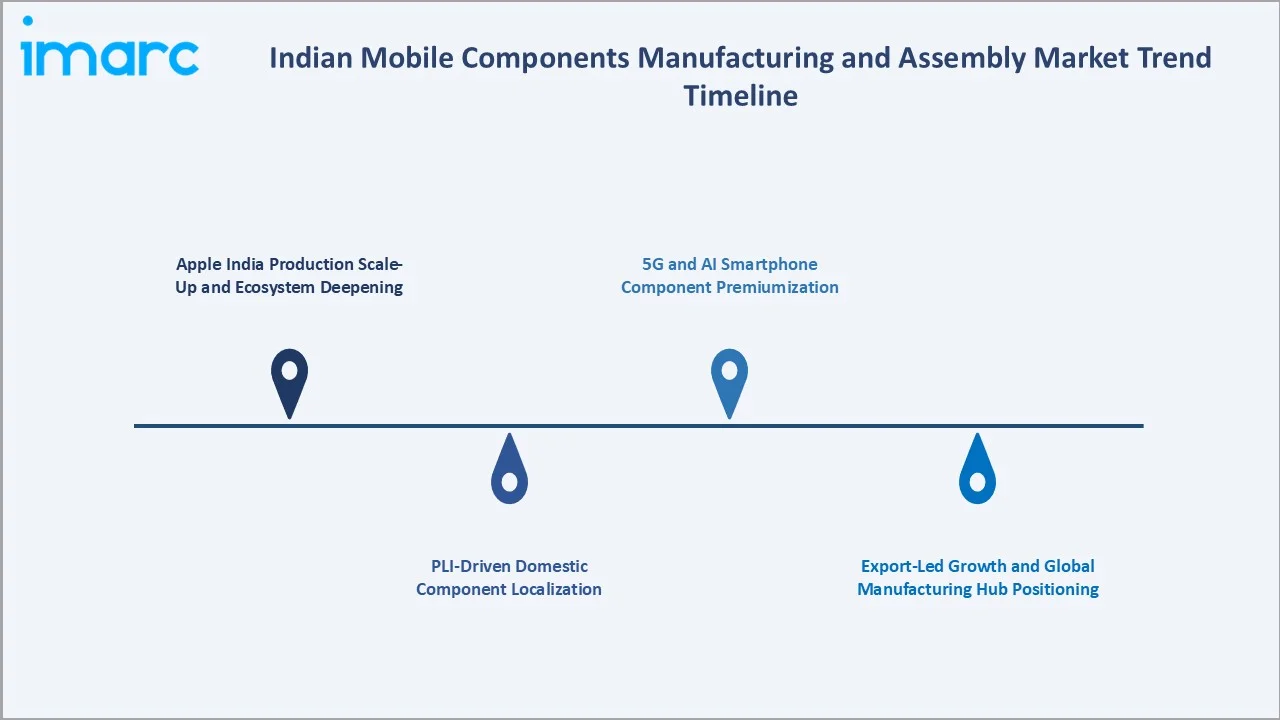

1. Apple India Production Scale-Up and Ecosystem Deepening

Apple Inc. assembled iPhones worth nearly USD 22 billion in India during FY2024–25, marking an increase of almost 60% compared to the previous year. Foxconn’s expansion in Sriperumbudur (Tamil Nadu) and Tata Electronics’ Narasapura plant are catalyzing a Tier-2 supplier ecosystem in South India, with 60+ Apple-qualified component suppliers expected to establish India operations by 2026.

2. PLI-Driven Domestic Component Localization

The PLI scheme’s Phase 2 component focus is incentivizing domestic production of displays (BOE and Foxconn display ventures), batteries (Tata Chemicals initiative), and acoustics (AAC Technologies India factory). According to the Ministry of Electronics and Information Technology (MeitY), domestic value addition has increased to nearly 18–20%, with smartphones contributing around INR 5.5 lakh crore in output and emerging as the key driver of growth in the electronics manufacturing sector.

3. Export-Led Growth and Global Manufacturing Hub Positioning

Smartphone exports increased by 58% to reach USD 13.38 billion, compared to USD 8.47 billion recorded during the same period in 2024. Samsung’s Noida facility has designated India as its primary manufacturing base for the Galaxy A-series globally, while Apple is actively qualifying Indian-made iPhones for export to Europe and the Middle East via the 0% tariff India–UAE CEPA route.

4. 5G and AI Smartphone Component Premiumization

India’s smartphone average selling price increased from USD 220 in 2023 to USD 250 in 2025 as consumers upgrade to AI-capable handsets with on-device ML processors, advanced camera arrays, and larger OLED displays. This ASP inflation is expanding the component bill of materials from USD 180 per device to USD 240–260, directly growing the addressable market for Indian assembly and component suppliers beyond volume growth alone.

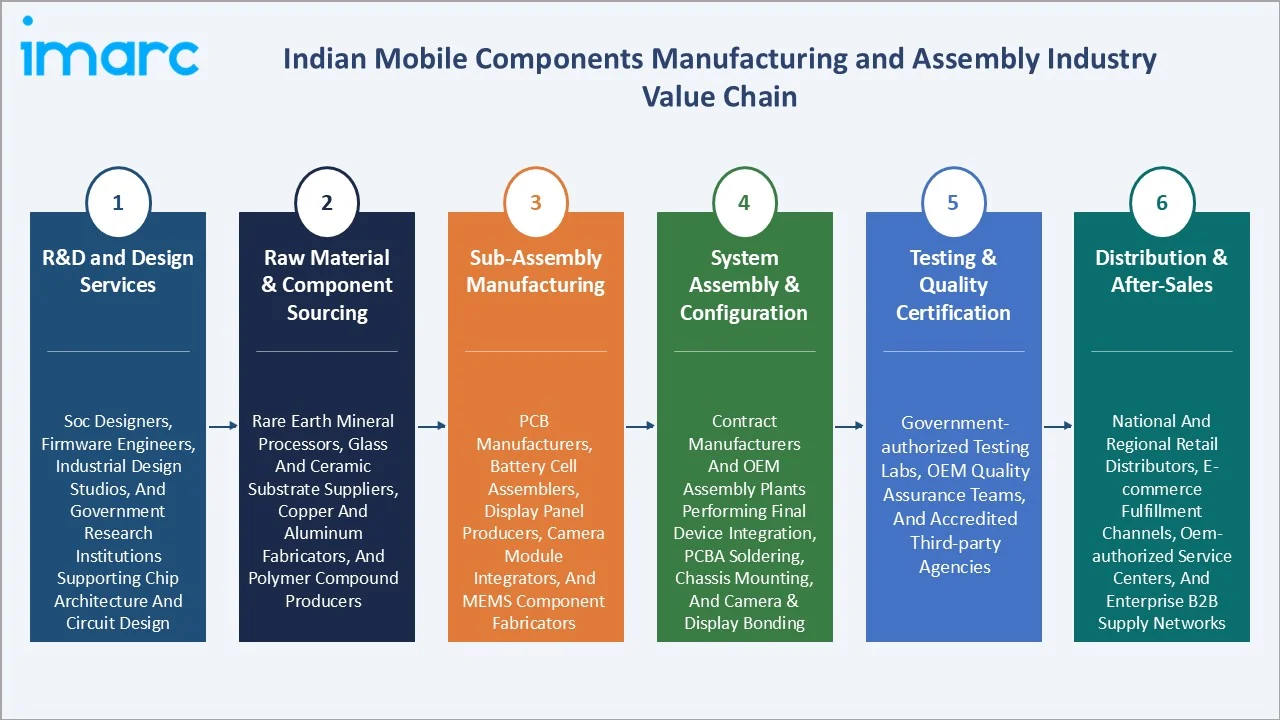

Industry Value Chain Analysis

India’s mobile components manufacturing and assembly value chain spans raw material and semiconductor procurement through end-user device distribution, with each stage occupied by specialized global OEMs, contract manufacturers, component suppliers, and domestic integrators.

|

Stage |

Key Participants / Examples |

|

R&D and Design Services |

SoC designers, firmware engineers, industrial design studios, and government research institutions supporting chip architecture and circuit design |

|

Raw Material & Component Sourcing |

Rare earth mineral processors, glass and ceramic substrate suppliers, copper and aluminum fabricators, and polymer compound producers |

|

Sub-Assembly Manufacturing |

PCB manufacturers, battery cell assemblers, display panel producers, camera module integrators, and MEMS component fabricators serving mobile OEMs |

|

System Assembly & Configuration |

Contract manufacturers and OEM assembly plants performing final device integration, PCBA soldering, chassis mounting, and camera & display bonding |

|

Testing & Quality Certification |

Government-authorized testing labs, OEM quality assurance teams, and accredited third-party agencies |

|

Distribution & After-Sales |

National and regional retail distributors, e-commerce fulfillment channels, OEM-authorized service centers, and enterprise B2B supply networks |

Technology Landscape in the Indian Mobile Components Manufacturing Industry

Display Module Technology

India’s display module assembly is transitioning from LCD to AMOLED/OLED, with Samsung Display’s Noida facility and BOE Technology’s proposed India plant targeting domestic supply for premium smartphones. AMOLED displays command 3–4× the unit value of LCD panels (USD 45–80 per unit vs USD 15–25), driving disproportionate value creation in the display sub-segment as India’s premium smartphone shipments grow.

Battery Pack and Cell Manufacturing

India’s battery pack assembly (combining imported cells with domestic housings and BMS electronics) represents a current localization of approximately 40% domestic content. The PLI-linked Advanced Chemistry Cell (ACC) scheme has committed INR 18,100 crores towards electric mobility and battery storage, with Tata Chemicals and Ola Electric among the primary beneficiaries.

Printed Circuit Board (PCB)

Union Electronics and IT Ministry of India announced the approval of the first tranche of seven projects under the Electronics Components Manufacturing Scheme (ECMS), aimed at strengthening domestic electronics production. The initiative will support local manufacturing of multi-layer PCBs, HDI PCBs, camera modules, copper clad laminates, and polypropylene films under the “Made in India” initiative.

Camera Module Integration

India’s camera module assembly is growing rapidly as multi-sensor configurations (triple, quad-camera) become standard across mid-range and premium smartphones. AAC Technologies’ India operations and new entrants from China’s optical supply chain are establishing India-based lens assembly and OIS module integration, targeting the USD 6–8 Billion annual camera module import opportunity for localization.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Assembly and Domestic Manufacturing |

Assembly |

70.0% |

2025 |

|

Mobile Type |

Smartphones |

65.0% |

2025 |

|

Mobile Components |

🔒 |

🔒 |

2025 |

|

State |

Andhra Pradesh |

30.0% |

2025 |

By Assembly and Domestic Manufacturing

The assembly segment dominates the Indian mobile components market with a 70.0% share in 2025. This segment encompasses final device integration, including PCB assembly, chassis mounting, display bonding, battery integration, and quality testing, conducted by contract manufacturers and vertically integrated OEMs.

To access detailed market analysis, Request Sample

Domestic manufacturing represents 30.0%, encompassing component-level production of batteries, displays, mechanical parts, and electronic sub-assemblies. While smaller in current share, domestic manufacturing is growing fastest at ~15.12% CAGR, supported by PMP tariff escalation schedules and state industrial development corporation incentives.

By Mobile Type

Smartphones command a 65.0% share of India’s mobile components market in 2025, reflecting both volume leadership and the high per-unit component value. The ultra-premium smartphone segment priced above INR 45,000 accounted for a record 17% market share in Q4 2025, driving above-average BoM value inflation and premium component demand growth.

Feature phones at 23.4% continue to serve India’s 200+ million non-smartphone users in rural and semi-urban markets, primarily served by domestic brands Lava, Itel, and Micromax. The Other Phones segment at 11.6% encompasses 2G/4G feature-rich devices, IoT-connected handsets, and basic mobile terminals for enterprise and government deployments.

Regional Market Insights

Andhra Pradesh’s market leadership (30.0%, 2025) is anchored by the Sri City SEZ in Chittoor, India’s largest integrated business city housing 250+ manufacturing companies, and Visakhapatnam’s electronics manufacturing cluster. The state government’s Electronics Policy 2021–2026 offers capital subsidies of up to 25% and stamp duty exemptions, attracting Foxconn’s display assembly facility, Samsung’s component manufacturing unit, and Bharat FIH’s mobile assembly operations.

Uttar Pradesh at 26.8% is the second-largest state market, anchored by Samsung’s Noida facility, India’s largest mobile manufacturing plant globally by production area, producing approximately 120 million devices annually. The UPEIDA Electronics Manufacturing Cluster Policy provides infrastructure, single-window clearance, and SGST reimbursement for mobile component manufacturers.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Andhra Pradesh |

30.0% |

Dedicated Special Economic Zones (SEZs) attracting large-scale mobile assembly and component manufacturing operations; strategic port connectivity supporting import of components and export of finished devices. |

|

Uttar Pradesh |

26.8% |

Established electronics manufacturing cluster in the NCR region with strong OEM and contract manufacturer presence; proximity to a large domestic consumer market driving distribution efficiency |

|

Telangana |

22.7% |

Dedicated electronics manufacturing zones with TSIC incentive frameworks; state government focus on attracting both domestic and foreign electronics investment through competitive fiscal incentives |

|

Others |

20.5% |

Large-scale contract assembly operations leveraging port infrastructure and skilled workforce; emerging component manufacturing ecosystem with R&D institutions |

Competitive Landscape

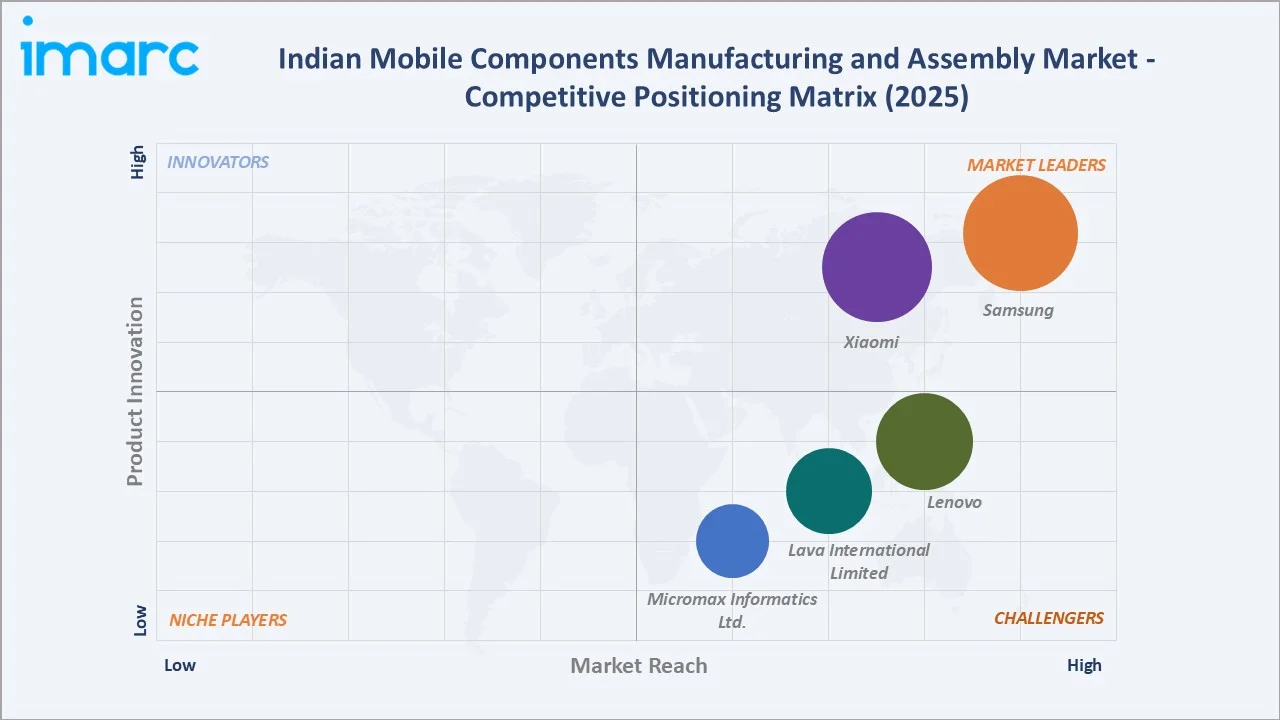

India’s mobile components manufacturing and assembly market exhibits moderate fragmentation at the assembly tier and high concentration at the component manufacturing level. The top five assembled device producers (Samsung, Xiaomi, Motorola, OPPO, vivo) collectively command approximately 75–80% of assembly revenue in 2025.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

SAMSUNG |

Samsung |

Market Leader |

World’s largest mobile plant (Noida, 120M units/yr); integrated display & battery supply chain; PLI Tier-1 beneficiary |

|

Xiaomi |

REDMI, POCO, Xiaomi |

Market Leader |

Value-segment smartphone dominance; Dixon Technologies assembly partnership; 40% domestic component sourcing target by 2026 |

|

Lenovo |

Motorola |

Strong Challenger |

Motorola brand India manufacturing; premium mid-range focus; R&D engineering in Bengaluru |

|

Lava International Limited |

Lava |

Challenger |

Largest Indian-owned mobile manufacturer; PLI beneficiary (6% incentive tier); Noida R&D center; 65% domestic component content |

|

Micromax Informatics Ltd. |

Micromax |

Challenger |

Re-launched IN series targeting mid-range segment; domestic brand with retail scale; Rudrapur, Uttarakhand manufacturing facility |

Component manufacturing is served by a mix of global Tier-1 suppliers and domestic SME manufacturers serving the mid-market.

Key Company Profiles

Samsung

Samsung, headquartered in Suwon, South Korea, is the global leader in mobile device manufacturing and India’s largest mobile phone producer by volume. Samsung’s Noida facility is the world’s largest mobile manufacturing plant by production area, producing approximately 120 million devices per year.

- Product Portfolio: Galaxy S-series (premium flagship), Galaxy A-series (global mid-range manufactured in India), Galaxy M-series (value online-first), and feature phone models for rural mass markets.

- Recent Developments: In December 2025, Samsung Electronics announced plans to expand smartphone display panel assembly operations in India at its Noida facility under the government’s PLI scheme.

- Strategic Focus: Premium smartphone market share defense; display and battery component localization under PMP; PLI-driven export expansion targeting USD 10 Billion in India-made device exports by 2027.

Xiaomi

Xiaomi, headquartered in Beijing, China, is India’s second-largest smartphone brand by volume and a major PLI beneficiary, manufacturing through a partnership with Dixon Technologies at Noida facilities.

- Product Portfolio: Xiaomi 14-series (premium flagship), Redmi Note-series (mid-range), Redmi A-series (entry-level), and POCO F-series (performance segment).

- Recent Developments: In January 2025, Tata Electronics announced discussions with Xiaomi and OPPO for smartphone manufacturing in India as the company expands beyond iPhone component production.

- Strategic Focus: Mid-range segment retention; India component localization to reduce PMP duty liability; POCO brand expansion in performance smartphones targeting the USD 250–350 price band.

Lava International Limited

Lava International Limited, headquartered in Noida, Uttar Pradesh, is India’s largest domestically owned mobile manufacturer and a Tier-1 PLI beneficiary with fully vertically integrated design, manufacturing, and R&D operations in India.

- Product Portfolio: Lava Agni series, Lava Blaze-series and Lava feature phones for the rural mass market.

- Recent Developments: In December 2024, Lava International is focusing on increasing domestic value addition in its smartphones by expanding local sourcing and strengthening component localization initiatives in line with the government’s electronics manufacturing push.

- Strategic Focus: Domestic component sourcing expansion; government and enterprise B2B supply contracts; design center expansion at Noida R&D campus targeting India-first product launches.

Market Concentration Analysis

India’s mobile components manufacturing and assembly market exhibits moderate fragmentation at the device assembly level, with the top five OEMs (Samsung, Xiaomi, Apple via contract, vivo, OPPO) holding approximately 75–80% of assembly-stage revenue in 2025. Below the top tier, a competitive mid-market of 20–25 domestic and contract manufacturers serves government supply, enterprise B2B, and rural mass-market segments.

Component manufacturing exhibits higher concentration, with the top three players in each component sub-segment (display, battery, PCBA) controlling 60–70% of sub-segment revenue. Samsung SDI and Amperex Technology (ATL) dominate battery supply, while Taiwan’s Unimicron and China’s Tripod Technology lead PCBA substrate supply, creating single-source dependency risks that the government’s PLI component scheme is specifically designed to address through domestic supply chain diversification.

Investment & Growth Opportunities

Fastest Growing Segments

Domestic manufacturing of displays and batteries (~15.12% CAGR), camera module assembly (~14.40% CAGR), and 5G antenna and RF component production (~14.00% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental addressable market of approximately USD 45–50 Billion within India’s mobile component ecosystem by 2034, as domestic value-addition transitions from 18% to 35–40%.

Emerging Market Expansion

Tamil Nadu (Apple ecosystem anchor), Karnataka (Tata Electronics, Google Pixel), and Gujarat (Oppo, Vivo) represent incremental mobile component manufacturing opportunities beyond the established Andhra Pradesh–UP–Telangana cluster. Entry strategies include anchor customer partnerships with Apple or Samsung, PLI Phase 2 application for component-specific incentives, and leveraging state Electronics Manufacturing Cluster (EMC 2.0) infrastructure with pre-built factory shells and single-window clearances.

Venture and Institutional Investment Trends

- PLI incentive outflows of USD 5.3 Billion through FY2026 are supplemented by PLI Phase 2 component-specific schemes targeting USD 3 Billion in additional manufacturing investment through 2028, creating a visible pipeline for component infrastructure scaling.

- India’s semiconductor fab investments are expected to reduce chip import dependency by USD 8–10 Billion annually by 2030, fundamentally improving the domestic component ecosystem’s cost competitiveness.

- Private equity investment in Indian contract manufacturing (Dixon Technologies, Amber Enterprises adjacency) is growing at 18–22% CAGR as global brands formalize India as a China-plus manufacturing base, creating institutional investment opportunities in electronics manufacturing service infrastructure.

Future Market Outlook (2026-2034)

India’s mobile components manufacturing and assembly market is positioned for sustained, high-growth expansion through 2034. From a base of USD 81.48 Billion in 2025, the market is projected to reach USD 253.88 Billion by 2034, representing total incremental value creation of USD 172.40 Billion at a CAGR of 13.46%. This growth is structurally assured by India’s multi-year PLI incentive pipeline, Apple and Samsung’s deepening India manufacturing commitments, and the systematic displacement of imported components by domestic production under PMP.

The technology transition from pure assembly to component manufacturing will define the market’s composition by 2034. Assembly’s share is projected to decline from 70.0% in 2025 to approximately 55–58% by 2034 as domestic manufacturing of displays, batteries, and PCBs scales. This structural shift creates replacement demand for advanced manufacturing equipment, component-specific PLI beneficiaries, and technical workforce development—each representing distinct investment opportunities.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 120 industry participants in 2024–2025, including mobile device OEM procurement heads, contract manufacturer operations directors, component supplier management, PLI scheme administrators, and institutional investors tracking India’s electronics manufacturing sector. Expert input validated market sizing, technology adoption rates, and state-level policy impact assessments.

Secondary Research

Secondary research encompassed vendor annual reports, ICEA mobile manufacturing policy submissions, MeitY PLI implementation data, DGFT import-export trade statistics (HS codes 8517, 8542, 8507), Counterpoint Research and IDC India smartphone shipment data, and industry publications including Digit, Gadgets360, and The Ken electronics manufacturing coverage.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating India smartphone shipment projections (units), average component BoM per device, domestic content ratio trajectories under PMP, and PLI-eligible production growth trajectories by beneficiary. A base-case CAGR of 13.46% reflects consensus estimates validated against PLI production milestone data, and MeitY disclosed manufacturing output from FY2020 to FY2025.

Indian Mobile Components Manufacturing and Assembly Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD, Million Units |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Mobile Types Covered | Smartphones, Feature Phones, Other Phones |

| Mobile Components Covered | Main Board and Sensor Flex, Display/Touchscreen, Camera (Primary/Secondary), Battery Pack, and Others |

| Assembly and Domestic Manufacturing Covered | Assembly, Domestic Manufacturing |

| Regions Covered | Uttar Pradesh, Andhra Pradesh, Telangana, Others |

| Companies Covered | SAMSUNG, Xiaomi, Lenovo, Lava International Limited, Micromax Informatics Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Indian mobile components manufacturing and assembly market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Indian mobile components manufacturing and assembly market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India mobile components manufacturing and assembly industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Indian Mobile Components Manufacturing and Assembly Market Report

The Indian mobile components manufacturing and assembly market reached USD 81.48 Billion in 2025 and is projected to reach USD 253.88 Billion by 2034.

The market is expected to grow at a CAGR of 13.46% during 2026-2034, driven by the PLI scheme incentives, rising smartphone demand, 5G adoption, and India’s emergence as a global mobile manufacturing hub.

Andhra Pradesh leads with a 30.0% share in 2025, anchored by the Sri City SEZ, state capital subsidies of up to 25% on fixed capital investment, and large-scale assembly operations by Foxconn, Samsung, and Bharat FIH.

Assembly dominates with a 70.0% share in 2025, encompassing final device integration by contract manufacturers including Foxconn, Pegatron, Dixon Technologies, and vertically integrated OEMs such as Samsung and Xiaomi, which together produce 330+ million devices per year.

Smartphones hold the largest share at 65.0%, driven by India’s 750+ million smartphone user base, Apple’s India production reaching USD 22 Billion, and the 5G upgrade cycle generating premium component demand worth USD 180–260 per device in BoM value.

Key players include Samsung, Xiaomi, Lenovo, Lava International Limited, and Micromax Informatics Ltd.

The Government of India’s PLI scheme for mobile manufacturing allocated USD 5.3 Billion in incentives (FY2021–2026). This policy framework, combined with PMP import duty differentials on sub-assemblies, has mobilized over USD 2.5 Billion in fresh manufacturing investment.

India’s transition is driven by the Phased Manufacturing Program’s escalating import duties on mobile sub-components, PLI Phase 2 component-specific incentives of 20–25% on capital expenditure, and OEM demand for higher domestic content to qualify for maximum PLI incentive tiers.

Key challenges include deep import dependency for core components, a skilled electronics manufacturing workforce deficit, power grid reliability constraints in Tier-2 manufacturing hubs, and working capital financing rates 2–3× higher than Chinese competitors.

Key investment opportunities include domestic display and AMOLED manufacturing, battery cell manufacturing under ACC PLI, camera module assembly localization, 5G RF component manufacturing, and PCBA bare substrate production.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)