Indian PCB (Printed Circuit Board) Market Size, Share, Trends and Forecast by Manufacturing Type, Application, Product Type, Layer, Segment, Laminate Type, and Region, 2026-2034

Indian PCB (Printed Circuit Board) Market Size, Share, Trends & Forecast (2026-2034)

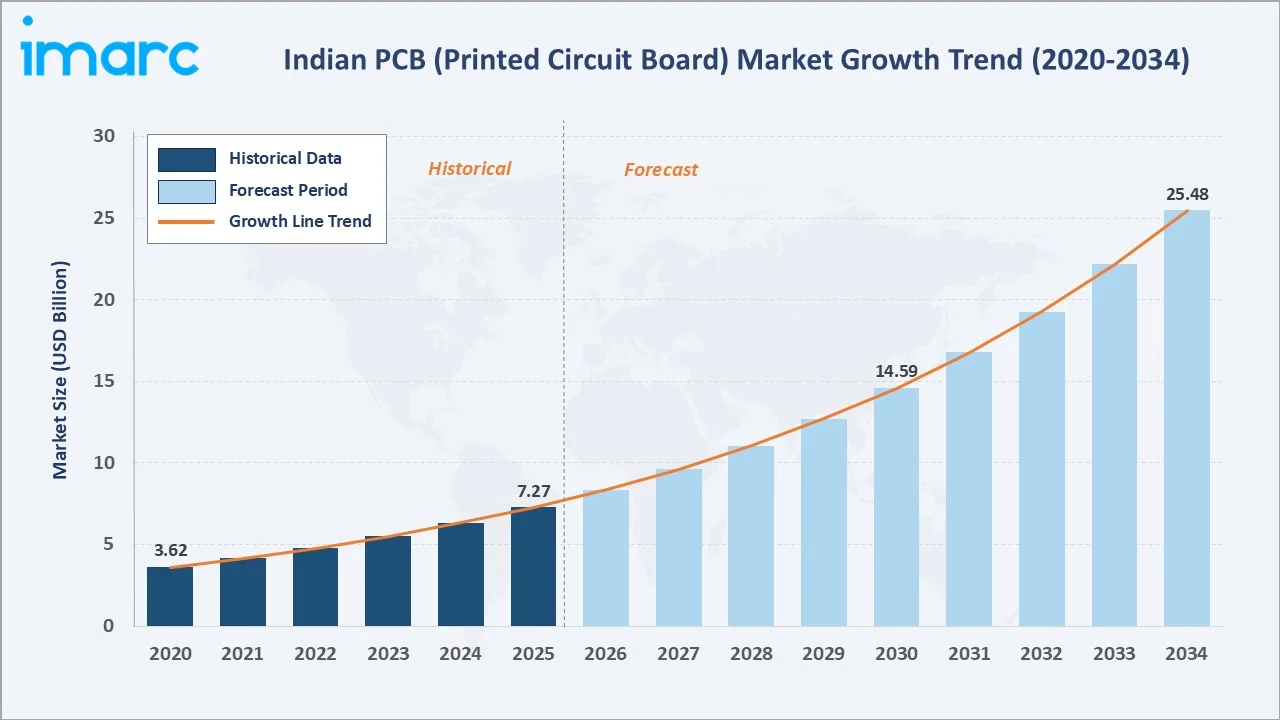

The Indian PCB (printed circuit board) market size reached USD 7.27 Billion in 2025 and is estimated to reach USD 8.4 Billion in 2026. The market is projected to reach USD 25.48 Billion by 2034, exhibiting a CAGR of 14.96% during 2026-2034. Government initiatives such as the PLI scheme for electronics manufacturing, rapid expansion of 5G infrastructure, and increasing domestic demand for consumer electronics are the primary forces driving Indian PCB market growth.

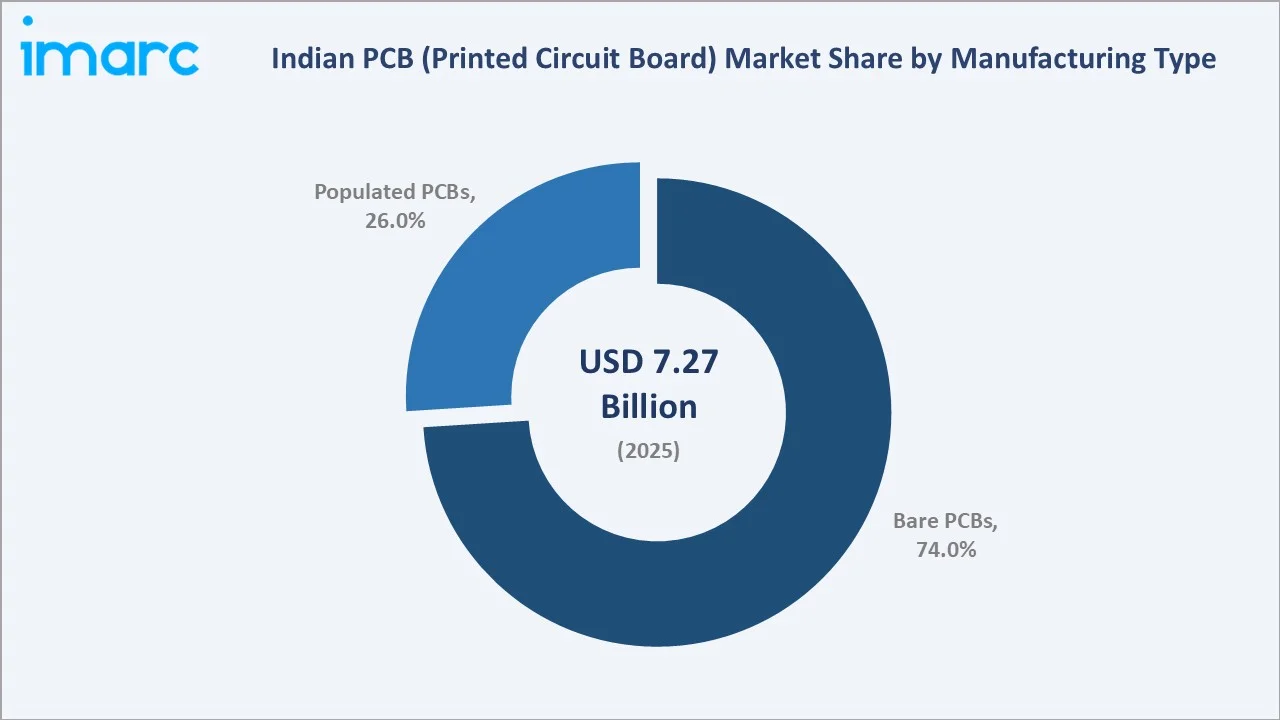

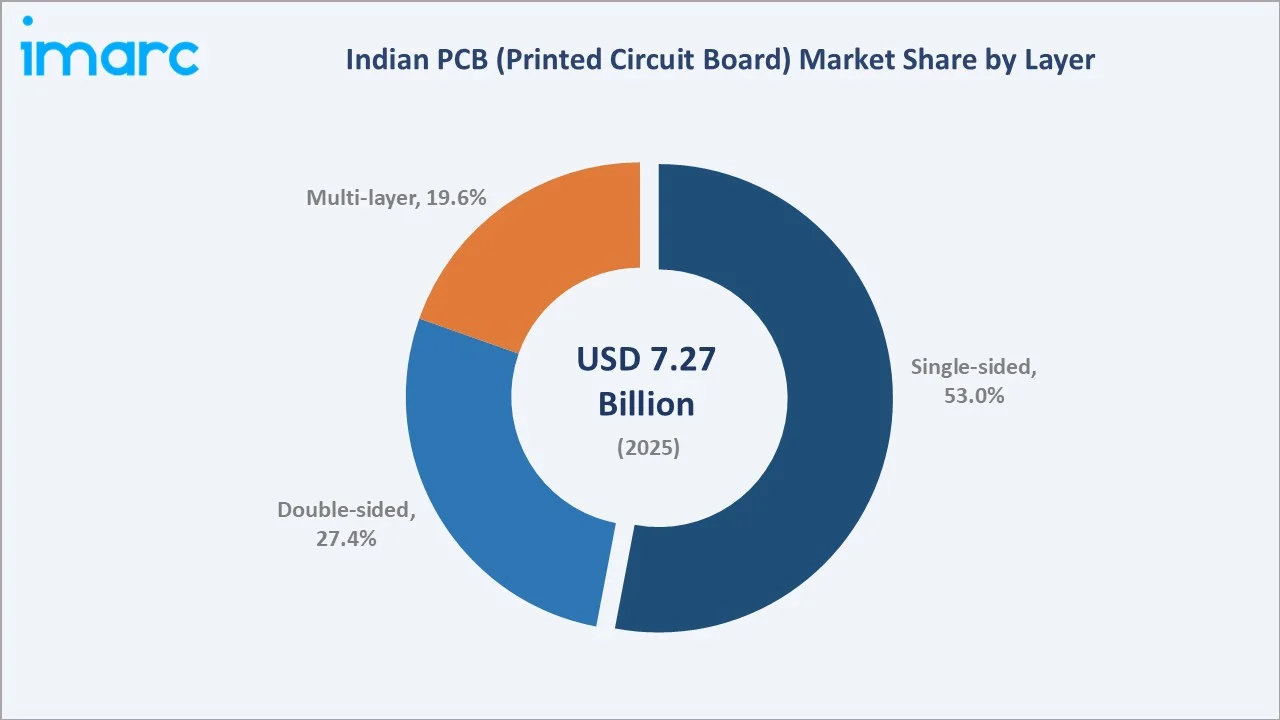

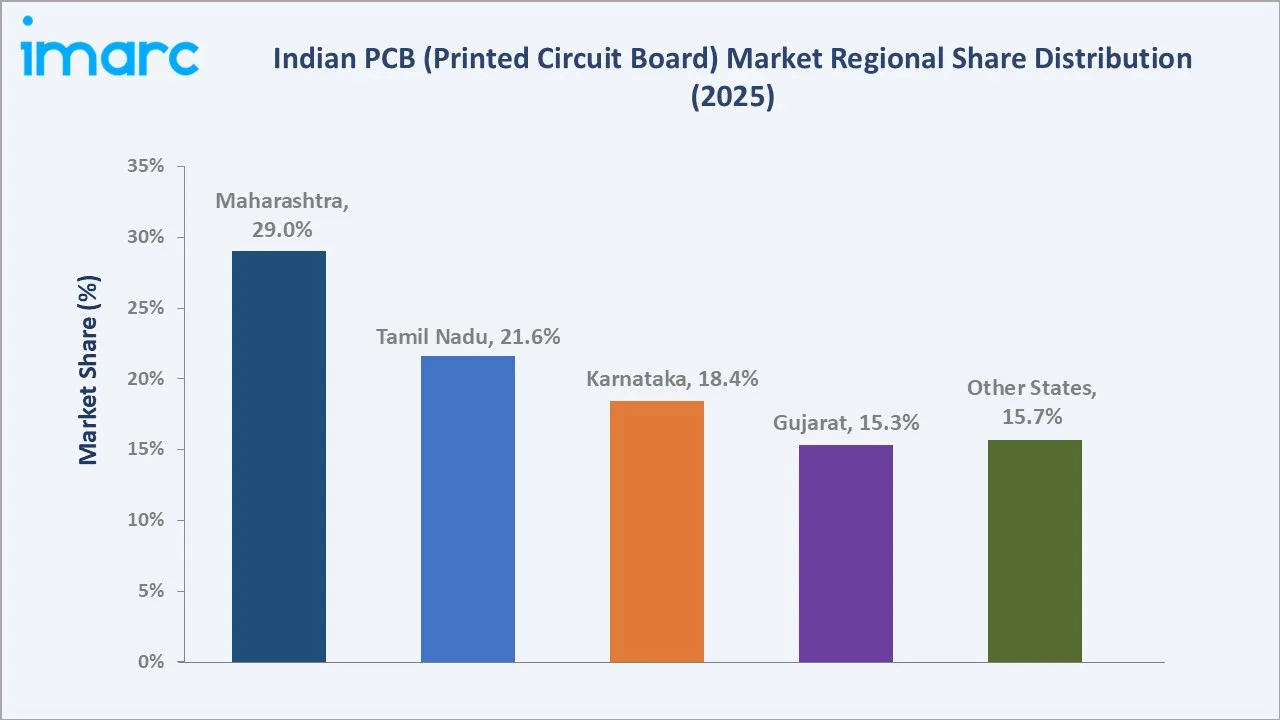

Bare PCBs dominate the manufacturing type at 74% in 2025, while single-sided PCBs lead the layer segment at 53%. Maharashtra commands a dominant 29% regional share in 2025, reflecting the state’s established electronics manufacturing ecosystem.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.27 Billion |

|

Market Size (2026) |

USD 8.4 Billion |

|

Forecast Market Size (2034) |

USD 25.48 Billion |

|

CAGR (2026-2034) |

14.96% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Maharashtra (29% share, 2025) |

|

Leading Manufacturing Type |

Bare PCBs (74%, 2025) |

|

Leading Layer |

Single-Sided (53%, 2025) |

The Indian PCB market growth trajectory from 2020 through 2034 reflects consistent electronics-driven demand, with the historical expansion to USD 7.27 Billion in 2025 and the forecast to USD 25.48 Billion capturing accelerating government policy support and digital transformation.

To get more information on this market, Request Sample

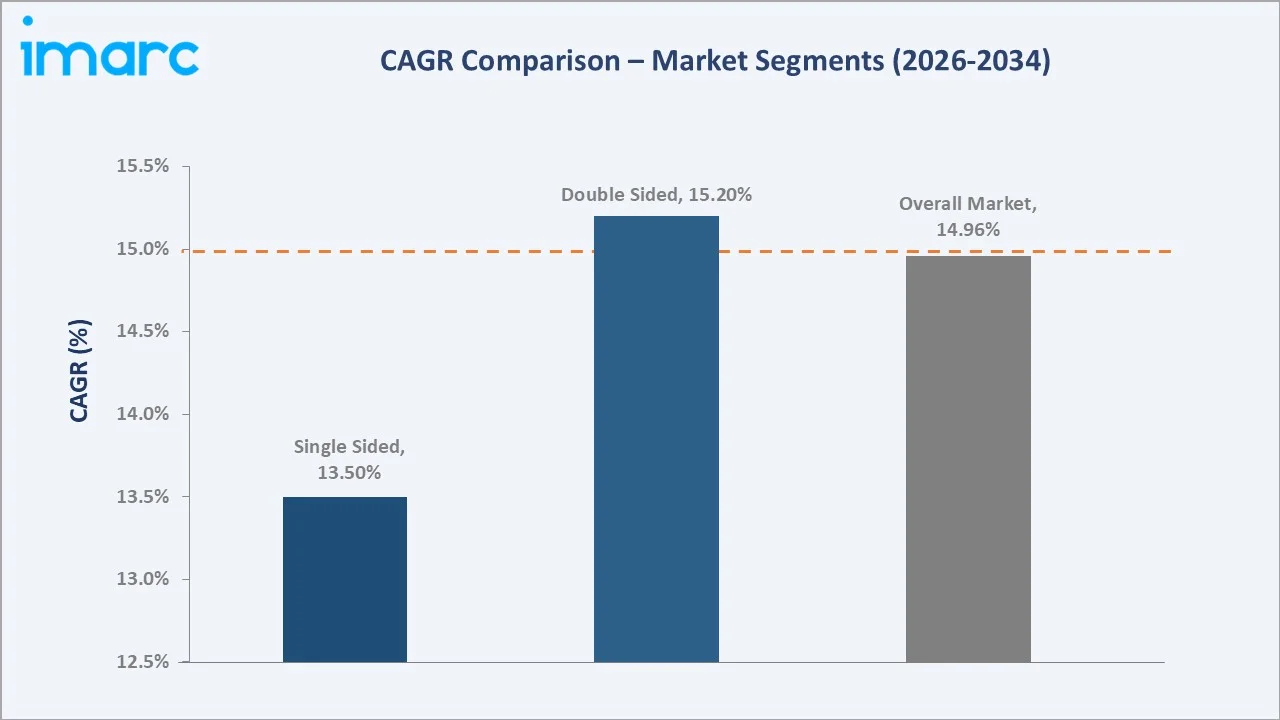

The CAGR trajectories across key manufacturing type, layer, and regional sub-segments highlight multi-layer PCBs and populated PCBs as the fastest-growing categories within the Indian PCB industry through 2034.

Executive Summary

The Indian PCB market is on an accelerated growth trajectory from USD 7.27 Billion in 2025 to USD 25.48 Billion by 2034. Printed circuit boards are essential components in virtually all electronic devices, serving as the backbone of India’s electronics manufacturing ambitions.

Bare PCBs dominate manufacturing type at 74% in 2025, reflecting India’s large-scale production of basic circuit boards for consumer electronics and industrial applications. Populated PCBs (26%) represent the value-added assembly segment growing at a faster rate driven by domestic EMS expansion.

Single-sided PCBs lead the layer segment at 53% in 2025, serving cost-sensitive consumer electronics and LED lighting applications. Maharashtra dominates regionally at 29% in 2025, followed by Tamil Nadu (21.6%) and Karnataka (18.4%).

Key Market Insights

|

Insight |

Data |

|

Largest Manufacturing Type |

Bare PCBs - 74% share (2025) |

|

Leading Layer |

Single-Sided - 53% share (2025) |

|

Leading Region |

Maharashtra - 29% share (2025) |

|

Second Largest Region |

Tamil Nadu - 21.6% share (2025) |

|

Top Companies |

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft, Epitome Components, Sulakshana Circuits Ltd, Hi-Q Electronics Pvt. Ltd, India Circuit Pvt. Ltd., Meena Circuits |

Key Analytical Observations Expanding on the Above Data:

- Bare PCBs at 74% in 2025 dominate because of India’s position as a cost-competitive manufacturing base for basic circuit boards used in consumer electronics, LED lighting, and industrial control systems where standard specifications meet volume requirements.

- Single-sided PCBs at 53% in 2025 lead because they represent the most cost-effective layer configuration for high-volume applications including LED drivers, power supplies, and basic consumer electronics that constitute the bulk of India’s PCB demand.

- Maharashtra’s 29% dominance in 2025 reflects the state’s established electronics manufacturing clusters, favorable industrial policy, proximity to major ports for raw material imports, and a skilled engineering workforce.

- Tamil Nadu at 21.6% in 2025 benefits from its strong automotive electronics base, government incentives through industrial parks, and established presence of multinational electronics companies.

Indian Printed Circuit Board Market Overview

A PCB (printed circuit board) is an essential electronic component that mechanically supports and electrically connects electronic components through conductive pathways, tracks, and signal traces etched from copper sheets laminated onto a non-conductive substrate.

The Indian PCB ecosystem integrates copper clad laminate suppliers, chemical processors, PCB fabricators, component assemblers, testing service providers, original equipment manufacturers (OEMs), and diverse end-use industries spanning consumer electronics, telecommunications, automotive, defence, and healthcare.

Market Dynamics

To evaluate market opportunities, Request Sample

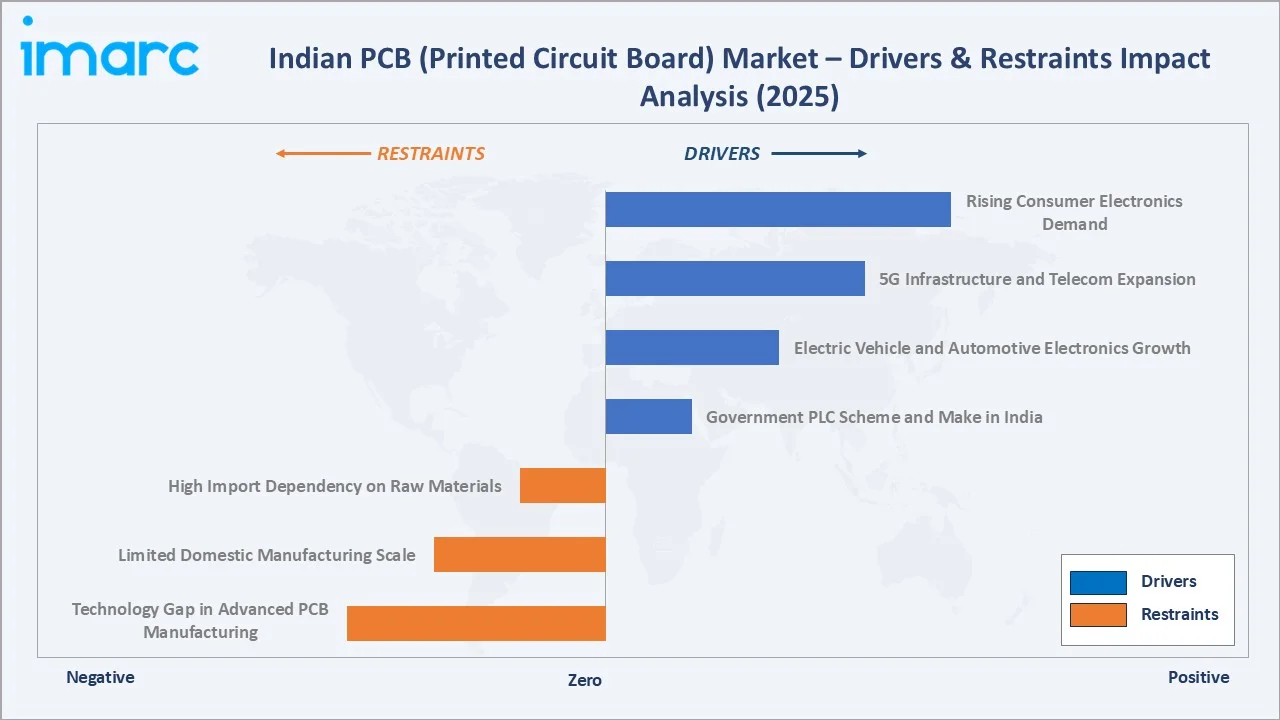

Market Drivers

- Government PLI Scheme and Make in India: The Production Linked Incentive (PLI) scheme for large-scale electronics manufacturing, with an outlay of INR 18,863.1 crore, is catalyzing domestic PCB production capacity expansion and attracting foreign direct investment into India’s electronics value chain.

- 5G Infrastructure and Telecom Expansion: India’s ongoing 5G network deployment across urban and semi-urban areas is generating substantial demand for high-frequency PCBs, antenna modules, and base station electronics.

- Electric Vehicle and Automotive Electronics Growth: India’s EV adoption acceleration, with government targets of 30% EV penetration by 2030, is driving demand for multilayer and high-density interconnect PCBs used in battery management systems and power electronics.

Market Restraints

- High Import Dependency on Raw Materials: A significant share of critical inputs is sourced from external markets, leading to potential supply chain disruptions and fluctuations in production costs; this dependence also exposes manufacturers to geopolitical risks, trade restrictions, and currency exchange volatility, which can affect operational stability, while the limited domestic availability of specialized inputs further constrains scalability and reduces the overall competitiveness of the industry.

- Limited Domestic Manufacturing Scale: Despite government incentives, India’s PCB manufacturing capacity remains limited compared to China, Taiwan, and South Korea, constraining the industry’s ability to capture the full domestic demand opportunity.

Market Opportunities

- Semiconductor Fab Ecosystem Development: India’s semiconductor mission with USD 10 Billion in incentives is creating an integrated electronics manufacturing ecosystem that will drive downstream PCB demand for chip packaging, testing boards, and substrate manufacturing.

- Defence and Aerospace Electronics Indigenization: India’s defence procurement policy mandating indigenous content requirements is creating protected demand for domestically manufactured military-grade PCBs with stringent reliability standards.

Market Challenges

- Technology Gap in Advanced PCB Manufacturing: Indian manufacturers lack capabilities in advanced HDI, flex-rigid, and high-layer-count PCB fabrication, necessitating significant capital investment and technology transfer for competitiveness in premium segments.

- Skilled Workforce Shortage: The electronics manufacturing sector faces a deficit of trained technicians proficient in advanced PCB fabrication processes, quality control, and testing methodologies.

Emerging Market Trends

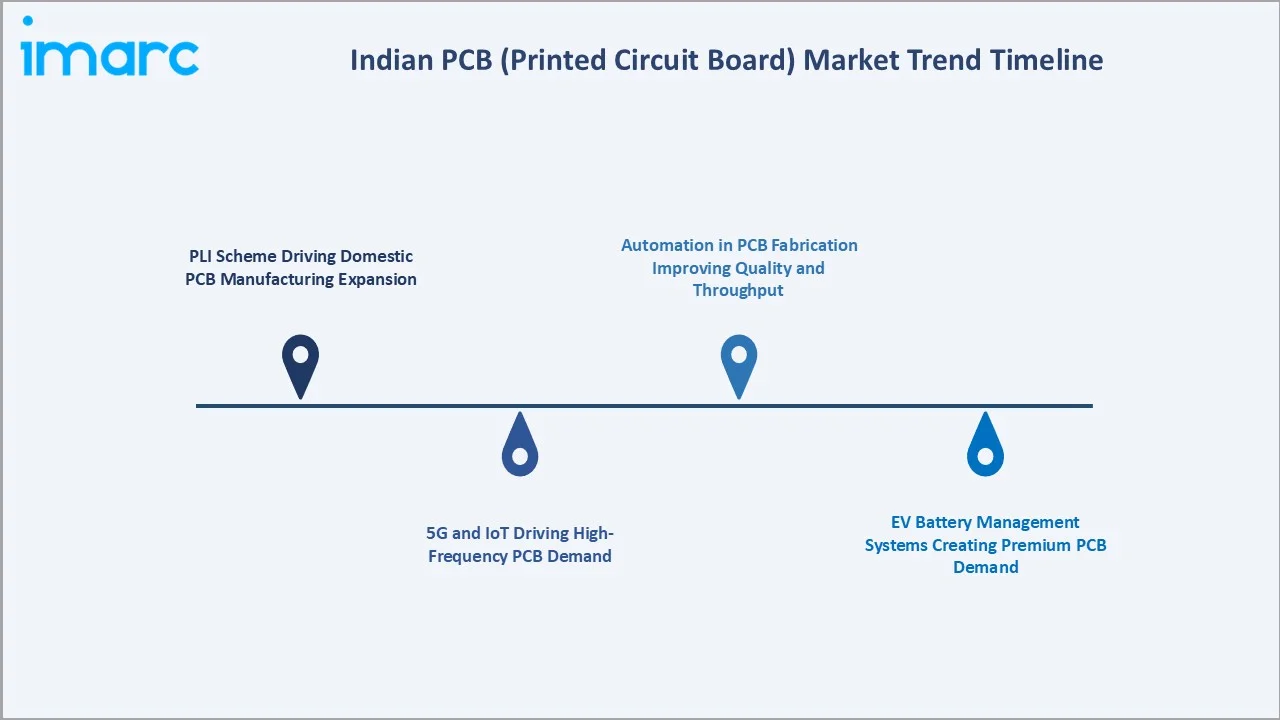

1. PLI Scheme Driving Domestic PCB Manufacturing Expansion

The Government of India’s PLI scheme for electronics manufacturing is transforming the domestic PCB landscape. Multiple companies have announced greenfield PCB manufacturing facilities, with investment commitments exceeding INR 5,000 crore in capacity expansion.

2. 5G and IoT Driving High-Frequency PCB Demand

The rollout of 5G networks across India is creating demand for advanced high-frequency PCB substrates. IoT device proliferation in smart city and industrial automation applications is generating volume demand for compact, multilayer PCB designs.

3. EV Battery Management Systems Creating Premium PCB Demand

India’s electric vehicle transition is generating specialized PCB demand for battery management systems, motor controllers, and charging infrastructure electronics requiring high-current handling and thermal management capabilities.

4. Automation in PCB Fabrication Improving Quality and Throughput

Indian PCB manufacturers are investing in automated optical inspection (AOI), laser direct imaging (LDI), and CNC drilling systems to improve yield rates, reduce defect density, and achieve cost competitiveness with Asian manufacturing peers.

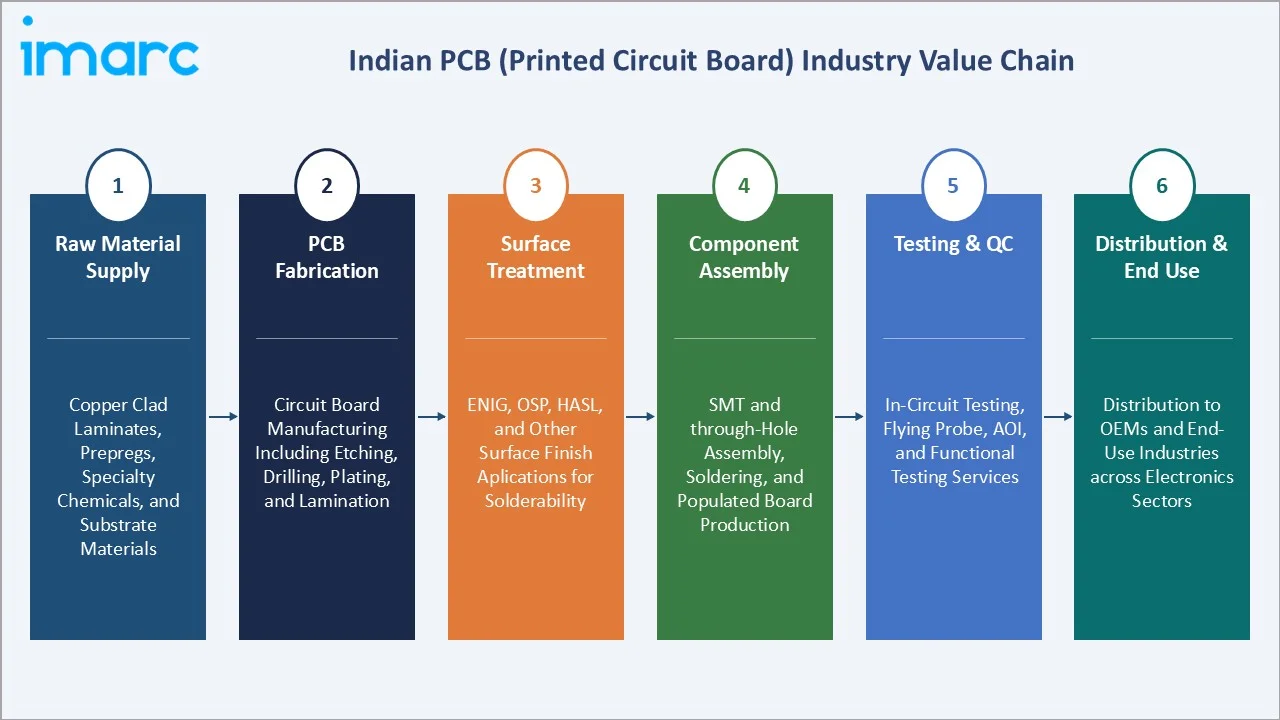

Industry Value Chain Analysis

The Indian PCB value chain spans six stages from raw material procurement through end-use integration. PCB fabrication and component assembly capture the highest value-add margins, while raw material sourcing and testing generate significant quality differentiation.

|

Stage |

Description |

|

Raw Material Supply |

Copper clad laminates, prepregs, specialty chemicals, and substrate materials |

|

PCB Fabrication |

Circuit board manufacturing including etching, drilling, plating, and lamination |

|

Surface Treatment |

ENIG, OSP, HASL, and other surface finish applications for solderability |

|

Component Assembly |

SMT and through-hole assembly, soldering, and populated board production |

|

Testing & QC |

In-circuit testing, flying probe, AOI, and functional testing services |

|

Distribution & End Use |

Distribution to OEMs and end-use industries across electronics sectors |

Vertically integrated PCB manufacturers with in-house surface treatment and testing capabilities achieve lower production costs and faster turnaround times than subcontracted fabrication models, providing competitive advantage in India’s price-sensitive market.

Technology Landscape in the Indian PCB Industry

PCB Fabrication Technology: From Single-Sided to HDI

Indian PCB manufacturers primarily operate in single-sided and double-sided board fabrication using subtractive etching processes. Advanced manufacturers are investing in sequential lamination and laser microvia drilling capabilities to enter the multilayer and HDI segments.

Material Innovation: High-Frequency and Lead-Free Substrates

The transition to lead-free soldering processes (RoHS compliance) and adoption of high-frequency laminate materials are enabling Indian manufacturers to serve telecommunications and automotive applications requiring enhanced signal integrity.

Surface Treatment Technology: ENIG and OSP

Electroless Nickel Immersion Gold (ENIG) and Organic Solderability Preservative (OSP) surface finishes are the dominant treatment methods in Indian PCB manufacturing, providing reliable soldering surfaces for SMT component assembly.

Digital Design and CAD Integration

Indian PCB design houses are adopting advanced EDA tools for complex multilayer PCB routing, signal integrity analysis, and design-for-manufacturing optimization, accelerating product development cycles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Manufacturing Type |

Bare PCBs |

74.0% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Product Type |

🔒 |

🔒 |

2025 |

|

Layer |

Single-Sided |

53.0% |

2025 |

|

Segment |

🔒 |

🔒 |

2025 |

|

Laminate Type |

🔒 |

🔒 |

2025 |

|

Region |

Maharashtra |

29.0% |

2025 |

By Manufacturing Type

Bare PCBs command a 74.0% majority share in 2025 owing to India’s large-scale production of basic circuit boards for consumer electronics, LED lighting, industrial controls, and power supply applications. The cost-competitive pricing of bare board fabrication makes India an attractive sourcing destination.

To access detailed market analysis, Request Sample

Populated PCBs at 26.0% in 2025 represent the assembled board segment where electronic components are soldered onto bare boards. This segment is growing fastest, driven by the expansion of electronic manufacturing services (EMS) companies establishing assembly operations in India.

By Layer

Single-sided PCBs dominate the layer segment at 53.0% in 2025, representing the highest-volume, most cost-efficient configuration for standard consumer electronics applications. These boards serve LED lighting, simple power supplies, calculators, and basic control circuits.

Double-sided PCBs at 27.4% in 2025 provide conductivity on both surfaces, enabling more complex circuit routing for telecommunication equipment, automotive electronics, and industrial instrumentation applications requiring higher component density.

Multi-layer PCBs at 19.6% in 2025 serve advanced applications in smartphones, networking equipment, defence electronics, and medical devices. This segment is growing at the fastest rate within the layer category due to increasing electronic complexity.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Maharashtra |

29.0% |

Established electronics manufacturing; port access; industrial policy support |

|

Tamil Nadu |

21.6% |

Automotive electronics hub; industrial parks; MNC presence |

|

Karnataka |

18.4% |

IT-electronics ecosystem; defence electronics; R&D infrastructure |

|

Gujarat |

15.3% |

Special investment regions; emerging electronics manufacturing corridor |

|

Other States |

15.7% |

Emerging electronics manufacturing hubs across multiple states |

Maharashtra’s 29.0% market dominance in 2025 is driven by its established electronics manufacturing clusters, proximity to India’s largest container port for raw material imports, and a supportive industrial policy framework that attracts both domestic and international PCB manufacturers.

Tamil Nadu at 21.6% in 2025 benefits from its position as India’s automotive electronics capital, with major global OEMs sourcing PCBs locally for vehicle electronics, combined with state government incentives for electronics manufacturing investment.

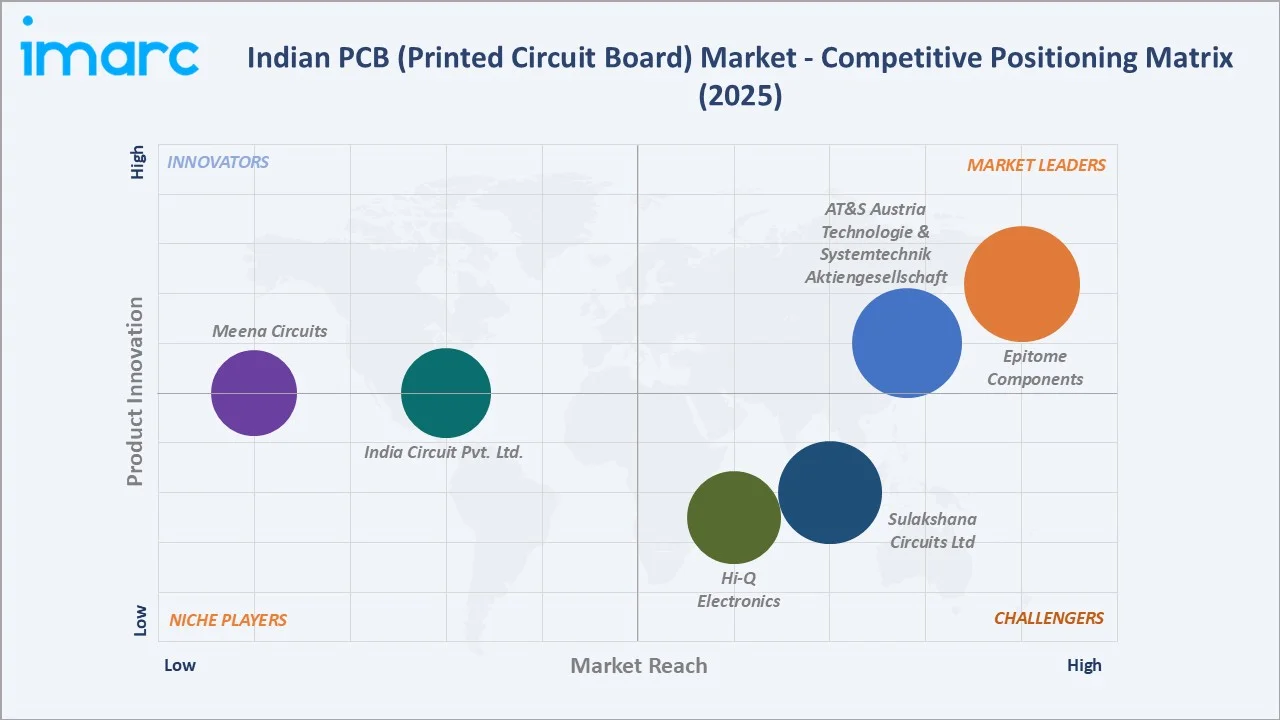

Competitive Landscape

The Indian PCB market is moderately fragmented, with domestic manufacturers holding strong positions in standard single-sided and double-sided board segments, while international companies lead in advanced multilayer and HDI PCB technologies.

|

Company Name |

Key Products |

Position |

Strategic Focus |

|

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft |

Double-sided, Flexible and rigid-flexible printed circuit boards, HDI printed circuit boards, Multilayer printed circuit boards, Substrate-like PCBs, Thermally enhanced printed circuit boards |

Leader |

Advanced technology; automotive & telecom |

|

Epitome Components |

Single & Double-sided PCBs, Multi-Layer, R.F PCB |

Leader |

Domestic leader; consumer electronics |

|

Sulakshana Circuits Ltd |

Multilayer, FR4 (Tg 135, Tg 170), RT/ duroid, Teflon PCBs |

Challenger |

Industrial & telecom applications |

|

Hi-Q Electronics Pvt. Ltd |

Rigid & Flexible PCBs, Multilayer PCBs, HDI PCBs |

Challenger |

Quality focus; niche applications |

|

India Circuit Pvt. Ltd. |

Single Sided PCB, Double Sided PCB, Metal Core PCB |

Emerging |

LED PCB specialist |

|

Meena Circuits |

Multilayer PCBs, Metal Core PCBs, Single Sided PCBs |

Emerging |

Domestic consumer electronics supply |

Key players include AT&S Austria Technologie & Systemtechnik Aktiengesellschaft, Epitome Components, Sulakshana Circuits Ltd, Hi-Q Electronics Pvt. Ltd, India Circuit Pvt. Ltd., Meena Circuits, and others.

Key Company Profiles

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft is a global leader in advanced PCB and IC substrate manufacturing with operations in India. The company specializes in high-density interconnect, IC substrates, and multilayer PCBs for automotive, industrial, and mobile device applications.

- Product Portfolio: Offers Double-sided, Flexible and rigid-flexible printed circuit boards, HDI printed circuit boards, Multilayer printed circuit boards, Substrate-like PCBs, Thermally enhanced printed circuit boards.

- Recent Developments: In October 2023, AT&S India, was recognized at the 48th ELCINA Awards for its strong commitment to eco-friendly PCB manufacturing and overall operational excellence, securing top honors in environmental sustainability as well as high-end PCB production. The company’s Nanjangud facility incorporates advanced wastewater recycling systems and complies with global environmental standards, reflecting its focus on sustainable manufacturing practices alongside technological advancement and capacity expansion.

- Strategic Focus: AT&S leverages its global technology leadership to serve India’s premium PCB demand in automotive, telecommunications, and industrial electronics, positioning as the technology benchmark for domestic manufacturers.

Epitome Components

Epitome Components is one of India’s largest domestic PCB manufacturers, specializing in single-sided and double-sided boards for the consumer electronics, LED, and industrial sectors.

- Product Portfolio: Offers Single & Double-sided PCBs, Multi-Layer, R.F PCB.

- Strategic Focus: Epitome’s strategy focuses on volume leadership in standard PCBs through cost-competitive manufacturing and quick delivery, targeting the high-volume consumer electronics and LED lighting markets.

Market Concentration Analysis

The Indian PCB market is moderately fragmented with numerous small and medium-sized manufacturers serving regional demand, while a handful of larger companies hold disproportionate shares in their respective technology segments.

Consolidation is expected to accelerate as PLI scheme incentives favour larger-scale manufacturers capable of meeting minimum investment thresholds. Technology-driven consolidation will see advanced multilayer and HDI-capable manufacturers acquiring smaller single-sided board producers.

Investment & Growth Opportunities

Fastest-Growing Segments

Multi-layer PCBs represent the highest-growth layer segment through 2034, driven by 5G infrastructure, automotive electronics, and smartphone manufacturing demand. Populated PCBs represent the fastest-growing manufacturing type as EMS operations expand domestically.

Emerging Markets

Gujarat and Karnataka are the fastest-growing state markets through 2034. Special investment regions and established IT-electronics ecosystems are attracting major PCB manufacturing investment commitments across these states.

Venture & Investment Trends

Private equity and venture capital interest in India’s PCB manufacturing sector is growing significantly. Government incentive programmes, rising domestic electronics demand, and import substitution opportunities are creating attractive return profiles for investors.

Future Market Outlook (2026-2034)

The Indian PCB market is forecast to expand from USD 7.27 Billion in 2025 to USD 25.48 Billion by 2034 at a CAGR of 14.96%, adding USD 18.21 Billion in incremental annual market value over the forecast period.

Three forces will most significantly shape the Indian PCB industry through 2034. First, the government’s semiconductor and electronics manufacturing ecosystem development will create integrated demand. Second, 5G and AI-driven electronics proliferation will drive advanced PCB adoption. Third, automotive electrification will generate premium multilayer PCB demand.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024-2025 with Indian PCB industry stakeholders, including senior executives at leading manufacturers, electronics procurement managers, industry association representatives, and government policy officials.

Secondary Research

Key secondary sources include MeitY Annual Reports, IPC World PCB Production Reports, India Electronics and Semiconductor Association (IESA) publications, industry trade publications, company annual reports, and government policy documents.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting models, incorporating GDP growth rates, electronics production indices, PLI scheme investment data, and historical market patterns. Scenario analysis was performed to account for policy and macroeconomic uncertainty.

Indian PCB (Printed Circuit Board) Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Manufacturing Types Covered |

Bare PCBs, Populated PCBs |

|

Applications Covered |

Consumer Electronics, Communication, Industrial Electronics, Computers, Military & Aerospace, Automotive, Medical Instrumentation, Others |

|

Product Types Covered |

Rigid 1-2 Sided, Standard Multilayer, Flexible Circuits, HDI/Microvia/Build-Up, Rigid Flex, Others |

|

Layers Covered |

Single-Sided, Double-Sided, Multi-Layer |

|

Segments Covered |

Rigid PCBs, Flexible PCB |

|

Laminate Types Covered |

FR-4, Polyamide, CEM-1, Paper, Others |

|

States Covered |

Maharashtra, Tamil Nadu, Karnataka, Gujarat, Other States |

|

Companies Covered |

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft, Epitome Components, Sulakshana Circuits Ltd, Hi-Q Electronics Pvt. Ltd, India Circuit Pvt. Ltd., Meena Circuits, etc. |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian PCB (Printed Circuit Board) Market Report

The Indian PCB market reached USD 7.27 Billion in 2025, reflecting consistent demand from electronics manufacturing expansion, government policy support, and growing domestic consumer electronics consumption.

The market is projected to reach USD 25.48 Billion by 2034, growing at a CAGR of 14.96% during 2026-2034, driven by PLI scheme investment, 5G deployment, and EV electronics adoption.

Bare PCBs lead with a 74% share in 2025, serving the majority of consumer electronics, LED lighting, and industrial applications with cost-competitive standard board fabrication.

Single-sided PCBs lead at 53% in 2025, representing the most cost-efficient layer configuration for high-volume consumer electronics and industrial control applications.

Maharashtra commands a 29% market share in 2025, driven by established electronics clusters, proximity to major ports, and supportive industrial policy frameworks.

Multi-layer PCBs are the fastest-growing layer segment through 2034, driven by 5G infrastructure, smartphone manufacturing, and automotive electronics applications.

Leading companies include AT&S Austria Technologie & Systemtechnik Aktiengesellschaft, Epitome Components, Sulakshana Circuits Ltd, Hi-Q Electronics Pvt. Ltd, India Circuit Pvt. Ltd., Meena Circuits.

Key applications include consumer electronics, telecommunications, industrial electronics, automotive, defence and aerospace, medical instrumentation, and computing.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)