Indian Pesticides Market Size, Share, Trends and Forecast by Product Type, Segment, Formulation, Crop Type, and State, 2026-2034

Indian Pesticides Market Summary:

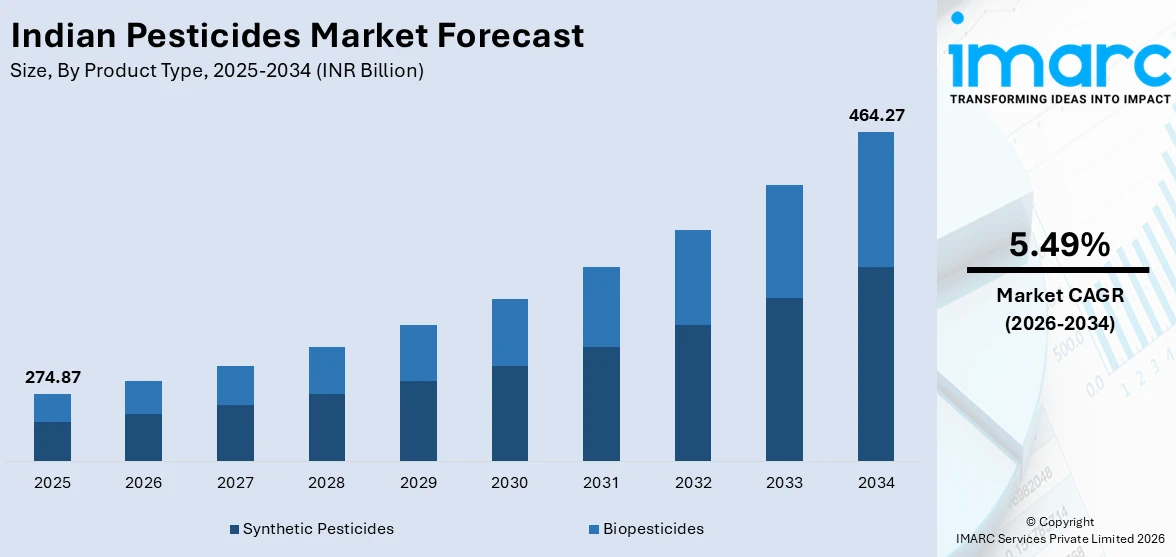

The Indian pesticides market size was valued at INR 274.87 Billion in 2025 and is projected to reach INR 464.27 Billion by 2034, growing at a compound annual growth rate of 5.49% from 2026-2034.

The Indian pesticides sector is undergoing consistent growth fueled by the nation's rising agricultural intensification and the need to improve food security for an increasing population. The growing use of contemporary agricultural methods, government assistance via subsidies and extension services, along with heightened awareness about integrated pest management, are influencing the market demand. Improvements in pesticide formulations, the transition to high-yield crop varieties, and the growing distribution networks are further contributing to the Indian pesticides market share.

Key Takeaways and Insights:

- By Product Type: Synthetic pesticides dominate the market with a share of 97.0% in 2025, driven by their proven efficacy across diverse pest categories, widespread availability through established distribution channels, and strong farmer preference for conventional crop protection solutions.

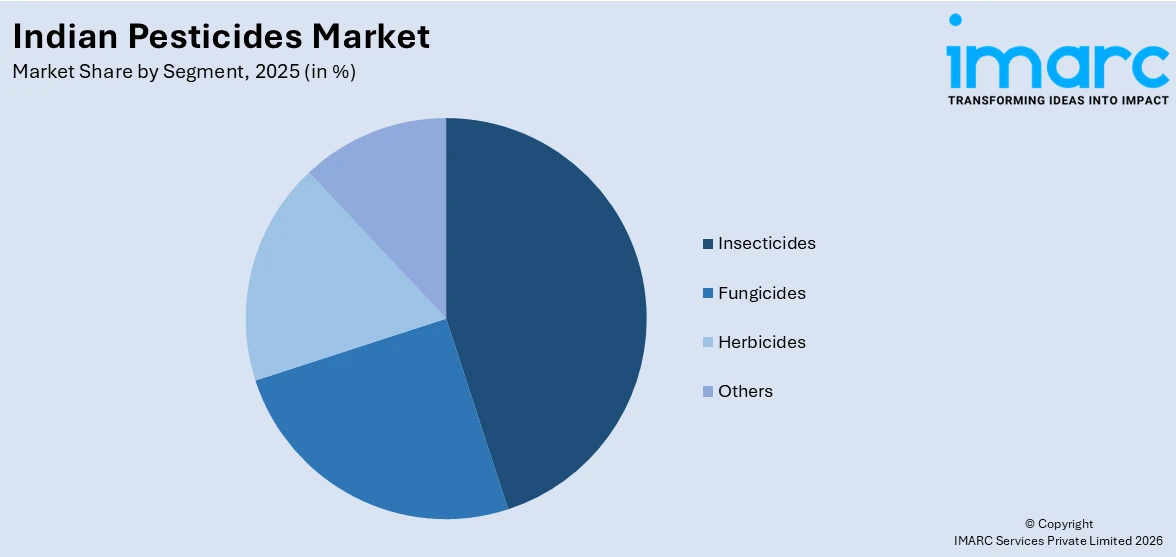

- By Segment: Insecticides lead the market with a share of 41.0% in 2025, owing to the high prevalence of insect pests across major cereal and horticultural crops, tropical climatic conditions favoring pest proliferation, and extensive application in paddy, cotton, and vegetable cultivation.

- By Formulation: Liquid represents the largest segment with a market share of 60.0% in 2025, reflecting its ease of application through spraying equipment, superior crop coverage, compatibility with modern drone-based spraying technologies, and faster absorption rates.

- By Crop Type: Cereals dominate the market with a share of 42.0% in 2025. This dominance is because of India's extensive cultivation of rice, wheat, and maize, which collectively cover the largest agricultural acreage and require significant pest management interventions.

- By State: Uttar Pradesh leads the market with a share of 20.0% in 2025, due to its position as the largest agricultural state with extensive cereal and sugarcane cultivation, high pest pressure, and large-scale farming operations.

- Key Players: The Indian pesticides market exhibits strong competitive intensity, with established domestic agrochemical manufacturers competing alongside multinational crop protection companies across diverse product segments, price tiers, and geographic markets.

To get more information on this market Request Sample

The Indian pesticides sector is gaining traction owing to swift agricultural modernization, rising mechanization, and the adoption of precision farming technologies that enhance efficiency and minimize input wastage. Farmers are embracing data-driven and automated systems for crop protection to boost productivity, reduce losses, and guarantee efficient pesticide use. The shift towards precise spraying methods enhances cost-effectiveness while tackling environmental and safety issues. Technological advancements are further enhancing pest detection precision, allowing for prompt action and better yield results. In line with this, in 2025, scientists at IIT Kharagpur created a semi-automatic farm robot that can identify plant diseases using camera image analysis and accurately spray pesticides. The patented system functioned for approximately 1.5 hours per charge, spans 40–50 meters with complete rotation capability, and acted as a terrestrial alternative to drones, minimizing chemical exposure and enhancing crop quality standards

Indian Pesticides Market Trends:

Growing Food Demand and Crop Yield Requirements

Rising population levels and expanding food consumption requirements remain central to the growth of the Indian pesticides market. Farmers face sustained pressure to increase agricultural productivity and maintain consistent crop output despite constraints on cultivable land. Pest infestations, plant diseases, and weed competition continue to threaten yield stability and quality, reinforcing the need for reliable crop protection solutions. According to IASP, India’s population is projected to peak at approximately 1.8 to 1.9 billion by 2080, underscoring the long-term imperative to strengthen food production capacity. In this environment, both chemical and biological pesticides play an essential role in minimizing crop losses, protecting harvest quality, and supporting national food security objectives through improved farm productivity.

Advancement and Commercialization of Eco-Friendly Biopesticides

The development and commercialization of eco-friendly biopesticides are emerging as a significant driver of growth in the Indian pesticides market. Increasing regulatory scrutiny, residue compliance requirements, and demand for safer crop protection solutions are encouraging research institutions and manufacturers to invest in biological alternatives. Innovations that match the efficacy of chemical pesticides while improving soil health and plant vitality are gaining acceptance among farmers. A notable example is the 2025 announcement by ICAR-Indian Institute of Spices Research, Kozhikode, regarding a Lecanicillium psalliotae-based biopesticide for controlling cardamom thrips. Field trials in Kerala demonstrated performance comparable to chemical insecticides, and the CIBRC-tested product is now ready for commercial licensing, strengthening the transition toward sustainable and residue-compliant crop protection solutions.

Strengthening Regulatory Support and Compliance Infrastructure

Enhanced regulatory guidance and institutional support are contributing to structured growth in the Indian pesticides market. As compliance requirements become more detailed and export standards more stringent, manufacturers and formulators require clarity to ensure uninterrupted operations. Industry-led platforms that simplify regulatory interpretation reduce uncertainty and support timely product approvals and market access. Clearer understanding of evolving norms also improves alignment with domestic and international quality benchmarks. In 2025, the Pesticides Manufacturers and Formulators Association of India launched a dedicated HelpDesk to assist stakeholders with queries related to IPMS, regulatory obligations, and export guidelines. The initiative was designed to strengthen compliance awareness, facilitate smoother adaptation to policy changes, and support sustainable expansion of the crop protection industry.

Market Outlook 2026-2034:

The Indian pesticides sector is set for continuous growth, supported by agricultural intensification, greater crop diversification, and heightened technology adoption. The market generated a revenue of INR 274.87 Billion in 2025 and is projected to reach a revenue of INR 464.27 Billion by 2034, growing at a compound annual growth rate of 5.49% from 2026-2034. Increasing local manufacturing capabilities, governmental backing for contemporary agriculture, and heightened awareness of sustainable pest control are anticipated to boost revenue potential and create a more competitive and developed pesticide market throughout India.

Indian Pesticides Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Synthetic Pesticides |

97.0% |

|

Segment |

Insecticides |

41.0% |

|

Formulation |

Liquid |

60.0% |

|

Crop Type |

Cereals |

42.0% |

|

State |

Uttar Pradesh |

20.0% |

Product Type Insights:

- Synthetic Pesticides

- Biopesticides

Synthetic pesticides dominate with a market share of 97.0% of the total Indian pesticides market in 2025.

Synthetic pesticides lead the market because of their strong efficacy, wide-ranging effectiveness, and rapid pest management results. Farmers in key agricultural states depend on synthetic products to safeguard their crops from pests, weeds, and fungal attacks. These products provide reliable performance in various agricultural climatic conditions and are suitable for large-scale farming practices. Their comparatively reduced cost per hectare in relation to some bio-based alternatives also facilitates broad adoption. Robust distribution systems, proactive marketing by agrochemical firms, and convenient access via rural shops further enhance market infiltration, guaranteeing ongoing demand in essential crop categories.

Synthetic pesticides gain from already existing manufacturing capabilities and ongoing product development by both domestic and international agrochemical companies. India is a major global producer and exporter of generic agrochemicals, ensuring competitive prices and a steady supply in the local market. Regulatory endorsements and farmer knowledge of established active ingredients promote continued usage. Intensive farming of cereals, cotton, sugarcane, and horticultural crops raises pest populations, leading to increased dependence on chemical pest control measures. Financial organizations and input vendors frequently package synthetic pesticides with seed and fertilizer sales, promoting their use.

Segment Insights:

Access the comprehensive market breakdown Request Sample

- Insecticides

- Fungicides

- Herbicides

- Others

Insecticides lead with a market share of 41.0% of the total Indian pesticides market in 2025.

Insecticides dominate the market owing to the continual occurrence of insect invasions in major crops like rice, cotton, pulses, and vegetables. Beneficial tropical and subtropical climate conditions enable pest reproduction throughout the year, heightening the risks of crop damage. Farmers focus on efficient pest management to protect harvests and uphold produce quality, especially in economically important crops. In response to this demand, Insecticides India Limited introduced Sparcle in 2025, a Triflumezopyrim 10% w/w SC insecticide for paddy, created in collaboration with Corteva Agriscience to control brown plant hopper and improve rice yield and profitability.

Insecticides also benefit from continuous product development, including combination formulations and targeted molecules designed to address resistance issues. Domestic manufacturers and multinational companies actively promote new active ingredients to improve efficacy and expand crop coverage. Government support for boosting agricultural productivity and ensuring food security encourages timely pest management practices, reinforcing insecticide demand. High export-oriented cultivation of crops such as cotton and fruits necessitates strict pest control to meet quality standards. Input dealers and agronomists frequently recommend insecticides as part of standard crop protection packages, strengthening repeat purchases. This consistent requirement across crop cycles secures their leadership within the Indian pesticides market.

Formulation Insights:

- Liquid

- Dry

Liquid exhibits a clear dominance with a 60.0% share of the total Indian pesticides market in 2025.

Liquid holds the biggest market share attributed to its ease of application, uniform coverage, and compatibility with conventional spraying equipment. Farmers widely prefer liquid concentrates and emulsifiable solutions as they can be easily mixed with water and applied across large fields using knapsack and power sprayers. This formulation ensures better adhesion to plant surfaces and quicker absorption, improving pest control efficiency. Liquid pesticide is suitable for a broad range of crops, including cereals, cotton, fruits, and vegetables, supporting higher consumption volumes. Strong availability through agro retail networks and clear dosage instructions further enhance farmer convenience and repeat usage.

Liquid formulation also offers flexibility in blending multiple active ingredients, enabling combination products that address insects, fungi, and weeds simultaneously. Agrochemical companies focus heavily on liquid products due to easier manufacturing scalability and packaging efficiency. Transport and storage systems are well established for bottled and containerized liquids, reducing logistical challenges. Farmers perceive liquid pesticide as delivering faster visible results compared to certain dry formulations, strengthening preference during peak pest outbreaks. Extension workers and input dealers commonly recommend liquid variants as part of crop protection schedules. This widespread acceptance and operational practicality secure its dominant position in the market.

Crop Type Insights:

- Cereals

- Fruits

- Vegetables

- Plantation Crops

- Others

Cereals dominate with a market share of 42.0% of the total Indian pesticides market in 2025.

Cereals represent the largest segment driven by their extensive cultivation area and central role in national food security. Crops, such as rice and wheat, occupy a significant share of total sown area, creating sustained demand for crop protection products across multiple growing seasons. These crops are highly susceptible to insects, weeds, and fungal diseases, prompting regular pesticide application to safeguard yields. Government procurement systems and minimum support prices encourage farmers to maintain productivity, reinforcing consistent input usage. The scale of cereal farming, particularly in states like Punjab, Haryana, and Uttar Pradesh, drives high volume pesticide consumption annually.

Cereal crops also require protection at various growth stages, increasing the frequency of pesticide applications throughout the cultivation cycle. Herbicides are widely used in wheat and rice fields to control weed competition, while insecticides and fungicides address pests and diseases that threaten grain quality. Mechanized farming practices in major cereal producing regions support efficient pesticide spraying across large tracts of land. Research institutions and agrochemical companies continuously introduce formulations tailored for cereal specific pests, strengthening targeted adoption. Financial access to credit and input subsidies further enables timely pesticide purchases. This broad and recurring demand secures cereals as the leading crop segment in the Indian pesticides market.

State Insights:

- Uttar Pradesh

- Punjab

- Maharashtra

- Rajasthan

- Haryana

- Others

Uttar Pradesh leads with a market share of 20.0% of the total Indian pesticides market in 2025.

Uttar Pradesh leads the market because of vast agricultural land base and diverse crop cultivation. The state is a major producer of cereals, sugarcane, pulses, and vegetables, all of which require regular crop protection to maintain yields and quality. High cropping intensity and multiple sowing cycles increase the frequency of pesticide applications across seasons. Favorable climatic conditions also support pest and disease incidence, driving consistent demand for insecticides, herbicides, and fungicides. Extensive rural distribution networks and a large base of small and medium farmers further contribute to strong and recurring pesticide consumption statewide.

The dominance of Uttar Pradesh is further supported by strong access to credit facilities that enable timely pesticide purchases. Government programs promoting higher farm productivity encourage adoption of modern crop protection practices. For instance, in 2025, the Uttar Pradesh government launched drone-based crop protection in six districts to modernize farming and raise farmer incomes. Under a pilot project, drones were spraying nano urea and pesticides across Lucknow, Gorakhpur, Bahraich, Muzaffarnagar, Ghaziabad, and Kanpur Nagar, covering up to 12 acres per hour with greater precision and reduced labor. Implemented through the Atmanirbhar Krishak Samanvit Vikas Yojana and the Agriculture Infrastructure Fund, the initiative also included farmer training and plans for expansion to more districts.

Market Dynamics:

Growth Drivers:

Why is the Indian Pesticides Market Growing?

Intensification of Agricultural Practices

The gradual shift toward intensive farming systems is strengthening pesticide usage across major crop-growing regions. Multiple cropping cycles, high-yield seed varieties, and expanded irrigation coverage increase vulnerability to pests and plant diseases. Intensive cultivation often creates favorable conditions for rapid pest multiplication, requiring timely intervention through crop protection products. Commercial farming operations prioritize consistent quality and uniform output, reinforcing the need for reliable pest control measures. As farming practices evolve toward higher productivity models, pesticide usage remains a critical component in managing biological threats and protecting investments made in seeds, fertilizers, and irrigation infrastructure.

Technological Advancements in Formulations

Innovation in pesticide formulations is supporting market growth by improving product performance and safety. Development of advanced molecules, controlled-release formulations, and combination products enhances efficacy against resistant pest strains. Improved formulation technologies also aim to reduce environmental impact and optimize dosage efficiency. Manufacturers are investing in research and development (R&D) to introduce differentiated products tailored to specific crops and climatic conditions. The availability of technologically advanced solutions strengthens farmer confidence and encourages product upgrades. Continuous innovation in formulation science is expanding application versatility and reinforcing the long-term demand for crop protection products in India.

Emergence of Crop-Specific Protection Solutions

The growing availability of crop-specific pesticide formulations is supporting targeted pest management strategies. Manufacturers are developing products tailored to particular crops, pest types, and regional climatic conditions. Customized solutions enhance efficacy while minimizing unnecessary application. Farmers increasingly prefer specialized products that address precise agronomic challenges. The emphasis on crop-specific innovation is encouraging diversification within product portfolios and expanding the range of solutions available to cultivators across various agricultural segments. For instance, in 2026, FMC India launched Tirracto, a new insecticide for sugarcane offering broad-spectrum control against key pests. The premix combines Rynaxypyr and Clothianidin to deliver systemic and contact action, targeting termites, white grubs, and shoot borers. The company said the one-shot solution supports better crop establishment, improved tillering, and higher yields without harming soil health.

Market Restraints:

What Challenges the Indian Pesticides Market is Facing?

Growing Regulatory Restrictions on Chemical Pesticides

Increasing regulatory scrutiny and periodic bans on specific chemical active ingredients are constraining the market growth. The government's evolving pesticide registration framework, combined with stricter residue limits aligned with international standards, is narrowing the range of permissible products and compelling manufacturers to reformulate portfolios, adding development costs and creating uncertainty in the market.

Rising Adoption of Alternative Pest Management Practices

The expanding adoption of integrated pest management, organic farming, and biological control methods is steadily reducing reliance on synthetic chemical pesticides in India. Policy support for natural farming practices and increasing consumer preference for residue-free food are encouraging farmers to adopt safer crop protection alternatives, intensifying competitive pressure on conventional pesticide manufacturers and distributors.

Prevalence of Counterfeit and Substandard Products

The widespread circulation of counterfeit and adulterated pesticides in the Indian market erodes farmer confidence, reduces crop protection effectiveness, and damages legitimate manufacturer revenues. Estimates suggest that fake products may account for a significant portion of the market, undermining agricultural productivity and the overall credibility of the crop protection value chain.

Competitive Landscape:

The Indian pesticides market is characterized by intense competition among established domestic manufacturers and multinational crop protection companies operating across diverse product categories and price segments. Companies are competing through portfolio diversification, new product launches, formulation innovation, and expansion of distribution networks to capture market share. Strategic investments in research activities, backward integration of manufacturing capabilities, and partnerships with agricultural technology platforms are shaping the competitive dynamics. The market is also witnessing increasing competition from biopesticide manufacturers as sustainability considerations influence procurement decisions. Digital marketing, farmer engagement programs, and advisory-based selling models are becoming critical differentiators as companies seek to strengthen brand loyalty and expand their geographic footprint across India's diverse agricultural markets.

Recent Developments:

- August 2025: Kan Biosys launched its ROFA™ range of 100% water-soluble specialty fertilizers and three CIB-registered neem-based biopesticides at an event in Pune. Developed with De Sangosse, the ROFA™ portfolio included 12 crop-specific fertilizers aimed at precise nutrition, improved yield, and soil health, supported by over two decades of agronomic research. The company said the launch marks a major step toward sustainable, residue-free farming and improved profitability for Indian farmers.

- September 2025: Corteva Agriscience launched two new pesticides in India targeting Downy Mildew in grapes and Late Blight in potatoes. Based on its Zorvec technology, the product Zorvec Entecta offered quick rainfast protection within 20 minutes of spraying and long-lasting disease control. The company said the launch was expected to reduce crop losses, improve yields, and enhance profitability for grape and potato farmers.

Indian Pesticides Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | INR Billion |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product types Covered | Synthetic Pesticides, Biopesticides |

| Segments Covered | Insecticides, Fungicides, Herbicides, Others |

| Formulations Covered | Liquid, Dry |

| Crop Types Covered | Cereals, Fruits, Vegetables, Plantation Crops, Others |

| States Covered | Uttar Pradesh, Punjab, Maharashtra, Rajasthan, Haryana, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Pesticides Market Report

The Indian pesticides market size was valued at INR 274.87 Billion in 2025.

The Indian pesticides market is expected to grow at a compound annual growth rate of 5.49% from 2026-2034 to reach INR 464.27 Billion by 2034.

Synthetic pesticides dominate the market with 97.0% revenue share in 2025, driven by their proven efficacy across diverse pest categories, widespread availability through established distribution channels, and strong farmer preference for conventional crop protection solutions.

Key factors driving the Indian pesticides market include the rising development and commercialization of eco-friendly biopesticides, supported by regulatory pressure and residue compliance needs, as seen in ICAR-IISR’s 2025 Lecanicillium psalliotae-based solution for cardamom thrips, validated through Kerala field trials and cleared for licensing.

Major challenges include the growing regulatory restrictions on specific chemical active ingredients, rising adoption of alternative pest management practices such as organic farming and integrated pest management, prevalence of counterfeit products, and increasing environmental and health concerns driving demand shifts toward biological alternatives.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade