Indian Sanitary Napkin Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Indian Sanitary Napkin Market Size, Share, Trends & Forecast (2026-2034)

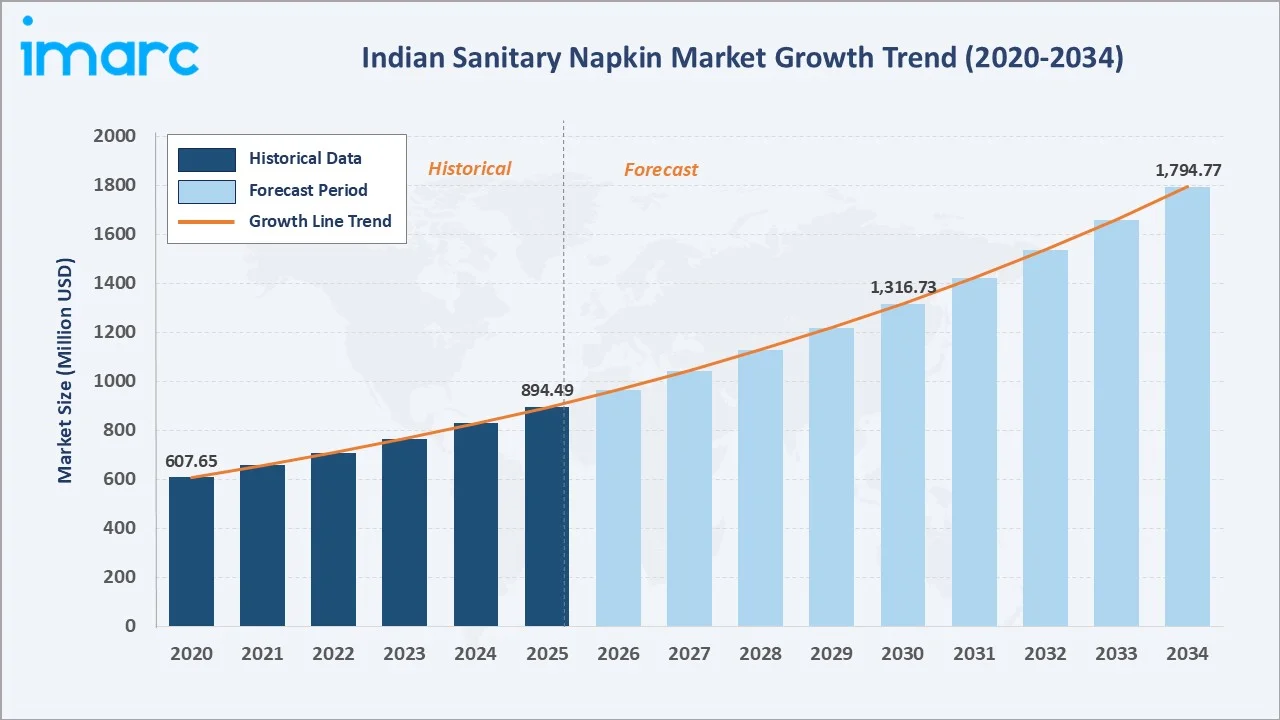

The Indian sanitary napkin market reached USD 894.49 Million in 2025 and is projected to reach USD 1,794.77 Million by 2034, growing at a CAGR of 8.04% during 2026-2034. The market is driven by rising menstrual hygiene awareness, improving female literacy, and expanding access to affordable products through government and NGO initiatives. In India, the National Family Health reports that over 70% of females living in urban areas and 48% of females in rural India use sanitary napkins. This growing adoption indicates expanding demand potential, particularly in rural areas, is driving market expansion by encouraging wider distribution, affordable product offerings, and menstrual hygiene awareness initiatives. Disposable menstrual pads dominate at 72.0%. Pharmacies lead distribution at 31.0%. Maharashtra commands 20.0% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 894.49 Million |

|

Forecast Market Size (2034) |

USD 1,794.77 Million |

|

CAGR (2026-2034) |

8.04% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Disposable Menstrual Pads (72.0%, 2025) |

|

Dominant Distribution Channel |

Pharmacies (31.0%, 2025) |

|

Leading Region |

Maharashtra (20.0%, 2025) |

India's sanitary napkin market expanded from USD 607.65 Million in 2020 to USD 894.49 Million in 2025, anchored at USD 1,316.73 Million in 2030, and forecast to reach USD 1,794.77 Million by 2034. The sanitary napkin penetration gap in India represents the market's most commercially significant structural growth driver.

To get more information on this market, Request Sample

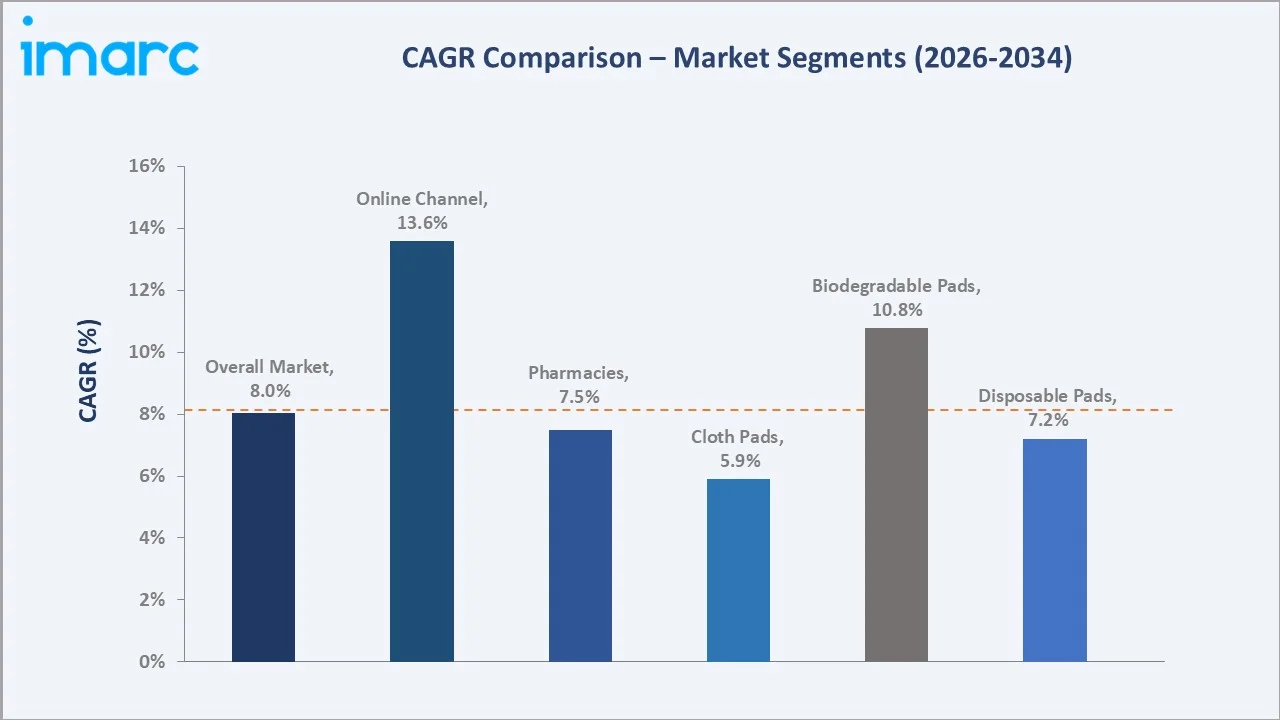

Biodegradable pads grow fastest at ~10.8% CAGR through eco-product demand from urban millennial consumers, rising FMCG brand sustainability commitments, and the government's growing recognition of plastic sanitary napkin waste as an environmental priority. The online channel is growing at ~13.6% CAGR, as 4G/5G rural smartphone penetration, social commerce expansion, and D2C subscription models collectively make it the fastest-growing sanitary napkin purchase channel in India.

Executive Summary

The Indian sanitary napkin market reached USD 894.49 Million in 2025, representing one of the most commercially significant menstrual hygiene markets by opportunity gap. The Indian sanitary napkin market operates at the intersection of FMCG commercial competition, government menstrual hygiene program implementation, and social development. The market is projected to reach USD 1,794.77 Million by 2034.

Disposable menstrual pads at 72.0% dominate through Whisper and Stayfree's distribution infrastructure, reaching Indian retail outlets and the commercial accessibility of entry-level pad pricing that creates the mass market volume. Pharmacies at 31.0% leads the market by distribution channel. Maharashtra leads regionally at 20.0%.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Disposable Menstrual Pads - 72.0% share (2025) |

|

Dominant Distribution Channel |

Pharmacies - 31.0% market share (2025) |

|

Leading Region |

Maharashtra - 20.0% market share (2025) |

|

Market Opportunity |

Rural menstrual hygiene government schemes; biodegradable pad innovation; D2C online brand growth; GST reduction advocacy; period poverty elimination programmes; institutional and school-level distribution |

Key Analytical Observations Supporting the Above Data:

- Disposable Menstrual Pads at 72.0%: The disposable menstrual pads dominate due to their wide availability, affordability, ease of use, and strong consumer familiarity. Higher adoption across both urban and rural areas, supported by retail and government distribution channels, further strengthens its leading share.

- Pharmacies at 31.0%: The pharmacies dominate due to easy accessibility, consumer trust, and the availability of multiple branded products. Pharmacists also provide a discreet and reliable purchase channel, especially in urban and semi-urban areas.

- Maharashtra at 20.0%: Maharashtra dominates due to its large urban population, higher female literacy, strong retail/pharmacy network, and rising menstrual hygiene awareness. Higher disposable incomes and better access to branded hygiene products further support market growth in the state.

Indian Sanitary Napkin Market Overview

The Indian sanitary napkin market is growing steadily, driven by rising menstrual hygiene awareness, increasing female literacy, and improved access to affordable hygiene products. Government initiatives, expanding retail and pharmacy networks, and growing demand for disposable and eco-friendly pads are further supporting market expansion across urban and rural areas.

The sanitary napkin ecosystem integrates raw material suppliers, multinational FMCG manufacturers, Indian biodegradable innovators, government distribution schemes, multi-channel retail, and the menstrual health NGO ecosystem, creating India's uniquely complex feminine hygiene market where commercial, government, and social development objectives intersect at every channel, price point, and geographic level simultaneously.

Market Dynamics

To evaluate market opportunities, Request Sample

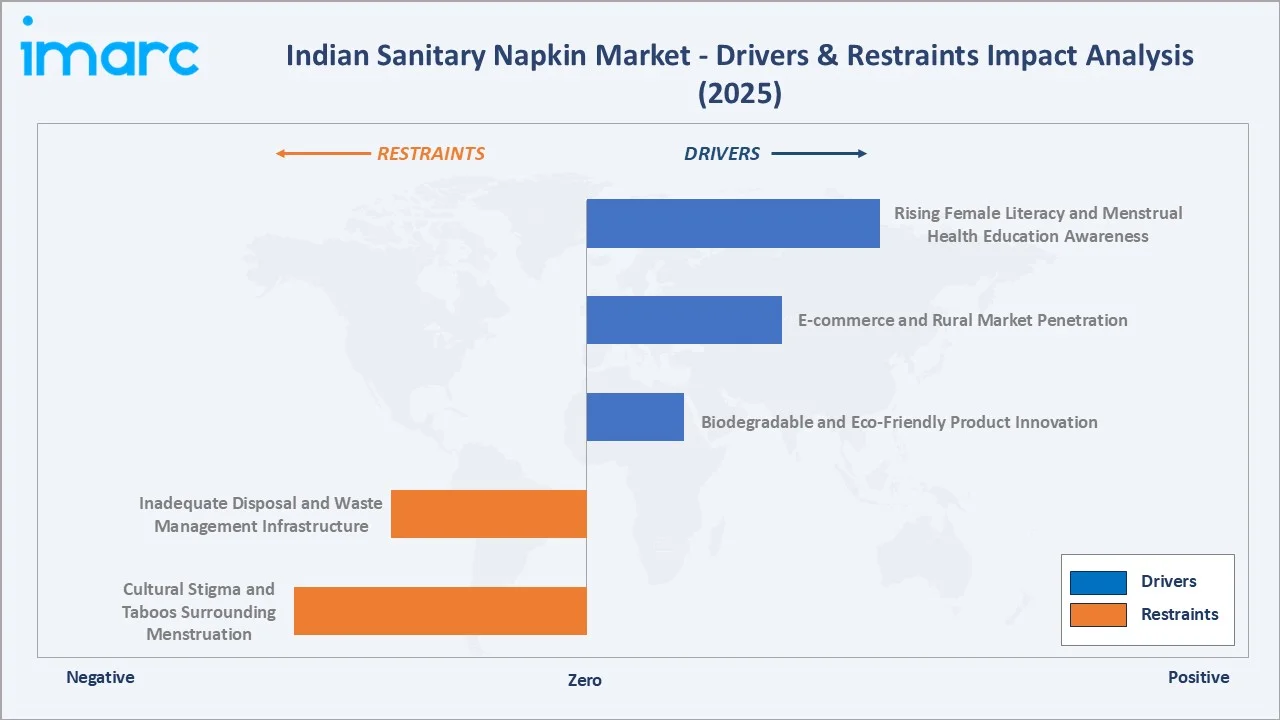

Market Drivers

- Rising Female Literacy and Menstrual Health Education Awareness: According to the Periodic Labour Force Survey (PLFS) 2023–24, the female literacy rate in India reached nearly 74.6% among women aged 7 years and above. Rising literacy levels are supporting menstrual health education awareness by enabling women to better understand hygiene practices, health risks, and the benefits of sanitary napkin usage. Increased awareness through education, schools, and digital platforms is encouraging the adoption of hygienic menstrual products, thereby driving the growth of the Indian sanitary napkin market. Greater awareness about the health risks associated with unhygienic alternatives has increased the preference for sanitary napkins. In addition, improved access to information through digital media and healthcare outreach programs is boosting product acceptance across rural and urban areas.

- E-commerce and Rural Market Penetration: E-commerce and rural market penetration are improving product accessibility beyond traditional retail channels. Online platforms offer wider product choices, discreet purchasing, discounts, and doorstep delivery, encouraging more women to adopt sanitary napkins. Meanwhile, rural distribution through pharmacies, kirana stores, NGOs, and government initiatives is expanding reach in underserved areas. This growing availability is helping convert low-penetration regions into key growth markets.

- Biodegradable and Eco-Friendly Product Innovation: Biodegradable and eco-friendly product innovation addressing growing concerns over plastic waste and disposal challenges. Brands are introducing organic cotton, bamboo-based, compostable, and chemical-free pads to attract environmentally conscious consumers. These products also appeal to women seeking safer and skin-friendly menstrual hygiene options. Rising sustainability awareness and premium product demand are encouraging companies to expand their eco-friendly sanitary napkin portfolios.

Market Restraints

- Inadequate Disposal and Waste Management Infrastructure: An estimated 121 million women and adolescent girls use 8 sanitary napkins on average every month in India; this generates 113,000 tons of menstrual waste annually. This inadequate disposal and waste management infrastructure creates concerns over the safe disposal of used sanitary products. Limited availability of disposal bins, incinerators, and proper waste collection systems, especially in rural and semi-urban areas, discourages regular product usage. Environmental concerns related to plastic-based sanitary pads further affect consumer perception and adoption. These challenges are increasing the demand for sustainable alternatives while restraining the growth of conventional disposable sanitary napkins.

- Cultural Stigma and Taboos Surrounding Menstruation: Cultural stigma and taboos surrounding menstruation limit open discussions about menstrual hygiene. Many women, especially in rural areas, feel hesitant to purchase sanitary napkins due to embarrassment or social restrictions. Myths and a lack of family support also reduce awareness and product adoption. As a result, some consumers continue using traditional alternatives, slowing market penetration.

Market Opportunities

- Period Poverty Elimination Creating New Market Entrants: Efforts to eliminate period poverty are creating significant opportunities by encouraging greater access to affordable menstrual hygiene products. Government programs, NGOs, and social enterprises are supporting low-cost sanitary napkin distribution in underserved communities. This has attracted new market entrants offering economical, reusable, and eco-friendly products tailored to rural and low-income consumers. Increasing awareness and demand in previously untapped regions are further expanding growth opportunities for manufacturers.

- Institutional and Workplace Menstrual Hygiene Supply: Institutional and workplace menstrual hygiene supply is creating new opportunities as schools, colleges, offices, and public institutions increasingly provide sanitary products to support women’s health and hygiene. Government initiatives and corporate wellness programs are encouraging the installation of sanitary napkin vending machines and disposal units in workplaces and educational institutions. This growing institutional demand is expanding bulk procurement opportunities for manufacturers. In addition, rising focus on employee well-being and menstrual health awareness is supporting long-term market growth.

Market Challenges

- Preference for traditional menstrual alternatives in some regions: Preference for traditional menstrual alternatives in some regions is slowing the shift toward commercial hygiene products. Many women continue using cloth or other reusable materials due to affordability, familiarity, limited awareness, or cultural habits. This reduces demand for sanitary napkins, especially in rural and low-income areas. As a result, companies need stronger awareness campaigns, affordable pricing, and wider rural outreach to improve adoption.

- Lack of access to proper sanitation facilities in certain areas: Lack of access to proper sanitation facilities in certain areas limits the safe and convenient use of sanitary products. In many rural and underserved regions, inadequate access to clean toilets, water supply, and disposal systems discourages regular sanitary napkin usage. Women often face difficulties in changing and disposing of pads hygienically, leading to continued reliance on traditional alternatives. These infrastructure gaps hinder market penetration and slow the adoption of menstrual hygiene products.

Emerging Market Trends

1. D2C Brand Revolution Challenging Multinational FMCG Dominance

The D2C brand revolution is emerging as local startups offer affordable, organic, biodegradable, and customized menstrual hygiene products. These brands use e-commerce, social media, and subscription models to reach consumers directly and build strong customer loyalty. Their focus on transparency, sustainability, and women-centric branding is challenging the dominance of multinational FMCG players. This is increasing competition and encouraging innovation across the market.

2. Menstrual Health as Social Enterprise and Impact Investing Target

Menstrual health is emerging as a social enterprise and impact investing focus in India, as investors support businesses that improve access to affordable sanitary napkins. Startups and NGOs are developing low-cost, biodegradable, and locally manufactured products for rural and underserved communities. This trend is combining commercial growth with social impact by addressing period poverty and hygiene awareness. As a result, more mission-driven brands are entering the Indian sanitary napkin market.

3. Menstrual Cup and Period Underwear Creating Alternative Category Competition

Menstrual cups and period underwear offer reusable, cost-effective, and eco-friendly options, appealing to urban, educated, and sustainability-conscious consumers. Their growing acceptance is encouraging sanitary napkin brands to innovate with biodegradable, organic, and premium product lines. In July 2025, the Thiruvananthapuram Corporation introduced an initiative to distribute 25,000 menstrual cups to girl students in government schools across the city. The project aims to promote menstrual hygiene while encouraging the use of reusable, healthy, sustainable, and cost-effective alternatives to sanitary napkins, which contribute to waste generation. Such initiatives are increasing awareness and acceptance of reusable products, encouraging sanitary napkin brands to innovate with biodegradable and sustainable offerings.

4. Plastic Waste Regulation Creating Structural Shift Toward Biodegradable Product Certification

Plastic waste regulations are creating a structural shift by pushing manufacturers to reduce plastic content and adopt biodegradable materials. Brands are increasingly seeking eco-friendly and compostable product certifications to build consumer trust and meet sustainability standards. This is encouraging innovation in organic cotton, bamboo fiber, and plant-based absorbent materials. As a result, biodegradable sanitary napkins are gaining traction as a long-term growth segment.

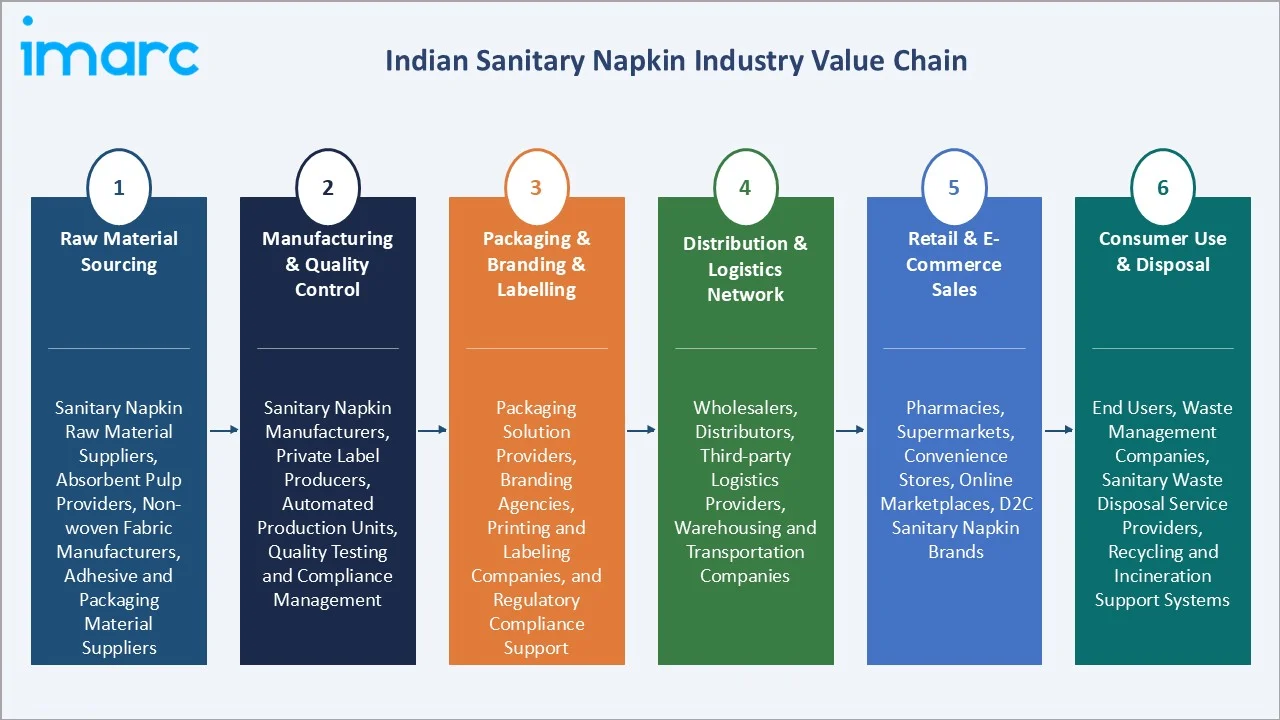

Industry Value Chain Analysis

India's sanitary napkin value chain integrates imported raw material sourcing, domestic manufacturing, packaging, branding, and labelling, distribution and logistics, retail and e-commerce, and consumer use and disposal.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Sanitary napkin raw material suppliers, absorbent pulp providers, non-woven fabric manufacturers, adhesive and packaging material suppliers |

|

Manufacturing & Quality Control |

Sanitary napkin manufacturers, private label producers, automated production units, quality testing and compliance management |

|

Packaging & Branding & Labelling |

Packaging solution providers, branding agencies, printing and labeling companies, and regulatory compliance support |

|

Distribution & Logistics Network |

Wholesalers, distributors, third-party logistics providers, warehousing and transportation companies |

|

Retail & E-Commerce Sales |

Pharmacies, supermarkets, convenience stores, online marketplaces, D2C sanitary napkin brands |

|

Consumer Use & Disposal |

End users, waste management companies, sanitary waste disposal service providers, recycling and incineration support systems |

The manufacturing stage is the value chain's most commercially concentrated phase. The distribution stage's complexity creates the distribution reach advantage that established multinational brands maintain above Indian D2C challengers.

Technology Landscape in the Indian Sanitary Napkin Industry

Absorbent Core Technology Evolution

The evolution of absorbent core technology improves product comfort, absorption capacity, and leakage protection. Manufacturers are increasingly adopting superabsorbent polymers (SAP), ultra-thin core designs, and breathable layers to enhance user convenience and hygiene. These innovations are helping brands differentiate their products and attract premium consumers. In addition, advanced absorbent technologies are supporting the development of lighter, skin-friendly, and high-performance sanitary napkins.

Manufacturing Process Technology for Low-Cost Pad Production

Manufacturing process technology for low-cost pad production, enabling affordable and large-scale manufacturing. Companies are adopting automated and semi-automated production systems to reduce labor costs, improve efficiency, and increase output. Compact manufacturing machines and localized production units are also helping small enterprises and NGOs produce low-cost sanitary napkins for rural markets. These technological advancements are improving product accessibility and supporting wider menstrual hygiene adoption across India.

Digital Health and Period Tracking Technology

Digital health and period tracking technology are increasing consumer engagement and personalized menstrual care. Brands are integrating mobile apps, AI-based cycle tracking, and health monitoring features to help women manage menstrual health more effectively. In December 2024, Asan introduced a 100% free period tracking app to help Indian women better understand and manage their menstrual cycles. The app offers built-in analytics and insights, serving as a digital health companion from puberty through menopause. These technologies also enable companies to gather consumer insights and offer customized product recommendations. As awareness of menstrual wellness grows, digital platforms are strengthening brand loyalty and expanding the scope of smart feminine hygiene solutions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Disposable Menstrual Pads |

72.0% |

2025 |

|

Distribution Channel |

Pharmacies |

31.0% |

2025 |

|

Region |

Maharashtra |

20.0% |

2025 |

By Product Type

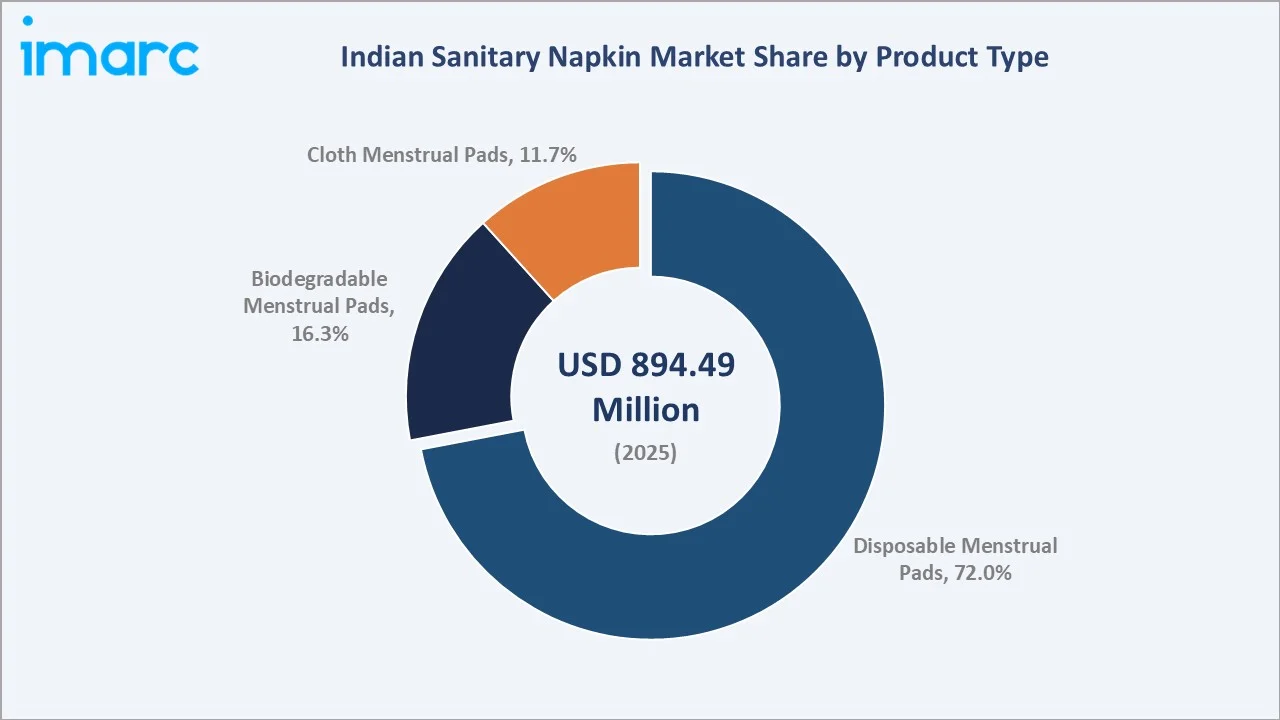

Disposable menstrual pads lead at 72.0% (2025). The disposable menstrual pads segment dominates due to its convenience, affordability, and easy availability across pharmacies, supermarkets, and online channels. Strong consumer familiarity and preference for single-use hygiene products support higher adoption. Wide distribution through government, NGO, and retail networks further strengthens its market share.

To access detailed market analysis, Request Sample

Biodegradable menstrual pads at 16.3% represent the fastest-growing commercial segment at ~10.8% CAGR, driven by emerging eco-brand competition supported by biodegradable certification. Cloth menstrual pads at 11.7% represent both the traditional rural cloth use and the emerging urban reusable cloth pad market.

By Distribution Channel

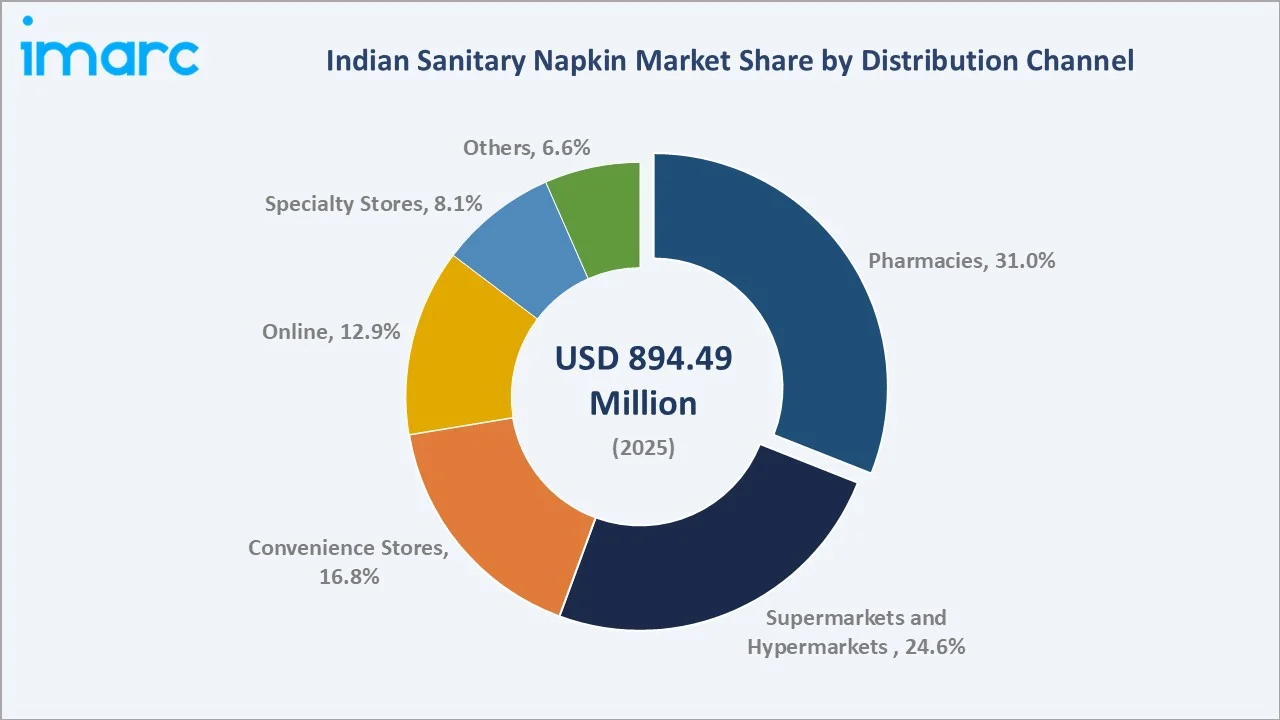

Pharmacies lead at 31.0% (2025). The pharmacy channel encompasses MedPlus, Apollo Pharmacy, and other pharmacy outlets as the primary trusted sanitary napkin purchase point for urban and semi-urban Indian women. Pharmacy's ~7.5% CAGR reflects premium brand growth as urban consumers trade.

Supermarkets and hypermarkets at 24.6% reflect D-Mart, Reliance Fresh, Smart Bazaar, and other supermarkets and hypermarkets' modern trade sanitary napkin sales, where promotional pricing and category adjacency with other FMCG personal care creates impulse and planned purchase. Convenience stores at 16.8% represent India's kiranas as the sanitary napkin distribution backbone in Tier-2, Tier-3, and rural markets. Online at 12.9% grows fastest at ~13.6% CAGR through D2C subscription brands and Amazon/Flipkart e-commerce penetration into smaller Indian towns.

Regional Market Insights

|

Region |

Share (2025) |

Key Indian Sanitary Napkin Market Drivers & Characteristics |

|

Maharashtra |

20.0% |

Driven by a large urban population, strong retail infrastructure, high female literacy, and increasing awareness regarding menstrual hygiene products. |

|

Delhi-NCR |

17.6% |

Supported by high disposable income levels, strong pharmacy and e-commerce penetration, and growing demand for premium and organic sanitary napkin products. |

|

Tamil Nadu |

15.3% |

Driven by high literacy rates, government menstrual hygiene initiatives, and increasing adoption of sanitary napkins across educational institutions and rural communities. |

|

Karnataka |

13.4% |

Driven by an urban consumer base, a rising working women population, and an increasing preference for technologically advanced and eco-friendly hygiene products. |

|

Gujarat |

11.2% |

Supported by improving healthcare awareness, expanding retail distribution, and growing demand from semi-urban and rural consumers. |

|

Others |

22.5% |

The others category includes the remaining Indian states and Union Territories, where market growth is supported by rising menstrual hygiene awareness, government distribution programs, and increasing rural penetration. |

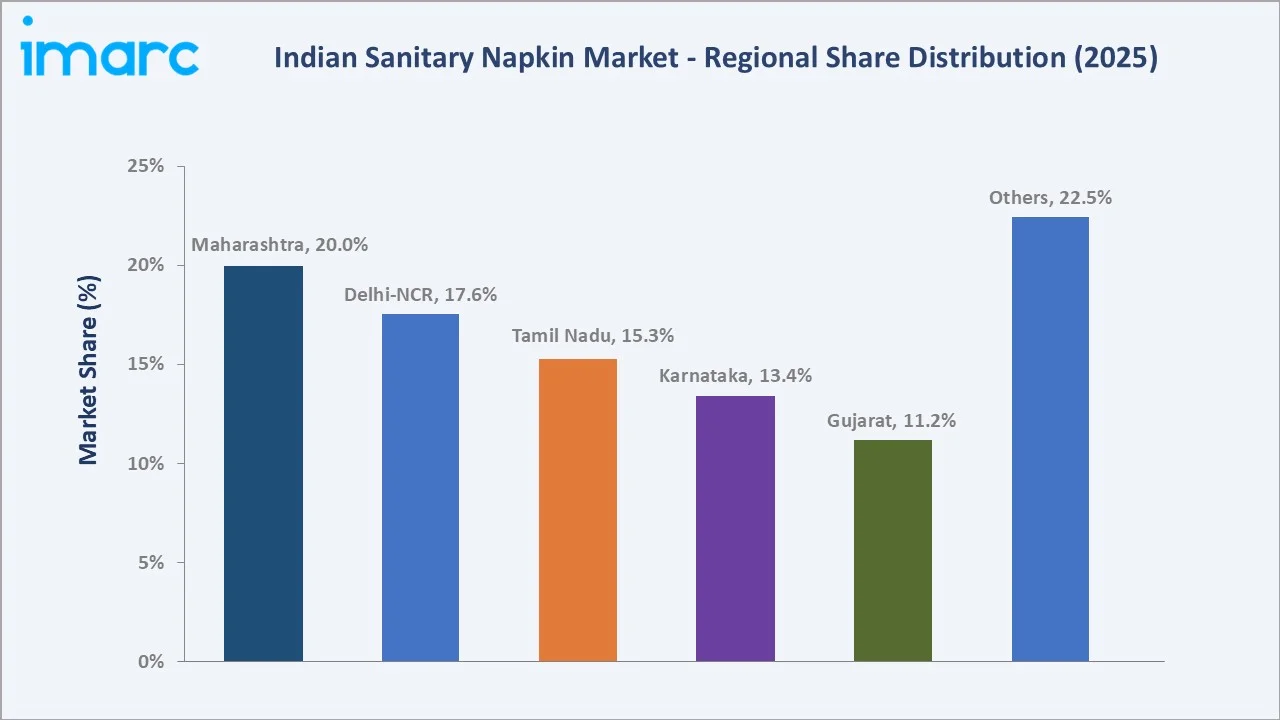

Maharashtra and Delhi-NCR's combined 37.6% market share reflects India's two most economically active metropolitan states, providing the premium pad value concentration. Tamil Nadu and Karnataka's combined 28.7% reflects South India's above-national-average female literacy, government scheme infrastructure, and D2C brand presence, creating above-proportional FMCG feminine hygiene market development.

Gujarat's 11.2% reflects above-average economic productivity and an emerging biodegradable product manufacturing base. The others category at 22.5%, encompassing Uttar Pradesh, Rajasthan, Bihar, Madhya Pradesh, West Bengal, and all other states, represents India's most commercially under-penetrated but highest-potential regional market.

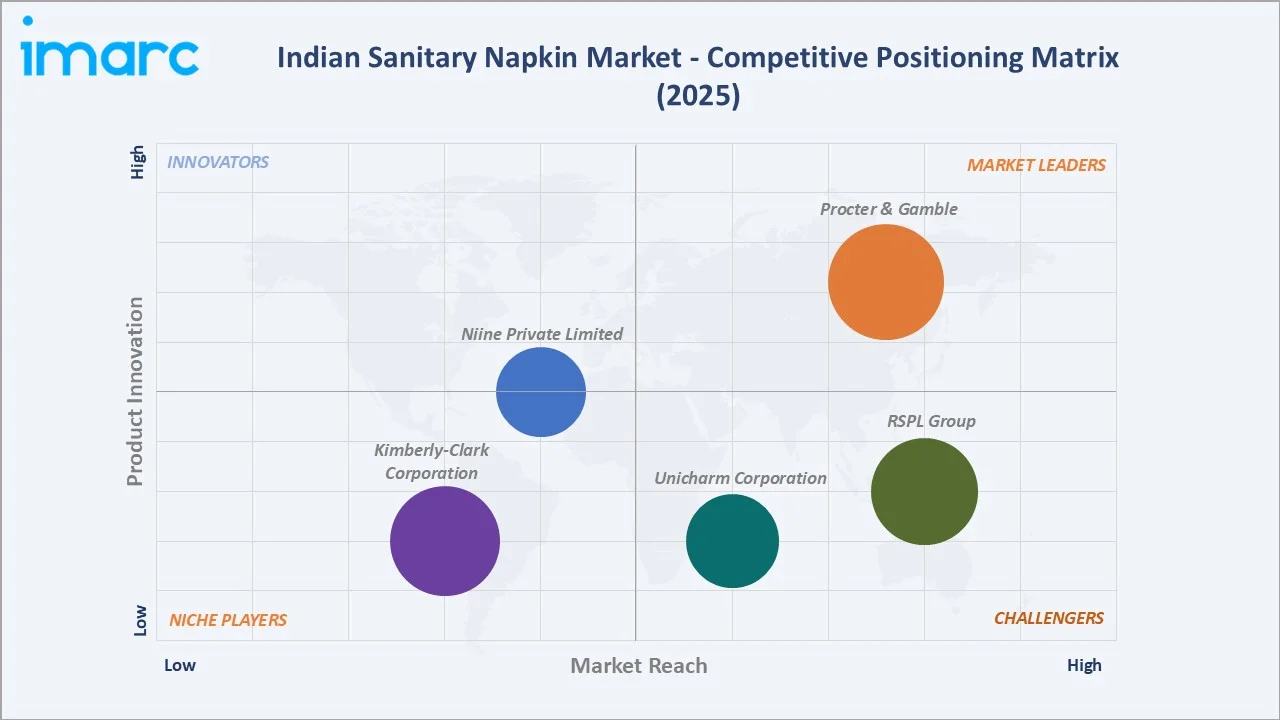

Competitive Landscape

India's sanitary napkin market competitive landscape is evolving from a two-brand MNC duopoly toward a multi-tier competitive structure encompassing MNC leaders, Indian conglomerates, Indian biodegradable innovators, and D2C premium startups.

|

Company Name |

Key Brands |

Market Position |

Core Strength |

|

Procter & Gamble |

Whisper |

Market Leader |

Procter & Gamble holds a dominant position through its brand Whisper, which is a market leader. |

|

Kimberly-Clark Corporation |

Kotex |

Niche Player |

Kimberly-Clark Corporation plays a significant role through its premium feminine hygiene brand, Kotex. |

|

RSPL Group |

Pro-ease |

Strong Challenger |

RSPL Group plays a significant role in the Indian sanitary napkin market through its brand Pro-Ease, positioning itself as a value-for-money, high-quality player. |

|

Unicharm Corporation |

Sofy |

Strong Challenger |

Unicharm Corporation is a major player in the Indian sanitary napkin market, primarily through its brand Sofy. Unicharm focuses on high-quality, innovative feminine care, aimed at improving menstrual hygiene and reducing discomfort. |

|

Niine Private Limited |

Niine |

Established Player |

Niine Private Limited plays a significant role in the Indian sanitary napkin market by prioritizing affordable, eco-friendly, and accessible menstrual hygiene products while actively challenging taboos through awareness campaigns. |

The competitive landscape is additionally shaped by India's GST rate for sanitary napkins, creating pricing transparency pressure, all brands operating on zero GST, creating a level playing field where import content cost is the primary manufacturing cost differentiator between Indian-manufactured pads and imported or MNC pads with higher supply chain sophistication.

Key Company Profiles

Procter & Gamble

Procter & Gamble is one of the leading players in the Indian sanitary napkin market through its well-known feminine hygiene brand, Whisper. The company has a strong presence across urban and rural India, supported by extensive retail, pharmacy, and e-commerce distribution networks.

- Key Brands: Whisper

- Recent Developments: In January 2026, Whisper India introduced a new range of period panties, promoted by cricketer Jemimah Rodrigues. Offering 360-degree protection, the product is designed for active young women seeking greater comfort, convenience, and freedom compared to traditional sanitary pads.

- Strategic Focus: Product innovation, premiumization, and expanding its Whisper portfolio with pads and period panties.

RSPL Group

RSPL Group is an Indian FMCG company with a growing presence in the sanitary napkin market through its feminine hygiene brand offerings. The company leverages its strong distribution network, extensive rural reach, and experience in consumer goods to expand access to affordable menstrual hygiene products across India.

- Key Brands: Pro-ease.

- Strategic Focus: Expanding affordable sanitary napkin offerings for mass-market, semi-urban, and rural consumers.

Market Concentration Analysis

India's sanitary napkin market is highly concentrated at the branded volume tier. This concentration reflects 35+ years of brand-building investment and distribution infrastructure development that cannot be replicated by new entrants in short timeframes. The unbranded and government scheme market represents an additional estimated USD 100-150 Million in sanitary napkin value that is competed for by domestic manufacturers and local manufacturers rather than MNC brands.

Market concentration is declining at the premium urban tier. The D2C market concentration is itself fragmented, with no single D2C brand achieving the scale to challenge multinational pharmacy channel dominance but collectively creating a premium ecosystem that is progressively attracting venture capital, media attention, and consumer trial that may catalyse consolidation through acquisition.

Investment & Growth Opportunities

Highest Growth Segments

Biodegradable menstrual pads (~10.8% CAGR), online distribution channel (~13.6% CAGR), rural market penetration (UP, Bihar, Rajasthan, MP at estimated 12-15% CAGR from low base), period poverty elimination first-time commercial pad adoption (~15% volume CAGR in government scheme converted markets), D2C premium subscription segment (~20% CAGR in urban Tier-1 cities), and corporate institutional supply (~18% CAGR) represent India's highest-growth sanitary napkin investment vectors through 2034.

Emerging Investment Opportunities

India's rural sanitary napkin penetration gap represents the market's single largest untapped commercial opportunity. Investment in rural distribution infrastructure positions for above-market revenue as the inevitable rural penetration expansion occurs through 2026-2034.

Investment Themes

- Rural SHG micro-enterprise distribution network for accessible sanitary napkin last-mile supply: Partnering with the government to create a commercial sanitary napkin micro-distribution system that reaches the Indian villages where pharmacies and modern trade retail do not exist. SHG distribution model economics create shared value above pure commercial distribution.

- D2C period care subscription platform creating high-LTV urban premium period care consumer relationships: India's urban millennial and Gen Z women with smartphones, digital payment capability, and demonstrated premium FMCG spending represent the addressable market for a period care D2C subscription platform offering biodegradable or organic certified pads, complementary intimate hygiene, and menstrual health content at a subscription equivalent.

Future Market Outlook (2026-2034)

India's sanitary napkin market is projected to grow from USD 894.49 Million in 2025 to USD 1,794.77 Million by 2034, delivering an 8.04% CAGR over the forecast period. The market's anchor value of USD 1,316.73 Million in 2030 represents the Indian sanitary napkin industry at its most transformative commercial inflection. Rural market penetration will have reached 50-55% through the combined effect of government scheme foundation and commercial market development, biodegradable pads will have crossed 25% market share as regulatory standards create mandatory eco-product transformation, and online channels will have reached 20-22% of total sanitary napkin distribution through rural e-commerce expansion and D2C subscription normalization.

Three structural forces define India's sanitary napkin market growth through 2034 with certainty. India's demographic dividend creates a mathematically certain consumer base expansion that no commercial downside can reverse, given the fundamental personal hygiene need driving demand. Government investment in menstrual hygiene access. The biodegradable product transition driven by regulatory evolution and consumer eco-consciousness creates market value growth above volume growth as consumers trade up from conventional pads toward certified biodegradable alternatives over the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including Business Development Directors, Marketing Directors, Founders, government scheme managers, NGO programme managers, and retail category managers.

Secondary Research

Secondary research encompassed the National Family Health Survey, demographic updates, Solid Waste Management Rules and guidelines for sanitary napkins, Absorbent Hygiene Products for Women standard, Menstrual Hygiene Policy, annual report, India retail audit data for sanitary napkin market share (secondary analysis), company annual reports, and India Internet Report. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using penetration-based growth model: (i) menstruating female population by state; (ii) menstrual hygiene protection rate by state; (iii) commercial sanitary napkin product type split applied to commercially active menstrual hygiene users; (iv) average revenue per user by product type and state income bracket; (v) distribution channel mix evolution based on e-commerce penetration trend and pharmacy versus modern trade shift.

Indian Sanitary Napkin Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Disposable menstrual pads, Cloth menstrual pads and Biodegradable menstrual pads |

| Distribution Channels Covered |

Supermarkets and Hypermarkets, Pharmacies, Convenience Stores, Online, Specialty Stores and Others |

| Regions Covered | Maharashtra, Delhi-NCR, Tamil Nadu, Karnataka, Gujarat, Others |

| Companies Covered | Procter & Gamble, Kimberly-Clark Corporation, RSPL Group, Unicharm Corporation, Niine Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Sanitary Napkin Market Report

India's sanitary napkin market reached USD 894.49 Million in 2025. Disposable menstrual pads dominate at 72.0% through Whisper's distribution infrastructure covering Indian retail outlets. Pharmacies lead distribution at 31.0% through India's cultural preference for discreet pharmacy sanitary napkin purchase. Maharashtra leads regionally at 20.0% through Mumbai's FMCG concentration and Maharashtra's above-national female literacy and purchasing power.

India's sanitary napkin market grows at 8.04% CAGR during 2026-2034, reaching USD 1,794.77 Million by 2034. Biodegradable pads grow fastest at ~10.8% CAGR through eco-consumer demand and regulatory direction. Online channel grows fastest at ~13.6% CAGR through rural 4G penetration, social commerce, and D2C subscription normalization. The overall market growth is sustained by India's non-commercial menstrual management users converting to commercial pad adoption through government schemes, rural e-commerce, and rising income.

Disposable menstrual pads lead at 72.0% through the commercial maturity built by Whisper.

Pharmacies lead at 31.0% through India's cultural preference for discreet sanitary napkin pharmacy purchase, and pharmacy outlet penetration, creating pharmacy as the default sanitary napkin purchase channel.

Maharashtra leads at 20.0% through Mumbai's FMCG headquarters concentration, Maharashtra's urban female literacy rate, and premium retail infrastructure supporting above-national pad adoption and per-pad trading up.

Leading companies include Procter & Gamble, Kimberly-Clark Corporation, RSPL Group, Unicharm Corporation, and Niine Private Limited, among others.

India's sanitary napkin market is projected to reach approximately USD 1,316.73 Million by 2030, with rural market penetration nationally from baseline through government scheme foundation and rural e-commerce expansion, biodegradable pad market share growth as regulatory compliance incentivises biodegradable product development across all major brands, online channel growth of total distribution as social commerce and rural delivery mature, and D2C premium subscription platforms collectively achieving high revenue.

India's sanitary napkin market faces significant environmental challenges from conventional disposable pad waste. Biodegradable pad adoption, napkin waste composting technology, and Extended Producer Responsibility mandate for sanitary napkin manufacturers collectively represent India's three-track environmental response to the sanitary napkin waste challenge that will progressively transform product design and waste management infrastructure through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)