Indian Solar Electric System and Inverter Market Size, Share, Trends and Forecast by Technology Type, Installation Type, Inverter Type, and Region, 2026-2034

Indian Solar Electric System and Inverter Market Summary:

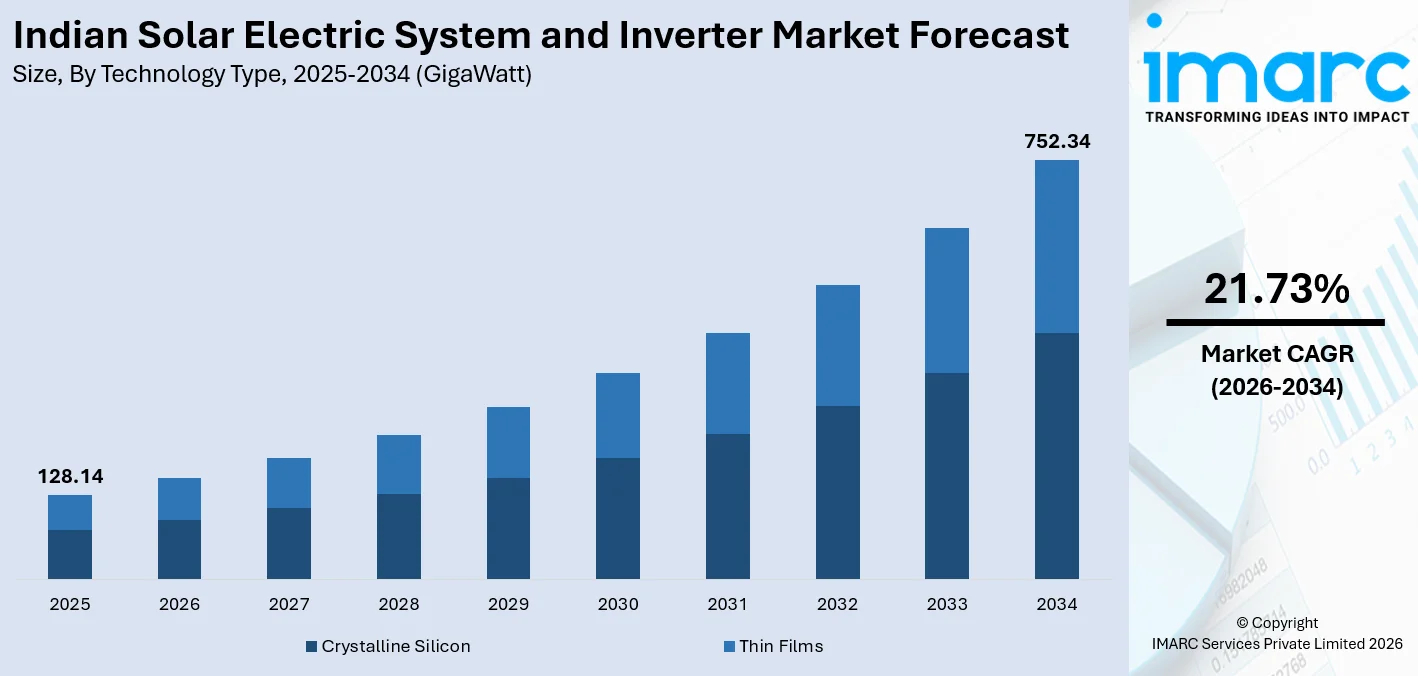

The Indian solar electric system and inverter market size reached 128.14 GigaWatt in 2025 and is projected to reach 752.34 GigaWatt by 2034, growing at a compound annual growth rate of 21.73% from 2026-2034.

The Indian solar electric system and inverter market is experiencing robust momentum as the country accelerates its transition toward clean energy and sustainable power generation. Expanding rooftop adoption, strengthening domestic manufacturing ecosystems, and rising demand for energy-efficient power conversion systems are reshaping the solar landscape. Supportive policy frameworks, growing renewable energy integration across residential and industrial sectors, and advancements in photovoltaic and inverter technologies are reinforcing long-term market expansion, positioning India as a leading destination for solar energy deployment and Indian solar electric system and inverter market share.

Key Takeaways and Insights:

- By Technology Type: Crystalline silicon dominates the market with a 87% share in 2025, due to its inherent efficiency, manufacturing base, and compatibility with newer cell technologies.

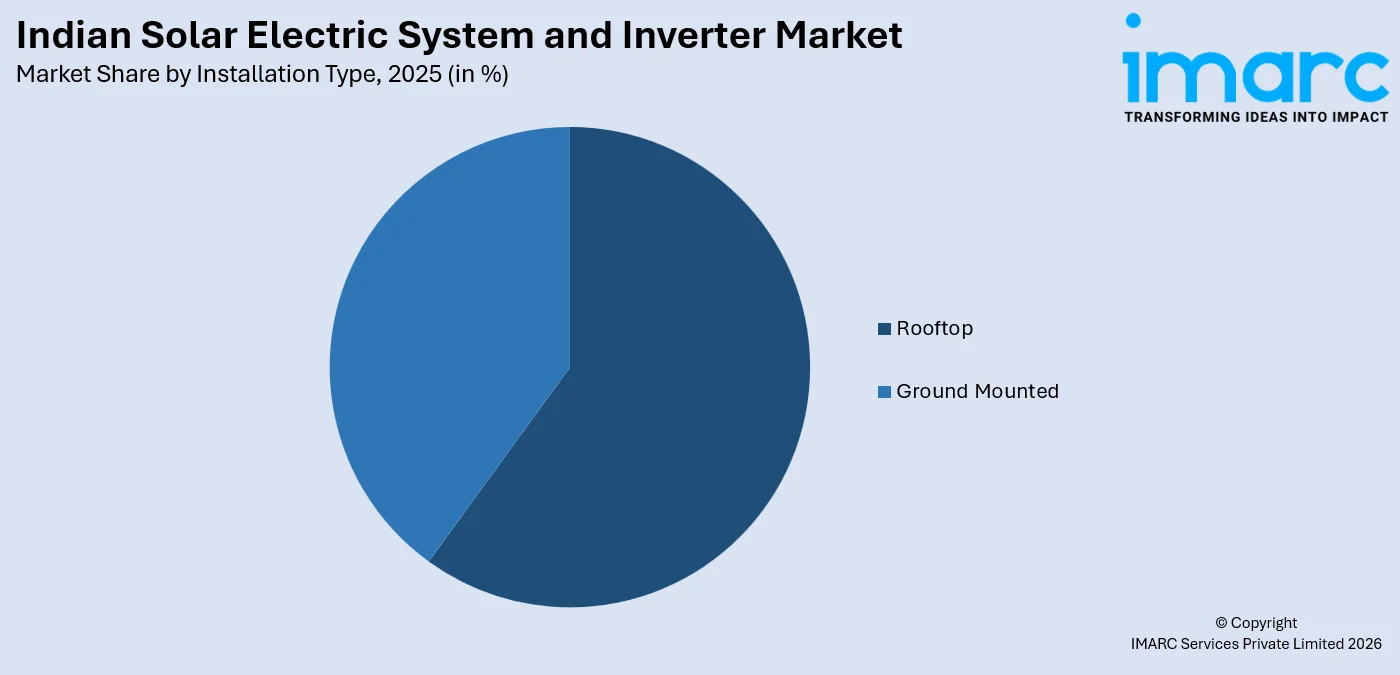

- By Installation Type: Rooftop leads the market with a 60% share in 2025, fuelled by the growing demand for residential and commercial installations through government subsidy schemes and net metering benefits.

- Key Players: The Indian solar electric system and inverter industry has a competitive landscape with major solar panel and solar inverter manufacturers including Vikram Solar Pvt Ltd, Waree Solar Energy Pvt Ltd, Adani Enterprises Ltd, Goldi Green Technologies Pvt Ltd, Tata Power Solar Systems Ltd, Moser Baer Solar Ltd, XL Energy Ltd, Solar Semiconductor Pvt Ltd, Emmvee Photovoltaics Pvt Ltd, Navitas Green Solutions Pvt Ltd, ABB, TMEIC, SMA, Hitachi, Sungrow Power Supply Co., Ltd., Huawei, and Schneider Electric.

To get more information on this market Request Sample

The Indian solar electric system and inverter market is growing significantly with the growth in the Indian renewable energy market and the Indian manufacturing sector. India’s solar capacity has grown by over 40 times in the last ten years, increasing from merely 3 GW in 2014 to around 130 GW in October 2025. Solar energy is currently the largest contributor to India’s renewable energy market. India’s non-fossil fuel capacity of 500 GW by 2030 is still a guiding light for the Indian renewable energy market’s project pipeline, and many investors are investing in the Indian renewable energy market. India’s residential rooftop solar energy market is growing significantly, with the total installed capacity increasing to 20.8 GW in the last quarter of 2025, with the PM Surya Ghar program, under which almost 24 lakh households have been able to adopt solar energy as a source of energy for their homes.

Indian Solar Electric System and Inverter Market Trends:

Rapid Expansion of Rooftop Solar Installations

The rooftop solar sector in India is witnessing unprecedented growth, fueled by government-backed subsidy schemes and digital approval mechanisms. India has successfully installed 7.1 GW of rooftop solar capacity in 2025, witnessing a 122% increase in rooftop solar installations in India, up from 3.2 GW in 2024. Residential consumers contributed to nearly 76% of the total rooftop solar capacity additions, showing promising growth in the Indian solar electric system and inverter market.

Transition to Advanced Photovoltaic Cell Technologies

The Indian solar market is witnessing a rapid shift from traditional mono PERC to advanced solar cell configurations such as TOPCon, HJT, and bifacial cells. These advanced solar cells provide increased energy yield and performance in varying climatic conditions. By 2025, TOPCon solar cells comprised a significant share of domestic solar module production as manufacturers increased their integrated production capacities to meet the increasing demand for high-performance solar systems. Canadian Solar Inc. announced in 2025 the launch of its next-generation Low Carbon (LC) solar modules, which incorporate advanced wafer technology with cutting-edge HJT solar cells. Low Carbon solar modules achieve an unparalleled carbon footprint of just 285 kg CO2e/kW, making it one of the lowest for any silicon-based solar module in the world, setting a new benchmark in green solar manufacturing.

Surge in Domestic Solar Manufacturing Capacity

India’s solar manufacturing ecosystem is expanding at an accelerated pace, supported by policy incentives and rising domestic demand. With Prime Minister Shri Narendra Modi at the helm, the nation has achieved an extraordinary addition of 25 GW in renewable energy capacity, representing a nearly 35% rise compared to last year's increase of 18.57 GW. This rapid scale-up is strengthening supply chain resilience and reducing import dependency across the value chain.

Market Outlook 2026-2034:

India’s solar electric system and inverter market is poised for sustained expansion, underpinned by strong policy continuity, growing rooftop adoption, and a maturing domestic manufacturing base. The market generated a revenue of 128.14 GigaWatt in 2025 and is projected to reach a revenue of 752.34 GigaWatt by 2034, growing at a compound annual growth rate of 21.73% from 2026-2034. Increasing investments in advanced cell technologies, expanding charging infrastructure for energy storage integration, and strengthening grid connectivity are expected to support higher deployment volumes and foster a more competitive, resilient solar ecosystem across the country.

Indian Solar Electric System and Inverter Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Technology Type |

Crystalline Silicon |

87% |

|

Installation Type |

Rooftop |

60% |

Technology Type Insights:

- Crystalline Silicon

- Thin Films

Crystalline silicon leads the market with a share of 87% of the total Indian solar electric system and inverter market in 2025.

The dominance of crystalline silicon technology in India’s solar electric system market is also expected to continue in the future, driven by its existing manufacturing base, high conversion efficiency, and versatility for use in utility-scale and distributed solar systems. The technology also enjoys the advantages of ongoing developments in solar cells, such as the adoption of mono PERC and advanced TOPCon cells to achieve higher energy production from solar systems. The increase in domestic manufacturing capacity in India, enabled by the Production Linked Incentive scheme for high-efficiency solar modules, has further solidified the position of crystalline silicon technology in solar systems.

In addition, increasing demand for crystalline silicon in rooftop, ground-mounted, and hybrid solar applications is further strengthening this segment. Manufacturers are investing in integrated production facilities for wafers, cells, and modules to achieve economies of scale and quality assurance. The Approved List of Models and Manufacturers Mandate has helped accelerate the adoption of crystalline silicon modules manufactured domestically, and the Basic Customs Duty rates for imported cells and modules have helped crystalline silicon products gain a competitive advantage in the market.

Installation Type Insights:

Access the comprehensive market breakdown Request Sample

- Ground Mounted

- Rooftop

Rooftop dominates with a share of 60% of the total Indian solar electric system and inverter market in 2025.

Solar rooftop has been identified as the fastest-growing segment of the solar market in India, with the government offering significant incentives and more and more consumers becoming aware of the importance of solar energy. The PM Surya Ghar: Muft Bijli Yojana scheme, initiated in February 2024 with an allocation of more than INR 75,000 crore, has been successful in encouraging more and more people to adopt solar energy for household purposes with a subsidy of up to INR 78,000 and free electricity up to 300 units monthly. In 2025, cumulative rooftop capacity stood at 20.8 GW.

The rooftop segment is benefiting from positive net metering policies, decreasing costs of systems, and increased adoption of digital approval systems to facilitate installation. Commercial and industrial customers are increasingly opting for rooftop solar systems to save on their electricity costs and to achieve their corporate social responsibility goals. Additionally, time-of-the-day tariffs and new metering laws are also contributing to increased adoption of solar systems in urban areas, residential complexes, and industries.

Inverter Type Insights:

- Central Inverter

- String Inverter

- Others

Central inverters are still preferred for large-scale utility and solar park developments in India due to their high power handling capability, lower cost per kilowatt of power, and efficient performance in megawatt-scale systems.

String inverters are also witnessing high adoption in rooftop and commercial solar systems in India due to their flexibility, ease of installation, and suitability for distributed solar systems in residential and commercial applications.

Other inverter technologies, such as microinverters and power optimizers, are also coming up in India, particularly for panel-level monitoring and optimization in residential rooftop solar systems with issues of shading or orientation of solar panels.

Regional Insights:

- Telangana

- Rajasthan

- Andhra Pradesh

- Tamil Nadu

- Karnataka

- Gujarat

- Others

Telangana is advancing its solar deployment through favorable state-level policies, expanding utility-scale solar parks, and growing rooftop adoption across urban and semi-urban areas to support clean energy goals.

Rajasthan leads in utility-scale solar capacity with approximately 26.9 GW installed by March 2025, benefiting from abundant solar irradiance, extensive desert land availability, and well-developed solar park infrastructure.

Andhra Pradesh is expanding its solar footprint through large-scale ground-mounted projects, favorable land policies, and growing investments in renewable energy infrastructure to meet rising power demand.

Tamil Nadu is strengthening its solar ecosystem with expanding manufacturing capabilities, growing rooftop adoption in commercial and industrial segments, and strong policy support for renewable energy integration.

Karnataka is leveraging its favorable solar resource base and progressive renewable energy policies to expand both utility-scale and distributed solar installations across the state’s growing industrial corridors.

Gujarat is a leading state for solar deployment, with approximately 12.8 GW of utility-scale capacity and the largest share of cumulative rooftop installations, supported by proactive state policies and industrial demand.

Market Dynamics:

Growth Drivers:

Why is the Indian Solar Electric System and Inverter Market Growing?

Comprehensive Government Policy Support and National Renewable Energy Targets

The Indian government has established an ambitious renewable energy roadmap that provides long-term visibility and investment confidence for the solar sector. National-level missions and state-level programs are creating a multi-layered policy ecosystem that supports solar deployment across utility-scale, commercial, industrial, and residential segments. Fiscal incentives, production-linked subsidies, and streamlined regulatory approvals are lowering barriers to entry and encouraging broad participation from domestic and international investors. Dedicated programs targeting rooftop solar adoption among households and agricultural solar pump deployment are expanding the addressable market beyond traditional utility-scale projects. These coordinated policy efforts are establishing India as a globally significant solar deployment destination, reinforcing investor confidence and accelerating the pace of capacity additions across the value chain. India Records 44.5 GW Renewable Energy Capacity Addition in 2025 (up to November 2025), Almost Doubling Yearly Installations. Solar Installed Capacity Reaches 132.85 GW as India Adds Around 35 GW, Wind Hits 54 GW Following 5.82 GW Rise.

Declining Technology Costs and Improving Solar System Economics

The sustained reduction in solar module, cell, and inverter costs is making solar energy increasingly competitive with conventional power sources across India. Advances in manufacturing processes, economies of scale from expanding production capacities, and technology improvements in photovoltaic cell architectures are driving down the levelized cost of solar energy. Lower system costs are making rooftop solar economically viable for a broader range of residential and commercial consumers, while utility-scale project developers benefit from more competitive tariff structures. The improving cost dynamics are also attracting new consumer segments, including small and medium enterprises, agricultural operations, and institutional facilities, thereby broadening the market’s growth base and strengthening the overall demand trajectory for solar electric systems and inverters. In 2025, SolarYaan has launched a new line of three-phase hybrid inverters (5–125 kW) paired with modular storage batteries (6–16 kWh), at the Renewable Energy India (REI) Expo 2025, being held at Greater Noida.

Strengthening Domestic Manufacturing Ecosystem and Supply Chain Localization

India’s expanding domestic solar manufacturing capacity is playing a critical role in strengthening supply chain resilience, reducing import dependency, and lowering project costs. The government’s push for backward integration across the solar value chain, from polysilicon and wafers to cells, modules, and inverters, is fostering a self-reliant manufacturing ecosystem. Quality control frameworks, standardized certification requirements, and mandates for domestically produced components are improving product reliability and consumer confidence. The localization of solar manufacturing is also generating employment opportunities, supporting ancillary industries, and contributing to broader industrial development objectives. As manufacturers continue to scale production and adopt advanced technologies, the domestic ecosystem is becoming increasingly competitive, supporting higher deployment volumes and reinforcing the long-term growth of the solar market.

Market Restraints:

What Challenges the Indian Solar Electric System and Inverter Market is Facing?

Upstream Supply Chain Dependency and Raw Material Constraints

India’s solar manufacturing sector remains significantly dependent on imported polysilicon, wafers, and critical raw materials, creating supply chain vulnerabilities and exposure to global price fluctuations. Limited domestic production capacity for upstream components increases cost uncertainty and can lead to project delays. This dependency on external supply sources undermines the objective of achieving full value chain self-sufficiency and exposes manufacturers and developers to geopolitical and trade-related risks that can impact project timelines and profitability.

Grid Integration and Transmission Infrastructure Limitations

Inadequate transmission infrastructure and grid integration challenges continue to constrain the efficient evacuation of solar power from generation sites to demand centers. Many solar-rich states face congestion on existing transmission lines, leading to curtailment of generated power. The intermittent nature of solar energy also requires investments in energy storage and grid management systems to ensure reliable power supply, adding complexity and cost to the overall solar deployment framework.

High Initial Investment and Financing Challenges

The upfront capital expenditure for solar installations, including modules, inverters, mounting structures, and balance-of-system components, remains a significant barrier for many potential adopters, particularly small-scale residential and agricultural consumers. While long-term operational savings are substantial, access to affordable financing, especially in rural and semi-urban areas, remains limited. High interest rates on project loans and complex subsidy disbursement processes can further discourage adoption among price-sensitive customer segments.

Competitive Landscape:

The Indian solar electric system and inverter market features a dynamic and increasingly competitive landscape, with participants spanning the entire value chain from upstream manufacturing to downstream project development and installation. The market is characterized by a mix of established domestic manufacturers and international technology providers competing across module production, inverter supply, and engineering-procurement-construction services. Competition is intensifying as participants expand production capacities, adopt advanced cell technologies, and invest in backward integration to achieve cost leadership and quality differentiation. Strategic partnerships, technology licensing agreements, and geographic expansion within the country are reshaping competitive dynamics. The growing rooftop solar segment is attracting new entrants and fostering innovation in distributed energy solutions, smart inverter technologies, and digital energy management platforms. This competitive environment is driving efficiency improvements, product diversification, and pricing optimization across the market.

Some of the key market players include:

- Solar Panel

- Vikram Solar Pvt Ltd

- Waree Solar Energy Pvt Ltd

- Adani Enterprises Ltd

- Goldi Green Technologies Pvt Ltd

- Tata Power Solar Systems Ltd

- Moser Baer Solar Ltd

- XL Energy Ltd

- Solar Semiconductor Pvt Ltd

- Emmvee Photovoltaics Pvt Ltd

- Navitas Green Solutions Pvt Ltd

- Solar Inverter

- ABB

- TMEIC

- SMA

- Hitachi

- Sungrow Power Supply Co., LTD.

- Huawei

- Schneider Electric

Recent Developments:

- In November 2025, Tata Power announced plans to set up a 10 GW wafer and ingot manufacturing facility to strengthen its position across the solar component value chain. The company currently has an integrated solar module and cell manufacturing capacity of 4.9 GW and is finalizing the location and technology for the new plant.

- In August 2025, Eastman Auto & Power Limited (EAPL), a prominent player in innovative and sustainable energy solutions, has today unveiled its SolarLink Grid-Tie Inverter Series, representing a major advancement in the company's goal to provide high-performance, future-oriented solar solutions. The SolarLink series is intended for residential and commercial use, featuring capacities from 3 kW to 110 kW. SolarLink provides smart energy conversion for both small homes and large commercial locations, supported by Eastman's reputation for reliability, longevity, and technical expertise.

Frequently Asked Questions About the India Solar Electric System and Inverter Market Research Report and Industry Forecast Report

The Indian solar electric system and inverter market size reached 128.14 GigaWatt in 2025.

The Indian solar electric system and inverter market is expected to grow at a compound annual growth rate of 21.73% from 2026-2034 to reach 752.34 GigaWatt by 2034.

Crystalline silicon, holding the largest share of 87% in 2025, remains the dominant technology in India’s solar electric system market, driven by its proven efficiency, mature manufacturing infrastructure, and compatibility with advanced cell technologies including TOPCon and bifacial configurations.

Key factors driving the Indian solar electric system and inverter market include supportive government policies, expanding rooftop solar adoption, declining technology costs, growing domestic manufacturing capacity, rising energy demand, and increasing investments in renewable energy infrastructure.

Major challenges include upstream supply chain dependency on imported raw materials, grid integration and transmission infrastructure limitations, high initial investment costs, complex subsidy disbursement processes, and workforce skill shortages in installation and maintenance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)