Indian Textile and Apparel Market Size, Share, Trends and Forecast by Raw Material, Application, Product Type, and State, 2026-2034

Indian Textile and Apparel Market Size, Share, Trends & Forecast (2026-2034)

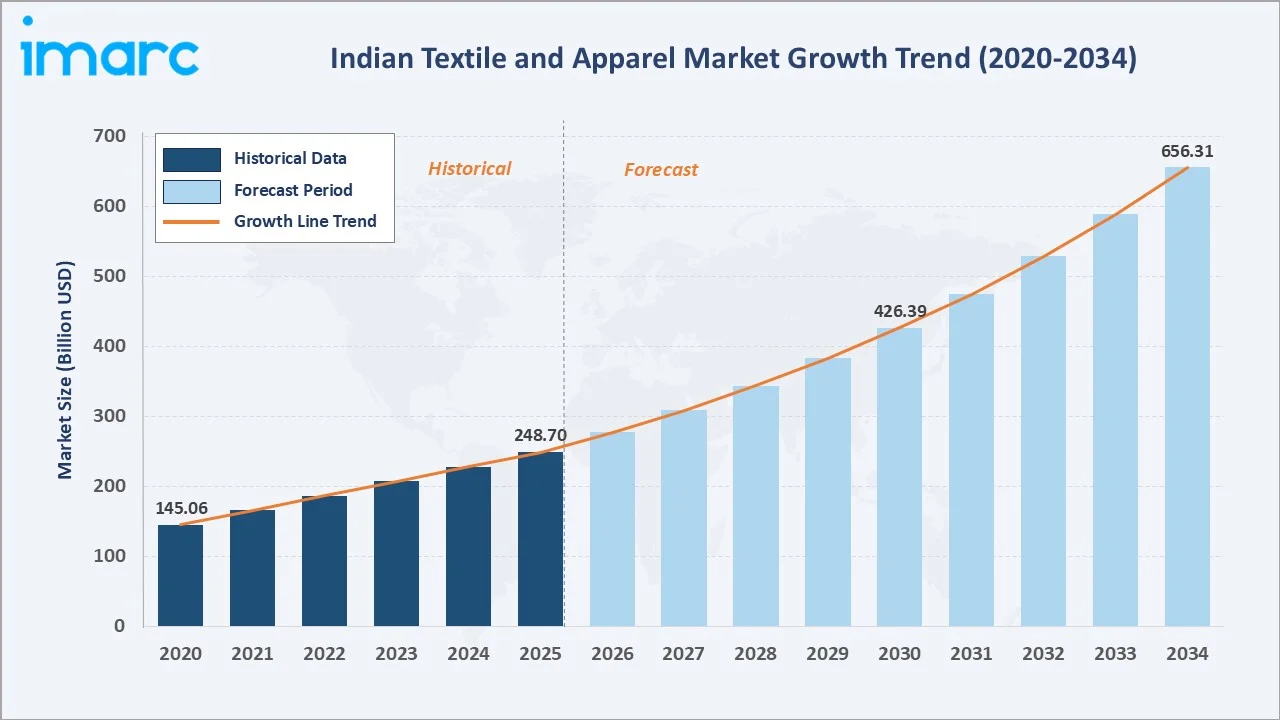

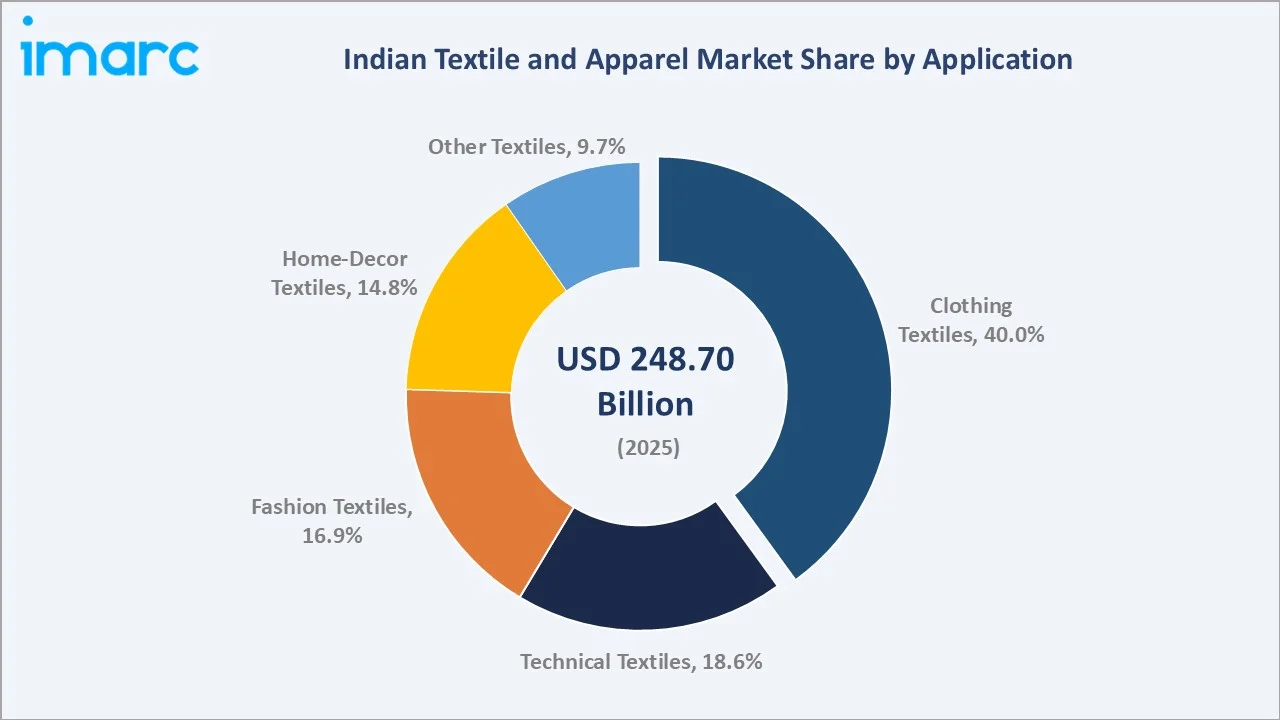

The Indian textile and apparel market reached USD 248.70 Billion in 2025 and is projected to reach USD 656.31 Billion by 2034, growing at a CAGR of 11.38% during 2026-2034. The market is driven by rising domestic consumption, growing fashion and e-commerce penetration, and strong export demand. Government support through PLI schemes, textile parks, and Make in India initiatives is further strengthening manufacturing capacity and industry growth. In 2024-25, India’s textile and apparel exports reached around US$ 37.0 billion, recording nearly 6% growth compared to 2023-24. This improving demand for Indian textile products is strengthening export revenues, production activity, and capacity utilization across spinning, weaving, garmenting, and apparel manufacturing segments. Natural fibres dominate at 56.0%. Clothing textiles lead the application at 40.0%. Maharashtra commands 20.0% of the national market share.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 248.70 Billion |

| Forecast Market Size (2034) | USD 656.31 Billion |

| CAGR (2026-2034) | 11.38% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Leading Raw Material | Natural Fibres (56.0% share, 2025) |

| Leading Application | Clothing Textiles (40.0% share, 2025) |

| Leading Region | Maharashtra (20.0% share, 2025) |

Indian textile and apparel market expanded from USD 145.06 Billion in 2020 to USD 248.70 Billion in 2025, anchored at USD 426.39 Billion in 2030, and forecast to reach USD 656.31 Billion by 2034. COVID-19's 2020 disruption was followed by the most significant policy stimulus in India's post-liberalization textile history.

To get more information on this market, Request Sample

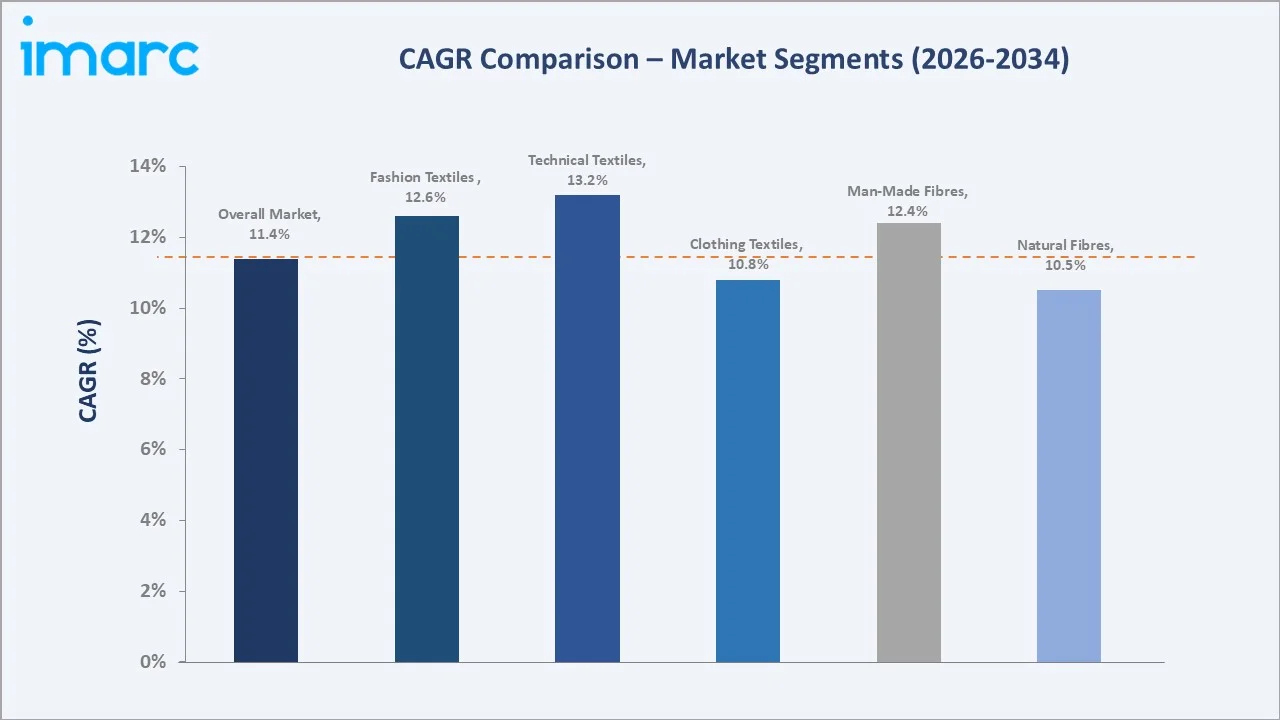

Technical textiles grow fastest at ~13.2% CAGR through the National Technical Textiles Mission (NTTM) mandating technical textile procurement in government infrastructure projects, defence procurement, and healthcare procurement. Man-made fibres grow at ~12.4% CAGR through Surat's expanding synthetic processing capacity and India's shift toward performance apparel and athleisure-driven fabric demand.

Executive Summary

Indian textile and apparel market reached USD 248.70 Billion in 2025, representing one of the world's largest textile economies. Indian textile sector provides direct employment to many Indian people and indirect employment across farming, trading, and support industries, making the textile sector's 11.38% growth trajectory among the most economically consequential market expansions in India's developing economy. The market is projected to reach USD 656.31 Billion by 2034.

Natural fibres at 56.0% dominate through India's status as one of the largest cotton producers, the silk producer, and the jute producer, creating the most commercially diverse natural fibre production base of any national textile market. Clothing textiles at 40.0% leads application through India's consumer mass market and export garment manufacturing. Maharashtra leads regionally at 20.0% through Mumbai's commercial dominance and Bhiwandi's distribution primacy.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Raw Material | Natural Fibres – 56.0% share (2025) |

| Leading Application | Clothing Textiles – 40.0% share (2025) |

| Leading Region | Maharashtra – 20.0% share (2025) |

| Market Opportunity | PLI scheme; mega textile parks; technical textile target; sustainability and circularity premium segment growth; D2C fashion brand ecosystem |

Key Analytical Observations Supporting The Above Data:

- Natural Fibres at 56.0%: The natural fibres dominate due to the country's large production of cotton, jute, silk, and wool, supported by a strong agricultural base and established textile manufacturing ecosystem. Growing consumer preference for breathable, sustainable, and biodegradable fabrics further strengthens demand for natural fibre-based products.

- Clothing Textiles at 40.0%: The clothing textiles dominate due to strong domestic demand for ethnic wear, casual wear, formal wear, innerwear, and fashion apparel. Rising disposable incomes, urbanization, e-commerce growth, and export demand further support large-scale clothing textile consumption.

- Maharashtra at 20.0%: Maharashtra dominates regionally due to its strong cotton textile base, large garment manufacturing clusters, and established textile hubs such as Mumbai, Solapur, and Bhiwandi. Strong port connectivity, skilled labor availability, and export-oriented production further support its leading position.

Indian Textile and Apparel Market Overview

Indian textile and apparel market is the most commercially complex national textile economy, combining the largest cotton and jute producing agriculture sector, polyester and viscose synthetic fibre manufacturing, one of the largest garment export industries, India's most diverse handloom and craft textile heritage, and India's fastest-growing fashion e-commerce market. The market's commercial architecture spans micro, small, and medium enterprises in weaving, processing, and garment making in a commercial sector where both handloom artisans coexist within the same national market definition.

The textile and apparel ecosystem integrates raw material producers, yarn manufacturers, fabric producers, garment manufacturers, branded apparel companies, retail channels, and export facilitation. Macroeconomic factors include rising disposable incomes, rapid urbanization, population growth, and increasing consumer spending on fashion and lifestyle products.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

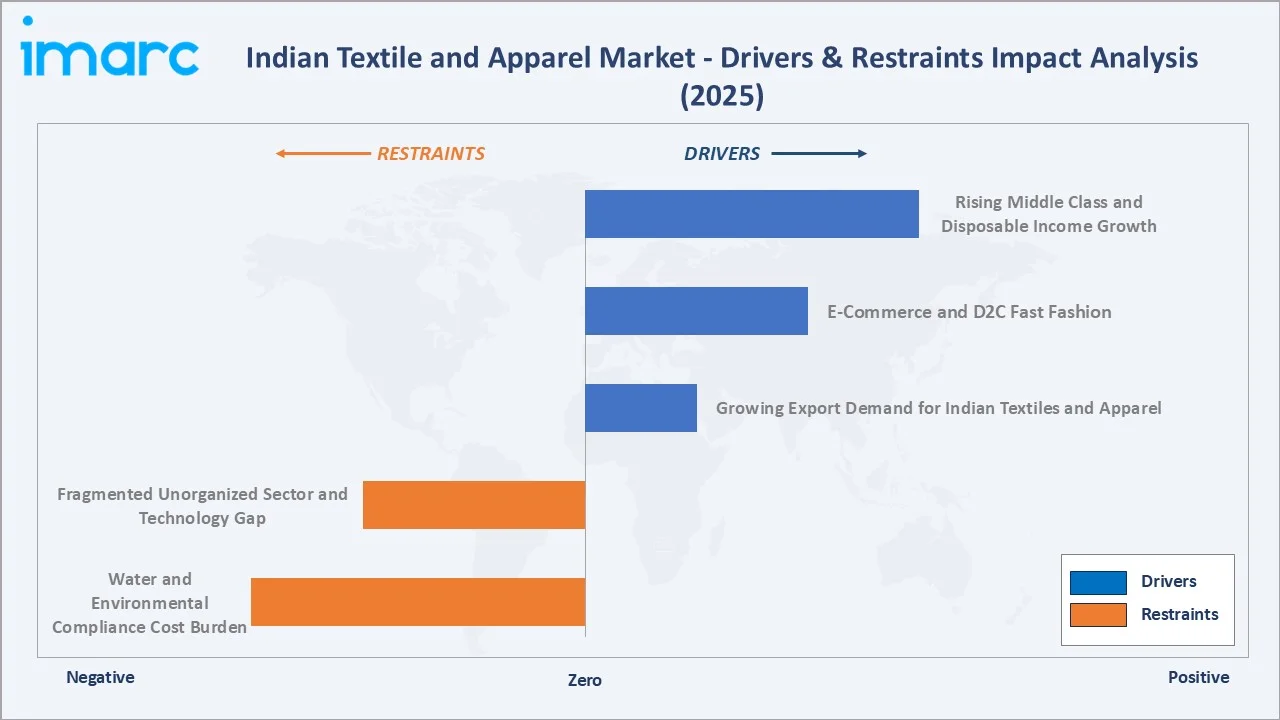

- Rising Middle Class and Disposable Income Growth: India’s middle class is projected to be the fastest-growing major population segment, reaching 38% by 2031 and 60% by 2047. By 2030, India is expected to add around 75 million middle-class households and 25 million affluent households, together accounting for 56% of total households. This rising middle class and disposable income growth are increasing consumer spending on clothing, fashion, and lifestyle products. Higher household incomes are encouraging demand for premium apparel, branded garments, ethnic wear, and fast-fashion products. Urban consumers are also purchasing apparel more frequently through organized retail and e-commerce channels. This expanding purchasing power is supporting growth across both mass-market and premium textile segments.

- E-Commerce and D2C Fast Fashion: E-commerce and D2C fast fashion are expanding consumer access to a wide variety of clothing, brands, and fashion trends across urban and rural areas. Direct-to-consumer (D2C) brands leverage digital platforms to launch new collections quickly and respond to changing fashion preferences. Online shopping, attractive discounts, and faster delivery services are encouraging more frequent apparel purchases. This has increased demand for textile production, garment manufacturing, and supply chain agility across the industry.

- Growing Export Demand for Indian Textiles and Apparel: Growing export demand for Indian textiles and apparel is increasing production volumes, capacity utilization, and investment across spinning, weaving, processing, and garment manufacturing segments. Strong demand from major markets is boosting export revenues and encouraging manufacturers to expand operations. In 2024-25, India’s textile and apparel exports reached around US$ 37.0 billion, recording nearly 6% growth compared to 2023-24. This is creating employment opportunities and supporting the modernization of textile production facilities.

Market Restraints

- Fragmented Unorganized Sector and Technology Gap: Many small and unorganized manufacturers operate with limited access to modern machinery, automation, and digital technologies. This often results in lower productivity, inconsistent product quality, and higher production costs. Limited investment capacity can also slow the adoption of advanced textile processing and sustainable manufacturing practices. As global competition intensifies, these challenges may affect the industry's ability to scale efficiently and meet international quality standards.

- Water and Environmental Compliance Cost Burden: Textile dyeing, bleaching, and processing operations consume significant amounts of water and generate wastewater that must be treated before discharge. Compliance with pollution control norms, effluent treatment requirements, and sustainability standards increases operational and capital expenditure for manufacturers. Smaller textile units often face challenges in meeting these requirements due to limited financial resources. These costs can reduce profitability and affect the competitiveness of Indian textile producers in global markets.

Market Opportunities

- Technical Textiles and Smart Fabrics Development: Technical textiles and smart fabrics development are expanding textile applications beyond traditional clothing into healthcare, defense, automotive, construction, agriculture, and industrial sectors. Growing demand for functional textiles with features such as durability, antimicrobial properties, temperature regulation, and sensor integration is encouraging innovation. Government initiatives, including the National Technical Textiles Mission, are supporting R&D and domestic manufacturing. This shift toward high-value, technology-driven textiles can enhance profitability and strengthen India’s global competitiveness.

- Digital Textile Printing and Advanced Manufacturing Technologies: Digital textile printing and advanced manufacturing technologies enable faster design changes, lower fabric wastage, and cost-efficient small-batch production. Automation, AI-based design tools, and digital printing help manufacturers respond quickly to fashion trends and customized apparel demand. These technologies also improve quality consistency, reduce lead times, and support sustainable production practices.

Market Challenges

- Volatility in Cotton and Raw Material Prices: Fluctuations in cotton, yarn, dyes, chemicals, and synthetic fiber prices can significantly impact production costs. Unpredictable raw material expenses make pricing and inventory planning difficult for manufacturers. This can compress profit margins, particularly for small and medium-sized textile producers. Frequent price swings may also reduce export competitiveness and affect long-term supply chain stability.

- Rising Labor and Compliance Costs: Increasing production expenses across spinning, weaving, processing, and garment manufacturing units. Higher wages, worker welfare requirements, safety norms, and social compliance standards add to operating costs. Export-oriented manufacturers also need to meet global labor and ethical sourcing requirements. These costs can reduce margins and weaken competitiveness against lower-cost textile-producing countries.

Emerging Market Trends

1. PM MITRA Textile Parks Creating India's First Integrated Cluster Infrastructure

The government of India approved the establishment of PM Mega Integrated Textile Region and Apparel (PM MITRA) Parks at seven locations: Virudhnagar in Tamil Nadu, Warangal in Telangana, Navsari in Gujarat, Kalaburagi in Karnataka, Dhar in Madhya Pradesh, Lucknow in Uttar Pradesh, and Amravati in Maharashtra. The initiative has an outlay of Rs. 4,445 crore for seven years up to 2027-28. These PM MITRA textile parks are creating integrated textile clusters with spinning, weaving, processing, dyeing, garmenting, logistics, and common infrastructure at one location. This reduces production delays, lowers logistics costs, and improves supply chain efficiency. The parks also support large-scale investment, modern technology adoption, and export-oriented manufacturing. As a result, Indian textile industry is moving toward more organized, competitive, and globally integrated production hubs.

2. Athleisure and Performance Fabric Revolution Transforming Indian Fashion Apparel

Athleisure and performance fabrics are emerging as consumers increasingly prefer comfortable, stretchable, breathable, and multifunctional clothing. Rising fitness awareness, hybrid work lifestyles, and demand for casual fashion are boosting sportswear-inspired apparel. This is encouraging manufacturers to develop moisture-wicking, quick-dry, antimicrobial, and lightweight fabrics. As a result, Indian fashion apparel is shifting toward functional, everyday performance wear.

3. Sustainability and Circular Economy Reshaping Premium Textile Export

Sustainability and the circular economy are reshaping premium textile exports in India as global brands increasingly demand eco-friendly, traceable, and ethically produced textiles. Manufacturers are adopting recycled fibers, organic cotton, water-efficient processing, and textile waste recycling to meet international sustainability standards. Growing emphasis on regulatory compliance and circular production models is helping Indian exporters access premium markets and strengthen their competitiveness in Europe, North America, and other environmentally conscious regions.

4. Digital Fashion and AI-Driven Design Transforming Indian Apparel Innovation

Digital fashion and AI-driven design are helping brands create faster designs, predict fashion trends, and personalize collections for consumers. AI tools support demand forecasting, virtual sampling, size optimization, and reduced product development time. This improves speed-to-market, lowers design waste, and supports more responsive apparel production.

Industry Value Chain Analysis

Indian textile and apparel value chain is the most geographically distributed national textile production system. The value chain's commercial efficiency improves with each stage of vertical integration, the cotton-to-denim-to-brand model capturing value at each stage versus commodity yarn producers capturing only spinning margin above cotton farming margin.

| Stage | Key Participants |

|---|---|

| Raw Material Fibre & Yarn Production | Cotton, man-made fibre, wool, silk, jute production, and yarn manufacturing |

| Fabric Weaving, Knitting & Production | Fabric manufacturing through weaving, knitting, nonwoven processing, and specialty textile production |

| Processing, Dyeing & Finishing | Textile wet processing, dyeing, printing, finishing, coating, and value-addition activities |

| Garment Cutting, Sewing & Manufacturing | Apparel design, cutting, stitching, garment manufacturing, and product assembly |

| Branding, Packaging & Quality Control | Brand development, product packaging, testing, certification, quality assurance, and compliance management |

| Retail & Export Distribution | Domestic retailing, e-commerce sales, wholesale distribution, export marketing, and international trade operations |

The processing (dyeing, printing, finishing) stage is the value chain's most commercially contested and environmentally challenged phase. The export distribution stage's commercial evolution is creating India's first DTC international fashion brand exports.

Technology Landscape in the Indian Textile and Apparel Industry

Spinning and Weaving Technology

The adoption of automated spinning machines, air-jet looms, rapier looms, and digital monitoring systems improves production speed, fabric quality, and operational efficiency while reducing material wastage and labor dependency. Modern spinning and weaving solutions also support the manufacture of high-value fabrics for apparel, technical textiles, and export markets. As textile manufacturers upgrade facilities, technology-driven production is becoming a key factor in enhancing global competitiveness.

Sustainable Processing Technology

Sustainable processing technology supported by the adoption of water-efficient dyeing, low-impact chemicals, digital printing, and energy-efficient processing systems. Manufacturers are increasingly investing in zero-liquid-discharge (ZLD) facilities, wastewater recycling, and renewable energy integration to meet environmental regulations and sustainability goals. In September 2025, Arvind Limited advanced sustainable textile manufacturing by installing India’s first supercritical CO₂ dyeing machine at its Ahmedabad facility. Developed in collaboration with H&M Group and Deven Supercriticals, the initiative introduced an eco-friendly fabric dyeing technology that reduces reliance on conventional water-intensive dyeing processes. These technologies help reduce water consumption, chemical usage, and carbon emissions while improving resource efficiency. As global brands prioritize sustainable sourcing, eco-friendly textile processing is becoming a key competitive differentiator for Indian manufacturers.

Fashion Technology and E-Commerce Innovation

Fashion technology and e-commerce innovation enable AI-driven trend forecasting, virtual try-ons, personalized recommendations, and digital product design. E-commerce platforms provide brands with real-time consumer insights, helping them respond quickly to changing fashion preferences. Technologies such as 3D design, virtual sampling, and automated inventory management reduce development time and improve supply chain efficiency. As online fashion retail expands, digital innovation is transforming how apparel is designed, marketed, and sold in India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Raw Material |

Natural Fibres |

56.0% |

2025 |

|

Application |

Clothing Textiles |

40.0% |

2025 |

|

Product Type |

Fabric |

38.0% |

2025 |

|

State |

Maharashtra |

20.0% |

2025 |

By Raw Material

Natural fibres lead at 56.0% (2025). India's natural fibre textile market encompasses the most diverse crop-to-craft natural fibre chain, with cotton, silk, jute, wool, and specialty fibres. Natural fibres' ~10.5% CAGR reflects organic cotton premium adoption, handloom luxury positioning, and government protection, creating defensible premium segments.

To access detailed market analysis, Request Sample

Man-made fibres at 44.0% grow fastest at ~12.4% CAGR through world-scale polyester, viscose leadership, and technical textile demand for synthetic geotextiles, agrotextiles, and medical nonwovens.

By Application

Clothing textiles lead at 40.0% (2025). India's mass domestic clothing market and garment export collectively create the largest single application segment. Fashion textiles at 16.9% grow at ~12.6% CAGR through the D2C fast fashion revolution and the growing luxury ethnic wear market. Technical textiles at 18.6% grow fastest at ~13.2% CAGR through healthcare nonwoven demand.

Home-decor textiles at 14.8% encompass the Welspun home textile export segment plus India's rapidly growing domestic premium home textile market, driven by growing middle-class homeownership and interior decor consciousness. Other textiles at 9.7% include industrial fabrics, packaging textiles, and specialty segments growing at a 10-11% CAGR through technical and industrial application expansion.

Regional Market Insights

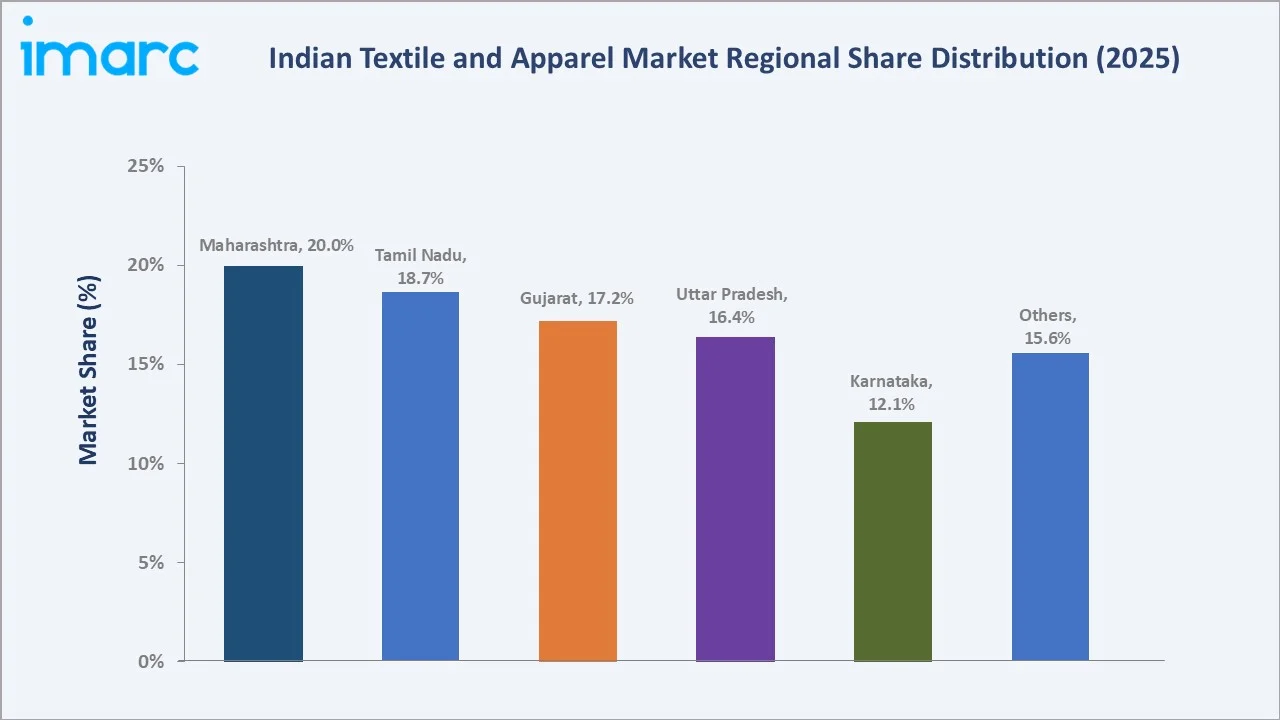

| State | Share | Key Indian Textile and Apparel Market Drivers & Characteristics |

|---|---|---|

| Maharashtra | 20.0% | Driven by a strong cotton textile base, large garment manufacturing clusters, export-oriented production facilities, and a well-developed logistics infrastructure. |

| Tamil Nadu | 18.7% | Supported by a highly integrated textile value chain spanning spinning, knitting, processing, and apparel manufacturing, along with a strong export presence. |

| Gujarat | 17.2% | Benefits from extensive cotton cultivation, large-scale textile processing capacity, synthetic textile production, and a strong industrial ecosystem supporting textile manufacturing. |

| Uttar Pradesh | 16.4% | Driven by its diverse textile traditions, growing apparel manufacturing sector, handloom industry, and increasing investments in textile infrastructure. |

| Karnataka | 12.1% | Supported by garment exports, silk production, technical textile development, and a growing organized apparel manufacturing base. |

| Others | 15.6% | The other category includes textile-producing states benefiting from cotton cultivation, handloom activities, garment manufacturing, technical textiles, and expanding domestic and export demand. |

Maharashtra's 20.0% market leadership is reinforced by Bhiwandi being one of India's textile distribution capitals. Tamil Nadu's 18.7% reflects knitwear export, making it one of the largest single-city knitwear export hubs by volume. Gujarat's 17.2% reflects Surat's status as one of the largest synthetic fabric manufacturing centers.

Uttar Pradesh's 16.4% reflects the state's combination of India's richest craft textile traditions with the fastest-growing apparel export cluster and the largest rural textile consumption market. The others 15.6%, encompassing all remaining states, is growing at above-national CAGR through Rajasthan's craft export growth, West Bengal's jute technical textile expansion, and Telangana-Andhra's combined silk and technical textile development through the newly created PM MITRA park investment.

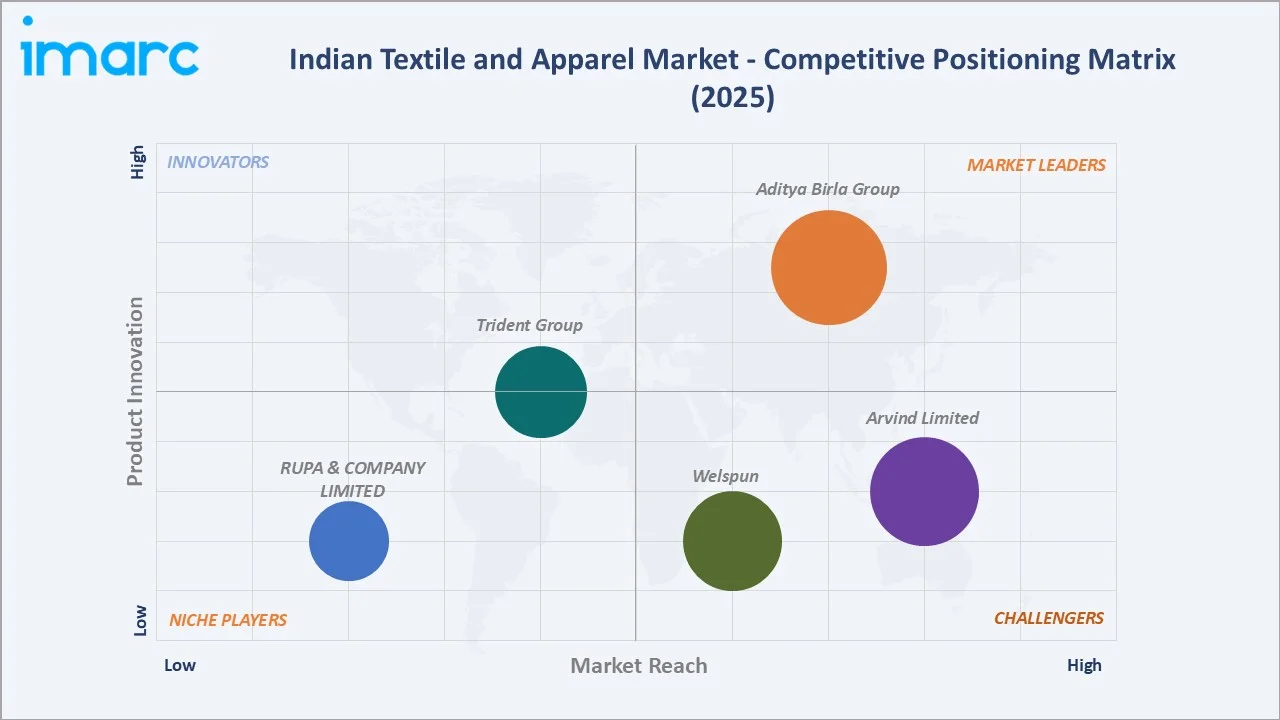

Competitive Landscape

Indian textile and apparel market's competitive landscape is the most commercially stratified. The organized sector accounts for approximately 35-40% of Indian textile market by value, with the unorganized sector accounting for 60-65% by value, a commercial structure fundamentally different from China's predominantly organized textile sector and creating India's unique challenge of simultaneously developing organized sector scale and protecting unorganized sector livelihoods.

| Company Name | Key Brands | Market Position | Core Strength |

|---|---|---|---|

| Aditya Birla Group | Linen Club, Liva, Raysil | Market Leader | Vertically integrated textile and apparel operations spanning fiber production, fabric manufacturing, and branded fashion retail. |

| Arvind Limited | Flying Machine, Arrow, US Polo, Calvin Klein, Tommy Hilfiger | Strong Challenger | Leadership in denim and woven textiles with extensive vertically integrated manufacturing capabilities. |

| Welspun | Christy, Spaces, Welspun, Martha Stewart, Welhome | Strong Challenger | Focus on home textiles including towels, bed linen, rugs, and global export-oriented manufacturing. |

| Trident Group | myTrident, Everyday Home, Everyday Oasis | Established Player | Large-scale home textile manufacturing with strong presence in bed linens, towels, and integrated production facilities. |

| RUPA & COMPANY LIMITED | FRONTLINE, EURO, Bumchums, Softline, Jon, COLORS, THERMOCOT, Peek-a-boo, TORRIDO | Niche Player | Leading knitwear, hosiery, innerwear, and casual wear manufacturer with extensive pan-India distribution. |

The competitive landscape is being reshaped by three forces: D2C brand proliferation, private label retail expansion, and the new entrant premium.

Key Company Profiles

Aditya Birla Group

Aditya Birla Group is one of India's largest textile and apparel conglomerates, operating across the value chain through businesses in specialty fibers, yarns, fabrics, apparel, fashion retail, and branded clothing.

- Key Brands: Linen Club, Liva, Raysil.

- Recent Developments: In September 2025, Aditya Birla Fashion and Retail Ltd. launched the OWND!, a bold new fashion brand designed for India's Gen Z and youthful, trend-conscious consumers.

- Strategic Focus: Expanding sustainable and specialty fiber production, strengthening its branded fashion portfolio, and enhancing value-added textile manufacturing.

Arvind Limited

Arvind Limited is one of India’s leading integrated textile and apparel companies with operations spanning cotton shirting, denim, knit fabrics, woven fabrics, garments, advanced materials, and textile engineering. Arvind has a strong presence across the textile value chain, from fabric manufacturing to garment production and retail.

- Key Brands: Flying Machine, Arrow, US Polo, Calvin Klein, Tommy Hilfiger.

- Recent Developments: In June 2025, Fashion for Good and Arvind Limited launched Future Forward Factories India, an initiative aimed at creating a practical blueprint for sustainable textile manufacturing and building a demonstration facility to apply these innovations. The project targets a 93% reduction in greenhouse gas emissions compared to conventional manufacturing and focuses on making Tier 2 factories more environmentally responsible and economically viable.

- Strategic Focus: Advancing sustainable textile manufacturing, expanding value-added and technical textiles, and strengthening its position in premium fabrics and apparel.

Market Concentration Analysis

Indian textile and apparel market concentration is the most unusual among major manufacturing sectors, extremely high in specific sub-segments, alongside extreme fragmentation in others. The organized branded apparel market is moderately concentrated. Technical textiles are the most concentrated sub-segment for premium products. E-commerce is progressively increasing concentration at the fashion distribution level with Myntra, Ajio, Amazon, and Meesho collectively controlling 60%+ of India's online fashion GMV, creating a platform duopoly-oligopoly in the fastest-growing fashion distribution channel that threatens mid-size brand companies' direct consumer access. The platform concentration creates commercial dependency where brands' online visibility is controlled by Myntra or Ajio's algorithm above the brand's own marketing investment.

Investment & Growth Opportunities

Highest Growth Segments

Technical textiles (~13.2% CAGR), fashion textiles D2C (~12.6% CAGR), man-made fibres (~12.4% CAGR), athleisure and performance fabric (~18-20% CAGR through India's fitness culture revolution), premium ethnic wear (~15% CAGR through organized luxury ethnic retail development), and sustainable and organic textile (~25% CAGR from small base through export market sustainability compliance) represent India's highest-growth textile investment vectors through 2034.

Emerging Investment Opportunities

PM MITRA textile parks represent the most commercially certain textile investment opportunity in India's 2026-2034 period, 7 designated parks, creating plug-and-play manufacturing infrastructure for fibre-to-fashion integration. Early PM MITRA tenant companies receive first-mover infrastructure advantage and the most commercially significant benefit: colocation with other value chain players, creating cluster agglomeration economics that reduce inter-cluster logistics cost for fully integrated PM MITRA park manufacturing.

Investment Themes

- Premium ethnic wear organized retail creating India's first national ethnic fashion brand above regional boutique: India's ethnic wear market is currently served predominantly by unorganized regional boutiques and local designers without a national brand above the luxury tier, creating a commercial opportunity for an organized premium ethnic wear retail brand that can capture 5-10% of the fragmented premium ethnic market.

- Sustainable textile certification investment for premium export market access: GOTS (Global Organic Textile Standard) certification for organic cotton textiles, Better Cotton Initiative (BCI) membership for standard cotton with environmental improvement, and chemical management certification for synthetic textile processing collectively create a sustainability certification premium above conventional equivalent textile pricing in EU, US, and Japanese premium retail markets.

Future Market Outlook (2026-2034)

Indian textile and apparel market is projected to grow from USD 248.70 Billion in 2025 to USD 656.31 Billion by 2034, delivering an 11.38% CAGR over the forecast period. The market's anchor value of USD 426.39 Billion in 2030 represents Indian textile industry at its most commercially transformative inflection. PM MITRA parks will have achieved commercial production with 7 parks operational and beginning cluster economics realization, India's technical textile sector growth, and India's total textile export growth, driving the market growth.

Three structural forces define Indian textile market growth through 2034 with exceptional confidence. India's demographic dividend creates mathematically certain textile market volume and value growth that no policy disruption can reverse, given the fundamental clothing consumption requirement driving demand. Government policy activation creates above-market investment pull that compounds commercial market growth. India's supply chain diversification opportunity creates structural export demand growth that is policy-mandated by brand companies' risk management above commercial sourcing optimization.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Chairman and Managing Directors; Chief Executive Officers; Export Directors; state textile policy officials; and retail and e-commerce specialists.

Secondary Research

Secondary research encompassed the Ministry of Textiles Annual Report 2024; cotton textile export statistics; Textiles Export Promotion Council export data; National Technical Textiles Mission progress report; PM MITRA scheme documentation and selected park status reports; and company annual reports. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a dual-track model: demand-side and supply-side. Export component modelled separately from domestic consumption using bilateral trade agreement market access impact assessment, and global textile import demand growth projections from UN Comtrade.

Indian Textile and Apparel Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Raw Materials Covered | Natural Fibres, Man-made Fibres |

| Applications Covered | Clothing Textiles, Technical Textiles, Fashion Textiles, Homer-Décor Textiles, Other Textiles |

| Product Types Covered | Yarn, Fabric, Fibre, Others |

| States Covered | Maharashtra, Uttar Pradesh, Tamil Nadu, Gujarat, Karnataka, Others |

| Companies Covered | Aditya Birla Group, Arvind Limited, Welspun, Trident Group, RUPA & COMPANY LIMITED, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indian Textiles and Apparel Market Report

Indian textile and apparel market reached USD 248.70 Billion in 2025. The market is driven by rising domestic consumption, growing middle-class income, urban fashion demand, and expanding e-commerce penetration. Strong export demand, PM MITRA textile parks, PLI support, and rising interest in technical and sustainable textiles are further strengthening market growth.

Indian textile and apparel market grows at 11.38% CAGR during 2026-2034, reaching USD 656.31 Billion by 2034, supported by rising domestic consumption, exports, e-commerce, and government-led textile infrastructure initiatives.

Natural fibres lead at 56.0% through India's world-leading cotton, silk, and jute production, creating the most commercially diverse natural fibre textile base globally.

Clothing textiles lead at 40.0% through India's domestic mass market and garment export, creating the dual-market commercial foundation unmatched by other application segments.

Maharashtra leads at 20.0% through Mumbai's headquarters concentration and Bhiwandi's position as Indian textile distribution center handling most of India's synthetic textile volume.

Leading companies include Aditya Birla Group, Arvind Limited, Welspun, Trident Group, and RUPA & COMPANY LIMITED, among others.

Three priority investment opportunities: PM MITRA Park tenant positioning for cluster economics advantage; premium ethnic wear organized retail creating India's first national brand; and technical textile manufacturing for government mandate procurement.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)