India Tomato Processing Market Size, Share, Trends and Forecast by Distribution Channel, End-Use, and Region, 2026-2034

India Tomato Processing Market Summary:

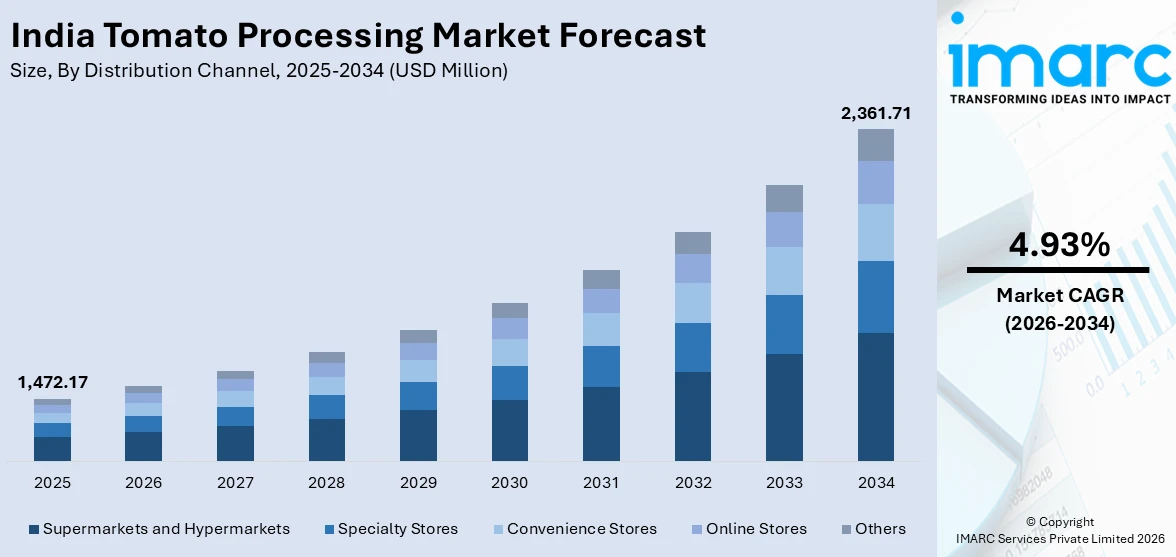

The India tomato processing market size was valued at USD 1,472.17 Million in 2025 and is projected to reach USD 2,361.71 Million by 2034, growing at a compound annual growth rate of 4.93% from 2026-2034.

The India tomato processing market is expanding steadily as urbanization, rising disposable incomes, and evolving dietary preferences drive increased consumption of processed tomato products. The growing penetration of quick-service restaurants, expanding modern retail formats, and escalating demand for convenience foods are reinforcing the shift toward packaged sauces, ketchups, pastes, and canned tomato products. Advanced processing technologies, innovative packaging solutions, and supportive government policies for agro-processing infrastructure are further strengthening the India tomato processing market share.

Key Takeaways and Insights:

- By Distribution Channel: Supermarkets and hypermarkets dominate the market with a share of 38.0% in 2025, driven by wide product assortments, bulk purchasing options, and organized retail expansion across urban and semi-urban regions.

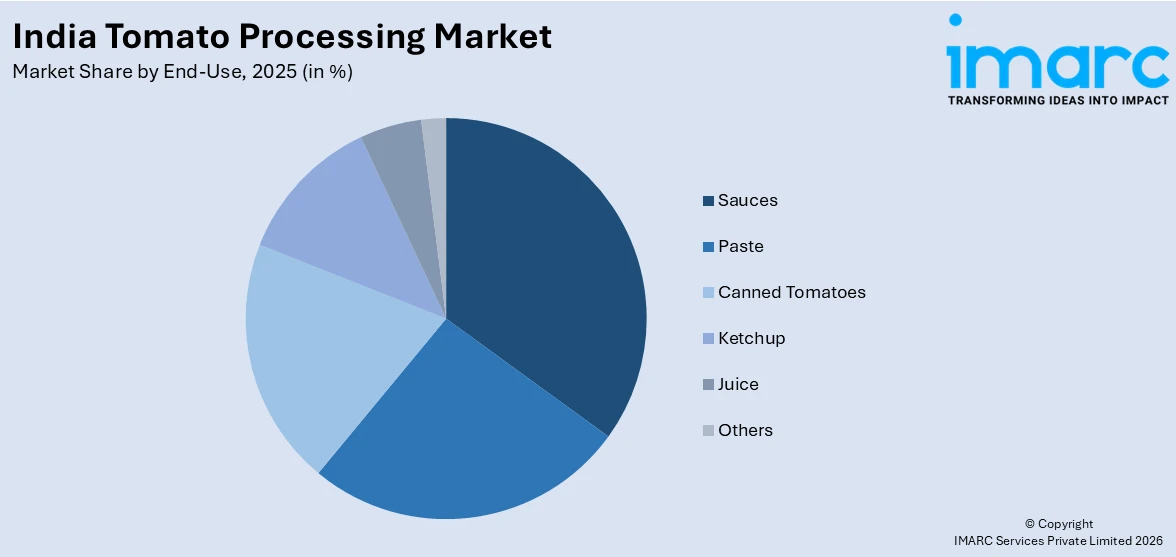

- By End-Use: Sauces lead the market with a share of 30.0% in 2025, owing to their widespread culinary application across Indian households and the rapidly growing foodservice sector.

- By Region: North India represents the largest segment with a market share of 32.0% in 2025, supported by high population density, strong organized retail presence, and well-established food processing infrastructure.

- Key Players: The India tomato processing market features a moderately competitive landscape with established multinational corporations and domestic manufacturers competing across product categories, distribution channels, and price segments to capture growing consumer demand for value-added tomato products.

To get more information on this market Request Sample

The India tomato processing market is being reshaped by converging forces of rapid urbanization, expanding food processing infrastructure, and shifting consumer preferences toward convenience-oriented food products. India, the world's second-largest tomato producer, processes only a fraction of its annual harvest, presenting significant untapped potential. The government's Pradhan Mantri Kisan SAMPADA Yojana (PMKSY), with a cumulative investment exceeding INR 21,917 crore across 1,185 operational projects as of 2025, is strengthening cold chain infrastructure and processing capacities nationwide. Meanwhile, the explosive growth of quick-commerce platforms, which collectively achieved approximately USD 6-7 billion in gross merchandise value in 2024, is creating new distribution pathways for processed tomato products, accelerating consumer access in metropolitan and tier-two cities alike. The rising investments in modern packaging technologies and value-added product development are further enhancing shelf life and product differentiation. Additionally, increasing collaboration between food processors and organized retail chains is expanding market penetration and reinforcing supply chain efficiency across regions.

India Tomato Processing Market Trends:

Rising Adoption of Health-Conscious and Clean-Label Tomato Products

Indian consumers are increasingly gravitating toward processed tomato products that emphasize natural ingredients, minimal preservatives, and organic sourcing. The demand for clean-label formulations in sauces, purees, and ketchups is accelerating as health awareness rises across urban demographics. For instance, in January 2025, CURRYiT, a New Delhi-based start-up, launched India's first preservative-free and chemical-free tomato puree, formulated with 99% fresh tomatoes, olive oil, and salt. This trend is catalyzing product innovation across the India tomato processing market growth, as manufacturers reformulate offerings to meet evolving consumer expectations for transparency and nutrition.

Expansion of Quick-Commerce and Digital Distribution Channels

The rapid proliferation of quick-commerce platforms in India is transforming the distribution landscape for processed tomato products. Ultra-fast delivery services operating through dense dark-store networks are enabling consumers to access sauces, ketchups, and tomato pastes within minutes. The India q-commerce market size reached USD 3.6 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 106.2 Billion by 2033, exhibiting a growth rate (CAGR) of 45.60% during 2025-2033. This digital retail expansion is significantly broadening the reach and accessibility of processed tomato products across metropolitan and emerging urban centers.

Government-Led Strengthening of Agro-Processing Infrastructure

Federal and state governments in India are intensifying investments in food processing and cold chain infrastructure, directly benefiting the tomato processing value chain. The Union Cabinet, in July 2025, approved an additional allocation of INR 1,920 crore to the PMKSY scheme, raising the total outlay to INR 6,520 crore for the 15th Finance Commission cycle. This enhanced funding supports the establishment of 50 multi-product food irradiation units. These infrastructure developments are reducing post-harvest losses, improving product quality, and expanding processing capacity across major tomato-growing states.

Market Outlook 2026-2034:

The India tomato processing market is poised for sustained expansion over the forecast period as rising urbanization, growing working-class populations, and expanding quick-service restaurant chains continue to fuel demand for processed tomato products. Increasing investments in cold chain logistics and processing technologies, coupled with supportive government schemes, are expected to strengthen production capacities and reduce post-harvest wastage across major tomato-growing regions. Furthermore, the introduction of innovative product formats and premium value-added offerings is likely to enhance consumer engagement and drive higher revenue realization across both retail and institutional channels. The market generated a revenue of USD 1,472.17 Million in 2025 and is projected to reach a revenue of USD 2,361.71 Million by 2034, growing at a compound annual growth rate of 4.93% from 2026-2034.

India Tomato Processing Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Distribution Channel |

Supermarkets and Hypermarkets |

38.0% |

|

End-Use |

Sauces |

30.0% |

|

Region |

North India |

32.0% |

Distribution Channel Insights:

- Supermarkets and Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Others

Supermarkets and hypermarkets dominate with a market share of 38.0% of the total India tomato processing market in 2025.

Supermarkets and hypermarkets serve as the primary distribution channel for processed tomato products in India, leveraging their expansive shelf space, organized product displays, and competitive pricing strategies to attract consumer footfall. These large-format retail outlets offer a comprehensive range of tomato-based products, from mass-market ketchups and sauces to premium organic purees, enabling consumers to compare brands and make informed purchasing decisions. India's organized retail sector has been expanding rapidly, with modern trade formats penetrating tier-two and tier-three cities, thereby extending the geographic reach of processed tomato product distribution.

The dominance of supermarkets and hypermarkets is further reinforced by their capacity to negotiate favorable terms with manufacturers, offer promotional discounts, and maintain consistent product availability. India's food and grocery retail landscape has witnessed significant investment, with major retail chains aggressively expanding their store networks across both metropolitan and semi-urban areas. World Food India 2024, held in September 2024 in New Delhi, attracted over 2,390 foreign delegates and 1,557 exhibitors from 108 countries, underscoring the growing international interest in India's organized food retail ecosystem and its role in distributing processed food products.

End-Use Insights:

Access the comprehensive market breakdown Request Sample

- Sauces

- Paste

- Canned Tomatoes

- Ketchup

- Juice

- Others

Sauces lead with a share of 30.0% of the total India tomato processing market in 2025.

Tomato-based sauces represent the largest end-use category in the India tomato processing market, driven by their versatile application in both traditional Indian cooking and the rapidly growing fast-food segment. The rapid expansion of quick-service restaurants, casual dining outlets, and cloud kitchens across India has substantially increased the demand for tomato-based sauces, which serve as essential components in pizza bases, pasta dishes, and dipping accompaniments. Evolving dietary patterns and a growing inclination toward flavorful, convenience-driven meal options are further supporting the steady growth of the sauce segment within the broader processed food industry.

The sauces segment also benefits from rising innovation in product formulations, including organic, no-onion-no-garlic variants, and regional flavor adaptations that cater to India's diverse culinary landscape. Manufacturers are introducing health-conscious options with reduced sugar and sodium content to appeal to wellness-oriented consumers. The foodservice sector, spanning from large international chains to regional street food vendors, relies heavily on pre-prepared tomato-based sauces, ensuring consistent demand volumes and positioning the segment for continued leadership within the India tomato processing market.

Regional Insights:

- North India

- West and Central India

- South India

- East India

North India represents the largest share at 32.0% of the total India tomato processing market in 2025.

North India holds a dominant regional position in the tomato processing market, supported by its large consumer base, rapid urban development, and the presence of major metropolitan centers such as Delhi-NCR, Lucknow, and Jaipur. The region is characterized by strong, organized retail penetration, efficient distribution frameworks, and close connectivity to established food processing clusters. Furthermore, the focus on the revitalization of the local processing ecosystem and the overall value chain in North India can also be observed in collaboration between governmental organizations, learning institutions, and industry players to increase tomato and paste production.

High disposable income and high population rate of young people living in the region, coupled with their high levels of penetration of quick-service restaurants and fast-food chains, create a high demand for processed tomato products. North India is another important consumption center of ketchup, sauces, and tomato paste, which are widely used in the street food culture and home cooking. The increased availability of branded processed tomato products to consumers in the region, due to increased growth of quick-commerce services in the region and neighbouring cities, is further strengthening the dominance of the region in the national market.

Market Dynamics:

Growth Drivers:

Why is the India Tomato Processing Market Growing?

Rapid Urbanization and Changing Consumer Dietary Preferences

India's accelerating urbanization is fundamentally transforming food consumption patterns, generating sustained demand for processed and convenience food products. As working professionals, nuclear families, and dual-income households seek time-saving meal solutions, the demand for ready-to-use tomato sauces, ketchups, pastes, and purees has increased significantly. The India food processing market size reached INR 30,498.0 Billion in 2024. Looking forward, IMARC Group expects the market to reach INR 65,244.8 Billion by 2033, exhibiting a growth rate (CAGR) of 8.38% during 2025-2033, reflecting the structural shift toward packaged foods. Urban consumers increasingly prefer branded tomato products for their consistency, extended shelf life, and ease of preparation, driving sustained market expansion across all processed tomato categories.

Supportive Government Policies and Investment in Food Processing Infrastructure

The Indian government's proactive policy framework is playing a pivotal role in strengthening the tomato processing industry's capacity and competitiveness. The Pradhan Mantri Kisan SAMPADA Yojana, with a cumulative 1,601 approved projects carrying a total project cost of INR 30,656.57 crore and approved grants of INR 8,853.38 crore as of June 2025, is building modern processing and cold chain infrastructure across the country. The Operation Greens scheme, originally designed for tomato, onion, and potato value chains, provides subsidies for transportation and storage to reduce post-harvest losses. Additionally, the Production Linked Incentive Scheme for Food Processing Industry, with an outlay of INR 10,900 crore, has approved 171 proposals leading to investments of INR 8,910 crore and the creation of approximately 2.89 lakh jobs, collectively fostering a favorable ecosystem for tomato processing market growth.

Expansion of Organized Retail and E-Commerce Distribution Networks

The rapid expansion of organized retail and digital commerce platforms is significantly broadening the distribution reach of processed tomato products across India. Modern trade formats, including supermarkets and hypermarkets, are aggressively expanding into tier-two and tier-three cities, while e-commerce and quick-commerce platforms are making processed foods accessible to a wider consumer base with ultra-fast delivery capabilities. The India e-commerce market size was valued at USD 129.72 Billion in 2025 and is projected to reach USD 651.10 Billion by 2034, growing at a compound annual growth rate of 19.63% from 2026-2034. The integration of processed tomato products into the catalogues of major online grocery platforms and 10-minute delivery services is creating new consumption occasions and attracting first-time buyers, thereby amplifying market growth across geographic segments.

Market Restraints:

What Challenges the India Tomato Processing Market is Facing?

Seasonal Price Volatility and Raw Material Supply Instability

The India tomato processing market faces significant challenges from seasonal fluctuations in raw tomato prices and supply disruptions caused by unpredictable weather patterns. Monsoon variations, pest infestations, and transportation bottlenecks during rainy seasons create supply-demand imbalances that increase input costs for processors and compress profit margins, hindering consistent production planning and pricing stability.

Inadequate Cold Chain and Post-Harvest Infrastructure

Despite government initiatives, India continues to experience substantial post-harvest losses in tomato crops due to insufficient cold storage facilities, inadequate refrigerated transportation, and limited processing infrastructure in rural producing regions. These gaps reduce the volume of tomatoes available for processing and increase wastage along the supply chain, constraining market capacity and elevating procurement costs for processing units.

Intense Competition from Unorganized and Low-Cost Producers

The presence of a large unorganized sector comprising small-scale local manufacturers of sauces, ketchups, and paste products creates pricing pressure on branded and organized processors. These unorganized players often operate with lower overhead costs and less stringent quality controls, offering products at significantly lower price points that appeal to price-sensitive consumers, particularly in semi-urban and rural markets.

Competitive Landscape:

The India tomato processing market exhibits a moderately fragmented competitive landscape characterized by the coexistence of established multinational food conglomerates, domestic FMCG brands, and emerging regional players. Market participants are investing in product diversification, premium and organic product lines, innovative packaging formats, and expanded distribution networks to strengthen market positioning. Competition is intensifying as manufacturers leverage advanced processing technologies to improve product quality and shelf life while simultaneously pursuing cost efficiencies. The growing influence of private-label products from major retail chains and the entry of international specialty brands are adding new competitive dimensions. Strategic partnerships with agricultural cooperatives and farmer producer organizations for raw material sourcing are emerging as key differentiators in the competitive landscape.

Recent Developments:

- In March 2026, Pluckk broadened its portfolio of clean-label offerings by introducing a healthier variant of tomato ketchup aimed at urban Indian consumers prioritizing better daily dietary options. Crafted in limited batches, the product is made from authentic tomato paste and utilizes jaggery instead of refined sugar to provide natural sweetness. Marketed as a lower-calorie choice, the ketchup excludes preservatives, synthetic thickeners, xanthan gum, and commonly used additives such as sodium benzoate, distinguishing it from traditional ketchup formulations available in the market.

- In January 2025, the Ministry of Food Processing Industries, Punjab Agricultural University, Punjab Agro Industries Corporation, and Hindustan Unilever Limited announced joint deliberations aimed at enhancing tomato production and paste manufacturing in Punjab to strengthen the domestic tomato processing value chain.

India Tomato Processing Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others |

| End-Uses Covered | Sauces, Paste, Canned Tomatoes, Ketchup, Juice, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Tomato Processing Market Research Report and Industry Forecast Report

The India tomato processing market size was valued at USD 1,472.17 Million in 2025.

The India tomato processing market is expected to grow at a compound annual growth rate of 4.93% from 2026-2034 to reach USD 2,361.71 Million by 2034.

Supermarkets and hypermarkets held the largest share at 38.0% in 2025, driven by their extensive product assortments, organized retail expansion across urban and semi-urban areas, competitive promotional strategies, and the growing consumer preference for one-stop shopping destinations.

Key factors driving the India tomato processing market include rapid urbanization, changing dietary preferences toward convenience foods, supportive government policies and investments in food processing infrastructure, expanding organized retail and e-commerce distribution channels, and increasing adoption of health-conscious products.

Major challenges include seasonal price volatility in raw tomato supply, inadequate cold chain and post-harvest infrastructure in producing regions, intense competition from unorganized low-cost producers, high tomato crop wastage due to logistical gaps, and fluctuating input costs driven by weather disruptions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)