Indonesia Drones Market Size, Share, Trends and Forecast by Type, Component, Payload, Point of Sale, End-Use Industry, and Region, 2026-2034

Indonesia Drones Market Summary:

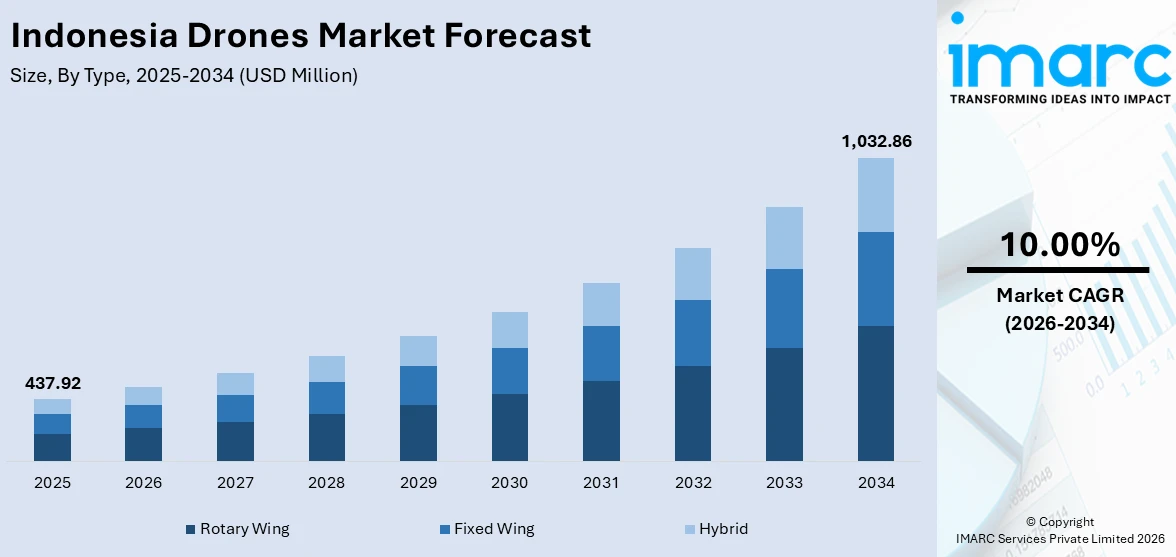

The Indonesia drones market size was valued at USD 437.92 Million in 2025 and is projected to reach USD 1,032.86 Million by 2034, growing at a compound annual growth rate of 10.00% from 2026-2034.

The Indonesia drones market is gaining robust momentum as the nation accelerates its digital transformation and modernizes key industries including agriculture, defense, and infrastructure development. Rising government investment in military capabilities, coupled with increasing adoption of precision farming technologies across the archipelago, is driving strong demand for unmanned aerial systems. Advancements in drone autonomy, sensor integration, and AI-powered analytics are reshaping operational efficiencies across both commercial and defense applications, positioning Indonesia as an emerging drone hub in Southeast Asia and bolstering the Indonesia drones market share.

Key Takeaways and Insights:

- By Type: Rotary wing dominates the market with a share of 50% in 2025, owing to its superior hovering capability, vertical takeoff and landing flexibility, and widespread applicability across agriculture, surveillance, and infrastructure inspection tasks throughout the Indonesian archipelago.

- By Component: Hardware leads the market with a share of 54% in 2025. This dominance is driven by continuous demand for airframes, propulsion systems, cameras, and sensor payloads that form the foundational architecture of drone platforms deployed across commercial and military applications.

- By Payload: 25-170 kilograms represents the biggest segment with a market share of 45% in 2025, reflecting the growing deployment of medium-payload drones for defense reconnaissance, agricultural spraying, and logistics operations that require substantial carrying capacity.

- By Point of Sale: Original equipment manufacturers (OEM) represent the largest segment with 68% share in 2025, driven by large-scale government and defense procurement contracts that favor direct manufacturer supply channels for quality assurance and technology transfer agreements.

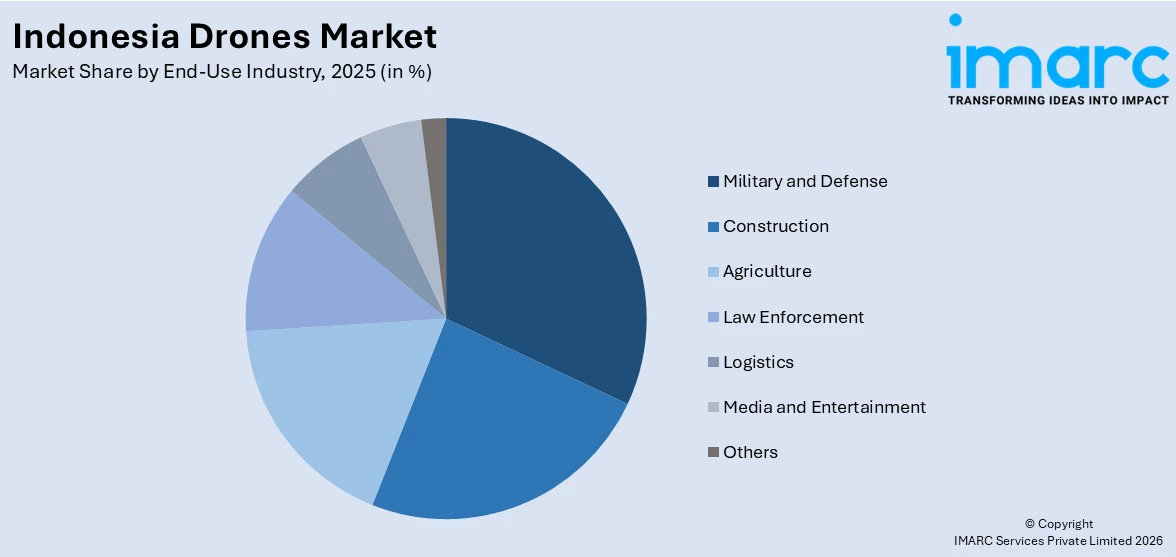

- By End-Use Industry: Military and defense exhibit a clear dominance in the market with 30% share in 2025, reflecting Indonesia’s strategic emphasis on strengthening surveillance, border security, and maritime domain awareness across its vast archipelagic territory.

- Key Players: Key players drive the Indonesia drones market by expanding product portfolios, investing in indigenous manufacturing capabilities, forging international defense partnerships, and strengthening distribution networks. Their focus on technology transfer, precision agriculture solutions, and AI integration accelerates adoption across diverse sectors.

To get more information on this market Request Sample

The Indonesia drones market is advancing as government agencies, industries, and defense establishments embrace unmanned aerial technologies for enhanced operational capabilities and data-driven decision-making. A major factor shaping this trajectory is the nation’s accelerating military modernization under President Prabowo Subianto’s defense strategy, which is fueling substantial procurement of advanced unmanned combat and surveillance platforms. For instance, in February 2025, Turkish drone manufacturer Baykar signed a joint venture agreement with Indonesian defense company Republikorp to establish a drone manufacturing facility in Indonesia. Simultaneously, the agricultural sector is witnessing rapid drone adoption for precision spraying, crop monitoring, and plantation management across palm oil estates and rice paddies. Expanding regulatory clarity from the Directorate General of Civil Aviation, growing domestic manufacturing capabilities, and rising interest in drone-as-a-service models are contributing to a more favorable environment for sustained Indonesia drones market growth.

Indonesia Drones Market Trends:

Rapid Expansion of Agricultural Drone Applications

Indonesia is experiencing a significant surge in agricultural drone deployment as farmers and plantation operators adopt precision technologies to improve crop yields and reduce operational costs. Drones equipped with multispectral imaging, automated spraying systems, and AI-driven analytics are transforming traditional farming practices across rice paddies and palm oil estates. For instance, in August 2025, Terra Drone Corporation signed a sales partnership agreement with PT Yanmar Diesel Indonesia for distribution of its G20 and E16 agricultural drones, with approximately 120 units scheduled for delivery within 2025. Drone-as-a-service models are enabling smallholder farmers across islands such as Java, Sumatra, and Kalimantan to access advanced technologies without steep initial investments, supporting food security and Indonesia drones market growth.

Growing Military Drone Procurement and Domestic Manufacturing

Indonesia’s defense sector is witnessing an unprecedented push toward integrating unmanned aerial systems into military operations, driven by maritime security imperatives and broader regional defense dynamics. The government is prioritizing the acquisition of medium-altitude long-endurance and high-altitude long-endurance platforms for intelligence, surveillance, and reconnaissance missions. For instance, in 2024, Indonesia signed a USD 300 Million deal with Turkish Aerospace Industries to procure 12 ANKA drones, with six units built in Turkey and six assembled locally by Indonesian aerospace firm PTDI, including technology transfer arrangements. These developments are positioning Indonesia as an emerging center for drone manufacturing in Southeast Asia.

Advancement in Drone Traffic Management and Regulatory Frameworks

Indonesia is making meaningful strides in establishing drone traffic management infrastructure to support the safe scaling of commercial drone operations. The Directorate General of Civil Aviation is working to clarify operating frameworks for commercial drone use, enhancing investor confidence and market expansion. For instance, Terra Drone Corporation conducted Indonesia's first multi-drone flight demonstration utilizing an Unmanned Traffic Management platform in the suburbs of Jakarta, as part of a project supported by Japan's Ministry of Economy, Trade, and Industry. These initiatives are laying the groundwork for broader drone deployment across logistics, infrastructure inspection, and urban air mobility applications.

Market Outlook 2026-2034:

Indonesia’s drones market is positioned for robust expansion, supported by accelerating military modernization, rising precision agriculture adoption, and maturing regulatory ecosystems. The market generated a revenue of USD 437.92 Million in 2025 and is projected to reach a revenue of USD 1,032.86 Million by 2034, growing at a compound annual growth rate of 10.00% from 2026-2034. Increasing government defense expenditure, with Indonesia’s 2025 defense budget rising to approximately IDR 165.2 Trillion, is creating a strong foundation for continued military drone acquisition. Simultaneously, the expansion of domestic manufacturing capabilities through international joint ventures, along with the growing adoption of drone-based services in agriculture, construction, and logistics, are expected to foster a more competitive, innovative, and sustainable drone ecosystem across the Indonesian archipelago throughout the forecast period.

Indonesia Drones Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Type | Rotary Wing | 50% |

| Component | Hardware | 54% |

| Payload | 25-170 Kilograms | 45% |

| Point of Sale | Original Equipment Manufacturers (OEM) | 68% |

| End-Use Industry | Military and Defense | 30% |

Type Insights:

- Fixed Wing

- Rotary Wing

- Hybrid

Rotary wing dominates with a market share of 50% of the total Indonesia drones market in 2025.

Rotary wing drones have emerged as the most widely deployed drone type in Indonesia, driven by their versatile flight characteristics including vertical takeoff and landing, hovering stability, and maneuverability in confined spaces. These attributes make them indispensable for applications ranging from agricultural crop spraying and infrastructure inspection to military surveillance across the nation's diverse and challenging terrain. Indonesia's vast archipelagic geography demands platforms that can operate effectively in varied environments, from dense urban settings in Java to remote plantation areas in Kalimantan and Sumatra, reinforcing the preference for rotary wing configurations.

The agricultural sector in particular has fueled rotary wing adoption, with multirotor drones being extensively used for precision spraying on palm oil plantations and rice paddies. State-owned enterprises and private operators are increasingly deploying these platforms for automated spraying, fertilizer spreading, and crop health monitoring, achieving more uniform coverage and reducing chemical use compared to manual methods. Defense and law enforcement agencies also rely heavily on rotary wing platforms for tactical reconnaissance, border surveillance, and maritime patrol missions across the archipelago.

Component Insights:

- Hardware

- Software

- Accessories

Hardware leads the market with a share of 54% of the total Indonesia drones market in 2025.

Hardware components constitute the backbone of every drone platform, encompassing airframes, propulsion systems, flight controllers, cameras, sensors, and communication modules. The dominance of this segment in Indonesia reflects the substantial upfront investment required for physical drone infrastructure across both commercial and military procurement programs. As government defense contracts and agricultural modernization initiatives drive bulk platform acquisitions, hardware expenditure continues to account for the majority of market revenues, supported by growing demand for advanced sensor payloads and ruggedized airframe designs suited to tropical operating conditions.

Local manufacturing efforts are further strengthening hardware demand within the Indonesian market. Domestic companies are actively pursuing local content certification for their in-house developed drone platforms, improving eligibility for government and public sector projects while enabling more efficient maintenance operations. Indigenous manufacturers and system integrators are contributing to hardware development through localized production of airframes, propulsion components, and sensor assemblies, reducing import dependency and supporting the government's broader industrial self-sufficiency objectives in the unmanned aerial systems sector.

Payload Insights:

- <25 Kilograms

- 25-170 Kilograms

- >170 Kilograms

25-170 kilograms is the largest segment, accounting for 45% of the total Indonesia drones market in 2025.

The 25-170 kilograms payload category has established itself as the dominant segment in Indonesia's drone market, driven by its suitability for both military reconnaissance operations and commercial applications requiring substantial carrying capacity. Defense-oriented platforms in this weight class are deployed for intelligence, surveillance, and reconnaissance missions across Indonesia's extensive maritime boundaries, while commercial operators utilize them for large-scale agricultural spraying, heavy-payload delivery, and industrial infrastructure inspection tasks that demand robust lifting capabilities beyond what lighter drone categories can provide.

Military procurement has been a particularly strong driver for this payload category. Indonesia's defense modernization strategy emphasizes acquiring medium-altitude long-endurance platforms falling within this payload range, designed for extended surveillance and strike-capable reconnaissance missions. The planned integration of such systems across the Indonesian Air Force, Army, and Navy is expected to significantly enhance the nation's territorial monitoring capabilities, reinforcing the strategic importance of the medium-payload drone segment as the country strengthens its maritime domain awareness and border security infrastructure.

Point of Sale Insights:

- Original Equipment Manufacturers (OEM)

- Aftermarket

Original equipment manufacturers (OEM) hold the largest share at 68% of the total Indonesia drones market in 2025.

The OEM channel commands a substantial majority of the Indonesia drones market, reflecting the dominance of direct manufacturer procurement in both defense and commercial sectors. Government defense contracts, which represent a significant portion of drone spending, typically involve direct procurement from original equipment manufacturers to ensure platform integrity, warranty coverage, and compliance with technology transfer requirements mandated under Indonesian defense procurement laws. This preference for OEM channels is reinforced by the complexity of advanced unmanned systems that require manufacturer-backed integration, calibration, and after-sales support.

International OEMs and their local joint venture partners are expanding their footprint in Indonesia through direct sales agreements and co-production arrangements. These OEM-driven partnerships involve establishing local entities for the manufacturing, assembly, and maintenance of unmanned aerial vehicles, with procurement sourced directly from the manufacturer. This model ensures quality assurance while facilitating the technology transfer that underpins Indonesia's defense industrial development strategy, allowing the nation to build indigenous capabilities while maintaining access to cutting-edge platforms from established global drone producers.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Agriculture

- Military and Defense

- Law Enforcement

- Logistics

- Media and Entertainment

- Others

Military and defense represent the leading segment with a 30% share of the total Indonesia drones market in 2025.

The military and defense sector is the largest end-use industry for drones in Indonesia, propelled by the nation's strategic imperative to modernize its armed forces and protect its vast maritime territory spanning thousands of islands. The current administration has significantly escalated defense spending priorities, creating substantial procurement opportunities for advanced unmanned aerial systems capable of intelligence gathering, border surveillance, and maritime patrol operations. This emphasis on strengthening national security through technological advancement continues to position defense as the primary demand driver within the Indonesian drone market.

Indonesia's military drone acquisitions encompass a wide range of platforms, from tactical surveillance drones to armed combat aerial vehicles and naval unmanned systems. The expanding scope of unmanned systems procurement extends beyond aerial platforms to include surface and underwater robotic systems for mine countermeasure and maritime security applications. The armed forces' increasing emphasis on integrated drone operations, supported by doctrinal reforms prioritizing emerging technologies and joint-service interoperability, is further reinforcing the military and defense segment's market leadership position across the Indonesian drone ecosystem.

Regional Insights:

- Java

- Sumatra

- Kalimantan

- Sulawesi

- Others

Java is the primary hub for Indonesia’s drone market, driven by the concentration of military installations, government agencies, defense procurement offices, and technology companies in the Jakarta metropolitan area. The region’s advanced infrastructure, major universities, and dense urban environment support both defense and commercial drone applications. Java’s agricultural activities, including rice cultivation, also contribute to growing demand for precision farming drones across the region.

Sumatra is emerging as a significant market for agricultural drones, driven by the island’s vast palm oil plantations and crop cultivation areas that benefit from precision spraying, pest management, and crop monitoring technologies. The region’s challenging terrain and large-scale plantations create strong demand for drone-based services that can cover extensive areas efficiently while reducing reliance on manual labor and improving operational productivity across the agricultural value chain.

Kalimantan represents a growing drone market supported by the region’s extensive palm oil estates, mining operations, and forestry activities that benefit from aerial surveying and monitoring capabilities. The ongoing development of Indonesia’s new capital city, Nusantara, in East Kalimantan is expected to create additional demand for construction drones, infrastructure inspection platforms, and urban planning applications that leverage advanced aerial mapping technologies.

Sulawesi is gradually adopting drone technologies across agriculture and infrastructure development, with growing interest in precision farming solutions for rice cultivation and plantation management. The region’s diverse topography, spanning mountainous terrain and coastal zones, presents opportunities for drones in disaster management, environmental monitoring, and maritime surveillance applications, contributing to the emerging drone ecosystem across eastern Indonesia.

Market Dynamics:

Growth Drivers:

Why is the Indonesia Drones Market Growing?

Accelerating Military Modernization and Defense Procurement

Indonesia's defense sector is undergoing a significant transformation, with the current administration prioritizing military modernization as a cornerstone of national security policy. The government's commitment to gradually elevating defense spending is generating substantial procurement opportunities for advanced unmanned aerial systems. Drones are increasingly recognized as cost-effective force multipliers capable of enhancing maritime surveillance, border security, and intelligence gathering across Indonesia's extensive territorial waters. The strategic shift toward integrating drone capabilities into all branches of the armed forces is creating a sustained demand pipeline, with international joint ventures and co-production agreements strengthening Indonesia's defense posture while fostering domestic manufacturing capabilities through mandated technology transfer arrangements. These initiatives are positioning the nation as an emerging hub for unmanned combat and reconnaissance platforms in Southeast Asia, supporting long-term force modernization objectives across air, land, and naval domains.

Rising Adoption of Precision Agriculture Technologies

Indonesia's agricultural sector, which remains a critical component of the national economy, is witnessing a fundamental shift toward technology-driven farming practices. The deployment of drones for crop monitoring, precision spraying, fertilizer application, and pest management is expanding rapidly across the nation's major cultivation areas, including rice paddies in Java and palm oil plantations in Sumatra and Kalimantan. Drone-as-a-service models are enabling smallholder farmers to access advanced aerial technologies without prohibitive capital expenditures. Government support and international partnerships are accelerating this adoption, with collaborative projects aimed at demonstrating and expanding drone-based agricultural solutions using high-precision positioning systems. These efforts are building a more robust agricultural drone ecosystem, improving food security, reducing environmental impact, and lowering dependency on manual labor across Indonesia's farming landscape.

Expanding Digital Infrastructure and Regulatory Clarity

Indonesia's improving digital infrastructure, including broadband connectivity and satellite communication networks, is facilitating the real-time data transmission and remote operation capabilities essential for advanced drone applications. The Directorate General of Civil Aviation has introduced regulatory reforms that clarify operating frameworks for commercial drone operations, enhancing investor confidence and enabling broader market participation. These developments are creating a more predictable business environment for drone manufacturers, service providers, and operators. The emergence of unmanned traffic management systems is further supporting market expansion, with demonstration projects simulating applications in agriculture, logistics, and security monitoring validating the feasibility of coordinated multi-drone operations. As the regulatory and infrastructure foundations strengthen, the drone market is expected to benefit from expanded commercial applications, increased private investment, and growing cross-sector adoption throughout the archipelago.

Market Restraints:

What Challenges the Indonesia Drones Market is Facing?

Regulatory Complexity and Airspace Management Challenges

Despite progress in regulatory reform, Indonesia’s drone operating framework remains complex and fragmented, with varying enforcement across regions and limited clarity on emerging applications such as beyond visual line of sight operations and autonomous delivery services. The absence of a comprehensive, unified national drone policy creates uncertainty for commercial operators, potentially delaying investment decisions and restricting the scalability of drone-based services across the archipelago.

Limited Domestic Manufacturing Capability and Import Dependency

Indonesia’s domestic drone manufacturing sector is still at a relatively nascent stage compared to established global producers, resulting in significant reliance on imported platforms and components. This dependency exposes the market to supply chain vulnerabilities, currency fluctuation risks, and higher procurement costs. While joint venture arrangements with international manufacturers are helping bridge this gap, developing a fully self-sufficient indigenous drone production ecosystem requires sustained investment in research, workforce training, and industrial infrastructure.

Skilled Workforce Shortage and Training Gaps

The rapid expansion of drone applications across military, agricultural, and commercial sectors is outpacing the availability of qualified drone operators, maintenance technicians, and data analysts in Indonesia. Training programs remain inconsistent, particularly for small drone operators who lack standardized military-grade instruction. The shortage of skilled personnel limits operational effectiveness, restricts the pace of adoption, and creates potential safety risks as demand for drone services continues to accelerate across diverse industries.

Competitive Landscape:

The Indonesia drones market features a dynamic competitive landscape with a mix of international technology leaders and emerging domestic manufacturers. Global players are strengthening their presence through joint ventures, technology transfer agreements, and strategic partnerships with Indonesian defense and industrial entities. Domestic companies are investing in indigenous platform development, agricultural drone solutions, and localized service networks to capture growing demand. Competition is intensifying across segments, driven by increasing government procurement, expanding commercial applications, and rising interest in drone-as-a-service business models that lower barriers to adoption for smaller enterprises and individual farmers.

Indonesia Drones Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed Wing, Rotary Wing, Hybrid |

| Components Covered | Hardware, Software, Accessories |

| Payloads Covered | <25 Kilograms, 25-170 Kilograms, >170 Kilograms |

| Points of Sales Covered | Original Equipment Manufacturers (OEM), Aftermarket |

| End-Use Industries Covered | Construction, Agriculture, Military and Defense, Law Enforcement, Logistics, Media and Entertainment, Others |

| Regions Covered | Java, Sumatra, Kalimantan, Sulawesi, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Indonesia Drones Market Research Report and Industry Forecast Report

The Indonesia drones market size was valued at USD 437.92 Million in 2025.

The Indonesia drones market is expected to grow at a compound annual growth rate of 10.00% from 2026-2034 to reach USD 1,032.86 Million by 2034.

Rotary wing dominated the market with a share of 50%, driven by its versatile flight capabilities, hovering stability, and widespread deployment across agriculture, defense surveillance, and infrastructure inspection applications throughout Indonesia.

Key factors driving the Indonesia drones market include accelerating military modernization and defense procurement, rising adoption of precision agriculture technologies, expanding digital infrastructure, growing regulatory clarity, and increasing domestic manufacturing capabilities.

Major challenges include regulatory complexity and airspace management limitations, limited domestic manufacturing capability, heavy import dependency, skilled workforce shortages, inconsistent operator training standards, and high upfront procurement costs for advanced drone platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)