Industrial Lubricants Market Size, Share, Trends and Forecast by Product Type, Base Oil, End-Use Industry, and Region, 2026-2034

Industrial Lubricants Market Size and Share:

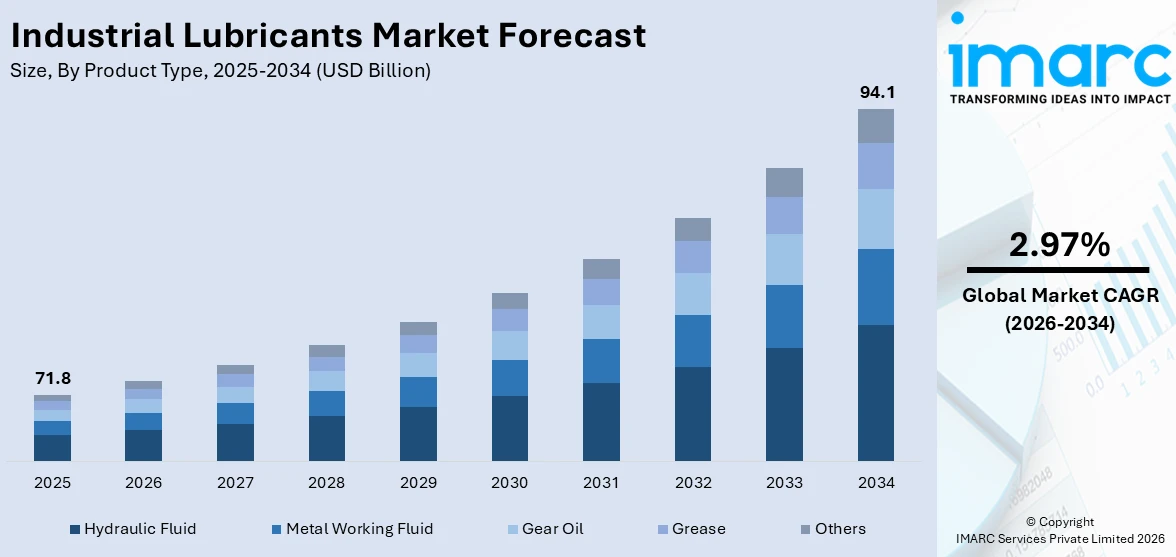

The global industrial lubricants market size was valued at USD 71.8 Billion in 2025. The market is projected to reach USD 94.1 Billion by 2034, exhibiting a CAGR of 2.97% from 2026-2034. Asia Pacific currently dominates the market, holding a market share of over 43.6% in 2025. The market is driven by growth in industrial automation, manufacturing and construction activity, and enhanced adoption in automotive and power generation industries. Synthetics and bio-based lubricants are being improved with advancements in equipment efficiency, wear reduction, and sustainability efforts. Growth in emerging markets, especially Asia Pacific, driven by fast-paced industrialization and infrastructure growth, also reinforces the demand in the market. The synergistic impact of technological advancement, environmentally friendly formulations, and increasing industrial processes is redefining the world, leading to a change in the overall industrial lubricants market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 71.8 Billion |

|

Market Forecast in 2034

|

USD 94.1 Billion |

| Market Growth Rate 2026-2034 | 2.97% |

The growing use of automation and Industry 4.0 technology in manufacturing, energy, and automotive industries is a key driver for industrial lubricants. The increasing dependence on robot systems, intelligent factories, and automated production lines generates a compelling need for high-performance lubricants to ensure operational efficiency, reduce friction, and maximize the service life of precision equipment. Industrial lubricants play a critical role in managing heat dissipation, wear reduction, and consistent performance under demanding operating conditions. At the same time, advancements in sophisticated synthetic and bio-based formulations with improved thermal stability, extended service life, and environmental compliance are building market opportunities. These technologies not only facilitate smoother operation of automated machinery but also boost sustainability efforts by minimizing waste and energy usage. As per sources, in April 2024, Castrol launched the MoreCircular program in the U.S., integrating re-refined base oil into premium lubricants to reduce carbon footprint and advance a circular lubricant industry. Moreover, industrial lubricants are becoming increasingly vital to the smooth functioning of advanced automated manufacturing ecosystems, underpinning market development over the next few years.

To get more information on this market Request Sample

The United States is a predominant participant in the industrial lubricants market, driven by strong manufacturing growth and major construction projects with a share of 80.60% in 2024. Industrial participants are spending on advanced lubricant solutions to cope with high performance and operating efficiency standards, ensuring smooth machine operation and minimizing downtime. Construction and industrial processes continue to expand slowly, highlighting the significance of industrial lubricants in optimizing power transmission, wear reduction, and maximum performance in heavy machinery, manufacturing lines, and construction machinery. The rising use of advanced equipment, combined with the incorporation of automation and precision systems, will likely support the demand for high-performance lubricants. The industrial lubricants market forecast indicates steady expansion, driven by technological advancements, industrial automation, and ongoing investment in operational efficiency, making these products essential for supporting the evolving needs of modern industries.

Industrial Lubricants Market Trends:

Industrial Lubricants in Power Generation and Renewable Energy

The increasing utilization of industrial lubricants in the power generation sector is a major factor driving market growth. These lubricants are extensively used in coal, steam, and gas power plants to improve equipment reliability, decrease operating expenses, increase machinery life, and safeguard essential parts like turbines, generators, boiler feed pumps, and mills against harsh operational conditions. Aside from traditional power generation, the amplifying use of industrial lubricants in renewable energy plants, including wind, hydroelectric, and nuclear power plants, equally propels market growth. Lubricants are crucial in sustaining the performance and efficiency of renewable energy equipment, facilitating smooth running under changing loads and environmental conditions. With growing energy production relying on sustainable energy sources, high-performance lubricants that maximize equipment performance and reliability are gaining prominence, further solidifying their strategic position in both conventional and renewable power generation markets and helping fuel consistent industrial lubricants market trends.

Automotive Applications and Bio-Based Lubricants

Industrial lubricants are extensively used in the automotive sector for the protection and performance enhancement of engines, transmissions, brakes, gears, wheels, and other important parts in passenger cars, commercial vehicles, construction equipment, and specialized machinery. Their use promotes smoother running, minimizes wear and tear, and overall vehicle efficiency, driving market demand. On the other hand, the growth of bio-based lubricants from biodegradable feedstocks has become a strong growth driver. These eco-friendly formulations minimize the need for petroleum-derived raw materials, reduce their ecological footprint, and impart enhanced viscosity, low volatility, and high-pressure performance. The growing focus on sustainability and legislative compliance in automotive production has prompted the use of bio-based lubricants. As such, the doubling impact of increasing automotive production and the transition towards sustainable lubricant products keeps fueling market growth, putting industrial lubricants at the forefront as an essential facilitator of improved vehicle performance and environmental responsibility.

Industrial Automation and Emerging Industries

The growth of industrial automation and robotic processing in manufacturing, packaging, and food processing industries has increased the demand for industrial lubricants considerably. These products guarantee maximum maintenance, minimize friction, and prolong the operating lifespan of machines and automated systems. Furthermore, advanced industrialization, rapid infrastructural development, and the implementation of government policies fostering bio-based lubricants are driving market development. Mass research and development efforts have also promoted innovation, maximizing product performance in a wide range of industrial applications. Lubricants also find growing applications in upcoming industries like marine and textile units, which speaks volumes about their versatility. Global industrial activity is still growing progressively, reinforcing the role of industrial lubricants in ensuring equipment efficiency, minimizing downtime, and maintaining operational dependability. All these aspects combined contribute to the vital role played by industrial lubricants in responding to the changing needs of contemporary industrial environments, paving the way for their ongoing growth and market significance.

Industrial Lubricants Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global industrial lubricants market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on product type, base oil, and end-use industry.

Analysis by Product Type:

- Hydraulic Fluid

- Metal Working Fluid

- Gear Oil

- Grease

- Others

The hydraulic fluid market accounted for a 27.6% share in 2025, indicative of its key function in maintaining industrial and mobile hydraulic systems in diverse industries. Hydraulic fluids play a critical function in transferring power in machinery while serving as lubricants, anti-corrosion agents, and temperature regulators. They are applied across construction equipment, manufacturing machinery, and automotive uses, where the delivery of dependable performance is critical to avoid operation downtime and enhance equipment longevity. Improvements in hydraulic fluid compositions, in the form of synthetic and bio-based variants, have also enhanced their market share by providing better viscosity, thermal stability, and wear protection at hostile operating conditions. Mechanization of manufacturing units and infrastructure development activities across the world is leading to high-performance hydraulic fluid demand. The growth in the segment is also facilitated by increasing use of automated equipment and precision machines, which need specialty fluids in order to stay efficient, cut down on friction, and avoid failure of components, validating hydraulic fluid as a top product category in the industrial lubricants market.

Analysis by Base Oil:

Access the comprehensive market breakdown Request Sample

- Mineral Oil

- Synthetic Oil

- Bio-based Oil

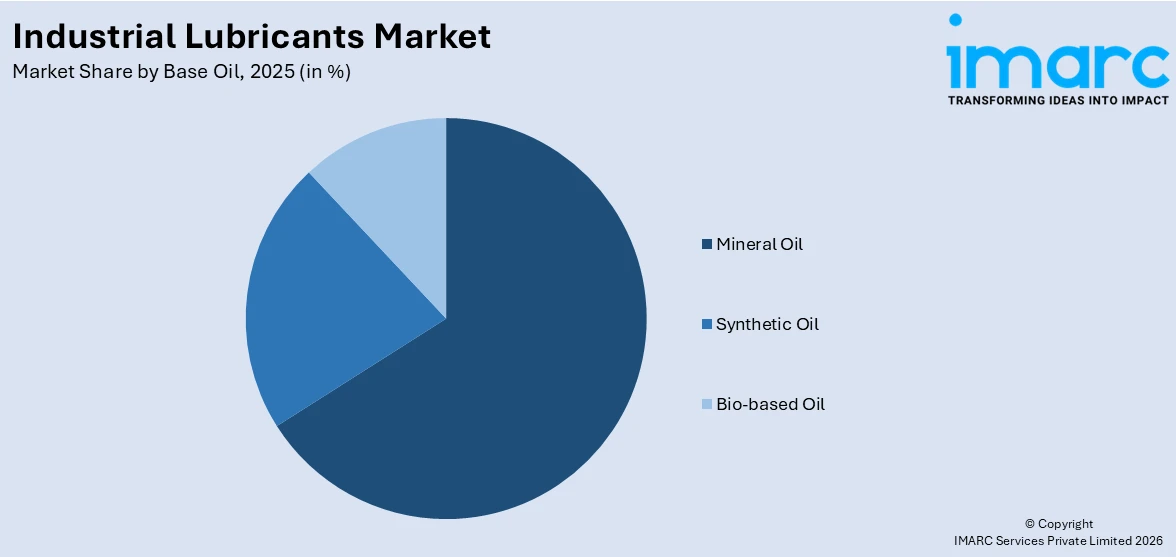

The mineral oil category contributed 66.2% in 2025 and continues to be a mainstream base oil in industrial lubricants on account of its low cost, ubiquity, and versatility for formulations. Mineral oils are the building blocks for hydraulic fluids, engine oils, and gear oils with consistent lubricity, heat stability, and protection from wear and oxidation. Their widespread applications in automotive, manufacturing, and construction industries underscore their flexibility across high-demanding applications. Furthermore, continuous research has also resulted in advanced mineral oil blends with superior performance attributes, allowing them to fulfill current machinery demands. Even with the increasing availability of synthetic and bio-based counterparts, mineral oil continues to enjoy strong presence in emerging markets and cost-sensitive regions. The segment's continued growth is a testament to its critical function in guaranteeing equipment efficiency, reducing operational downtime, and sustaining industrial machinery across various sectors, solidifying its status as a top base oil in the world's industrial lubricants industry.

Analysis by End-Use Industry:

- Construction

- Metal & Mining

- Cement Production

- Power Generation

- Automotive

- Chemical Production

- Oil & Gas

- Textile Manufacturing

- Food Processing

- Agriculture

- Pulp & Paper

- Others

Power generation leads with a 24% share, driven by rising electricity demand, renewable energy expansion, and the critical need for uninterrupted operations, efficiency, and equipment reliability in power plants. The growing reliance on advanced turbines and heavy machinery further fuels lubricant consumption, as high-performance products are essential to minimize downtime, reduce maintenance costs, and enhance overall energy output.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

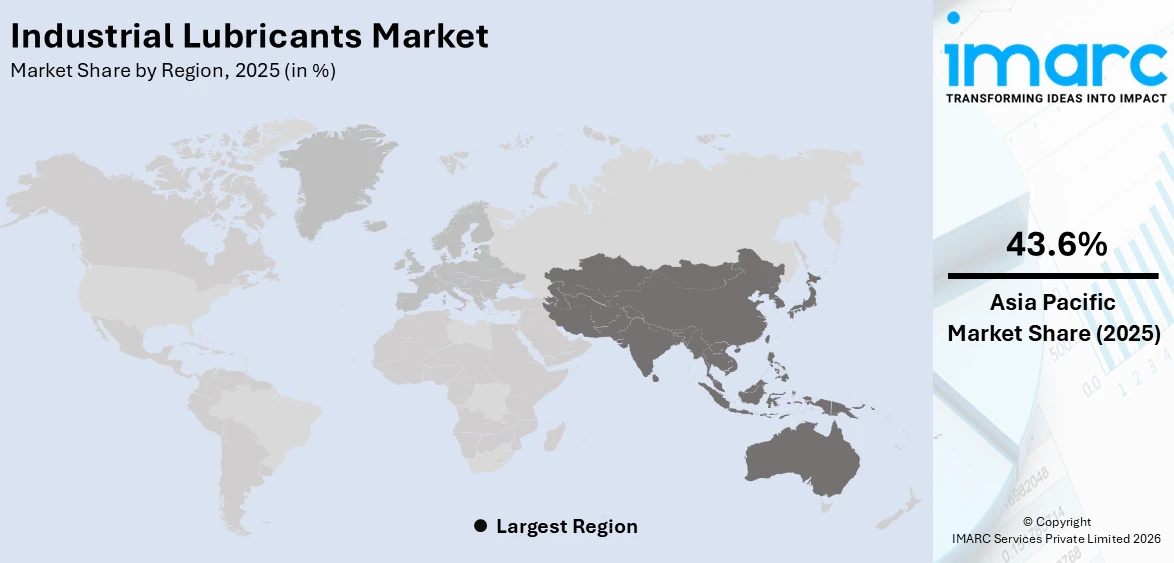

The Asia Pacific region accounted for a 43.6% share in 2025, fueled by industrialization, urbanization, and country-wide large-scale infrastructure and manufacturing projects in nations like China, India, Japan, and Southeast Asian nations. The industrial development of the region has resulted in higher usage of industrial lubricants in sectors such as automotive, construction, power generation, and manufacturing. Higher investments in mechanized and automated equipment have also further driven the demand for high-performance lubricants that offer thermal stability, anti-wear protection, and longer service life. Moreover, the movement toward sustainable and bio-based lubricants is also taking pace due to regulation mandates and environmental concerns. Increased industrial production and infrastructure project development, combined with increased vehicle manufacturing, have made the Asia Pacific region a key growth center. The industrial lubricants market in the region continues to experience strong demand, as a result of both technological development and the necessity for effective equipment maintenance across various industrial applications.

Key Regional Takeaways:

North America Industrial Lubricants Market Analysis

North America industrial lubricants market is witnessing steady growth due to growing manufacturing, construction, and automotive industries in the region. Growing adoption of newer machinery and industrial automation has seen greater demand for high-performance lubricants that improve equipment efficiency, minimize wear, and provide reliability during operation. Industrial lubricants are found to be used extensively in power generation, construction, and transportation sectors, where they are instrumental in preserving the performance of machinery under challenging conditions. Furthermore, the trend towards environmentally friendly and bio-based lubricants is picking up steam, with strong regulatory policies and sustainability initiatives backing it up. The industry is also impacted by continuing investments made in infrastructure development, urbanization, and industrial equipment modernization. Availability of well-established supply chains, technological innovations in lubricant formulations, and high operational efficiency focus further support market dynamics. Overall, these factors place North America as a mature and technologically sophisticated market with high industrial lubricant demand.

United States Industrial Lubricants Market Analysis

The United States industrial lubricants market is led mainly by the country's robust industrial sector, continuous development of manufacturing, and a steady emphasis on equipment maintenance and performance. As the automotive, aerospace, construction, energy, and metalworking industries are among the largest users of machinery, high-performance lubricants are necessary to maintain efficiency in operations, minimize wear and tear, and maximize the life of equipment. Increased developments in automated manufacturing systems and precision machinery also necessitate lubricants with high-pressure, temperature, and contamination endurance, further driving market demand. Further, the growth in the construction and mining industries is boosting the use of heavy-duty lubricants for off-road machinery and extreme operating conditions. Based on the Census Bureau, spending on construction activity accounted for a seasonally adjusted annual rate of about USD 2,136.2 Billion in June of 2025. Spending on construction activity between January and June 2025 was USD 1,036.1 Billion. Also contributing to the market are environmental laws and sustainability objectives, as they continue to drive the production and use of bio-based and synthetic lubricants with reduced emissions and extended service life. The renewed domestic manufacturing under government stimulus is also likely to boost industrial activity and subsequently lubricant demand.

Asia Pacific Industrial Lubricants Market Analysis

The Asia Pacific industrial lubricants market is growing as a result of swift industrialization, infrastructure growth, and the growth of major sectors like manufacturing, construction, mining, and transport. For example, the Index of Industrial Production in India saw a 2.9% growth during February 2025, reflecting the strong industrialization across the nation, according to the Press Information Bureau (PIB). These include China, India, Japan, and South Korea, which have robust demand for high-performance lubricants to sustain heavy equipment, production machinery, and automation systems. The growth in the region's construction and mining sectors also demands tough lubricants that can withstand harsh operating environments and prolong equipment life. On top of this, increasing energy demand, such as wind and thermal power generation expansion, is itself driving turbine and generator lubricant consumption significantly. Automotive and shipbuilding sectors also drive market growth with the demand for specialized fluids used in manufacturing processes.

Europe Industrial Lubricants Market Analysis

The Europe industrial lubricants market outlook is primarily driven by a well-established base of manufacturing, increasing energy efficiency demand, and robust regulatory emphasis on sustainability and environmental concerns. Such major industries as automotive, aerospace, marine, metalworking, and power generation depend heavily upon high-performance lubricants to maximize equipment reliability, reduce friction, and decrease downtime. As more industries implement Industry 4.0 and smart manufacturing, there is an increasing demand for evolved lubricants that can accommodate precision equipment and automated technologies. The focus of the region towards carbon neutrality and lower emissions is also propelling the adoption of synthetic and bio-based lubricants that have longer life cycles and less environmental footprints. Additionally, the increasing emphasis on circular economy practices is driving demand for recyclable and environmentally friendly lubricant solutions. The expansion of wind energy and other renewable projects is also contributing substantially to lubricant consumption, as these systems require specialized fluids for long-term, low-maintenance operation. In a February 2025 industry report, installations of new wind energy in Europe totaled 16.4 GW in 2024, bringing the overall wind energy capacity in the region to 285 GW. Between 2025 and 2030, the continent will install 187 GW of new wind energy installations, bringing overall wind energy capacity to 450 GW by 2030.

Latin America Industrial Lubricants Market Analysis

The industrial lubricants market in Latin America is growing strongly because of increasing industrial activity, especially within mining, manufacturing, agriculture, and construction industries. Brazil, Mexico, and Chile are increasingly spending on infrastructure development and extraction of resources, which both are heavily dependent on proper lubrication solutions for heavy-duty equipment and machinery. The farm sector, being a major contribution to regional economies, is also making a large contribution towards lubricant demand in tractors, harvesters, and irrigation systems. For example, Argentina's agriculture sector contributed 15.7% towards the country's GDP in 2021 and 10.6% of taxation revenues. Apart from this, modernization of manufacturing units and greater emphasis on machine care are also driving the use of high-performance and synthetic lubricants.

Middle East and Africa Industrial Lubricants Market Analysis

Middle East and Africa industrial lubricants market is highly impacted by the dominating presence of the oil and gas sector in the region, widespread construction activities, and booming manufacturing industries. For example, Saudi Arabia in 2023 was the leading global exporter of crude oil and the third-largest producer of crude oil and condensate, with about 9.5 Million b/d of crude oil production, as reported by the Energy Information Administration (EIA). In addition, urbanization and projects driven by government, mainly in the Gulf states, are creating demand for lubricants in transport and construction. Apart from this, Africa's mining industry, specifically for metals and minerals, also depends significantly on industrial lubricants for the reliability and efficiency of equipment. Increasing demand for long-lasting and high-performance lubricants is also defining product innovation in the region.

Competitive Landscape:

The industrial lubricants market competitive environment is typified by high innovation, product diversification, and global and regional market expansion strategies. Advanced formulations, such as synthetic and bio-based lubricants, are the area of focus for the major players in order to address changing industrial needs for high-performance, eco-friendly products. Firms are spending more on research and development to improve product efficiency, minimize operating wear, and ensure thermal stability, aimed at applications such as automotive, building, power generation, and manufacturing. Cooperation with machinery manufacturers and involvement in major industrial projects allow market players to consolidate their position and customize products for particular applications. Moreover, the focus on sustainability and environmental conformity has resulted in the release of green lubricants, further fueling competition. Expansion strategies in regional markets, technological advancements, and product tailoring remain the driving forces for market dynamics, keeping companies nimble in attending to the varied needs of industrial end users and sustaining long-term growth in the industrial lubricants industry.

The report provides a comprehensive analysis of the competitive landscape in the industrial lubricants market with detailed profiles of all major companies, including:

- Bharat Petroleum Corporation Limited

- BP p.l.c

- Chevron Corporation

- China Petrochemical Corporation

- Clariant AG

- ExxonMobil Corporation

- Fuchs Petrolub SE

- Gulf Oil International Ltd (Hinduja Group)

- Hindustan Petroleum Corporation Limited (Oil and Natural Gas Corporation)

- Idemitsu Kosan Co. Ltd.

- Indian Oil Corporation Ltd.

- Petroliam Nasional Berhad (PETRONAS)

- Phillips 66 Company

- Shell plc

- TotalEnergies SE

Latest News and Developments:

- August 2025: TotalEnergies Marketing India Private Limited (TEMIPL) officially launched its new range of advanced Quartz car engine lubricants in India, certified by API SQ and ILSAC GF-7 performance regulations. The new range of automotive lubricants includes the Quartz 7000 Future GF-7 5W-30, the Quartz 9000 Future GF-7 0W20, and the Quartz 9000 Xtra Future XT 0W-16.

- July 2025: Castrol introduced its latest Castrol MHP range of industrial lubricants designed to be utilized in the upcoming generation of distillate fuel-powered four-stroke medium-speed engines. The new lineup includes the Castrol MHP 1-30 and MHP 1-40 and has been reformulated using a smaller base number.

- June 2025: Castrol officially launched its Castrol Intelligent Lubrication Solutions to assist industrial clients in extending asset life, minimizing downtime, and optimizing lubricant usage. This launch demonstrates Castrol's dedication to assisting industrial clients in enhancing the performance and efficiency of their equipment.

- May 2025: Shell introduced a brand new packaging style for its renowned Shell Helix line of industrial lubricants. This new design reflects the company’s ongoing development efforts, as well as its steadfast dedication to quality and innovation.

- February 2025: Interflon officially launched a new range of PFAS-free industrial lubricants developed using advanced MicPol technologies. With this launch, the company aims to provide companies with a high-performing PFAS-free lubricant that fulfills international regulatory requirements while reducing its negative effects on the environment.

Industrial Lubricants Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Hydraulic Fluid, Metal Working Fluid, Gear Oil, Grease, Others |

| Base Oils Covered | Mineral Oil, Synthetic Oil, Bio-based Oil |

| End-Use Industries Covered | Construction, Metal & Mining, Cement Production, Power Generation, Automotive, Chemical Production, Oil & Gas, Textile Manufacturing, Food Processing, Agriculture, Pulp & Paper, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Bharat Petroleum Corporation Limited, BP p.l.c, Chevron Corporation, China Petrochemical Corporation, Clariant AG, ExxonMobil Corporation, Fuchs Petrolub SE, Gulf Oil International Ltd (Hinduja Group), Hindustan Petroleum Corporation Limited (Oil and Natural Gas Corporation), Idemitsu Kosan Co. Ltd., Indian Oil Corporation Ltd., Petroliam Nasional Berhad (PETRONAS), Phillips 66 Company, Shell plc, TotalEnergies SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the industrial lubricants market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global industrial lubricants market.

- The study maps the leading as well as the fastest growing regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the industrial lubricants industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Industrial Lubricants Market Report

The industrial lubricants market was valued at USD 71.8 Billion in 2025.

The industrial lubricants market is projected to exhibit a CAGR of 2.97% during 2026-2034, reaching a value of USD 94.1 Billion by 2034.

The market for industrial lubricants is largely influenced by rising industrial automation, surging manufacturing and construction activities, and increasing adoption in automobile and power generation applications. Development in synthetic and bio-based lubricants, enhancing equipment efficiency, wear reduction, and environmental compliance, also further aids in long-term market growth.

Asia Pacific currently dominates the industrial lubricants market, accounting for a share of 43.6%. High-speed industrialization, expansive infrastructure development on a large scale, increasing car manufacturing, and extensive use of high-performance and eco-friendly lubricants are among the factors underpinning the region's leadership, making it a vital hub for the consumption of industrial lubricants in various end-use industries.

Some of the major players in the industrial lubricants market include Bharat Petroleum Corporation Limited, BP p.l.c, Chevron Corporation, China Petrochemical Corporation, Clariant AG, ExxonMobil Corporation, Fuchs Petrolub SE, Gulf Oil International Ltd (Hinduja Group), Hindustan Petroleum Corporation Limited (Oil and Natural Gas Corporation), Idemitsu Kosan Co. Ltd., Indian Oil Corporation Ltd., Petroliam Nasional Berhad (PETRONAS), Phillips 66 Company, Shell plc, TotalEnergies SE, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)