Injection Molded Plastics Market Report by Raw Material (Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), High-Density Polyethylene (HDPE), Polystyrene (PS), and Others), Application (Packaging, Consumables and Electronics, Automotive and Transportation, Building and Construction, Medical, and Others), and Region 2026-2034

Injection Molded Plastics Market Size:

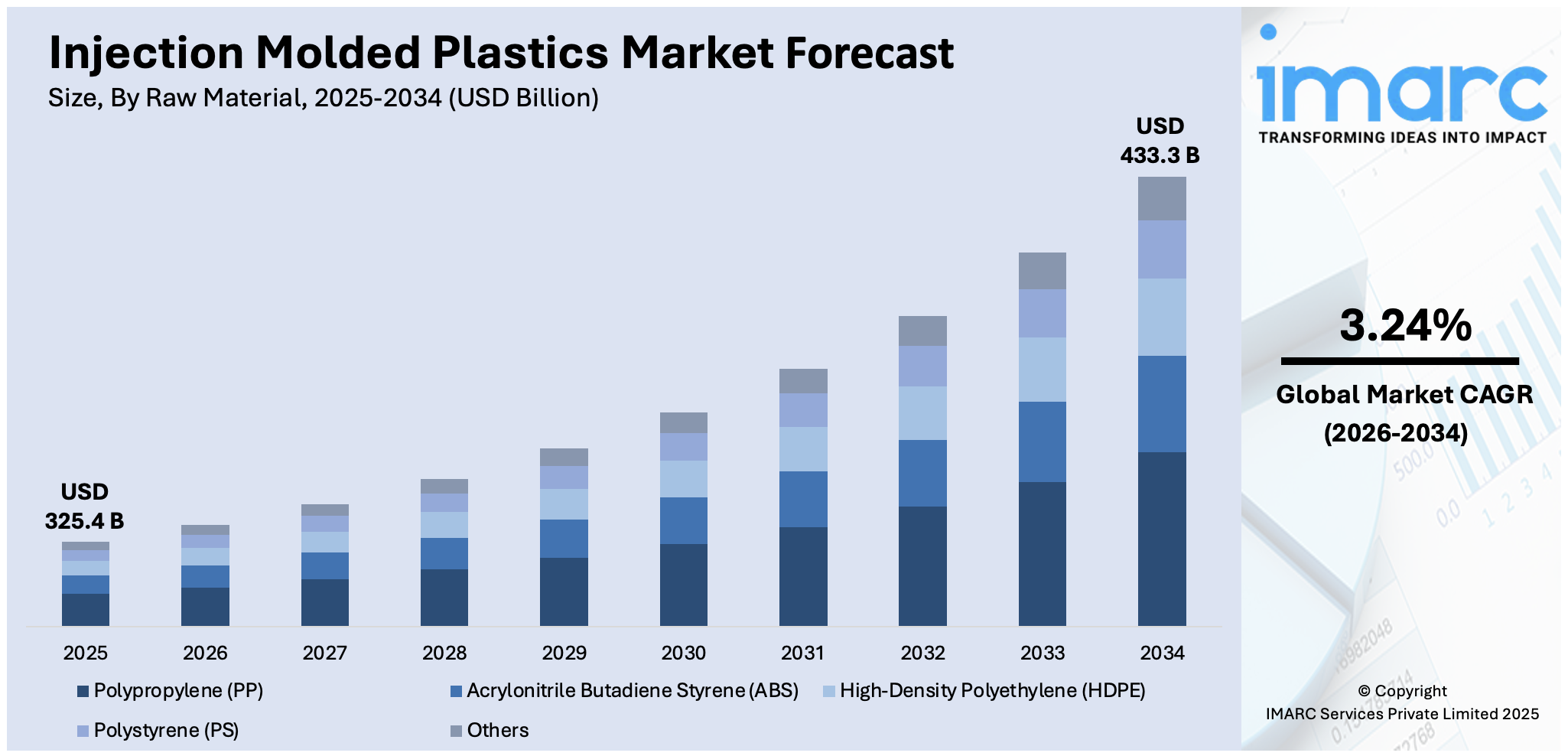

The global injection molded plastics market size reached USD 325.4 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 433.3 Billion by 2034, exhibiting a growth rate (CAGR) of 3.24% during 2026-2034. Asia Pacific currently dominates the market due to its large manufacturing base, cost-effective production capabilities, and growing demand in various industries like automotive and electronics. The market is majorly driven by increasing demand in key industries such as healthcare, automotive, and packaging, mainly fueled by their durable and lightweight attributes.

Market Size & Forecasts:

- Injection molded plastics market was valued at USD 325.4 Billion in 2025.

- The market is projected to reach USD 433.3 Billion by 2034, at a CAGR of 3.24% from 2026-2034.

Dominant Segments:

- Raw Material: Polypropylene (PP) accounts for the biggest market share attributed to its excellent balance of affordability, strength, and adaptability. Its durability against chemicals, moisture, and heat, combined with its simple processing, renders it a favored option for numerous applications throughout various industries.

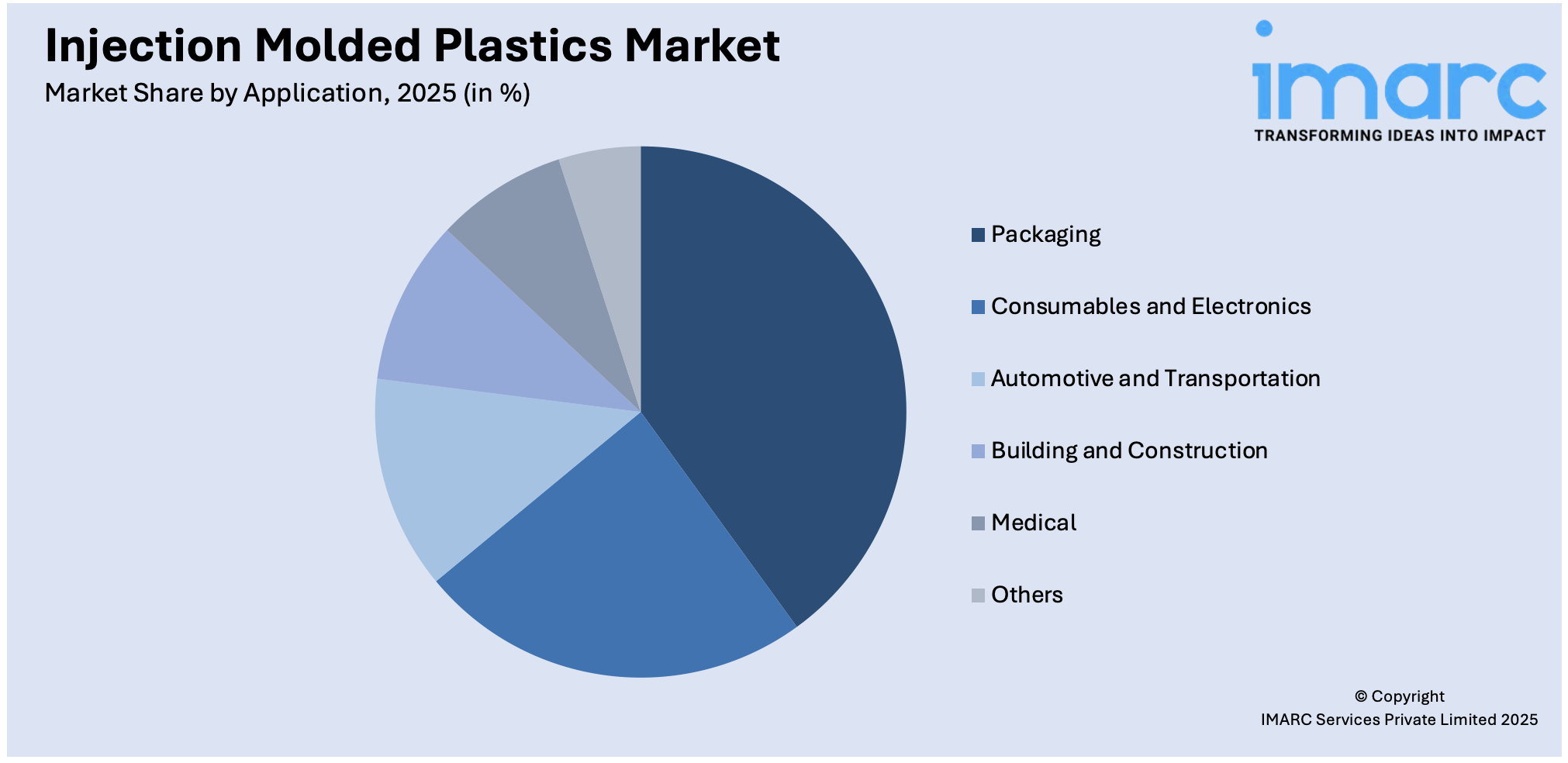

- Application: Packaging represents the largest segment because of its extensive role in guaranteeing product safety, convenience, and effective transportation. The adaptability, affordability, and capacity to form intricate designs render plastic packaging ideal for multiple sectors, boosting its considerable demand and market presence.

- Region: Asia Pacific dominates the injection molded plastics market owing to its strategic role as a manufacturing center, availability of inexpensive labor, and extensive industrial output. The area is supported by a strong supply chain, comprehensive infrastructure, and increasing demand in multiple sectors, impelling the market growth and innovation.

Key Players:

- The leading companies in injection molded plastics market include BASF SE, Chevron Phillips Chemical Company LLC, Eastman Chemical Company, Exxon Mobil Corporation, Huntsman International LLC, INEOS, LyondellBasell Industries Holdings B.V., SABIC, and The Dow Chemical Company.

Key Drivers of Market Growth:

- Automotive Sector Demand: The demand for injection molded plastics in the automotive market is influenced by the demand for lightweight, robust materials that enhance fuel efficiency and comply with environmental standards. This trend is further supported by the rising sales of electric vehicles (EVs), which is catalyzing the demand for high-performance plastics in car manufacturing.

- Healthcare Sector Growth: The healthcare industry is bolstering the market growth because of the accuracy, affordability, and hygiene of injection molded plastics. Their benefits, including simple sterilization, biocompatibility, and light weight, render them ideal for medical instruments, surgical equipment, and disposable items.

- Cost-Effectiveness of Molding: The affordability of injection molding allows large-scale manufacturing at minimal costs. By minimizing waste, accelerating production, and requiring less manual labor, it guarantees precision and decreases total production expenses. Its scalability and capacity to recycle waste materials further improve its cost-effectiveness for mass production.

- Technological Advancements: Improvements in injection molding technology are increasing production efficiency, lowering expenses, and enhancing product quality. The combination of artificial intelligence (AI) and sensors facilitates real-time enhancement, better precision, and energy efficiency, making it easier to satisfy the growing demand for high-quality, tailor-made products.

- Awareness about Sustainability: Sustainability is emerging as a crucial factor in the injection molded plastics sector, as companies and individuals pursue environment-friendly options. The emphasis on minimizing plastic waste and emissions encourages the creation of recyclable and bio-based materials, in addition to supporting energy-efficient production and circular economy methods.

- Regulations and Standards: Regulatory measures and sector benchmarks are propelling the injection molded plastics market growth by implementing tougher environmental guidelines concerning plastic usage, recycling, and waste handling. In reaction, the sector is creating recyclable and biodegradable materials while maintaining conformity with quality, safety, and performance standards in various industries.

To get more information on this market Request Sample

Future Outlook:

- Strong Growth Outlook: The injection molded plastics market is poised for strong growth due to increasing industrial demand, technological advancements, and the shift towards more sustainable and efficient manufacturing processes. The expanding use of injection molded plastics in diverse sectors, coupled with innovations in material science, is driving long-term market expansion.

- Market Evolution: The injection molded plastics market is evolving rapidly with advancements in automation, material innovations, and improved production techniques. Companies are focusing on enhancing efficiency, reducing waste, and incorporating sustainable practices, leading to a transformation in how products are designed, produced, and utilized across various industries.

Injection molded plastics are manufactured using thermoplastics, such as acrylonitrile butadiene styrene (ABS), high-density polyethylene (HDPE), low-density polyethylene (LDPE), polycarbonate (PC), polyamide (nylon), high impact polystyrene (HIPS), and polypropylene (PP). They are cost-effective and lightweight and consequently, their utilization is rising across the globe for producing numerous consumer goods. Besides this, they are also employed in different industries, such as packaging, electronics, and healthcare.

Injection Molded Plastics Market Trends:

Increasing Demand in Automotive Sector

The worldwide injection molded plastics market is seeing considerable demand from the automotive sector, motivated by this industry's focus on lightweight materials to improve fuel efficiency and lower emissions. Injection molded plastics are more frequently used in automotive parts, substituting conventional metals because of their affordability, adaptability, and outstanding strength. Moreover, the growing sales of electric vehicles (EVs) alongside the enforcement of strict environmental regulations are catalyzing the demand for high-performance plastics in automotive production. Industry reports show that in 2024, sales of battery-electric and plug-in hybrid vehicles rose by 22%, totaling 1.35 million units. This trend is supporting the growth of the market, especially in areas with robust automotive production capabilities, where the demand for lightweight, durable materials is becoming more essential.

Growing Applications in Healthcare

According to the injection molded plastics market forecast, healthcare sector is anticipated to remain one of the predominant drivers for the global market. Numerous surgical tools, medical equipment, and drug packaging today rely on injection molded plastics for their accuracy, affordability, and cleanliness. In August 2024, PCPI Plastics revealed the purchase of Sonolite Plastics Corporation’s injection molded medical product line, enhancing its medical production capabilities at its US facility. Moreover, these plastics provide advantages like simple sterilization, excellent biocompatibility, and lightweight characteristics, which make them suitable for cutting-edge healthcare technologies and single-use medical items. Continuous progress in medical technology, along with a heightened emphasis on infection control, highlights the growing need for these specialized plastics, further aiding the growth of the market in the healthcare industry.

Cost-Effectiveness of Injection Molding

Injection molding provides efficient high-volume manufacturing at comparatively low expenses because of decreased waste, quicker production rates, and limited necessity for manual involvement. The method enables great accuracy, decreasing the necessity for additional finishing or labor-heavy tasks, thereby minimizing total production expenses. With industries striving to enhance productivity, the affordability of injection molding presents a compelling choice for producers, particularly in large-scale manufacturing situations. Moreover, the capacity to repurpose waste material produced during manufacturing also lowers expenses. The injection molding process offers scalability and the ability to manufacture substantial amounts of uniform and high-quality items, making it an attractive option for companies aiming to satisfy significant demand effectively and affordably. This financial benefit is a crucial reason for the ongoing expansion of the market.

Injection Molded Plastics Market Growth Drivers:

Technological Advancements

Technological progress in injection molding equipment is increasing production efficiency, lowering expenses, and improving product quality. The incorporation of AI and sophisticated sensors into injection molding systems allows manufacturers to enhance production instantly. In 2024, Haitian UK introduced its 5th Generation injection molding machines, featuring AI and smart sensors for enhanced production efficiency. These devices incorporated sophisticated capabilities like self-recognition, self-adaptation, and smart energy management, enhancing operational efficiency and reducing waste. Equipped with standard features such as HT Inject, HT Energy, and HT Clamp, these machines also promoted improved energy efficiency and superior connectivity, leading to greater cost savings. With businesses aiming for greater accuracy and increased automation, such technological progress is vital for satisfying the growing need for high-quality, customizable goods.

Shift Towards Sustainability and Eco-friendly Practices

Sustainability issues are emerging as a key factor in the injection molded plastics industry, as individuals and companies alike are progressively looking for eco-friendly options. The drive to lessen plastic waste and carbon emissions is encouraging the creation of bio-based and recyclable substances for injection molding. Advancements, such as compostable plastics and reusable polymers, are aiding in achieving worldwide sustainability objectives. Producers are incorporating energy-saving methods and working to lower emissions in the manufacturing process. The emergence of circular economies, in which products are intended for reuse and recycling, is encouraging companies to investigate sustainable plastic options. For instance, in 2024, Origin Materials and PackSys Global unveiled a manufacturing system for PET caps and closures at NPE2024, employed injection molding to create monomaterial plastic bottles that possess enhanced barrier properties, increasing recyclability. With stricter regulations on waste management and environmental protection, companies are adopting such green initiatives to meet individual expectations.

Government Regulations and Industry Standards

With growing environmental concerns, governments around the globe are implementing more rigorous regulations related to plastic usage, recycling, and waste management. As a response, the injection molding sector is evolving by creating recyclable, biodegradable, and eco-friendly plastics to meet these regulations. Additionally, sectors like automotive, healthcare, and electronics necessitate that products comply with particular standards concerning quality, safety, and performance, promoting the utilization of precision injection molding techniques. Producers must guarantee that their plastic parts comply with strict regulatory standards regarding material safety, strength, and environmental effects. These rules not only enhance innovation in material creation but also promote the use of sophisticated manufacturing techniques that satisfy compliance standards. With global regulations becoming stricter, the injection molded plastics industry is adapting, guaranteeing the fulfillment of sustainable and high-quality criteria.

Injection Molded Plastics Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on raw material and application.

Breakup by Raw Material:

- Polypropylene (PP)

- Acrylonitrile Butadiene Styrene (ABS)

- High-Density Polyethylene (HDPE)

- Polystyrene (PS)

- Others

Polypropylene (PP) accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the raw material. This includes polypropylene (PP), acrylonitrile butadiene styrene (ABS), high-density polyethylene (HDPE), polystyrene (PS), and others. According to the report, polypropylene (PP) represented the largest segment.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Packaging

- Consumables and Electronics

- Automotive and Transportation

- Building and Construction

- Medical

- Others

Packaging holds the largest share of the industry

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes packaging, consumables and electronics, automotive and transportation, building and construction, medical, and others. According to the report, packaging accounted for the largest market share.

Breakup by Region:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest injection molded plastics market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for injection molded plastics.

Competitive Landscape:

The report has also provided a comprehensive analysis of the competitive landscape in the global injection molded plastics market. Detailed profiles of all major companies have also been provided. Some of the companies covered include:

- BASF SE

- Chevron Phillips Chemical Company LLC

- Eastman Chemical Company

- Exxon Mobil Corporation

- Huntsman International LLC

- INEOS

- LyondellBasell Industries Holdings B.V.

- SABIC

- The Dow Chemical Company

Kindly note that this only represents a partial list of companies, and the complete list has been provided in the report.

Injection Molded Plastics Market News:

- In July 2025, APSX LLC launched the APSX‑LSR, a benchtop liquid silicone rubber (LSR) injection molding machine. Designed for engineers and startups, it runs on 115V AC with under 1 kW power and delivers a 6-g shot in 63 seconds. It features an integrated dual-cartridge pump and supports multiple Shore hardness LSR materials.

- In July 2025, Avery Dennison launched an RFID-enabled In-Mold Label (IML) portfolio designed to be embedded into plastic items during the injection molding process. These durable labels enhance tracking, reuse, and sustainability across industries by withstanding high heat and repeated washing. The technology supports circular systems, improving inventory visibility and reducing waste.

- In June 2025, Central Community College (CCC) in Nebraska launched a two-week injection molding bootcamp to train new workers for the plastics industry. The program uses CCC’s 4,000-ft² lab with five injection molding machines and includes hands-on training in plastics fundamentals. It supports regional workforce development and offers a 12-credit certificate in Plastics Engineering Technology.

- In January 2024, Arterex, a leading medical device company, announced a strategic acquisition of Micromold Inc., a prominent injection molded plastics provider. As per agreement terms, Micromold will allocate its 24/7 operations to Arterex’s division in Mexico.

- In June 2024, New Pendulum Corporation announced strategic acquisition of Bardot Plastics Inc., an injection molding company. This move is anticipated to expand New Pendulum’s presence in plastic manufacturing segment, with its portfolio now including injection as well as rotational molding.

Injection Molded Plastics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Raw Materials Covered | Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), High-Density Polyethylene (HDPE), Polystyrene (PS), Others |

| Applications Covered | Packaging, Consumables and Electronics, Automotive and Transportation, Building and Construction, Medical, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BASF SE, Chevron Phillips Chemical Company LLC, Eastman Chemical Company, Exxon Mobil Corporation, Huntsman International LLC, INEOS, LyondellBasell Industries Holdings B.V., SABIC, The Dow Chemical Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Injection Molded Plastics Market Report

The global injection molded plastics market was valued at USD 325.4 Billion in 2025.

We expect the global injection molded plastics market to exhibit a CAGR of 3.24% during 2026-2034.

The rising adoption of injection molded plastics across various industries, such as packaging, electronics, healthcare, etc., for manufacturing films, bags, medical devices, cellular phones, utensils, athletic apparel, etc., is primarily driving the global injection molded plastics market.

The sudden outbreak of the COVID-19 pandemic had led to the implementation of stringent lockdown regulations across several nations, resulting in the temporary closure of numerous end-use industries for injection molded plastics.

Based on the raw material, the global injection molded plastics market has been segregated into Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), High-Density Polyethylene (HDPE), Polystyrene (PS), and others. Among these, Polypropylene (PP) currently holds the largest market share.

Based on the application, the global injection molded plastics market can be bifurcated into packaging, consumables and electronics, automotive and transportation, building and construction, medical, and others. Currently, the packaging industry exhibits a clear dominance in the market.

On a regional level, the market has been classified into North America, Asia-Pacific, Europe, Latin America, and Middle East and Africa, where Asia-Pacific currently dominates the global market.

Some of the major players in the global injection molded plastics market include BASF SE, Chevron Phillips Chemical Company LLC, Eastman Chemical Company, Exxon Mobil Corporation, Huntsman International LLC, INEOS, LyondellBasell Industries Holdings B.V., SABIC, and The Dow Chemical Company.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)