Interactive Whiteboard (IWB) Market Size, Share, Trends and Forecast by Technology, Type, Projection Technique, Screen Size, End Use Sector, and Region, 2026-2034

Interactive Whiteboard (IWB) Market Size and Share:

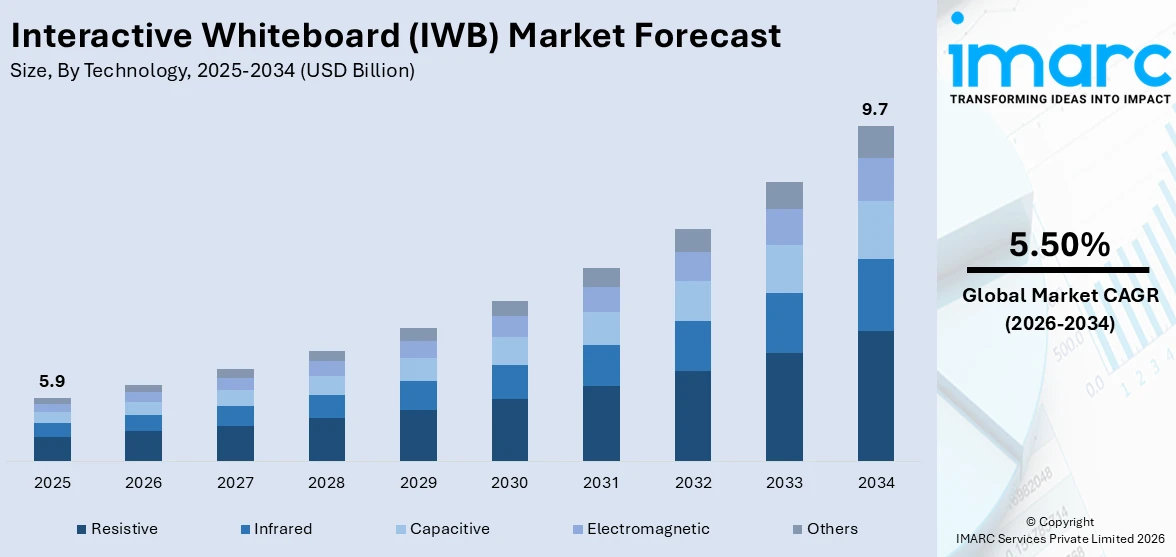

The global interactive whiteboard (IWB) market size was valued at USD 5.9 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 9.7 Billion by 2034, exhibiting a CAGR of 5.50% during 2026-2034. North America dominated the market in 2025. The growing application in educational institutes, increasing need for interactive learning, and rising adoption of smart devices represent some of the key factors contributing to the Interactive whiteboard (IWB) market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 5.9 Billion |

| Market Forecast in 2034 | USD 9.7 Billion |

| Market Growth Rate (2026-2034) | 5.50% |

The market is primarily driven by the increasing adoption of digital learning tools across schools and universities to enhance student engagement and collaboration. Government initiatives promoting smart education infrastructure, especially in developing nations, are also boosting demand. In corporate sectors, IWBs are gaining popularity for virtual meetings, brainstorming sessions, and remote collaboration. Technological advancements like multi-touch capability, cloud connectivity, and integration with software platforms have improved functionality and appeal. The growing use of e-learning platforms and blended learning models further supports Interactive whiteboard (IWB) market growth. Additionally, increased investment in EdTech startups and demand for real-time content sharing in classrooms and boardrooms are creating new opportunities. However, the market also faces competition from low-cost alternatives like tablets and touchscreen displays, which may influence future growth trajectories.

To get more information on this market Request Sample

The market is witnessing increased integration of AI-driven visual collaboration solutions with workflow management platforms. This shift supports hybrid work models, boosts meeting productivity, and simplifies task coordination across educational and enterprise environments, enhancing the value proposition of interactive whiteboards in the US market. For instance, in December 2024, Wrike announced its acquisition of Klaxoon, a provider of a visual collaboration platform. This move integrates Klaxoon’s AI-driven visual tools with Wrike’s work management solutions, enhancing workflow efficiency and collaboration.

Interactive Whiteboard (IWB) Market Trends:

Rising Adoption of Digital Collaboration Tools

As digitalization becomes a central force in driving global economic development, there is a growing shift toward tools that support intelligent communication and seamless interaction. Interactive whiteboards are gaining momentum across education, business, and training environments due to their ability to enhance engagement through real-time input, integrated media, and collaborative content sharing. With economies focusing more on digital-first strategies, institutions are increasingly investing in technologies that support flexible and connected workspaces. The appeal of interactive whiteboards lies in their role in enabling smart, integrated, and responsive environments that match the evolving expectations of digitally driven ecosystems. This shift reflects a broader move toward immersive and efficient tools for modern communication and learning needs. For example, the Global Digitalization Index 2024 reported that 70% of global economic growth over the next five years will be driven by digitalization and intelligence.

Expanding Smartphone Penetration Driving Interactive Learning Tools

Based on the Interactive whiteboard (IWB) market outlook, the rapid increase in smartphone usage worldwide has created a digitally fluent population accustomed to touch-based, interactive technologies. This behavioral shift is influencing expectations in classrooms and workspaces, where users now seek similar responsiveness and connectivity in shared environments. Interactive whiteboards, with their intuitive interfaces and multi-device integration, are becoming essential tools for digital collaboration. As personal device familiarity rises, there is a growing demand for larger, more versatile displays that support gesture-based control, real-time annotation, and seamless content sharing. This expanding digital ecosystem encourages the use of interactive solutions that mirror the functionality of everyday devices, positioning interactive whiteboards as a natural extension of the modern user’s digital experience across education, training, and enterprise settings. For instance, the Global 2025 Digital Overview Report revealed that in 2020, there were 5.9 billion smartphones in use, increasing by 240 million from the previous year. By January 2025, the global total reached 7.42 billion, with an average annual addition of 361.5 million devices over the past five years.

AI Integration Spurring Demand for Smarter Collaborative Displays

The Interactive whiteboard (IWB) market forecast indicates that widespread adoption of artificial intelligence across global enterprises is reshaping expectations for workplace technology. As more organizations embed AI into their operations, there is a growing need for interactive tools that can match the intelligence and agility of these systems. Interactive whiteboards are evolving to support this shift, offering enhanced functionality such as automated transcription, voice recognition, smart content suggestions, and real-time data visualization. These capabilities align with AI-driven workflows, enabling more efficient meetings, brainstorming sessions, and remote collaborations. The increasing use of AI is not only transforming backend systems but also influencing how teams engage and share ideas, creating strong momentum for intelligent, responsive display solutions that integrate seamlessly with AI-powered environments. For example, the latest industry report indicated that 78% of global companies currently use AI, while 82% are either using or exploring AI implementation within their organizations.

Interactive Whiteboard (IWB) Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global interactive whiteboard (IWB) market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on technology, type, projection technique, screen size, and end use sector.

Analysis by Technology:

- Infrared

- Resistive

- Capacitive

- Electromagnetic

- Others

As per the interactive whiteboard (IWB) market report, resistive stood as the largest technology in 2025 due to its cost-effectiveness and durability. Resistive touchscreens operate through pressure sensitivity, allowing input via a finger, stylus, or even a gloved hand, making them ideal for diverse educational and training environments. These whiteboards are less affected by dust or moisture, which enhances their longevity in classrooms and industrial settings. Moreover, their affordability compared to capacitive or infrared alternatives makes them attractive for institutions in developing regions with limited budgets. As schools and enterprises expand digital learning and collaboration tools, the adoption of resistive IWBs is gaining traction, especially where robust, low-maintenance solutions are prioritized. This supports their growing market demand globally.

Analysis by Type:

- Fixed

- Portable

Portable led the market in 2025, owing to rising demand for flexible, mobile, and space-saving solutions. Portable IWBs are easy to set up and dismantle, making them ideal for dynamic environments such as remote classrooms, business meetings, training workshops, and field operations. These systems often include lightweight projectors and interactive modules that can transform any flat surface into a smart board, reducing reliance on fixed infrastructure. Their affordability and versatility make them particularly attractive to small institutions, startups, and organizations with hybrid work or learning models. As education and corporate sectors prioritize mobility and cost-efficiency, the popularity of portable IWBs continues to grow, boosting overall market expansion.

Analysis by Projection Technique:

- Front Projection

- Rear Projection

Front projection IWBs, where the projector is placed in front of the board, are widely used due to their low cost and ease of installation, especially in classrooms and meeting rooms with controlled lighting. Rear projection IWBs, though more expensive, offer a superior user experience by eliminating shadow interference and glare, making them ideal for high-end corporate or design environments. Together, these segments cater to different budget and performance needs, encouraging broader market penetration. The flexibility to choose between these projection types enables customized setups across diverse educational and enterprise applications, pushing market growth forward.

Analysis by Screen Size:

- IWBs with a Screen Size Up to 69”

- IWBs with a Screen Size Ranging from 70”–90”

- IWBs with a Screen Size Above 90”

IWBs with a screen size ranging from 70”–90” led the market in 2025 because of their optimal balance between visibility and space efficiency. These mid-to-large displays provide ample surface area for collaborative work, making them ideal for classrooms, training centers, and conference rooms. They enhance visual engagement, allow multiple users to interact simultaneously, and support detailed presentations without requiring excessive wall space. Educational institutions and businesses prefer this size range as it accommodates a wide variety of content types, i.e., videos, diagrams, and annotations, while remaining manageable in terms of installation and cost. The increasing focus on interactive and immersive learning or meeting environments continues to boost demand for IWBs in this screen size segment.

Analysis by End Use Sector:

Access the comprehensive market breakdown Request Sample

- Education

- Corporate

- Government

- Others

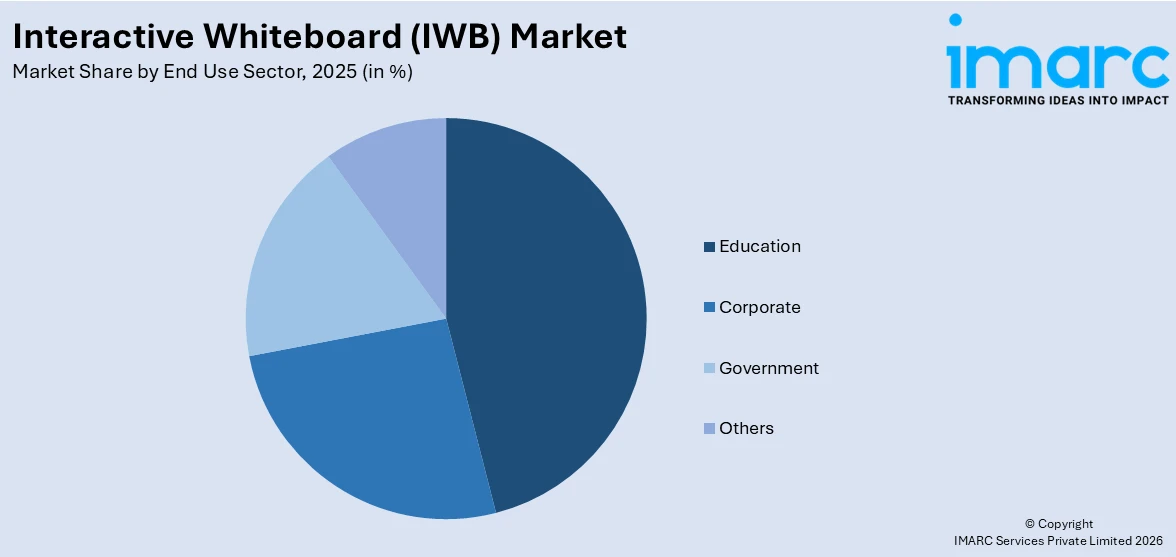

Education led the market in 2025, fueled by growing emphasis on digital learning and classroom interactivity. Schools and universities are increasingly integrating IWBs to enhance student engagement, support diverse teaching methods, and facilitate real-time collaboration. These tools allow teachers to incorporate multimedia content, conduct virtual lessons, and use interactive applications that cater to different learning styles. Government initiatives promoting smart classrooms, especially in developing countries, are accelerating adoption rates. IWBs also support hybrid and remote learning setups, making them valuable in today’s evolving education landscape. As institutions seek to modernize teaching infrastructure, the demand for IWBs in the education segment continues to rise, contributing significantly to overall market growth.

Regional Analysis:

- Asia Pacific

- Europe

- North America

- Middle East and Africa

- Latin America

In 2025, North America accounted for the largest market share as there are strong investments in educational technology, corporate digitization, and advanced learning infrastructure. Schools, colleges, and universities across the U.S. and Canada are widely adopting IWBs to support interactive and blended learning models. Additionally, the region’s corporate sector is using IWBs to enhance productivity through collaborative tools in conference rooms and remote work environments. Supportive government funding for digital classrooms and a high level of technological awareness further boost regional demand. Presence of key market players and rapid adoption of EdTech innovations position North America as a major contributor to market expansion, with steady growth across both educational and commercial applications.

Key Regional Takeaways:

United States Interactive Whiteboard (IWB) Market Analysis

The United States interactive whiteboard (IWB) market is primarily driven by the growing adoption of digital learning tools in schools to enhance engagement and improve learning outcomes. An industry report indicated that 63% of students in the United States engage in online learning daily, reflecting a strong reliance on digital education resources. Additionally, 77% of public schools have transitioned to digital education. In line with this, the increasing demand for collaborative technologies in corporate environments is pushing the market forward, as businesses aim to streamline communication and team interaction. Similarly, continual advancements in touchscreen and display technology, such as improved resolution and touch accuracy, are enhancing the market appeal. The rising integration of AI and machine learning in interactive whiteboards, augmenting functionality and enabling smarter and more intuitive systems, is fostering market expansion. Furthermore, the ongoing shift towards hybrid work models, accelerating the need for effective virtual collaboration tools, is propelling market growth. The expansion of STEM education, driving the adoption of interactive whiteboards in classrooms, is impelling the market. Moreover, increasing cost reductions in production and technological advancements are making these devices more affordable, thereby impacting the market trends.

Europe Interactive Whiteboard (IWB) Market Analysis

The Europe interactive whiteboard market is majorly propelled by the increasing adoption of e-learning in both academic and corporate sectors. In addition to this, the expansion of smart classrooms across European schools, fostering the need for advanced teaching tools, is strengthening market demand. The emerging trend of digitalization in education is driving governments to invest in interactive whiteboards for schools, which is encouraging higher product uptake. Furthermore, the rise of remote and hybrid work models, augmenting the demand for interactive technology in corporate collaboration settings, is accelerating market growth. As of October 2024, an industry analysis revealed that 41% of UK workers engaged in remote work at least part of the week, with 28% adopting a hybrid model and 13% working from home full-time. The ongoing advancements in touch sensitivity and multi-touch functionality improving user interaction are contributing to the market appeal. Moreover, the heightened demand for energy-efficient and eco-friendly technologies is increasing the adoption of sustainable interactive whiteboards in the market. Besides this, the growing need for personalized learning experiences, driving customization features in these devices, is creating lucrative market opportunities.

Asia Pacific Interactive Whiteboard (IWB) Market Analysis

The Asia Pacific market is advancing due to the rapid expansion of the education sector, with increasing investments in digital infrastructure. Similarly, the rising demand for interactive and engaging teaching tools, enhancing the integration of these boards in classrooms, is impelling the market. The ongoing shift towards technology-based learning in both schools and universities is fueling market expansion. Furthermore, the growth of corporate training and virtual collaboration tools in the region, augmenting their use in business settings, is strengthening the market demand. Additionally, government initiatives supporting digital education in countries like India and China are promoting the widespread product adoption. Moreover, the growing popularity of STEM education, fostering innovation and hands-on learning, is also providing an impetus to the market. As such, over the last few decades, the number of girls in the science stream has increased in India. The country now has over 40% female enrollment in STEM, according to UGC. Also, around 35% of students in computer science engineering courses are girls, as reported by AICTE.

Latin America Interactive Whiteboard (IWB) Market Analysis

In Latin America, the interactive whiteboard (IWB) market is progressing due to the increasing adoption of digital education solutions by schools and universities. Furthermore, favorable government initiatives promoting technological integration in education are supporting growth in the market. Similarly, the rise of e-learning platforms and distance education during the pandemic is fueling demand in the market. Apart from this, growing investments in corporate training programs, increasing the demand for interactive whiteboards to augment collaboration and productivity, are expanding the market reach. Accordingly, in 2024, Microsoft announced a 14.7 billion Reais investment in Brazil’s cloud and AI infrastructure. Through the ConectAI program, Microsoft will train 5 million people over three years in AI skills, fostering long-term economic benefits and workforce development.

Middle East and Africa Interactive Whiteboard (IWB) Market Analysis

The market in the Middle East and Africa is significantly influenced by increasing government initiatives to enhance educational infrastructure through digital tools. Similarly, rapid urbanization in the region demanding modernized educational and corporate environments, is stimulating the market accessibility. As per an industry report, more than 70% of enterprises are allocating resources to digital infrastructure, highlighting technology’s critical role in driving growth and operational efficiency. The growth of the corporate sector fostering the need for advanced collaboration technologies in meetings and training sessions, is impacting the market dynamics. Besides this, rising investments in smart city projects are driving demand for interactive technologies, enhancing public sector communication and engagement, thereby positively influencing the market.

Competitive Landscape:

The interactive whiteboard (IWB) market is currently driven by frequent product launches featuring AI tools, EDLA certification, and integration with popular platforms like Google Classroom and Microsoft Teams. Companies are also engaging in partnerships and collaborations to unify display and software capabilities for seamless classroom and business use. Research and development is focused on enhancing interactivity, security, and remote collaboration features. Some firms are expanding through acquisitions, while government initiatives continue to promote digital education infrastructure. Among these, product launches and strategic collaborations are the most common practices, reflecting rapid innovation and convergence between hardware and digital collaboration ecosystems.

The report provides a comprehensive analysis of the competitive landscape in the interactive whiteboard (IWB) market with detailed profiles of all major companies, including:

- Hitachi, Ltd.

- Panasonic Corporation

- LG Display

- Foxconn

- NetDragon Websoft

- Samsung Electronics

- NEC Display

- Ricoh

- Returnstar Interactive Technology

- Boxlight Corporation

- Cisco Systems

- Alphabet

- Microsoft Corporation

- Luidia, Inc

Latest News and Developments:

- May 2025: Optoma launched its Creative Touch 3-Series Interactive Displays with Google EDLA certification and AI-enabled tools like handwriting recognition and smart sketching. Tailored for education and corporate use, these interactive whiteboards offer wireless sharing and annotation, enhancing collaboration, safety, and workflow efficiency.

- January 2025: Samsung launched its AI-powered WAFX-P Interactive Display. Available in 65", 75", and 86", the display features tools like AI Summary, Live Transcript, and Circle to Search. Designed for interactive whiteboard use, it enhances lesson planning, collaboration, and accessibility in AI-enabled classrooms.

- January 2025: SMART Technologies unveiled the SMART Board Mini interactive podium and TAA-compliant M Pro display. Designed for education, business, and secure sectors, these interactive whiteboard solutions offer digital inking, hybrid meeting tools, and OPS PC support, enhancing engagement, security, and collaboration across instructional and enterprise environments.

- January 2025: MAXHUB announced that it would pre-launch its 92" XBoard Interactive Display for Microsoft Teams Rooms at ISE 2025. Designed as an all-in-one interactive whiteboard solution, it integrates a 5K display, audio, camera, and computing for seamless collaboration, supporting both local and remote meetings with advanced Intel processors and Microsoft Teams certification.

- January 2025: i3-Technologies and CTOUCH launched i3CONNECT, a unified brand delivering interactive whiteboards, collaboration tools, and accessories for education and business. i3CONNECT focuses on sustainable, future-ready solutions that enhance engagement and creativity in classrooms and meeting rooms, blending both companies' innovation and expertise under one collaborative technology platform.

- August 2024: Optoma launched the IFP53 interactive touch panel with Google EDLA certification, enhancing educational tools. The updated Optoma Management Cloud (OMS) enables centralized device control, remote diagnostics, and improved workflows for IT admins. The IFP53 also supports advanced AI, Google Classroom integration, and multi-user collaboration, launching soon in Taiwan.

- July 2024: BenQ India launched the Google EDLA-certified BenQ Board RE04 Series, available in 65", 75", and 86" models. Featuring 4K UHD resolution, Google services integration, and advanced collaboration tools, the series supports education and corporate environments.

Interactive Whiteboard (IWB) Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Infrared, Resistive, Capacitive, Electromagnetic, Others |

| Types Covered | Fixed, Portable |

| Projection Techniques Covered | Front Projection and Rear Projection |

| Screen Sizes Covered | IWBs with a Screen Size Up to 69”, IWBs with a Screen Size Ranging from 70”–90”, IWBs with a Screen Size Above 90” |

| End Use Sectors Covered | Education, Corporate, Government, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Hitachi, Ltd., Panasonic Corporation, LG Display, Foxconn, NetDragon Websoft, Samsung Electronics, NEC Display, Ricoh, Returnstar Interactive Technology, Boxlight Corporation, Cisco Systems, Alphabet, Microsoft Corporation, Luidia, Inc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the interactive whiteboard (IWB) market from 2020-2034.

- The interactive whiteboard (IWB) market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the interactive whiteboard (IWB) industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Interactive Whiteboard (IWB) Market Report

The interactive whiteboard (IWB) market was valued at USD 5.9 Billion in 2025.

The interactive whiteboard (IWB) market is projected to exhibit a CAGR of 5.50% during 2026-2034, reaching a value of USD 9.7 Billion by 2034.

The interactive whiteboard (IWB) market is driven by rising adoption of digital learning tools, increasing demand for interactive classrooms, government initiatives in smart education, corporate training needs, and technological advancements like multi-touch and cloud integration. Growing e-learning platforms and remote collaboration also support market expansion across education and enterprise sectors.

North America dominated the interactive whiteboard (IWB) market in 2025, driven by strong EdTech adoption, high digital classroom penetration, government funding for smart education, and widespread use in corporate training.

Some of the major players in the interactive whiteboard (IWB) market include Hitachi, Ltd., Panasonic Corporation, LG Display, Foxconn, NetDragon Websoft, Samsung Electronics, NEC Display, Ricoh, Returnstar Interactive Technology, Boxlight Corporation, Cisco Systems, Alphabet, Microsoft Corporation, Luidia, Inc, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)