Ion Exchange Membrane Market Size, Share, Trends and Forecast by Charge, Material, Structure, Application, and Region, 2026-2034

Ion Exchange Membrane Market Size and Trends:

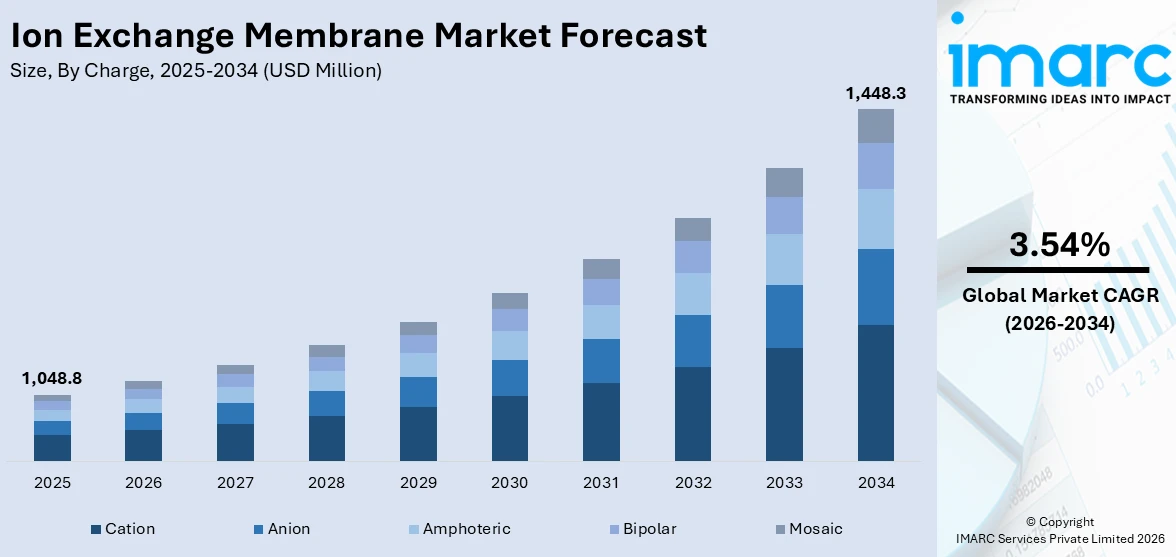

The global ion exchange membrane market size was valued at USD 1,048.8 Million in 2025. Looking forward, IMARC Group estimates the market to reach USD 1,448.3 Million by 2034, exhibiting a CAGR of 3.54% during 2026-2034. Asia-Pacific currently dominates the market, holding a significant market share of over 42.2% in 2025. The growing wastewater treatment projects, increasing use in the healthcare and energy storage sectors, and rising advancements in the chemical industry represent some of the key factors driving the market toward growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1,048.8 Million |

|

Market Forecast in 2034

|

USD 1,448.3 Million |

| Market Growth Rate (2026-2034) | 3.54% |

The ion exchange membrane market is driven by several key factors including the expansion of wastewater treatment projects that require advanced purification technologies. An increased demand in the healthcare sector for medical devices and pharmaceutical applications also propels market growth. Additionally, the rising energy storage needs particularly in fuel cells and batteries significantly contribute to the market's expansion. Advancements in the chemical industry such as enhanced separation and catalysis processes along with stringent environmental regulations and a global push for sustainable and renewable energy solutions further drive the adoption and development of ion exchange membranes. Furthermore, continuous technological innovations in membrane materials and manufacturing processes improve performance, durability and cost-effectiveness making ion exchange membranes more versatile and attractive for a wide range of applications. For instance, in December 2023, Asahi Kasei Corp announced an investment in Canadian startup Ionomr Innovations which produces advanced anion exchange membranes (AEM) for green hydrogen production. This investment supports scalable and cost-effective electrolysis using renewable energy positioning Asahi Kasei as a key player in the hydrogen sector as nations strive for zero-emission goals.

To get more information on this market Request Sample

The US ion exchange membrane market is propelled by several key drivers including robust wastewater treatment initiatives driven by stringent environmental regulations and the need for sustainable water management. The expanding healthcare sector with increased demand for medical devices and pharmaceutical applications also significantly boosts market growth. Additionally, the surge in energy storage solutions particularly fuel cells and advanced batteries supporting renewable energy projects plays a crucial role. For instance, in August 2024, the U.S. Department of Energy opened the 93000 square foot Grid Storage Launchpad at the Pacific Northwest National Lab to enhance battery research. This facility will enable testing of advanced energy storage technologies supporting grid resilience and security while fostering collaboration to drive innovation in clean energy solutions. Advancements in the chemical industry such as enhanced separation and catalysis processes further drive adoption. Government support for clean energy and sustainability alongside technological innovations improving membrane efficiency and durability are pivotal in expanding the US ion exchange membrane market.

Ion Exchange Membrane Market Trends:

Technological Advancements

The market is experiencing significant technological advancements aimed at enhancing membrane performance and longevity. The development of more durable, selective, and high-performance membranes focuses on improving resistance to chemical degradation and physical wear ensuring longer operational lifespans and reducing maintenance costs. For instance, in March 2024, Ionomr Innovations Inc launched an iridium free Catalyst Coated Membrane (CCM) utilizing its Aemion® Anion Exchange Membranes (AEMs) for low-cost green hydrogen production. This innovative product eliminates the use of iridium and harmful perfluorinated substances found in traditional materials. Enhanced selectivity allows for more efficient ion separation increasing the overall efficiency of processes like water purification and energy storage. Innovations in membrane materials such as the use of nanocomposites and hybrid membranes are at the forefront of these advancements.

Increased Adoption in Renewable Energy

The market is witnessing heightened adoption in the renewable energy sector driven by the expanding use of ion exchange membranes in fuel cells and electrolyzers for green hydrogen production. These membranes enhance the efficiency and scalability of electrolysis processes making green hydrogen a viable and sustainable energy source. For instance, in September 2024, Hygreen Energy launched its first Anion Exchange Membrane (AEM) electrolyzer system expanding its hydrogen production offerings. The system boasts a customizable 100 Nm3/h output and a broad operating range. Additionally, ion exchange membranes are being integrated with solar and wind energy systems to improve energy storage solutions. By facilitating efficient ion transport these membranes enable better storage and conversion of renewable energy supporting grid stability and the transition to a low-carbon economy. This integration not only boosts renewable energy adoption but also accelerates the development of sustainable infrastructure worldwide.

Sustainability and Environmental Focus

There is a significant shift towards using ecofriendly membrane materials and adopting sustainable manufacturing processes in the ion exchange membrane market. Manufacturers are increasingly selecting biodegradable or less toxic materials to minimize environmental impact. Additionally, green manufacturing techniques such as reducing energy consumption and utilizing renewable resources are being implemented to lower the carbon footprint. For instance, in April 2024, LANXESS introduced ion exchange resins from its Lewatit UltraPure range for water treatment in PEM electrolysis enabling efficient hydrogen production from renewable energy. The technology requires continuous purification of process water supporting a sustainable low-emission hydrogen economy essential for future energy transitions. Moreover, there is a strong emphasis on reducing membrane waste through innovative recycling methods and designing membranes for easier disassembly and reuse. Improving recyclability not only conserves resources but also aligns with circular economy principles ensuring that membrane materials can be efficiently recovered and repurposed thereby enhancing overall sustainability.

Ion Exchange Membrane Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global ion exchange membrane market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on charge, material, structure, application and region.

Analysis by Charge:

- Cation

- Anion

- Amphoteric

- Bipolar

- Mosaic

Cation stands as the largest component in 2025, holding around 44.1% of the market. According to the report, cation represented the largest segment. This dominance is primarily driven by the extensive use of cation exchange membranes in water purification and softening processes effectively removing harmful positively charged ions such as calcium and magnesium. Additionally, cation membranes are pivotal in various industrial applications including chemical manufacturing, metal finishing and electrochemical systems like fuel cells. The rising demand for high-purity water in the pharmaceutical and electronics sectors further propels the growth of this segment. Advances in membrane technology such as enhanced ion selectivity and increased durability have improved performance and broadened application scopes thereby reinforcing the cation segment’s leading position in the global market.

Analysis by Material:

- Hydrocarbon Membrane

- Perfluorocarbon Membrane

- Inorganic Membrane

- Composite Membrane

- Partially Halogenated Membrane

Inorganic membrane leads the market with around 31.7% of market share in 2025. According to the report inorganic membrane accounted for the largest market share as it offers stability to high temperatures and to wetting-drying cycles over organic membranes. Moreover, the rising adoption of inorganic membrane to enhance conductivity of the membranes and prevent their dehydration under high temperature is impelling the market growth. Additionally, inorganic membranes provide superior chemical resistance making them ideal for harsh industrial environments such as chemical processing and energy production. Their extended lifespan and lower maintenance requirements further boost their preference over organic alternatives. Advances in material science have led to the development of more efficient and cost-effective inorganic membranes expanding their applications. Furthermore, the increasing emphasis on sustainable and energy-efficient processes across various industries is driving the demand for high-performance inorganic membranes thereby significantly contributing to the overall market expansion.

Analysis by Structure:

- Heterogeneous Membrane

- Homogenous Membrane

Heterogenous membrane leads the market with around 64.7% of market share in 2025. According to the report, heterogenous membrane accounted for the largest market share. This leadership is driven by the membrane’s complex structure which offers enhanced mechanical strength and superior ion selectivity compared to homogenous membranes. Heterogeneous membranes are highly favored in applications requiring robust performance under varying operational conditions such as wastewater treatment, industrial separation processes and advanced electrochemical systems. Their ability to efficiently separate a wide range of ions makes them indispensable in sectors like chemical manufacturing, pharmaceuticals and energy storage. Additionally, ongoing advancements in fabrication techniques have improved the durability and efficiency of heterogeneous membranes expanding their applicability and reinforcing their dominant market position. The flexibility and high performance of heterogeneous membranes continue to attract significant investment and adoption across diverse industries ensuring sustained growth and leadership in the global market.

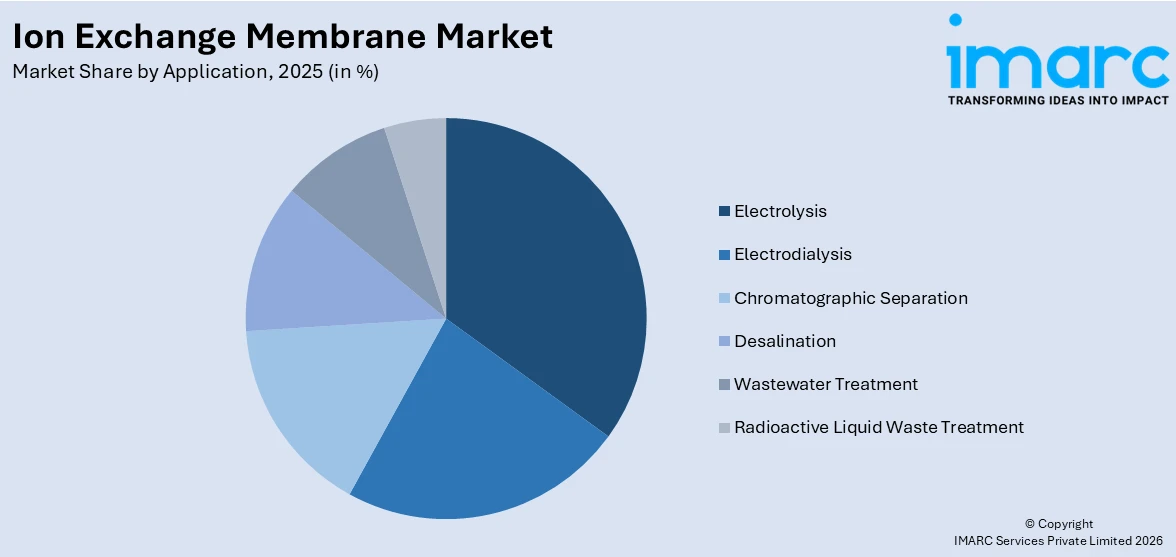

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Electrodialysis

- Electrolysis

- Chromatographic Separation

- Desalination

- Wastewater Treatment

- Radioactive Liquid Waste Treatment

Electrolysis leads the market with around 35.2% of market share in 2025. According to the report, electrolysis accounts for the largest share of the market driven by its crucial role in chemical processing, chloralkali and hydrogen production and metal extraction. The increasing demand for chlorine, caustic soda and other chlorine- and sodium-derived products further propels this dominance. Advancements in ion exchange membrane technologies tailored for electrolysis have significantly enhanced efficiency, durability and scalability making them indispensable for large-scale hydrogen production. Additionally, the integration of renewable energy sources with electrolysis processes supports sustainable and low-carbon industrial practices. Increased investments in research and development are fostering innovative membrane solutions, solidifying electrolysis as the leading segment in the market.

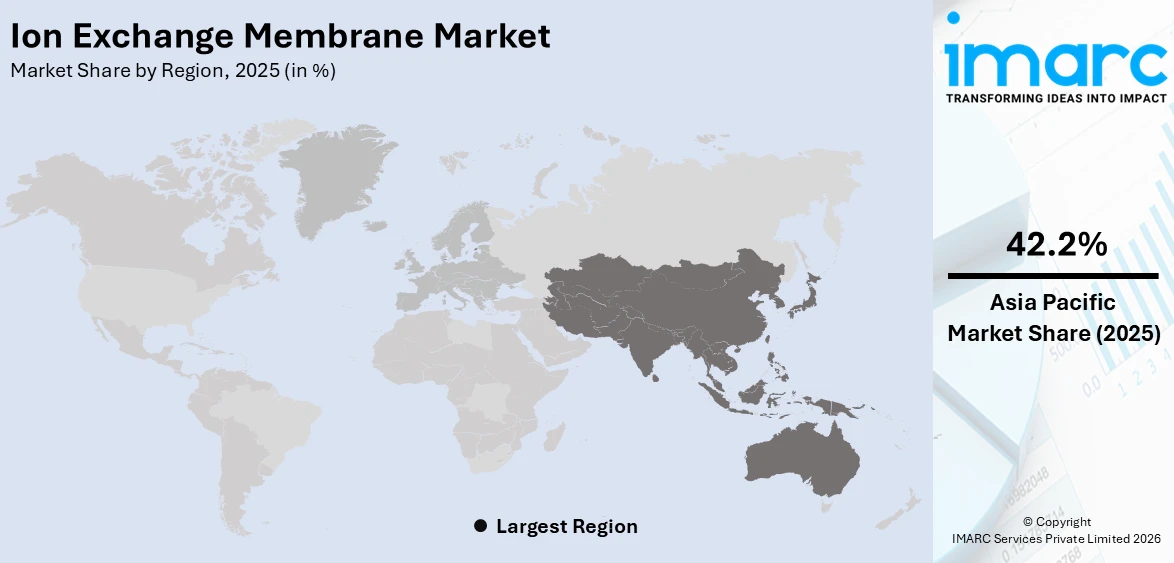

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, Asia-Pacific accounted for the largest market share of over 42.2%. According to the report, Asia Pacific was the largest market for ion exchange membrane. The Asia-Pacific ion exchange membrane market is experiencing growth driven by the region's increasing focus on clean energy solutions such as hydrogen production through water electrolysis. Countries like China, Japan and South Korea are actively investing in renewable energy projects and scaling up green hydrogen production capacities fostering the demand for ion exchange membranes. Governments and private sectors are implementing policies and funding research to improve water treatment facilities particularly in regions with water scarcity and industrial pollution challenges. Industries are continuously adopting ion exchange membranes for wastewater treatment to meet stricter environmental regulations. Companies are innovating in membrane technologies to enhance ion selectivity and durability particularly in desalination and energy storage applications. The semiconductor and electronics industries in countries like Taiwan and South Korea are expanding their manufacturing capacities driving the need for ultrapure water systems reliant on ion exchange membranes. According to the International Trade Administration, semiconductors (chips) are South Korea’s largest export item accounting for 18.9 percent of the country’s total exports in 2022. Industry players are entering collaborations with research institutions and launching localized production units to cater to the specific requirements of the Asia-Pacific market ensuring faster adoption and sustained growth.

Key Regional Takeaways:

North America Ion Exchange Membrane Market Analysis

The North America ion exchange membrane market is experiencing robust growth driven by the region’s emphasis on advanced water treatment and renewable energy initiatives. In the United States, increasing adoption of desalination technologies addresses water scarcity in drought-prone areas while stringent environmental regulations compel industries to implement sophisticated wastewater treatment solutions. Canada is expanding its infrastructure for clean water and investing in hydrogen fuel cells to support its green energy transition. Mexico is enhancing its water purification systems and leveraging ion exchange membranes in its burgeoning petrochemical and manufacturing sectors. Additionally, federal initiatives like the Inflation Reduction Act in the US promote cleaner energy solutions boosting demand for ion exchange membranes in hydrogen production and energy storage applications. Continuous technological innovations and significant government support across North America are further propelling the market ensuring sustainable and efficient applications across various industries.

United States Ion Exchange Membrane Market Analysis

In 2025, US accounted for a share of 81.60% of the North America market. The ion exchange membrane market in the United States is currently being driven by the increasing adoption of advanced desalination technologies to address growing water scarcity concerns particularly in drought-prone states like California and Arizona. Industrial sectors are actively implementing ion exchange membranes in water treatment plants to comply with stringent environmental regulations for wastewater discharge. According to the Cybersecurity and Infrastructure Security Agency (CISA), there are more than 16,000 wastewater treatment systems across the United States. Additionally, the energy industry is leveraging ion exchange membranes in hydrogen fuel cells which are gaining traction due to the accelerating push for cleaner energy solutions under federal initiatives like the Inflation Reduction Act. Manufacturers are continuously innovating membrane technology to enhance ion selectivity and durability meeting the rising demand for efficient and sustainable solutions in electrochemical applications. The food and beverage industry is also deploying these membranes for applications like demineralization and concentration of juices aligning with the sector's emphasis on sustainability and waste reduction. Meanwhile, academic and private research institutions are expanding their investments in the development of ion exchange membranes for emerging uses, such as flow batteries and biopharma applications. Furthermore, the government is actively supporting the market through research grants and tax incentives to promote the adoption of advanced membrane technologies in renewable energy and water conservation projects.

Europe Ion Exchange Membrane Market Analysis

The Europe ion exchange membrane market is currently witnessing robust growth driven by multiple specific factors. Industries are increasingly adopting ion exchange membranes for water treatment as they continue to face stringent EU regulations on wastewater management and water quality standards. The adoption of renewable energy is surging with applications like hydrogen production and fuel cells expanding rapidly where ion exchange membranes are crucial for enhancing efficiency and reducing energy losses. According to the European Environment Agency, EU has achieved its 20% renewable energy target in 2020. Manufacturers are investing heavily in research to develop advanced membranes with higher durability and selectivity, catering to the growing demand for energy-efficient desalination and industrial separation processes. Additionally, the pharmaceutical and biotechnology sectors are actively utilizing ion exchange membranes for high-purity separation in drug formulation and laboratory diagnostics. Governments across Europe are deploying policies promoting sustainable industrial practices, which is accelerating the uptake of these membranes in chemical, food, and beverage processing. Emerging applications in electrochemical energy storage, such as redox flow batteries, are also driving innovation and market adoption. Meanwhile, partnerships between technology providers and end-users are facilitating customized solutions, addressing industry-specific challenges and further boosting demand for ion exchange membranes in Europe. These factors collectively underscore the dynamic growth trajectory of the market in the region.

Latin America Ion Exchange Membrane Market Analysis

The Latin America ion exchange membrane market is currently being driven by several region-specific factors that reflect the evolving industrial landscape and environmental priorities. Increasing investments in desalination plants across countries like Mexico and Chile are boosting the demand for ion exchange membranes, as these membranes are playing a crucial role in addressing water scarcity issues. Governments are implementing stricter environmental regulations to control industrial effluents, prompting industries to adopt advanced wastewater treatment technologies, which include ion exchange membranes. Additionally, the renewable energy sector in Latin America is expanding rapidly, with proton exchange membranes being integrated into fuel cell systems for clean energy storage and generation, particularly in Brazil's energy transition initiatives. According to the International Energy Agency, access to electricity across Brazil is almost universal and renewables meet almost 45% of primary energy demand, making Brazil’s energy sector one of the least carbon-intensive in the world. Chemical and petrochemical industries in the region are actively upgrading their separation processes to enhance operational efficiency, relying on ion exchange membranes for superior ion separation and cost savings. Meanwhile, the food and beverage sector is using these membranes to improve the quality of processed products, meeting growing consumer demand for high-purity ingredients. Researchers and companies are also collaborating on new applications, such as lithium extraction from brines in Bolivia and Argentina, leveraging ion exchange membranes to streamline production processes and support the region’s booming lithium battery industry.

Middle East and Africa Ion Exchange Membrane Market Analysis

The Ion Exchange Membrane market in the Middle East and Africa is currently being driven by the rising investments in water desalination projects, as regional governments are prioritizing solutions to address acute water scarcity issues. Countries like Saudi Arabia and the UAE are deploying advanced technologies for seawater desalination, where ion exchange membranes are gaining prominence due to their efficiency and cost-effectiveness. Simultaneously, the growing adoption of renewable energy sources is supporting the development of hydrogen production plants, particularly in nations like South Africa and Oman, where green hydrogen projects are accelerating the demand for ion exchange membranes used in electrolysis processes. For instance, in 2024, Oman aims for renewable energy to constitute 39% of its total energy supply by 2040 and targets zero carbon neutrality by 2050. Industrial sectors, including petrochemicals and mining, are increasingly focusing on wastewater treatment and resource recovery, leveraging ion exchange membranes for enhanced performance and sustainability. In addition, regulatory frameworks and initiatives promoting environmental conservation are compelling industries to adopt cleaner technologies, fuelling the market further. The region is also witnessing a surge in public-private partnerships to develop membrane-based water treatment and energy projects, ensuring consistent growth in demand for these membranes. Furthermore, technological advancements and localization of manufacturing in countries like Egypt are enhancing market accessibility and reducing dependency on imports, strengthening the overall market momentum.

Competitive Landscape:

The ion exchange membrane market is highly competitive, characterized by numerous established players and emerging innovators striving to enhance product performance and reduce costs. Companies focus on technological advancements, such as developing more durable and selective membranes, to differentiate themselves and capture greater market share. Strategic initiatives like mergers, acquisitions, and partnerships are common, enabling firms to expand their capabilities and geographic reach. For instance, in July 2024, 3M invested in Ohmium International, a leader in green hydrogen production. This partnership focuses on advanced electrolyzer systems, including Proton Exchange Membrane technology, to enhance efficiency. The collaboration supports 3M's commitment to a low-carbon economy and advancing climate technologies alongside renewable energy sources. Additionally, competitive pricing and efficient supply chain management are critical factors for maintaining profitability and attracting customers. Continuous investment in research and development drives innovation, while the ability to quickly adapt to regulatory changes and market demands serves as a key differentiator in this dynamic landscape.

The report has also analysed the competitive landscape of the market with some of the key players being:

- 3M Company

- AGC ENGINEERING Co. Ltd

- Asahi Kasei Corporation

- Dioxide Materials

- Dow Inc.

- DuPont de Nemours Inc.

- Fujifilm Holdings Corporation

- General Electric Company

- Lanxess AG

- Merck KGaA

- ResinTech Inc.

- Saltworks Technologies Inc.

- Toray Industries Inc.

Latest News and Developments:

- May 2019: CAPLINQ Europe BV announced that it will become Ionomr Innovations’ “European Market Partner” to further promote its Aemion™ and Pemion™ advanced ion-exchange membranes and polymers to its customers in Europe.

- February 2021: AFC Energy, a provider of hydrogen power generation technologies, announced the launch of its Anion Exchange Membrane (AEM) fuel cell test facility hosted at the company’s Surrey headquarters in the United Kingdom.

- April 2021: Asahi Kasei’s Specialty Solutions SBU launched a Customer Success Department in the Ion Exchange Membrane Business Unit of its Membrane Solutions Division in order to advance the new services in alignment with R2 for the provision of total solutions to the chlor-alkali industry.

- September 2024: Industrie De Nora, an Italian multinational company listed on the Euronext Milan, specialized in sustainable electrochemical technologies and in the emerging green hydrogen industry, is launching a regional version of its CECHLO-MS 200 ion exchange membrane electrolysis (IEM) technology for the North American market.

Ion Exchange Membrane Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charges Covered | Cation, Anion, Amphoteric, Bipolar, Mosaic |

| Materials Covered | Hydrocarbon Membrane, Perfluorocarbon Membrane, Inorganic Membrane, Composite Membrane, Partially Halogenated Membrane |

| Structures Covered | Heterogeneous Membrane, Homogenous Membrane |

| Applications Covered | Electrodialysis, Electrolysis, Chromatographic Separation, Desalination, Wastewater Treatment, Radioactive Liquid Waste Treatment |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3M Company, AGC ENGINEERING Co. Ltd, Asahi Kasei Corporation, Dioxide Materials, Dow Inc., DuPont de Nemours Inc., Fujifilm Holdings Corporation, General Electric Company, Lanxess AG, Merck KGaA, ResinTech Inc., Saltworks Technologies Inc., Toray Industries Inc. etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the ion exchange membrane market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global ion exchange membrane market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the ion exchange membrane industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Ion Exchange Membrane Market Report

An ion exchange membrane is a hydrophilic polymer film that has ionic groups covalently bonded to its structure. This membrane selectively transports ions of opposite charges and can be categorized into three types: cation exchange membranes, anion exchange membranes, and combined cation/anion exchange membranes, depending on the type of fixed ionic groups present.

The ion exchange membrane market was valued at USD 1,048.8 Million in 2025.

IMARC estimates the global ion exchange membrane market to exhibit a CAGR of 3.54% during 2026-2034.

The market is driven by expanding wastewater treatment projects, increased demand in the healthcare sector, rising energy storage needs in fuel cells and batteries, advancements in the chemical industry, stringent environmental regulations, and a global push for sustainable and renewable energy solutions.

In 2025, cation represented the largest segment by charge, driven by driven by extensive use in water purification and industrial applications.

Inorganic Membrane leads the market by material owing to their superior chemical resistance and stability under harsh conditions.

The Heterogeneous Membrane is the leading segment by structure, driven by its enhanced mechanical strength and superior ion selectivity.

The Electrolysis is the leading segment by application, driven by its crucial role in chemical processing, hydrogen production, and metal extraction.

On a regional level, the market has been classified into North America, Asia Pacific, Europe, Latin America, and Middle East and Africa, wherein Asia Pacific currently dominates the global market.

Some of the major players in the global ion exchange membrane market include 3M Company, AGC ENGINEERING Co. Ltd, Asahi Kasei Corporation, Dioxide Materials, Dow Inc., DuPont de Nemours Inc., Fujifilm Holdings Corporation, General Electric Company, Lanxess AG, Merck KGaA, ResinTech Inc., Saltworks Technologies Inc. and Toray Industries Inc. etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade