Italy Drones Market Size, Share, Trends and Forecast by Type, Component, Payload, Point of Sale, End-Use Industry, and Region, 2026-2034

Italy Drones Market Summary:

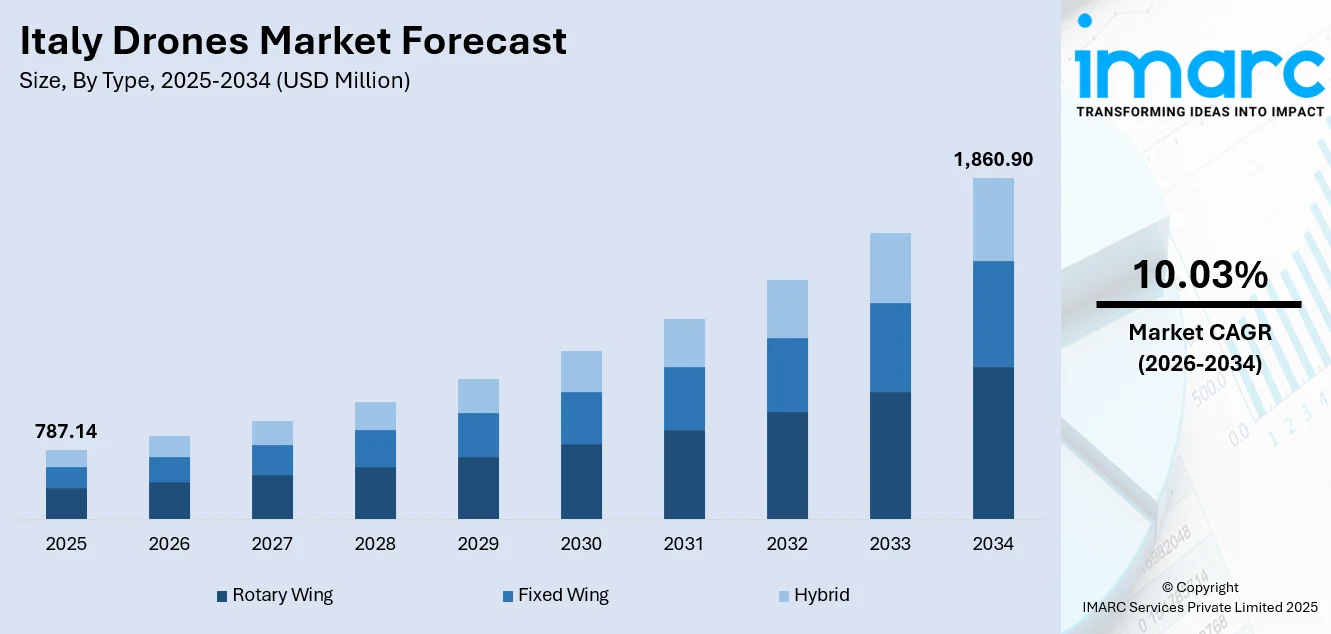

The Italy drones market size was valued at USD 787.14 Million in 2025 and is projected to reach USD 1,860.90 Million by 2034, growing at a compound annual growth rate of 10.03% from 2026-2034.

The market is witnessing growth, as defense modernization efforts, agricultural digitalization, and infrastructure oversight needs align to promote adoption across various sectors. Collaborative alliances between local aerospace firms and global drone producers are enhancing the nation's standing in the European unmanned aerial systems arena. Increasing use in precision agriculture, energy infrastructure inspection, and public safety operations is generating significant growth opportunities. The alignment of regulatory standards within European aviation structures, technological progress in autonomous flying technologies, and rising public funding for defense initiatives are transforming Italy's drone landscape.

Key Takeaways and Insights:

- By Type: Rotary wing dominates the market with a share of 51.02% in 2025, due to its superior hovering capabilities, operational versatility for aerial photography, inspection tasks, and agricultural monitoring applications across Italy's diverse terrain.

- By Component: Hardware leads the market with a share of 54.01% in 2025, reflecting strong demand for advanced airframes, propulsion systems, sensors, and communication equipment essential for commercial and defense drone platforms.

- By Payload: 25-170 kilograms represent the largest segment with a market share of 45.04% in 2025, owing to its suitability for medium-range surveillance, agricultural spraying operations, and cargo delivery missions.

- By Point of Sale: Original equipment manufacturers (OEM) dominate the market with a share of 70.05% in 2025, as defense procurement and commercial fleet acquisitions favor direct OEM relationships for quality assurance and technical support.

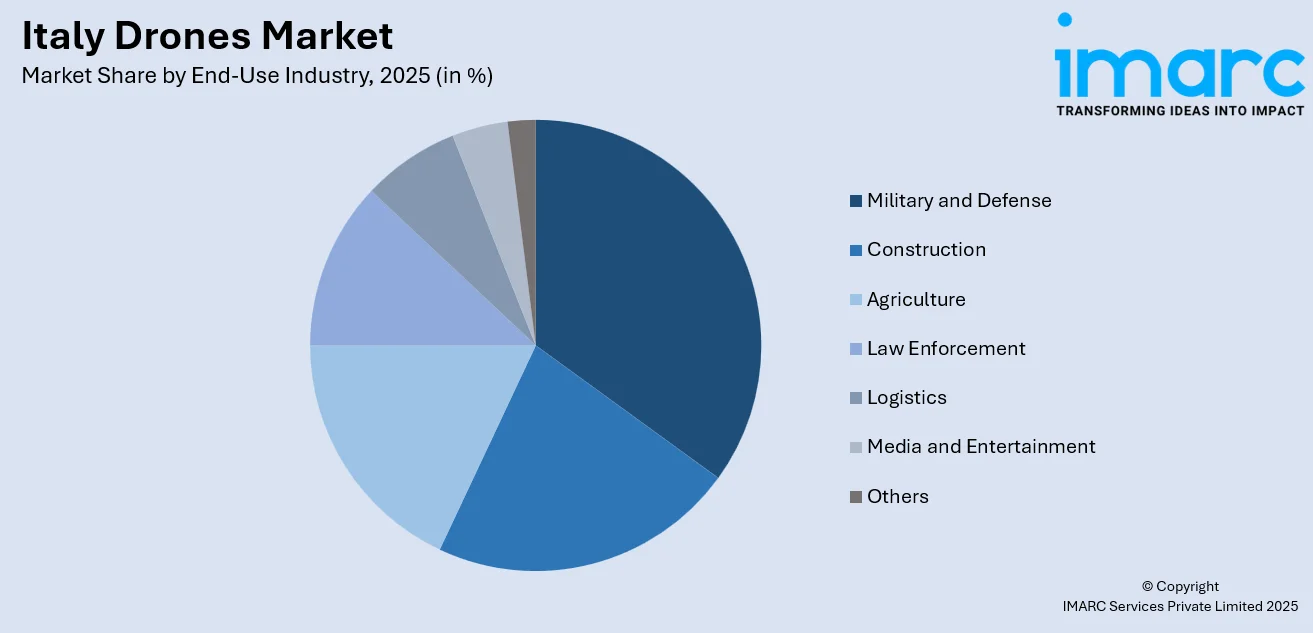

- By End-Use Industry: Military and defense represent the largest segment with a market share of 31.03% in 2025, driven by Italy's defense modernization programs and European security imperatives requiring advanced unmanned aerial capabilities.

- Key Players: The Italy drones market exhibits moderate competitive intensity, characterized by strategic partnerships between domestic aerospace leaders and international drone manufacturers competing across defense, commercial, and agricultural segments.

To get more information on this market Request Sample

The drone market in Italy is experiencing growth driven by increasing usage in logistics, agriculture, defense, and advanced technology industries. The logistics industry is supporting the demand as companies explore drone-based last-mile delivery systems to improve distribution efficiency alongside the growing e-commerce activity. Advancements in battery efficiency, sensor integration, artificial intelligence (AI), and autonomous navigation are allowing drones to undertake more intricate commercial operations with less human participation. Defense modernization initiatives are further boosting the demand via investments in surveillance, reconnaissance, and the incorporation of naval drones. This was emphasized in 2025 when Italy entered into a $46.6 million agreement with AeroVironment to purchase Jump 20 fixed-wing drones, substituting its Shadow UAV fleet via a five-year contract that included engineering, maintenance, and support. Jump 20 drones further improved Italy's reconnaissance and surveillance operations with more than 13 hours of endurance and the ability to take off and land without a runway.

Italy Drones Market Trends:

Increasing Adoption in Logistics and Delivery Services

The logistics sector is becoming a major factor influencing the Italy drone market as businesses increasingly evaluate aerial delivery solutions to improve distribution efficiency. Drones offer strong potential for last-mile operations, particularly in remote or difficult-to-access areas, helping reduce transit times and operational costs. This demand is reinforced by the growth of Italy’s online retail environment, as IMARC Group reported that the country’s e-commerce market size reached USD 673.0 Million in 2025, encouraging investment in faster delivery infrastructure. Ongoing regulatory developments and advances in payload capacity and flight reliability are further supporting commercial adoption of drone-based logistics services nationwide.

Advancements in Drone Technology and Autonomous Capabilities

Advancements in drone technology are strengthening the Italy drone market growth by expanding operational performance and commercial viability. Improvements in battery efficiency, flight stability, sensor integration, and autonomous navigation are enabling drones to perform complex tasks with greater reliability and minimal human intervention. This progress is supported by industry adoption milestones, as in 2025 Amazon selected Italy as the first European country to host a Prime Air drone delivery hub in San Giovanni Teatino, Abruzzo, enabling 60-minute parcel deliveries using autonomous electric drones. Such developments highlight how AI-driven systems and sophisticated platforms are accelerating drone integration across diverse Italian sectors.

Rise of Precision Agriculture and Smart Farming Practices

The adoption of drones in the Italy agricultural sector is supporting the market growth as farmers increasingly pursue technology-based solutions for efficient crop management. Drones enable aerial monitoring of soil conditions, irrigation performance, pest activity, and crop health through multispectral imaging, improving productivity while reducing resource wastage. This shift toward precision farming is reflected in commercial initiatives, as in 2025 Envirotech Vehicles signed an LOI with Italy-based Studio di Agronomia Baffetti to deploy heavy-lift agricultural drones in Tuscany from Spring 2026 for vineyard and olive grove spraying. The partners also aimed to establish Italy’s first certified commercial drone-spraying authority under EU aviation and environmental rules.

Market Outlook 2026-2034:

The Italy drones market shows significant growth potential over the forecast period, driven by defense modernization programs, agricultural digitalization efforts, and the expanding range of commercial applications. The market generated a revenue of USD 787.14 Million in 2025 and is projected to reach a revenue of USD 1,860.90 Million by 2034, growing at a compound annual growth rate of 10.03% from 2026-2034. This growth is fueled by increasing adoption across industries, including defense, agriculture, and logistics, as drones become essential tools for innovation and efficiency.

Italy Drones Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Rotary Wing |

51.02% |

|

Component |

Hardware |

54.01% |

|

Payload |

25-170 Kilograms |

45.04% |

|

Point of Sale |

Original Equipment Manufacturers (OEM) |

70.05% |

|

End-Use Industry |

Military and Defense |

31.03% |

Type Insights:

- Fixed Wing

- Rotary Wing

- Hybrid

Rotary wing dominates with a market share of 51.02% of the total Italy drones market in 2025.

Rotary wing holds the biggest market share because of its adaptability and capacity to function in various environments. This section is perfect for activities like aerial photography, surveying, agriculture, and infrastructure inspections, where both stability and maneuverability are essential. The capacity to remain stationary and ascend or descend vertically provides rotary wing drone a notable edge over fixed-wing types, particularly in cities or environments with restricted space. This adaptability makes it the favored option for both industrial and commercial uses throughout Italy.

Additionally, the growing focus on industries like agriculture, logistics, and public safety further drives the demand for rotary wing drone. In agriculture, this drone is increasingly used for crop monitoring and precision farming, providing real-time data for better decision-making. Similarly, in the logistics and emergency response sectors, its ability to quickly reach hard-to-access areas is invaluable. As regulations become more drone-friendly and the technology continues to advance, the adoption of rotary wing drone in Italy’s commercial and industrial sectors is growing significantly.

Component Insights:

- Hardware

- Software

- Accessories

Hardware leads with a market share of 54.01% of the total Italy drones market in 2025.

Hardware represents the largest segment, driven by the increasing demand for high-performance and reliable drone systems. The core hardware components, including motors, batteries, sensors, cameras, and flight controllers, are crucial for ensuring optimal functionality across various applications, such as aerial photography, surveying, and agriculture. As industries adopt drones for an increasing range of tasks, there is a higher need for more sophisticated hardware. High-quality components enable drones to perform specialized tasks with greater precision, leading to enhanced demand in both commercial and industrial sectors across Italy.

Furthermore, advancements in drone hardware technology are significantly improving overall performance, efficiency, and durability. For instance, lighter and more efficient batteries extend flight times, while advanced sensors and cameras enhance data collection capabilities for applications like environmental monitoring and infrastructure inspections. This growing need for cutting-edge hardware is resulting in manufacturers focusing on developing high-quality components that cater to both civilian and commercial drone users. As Italy continues to invest in drone adoption across multiple industries, hardware components remains central to the market growth and innovation.

Payload Insights:

- <25 Kilograms

- 25-170 Kilograms

- >170 Kilograms

25-170 kilograms exhibit a clear dominance with a 45.04% share of the total Italy drones market in 2025.

The 25-170 kilograms leads the market attribute to their versatility and ability to support a wide range of commercial applications. Drones within this weight range are typically used for industrial purposes, such as agricultural spraying, infrastructure inspections, and logistics, where larger payload capacities are necessary. These drones can carry more powerful cameras, sensors, or cargo, enabling them to perform demanding tasks more efficiently. The growing use of drones in sectors like construction, agriculture, and energy further drives the demand for these mid-weight payload drones, offering a balance of power and maneuverability.

In addition, the 25–170 kilograms offer a strong balance of cost efficiency and performance, making them a preferred choice for many companies. They support a wide range of commercial and industrial applications without the high operating costs linked to larger, heavier drones. In Italy, this capacity is well suited for transporting goods across dense urban areas as well as remote regions, helping sectors like last-mile delivery, agriculture, and logistics improve efficiency and expand service reach.

Point of Sale Insights:

- Original Equipment Manufacturers (OEM)

- Aftermarket

Original equipment manufacturers (OEM) dominate with a market share of 70.05% of the total Italy drones market in 2025.

Original equipment manufacturers (OEMs) account for the majority of the market share due to their capacity to offer completely integrated and bespoke drone systems designed to meet particular industry requirements. OEMs are crucial in designing, manufacturing, and distributing high-quality drones that comply with regulatory standards and serve industries like agriculture, construction, and defense. Their ability to provide advanced drone technology with innovative features, including increased payload capacities, longer flight durations, and advanced sensors, positions them as the top option for companies looking for dependable and effective solutions.

Furthermore, OEMs benefit from established supply chains and strong relationships with various industries, allowing them to offer comprehensive after-sales support, including maintenance, software updates, and repair services. The demand for specialized drones, particularly those with unique payload capacities and advanced sensors, further contributes to the dominance of OEMs in the market. As businesses continue to seek optimized, industry-specific drone solutions, OEMs remain the go-to point of sale, providing tailored offerings that meet the evolving needs of commercial and industrial sectors.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Agriculture

- Military and Defense

- Law Enforcement

- Logistics

- Media and Entertainment

- Others

Military and defense lead with a market share of 31.03% of the total Italy drones market in 2025.

Military and defense dominate the market owing to the growing dependence on drones for surveillance, reconnaissance, and tactical missions. The Italian military and security forces are significantly investing in unmanned aerial systems (UAS) due to their capability to deliver real-time intelligence, improve situational awareness, and carry out precise strikes in areas of conflict. The versatility of drones, along with their capability to function in hazardous environments without risking personnel safety, renders them essential for national defense strategies and border monitoring, significantly contributing to their market share.

Moreover, Italy's defense industry has seen substantial advancements in drone technology, with military drones now capable of carrying advanced payloads like high-resolution cameras, radar, and electronic warfare systems. These innovations increase operational effectiveness in areas, such as counterterrorism, anti-smuggling, and maritime patrol. As global defense spending increases and the strategic value of drones continues to grow, the military and defense sector is expected to maintain its dominance in the market, with ongoing research and development (R&D) enhancing the capabilities of these critical assets.

Regional Insights:

- Northwest

- Northeast

- Central

- South

- Others

Northwest, including regions like Lombardy and Piedmont, is a vital segment in the drone market due to its technological and industrial strengths. The region’s advanced manufacturing sectors, particularly in aerospace and agriculture, catalyzes the demand for drones in logistics, surveying, and precision agriculture.

In Northeast, particularly Veneto and Friuli Venezia Giulia, drone adoption is rising across sectors like agriculture, infrastructure inspection, and environmental monitoring. The region’s strong industrial base and the growing interest in automation are driving the use of drones for both commercial and research applications.

Central, including Lazio and Tuscany, is seeing an increase in drone applications for industries such as tourism, agriculture, and media. With the growing support for tech innovation, regional initiatives are boosting the use of drones in surveying, monitoring, and entertainment, further shaping Italy’s drone market landscape.

In South, regions like Campania and Sicily are becoming more involved in drone technologies, driven by their emphasis on agriculture, infrastructure inspection, and emergency services. Government incentives and the rising interest in the use of drones for environmental monitoring are contributing to the growth of the market.

Others, such as smaller rural and remote areas, are gradually adopting drone technology for applications in agriculture, environmental protection, and logistics. These areas are focusing on research, development, and integrating drones into local services, broadening Italy’s overall drone market by diversifying its applications.

Market Dynamics:

Growth Drivers:

Why is the Italy Drones Market Growing?

Growth of Hydrogen and Alternative Energy Drone Solutions

The continuous innovation in alternative propulsion systems, particularly hydrogen fuel cell technology, is propelling the market growth. This trend represents a shift toward cleaner and longer-endurance drone operations, enabling new use cases beyond conventional battery limitations. In 2024, Intelligent Energy partnered with H2C and SAVE S.p.A to introduce hydrogen fuel cell–powered cargo drones in Italy’s Veneto region, highlighted by a simulated medical package delivery from Venice to Mestre Hospital. This marked Italy’s first ENAC-authorized hydrogen drone flight, demonstrating extended range and higher payload potential. Such advancements are supporting the market growth through sustainable aviation technologies.

Expansion of Domestic Drone Manufacturing

The Italy drone market growth is being driven by the expansion of local manufacturing capabilities through international partnerships. Leading drone companies are leveraging Italy’s well-established aerospace infrastructure to scale production and strengthen technological expertise. This trend is reflected in 2025, when Baykar planned to manufacture its AKINCI and TB2 military drones at Piaggio Aerospace facilities following its acquisition deal. The initiative also aimed to deepen cooperation with Leonardo on advanced drone systems. Such developments enhance domestic production capacity, encourage technology transfer, and reinforce Italy’s position as an important hub for drone innovation, contributing to the market growth.

Defense Modernization and Naval Drone Integration

Italy drone market is benefiting from rising defense modernization efforts, particularly within naval operations, creating a favorable outlook for advanced unmanned systems. Armed forces are increasingly integrating drones to strengthen intelligence, surveillance, and reconnaissance capabilities while improving operational efficiency and reducing personnel risk. This trend was evident in 2024, when the Italian Navy announced plans for the Sciamano Drone Carrier, a vessel developed with Fincantieri to launch and recover UAVs for ISR missions. The project included advanced command and control systems capable of managing large drone deployments, such as coordinated swarm operations, supporting sustained defense-driven demand.

Market Restraints:

What Challenges the Italy Drones Market is Facing?

Airspace Restrictions and Complex Authorization Requirements

Italy’s rich cultural heritage and dense urban areas result in extensive restricted airspace zones, severely limiting commercial drone operations in key economic regions. Cities like Rome, Venice, and Florence impose strict no-fly zones around historic landmarks, necessitating complex authorization processes. These regulations create significant barriers for businesses looking to utilize drones, stifling commercial applications and complicating operations in some of the country's most valuable economic hubs.

High Initial Investment Costs for Professional Operations

Professional-grade drone platforms, specialized payloads, and necessary certifications demand significant capital investments, creating barriers for small and medium-sized firms. Coupled with mandatory insurance requirements under European regulations, these high upfront costs restrict market adoption, particularly in agricultural and commercial sectors. This financial burden limits the ability of smaller businesses to leverage drone technology, hindering broader industry growth and market penetration.

Skilled Operator Shortages and Training Gaps

The drone market is encountering significant workforce development challenges, as the demand for certified operators and specialized technicians exceeds the capacity of available training infrastructure. This shortage of skilled professionals threatens to slow industry progress, with companies struggling to meet operational needs. Expanding and modernizing training programs will be crucial to address these gaps and ensure a capable workforce to support drone technology’s evolution.

Competitive Landscape:

The Italy drones market exhibits evolving competitive dynamics characterized by strategic partnerships between domestic aerospace leaders and international drone manufacturers. Market participants are pursuing differentiation through technological innovation, service integration, and regulatory compliance capabilities that address diverse client requirements across defense, commercial, and agricultural segments. Competition is increasingly shaped by vertical integration strategies, local manufacturing commitments, and comprehensive support offerings that strengthen client relationships beyond initial equipment sales. Strategic alliances and joint ventures are reshaping competitive positioning as European defense priorities create opportunities for manufacturers capable of delivering indigenous production capabilities addressing continental sovereignty objectives.

Recent Developments:

- October 2025: Italian shipbuilder Fincantieri unveiled its first underwater drone system, DEEP, aimed at protecting critical underwater infrastructure. The platform combined underwater sensors, autonomous vehicles, real-time command control, and AI-based data analysis for security and monitoring missions.

- September 2025: Italy’s FS Group signed a three-year agreement with aviation regulator ENAC to deploy long-distance drones for daily rail infrastructure monitoring. The partnership aimed to speed up drone adoption across the wider FS rail network while ensuring smoother regulatory approvals. This move supported more efficient inspection, safety oversight, and innovation in railway maintenance operations.

Italy Drones Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed Wing, Rotary Wing, Hybrid |

| Components Covered | Hardware, Software, Accessories |

| Payloads Covered | <25 Kilograms, 25-170 Kilograms, >170 Kilograms |

| Points of Sales Covered | Original Equipment Manufacturers (OEM), Aftermarket |

| End-Use Industries Covered | Construction, Agriculture, Military and Defense, Law Enforcement, Logistics, Media and Entertainment, Others |

| Regions Covered | Northwest, Northeast, Central, South, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Italy Drones Market Report

The Italy drones market size was valued at USD 1,860.90 Million in 2025.

The Italy drones market is expected to grow at a compound annual growth rate of 10.03% from 2026-2034 to reach USD 787.14 Million by 2034.

Rotary wing holds the largest revenue share of 51.02% in 2025, driven by superior hovering capabilities, operational versatility across diverse applications, and ease of deployment for agricultural monitoring, infrastructure inspection, and aerial photography throughout Italy.

Key factors driving the Italy drones market include the rising adoption of precision agriculture, where farmers use drones for crop monitoring, irrigation assessment, and efficient spraying. This trend is reflected in 2025, when Envirotech Vehicles signed an LOI with Studio di Agronomia Baffetti to deploy heavy-lift agricultural drones in Tuscany.

Major challenges include extensive airspace restrictions around cultural heritage sites and urban areas, high initial investment costs for professional-grade platforms and certifications, skilled operator shortages affecting military and commercial sectors, complex authorization requirements under specific category regulations, and evolving cybersecurity concerns affecting mission-critical applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)