Italy Plywood Market Size, Share, Trends and Forecast by Application, Sector, and Region, 2026-2034

Italy Plywood Market Summary:

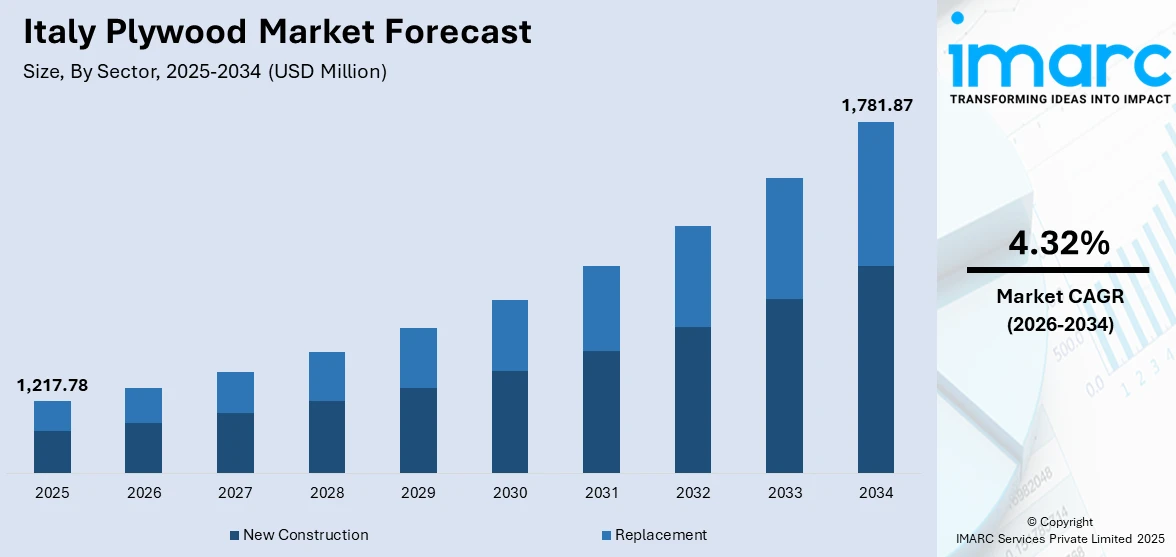

The Italy plywood market size was valued at USD 1,217.78 Million in 2025 and is projected to reach USD 1,781.87 Million by 2034, growing at a compound annual growth rate of 4.32% from 2026-2034.

The Italy plywood market is experiencing steady expansion, driven by the country's thriving furniture manufacturing industry, alongside consistent demand from residential construction and interior renovation activities. The growing emphasis on sustainable and certified wood products, combined with Italian craftsmanship traditions in decorative finishes and lightweight panel applications, continues to strengthen market positioning. Rising consumer preferences for eco-friendly materials, increasing adoption of Forest Stewardship Council (FSC) and Programme for the Endorsement of Forest Certification (PEFC) approved products, and advancements in production technologies are further propelling the market share.

Key Takeaways and Insights:

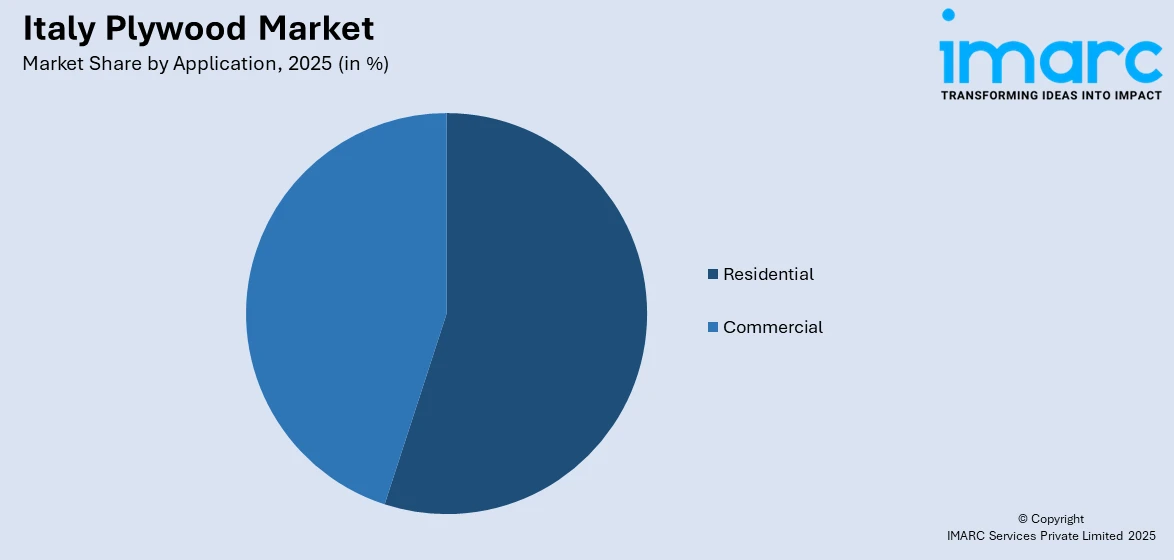

- By Application: Residential dominates the market with a share of 55.04% in 2025, driven by consistent demand for plywood in home construction, interior finishing, flooring applications, and furniture manufacturing for household use across Italian households.

- By Sector: New Construction leads the market with a share of 62% in 2025, due to steady residential and commercial building activities and plywood’s cost efficiency, versatility, and suitability for formwork, flooring, roofing, and interior applications.

- Key Players: Key players drive the Italy plywood market by expanding certified product portfolios, investing in sustainable manufacturing processes, strengthening distribution networks, and forming strategic partnerships across the furniture and construction supply chains to enhance market penetration and product accessibility.

To get more information on this market Request Sample

The Italy plywood market is advancing, as manufacturers, furniture producers, and construction companies embrace sustainable wood panel solutions for diverse applications. The country's position as one of Europe's largest furniture exporters creates substantial demand for high-quality plywood materials in cabinet making, interior design elements, and decorative applications. Italian consumers and businesses increasingly prioritize environmentally certified products, with FSC and PEFC certifications gaining prominence across the wood processing supply chain. The real estate industry benefits from ongoing renovation activities and home improvement projects, particularly in urban centers like Milan, Rome, and Florence where property values continue to rise. As per IMARC Group, the Italy real estate market size reached USD 10.2 Trillion in 2024. Manufacturing excellence in industrial regions, particularly Lombardy and Veneto, supports a robust domestic production base while meeting export demand.

Italy Plywood Market Trends:

Growing Emphasis on Sustainability and Environmental Certifications

The market for plywood in Italy is experiencing growing demand for sustainably produced and certified wood products, due to rising environmental awareness among consumers and enterprises. Italian companies are actively seeking FSC and PEFC certification to prove their responsible forest management practices and keep up with the changing regulations of the European Union. This trend is also affecting the purchasing decisions of companies in the construction industry and furniture producers, who are increasingly focusing on sustainable materials. Green building standards and labeling requirements are further promoting the preference for certified plywood products.

Advancements in Lightweight and Decorative Panel Applications

Italian plywood producers are diversifying their product lines with new and innovative lightweight materials and finishing options that meet the changing demands of interior design. The Italian tradition of craftsmanship helps in the development of value-added products, with high-quality surface finishes, rotary-cut veneers, and special laminates for high-end furniture use. Italian poplar plywood has also received recognition for its ability to be both light and workable, thus suitable for modern furniture designs that demand dimensional stability. During the Milan Design Week, held from 7 April- 13 April 2025, the Italian furniture brand Flexform showcased two installations at its flagship store and Chiostro Sant’Angelo. The installations displayed Flexform's range of indoor and outdoor furniture, blending technology with craftsmanship. These innovations are strengthening the positioning of Italian plywood in premium domestic and international furniture markets.

Integration of Domestic Poplar Cultivation and Circular Economy Practices

The Italy plywood market growth is supported by increasing integration between domestic poplar cultivation and manufacturing operations, creating sustainable short supply chains. Italian plywood producers are investing in agricultural farms dedicated to poplar cultivation for industrial supply, reducing dependence on imported raw materials while ensuring quality control. Italy possessed more than 11 Million hectares of forest covering substantial national territory as of 2024. This vertical integration improves supply reliability and stabilizes raw material costs for manufacturers. It also supports rural economic development while aligning plywood production with national sustainability and traceability objectives.

Market Outlook 2026-2034:

The Italy plywood market demonstrates promising growth prospects, as manufacturers continue to invest in sustainable production capabilities and expanding certified product offerings. The market generated a revenue of USD 1,217.78 Million in 2025 and is projected to reach a revenue of USD 1,781.87 Million by 2034, growing at a compound annual growth rate of 4.32% from 2026-2034. The furniture manufacturing sector remains a primary demand driver, with Italian producers maintaining global leadership in design innovation and quality craftsmanship. Residential construction activities, particularly renovation and interior improvement projects, sustain consistent plywood consumption across applications, including flooring, wall paneling, and cabinetry. The organized sector is expected to strengthen its dominance through enhanced distribution networks and quality assurance mechanisms.

Italy Plywood Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Residential |

55.04% |

|

Sector |

New Construction |

62% |

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

Residential dominates with a market share of 55.04% of the total Italy plywood market in 2025.

Residential maintains its leading position in the Italy plywood market, driven by consistent demand from home construction, renovation activities, and interior furnishing applications. Italian households demonstrate strong preference for quality wood-based materials in flooring, wall paneling, kitchen cabinetry, and furniture manufacturing. In 2024, Italy recorded 720,000 acquisitions of residential properties, marking an increase of 1.3% compared to 2023. The increasing trend of home improvement projects, particularly in major urban centers including Milan and Rome, sustains demand for plywood products in renovation and remodeling activities.

The segment benefits from Italy's strong furniture manufacturing tradition, where plywood serves as a primary substrate for cabinet making, wardrobe construction, and decorative interior elements. Italian consumers increasingly prioritize sustainable and certified materials for their homes, driving demand for FSC and PEFC certified plywood products. The home furniture industry in Italy is thriving, with plywood representing a critical raw material for domestic furniture production. Energy efficiency considerations in residential buildings also support demand for wood-based panel solutions that contribute to improved thermal insulation and sustainable construction practices.

Sector Insights:

- New Construction

- Replacement

New construction leads with a share of 62% of the total Italy plywood market in 2025.

New construction prevails the market in Italy as plywood is a fundamental material in building projects, adopted widely because of its strength, versatility, and economic viability. Plywood is used in formwork, flooring, roofing, walling, and interior finishing, making it a key material in various construction phases. Urban housing construction, mixed-use developments, and infrastructure-related real estate activities continue to drive the demand for plywood. Its ease of installation, strength, and adaptability to different architectural designs make it a preferred material in building construction.

Moreover, new construction projects are increasingly focusing on faster construction schedules and standardized materials, which further drives the demand for plywood. Plywood is more resistant to warping and cracking than solid wood, which makes it more economical in terms of material wastage during construction. Its adaptability to modern construction methods, prefabrication, and modular construction further cements its position in new construction projects. With the growing acceptance of engineered wood products that align with sustainable construction practices, plywood is a viable option that strikes a balance between performance, availability, and cost control in construction projects.

Regional Insights:

- Northwest

- Northeast

- Central

- South

- Others

Northwest is a key plywood demand market in Italy, backed by robust residential construction, commercial development, and renovation. Its proximity to industrial areas, furniture production hubs, and transportation infrastructure ensures consistent demand for structural and interior-grade plywood. The presence of established distribution and import networks further reinforces regional market position.

Northeast is backed by a well-established woodworking and furniture sector, ensuring consistent plywood demand for construction and value-added purposes. Robust export-oriented manufacturing, along with active residential and light industrial construction, ensures stable demand. Plywood is widely used in flooring substrates, wall panels, and prefabricated building components.

Central ensures stable plywood demand, backed by urban residential projects, public infrastructure development, and renovation of historic buildings. Demand is ensured by balanced use in structural, interior, and formwork applications. A strong government emphasis on construction quality further ensures stable plywood demand in residential and mixed-use projects.

The South market is shaped by rising residential construction, tourism-driven real estate development, and public infrastructure spending. Plywood is widely used in budget-conscious applications, including formwork and interior structures. Gradual development in construction activity and housing affordability is furthering modest but stable market growth.

Market Dynamics:

Growth Drivers:

Why is the Italy Plywood Market Growing?

Strong Furniture Manufacturing Industry Creating Sustained Demand

Italy's position as one of the world's leading furniture manufacturers and exporters generates substantial demand for high-quality plywood as a primary raw material for cabinet making, interior furnishings, and decorative applications. As per IMARC Group, the Italy furniture market size reached USD 26.70 Billion in 2024. Italian furniture commands premium positioning in global markets, with exports reaching major destinations, including France, Germany, and the United Arab Emirates. This export-oriented manufacturing base requires consistent supply of quality-controlled plywood meeting exacting specifications for surface finish, dimensional stability, and structural performance. The industry's emphasis on design innovation and craftsmanship excellence creates opportunities for specialized plywood products, including decorative veneered panels and engineered substrates, supporting complex furniture geometries. Rising demand for sustainable and certified materials in international markets further encourages Italian manufacturers to source eco-friendly plywood that aligns with global quality and environmental standards.

Renovation and Home Improvement Activities Supporting Market Expansion

The sustained activity in residential renovation and home improvement projects across Italy creates ongoing demand for plywood products in flooring, wall covering, cabinetry, and interior finishing applications. Italian government initiatives, including the Renovation Bonus 2024 offering 50% deduction for home improvements, encourage homeowners to undertake renovation projects requiring plywood materials. Property values in major Italian cities, such as Milan and Rome, continue to rise, motivating property owners to invest in interior improvements that enhance both functionality and aesthetic appeal. Interior design trends emphasizing natural wood aesthetics and sustainable materials further support demand for quality plywood products in residential applications. Additionally, increased focus on energy-efficient and durable home upgrades is driving plywood use in structural and interior applications. Homeowners are also opting for materials that offer long-term reliability and aesthetic appeal, further supporting plywood demand.

Technological Advancements and Product Innovations

Technological improvements and product innovations are significant growth drivers for the Italy plywood market. Manufacturers are increasingly developing engineered panels with enhanced strength, lightweight properties, and improved resistance to moisture, warping, and pests. Innovations, such as multi-layered poplar plywood, specialty laminates, and decorative finishes, allow the material to meet both aesthetic and functional requirements in modern construction and interior design. Enhanced machinery and automated production processes improve efficiency, reduce waste, and allow customized panel sizes to suit specific applications. These developments also enable the introduction of eco-friendly and certified products, meeting rising sustainability demands. The focus on innovation helps manufacturers differentiate their offerings, attract premium customers, and expand into new application segments. By combining performance, durability, and design versatility, technological advancements are enabling plywood to capture a larger share of both traditional construction and specialized design-oriented markets in Italy.

Market Restraints:

What Challenges the Italy Plywood Market is Facing?

Raw Material Supply Constraints and Price Volatility

The Italy plywood market faces challenges related to raw material availability and price fluctuations that impact production costs and profitability. Shortages of raw materials have created pressure on the wood panel industry, with producers seeking alternative sourcing strategies. While Italy possesses substantial forest resources, the industry historically relied on imported materials, creating vulnerability to supply chain disruptions and international price movements. These constraints require manufacturers to balance cost management with quality maintenance while navigating uncertain material markets.

Competition from Alternative Panel Materials

The Italy plywood market encounters competition from alternative wood-based panel materials, including particleboard and oriented strand board that offer lower price points for certain applications. Particleboard accounts for a majority of materials used in mass-produced furniture due to its affordability and engineering flexibility with laminates. Paper laminated particleboard panels have gained market share in furniture applications previously served by wood veneered products. This competitive pressure requires plywood manufacturers to emphasize quality differentiation and value-added applications where plywood's structural advantages remain compelling.

Stringent Environmental and Regulatory Requirements

Manufacturers in Italy face increasing challenges from environmental regulations and sustainability standards. Compliance with emission limits, waste management, and forest management criteria adds operational complexity and cost. These requirements can slow product approvals and limit sourcing options, particularly for imported timber. Plywood producers must invest in eco-friendly practices, maintain traceability across supply chains, and demonstrate compliance to retain market access and customer trust.

Competitive Landscape:

The Italy plywood market features a competitive landscape, comprising established domestic manufacturers, family-owned enterprises, and international players operating production facilities across various regions. Market participants differentiate through product quality, sustainability certifications, specialized applications, and distribution network strength. Companies are investing in manufacturing technology upgrades, capacity expansion, and environmental compliance to strengthen competitive positioning. Strategic partnerships between plywood producers and furniture manufacturers enable product development collaboration and supply chain integration. Innovations in design and surface finishes further allow companies to cater to premium segments and emerging interior design trends.

Recent Developments:

-

In April 2025, Panguaneta served as the main sponsor and technical partner for photographer Juergen Teller's exhibition in Sabbioneta, showcasing its Maple Superior plywood. Featuring premium poplar cores sourced from sustainably managed local plantations and refined rotary-cut maple faces, this plywood represented the perfect blend of adaptability, lightness, and natural allure.

Italy Plywood Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Residential, Commercial |

| Sectors Covered | New Construction, Replacement |

| Regions Covered | Northwest, Northeast, Central, South, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Italy Plywood Market Report

The Italy plywood market size was valued at USD 1,217.78 Million in 2025.

The Italy plywood market is expected to grow at a compound annual growth rate of 4.32% from 2026-2034 to reach USD 1,781.87 Million by 2034.

Residential dominated the market with a share of 55.04%, driven by consistent demand from home construction, interior renovation, flooring applications, and furniture manufacturing for household use across Italian residential properties.

Key factors driving the Italy plywood market include strong furniture manufacturing demand, growing emphasis on sustainability certifications, residential renovation activities, and increasing adoption of environmentally certified wood products.

Major challenges include raw material supply constraints, weakening residential construction activities, declining building permits, competition from alternative panel materials, and price volatility affecting production costs. Additionally, stringent environmental regulations and certification requirements can increase compliance costs and complicate production processes for manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)