Japan Aerospace Composites Market Size, Share, Trends and Forecast by Fiber Type, Resin Type, Aircraft Type, Application, and Region 2026-2034

Japan Aerospace Composites Market Size & Forecast 2026-2034

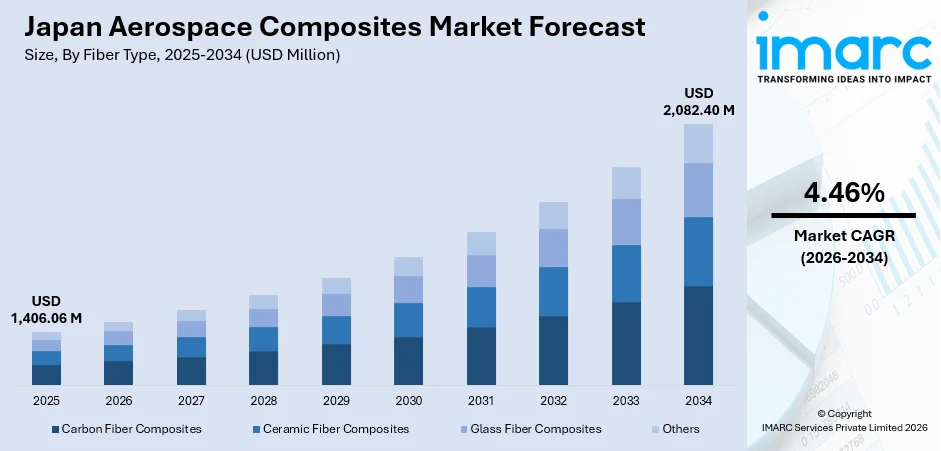

The Japan aerospace composites market size was valued at USD 1,406.06 Million in 2025. IMARC Group estimates the market to reach USD 2,082.40 Million by 2034, exhibiting a CAGR of 4.46% during 2026-2034, underpinned by deep integration into the global commercial aviation supply chain, a record Japanese defense budget of ¥8.7 trillion (US$55 billion) in 2025, up 9.4% from the previous year, and the country's expanding role in next-generation fighter and space launch programs. Japanese manufacturers Mitsubishi Heavy Industries, Kawasaki Heavy Industries, and Subaru Corporation collectively anchor Japan's role in the aerospace composites market share.

To get more information on this market Request Sample

Japan Aerospace Composites Industry Analysis - Key Insights

- Carbon fiber composites claim 68.4% by fiber type in 2025- Their unmatched strength-to-weight ratio, corrosion resistance, and integration into primary airframe structures (wings, fuselages, fairings) make every other fiber option a distant supporting act in Japan's aerospace supply chain.

- Epoxy commands with 72.6% by resin type in 2025- Epoxy's compatibility with carbon fiber prepregs, autoclave processing, and its proven aerospace certification pedigree lock it in as Japan's default matrix system for structural parts.

- Commercial aircraft holds 52.3% of aircraft type in 2025- and with Boeing 787 production running at approximately seven units per month and Japanese Tier 1 partners filling major structural roles, the commercial programme backlog provides durable, multi-year volume visibility for domestic composite manufacturers.

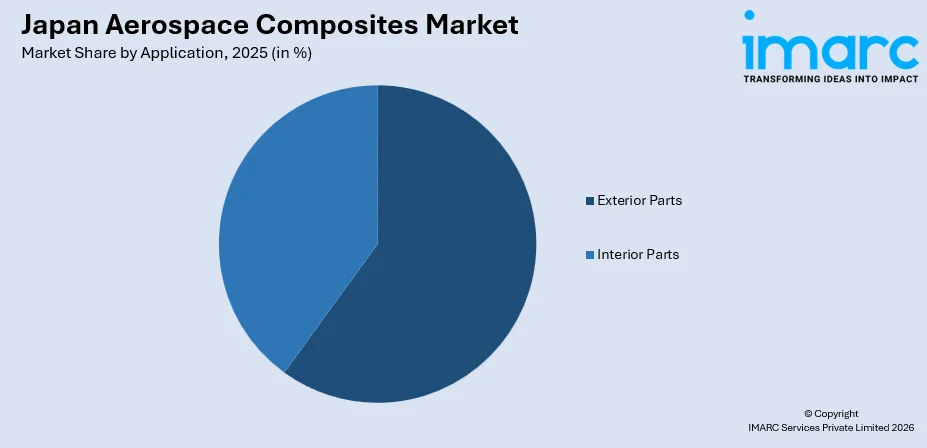

- Exterior parts take 58.7% of application share in 2025- driven by the structural loading requirements of wings, fuselages, and empennage sections that demand high-modulus carbon fiber with epoxy matrices.

- AFP/ATL leads manufacturing process at 36.2% in 2025- Automated fiber placement delivered improvement in production efficiency for complex aerostructure lay-ups and is the process of choice for wing skins and fuselage barrels at scale.

- Kanto Region dominates region at 39.5% in 2025- Toray Industries is headquartered in Tokyo, JAXA's principal research facilities are in the Kanto area, and the region hosts the highest density of aerospace R&D and advanced materials laboratories in Japan.

Japan Aerospace Composites Market Trends and Dynamics 2026

Market Trends

Thermoplastic Composites Gaining Rapid Traction in Japanese Aerospace Supply Chain

Japan's aerospace composites sector is shifting meaningfully toward thermoplastic matrix systems as manufacturers seek faster cycle times, weldability, and recyclability. In June 2025, Toray Advanced Composites, Daher, and TARMAC Aerosave jointly launched an End-of-Life Aircraft Recycling Programme for commercial aircraft production.

Automation-Led Manufacturing Transformation Elevating Quality and Throughput

Advanced automated fiber placement and automated tape laying systems are fundamentally altering the economics of Japan's composite aerostructure manufacturing. In February 2024, Mitsubishi Chemical Group developed a high-heat-resistant ceramic matrix composite utilizing pitch-based carbon fibers, achieving heat resistance up to 1,500°C for space industry applications.

Japan Space Strategy Fund Catalysing Composite Materials Innovation

Japan's government established a ¥1 trillion Space Strategy Fund, averaging ¥100 billion annually, directed at aerospace technology programs with explicit advanced composites content, including blended wing body structures, hydrogen-burning turbine components, and satellite aerostructures. The New Energy and Industrial Technology Development Organization (NEDO) is channeling considerable investment into advanced composite structures for next-generation propulsion platforms.

- eVTOL and Urban Air Mobility Composites: Japan's urban air mobility programs are generating demand for lightweight carbon fiber composite airframe structures, opening a nascent high-value segment for domestic material producers.

- Out-of-Autoclave Processing Expansion: OOA prepreg and resin transfer molding techniques are being adopted to reduce energy consumption, cut tooling costs, and enable faster part throughput for secondary aerospace structures.

- Digital Twin Integration in Composite Manufacturing: Japanese aerostructure manufacturers are deploying digital simulation and machine informatics to accelerate composite material qualification cycles and optimise lay-up sequences for complex wing and fuselage geometries.

- Recycled Carbon Fiber Commercialization: Driven by sustainability mandates and composite waste regulations, Japanese firms are advancing pyrolysis and solvolysis-based carbon fiber recovery for use in secondary aerospace and industrial applications.

Growth Drivers

Deep Integration into Boeing 787 and 777 Program Supply Chains

Japan's three principal heavy industrials collectively supply 35% of the Boeing 787's airframe content, with Mitsubishi Heavy Industries manufacturing the outer wing box, Kawasaki Heavy Industries producing the forward fuselage barrel and main landing gear wheel well, and Subaru Corporation fabricating the center wing box. As Boeing 787 production recovers toward higher monthly rates, the knock-on demand for composite components processed in Japan's Chubu and Kanto facilities directly amplifies Japan aerospace composites market growth.

Surging Japanese Defense Budget Fueling Advanced Composite Demand

Japan’s draft budget for fiscal year 2026, which begins in April, is 9.4% higher than the 2025 budget and represents the fourth year of the country’s five-year plan to double its annual defense spending to 2% of GDP.

Commercial Aviation Recovery and Rising Passenger Traffic Underpinning Aerostructure Orders

Japan's commercial aviation sector is on a steady recovery trajectory from pandemic-era disruptions, with SJAC data indicating that aircraft engine production has returned to pre-COVID levels and composite aerostructure output is following suit. The planned production ramp of the Boeing 787 program to higher monthly rates, supported by Japan's composite aerostructure suppliers, is creating forward demand visibility for carbon fiber prepreg and AFP-manufactured structural components.

- Toray's AP-G 2025 Carbon Fiber Investment: Toray expanded its capital investment in carbon fiber composites. The company previously invested 74 billion yen (about $560 million) over a three-year period ending in 2022, but it will more than double this amount to 165 billion yen (around $1.25 billion) for the three-year period ending in 2025, sustaining Japan's global supply capacity for aerospace-grade fiber.

- Space Launch Vehicle Composite Content Expansion: Japan's H3 rocket programme, H3 successor development, and defense budget are driving growing demand for AFP-processed composite fairings, motor cases, and structural panels.

- Japanese OEM Diversification Beyond Boeing Programmes: Kawasaki Heavy Industries and Mitsubishi Heavy Industries are expanding into domestic military transport, maritime patrol, and helicopter programs, each requiring high-volume composite structural parts.

Market Restraints

Dependence on a concentrated commercial aircraft programme base: Japan's aerospace composites demand is structurally concentrated around a small number of commercial aircraft platforms, particularly the Boeing 787. Any production rate disruption, program delays, or strategic shifts by a single OEM customer can disproportionately affect the order volumes and factory utilization rates.

High capital intensity and long qualification timelines: Aerospace-grade composite manufacturing requires exceptionally high upfront capital investment in autoclaves, AFP machine tooling, cleanroom facilities, and non-destructive inspection systems.

Recycling and end-of-life composite management challenges: Carbon fiber reinforced polymer structures remain difficult to recycle economically at scale, creating regulatory compliance pressure as aviation sustainability mandates tighten globally. The absence of a commercially mature domestic recycled carbon fiber ecosystem in Japan limits the circular economy credentials of Japanese aerospace composite producers and creates increasing scrutiny.

Japan Aerospace Composites Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

|

Fiber Type |

Carbon Fiber Composites |

68.4% |

2025 |

|

Resin Type |

Epoxy |

72.6% |

2025 |

|

Aircraft Type |

Commercial Aircraft |

52.3% |

2025 |

|

Application |

Exterior Parts |

58.7% |

2025 |

|

Manufacturing Process |

AFP/ATL |

36.2% |

2025 |

|

Region |

Kanto Region |

39.5% |

2025 |

Fiber Type Insights

Carbon Fiber Composites - 68.4% market share (2025) | Leading Fiber Type

Carbon fiber composites dominate Japan's aerospace composites market by a commanding margin, reflecting the material's unrivalled combination of specific strength, stiffness, fatigue resistance, and corrosion immunity that primary aerostructure programs demand. Toray Industries, the world's largest carbon fiber manufacturer, supplies TORAYCA T800S intermediate-modulus carbon fiber prepreg for the Boeing 787, making Japan structurally indispensable to one of aviation's most composite-intensive commercial platforms.

|

Segment Breakdown Carbon Fiber Composites (68.4%) · Ceramic Fiber Composites · Glass Fiber Composites · Others |

Resin Type Insights

Epoxy - 72.6% market share (2025) | Leading Resin Type

Epoxy resin systems command Japan's aerospace composites matrix market by a decisive margin, anchored by their proven performance in primary structural applications, superior fiber-to-matrix adhesion properties, and decades of aerospace qualification data accumulated across Boeing and JAXA programmes. Toray's 3900-series highly toughened carbon fiber-reinforced epoxy prepreg, the material of choice for the Boeing 787's main wings and fuselage barrel structures, exemplifies why epoxy remains structurally dominant: it is certified, performance-validated, and deeply embedded in Japan's aerostructure supply chain architecture.

|

Segment Breakdown Epoxy (72.6%) · Phenolic · Polyester · Polyimides · Thermoplastics · Ceramic and Metal Matrix · Others |

Aircraft Type Insights

Commercial Aircraft - 52.3% market share (2025) | Leading Aircraft Type

Commercial aircraft account for the majority of Japan's aerospace composites demand, driven by the country's deep structural integration into Boeing's widebody production programs. Japanese manufacturers supply approximately 35% of the 787 Dreamliner's airframe content, including wings, center wing boxes, forward fuselage sections, and aft fuselage panels.

|

Segment Breakdown Commercial Aircraft (52.3%) · Business Aviation · Civil Helicopters · Military Aircraft and Helicopters · Others |

Application Insights

Access the comprehensive market breakdown Request Sample

Exterior Parts - 58.7% market share (2025) | Leading Application

Exterior parts, encompassing wing skins, fuselage barrel sections, empennage structures, payload fairings, and control surfaces, account for the majority of Japan's aerospace composite applications by value, reflecting the structural loading requirements that mandate high-modulus carbon fiber with toughened epoxy matrix systems.

|

Segment Breakdown Exterior Parts (58.7%) · Interior Parts |

Manufacturing Process Insights

AFP/ATL - 36.2% market share (2025) | Leading Manufacturing Process

Automated fiber placement and automated tape laying systems lead Japan's aerospace composite manufacturing process landscape, reflecting the country's capital-intensive, precision-engineering industrial culture and the programme-scale requirements of Boeing widebody aerostructure production. The AFP/ATL process delivers four to eight times higher throughput than legacy manual lay-up, and Toray's H3 rocket fairing section adoption of slit-tape AFP prepreg specifically demonstrates the process's expansion beyond commercial aviation into space launch vehicle applications.

|

Segment Breakdown AFP/ATL (36.2%) · Layup · RTM/VARTM · Filament Winding · Others |

Regional Insights

Kanto Region - 39.5% market share (2025) | Leading Region

The Kanto Region commands Japan's aerospace composites market through its unmatched concentration of advanced materials producers, aerospace R&D institutions, and corporate headquarters of the country's major composite manufacturers. Toray Industries, the world's largest carbon fiber producer, supplying TORAYCA prepreg for the Boeing 787 programme and JAXA's H3 rocket, is headquartered in Chuo-ku, Tokyo

|

Metric

|

Details

|

|---|---|

| Market share in 2025 | 39.5% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | Carbon fiber producer headquarters, JAXA research infrastructure, R&D and materials qualification capacity, Boeing supply chain coordination |

| Outlook | Sustained leadership through R&D and production leadership |

|

Regional Breakdown Kanto Region (39.5%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

Kansai is Japan's second-largest aerospace composites region, anchored by Osaka's manufacturing base and the presence of aerospace-grade materials processing facilities. Osaka's dense chemical and advanced materials industrial cluster supports the resin and prepreg supply chains that feed both domestic and export-facing aerospace composite producers.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga |

| Key Growth Drivers | Teijin Tenax carbon fiber production, Osaka advanced chemicals cluster, resin and prepreg processing infrastructure |

| Outlook | Steady growth through thermoplastic composite expansion |

Central/Chubu Region:

Chubu is Japan's primary aerostructure manufacturing hub and the operational heart of the country's aerospace composite supply chain.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Boeing 787 aerostructure production volumes, MHI and KHI composite facilities, Dreamliner supply chain logistics hub, 777X composite panel programmes |

| Outlook | Highest composite volume output region through forecast period |

Kyushu-Okinawa Region:

Kyushu-Okinawa hosts Japan's most significant naval and defence aviation manufacturing cluster. Japan's record defense budget of JPY 8.7 trillion in fiscal 2025, supplementing the region's primary structure manufacturing volumes.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto |

| Key Growth Drivers | Defence composite manufacturing, F-35 MRO demand, P-1 and C-2 programme composite content, naval aviation expansion |

| Outlook | Accelerating growth driven by record defence expenditure |

Tohoku Region:

The region's manufacturing base, strengthened by post-2011 reconstruction investments, includes specialized composite fastening, bonding, and non-destructive inspection service providers that support Japan's broader aerospace supply chain.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima |

| Key Growth Drivers | Precision composite subassembly supply, reconstruction-linked manufacturing upgrades, aerospace service provider growth |

| Outlook | Moderate growth via supply chain integration |

.webp)

Market Outlook (2026-2034)

What is the future outlook of the Japan Aerospace Composites market?

The Japan Aerospace Composites market is expected to sustain steady revenue growth through 2034.

Japan's aerospace composites market is positioned for steady, structurally grounded expansion through 2034, anchored by the country's irreplaceable role in Boeing's widebody supply chain, a rapidly growing defence budget, and the government's ¥1 trillion Space Strategy Fund catalyzing advanced materials demand across space and next-generation aviation platforms. The NEDO's investments in blended wing body composite structures collectively reinforce the Japan aerospace composites market outlook.

Japan Aerospace Composites Market - Leading Key Players

Japan's aerospace composites market is dominated by a concentrated group of globally leading carbon fiber producers and precision aerostructure manufacturers whose long-term program agreements with Boeing define the competitive landscape.

| Company | Leading Brands/Products | Highlights |

|---|---|---|

|

Toray Industries Inc. |

TORAYCA Carbon Fiber, Toray Advanced Composites Aerospace Materials | Global leader in carbon fiber and composite materials widely used in aircraft structures, satellites, and aerospace components. |

|

Teijin Limited |

Tenax Carbon Fiber, Tenax Thermoplastic Composites |

Major Japanese manufacturer of high-performance carbon fiber composites used in aerospace structures due to their high strength and lightweight properties. |

|

JAMCO Corporation |

CFRP Structural Members, Aircraft Interior Composite Components |

Manufactures carbon fiber reinforced plastic (CFRP) structural parts and aircraft components for global aerospace manufacturers. |

Some of the other key players in Japan aerospace composites market are Mitsubishi Chemical Group Corporation, Mitsubishi Heavy Industries, Ltd., Kawasaki Heavy Industries, Ltd., Subaru Corporation, etc.

Latest Development & News

- In June 2025, Toray Advanced Composites, Daher, and TARMAC Aerosave launched a joint End-of-Life Aerospace Recycling Program for commercial aircraft production. In collaboration with Airbus, the initiative aims to improve recycling technologies in aerospace manufacturing by recovering and reusing end-of-life secondary structural components made from continuous fiber-reinforced thermoplastic composites.

- In February 2024, the Mitsubishi Chemical Group (MCG Group) announced the development of a high heat-resistant ceramic matrix composite (CMC) made using pitch-based carbon fibers. With the ability to withstand temperatures of up to 1,500°C, the material is expected to be primarily used in space industry applications.

Japan Aerospace Composites Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Fiber Types Covered | Carbon Fiber Composites, Ceramic Fiber Composites, Glass Fiber Composites, Others |

| Resin Types Covered | Epoxy, Phenolic, Polyester, Polyimides, Thermoplastics, Ceramic and Metal Matrix, Others |

| Aircraft Types Covered | Commercial Aircraft, Business Aviation, Civil Helicopters, Military Aircraft and Helicopters, Others |

| Applications Covered | Interior Parts, Exterior Parts |

| Manufacturing Processes Covered | AFP/ATL, Layup, RTM/VARTM, Filament Winding, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan aerospace composites market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan aerospace composites market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan aerospace composites industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Aerospace Composites Market Report

The Japan aerospace composites market reached a value of USD 1,406.06 Million in 2025.

The market is projected to grow at a CAGR of 4.46% during 2026-2034, reaching USD 2,082.40 Million by 2034.

Key growth drivers include the expanding aerospace industry, rising demand for lightweight high-strength materials to improve fuel efficiency, stringent environmental regulations, sustained R&D in composite technologies, and surging regional air travel.

The report covers segmentation by fiber type, resin type, aircraft type, application, manufacturing process, and region. Each segment includes detailed market size and forecast analysis.

Key trends include advancements in material science driving adoption of lightweight composites, tightening environmental regulations accelerating fuel-efficiency mandates, and deepening collaborations between aerospace OEMs and composite material suppliers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)