Japan Anime Market Size, Share, Trends and Forecast by Revenue Source and Region, 2026-2034

Japan Anime Market Size, Share, Trends & Forecast (2026-2034)

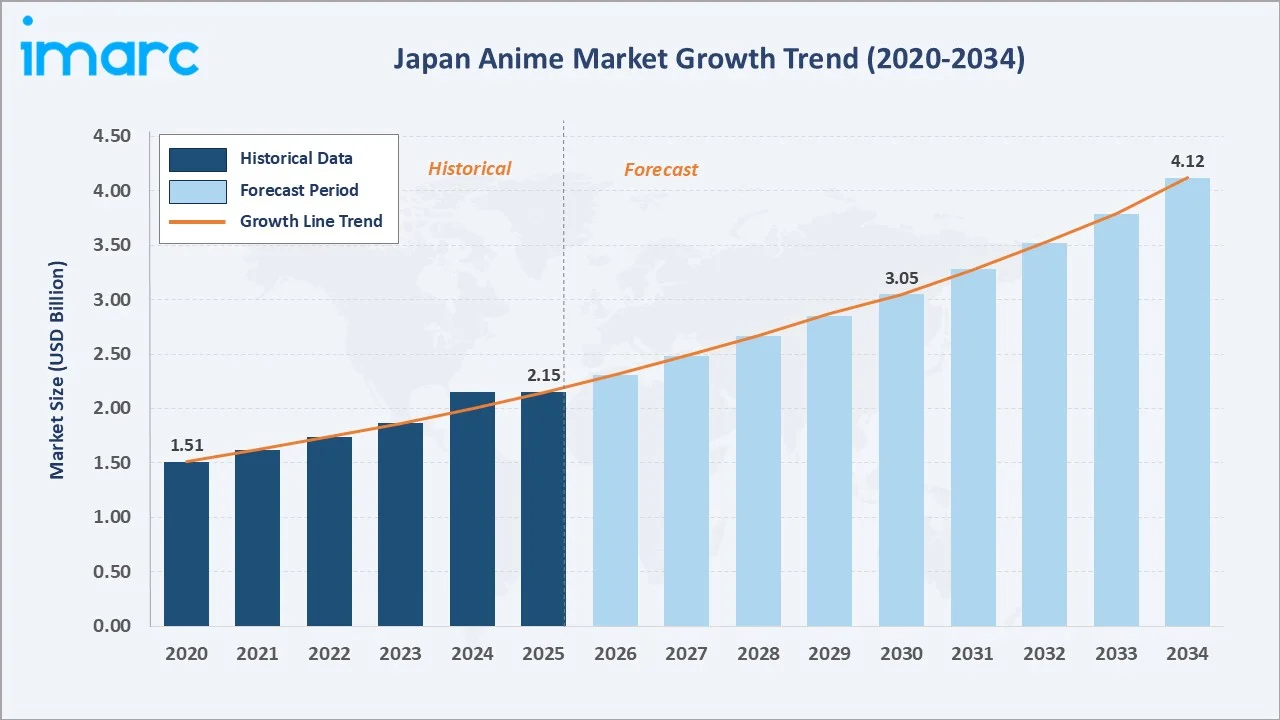

The Japan anime market was valued at USD 2.15 Billion in 2025 and is projected to reach USD 4.12 Billion by 2034, exhibiting a CAGR of 7.28% during 2026-2034. Rising global streaming demand, expanding overseas licensing, government-backed cultural promotion, and surging commercialization of anime intellectual property (IP) across merchandising, gaming, and live entertainment are the primary forces shaping market growth.

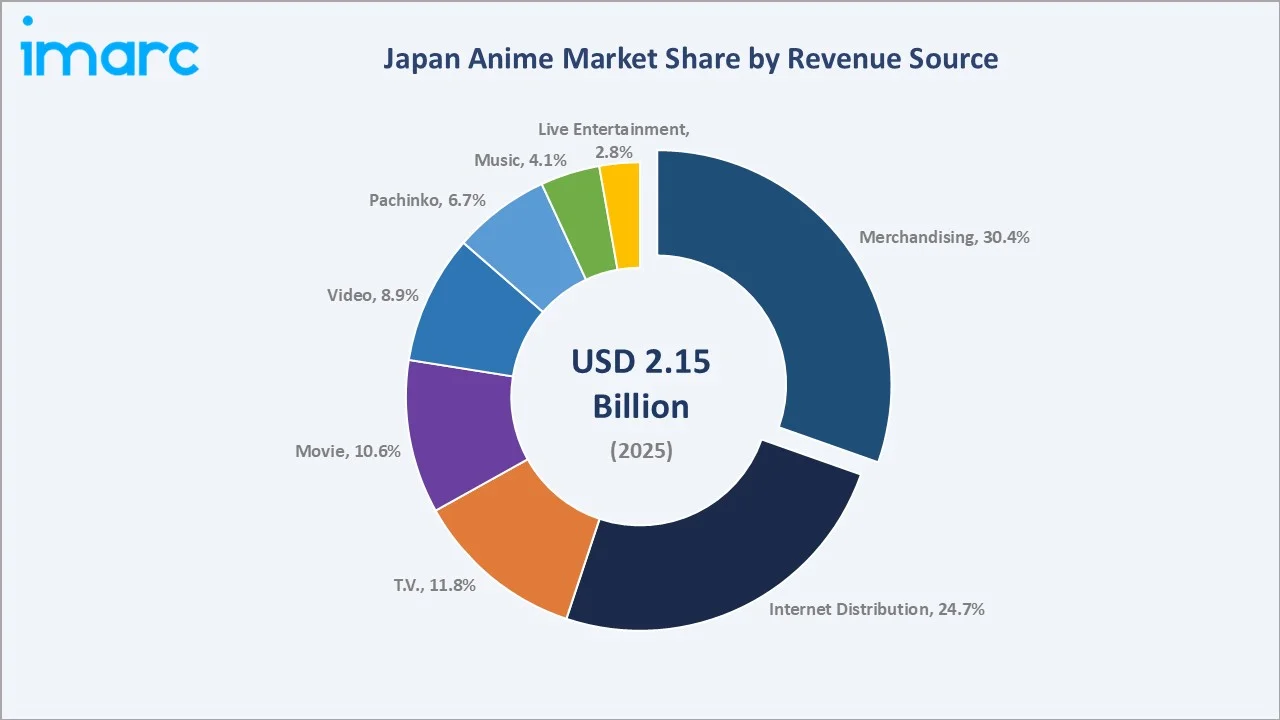

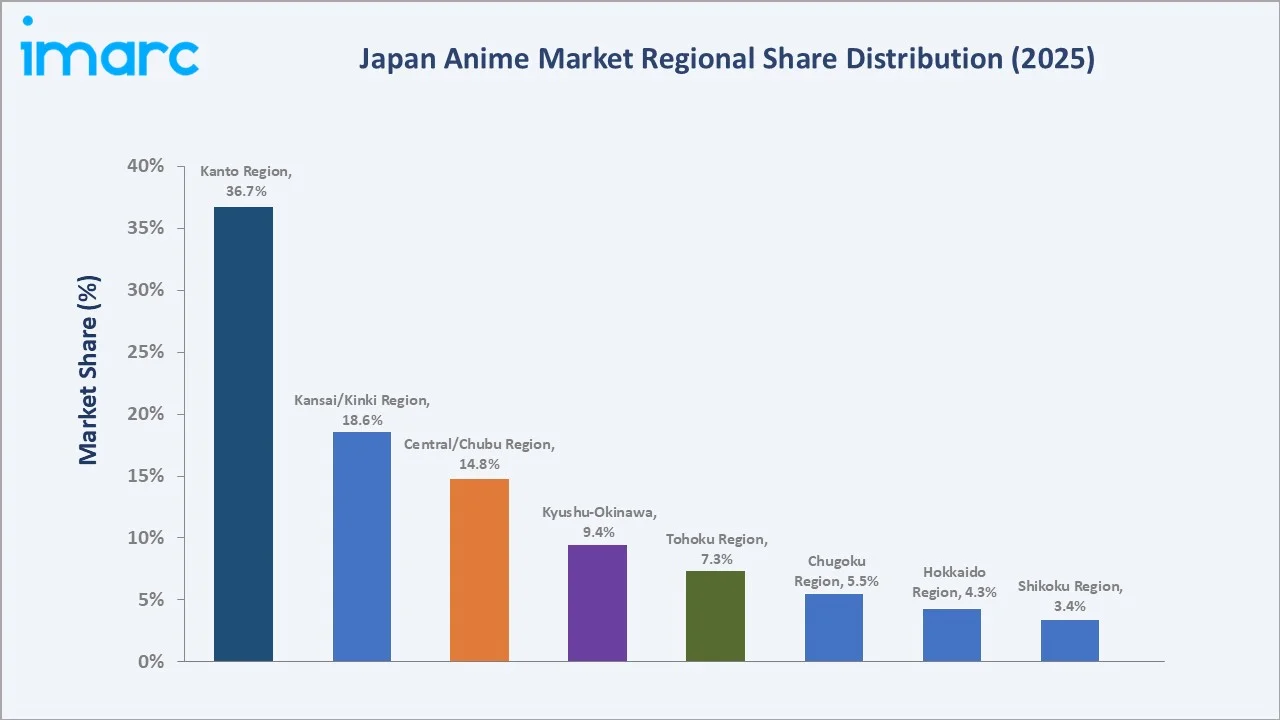

Merchandising leads the revenue source segment at 30.4% and Kanto Region commands 36.7% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.15 Billion |

|

Forecast Market Size (2034) |

USD 4.12 Billion |

|

CAGR (2026-2034) |

7.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (36.7%, 2025) |

|

Second Largest Region |

Kansai/Kinki Region (18.6%, 2025) |

|

Leading Revenue Source |

Merchandising (30.4%, 2025) |

The Japan anime market expanded from USD 1.51 Billion in 2020 to USD 2.15 Billion in 2025, driven by widening digital content consumption, growing global fan communities, and rapid broadening of dedicated anime streaming platforms worldwide. Anchored at USD 3.05 Billion in 2030, the forecast to USD 4.12 Billion by 2034 is supported by accelerating internet distribution adoption, expanding merchandise ecosystems, and the continued internationalization of anime IP.

To get more information on this market, Request Sample

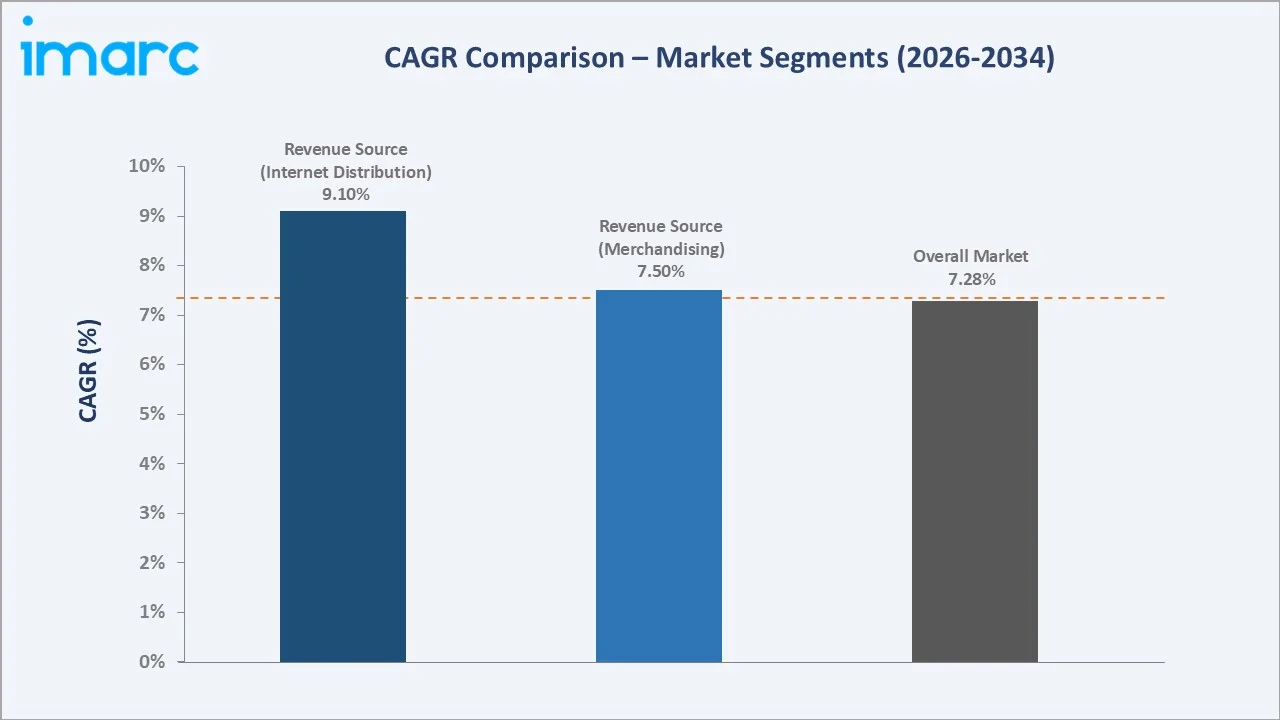

CAGR trajectories across revenue source and regional sub-segments show internet distribution, live entertainment, and music expanding faster than the overall 7.28% market CAGR, driven by global OTT platform adoption, rising premium fan engagement, and growing international streaming royalties.

Executive Summary

The Japan anime market is on a sustained growth trajectory from USD 1.51 Billion in 2020 to USD 4.12 Billion by 2034. The industry has transitioned from a primarily domestic entertainment sector into a globally recognized cultural export, generating revenue across merchandising, streaming, theatrical releases, home video, music, Pachinko licensing, and live entertainment.

Merchandising dominates the revenue source segment at 30.4% in 2025, supported by long-running franchise IP spanning toys, apparel, collectibles, and branded merchandise. Kanto Region commands 36.7% of regional share, anchored by the concentration of major animation studios and digital infrastructure in the Greater Tokyo metropolitan area. In March 2026, Kadokawa revealed intentions to create a new anime production center named ‘Studio One Base.’ The venue is set to be situated within the Sunshine City complex in Ikebukuro, a prominent entertainment area in northwestern Tokyo, and is expected to launch in autumn 2026.

Key Market Insights

|

Insight |

Data |

|

Leading Revenue Source |

Merchandising - 30.4% share (2025) |

|

Second Largest Revenue Source |

Internet Distribution - 24.7% share (2025) |

|

Leading Region |

Kanto Region - 36.7% share (2025) |

|

Second Largest Region |

Kansai/Kinki Region - 18.6% share (2025) |

|

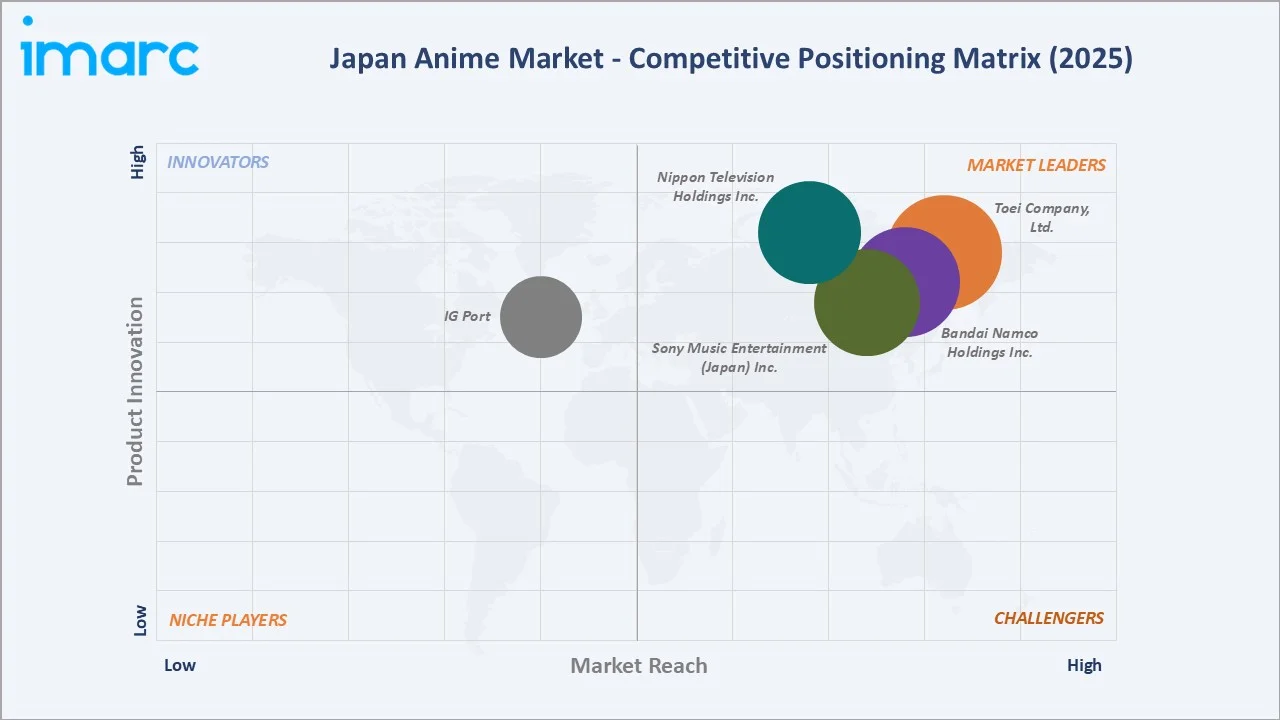

Top Companies |

Toei Company, Ltd., Bandai Namco Holdings Inc., Sony Music Entertainment (Japan) Inc., Nippon Television Holdings Inc., IG Port |

Key Analytical Observations Expanding On The Data Above:

- Merchandising dominance at 30.4% reflects the deep commercial embed of anime IP across consumer goods categories. Long-running franchises generate consistent royalty streams from toys, trading cards, limited-edition collectibles, and licensed apparel, with franchise longevity reducing per-unit marketing costs over time.

- Internet distribution at 24.7% is the second largest revenue source in the market, driven by the widespread adoption of subscription-based streaming platforms, growing accessibility of anime content, and increasing consumer preference for on-demand digital viewing across multiple devices.

- Kanto Region at 36.7% leads regional share, anchored by the Greater Tokyo metropolitan area's concentration of leading animation studios, production infrastructure, digital platform offices, and a large base of domestic anime consumers in Japan.

Japan Anime Market Overview

Anime refers to a style of hand-drawn and computer-generated animation originating in Japan, encompassing a broad spectrum of genres, including action, romance, fantasy, science fiction, horror, and slice-of-life. The Japan anime market spans the full commercial ecosystem from original IP creation, animation production, and content licensing through to consumer distribution across television broadcasting, theatrical release, home video, streaming platforms, physical merchandise, music publishing, and live event experiences.

The ecosystem integrates content creators, including mangaka and light novelists, animation production studios, voice acting agencies, music labels, licensing and distribution companies, broadcast networks, streaming platforms, merchandise manufacturers, retail channels, and fan communities. Together these stakeholders enable the delivery of anime content and related consumer experiences across both domestic and international markets, within an evolving commercial framework shaped by digital transformation and global audience expansion.

Market Dynamics

To evaluate market opportunities, Request Sample

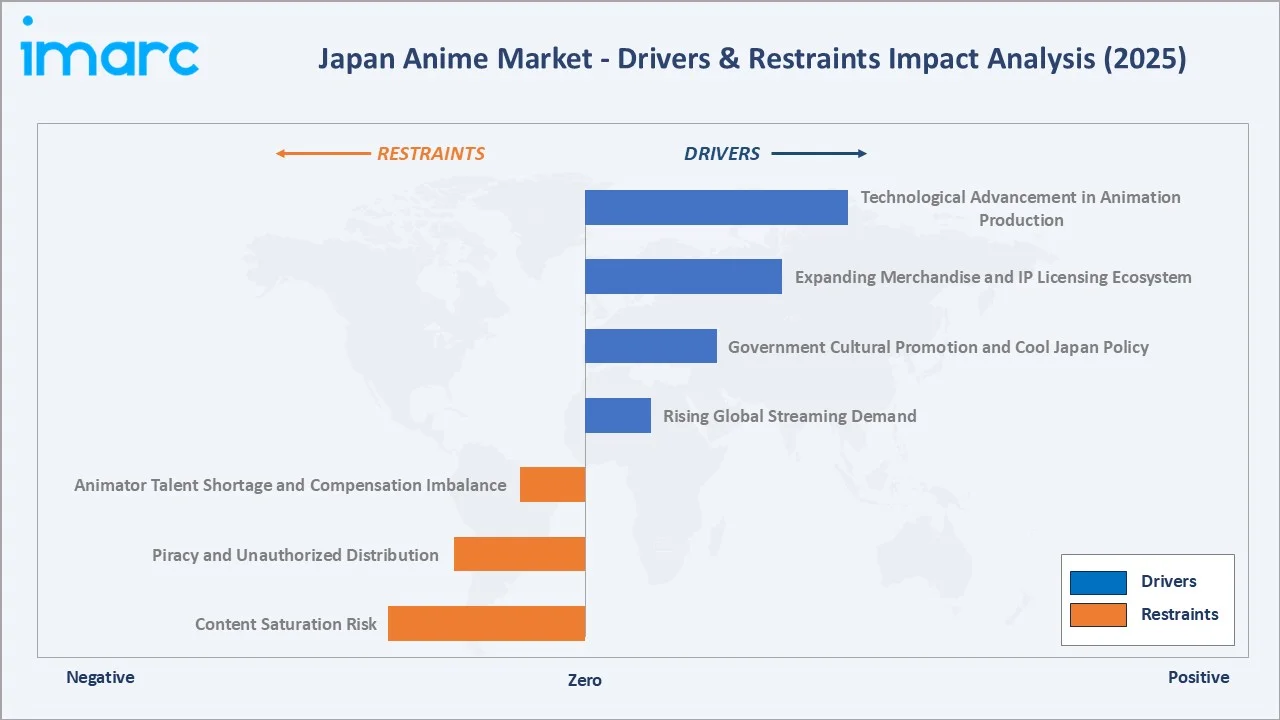

Market Drivers

- Rising Global Streaming Demand: The proliferation of subscription video-on-demand (SVOD) platforms has fundamentally transformed anime distribution economics. Global OTT operators have invested heavily in anime content libraries and original productions.

- Government Cultural Promotion and Cool Japan Policy: The Japanese government's Cool Japan initiative has provided institutional support for the anime industry through international promotion, export assistance, content localization efforts, overseas market development programs, and strategic investments in creative industries.

- Expanding Merchandise and IP Licensing Ecosystem: Anime IP has emerged as one of the most commercially versatile licensing categories in global consumer goods. Major studios routinely generate revenues multiple times their production budgets through merchandise licensing across toys, video games, apparel, stationery, and branded food and beverage.

- Technological Advancement in Animation Production: The adoption of computer-generated imagery, digital animation tools, cloud-based production workflows, and artificial intelligence (AI) for background generation, in-between frame automation, and quality control is improving output quality while reducing production cycle times. As per IMARC Group, the Japan AI market size was valued at USD 7.9 Billion in 2025.

Market Restraints

- Animator Talent Shortage and Compensation Imbalance: Japan's animation industry faces a chronic talent bottleneck. Low entry-level wages, demanding production schedules, and an aging workforce have contributed to recruitment and retention challenges, constraining production capacity and increasing operational pressure on animation studios.

- Piracy and Unauthorized Distribution: Despite advances in digital rights management and global takedown enforcement, anime piracy remains a material revenue drag. Unauthorized streaming and download platforms, particularly in regions with limited legal anime access, undermine direct subscription revenues and reduce potential merchandise conversion rates. The persistence of gray-market consumption in several high-growth emerging markets limits the addressable commercial opportunity for rights holders and licensed platform operators.

- Content Saturation Risk: The increasing volume of anime titles produced per season has led to audience selection overload and declining average viewership per title. This saturation risk pressures studios to invest more in marketing and franchise recognition, increasing per-title commercial risk and compressing returns on investment for mid-tier productions that lack established franchise recognition.

Market Opportunities

- Expansion of Internet Distribution and Global OTT Partnerships: The continued expansion of anime-focused streaming agreements with global SVOD platforms represents the most significant near-term revenue opportunity for Japanese studios and rights holders.

- Live Entertainment and Immersive Fan Experiences: Anime-themed concerts, stage productions, immersive exhibitions, themed cafes, and location-based entertainment attractions represent a structurally high-margin segment with strong growth potential.

Market Challenges

- Exchange Rate Volatility: Given the significant share of revenues derived from international licensing, overseas retail, and global streaming arrangements, the Japan anime market is sensitive to yen fluctuations. A stronger yen erodes the competitiveness of export pricing and compresses the yen-denominated value of foreign currency receipts, reducing effective margins for studios and distributors with substantial international exposure.

- Offshore Competition and Rising Production Costs: Competition from Korean webtoon adaptations, Chinese animation productions, and Western studios experimenting with anime-adjacent visual styles is introducing alternative content sources that may compete for some audience segments and streaming platform investment. Simultaneously, rising voice talent, CGI, and senior animator costs are compressing per-episode production budgets, requiring studios to optimize across larger production slates.

Emerging Market Trends

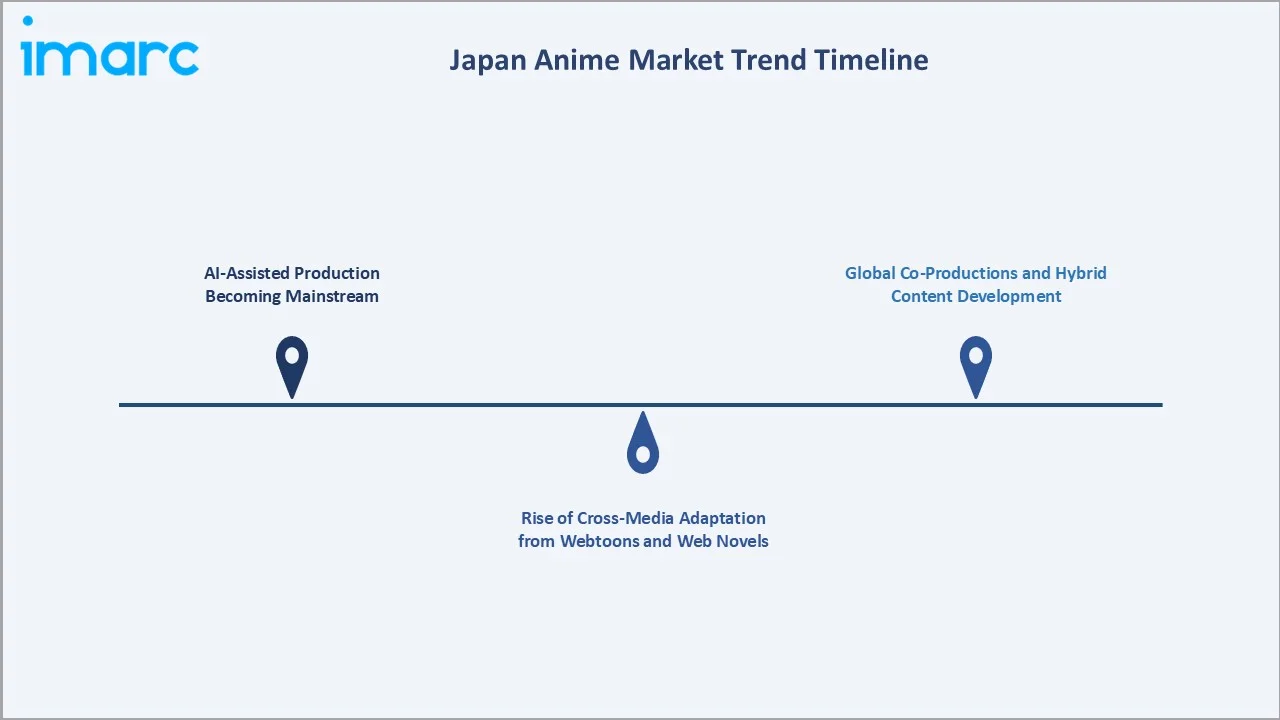

1. AI-Assisted Production Becoming Mainstream

AI tools are being systematically integrated across the anime production pipeline, from background art generation to automated in-between frame rendering and quality control. AI-assisted workflows are helping studios reduce production timelines, alleviate labor shortages, and improve cost efficiency, enabling creators to focus more resources on storytelling, character development, and high-value artistic tasks.

2. Rise of Cross-Media Adaptation from Webtoons and Web Novels

A growing pipeline of anime adaptations is being sourced from Korean webtoons and Japanese web novels published on digital platforms, diversifying the traditional manga-to-anime pipeline. This cross-media trend expands the universe of adaptable IP and introduces fresh narrative formats that appeal to demographics engaged with web-based serialized content, broadening the potential audience for new anime productions.

3. Global Co-Productions and Hybrid Content Development

Japanese studios are increasingly entering co-production agreements with North American, European, and Asian media companies to develop anime that blends Japanese aesthetics with internationally appealing narratives. These hybrid productions reduce per-territory marketing costs, facilitate pre-sale licensing, and help de-risk production financing by securing committed international broadcast and streaming deals before production completion.

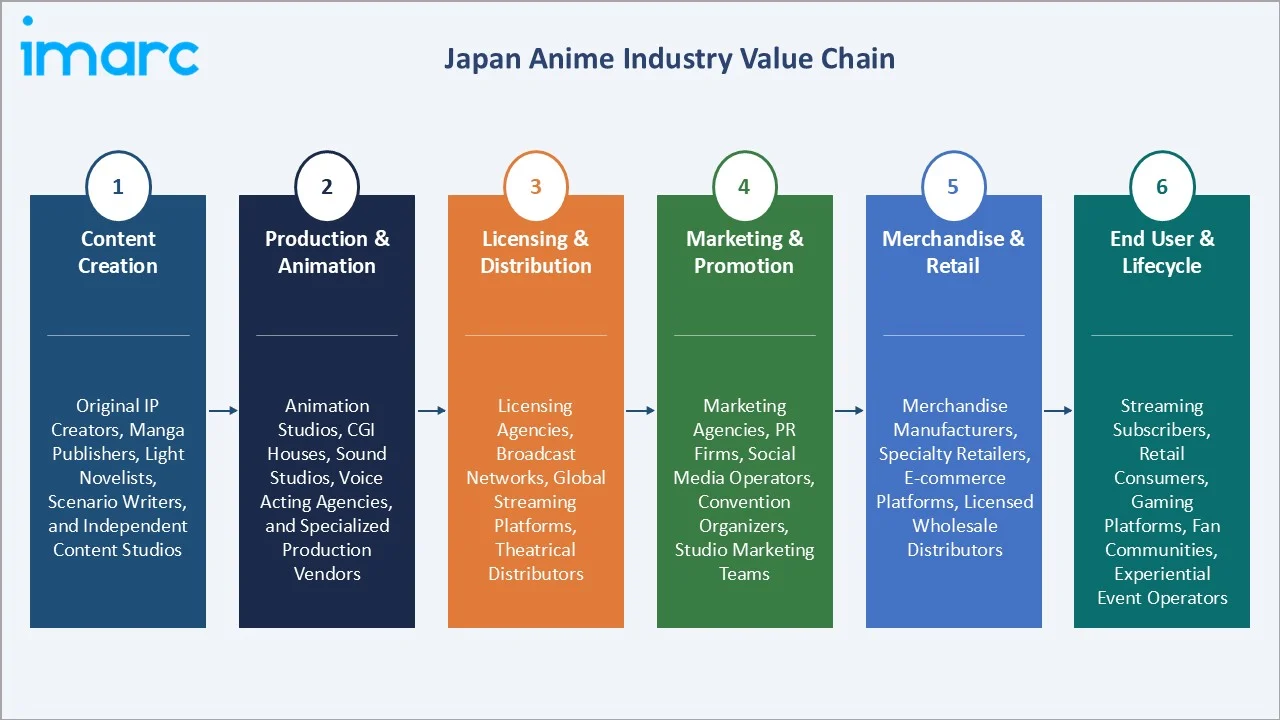

Industry Value Chain Analysis

The Japan anime industry value chain spans six integrated stages from original IP creation through to end user engagement, encompassing content development, production, licensing, marketing, retail distribution, and fan lifecycle management. Technology and platform infrastructure, IP licensing, and marketing capture the highest value-add, while compliance, quality standards, and creator relationships increasingly determine competitive position.

|

Stage |

Key Players / Examples |

|

Content Creation |

Original IP creators, manga publishers, light novelists, scenario writers, and independent content studios |

|

Production & Animation |

Animation studios, CGI houses, sound studios, voice acting agencies, and specialized production vendors |

|

Licensing & Distribution |

Licensing agencies, broadcast networks, global streaming platforms, theatrical distributors |

|

Marketing & Promotion |

Marketing agencies, PR firms, social media operators, convention organizers, studio marketing teams |

|

Merchandise & Retail |

Merchandise manufacturers, specialty retailers, e-commerce platforms, licensed wholesale distributors |

|

End User & Lifecycle |

Streaming subscribers, retail consumers, gaming platforms, fan communities, experiential event operators |

Leading anime companies with recognized franchises, extensive merchandising networks, streaming platform partnerships, and international licensing capabilities maintain stronger market presence and monetization opportunities than smaller niche studios.

Technology Landscape in the Japan Anime Industry

AI-Assisted Animation and Production Technology

AI is reshaping the anime production pipeline from pre-production through post-production. Studios are deploying AI tools for automated in-between frame generation, background art synthesis, and real-time rendering, reducing manual labor requirements at key production stages. Computer-generated imagery integration with hand-drawn animation has become standard across mid-tier and premium productions, enabling higher-quality visual output at competitive cost structures.

Digital Distribution and Streaming Infrastructure

Cloud-based content delivery networks and adaptive streaming protocols underpin global anime distribution. Digital platforms have invested in region-specific CDN infrastructure to support simultaneous global simulcast releases. Digital rights management systems have also matured, enabling granular geo-based licensing enforcement and real-time analytics that inform content investment decisions for both studios and platform operators.

Merchandise Digitization and E-Commerce Technology

The merchandise segment is undergoing technology-driven transformation through e-commerce platforms, direct-to-consumer digital storefronts, and limited-edition NFT-based digital collectibles. Augmented reality (AR) tools are being piloted for virtual merchandise previews, while AI-based demand forecasting is improving inventory management for licensed goods manufacturers, reducing overstock risk on seasonal franchise merchandise releases.

Immersive and Location-Based Experience Technology

Location-based entertainment venues are deploying projection mapping, spatial audio, and interactive AR installations to create immersive anime-themed visitor experiences. These technologies deepen fan engagement beyond passive content consumption and command premium admission pricing, expanding the industry's revenue mix beyond traditional broadcast and merchandise channels.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Revenue Source | Merchandising |

30.4% |

2025 |

|

Region |

Kanto Region |

36.7% |

2025 |

By Revenue Source

Merchandising commands 30.4% of the market in 2025, driven by the commercial depth of established anime IP across licensed consumer goods globally. The segment's high share reflects anime's unique characteristic as a cultural IP category that translates exceptionally well into physical consumer products, particularly limited-edition and collector-grade merchandise that commands premium pricing.

To access detailed market analysis, Request Sample

Internet distribution at 24.7% in 2025 is the market's second largest revenue source, driven by global SVOD expansion, simulcast delivery, and the structural migration of younger audiences to on-demand consumption. The segment's economics are improving as platform scale enables more favorable per-title licensing economics and as studios structure streaming rights as a primary rather than secondary distribution window.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

36.7% |

High concentration of animation studios; dense urban consumer base; strongest digital infrastructure and retail network for anime products |

|

Kansai/Kinki Region |

18.6% |

Major population center; established entertainment industry; strong consumer spending; key cultural tourism circuits |

|

Central/Chubu Region |

14.8% |

Growing merchandise manufacturing base; rising consumer income; expanding retail and e-commerce penetration |

|

Kyushu-Okinawa Region |

9.4% |

Tourism-linked anime consumption; rising youth population; growing presence of regional anime events and festivals |

|

Tohoku Region |

7.3% |

Steady consumer spending; regional cultural promotion initiatives; expanding broadband supporting digital distribution |

|

Chugoku Region |

5.5% |

Stable consumer base; growing anime-themed tourism tied to regional cultural heritage and local studio presence |

|

Hokkaido Region |

4.3% |

Loyal niche consumer base; seasonal tourism supporting limited-edition merchandise; growing digital streaming adoption |

|

Shikoku Region |

3.4% |

Smallest regional share; opportunities in digital distribution as connectivity infrastructure improves |

Kanto Region at 36.7% in 2025 leads the regional landscape, anchored by Tokyo's position as Japan's animation capital and home to the country's largest domestic anime consumer base. The region's mature digital ecosystem, premium retail environment, and concentration of all major studio and licensing operations sustain its structural leadership across both production and commercial activity.

Kansai/Kinki Region at 18.6% is the second-largest market, driven by Osaka and Kyoto's established media and entertainment infrastructure, strong consumer spending, and proximity to key cultural tourism destinations.

Competitive Landscape

The Japan anime market features a mix of large integrated entertainment conglomerates and specialist independent production studios. Competitive position is defined by IP ownership, franchise longevity, production capacity, distribution relationships, and international licensing reach. The market is moderately consolidated at the top, with a small number of well-capitalized studios controlling the most commercially valuable franchise portfolios, while a large ecosystem of independent studios competes on creative differentiation and niche audience appeal.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

|

Toei Animation (Dragon Ball, One Piece) |

Leader |

Franchise expansion and global IP licensing |

|

|

Bandai Namco Filmworks (Gundam) |

Leader |

Cross-media IP monetization and merchandise expansion |

|

Sony Music Entertainment (Japan) Inc. |

Demon Slayer, Sword Art Online |

Leader |

International streaming deals and original content investment |

|

|

Studio Ghibli (Spirited Away, My Neighbor Totoro) |

Leader |

Theatrical releases and global streaming expansion |

|

IG Port |

Production I.G (Haikyuu!!) |

Innovator |

International market expansion and co-production partnerships |

Key players include Toei Company, Ltd., Bandai Namco Holdings Inc., Sony Music Entertainment (Japan) Inc., Nippon Television Holdings Inc., and IG Port, among others.

Key Company Profiles

Toei Company, Ltd.

Toei Company, Ltd. is a diversified Japanese entertainment conglomerate. The company operates across film production, television, live events, theme parks, and character licensing.

- Product Portfolio: Toei Animation (Dragon Ball, One Piece); multi-generational franchise IP with global licensing, theatrical releases, and merchandise.

- Recent Developments: Toei Company, Ltd. relocated its headquarters to Kyobashi Edogrand in July 2025. The company has also continued strengthening its content distribution and licensing activities, leveraging its established anime franchises across streaming, theatrical, and merchandising channels.

- Strategic Focus: Expanding multi-generational anime IP globally through theatrical releases, SVOD licensing, and merchandise partnerships.

Bandai Namco Holdings Inc.

Bandai Namco Holdings Inc. is a leading Japanese entertainment conglomerate with operations spanning toy manufacturing, video game development, amusement facilities, and visual content production.

- Product Portfolio: Bandai Namco Filmworks (Gundam); anime production, merchandise licensing, gaming, and live events across global markets.

- Recent Developments: Bandai Namco Holdings has been strengthening anime IP monetization across gaming, streaming, and merchandise channels, and expanding its international presence through licensing and retail partnerships.

- Strategic Focus: Driving anime IP value across gaming, toys, collectibles, streaming, and amusement through an integrated group ecosystem.

Nippon Television Holdings Inc.

Nippon Television Holdings Inc. is a publicly listed Japanese broadcaster. The company operates across television broadcasting, content production, digital media, and entertainment events, with Studio Ghibli representing its most internationally associated content asset.

- Product Portfolio: Studio Ghibli (Spirited Away, My Neighbor Totoro); globally recognized theatrical anime films and premium merchandise.

- Recent Developments: Nippon Television Holdings has been expanding Studio Ghibli's reach across live entertainment, stage productions, and international streaming.

- Strategic Focus: Preserving and extending Studio Ghibli's prestige IP through international film distribution, live events, and branded experiences.

Market Concentration Analysis

The Japan anime market is moderately concentrated at the top tier, with the leading five players - Toei Company, Ltd., Bandai Namco Holdings Inc., Sony Music Entertainment (Japan) Inc., Nippon Television Holdings Inc., and IG Port - collectively controlling the most commercially valuable IP portfolios and commanding the strongest international licensing relationships in the industry.

Barriers to entry in the premium segment include high IP development costs, extended franchise-building timelines, deep established relationships with broadcast and streaming platforms, and the need for significant production infrastructure investment. These factors favor well-capitalized incumbents with proven franchise portfolios.

Consolidation is gradual but ongoing, with larger entertainment conglomerates acquiring specialist production studios and content libraries to secure IP ownership and production capacity. Strategic partnerships between studios and global streaming platforms are reinforcing competitive positioning for operators with strong content pipelines and established fan audiences.

Investment & Growth Opportunities

Fastest-Growing Segments

Internet distribution, with a projected CAGR above the overall 7.28% market rate through 2034, represents the highest-growth revenue segment, driven by continued global OTT investment in anime content libraries and the structural migration of consumption from broadcast to on-demand digital platforms. Live entertainment, though smallest in share at 2.8%, is expanding rapidly as studios invest in proprietary event IP.

Emerging Markets

Kansai/Kinki Region represents the largest opportunity in the Japan anime market due to their concentration of animation studios, media companies, and large consumer bases. Meanwhile, Central/Chubu Region, Kyushu-Okinawa Region, and Tohoku Region are emerging growth regions, supported by rising digital content consumption, anime tourism, and expanding merchandise demand.

Venture & Investment Trends

Investment is concentrating in digital animation technology, including AI-assisted production tools, cloud-based rendering infrastructure, and real-time collaboration platforms. Capital is also flowing into anime-focused streaming platforms targeting underserved international markets, premium live entertainment and fan experience concepts, and cross-media IP development that bridges anime with mobile gaming and NFT-based digital collectibles.

Future Market Outlook (2026-2034)

The Japan anime market is forecast to expand from USD 2.15 Billion in 2025 to USD 4.12 Billion by 2034 at a CAGR of 7.28%, adding roughly USD 1.97 Billion in incremental annual market value over the forecast period, equivalent to nearly doubling the current market size within a decade.

Four forces will define the market through 2034: the continued ascent of internet distribution at the expense of traditional broadcast; expanding international licensing revenue from global streaming and merchandise agreements; AI-assisted production enabling higher output without proportional cost escalation; and the maturation of live entertainment and immersive fan experience as a structurally distinct premium revenue stream.

By 2034, the Japan anime market is expected to be characterized by a more balanced revenue structure, with internet distribution closing the gap with merchandising as the leading revenue source, and live entertainment growing its share as studios invest in permanent and seasonal fan experience attractions globally. Regulatory developments, IP protection enforcement improvements in key international markets, and continued digital infrastructure investment are expected to further accelerate the formalization of the global anime consumption ecosystem.

Research Methodology

Primary Research

Primary research included structured engagements with animation studio executives, licensing and distribution specialists, streaming platform content managers, merchandise retail operators, and fan event organizers. These inputs validated market sizing, segment evolution dynamics, regional demand patterns, and revenue source trends across the forecast period.

Secondary Research

Secondary sources included the Association of Japanese Animations (AJA) annual industry data publications, Ministry of Economy Trade and Industry (METI) cultural industry statistics, Japan External Trade Organization (JETRO) export data, annual reports and investor presentations from listed animation studios and entertainment conglomerates, streaming platform earnings disclosures, and specialized entertainment industry trade publications.

Forecasting Models

Market forecasts utilized top-down and bottom-up modelling frameworks, combining domestic consumption data by revenue segment, international licensing revenue trajectories, digital platform subscriber and revenue-per-user evolution, and macroeconomic variables including consumer spending trends and exchange rate assumptions. Scenario analysis addressed regulatory developments, technology adoption pace, and international market expansion scenarios.

Japan Anime Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Revenue Sources Covered | T.V., Movie, Video, Internet Distribution, Merchandising, Music, Pachinko, Live Entertainment |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Toei Company Ltd., Bandai Namco Holdings Inc., Sony Music Entertainment (Japan) Inc., Nippon Television Holdings Inc., IG Port, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan anime market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan anime market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan anime industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Anime Market Report

The Japan anime market was valued at USD 2.15 Billion in 2025, driven by merchandising revenues, expanding global streaming distribution, and growing international licensing of Japanese animation IP.

The market is projected to grow at a CAGR of 7.28% during 2026-2034, reaching USD 4.12 Billion, supported by internet distribution expansion, merchandise ecosystem growth, and rising global fan communities.

Merchandising leads at 30.4% in 2025, driven by licensed consumer goods across toys, apparel, and collectibles tied to long-running franchise IP.

Kanto Region leads at 36.7% in 2025, anchored by the Greater Tokyo area's concentration of studios, distribution infrastructure, and the largest domestic anime consumer base in Japan.

Leading players include Toei Company, Ltd., Bandai Namco Holdings Inc., Sony Music Entertainment (Japan) Inc., Nippon Television Holdings Inc., and IG Port, among others.

Global SVOD platform investment in anime libraries, simulcast delivery models, and the structural migration of younger audiences to on-demand digital consumption are the primary drivers of internet distribution growth.

AI-assisted tools for background generation, in-between frame automation, and quality control are reducing production labor hours, enabling studios to maintain output volumes without proportional headcount increases.

Key challenges include a chronic animator talent shortage, persistent piracy in international markets, content saturation from high production volumes, and exchange rate sensitivity for export revenues.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)