Japan Battery Market Size, Share, Trends and Forecast by Type, Product, Application, and Region, 2026-2034

Japan Battery Market Size & Forecast 2026-2034

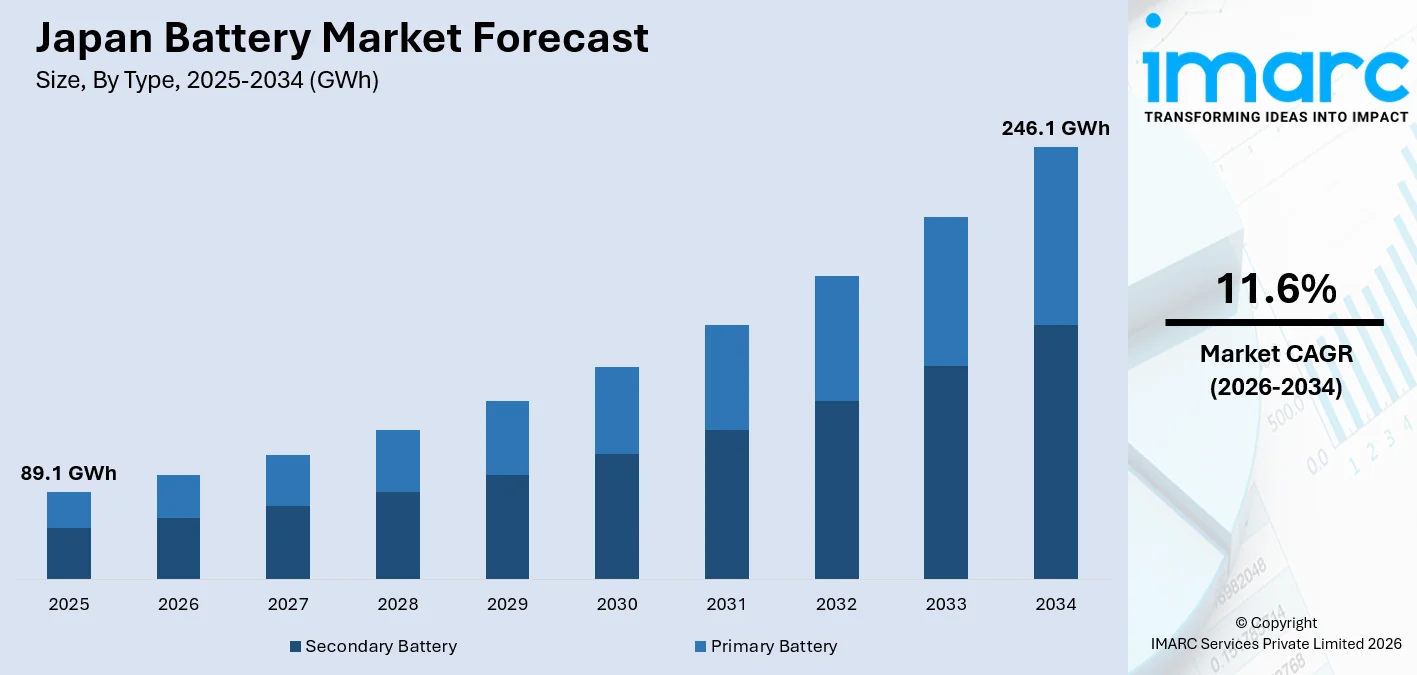

The Japan Battery market size, volumed at 89.1 GWh in 2025, is projected to reach 246.1 GWh by 2034, growing at a CAGR of 11.6% from 2026-2034, driven by Japan’s carbon neutrality commitments and accelerating EV adoption, prompting substantial government and corporate investment in domestic battery capacity and zero-emission transportation goals. In March 2025, Ample, Mitsubishi Fuso Truck and Bus Corporation, and Mitsubishi Motors Corporation deployed battery swapping stations across Tokyo, underpinning the Japan battery market share.

To get more information on this market Request Sample

Japan Battery Industry Analysis- Key Insights

- Secondary battery commands 88.0% of market share by type in 2025 - its rechargeable design is structurally indispensable for EV powertrains, industrial storage, and consumer electronics, and manufacturing scale keeps driving per-unit costs lower with each capacity expansion cycle.

- Lithium-ion leads product share at 51.0% in 2025 - its superior energy density, long cycle life, and cross-application compatibility from EV packs to grid storage make it the default chemistry across Japan’s entire battery ecosystem, ahead of lead-acid and nickel variants.

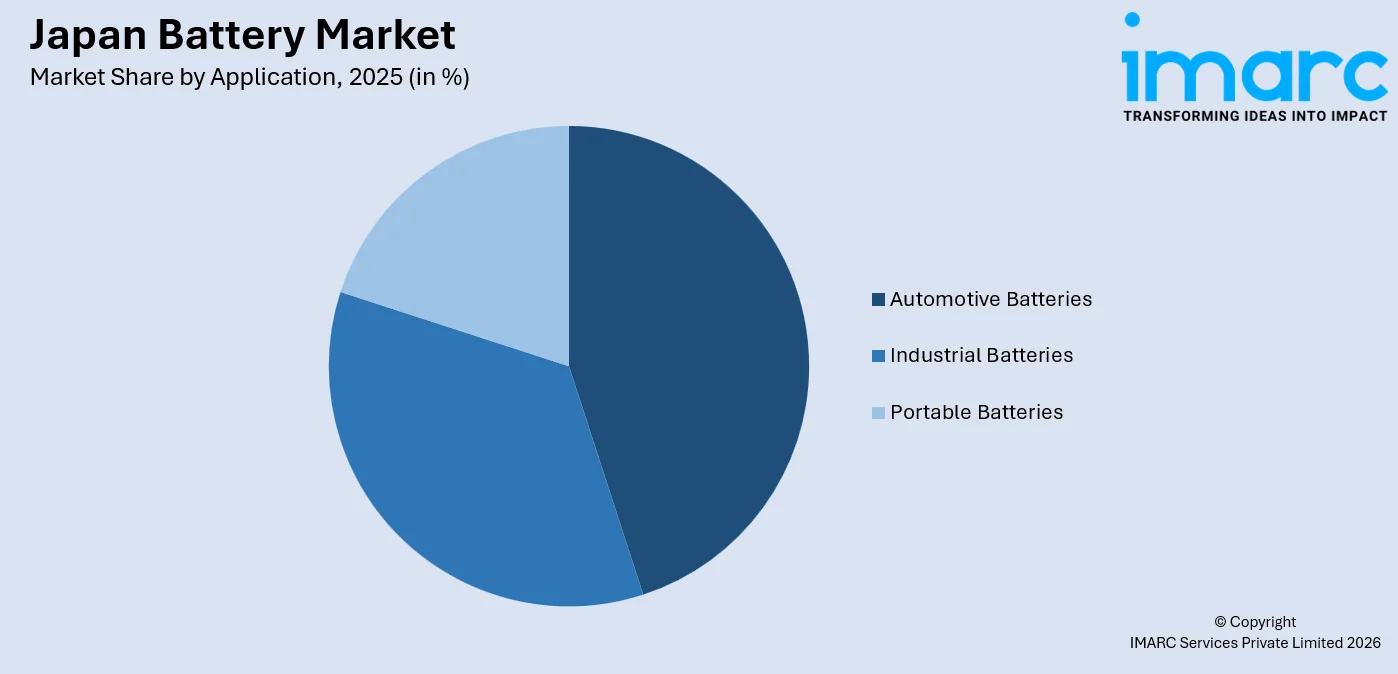

- Automotive batteries hold 45.0% application share in 2025 - Japan’s vehicle electrification push, backed by government subsidies and major automaker capital commitments, ensures automotive demand remains the single largest consumption driver by a wide margin over industrial and portable categories.

- Kanto Region leads regionally at 42.0% in 2025 - the concentration of major automakers, technology conglomerates, and Tokyo’s advanced industrial infrastructure makes this region the undisputed battery manufacturing, R&D, and consumption hub in Japan, anchoring nearly half of national demand.

Japan Battery Market Trends and Dynamic 2026

Market Trends

Next-generation battery innovation is transforming Japan’s technology roadmap

Japan battery market is at the forefront of next-generation cell development, with manufacturers investing heavily in solid-state and anode-free chemistries to overcome energy density and safety limitations of conventional lithium-ion technology. In September 2025, Panasonic Energy revealed a new anode-free lithium-ion battery production process that eliminates the anode during manufacturing, with commercial availability targeted by end-2027.

Residential energy storage is accelerating on the back of policy-driven solar mandates

Tokyo’s 2025 regulation mandating solar panels on all new homes has created a structural surge in demand for home battery systems. Rental listings that include solar panels recorded a 253% year-over-year increase in 2024, and the planned launch of Virtual Power Plant (VPP) programs in fiscal 2026 will further amplify the adoption of home energy storage, supporting sustained Japan Battery market growth through the forecast period.

- Solid-State Battery Commercialization: Japanese automakers and cell producers are accelerating solid-state development timelines, with Toyota targeting pilot sulphide solid-state output by 2027 and Idemitsu Kosan expanding its electrolyte manufacturing facility in Tokyo.

- Smart Battery Management Integration: Growing adoption of AI-enabled battery management systems in EV packs and stationary storage is improving cycle life, real-time monitoring, and predictive safety across Japan’s battery ecosystem.

- Grid-Scale Battery Deployment: Utility-scale battery installations are rapidly scaling to support Japan’s renewable energy integration and grid stabilization goals, with project pipelines growing substantially through 2030.

- Battery Second-Life Applications: Repurposing retired automotive battery packs for stationary energy storage is gaining traction in Japan, supported by government circular economy policies and manufacturers’ interest in extending battery value chains.

Growth Drivers

Government policy support and strategic manufacturing subsidies

Japan’s Ministry of Economy, Trade and Industry (METI) committed around USD 2 billion subsidy package in 2024 to fund 12 battery production projects, including those by Toyota, Nissan, and Panasonic, to expand Japan’s annual battery manufacturing capacity from 80 GWh to 120 GWh by 2030. These initiatives reflect the scale of public investment driving Japan's battery market trends toward self-sufficient, high-volume domestic production.

Japan’s vehicle electrification mandate and clean energy incentives

Electric vehicle (EV) subsidies increased from 900,000 yen (USD 5,700) to 1.30 million yen starting in January 2026, providing stronger support for the sector. Eco-Car Tax Reductions, weight tax exemptions, and acquisition tax benefits further lower consumer purchase barriers, underpinning durable OEM demand for automotive battery cells and reinforcing a positive Japan battery market forecast.

Renewable energy integration and grid storage infrastructure expansion

Japan’s decarbonization agenda is driving substantial investment in grid-scale battery storage alongside solar and offshore wind expansion. Panasonic, in partnership with Subaru, is developing a joint battery plant in Gunma Prefecture targeting 20 GWh of annual production capacity by 2030, backed by government subsidies, directly expanding the country’s storage infrastructure to balance variable renewable energy supply across the national grid.

- EV Fleet Electrification: Corporate and municipal EV fleet operators are scaling up battery procurement, supported by subsidy programs and infrastructure investments across Japan’s major urban centers.

- Consumer Electronics Demand: Japan’s advanced electronics sector sustains consistent lithium-ion demand across smartphones, laptops, hearables, and wearable devices from major domestic and international OEMs.

- Industrial and Data Centre Backup Power: Expanding data center infrastructure and critical industrial facilities are generating reliable demand for high-performance industrial battery systems and uninterruptible power supply solutions.

- Strategic R&D Investment: Targeted funding through METI’s Green Innovation Fund is accelerating next-generation battery commercialization timelines, attracting global technology partnerships to Japan’s battery R&D ecosystem.

Market Restraints

Critical mineral import dependence: Japan relies heavily on imported lithium, cobalt, and graphite for battery manufacturing, with sourcing concentrated among a limited number of overseas suppliers. This structural vulnerability to geopolitical disruptions and supply chain instability poses ongoing challenges for domestic battery production continuity and cost management.

High capital requirements for advanced manufacturing transitions: The shift to solid-state and next-generation battery technologies demands substantial capital investment in new production equipment, facility modifications, and process engineering. These elevated upfront costs create significant financial barriers, particularly for mid-sized domestic producers without large balance sheet capacity.

Underdeveloped EV charging infrastructure constraining consumer adoption: Japan’s public charging network remains insufficient relative to the pace of EV policy ambitions, with significant geographic gaps and a dominance of low-speed AC units that limit commercial fleet operators and discourage long-distance electric mobility adoption among price-sensitive consumers.

Japan Battery Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Secondary Battery | 88.0% | 2025 |

| Product | Lithium-Ion | 51.0% | 2025 |

| Application | Automotive Batteries | 45.0% | 2025 |

| Region | Kanto Region | 42.0% | 2025 |

Type Insights

Secondary Battery – 88.0% Market Share (2025) | Leading Type

Secondary batteries dominate Japan battery market due to their rechargeable nature, enabling repeated charge-discharge cycles essential for electric vehicles, energy storage systems, and consumer electronics. In May 2025, TDK Corp, Japan’s precision electronics manufacturer, began introducing its next-generation silicon anode batteries, which are expected to significantly improve secondary battery energy density and charge retention across automotive and portable device applications.

|

Segment Breakdown Secondary Battery (88.0%) · Primary Battery |

Product Insights

Lithium-Ion - 51.0% Market Share (2025) | Leading Product

Lithium-ion batteries lead Japan battery market by product, driven by their high energy density, long cycle life, and established compatibility across EV, industrial, and consumer electronics applications. As of September 2025, Panasonic Energy had cumulatively supplied approximately 20 billion lithium-ion EV batteries globally, underscoring the technology’s safety record and reinforcing its dominant position in the Japan battery market.

|

Segment Breakdown Lithium-Ion (51.0%) · Lead Acid · Nickel Metal Hydride · Nickel Cadmium · Others |

Application Insights

Access the comprehensive market breakdown Request Sample

Automotive Batteries - 45.0% Market Share (2025) | Leading Application

Automotive batteries represent the largest demand category in Japan's battery market, driven by the country’s accelerating push toward vehicle electrification. In January 2025, Mazda Motor Corporation announced plans to establish a lithium battery module pack factory in Yamaguchi, Japan. With 10 GWh annual manufacturing capacity to produce packs and modules for automotive cylindrical lithium-ion cells sourced from Panasonic Energy Co., Ltd.

|

Segment Breakdown Automotive Batteries (45.0%) · Industrial Batteries · Portable Batteries |

Regional Insights

Kanto Region - 42.0% Market Share (2025) | Leading Region

The Kanto Region commands the largest share of the Japan battery market, underpinned by the concentration of major automotive manufacturers, electronics companies, and Tokyo’s advanced technology research hubs. In November 2025, Panasonic Energy Co., Ltd. signed a multi-year agreement with Zoox to supply cylindrical 2170 lithium-ion batteries from early 2026, reinforcing the Kanto region’s role as the country’s premier battery supply origination hub.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

42.0%

|

|

Key States

|

Tokyo, Kanagawa, Chiba, Saitama, Ibaraki |

|

Major Growth Drivers

|

Automotive manufacturing hubs, technology R&D concentration, EV policy mandates, residential energy storage adoption |

|

Outlook

|

Dominant and fastest-expanding regional battery hub |

|

Regional Breakdown Kanto Region (42.0%) · Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kinki Region:

The Kinki Region is Japan’s second major battery manufacturing center, anchored by Panasonic Corporation’s Osaka headquarters, which governs the company’s global battery strategy. GS Yuasa’s solid-state battery pilot operations in Shiga Prefecture support Japan’s battery market through advanced R&D capabilities, strategic manufacturing investments, and next-generation battery technology development.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Osaka, Kyoto, Hyogo, Shiga, Nara |

|

Major Growth Drivers

|

Battery manufacturer headquarters, solid-state R&D, automotive OEM supply chains, export logistics via Osaka |

|

Outlook

|

Core strategic R&D and manufacturing direction hub |

Central/Chubu Region:

The Central/Chubu Region is the heartland of Japan’s automotive industry, with Toyota City (Aichi Prefecture) serving as the global headquarters of Toyota Motor Corporation. Toyota is investing approximately 245 billion yen to add 9 GWh of annual capacity for solid-state and prismatic batteries through its Prime Planet Energy & Solutions subsidiary, with full-scale production scheduled to begin by November 2026, directly expanding Chubu’s role in Japan’s automotive battery production center.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Aichi, Shizuoka, Nagano, Gifu, Niigata |

|

Major Growth Drivers

|

Toyota manufacturing ecosystem, automotive OEM battery procurement, solid-state commercialization, government manufacturing subsidies |

|

Outlook

|

Automotive battery production powerhouse |

Kyushu-Okinawa Region:

The Kyushu-Okinawa Region is a growing center for grid-scale battery storage deployment, benefiting from abundant solar and wind energy resources that require advanced storage to balance intermittency. The region is also attracting investments in large-scale energy storage systems and battery manufacturing projects to support Japan’s renewable energy expansion and grid stability.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Fukuoka, Kumamoto, Oita, Kagoshima, Okinawa |

|

Major Growth Drivers

|

Renewable energy integration, utility-scale BESS deployment, semiconductor and electronics manufacturing, regional decarbonization policy |

|

Outlook

|

Renewable energy-led battery storage growth |

Tohoku Region:

The Tohoku Region’s battery sector is shaped by post-Fukushima energy security imperatives and the government’s long-term decarbonization commitments. With Tohoku’s grid resilience requirements positioning the region as a key deployment zone for industrial and grid-scale battery systems supporting renewable energy integration and emergency backup power for critical infrastructure.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Miyagi, Fukushima, Iwate, Yamagata, Aomori |

|

Major Growth Drivers

|

Grid resilience investment, renewable energy storage, battery recycling development, post-disaster energy security |

|

Outlook

|

Energy security and grid resilience focus |

Chugoku Region:

The Chugoku Region is emerging as a center for automotive battery manufacturing and energy storage innovation. In August 2025, Toyota and Mazda began field tests of the Sweep Energy Storage System at Mazda’s Hiroshima Plant, connecting EV batteries to the facility’s electrical infrastructure to verify stable, efficient charging and test second-life battery integration.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Hiroshima, Okayama, Yamaguchi, Shimane |

|

Major Growth Drivers

|

Automotive manufacturing integration, EV battery field testing, second-life battery development, vehicle-to-grid technology |

|

Outlook

|

Automotive battery integration and circular economy hub |

Hokkaido Region:

Hokkaido’s battery market is driven by the region’s strong push toward renewable energy integration and grid modernization. Hokkaido’s cold climate and geographic isolation from the main grid further reinforce the strategic importance of local battery storage infrastructure for energy security.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Hokkaido |

|

Major Growth Drivers

|

Renewable energy grid support, cold-climate energy storage, regional grid isolation management, distributed BESS deployment |

|

Outlook

|

Renewable-driven grid storage expansion |

Shikoku Region:

Shikoku’s battery market is developing alongside Japan’s national energy transition policies. Japan’s Cabinet approved a Plan for Global Warming Countermeasures in February 2025, reaffirming the target of 100% electrified vehicle sales by 2035 and reinforcing sustained downstream battery demand across all regions. Shikoku’s proximity to the Kinki industrial corridor provides a foundation for gradual expansion into battery materials.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Ehime, Kagawa, Tokushima, Kochi |

|

Major Growth Drivers

|

EV policy-driven downstream demand, chemical industry proximity, grid storage adoption, national decarbonization alignment |

|

Outlook

|

Steady growth on policy-driven momentum |

Market Outlook 2026-2034

What is the future outlook of the Japan battery market?

Japan battery market is expected to sustain steady revenue growth through 2034.

Japan's battery market has a strong potential for growth over the forecast period, driven by the expansion of electric vehicle battery production, the increase in energy storage systems, and the pace of innovation in solid-state battery technology. The government's policy support, such as EV subsidies, the Green Growth Strategy, and the METI Green Innovation Fund, will ensure the continuation of capital expenditure into local battery production capacity.

Japan Battery Market - Leading Key Players

Japan battery market features an internationally competitive landscape of established manufacturers spanning automotive, industrial, grid-scale, and consumer applications. Key players are investing in next-generation cell chemistry, capacity expansions, global supply agreements, and circular battery economy initiatives to strengthen domestic and international market positioning.

| Company | Leading Brands | Highlights |

|---|---|---|

| EEMB Japan | EEMB | Designs precision lithium primary and rechargeable cells for IoT, medical, and industrial end-users; operates specialized battery R&D capabilities within Japan |

| GS Yuasa International Ltd. | Yuasa, GS, PRODA | Joint venture Lithium Energy Japan (LEJ) supplies batteries for Japan’s first mass-produced EV |

| Maxell, Ltd | Maxell iR, Maxell CR | World-class micro battery manufacturer specializing in coin-cell lithium batteries for hearing aids, wearables, and medical implants |

| Panasonic Corporation | Eneloop, Panasonic Energy | Designated Wakayama factory as global mother factory for 4680-format cell development; targets quadrupling production capacity to 200 GWh by fiscal 2031 through two-pillar Japan-North America strategy |

Some of the existing key players in the market are Maxell, Ltd, NGK Insulators Ltd., The Furukawa Battery Co., Ltd, Toshiba Corporation, etc.

Latest Development & News

- In February 2026, GS Yuasa International Ltd. announced its plan for the development and mass production of stationary lithium-ion batteries in Japan had been certified as a “Stable Supply Assurance Plan for Batteries” under the Ministry of Economy, Trade and Industry (METI). This includes an investment of approximately 70.3 billion yen for the construction of a facility with a capacity of 2 GWh and is expected to commence in October 2028.

- In December 2025, Japan’s government planned to raise subsidies for EVs to strengthen the EV market and the competitiveness of the battery industry in Japan. The government plans to raise the upper limit of the subsidy for EVs from 900,000 yen to 1.3 million yen, which is approximately 20% of the total price of EVs, in order to accelerate the EV market and support Japan’s battery and EV strategy.

- In April 2024, Panasonic Energy Co., Ltd. announced the completion of a new battery production development facility in its Suminoe plant in Osaka, Japan, aimed at advancing next-generation battery manufacturing technologies. The facility has a total area of 7,900 m² and supports pilot production and digital manufacturing technology development for batteries.

Japan Battery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GWh |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Primary Battery, Secondary Battery |

| Products Covered | Lithium-Ion, Lead Acid, Nickel Metal Hydride, Nickel Cadmium, Others |

| Applications Covered | Automotive Batteries, Industrial Batteries, Portable Batteries |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | EEMB Japan, GS Yuasa International Ltd., Maxell, Ltd, NGK Insulators Ltd., Panasonic Corporation, The Furukawa Battery Co., Ltd, Toshiba Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan battery market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan battery market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan battery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Battery Market Report

The Japan battery market reached a volume of 89.1 GWh in 2025.

The market is projected to grow at a CAGR of 11.6% during 2026-2034, reaching 246.1 GWh by 2034.

Key growth drivers include rising electric vehicle (EV) adoption, government funding for domestic battery manufacturing, renewable energy storage needs, and consumer electronics demand.

The report covers segmentation by type, product, application, and region. Each segment includes detailed market size and forecast analysis.

Major players in the Japan battery market include EEMB Japan, GS Yuasa International Ltd., Maxell, Ltd, NGK Insulators Ltd., Panasonic Corporation, The Furukawa Battery Co., Ltd, Toshiba Corporation, etc.

Key trends include usage of next-generation silicon anode batteries, solid-state technology development, grid-scale energy storage expansion, and EV battery swapping infrastructure.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)