Japan Bioreactor Market Size, Share, Trends and Forecast by Type, Usage, Scale, Control Type, and Region, 2026-2034

Japan Bioreactor Market Size & Forecast 2026-2034

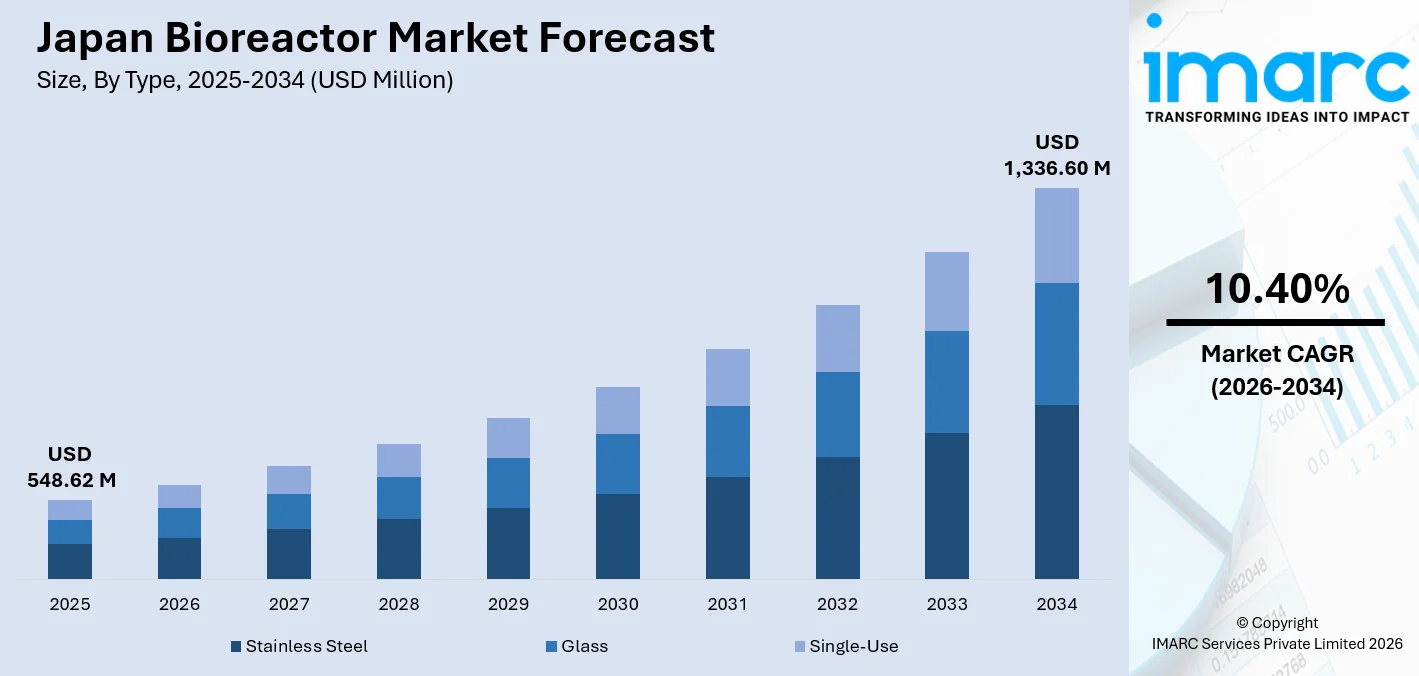

Japan bioreactor market size, valued at USD 548.62 Million in 2025, is projected to reach USD 1,336.60 Million by 2034, growing at a CAGR of 10.40% from 2026-2034, driven by Japan’s rapidly expanding biopharmaceutical industry, a strategic national focus on cell and gene therapies, and the accelerating deployment of automated bioprocessing infrastructure. Furthermore, Japan’s biopharmaceutical sector accelerates large-scale adoption of advanced bioprocess systems for biologics and regenerative medicine production, reinforcing sustained upstream demand across Japan bioreactor market.

To get more information on this market Request Sample

Japan Bioreactor Industry Analysis - Key Insights

- Stainless steel commands 55.0% of type share in 2025 - its unmatched structural integrity, autoclavability, and compatibility with large-volume manufacturing make it the backbone of Japan’s commercial biopharmaceutical production.

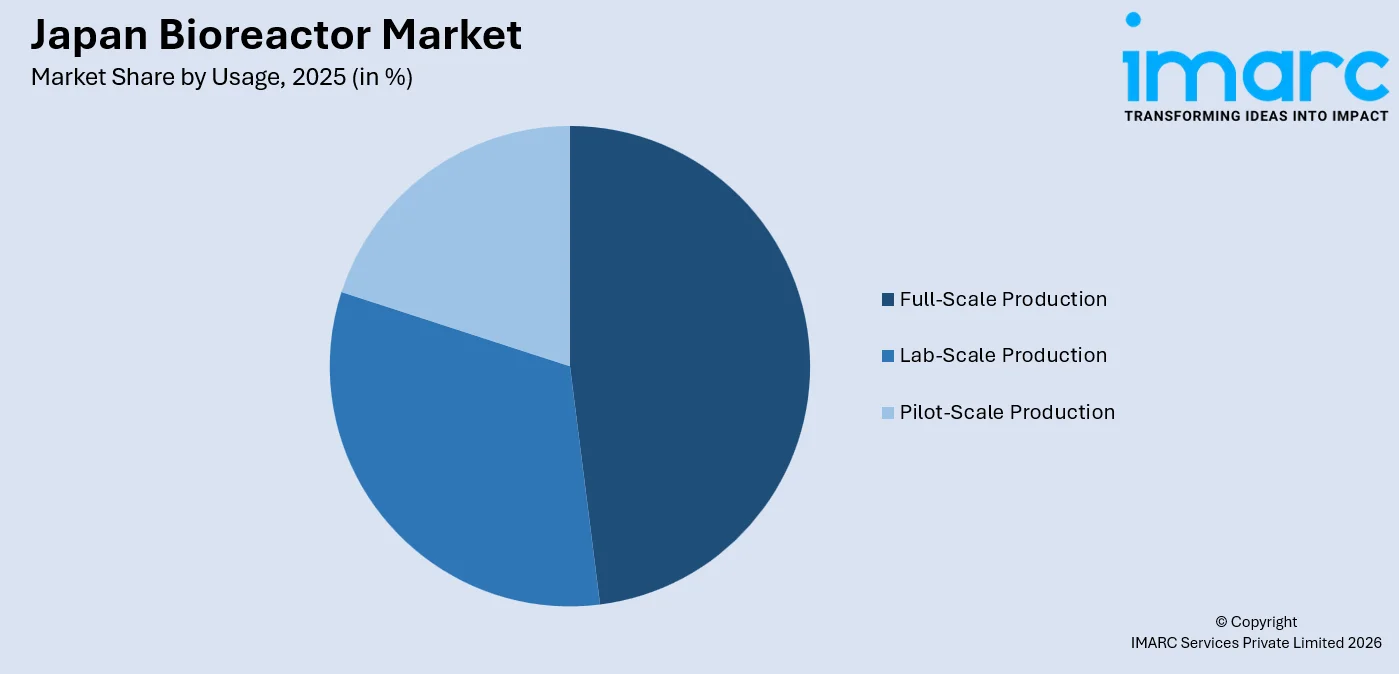

- Full-scale production leads usage at 48.0% in 2025 - nearly half of all bioreactor deployments are in commercial manufacturing operations, reflecting Japan’s maturing biologics pipeline and CDMO capacity expansion.

- Above 1500L holds scale 38.0% share in 2025 - the dominance of large-volume systems signals Japan’s prioritization of high-throughput monoclonal antibody and vaccine manufacturing over research-scale installations.

- Automated owns control type 72.0% in 2025 - the highest dominance figure across all segments. Japan’s precision manufacturing culture and stringent PMDA compliance requirements structurally favour fully automated process control over manual systems.

- Kanto Region leads regionally at 42.0% in 2025 - Tokyo and Yokohama anchor Japan’s largest concentration of biopharmaceutical manufacturers and CDMOs, with ongoing facility expansions sustaining the region’s commanding lead.

Japan Bioreactor Market Trends and Dynamic 2026

Market Trends

Shift toward single-use and hybrid bioprocessing architectures in Japan

Japan’s bioreactor landscape is undergoing a structural shift as manufacturers increasingly adopt hybrid strategies that combine stainless steel primary vessels with single-use downstream components to optimize cost efficiency and contamination control. In April 2025, Thermo Fisher Scientific Inc. launched the 5L DynaDrive Single-Use Bioreactor (S.U.B.), a bench-scale system offering seamless scalability from 1 to 5,000 liters with a 27% productivity increase over conventional glass bioreactors.

Digital transformation and real-time process monitoring reshaping bioprocessing operations

Advanced data integration and automated analytics are becoming central to Japan’s bioprocessing operations, driven by PMDA’s increasing emphasis on quality-by-design principles and continuous process verification. In April 2025, Sartorius Stedim Biotech entered a strategic partnership with Tulip Interfaces to launch Biobrain Operate, a suite of digital manufacturing applications that integrates with bioreactor equipment to reduce process variability, digitize operations, and streamline regulatory compliance documentation.

- PAT and In-Line Sensing Adoption: Process Analytical Technology tools, including in-line Raman spectroscopy, capacitance probes, and multiparameter sensors, are being integrated into bioreactor control systems to enable real-time batch monitoring and reduce off-line sampling requirements.

- Cell and Gene Therapy Scale-Up: Japan’s regenerative medicine regulatory fast-track framework is accelerating clinical and commercial-scale bioreactor deployments for autologous and allogeneic cell therapy manufacturing, particularly in Tokyo and Osaka.

- Continuous and Perfusion Bioprocessing: Perfusion-based bioreactor configurations enabling higher cell densities and continuous product harvest are gaining traction among Japan’s leading monoclonal antibody manufacturers, reducing batch timelines significantly.

- Sustainable Bioprocessing Materials: Development of biocompatible polymer films and biobased single-use components is advancing Japan’s biopharmaceutical sector’s environmental commitments while maintaining the sterility and performance standards required for GMP manufacturing.

Growth Drivers

Japan’s aging population and rising biopharmaceutical demand

Japan’s demographic profile, with one of the world’s highest populations of citizens aged 65 and above, is generating sustained demand for biologics, including monoclonal antibodies, biosimilars, and targeted therapies. The biopharmaceutical sector has been a significant contributor to Japan’s broader biotechnology market, reinforcing the upstream equipment demand for large-volume, automated bioreactors that define the Japan Bioreactor market trends.

Government strategic support through “Grand Design for New Capitalism” and biotechnology prioritization

Japan’s national biotechnology strategy explicitly designates regenerative medicine, cell therapies, and gene therapies as priority development areas under the Grand Design for New Capitalism policy framework. Industry-academia collaborations supported by public funding are further driving innovation in bioreactor design, single-use scale-up platforms, and automated process control technologies, directly expanding the addressable market through the Japan Bioreactor market forecast.

CDMO capacity expansion driving commercial bioreactor installation

Japan’s Contract Development and Manufacturing Organization (CDMO) sector is scaling rapidly to meet growing domestic and export demand for biologics and advanced therapies. In April 2025, AGC Biologics announced a strategic decision to deploy large-scale single-use technology at its new facility in Yokohama, Japan. The CDMO will install two 5,000 L Thermo Scientific DynaDrive Single-Use Bioreactors, positioning the site among Japan’s most advanced for large-scale mammalian biologics production, with GMP operations scheduled to begin in 2027.

- Vaccine Manufacturing Capacity Programs: Japan’s post-pandemic commitment to domestic vaccine sovereignty is sustaining investment in large-scale bioreactor infrastructure for mRNA, viral vector, and recombinant protein vaccine platforms.

- Biosimilar Market Expansion: Japan’s growing biosimilar approval pathway and healthcare cost containment policies are incentivizing domestic biologics manufacturers to invest in high-throughput full-scale bioreactor systems.

- Export-Oriented Biologics Manufacturing: Japan’s biopharmaceutical companies are targeting Asian export markets for biologics, requiring internationally compliant GMP-grade bioreactor facilities that meet ICH and WHO manufacturing standards.

- Technology Partnership and Licensing Activity: Partnerships between Japanese CDMOs and global bioprocessing technology providers are accelerating the deployment of next-generation automated, large-scale bioreactor platforms.

Market Restraints

High capital investment requirements for large-scale stainless steel bioreactor infrastructure: The installation, qualification, and validation of large-volume stainless steel bioreactor systems demand substantial capital expenditure and extended facility commissioning timelines. For emerging and mid-sized biotechnology companies, these upfront cost barriers limit access to commercial-scale manufacturing and can delay product development programs and regulatory submissions.

Complex regulatory validation requirements under PMDA oversight: Japan’s Pharmaceuticals and Medical Devices Agency imposes rigorous equipment qualification, process validation, and data integrity requirements for bioreactor-based biopharmaceutical manufacturing. Navigating multi-year validation programs, changing control procedures, and technology transfer documentation creates substantial operational and compliance burdens, particularly for companies transitioning between bioreactor platforms or scaling from pilot to full production.

Shortage of specialized bioprocessing engineering talent: The specialized skill sets required to operate, maintain, and optimize advanced automated bioreactor systems, including bioprocess engineers, automation specialists, and quality assurance scientists, remain in limited supply in Japan. The gap between industry demand and the academic training pipeline constrains the speed of facility ramp-up and technology adoption across the sector.

Japan Bioreactor Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Stainless Steel | 55.0% | 2025 |

| Usage | Full-Scale Production | 48.0% | 2025 |

| Scale | Above 1500L | 38.0% | 2025 |

| Control Type | Automated | 72.0% | 2025 |

| Region | Kanto Region | 42.0% | 2025 |

Type Insights

Stainless Steel - 55.0% Market Share (2025) | Leading Type

Stainless steel bioreactors maintain their dominant position in Japan market through their unmatched suitability for high-volume, multi-batch commercial manufacturing of monoclonal antibodies, vaccines, and recombinant proteins. Their robust construction, autoclavability, and compatibility with validated cleaning-in-place and sterilization-in-place systems make them the irreplaceable platform for Japan’s GMP-compliant biopharma manufacturers. Stainless steel’s dominance is further reinforced by Japan’s established quality culture in precision manufacturing.

|

Segment Breakdown Stainless Steel (55.0%) · Glass · Single-Use |

Usage Insights

Access the comprehensive market breakdown Request Sample

Full-Scale Production - 48.0% Market Share (2025) | Leading Usage

Full-scale production bioreactors command the largest usage share, reflecting Japan’s maturing commercial biologics pipeline and the transition of multiple products from clinical development into large-scale manufacturing. Japan’s biopharmaceutical sector accelerated the adoption of large-scale bioprocess systems for biologics and regenerative medicine production, with companies deploying full-scale systems capable of producing commercial volumes for domestic and export markets.

|

Segment Breakdown Full-Scale Production (48.0%) · Lab-Scale Production · Pilot-Scale Production |

Scale Insights

Above 1500L - 38.0% Market Share (2025) | Leading Scale

Above-1500L bioreactor systems account for the largest scale segment, driven by Japan’s commercial manufacturing priorities in monoclonal antibodies, biosimilars, and large-batch vaccines. The BioProcess International Asia conference held in Kyoto in October 2025 brought bioprocessing leaders together to advance upstream processing innovations, including scale-up methodologies for above-1500L configurations, highlighting the sector’s active investment in commercial-scale technology development.

|

Segment Breakdown Above 1500L (38.0%) · 5L-20L · 20L-200L · 200L-1500L |

Control Type Insights

Automated - 72.0% Market Share (2025) | Leading Control Type

Automated bioreactor control systems command a dominant share of the Japan market, the highest dominance figure across all four segments, reflecting Japan’s deeply embedded precision manufacturing culture and PMDA’s quality-by-design expectations. The push toward Industry 4.0 in Japanese biomanufacturing is accelerating automated bioreactor adoption. The Japan bioreactor market outlook remains strongly positive as manufacturers specify fully integrated automated systems for new CDMO builds and facility expansions, displacing manual control configurations from existing production lines.

|

Segment Breakdown Automated (72.0%) · Manual |

Regional Insights

Kanto Region - 42.0% Market Share (2025) | Leading Region

Kanto’s bioreactor ecosystem benefits from proximity to Japan’s largest regulatory and logistics infrastructure, including PMDA headquarters in Tokyo and Yokohama’s internationally connected port facilities. The region’s dense network of universities, clinical research organizations, and government-affiliated research institutes, including RIKEN and the National Institute of Biomedical Innovation, Health and Nutrition, sustains a continuous pipeline of early-stage bioprocessing demand that feeds commercial-scale installation activity.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

42.0%

|

|

Key States

|

Tokyo, Kanagawa (Yokohama), Saitama, Chiba, Ibaraki, Tochigi, Gunma, Yamanashi |

|

Major Growth Drivers

|

CDMO facility expansion, PMDA regulatory proximity, academic-industry R&D pipeline, export biologics manufacturing |

|

Outlook

|

Dominant national bioprocessing hub |

|

Regional Breakdown Kanto Region (42.0%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai Region represents one of Japan’s most significant bioreactor markets, built around a deep pharmaceutical manufacturing heritage and the globally recognized Kobe Medical Industry Development Project. The BioProcess International Asia conference in Kyoto in October 2025 highlighted Kansai’s growing role as a national forum for upstream bioprocessing innovation and technology exchange.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Osaka, Kyoto, Hyogo (Kobe), Nara, Shiga, Wakayama, Mie |

|

Major Growth Drivers

|

Pharma manufacturing cluster, Kobe medical industry initiative, cell therapy R&D, academic bioprocessing research |

|

Outlook

|

Second-largest regional market |

Central/Chubu Region:

The Central/Chubu Region supports bioreactor demand through a growing base of pharmaceutical and specialty chemical manufacturers embedded within Japan’s manufacturing heartland. The region’s strong industrial engineering expertise and supply chain infrastructure support bioreactor facility construction and maintenance services. Increasing biotechnology investment from Chubu-based companies transitioning from conventional pharma to biologics is expanding the region’s commercial bioreactor footprint.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Aichi (Nagoya), Shizuoka, Gifu, Mie, Nagano, Niigata, Toyama, Ishikawa, Fukui, Yamanashi |

|

Major Growth Drivers

|

Pharmaceutical manufacturing expansion, industrial engineering capability, specialty bioprocessing applications |

|

Outlook

|

Emerging biologics manufacturing base |

Kyushu-Okinawa Region:

Kyushu is positioning itself as a hub for biosimilar manufacturing and fermentation-based bioprocessing, supported by Fukuoka’s growing life science industry cluster and university research programs. The region benefits from relatively lower land costs and government incentives for biopharmaceutical facility development, attracting new entrants seeking commercial bioreactor infrastructure for biosimilar and specialty biologics production. Academic-industry collaborations between Kyushu University and biopharma companies are advancing bioprocessing technology development.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Fukuoka, Kumamoto, Nagasaki, Saga, Oita, Miyazaki, Kagoshima, Okinawa |

|

Major Growth Drivers

|

Biosimilar manufacturing, Fukuoka life science cluster, land cost advantages, government biotechnology incentives |

|

Outlook

|

Biosimilar and fermentation growth zone |

Tohoku Region:

Tohoku’s bioreactor market is driven by a network of university research institutes and government-sponsored clinical development programs that maintain consistent demand for pilot-scale and lab-scale bioprocessing equipment. Sendai and its surrounding academic corridor have seen increasing biotechnology activity supported by Japan’s regional innovation policy, directing public funding toward bioprocessing capability development outside Japan’s primary pharmaceutical corridors.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Miyagi (Sendai), Iwate, Aomori, Akita, Yamagata, Fukushima |

|

Major Growth Drivers

|

Academic research institutes, clinical trial infrastructure, government regional biotechnology support |

|

Outlook

|

Research and clinical-stage growth market |

Chugoku Region:

The Chugoku Region, with Hiroshima as its principal industrial center, supports bioreactor demand through pharmaceutical and chemical manufacturing companies that are incrementally transitioning toward biologics production. The region’s established manufacturing infrastructure provides the engineering and technical services foundation necessary for bioreactor installation and maintenance, with growing interest from specialty pharmaceutical companies evaluating the region for new biologics manufacturing facilities.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Hiroshima, Okayama, Yamaguchi, Shimane, Tottori |

|

Major Growth Drivers

|

Chemical-to-biologics manufacturing transition, specialty pharma expansion, industrial engineering services |

|

Outlook

|

Niche pharmaceutical and specialty applications |

Hokkaido Region:

Hokkaido’s bioreactor market is anchored in fermentation technology, reflecting the region’s long-established expertise in food biotechnology and agricultural bioprocessing. Sapporo-based research institutes and Hokkaido University’s biotechnology programs are expanding into pharmaceutical bioprocessing, creating early-stage demand for lab-scale and pilot-scale bioreactor systems. Government support for biotechnology diversification in Hokkaido is gradually broadening the region’s application scope beyond traditional fermentation.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Hokkaido (Sapporo) |

|

Major Growth Drivers

|

Fermentation expertise, Hokkaido University research, food bioprocessing, diversification into pharma |

|

Outlook

|

Fermentation and early pharma expansion |

Shikoku Region:

Shikoku’s bioreactor market is primarily driven by specialty chemical manufacturers and small pharmaceutical companies exploring biologics applications. The region benefits from proximity to Kansai’s established biopharma corridor and is gradually attracting biotechnology investment as Japan’s government promotes regional dispersion of advanced manufacturing capabilities. Demand currently centers on compact lab-scale and research-grade bioreactor systems.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Ehime, Kagawa, Kochi, Tokushima |

|

Major Growth Drivers

|

Specialty pharma, proximity to the Kansai cluster, government regional manufacturing incentives |

|

Outlook

|

Emerging niche market |

Market Outlook 2026-2034

What is the future outlook of the Japan bioreactor market?

The Japan bioreactor market is expected to sustain steady revenue growth through 2034

The Japan bioreactor market is positioned for robust expansion over the forecast period. Growth will be sustained by Japan’s ageing population driving biologics demand, government-backed CDMO expansion programs, and the accelerating deployment of large-volume automated bioreactor systems for monoclonal antibodies, cell therapies, and vaccines. The convergence of regulatory digitalization under PMDA, continuous bioprocessing adoption, and international export market development will collectively reinforce market expansion throughout the forecast horizon.

Japan Bioreactor Market - Leading Key Players

Japan bioreactor market is served by a competitive mix of global bioprocessing technology leaders and specialized equipment suppliers. Key players are driving market expansion through integrated automated platforms, expanded single-use portfolios, strategic CDMO partnerships, and digital bioprocessing solutions tailored to Japan’s rigorous PMDA regulatory environment.

| Company | Leading Brands | Highlights |

|---|---|---|

| Sartorius Stedim Biotech | BIOSTAT, Ambr, Celsius | Leading bioreactor and bioprocessing supplier; Biobrain Operate digital platform launched April 2025; global CDMO partnership network. |

| Thermo Fisher Scientific | HyPerforma, DynaDrive, Nunc | 5L DynaDrive S.U.B. launched April 2025 with 27% productivity gain; scalability platform from 1L to 5,000L for Japanese biopharma R&D and manufacturing |

| Cytiva (Danaher) | Xcellerex, FlexFactory, WAVE Bioreactor | FlexFactory platforms deployed at AGC Biologics Yokohama for mAb and mRNA production; multiple 2,000L systems operational from 2025 |

| Eppendorf AG | BioBLU, BioFlo, DASbox | Precision bench-scale and pilot bioreactor specialist; strong presence in Japanese universities and pharmaceutical R&D laboratories |

| Merck KGaA (MilliporeSigma) | Mobius | Single-use bioprocessing leader; Ultimus SU Process Container Film with 10x abrasion resistance; broad Japan CDMO and pharma customer base |

Latest Development & News

- In October 2025, the BioProcess International Asia conference was held in Kyoto, Japan, drawing leading bioprocessing professionals from across the region to discuss advances in bioprocessing technologies, including upstream processing, continuous manufacturing, and AI-driven bioprocess development. The event serves as a key platform for networking, innovation exchange, and collaboration across the biologics manufacturing ecosystem in Asia.

- In June 2025, AGC Biologics announced the expansion of its cell therapy development operations, launching process development and clinical manufacturing services at its Yokohama Technical Center in Japan. The new Yokohama operations will support pre-clinical and clinical manufacturing for autologous and allogeneic therapies, ahead of a larger biomanufacturing facility expected to begin operations in 2027, further expanding bioreactor-based production capacity in Japan.

- In April 2025, Thermo Fisher Scientific launched the 5L DynaDrive Single-Use Bioreactor, a bench-scale system designed for seamless scalability from 1 to 5,000 liters, offering a 27% productivity improvement over conventional glass bioreactors. The platform supports both large and small biopharma manufacturers in Japan with biobased film materials and consistent performance across process scales, addressing both research and commercial manufacturing needs.

Japan Bioreactor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Glass, Stainless Steel, Single-Use |

| Usages Covered | Lab-Scale Production, Pilot-Scale Production, Full-Scale Production |

| Scales Covered | 5L-20L, 20L-200L, 200L-1500L, Above 1500L |

| Control Types Covered | Manual, Automated |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market Trends, market forecasts, and dynamics of the Japan bioreactor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan bioreactor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan bioreactor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Bioreactor Market Report

The Japan bioreactor market reached a value of USD 548.62 Million in 2025.

The market is projected to grow at a CAGR of 10.40% during 2026-2034, reaching USD 1,336.60 Million by 2034.

Key growth drivers include surging biopharmaceutical demand, single-use bioreactor innovations, regulatory quality mandates, aging healthcare population, and sustainable bioprocessing focus.

The report covers segmentation by type, usage, scale, control type, and region. Each segment includes detailed market size and forecast analysis.

Key trends include automated control systems, perfusion technology adoption, cell culture advancements, and integration with artificial intelligence (AI) for process optimization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade