Japan Cloud Managed Services Market Size, Share, Trends and Forecast by Service Type, Deployment Model, Organization Size, Vertical, and Region 2026-2034

Japan Cloud Managed Services Market Size & Forecast 2026-2034

The Japan cloud managed services market size, valued at USD 10.79 Billion in 2025, is projected to reach USD 24.60 Billion by 2034, growing at a CAGR of 9.60% from 2026-2034, driven by the accelerating retirement of legacy IT infrastructure under Japan's "2025 Digital Cliff", a projected ¥12 trillion (~$80 billion) annual economic loss driving the demand for cloud managed services in Japan.

.webp)

To get more information on this market Request Sample

Japan Cloud Managed Services Industry Analysis — Key Insights

- Managed infrastructure services hold 27.0% of the market by service type in 2025- the single largest service category. Japan's "2025 Digital Cliff" modernization wave is channeling the largest share of cloud managed services budgets toward infrastructure migration, IaaS lifecycle management, and server and storage outsourcing.

- Public cloud commands 61.0% of the market by deployment model in 2025- a decisive majority driven by hyperscaler investment, Japan's ISMAP Government Cloud certification, and enterprise preference for AWS, Microsoft Azure, and Google Cloud as the default platforms for managed workloads.

- Large enterprises dominate with 68.0% share by organization size in 2025- reflecting the scale and budget intensity of enterprise-grade managed service contracts. Japan's top-tier corporations deploy full-stack cloud managed services spanning infrastructure, security, and network layers as part of multi-year transformation programs.

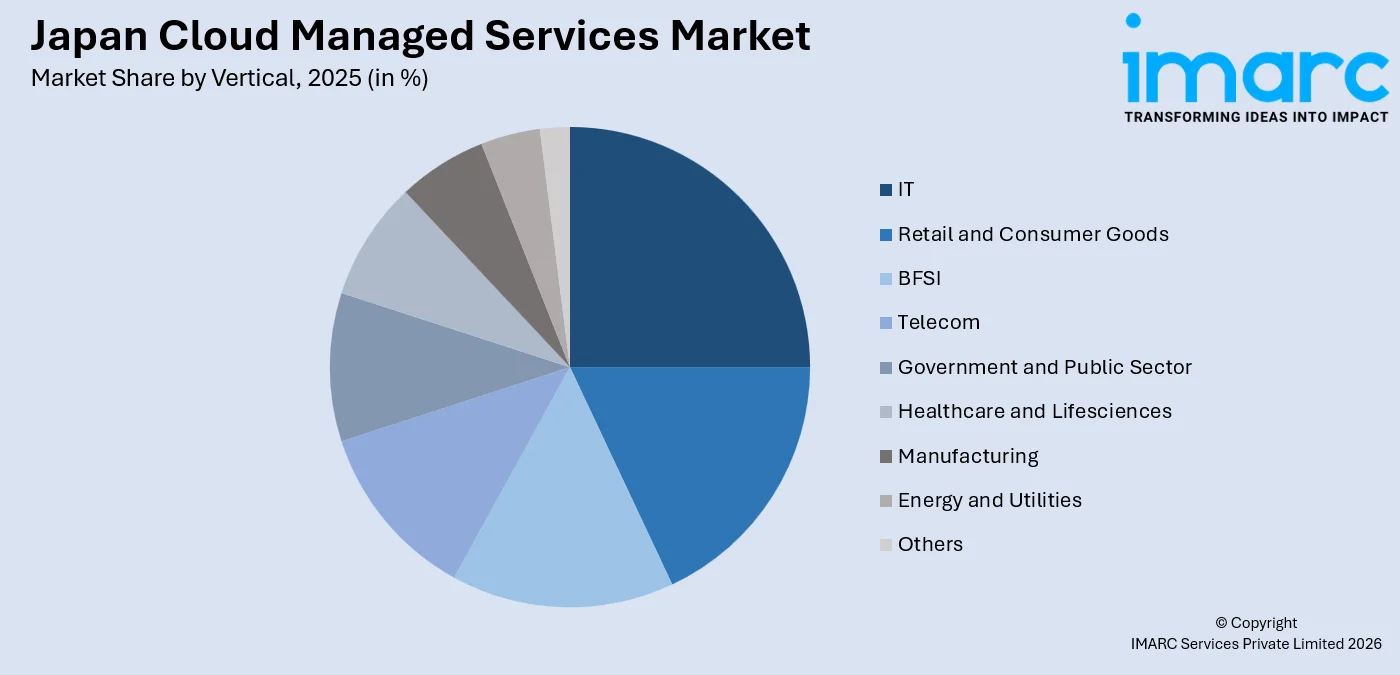

- IT leads vertical demand at 24.0% in 2025- the highest-spending vertical, as Japan's technology companies outsource internal cloud operations to specialists, freeing scarce engineering talent to focus on product development and AI innovation rather than infrastructure management.

- Kanto Region leads regionally at 45.0% share in 2025- with Tokyo's density of enterprise headquarters, government agencies, and hyperscaler data centers creating an unrivalled concentration of managed services demand across every service type and vertical sector.

Japan Cloud Managed Services Market Trends and Dynamic 2026

Market Trends

"2025 Digital Cliff" legacy modernization wave driving managed infrastructure migration at scale

Japan’s Ministry of Economy, Trade and Industry (METI) warned that failure to modernize legacy systems could impose JPY 12 trillion in annual economic losses. This has triggered the largest wave of IT infrastructure outsourcing in Japan's modern history, as banks, manufacturers, and public agencies race to migrate COBOL-era core systems to cloud-managed environments.

AI-native AIOps platforms transforming cloud infrastructure operations for enterprise clients

AI integration into managed service platforms is changing the economics of cloud operations, reducing manual intervention and compressing incident response times. In February 2026, Fujitsu Limited launched its AI-Driven Software Development Platform, an initiative designed to modernize software development with artificial intelligence and support sustainable growth for both customers and society. Fujitsu plans to use this platform to update all 67 types of medical and government business software products offered by Fujitsu Japan Limited by the end of fiscal year 2026.

Sovereign cloud and ISMAP certification are creating a structured two-tier managed services market

Japan's regulatory framework is partitioning the managed services market into ISMAP-certified sovereign-capable providers and standard commercial offerings. In October 2024, Oracle and NTT DATA Japan partnered to expand Japan's sovereign cloud services using Oracle Alloy, bundling managed infrastructure with data residency guarantees.

- Multi-Cloud FinOps Management: Enterprises running workloads across AWS, Azure, and Google Cloud are outsourcing cloud cost optimization and governance to managed service providers with cross-platform FinOps expertise to contain escalating multi-cloud spend.

- Mainframe-to-Cloud Migration Acceleration: Specialized migration toolchains, including Kyndryl's zCloud and TIS's Xenlon, are compressing project timelines by up to one-third, directly accelerating managed infrastructure deal conversion and contract pipeline growth.

- Green Data Centre Investment Incentives: Japan's Carbon Neutrality and Digital Transformation tax regime, stimulating managed infrastructure investments in regional sustainable facilities.

- Managed Security Bundling into Infrastructure Contracts: Rising ransomware incidents investigated by Japan's National Police Agency are compelling enterprises to bundle managed security operations into cloud infrastructure contracts, boosting average contract values across the managed services ecosystem.

Growth Drivers

Structural IT talent shortage converting in-house cloud operations to managed service outsourcing

Japan's shortage with more than 70% of organizations reporting understaffing in cloud disciplines according to the Linux Foundation's 2025 Japan Tech Talent Report, is the most reliable structural driver of Japan cloud managed services market growth. Enterprises unable to build and retain internal cloud operations teams are converting multi-year managed service contracts into their default operating model, boosting contract values and extending provider relationships across infrastructure, security, and network layers simultaneously.

Hyperscaler infrastructure investment, building cloud capacity for managed service monetization

Foreign technology investment is creating the physical foundation for cloud managed services expansion. In June 2025, KDDI and HPE collaborated to launch the Osaka Sakai Data Center by 2026 to support startups and enterprises with NVIDIA AI infrastructure for developing AI applications and training large language models. Managed security services in Japan are growing as cyber-insurance premiums spike and regulators mandate threat-monitoring baselines for critical infrastructure operators.

Government digital transformation mandates generating a sustained public-sector contract pipeline

To maximize the efficiency and effectiveness of digital technology, it is essential for national and local governments to collaborate, rather than having nearly 1,800 local governments independently develop and manage their own systems. This cooperative approach can help streamline resources and improve overall system performance.

- Cybersecurity Compliance Outsourcing Mandate: Mandatory cyber-risk disclosures on the Tokyo Stock Exchange and APPI amendments are compelling listed companies to outsource security operations to specialist managed security service providers with around-the-clock SOC capabilities.

- SME Cloud Adoption Acceleration: SMEs accessing government IT subsidies covering up to 75% of software costs are adopting cloud platforms requiring managed services for ongoing operation, creating an expanding second-tier market beyond large enterprises.

- Edge Computing Managed Infrastructure Expansion: Japan's edge computing market, generating demand for managed services operating distributed edge infrastructure across manufacturing, automotive, and smart city deployments.

- NTT Integration Creating Single-Vendor Managed Services Scale: Nippon Telegraph and Telephone Corp. (NTT)’s ¥2.37 trillion (US$16.3 billion) acquisition of NTT DATA Group, in June 2025, created Japan's largest integrated tech-services provider, offering enterprises a single-vendor option for end-to-end cloud managed operations.

Market Restraints

Deep-rooted corporate resistance to outsourcing sensitive IT operations: Japan's long-standing corporate culture of internalizing mission-critical IT operations, embedded through decades of keiretsu-model IT relationships with trusted system integrators, creates structural inertia against transitioning to third-party managed service models. Risk-averse organizations prioritize operational continuity and data control over the cost and agility benefits that managed service outsourcing offers.

Data sovereignty and regulatory compliance complexity constraining vendor selection: Japan's evolving data protection framework, APPI amendments, the Economic Security Promotion Act, and sector-specific financial and healthcare regulations create a demanding compliance environment. Organizations in regulated industries face narrow fields of ISMAP-certified, data-resident-compliant providers, raising procurement costs and extending decision timelines for managed service contract awards.

Provider-side talent shortage creating a managed services supply bottleneck: The same structural IT talent shortage that drives outsourcing demand also constrains managed service provider capacity to fulfil it. Providers struggle to recruit and retain cloud-certified engineers and security analysts, creating a supply bottleneck that limits geographic expansion, slows service innovation, and inflates delivery costs across the managed services ecosystem.

Japan Cloud Managed Services Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Service Type |

Managed Infrastructure Services |

27.0% |

2025 |

|

Deployment Model |

Public Cloud |

61.0% |

2025 |

|

Organization Size |

Large Enterprises |

68.0% |

2025 |

|

Vertical |

IT |

24.0% |

2025 |

|

Region |

Kanto Region |

45.0% |

2025 |

Service Type Insights

Managed Infrastructure Services – 27.0% Market Share (2025) | Leading Service Type

Managed infrastructure services hold the largest segment share because it captures the broadest spectrum of enterprise cloud outsourcing activity, server management, storage, virtualisation, Kubernetes orchestration, and IaaS lifecycle operations. The scale and urgency of Japan's legacy modernization wave is directly channeling the largest managed services budgets into infrastructure migration and operation. Kyndryl Japan announced in April 2025 the expansion of its zCloud service using the latest IBM mainframe “IBM Z” at a new data center near Tokyo, offering hybrid cloud environments combining mainframe-based mission-critical systems with cloud infrastructure for enterprises modernizing rather than replacing their core systems.

|

Segment Breakdown Managed Infrastructure Services (27.0%) · Managed Network Services · Managed Business Services · Managed Security Services · Managed Mobility Services · Managed Communication and Collaboration Services |

Deployment Model Insights

Public Cloud - 61.0% Market Share (2025) | Leading Deployment Model

Public cloud achieved decisive dominance as the deployment model for Japan's cloud managed services market, driven by hyperscaler infrastructure investment, Government Cloud certification requirements, and the economic advantages of elastic, pay-per-use managed environments. Japan cloud managed services market outlook indicates continued public cloud expansion, with 219 data centers, Japan was ranked 10th in the world for the number of data centers as of March 2024.

|

Segment Breakdown Public Cloud (61.0%) · Private Cloud |

Organization Size Insights

Large Enterprises - 68.0% Market Share (2025) | Leading Organization Size

Large enterprises command the market through their capacity to engage multi-year, multi-layer managed service contracts spanning infrastructure, security, and network operations simultaneously. Japan's top system integrators, NTT DATA, Fujitsu, and NEC, are deeply embedded in Japan's keiretsu corporate model, giving them preferred provider status with the country's largest corporations. KKR's USD 4.1 billion December 2024 tender for Fuji Soft, Japan's largest private-equity IT deal, signals the investment capital flowing into large-enterprise managed services platforms.

|

Segment Breakdown Large Enterprises (68.0%) · Small and Medium-sized Enterprises |

Vertical Insights

Access the comprehensive market breakdown Request Sample

IT - 24.0% Market Share (2025) | Leading Vertical

Japan's IT sector is the largest single buyer of cloud managed services, a structural reality explained by the sector's need to focus scarce engineering talent on product development and AI innovation rather than internal infrastructure management. In October 2025, NTT DOCOMO BUSINESS became Japan's first recipient of the APAC Gartner “Eye on Innovation Awards for Communication Service Providers (CSPs).” This reflects the IT sector's ongoing investment in managed digital transformation capabilities.

|

Segment Breakdown IT (24.0%) · Retail and Consumer Goods · BFSI · Telecom · Government and Public Sector · Healthcare and Lifesciences · Manufacturing · Energy and Utilities · Others |

Regional Insights

Kanto Region - 45.0% Market Share (2025) | Leading Region

Kanto's commanding market reflects Tokyo's unmatched density of enterprise IT decision-making, financial institutions, government agencies, and hyperscaler data center infrastructure. Kanto is also the primary landing zone for hyperscaler infrastructure investment. Power constraints in the Tokyo region are pushing edge computing deployments to secondary prefectures, creating a distributed managed services model anchored in Kanto but extending regionally.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 45.0% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | Government cloud migration programs, enterprise headquarters concentration, hyperscaler data center expansion, financial sector IT transformation |

| Outlook | Dominant region, deepening AI-managed infrastructure leadership |

|

Regional Breakdown Kanto Region (45.0%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

The Kansai/Kinki Region is Japan's second-largest cloud managed services market, with Osaka's manufacturing, pharmaceutical, and financial services clusters driving sustained demand for managed infrastructure, security, and business services. In June 2025, KDDI and HPE announced a collaboration to launch an AI data center in Osaka utilizing NVIDIA AI infrastructure, directly expanding the region's cloud infrastructure capacity and managed services addressable market.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga prefectures |

| Key Growth Drivers | KDDI-HPE AI data center, Expo 2025 digital infrastructure legacy, pharmaceutical blockchain adoption, manufacturing IT outsourcing growth |

| Outlook | Growing AI cloud infrastructure hub, post-Expo managed services expansion |

Central/Chubu Region:

The Central/Chubu Region, anchored by Nagoya's automotive and precision manufacturing ecosystem, is a fast-growing cloud managed services market driven by Industry 4.0 programs integrating IoT, 5G, and edge computing. The region is witnessing a boom in 5G-enabled IoT sensor deployments to counteract factory labor shortages in 2025.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Automotive Industry 4.0 OT/IT convergence, private 5G managed security, Toyota AI platform infrastructure, EV supply chain cloud adoption |

| Outlook | Industrial IoT driving managed OT security services growth |

Kyushu-Okinawa Region:

Kyushu is emerging as a semiconductor and data center hotspot, drawing hyperscale investments that stimulate local managed infrastructure and consulting contracts.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto prefectures |

| Key Growth Drivers | Semiconductor cluster managed infrastructure, NEC hydrogen-edge pilot, TSMC supplier ecosystem, data center hyperscale investment |

| Outlook | Fast-growing semiconductor-driven managed services market |

Tohoku Region:

Tohoku's cloud managed services adoption is expanding through regional revitalization funds supporting smart-agriculture and renewable energy management programs, both requiring cloud-based operational monitoring and ongoing managed services. The Regional Investment Promotion Tax Measure, renewed in Japan's 2025 budget, allows accelerated depreciation on qualifying cloud infrastructure, incentivizing data center investment in Tohoku's inland prefectures outside the Pacific earthquake belt and expanding the managed services delivery footprint into underserved regions.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima prefectures |

| Key Growth Drivers | Regional revitalization cloud infrastructure incentives, smart-agriculture managed services, renewable energy management cloud adoption |

| Outlook | Incentive-driven data center expansion opening managed services market |

Market Outlook (2026-2034)

What is the future outlook of the Japan cloud managed services market?

The Japan cloud managed services market is expected to sustain steady revenue growth through 2034.

The combination of a deepening structural IT talent shortage, sustained hyperscaler infrastructure investment, and the progressive expansion of SME cloud managed services adoption will maintain the market's growth trajectory. As AI platform operations, MLOps, generative AI infrastructure management, and autonomous cloud operations become standard enterprise requirements, managed service providers offering AI-native capabilities will capture premium contract values through the forecast period.

Japan Cloud Managed Services Market - Leading Key Players

The Japan cloud managed services market is served by a concentrated group of domestic system integration giants and global managed infrastructure specialists, all competing for long-term enterprise and government contracts.

| Company | Leading Services | Highlights |

|---|---|---|

|

NTT DATA Corporation |

NTT DATA Cloud Managed Services, NTT DATA Cloud Platform |

One of Japan’s largest IT service providers offering cloud integration, managed cloud, and digital transformation solutions for enterprises and government clients. |

|

Fujitsu Limited |

Fujitsu Hybrid IT Services |

Major Japanese technology company providing enterprise cloud infrastructure, hybrid cloud management, and managed IT services for large enterprises. |

|

NEC Corporation |

NEC Cloud IaaS |

Provides cloud infrastructure, managed services, and digital transformation solutions focused on security, compliance, and enterprise workloads. |

Some of the key market players in the Japan cloud managed services market are NTT DATA Corporation, Fujitsu Limited, NEC Corporation, Hitachi Ltd., Sakura Internet Inc., etc.

Latest Development & News

- In April 2025, Kyndryl Japan Co., Ltd. expanded its existing zCloud service, which enables businesses to build flexible mainframe platform environments based on their operational needs. The company enhances the service by deploying the latest IBM mainframe “IBM Z” provided by IBM Japan, Ltd., at a new data center that Kyndryl is building near Tokyo.

- In November 2024, Kyndryl launched a dedicated AI private cloud in Japan to support AI-driven innovation. Developed in collaboration with Dell Technologies through the Dell AI Factory with NVIDIA, the platform offers a secure, controlled, and sovereign cloud environment where organizations can develop, test, and deploy AI solutions to enhance competitiveness and accelerate business growth.

Japan Cloud Managed Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Service Types Covered | Managed Network Services, Managed Business Services, Managed Security Services, Managed Infrastructure Services, Managed Mobility Services, Managed Communication and Collaboration Services |

| Deployment Models Covered | Private Cloud, Public Cloud |

| Organization Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| Verticals Covered | Retail and Consumer Goods, BFSI, Telecom, Government and Public Sector, Healthcare and Lifesciences, Manufacturing, Energy and Utilities, IT, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan cloud managed services market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan cloud managed services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan cloud managed services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Cloud Managed Services Market Report

The Japan cloud managed services market was valued at USD 10.79 Billion in ?2025?.

The Japan cloud managed services market is anticipated to reach a value of USD 24.60 Billion by 2034.

Managed infrastructure services dominate the market with a share of 27.0%, driven by the scale of Japan's legacy modernization wave and the outsourcing of server, storage, virtualisation, and IaaS lifecycle operations to specialist managed service providers as enterprises retire COBOL-era core systems under the "2025 Digital Cliff" imperative.

Public cloud commands the market with a 61.0% share, reflecting hyperscaler infrastructure dominance, Japan's ISMAP Government Cloud certification framework, and enterprise preference for AWS, Microsoft Azure, and Google Cloud as the primary platforms for managed workload delivery.

Large enterprises dominate the market with 68.0% share, reflecting the scale and budget intensity of enterprise-grade managed service contracts. Japan's top-tier corporations deploy full-stack cloud managed services spanning infrastructure, security, and network layers as part of multi-year transformation programs.

IT sector leads the market with 24.0%, the highest-spending vertical, as Japan's technology companies outsource internal cloud operations to specialists, freeing scarce engineering talent to focus on product development and AI innovation rather than infrastructure management.

Kanto Region currently leads the Japan cloud managed services market, accounting for a share of 45.0%. The region's leadership is driven by Tokyo's unrivalled concentration of enterprise headquarters, government agencies, and hyperscaler data centers, making it the primary hub for managed services procurement and delivery across all service categories and vertical sectors.

Some of the major players in the Japan cloud managed services market include NTT DATA Corporation, Fujitsu Limited, NEC Corporation, Hitachi Ltd., Sakura Internet Inc., etc.

Key trends include the integration of AI-native AIOps platforms automating cloud infrastructure operations; the emergence of a two-tier ISMAP-certified sovereign versus standard managed services market; accelerating mainframe-to-cloud migration using specialized toolchains such as Kyndryl zCloud and TIS Xenlon; the bundling of managed security operations into broader infrastructure contracts as ransomware incidents escalate; and the shift from labor-based billing to outcome-based managed service contracts embedding AI and automation capabilities.

Key growth drivers include Japan's structural shortage of cybersecurity professionals compelling enterprises to outsource cloud operations; hyperscaler capacity expansion including Microsoft's USD 2.9 billion Japan investment and the June 2025 KDDI-HPE AI data center in Osaka; METI's JPY 12 trillion annual economic loss warning driving legacy modernization urgency.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)