Japan Commercial Vehicles Market Size, Share, Trends and Forecast by Vehicle Type, Engine Type, and Region, 2026-2034

Japan Commercial Vehicles Market Summary:

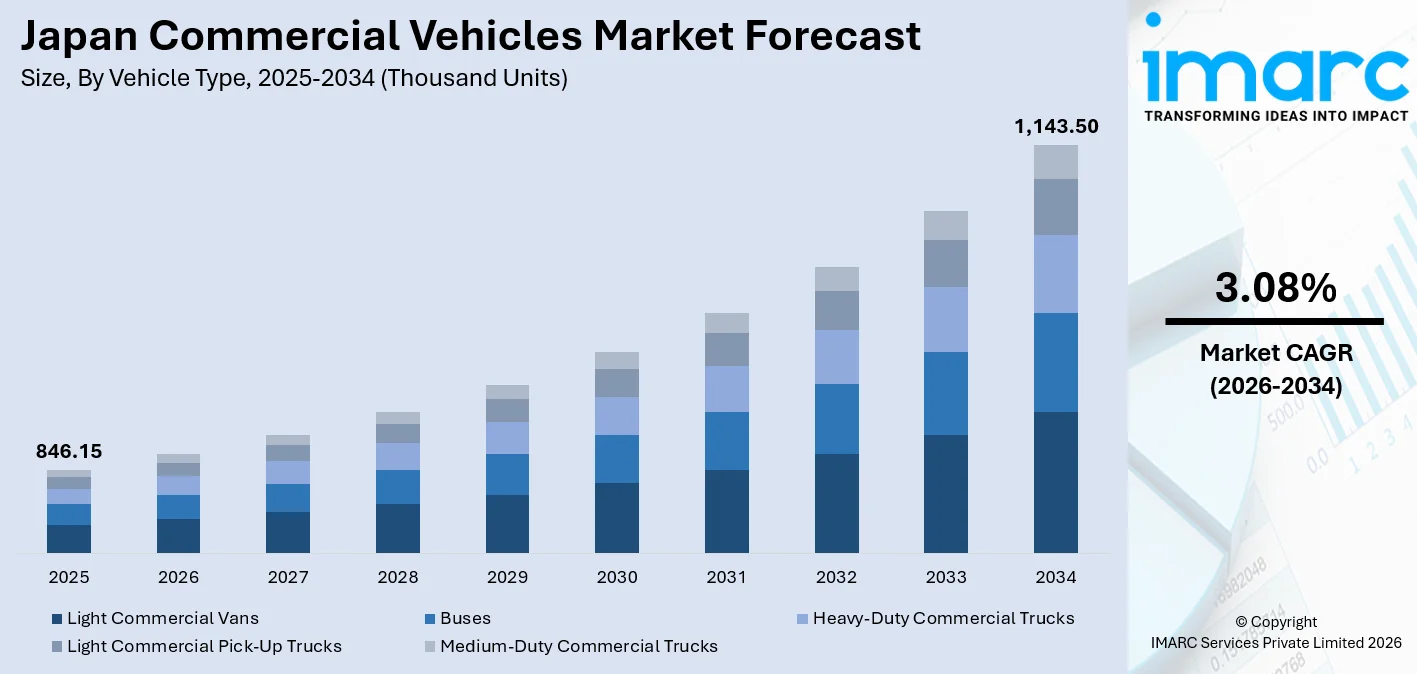

The Japan commercial vehicles market size was valued at 846.15 Thousand Units in 2025 and is projected to reach 1,143.50 Thousand Units by 2034, growing at a compound annual growth rate of 3.08% from 2026-2034.

Japan's commercial vehicles market is propelled by the rapid expansion of e-commerce logistics, growing demand for last-mile delivery solutions, and the country's ambitious push toward carbon-neutral transportation. Rising infrastructure investments, the integration of advanced driver assistance systems, and government-led electrification mandates are collectively reshaping fleet procurement patterns. The adoption of hybrid and electric powertrains across freight, public transport, and urban delivery is further contributing to the Japan commercial vehicles market share.

Key Takeaways and Insights:

- By Vehicle Type: Light commercial vans dominate the market with a share of 28.4% in 2025, driven by strong demand for urban delivery, last-mile logistics, and e-commerce fulfillment operations that require compact, maneuverable, and fuel-efficient load carriers across Japan's densely populated metropolitan corridors.

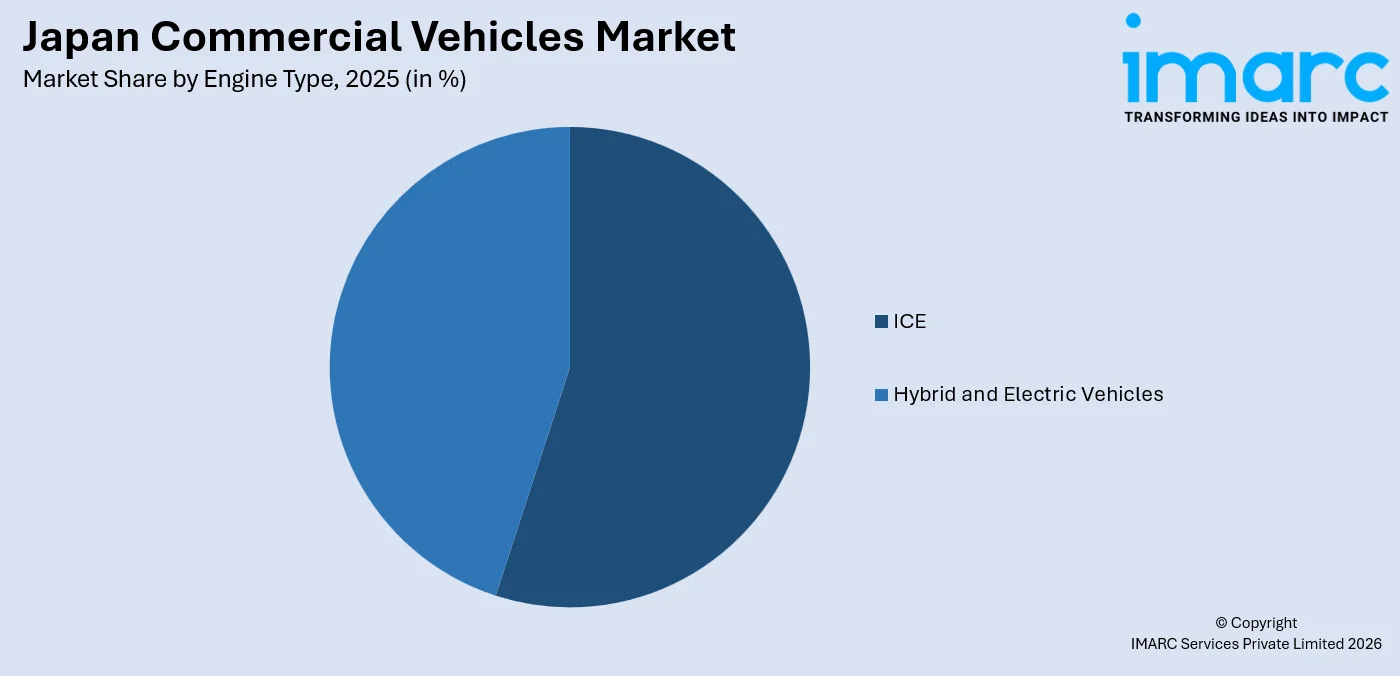

- By Engine Type: ICE leads the market with a share of 55.2% in 2025, owing to its proven reliability in long-haul and heavy-duty applications, widespread fueling infrastructure, lower acquisition costs compared to electrified alternatives, and the continued preference of fleet operators for conventional powertrains in commercial transportation.

- By Region: Kanto Region represents the largest region with 36.5% share in 2025, driven by the concentration of Japan's largest logistics hubs, manufacturing clusters, and port facilities around Tokyo and Yokohama, which generate substantial and consistent commercial vehicle demand across all vehicle types and engine categories.

- Key Players: Key players drive the Japan commercial vehicles market by expanding product portfolios, investing in electric and hybrid powertrains, and forming strategic alliances for autonomous driving technologies. Their focus on sustainable fleet solutions, telematics integration, and strengthening nationwide distribution networks accelerates adoption, meets evolving regulations, and ensures competitive positioning across diverse commercial vehicle segments and regional markets.

To get more information on this market Request Sample

Japan's commercial vehicle segment is presently undergoing a structural shift as it is influenced by various factors such as technology adoption, regulatory changes, and changes in logistics needs. The country's e-commerce segment is considered to be one of the most advanced in Asia and is currently sustaining strong demand for small vehicles used for delivering goods within cities. At the same time, Japan is currently facing a critical driver shortage in its logistics segment and is thus increasing investment in autonomous and semi-autonomous technologies used in its commercial vehicles. The regulatory environment is also playing a crucial role in the transition of Japan's commercial vehicle segment. The Japanese government has set decarbonization targets that have been approved by the cabinet and is thus forcing both manufacturers and operators to speed up their transition to cleaner alternatives. The regulatory needs are thus adding to the existing trend of transitioning to electric-powered commercial vehicles. The convergence of logistics modernization, workforce constraints, and environmental policy is compelling manufacturers to expand their zero-emission portfolios while retaining the reliability and cost-effectiveness that fleet operators demand. Strategic consolidation among legacy manufacturers is further reshaping competitive dynamics in the Japan commercial vehicles market share landscape.

Japan Commercial Vehicles Market Trends:

Surge in Last-Mile Delivery and Urban Logistics Demand

Japan's booming e-commerce ecosystem is fundamentally reshaping commercial vehicle utilization patterns. The rapid growth of home delivery services and online retail fulfillment has intensified demand for compact, efficient last-mile delivery vehicles in urban environments. Light commercial vans and pick-up trucks are seeing heightened procurement activity from logistics operators. In July 2025, Kao Corporation introduced Japan's first fully automated truck loading operation at its Toyohashi Plant, completed in collaboration with Toyota Industries Corporation to enhance warehouse-to-delivery efficiency and ease persistent labor shortages.

Integration of Advanced Driver Assistance Systems in Commercial Fleets

Japanese commercial vehicle manufacturers are increasingly embedding advanced driver assistance systems to address road safety requirements and respond to Japan's Traffic Safety Vision 2025. Fleet operators are prioritizing vehicles equipped with collision avoidance, lane departure warning, and adaptive cruise control technologies. In March 2025, Nissan conducted Japan's first public road test of a vehicle with no onboard driver in an urban environment in Yokohama's Minato Mirai district, underscoring the accelerating development of autonomous commercial vehicle capabilities and the country's readiness for next-generation fleet technology.

Electrification Push Driven by Regulatory Mandates and Corporate Sustainability Goals

Japan's commercial vehicle electrification is gaining momentum as regulatory pressure intensifies, and corporate sustainability commitments deepen. The government's target for electrified vehicles to constitute 20–30% of new light commercial vehicle sales by 2030 is compelling fleet operators to evaluate zero-emission alternatives. In January 2025, Fujitsu Limited and Sustainable Shared Transport, a division of Yamato Holdings, launched a cooperative delivery and transportation system to create a sustainable supply chain through information sharing, signaling the logistics sector's commitment to green operations and decarbonization across Japan.

Market Outlook 2026-2034:

The Japanese market for commercial vehicles is expected to record steady and consistent growth during the forecast period, with the sector benefiting from infrastructure and logistical developments, as well as the acceleration of Japan's electrification strategy. Renewal of the existing conventional vehicle fleet with hybrid, plug-in hybrid, and battery-electric variants will be accelerated, in line with Japan's carbon-neutral strategy. The Plan for Global Warming Countermeasures, adopted in February 2025, will ensure Japan continues to set ambitious carbon-neutral goals, with commercial vehicle manufacturers focused on developing next-generation powertrains. The Japanese market will also see continued growth in urban logistics, driven by e-commerce penetration, and autonomous driving technology will revolutionize freight operations, addressing the long-standing driver shortage. Strategic partnerships, including the landmark integration of Mitsubishi Fuso and Hino Motors, will redefine the competitive landscape, with efficiencies of scale driving the adoption of decarbonized commercial vehicle technology in Japan's fragmented regional markets. The market generated a revenue of 846.15 Thousand Units in 2025 and is projected to reach a revenue of 1,143.50 Thousand Units by 2034, growing at a compound annual growth rate of 3.08% from 2026-2034.

Japan Commercial Vehicles Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Vehicle Type |

Light Commercial Vans |

28.4% |

|

Engine Type |

ICE |

55.2% |

|

Region |

Kanto Region |

36.5% |

Vehicle Type Insights:

- Buses

- Heavy-Duty Commercial Trucks

- Light Commercial Pick-Up Trucks

- Light Commercial Vans

- Medium-Duty Commercial Trucks

Light commercial vans dominate with a market share of 28.4% of the total Japan commercial vehicles market in 2025.

Light commercial vans represent the most commercially active segment within Japan's commercial vehicle ecosystem, primarily driven by the country's robust e-commerce infrastructure and densely populated urban delivery corridors. Their compact dimensions make them ideally suited for navigating narrow city streets and high-density residential zones, where efficient parcel delivery is paramount. Rising consumer expectations for same-day and next-day delivery fulfillment have prompted logistics operators across major metropolitan areas to expand their light van fleets, reinforcing the segment's dominance across the country's commercial transportation landscape.

Manufacturers are actively responding to fleet electrification mandates by introducing hybrid and battery-electric variants of light commercial vans, broadening their appeal to sustainability-oriented fleet operators. Government-led fiscal incentives targeting fuel-efficient commercial vehicles have further strengthened the procurement case for advanced powertrain configurations, encouraging fleet owners to accelerate replacement cycles in favor of lower-emission alternatives. Ongoing investment in autonomous driving research and next-generation vehicle development infrastructure underscores the industry's long-term commitment to transforming light commercial van capabilities, positioning this segment at the forefront of Japan's broader commercial vehicle modernization agenda.

Engine Type Insights:

Access the comprehensive market breakdown Request Sample

- Hybrid and Electric Vehicles

- ICE

ICE leads with a share of 55.2% of the total Japan commercial vehicles market in 2025.

Internal combustion engine vehicles retain their dominant position in Japan's commercial vehicle market, underpinned by the proven reliability of diesel powertrains in demanding freight and construction applications. Extensive nationwide fueling infrastructure, established maintenance ecosystems, and comparatively lower upfront acquisition costs continue to make ICE vehicles the preferred choice for fleet operators managing large commercial fleets. Medium-duty and heavy-duty truck segments are particularly reliant on diesel ICE configurations, given the high torque requirements and operational endurance demanded in long-haul and regional distribution missions.

Despite rising momentum around electrification, ICE commercial vehicles continue to benefit from continuous efficiency improvements as manufacturers comply with Japan's increasingly stringent emission standards. Leading automotive manufacturers are actively pursuing the development of next-generation internal combustion engines compatible with electrified drivetrains, demonstrating the industry's intent to modernize rather than immediately retire ICE technology. The phased transition toward hybrid and electric configurations ensures that ICE's market share, while gradually declining, will remain substantial throughout the early years of the forecast period.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represents the largest region with 36.5% share of the total Japan commercial vehicles market in 2025.

The commanding position enjoyed by the Kanto Region in terms of commercial vehicles in Japan is a direct result of its position as the premier economic hub in the country. The Kanto Region is home to the most populous concentration of manufacturing plants, logistics parks, and distribution centers in all of Japan. The Kanto region is home to a significant share of Japan's port operations, including the Tokyo Port and Yokohama Port. These ports are responsible for a significant share of import and export activities in Japan, thus ensuring a steady demand for commercial vehicles of all categories.

The Kanto Region is also a leader in terms of the use of electric and autonomous commercial vehicles in Japan, owing to a variety of government incentives in the Tokyo Metropolitan Area. The region is home to a dense concentration of economic and technological infrastructure, which has led to a number of technology ecosystems. It is thus no surprise that the Kanto Region is the proving ground for all forms of cutting-edge commercial vehicle technologies in all of Japan.

.webp)

Market Dynamics:

Growth Drivers:

Why is the Japan Commercial Vehicles Market Growing?

Rapid Expansion of E-Commerce and Last-Mile Logistics Infrastructure

Japan's e-commerce sector has experienced sustained and significant growth, fundamentally transforming the country's logistics landscape and commercial vehicle procurement patterns. The surge in online retail activity has created intense demand for efficient last-mile delivery solutions, with logistics operators expanding their fleets of light commercial vans and pick-up trucks to meet consumer expectations for rapid, reliable parcel delivery. Japan's high population density in metropolitan areas, combined with its sophisticated retail infrastructure, has accelerated the proliferation of same-day and next-day delivery services, placing considerable pressure on fleet operators to scale their delivery capacity. Furthermore, the integration of digital logistics management platforms has improved vehicle routing efficiency, enabling operators to extract greater operational value from their commercial vehicle fleets. Suburban and rural e-commerce penetration is also increasing, expanding the geographic footprint of last-mile logistics requirements beyond traditional urban centers. This expansion is necessitating procurement of versatile commercial vehicles capable of navigating both urban traffic environments and rural access roads. Fleet electrification within the last-mile delivery segment is also accelerating, as operators seek to reduce operating costs while complying with evolving urban emission regulations, further stimulating commercial vehicle market growth in Japan.

Government Infrastructure Investment and Transportation Policy Support

Japan's central and municipal governments are channeling substantial financial resources into infrastructure modernization programs that directly benefit the commercial vehicle sector. Road expansion projects, highway rehabilitation programs, and intermodal freight terminal upgrades are improving the operational efficiency of commercial vehicle fleets across the country. Government-sponsored subsidies for zero-emission commercial vehicles, including clean energy vehicle grant programs and vehicle weight tax exemptions for fuel-efficient models, are reducing the financial barriers associated with fleet modernization. Cabinet-approved decarbonization commitments, with commercial vehicle electrification explicitly identified as a strategic priority for achieving carbon neutrality, are providing regulatory certainty that incentivizes both fleet operators and manufacturers to accelerate investment in hybrid and electric commercial vehicle platforms. Municipal low-emission zone initiatives in major urban agglomerations are further compelling fleet owners to procure compliant vehicles ahead of enforcement deadlines, creating a predictable and sustained demand environment for commercial vehicle market expansion throughout the forecast period.

Technological Advancements in Autonomous and Semi-Autonomous Commercial Vehicle Systems

Japan's commercial vehicle industry is experiencing a technology-driven transformation accelerated by chronic driver shortages, aging demographics, and government-backed autonomous mobility initiatives. Regulatory restrictions on driver overtime hours have created significant capacity constraints in Japan's freight transportation network, compelling manufacturers and technology developers to respond with rapid deployment of advanced autonomous systems across multiple levels of driving automation. Japan's Ministry of Land, Infrastructure, Transport and Tourism has been actively supporting demonstration projects for autonomous highway freight operations, creating a regulatory environment conducive to technology adoption. Sustained investment in dedicated autonomous driving test infrastructure by leading commercial vehicle manufacturers further reinforces the industry's long-term commitment to autonomous capability development. The progressive integration of advanced driver assistance technologies including collision avoidance, lane keeping, and adaptive cruise control is also improving vehicle safety profiles, reducing accident-related downtime and insurance costs for fleet operators, compelling fleet managers to prioritize technology-equipped commercial vehicles and stimulating demand across the market.

Market Restraints:

What Challenges the Japan Commercial Vehicles Market is Facing?

High Upfront Costs of Electrified Commercial Vehicles

The transition toward hybrid and battery-electric commercial vehicles is constrained by significantly higher upfront acquisition costs compared to conventional ICE vehicles. Fleet operators, particularly small and medium-sized logistics companies, face considerable capital expenditure pressure when electrifying their fleets. While government subsidies partially offset these costs, total cost of ownership calculations over typical commercial vehicle lifecycle periods remain challenging for operators with limited access to capital or short-term fleet planning horizons, slowing the overall rate of electrification adoption across Japan's commercial vehicle fleet base.

Insufficient Charging and Hydrogen Refueling Infrastructure

Japan's commercial vehicle electrification agenda is materially constrained by gaps in charging infrastructure, particularly for heavy and medium-duty vehicles with high energy requirements and demanding duty cycles. Dedicated high-capacity charging facilities at logistics hubs, highway rest stops, and industrial zones remain insufficient relative to projected fleet electrification timelines. Hydrogen refueling infrastructure, critical for fuel cell commercial vehicles targeting long-haul freight, is also underdeveloped outside major metropolitan corridors, limiting the operational viability of zero-emission commercial vehicles across Japan's regional and rural transportation networks.

Acute Shortage of Qualified Commercial Vehicle Drivers

Japan's commercial transportation sector is experiencing a structural deficit of qualified truck and bus drivers, exacerbated by the aging workforce, declining youth interest in driving careers, and regulatory restrictions on driver overtime hours that took effect in April 2024. This driver shortage reduces the effective operational capacity of existing commercial vehicle fleets while complicating fleet expansion strategies for logistics operators. Although autonomous vehicle development is progressing, commercially deployable Level 4 autonomous freight solutions remain in demonstration phases, leaving fleet operators vulnerable to chronic driver supply constraints throughout the near-to-medium forecast term.

Competitive Landscape:

Japan's commercial vehicles market has a highly competitive profile, with a small number of well-established local players dominating the market. These players compete with each other based on innovations in the powertrains, telematics, geographical reach, and total cost of ownership. The industry has witnessed strategic consolidations, with the top players forming partnerships to share the costs of developing the next generation of electrified and autonomous vehicles. The players are now competing based on the adoption of connected vehicle technology, AI-based fleet management, and software updates. The international players in the commercial vehicle industry are looking for opportunities to gain a foothold in the Japanese market, specifically in the segment of electric buses and zero-emission trucks. Thus, the competitive intensity of the commercial vehicles market of Japan is set to increase as the transition towards electrified vehicles gains momentum, thereby forcing all the players to hasten the development of battery, charging, and autonomous driving technology.

Japan Commercial vehicles Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Buses, Heavy-Duty Commercial Trucks, Light Commercial Pick-Up Trucks, Light Commercial Vans, Medium-Duty Commercial Trucks |

| Engine Types Covered | Hybrid and Electric Vehicles, ICE |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Commercial Vehicles Market Report

The Japan commercial vehicles market size was valued at 846.15 Thousand Units in 2025.

The Japan commercial vehicles market is expected to grow at a compound annual growth rate of 3.08% from 2026-2034 to reach 1,143.50 Thousand Units by 2034.

Light commercial vans dominated the market with a share of 28.4%, driven by strong urban delivery demand, e-commerce fulfillment growth, and their compact adaptability across Japan's densely populated metropolitan delivery corridors, making them the most widely procured vehicle type in the market.

Key factors driving the Japan commercial vehicles market include rapid e-commerce expansion, government infrastructure investment, electrification mandates, autonomous driving technology adoption, and logistics sector modernization to address Japan's chronic commercial driver shortage.

Major challenges include high upfront costs of electrified commercial vehicles, insufficient charging and hydrogen refueling infrastructure, an acute shortage of qualified commercial vehicle drivers, and the technological and regulatory complexity of deploying commercially viable autonomous freight solutions at scale.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade