Japan Confectionery Market Size, Share, Trends and Forecast by Product Type, Age Group, Price Point, Distribution Channel, and Region, 2026-2034

Japan Confectionery Market Size, Share, Trends & Forecast (2026-2034)

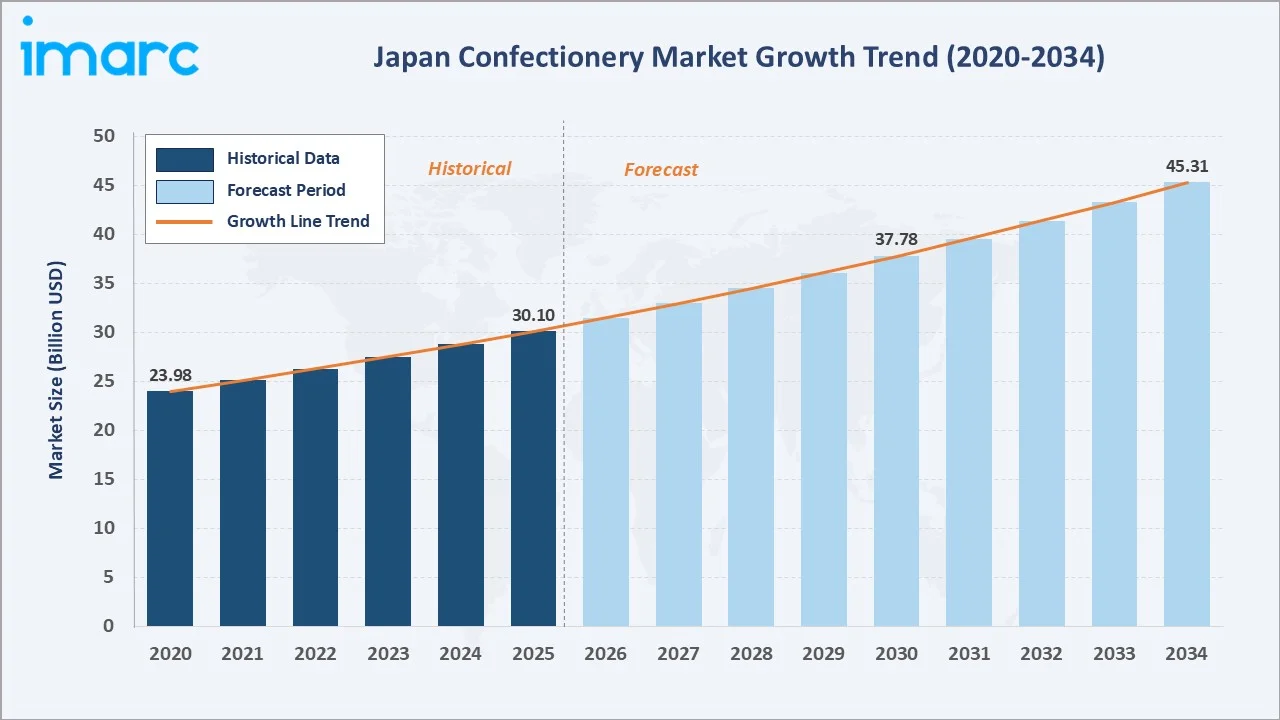

The Japan confectionery market was valued at USD 30.10 Billion in 2025 and is projected to reach USD 45.31 Billion by 2034, exhibiting a CAGR of 4.65% during 2026-2034. Rising disposable incomes, deep-rooted gifting culture, and continuous flavor innovation are the primary drivers shaping market growth, supported by recent product launches such as Meiji Holdings Co., Ltd.'s Almond Chocolate Crunch Okinawa Salt range introduced in June 2025, which underscores the appetite for premium, regionally inspired sweets.

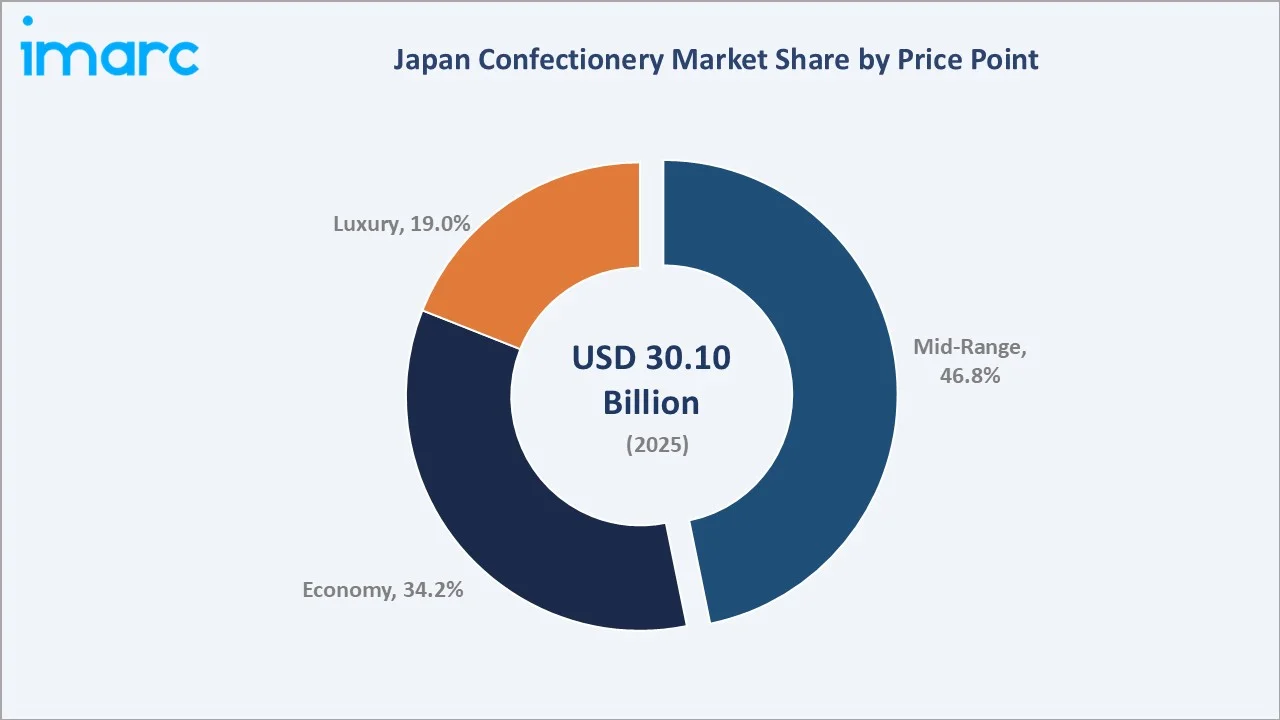

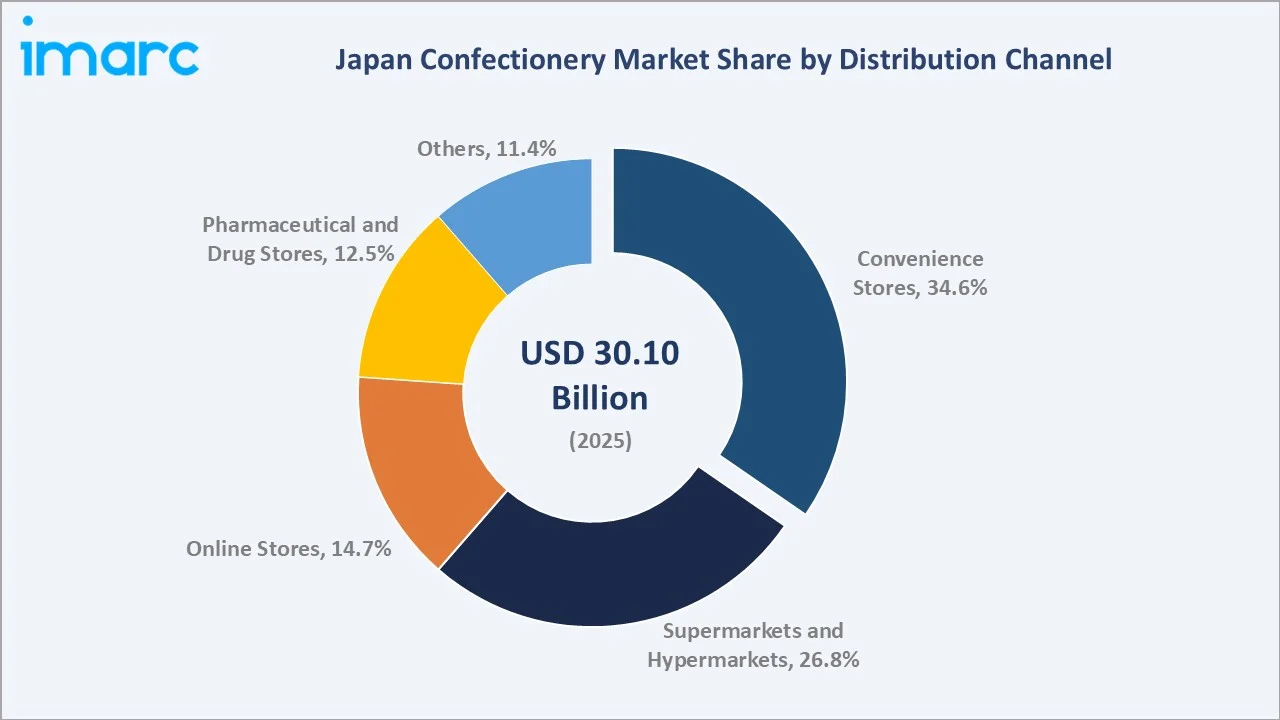

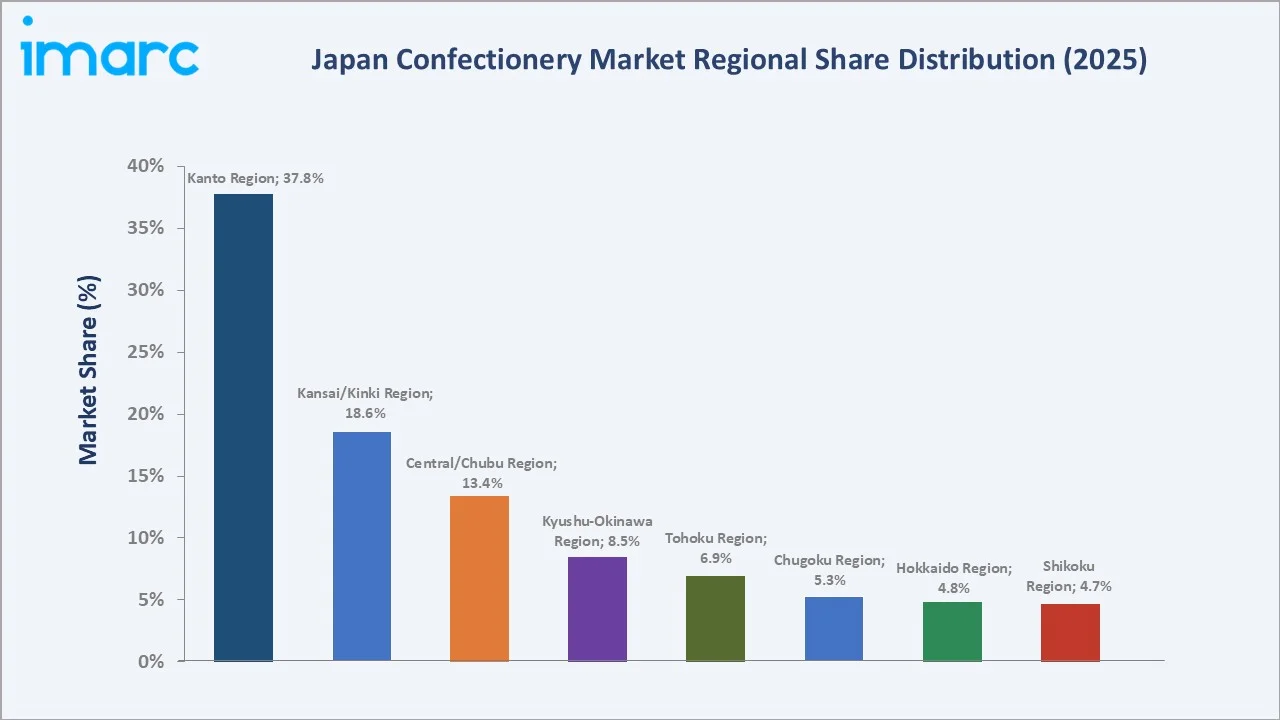

Mid-range leads the price point segment at 46.8%, convenience stores dominate distribution channel at 34.6%, and Kanto Region commands 37.8% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 30.10 Billion |

|

Forecast Market Size (2034) |

USD 45.31 Billion |

|

CAGR (2026-2034) |

4.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (37.8%, 2025) |

|

Fastest Growing Region |

Hokkaido Region (4.8%, 2025) |

|

Leading Price Point |

Mid-Range (46.8%, 2025) |

|

Leading Distribution Channel |

Convenience Stores (34.6%, 2025) |

The Japan confectionery market expanded from USD 23.98 Billion in 2020 to USD 30.10 Billion in 2025, lifted by rising disposable incomes, the steady recovery of inbound tourism, and continuous flavor innovation. Anchored at USD 37.78 Billion in 2030, the forecast to USD 45.31 Billion by 2034 is supported by strong demand for premium gifting, e-commerce expansion, and health-functional sweets across both urban and regional markets.

To get more information on this market, Request Sample

CAGR trajectories across the price point and distribution channel sub-segments show online stores and luxury price point expanding faster than the overall 4.65% market CAGR, driven by direct-to-consumer (D2C) brand growth, premiumization, and digital gifting platforms.

Executive Summary

The Japan confectionery market is on a steady growth path from USD 23.98 Billion in 2020 to a projected USD 45.31 Billion by 2034. Sweets have remained an integral part of Japanese daily life, gifting traditions, and seasonal celebrations. Rising disposable incomes, premiumization, and broadening pop-culture collaborations are encouraging households to trade up to higher-quality chocolates, gummies, and baked confections. Continuous innovations in flavor profiles and packaging formats are reinforcing demand across both urban hubs and regional cities.

Mid-range dominates price point at 46.8% in 2025, supported by widely available branded chocolates, biscuits, and gummies sold through convenience stores and supermarkets. Convenience stores lead distribution channel at 34.6%, fueled by Japan's high store density, fresh product rotation, and impulse-purchase behavior. Kanto Region commands 37.8% share, led by Tokyo metropolitan demand, premium retail concepts, and tourist spending. In November 2024, FamilyMart launched the ‘Neo Wagashi’ line in Japan, reimagining traditional dorayaki and Fluffy Nama Daifuku to appeal to younger consumers, illustrating how legacy formats are being refreshed for modern shoppers.

Key Market Insights

|

Insight |

Data |

|

Leading Price Point |

Mid-Range - 46.8% share (2025) |

|

Second Price Point |

Economy - 34.2% share (2025) |

|

Leading Distribution Channel |

Convenience Stores - 34.6% share (2025) |

|

Second Distribution Channel |

Supermarkets and Hypermarkets - 26.8% share (2025) |

|

Leading Region |

Kanto Region - 37.8% share (2025) |

|

Second Region |

Kansai/Kinki Region - 18.6% share (2025) |

|

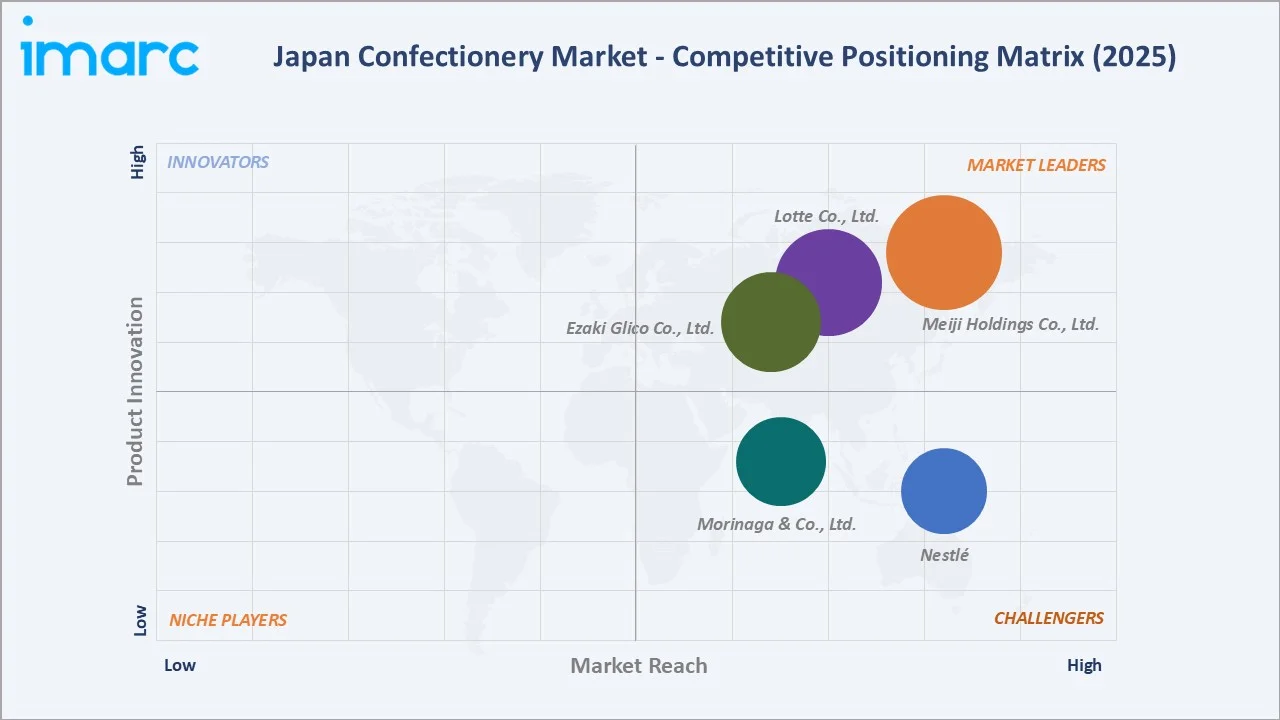

Top Companies |

Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., Morinaga & Co., Ltd., and Nestlé |

Key Analytical Observations Expanding on the Data Above:

- Mid-range dominance at 46.8% is supported by Japan's preference for value-for-money branded chocolates, gummies, and biscuits sold through convenience stores and supermarkets. Familiar local brands and consistent quality reinforce repeat purchase across everyday occasions.

- Economy share at 34.2% reflects strong demand for affordable indulgence among younger consumers, school-going children, and price-sensitive households, with frequent promotional pricing and multi-pack formats keeping the segment competitive.

- Convenience stores leadership at 34.6% is anchored by Japan’s convenience store network, which comprised more than 56,000 outlets in 2025, providing round-the-clock availability, frequent product rotation, and unmatched access to limited-edition seasonal launches.

- Supermarkets and hypermarkets at 26.8% serve household-level grocery missions, with multi-pack family formats, ingredient transparency, and bulk gifting assortments anchoring weekly shopper baskets across regional cities.

- Kanto Region at 37.8% leads owing to Tokyo's dense retail footprint, corporate gifting demand, and tourism-driven specialty purchases, with Greater Tokyo continuing to anchor premium brand launches and flagship store concepts.

Japan Confectionery Market Overview

Confectionery in Japan covers chocolate, gummies, hard candies, caramels, biscuits, baked sweets, and traditional wagashi, sold in formats ranging from individual on-the-go items to elaborate gift assortments. The category blends domestic heritage products with global brand offerings tailored to Japanese taste profiles such as matcha, yuzu, sakura, and roasted soy.

The ecosystem connects upstream cocoa, sugar, and dairy suppliers with domestic manufacturers, specialty packaging firms, and a dense retail network spanning convenience stores, supermarkets, drug stores, department store food halls, and rapidly expanding online channels. Strict food-safety regulation and a strong gifting culture together shape product development priorities across the value chain.

Market Dynamics

To evaluate market opportunities, Request Sample

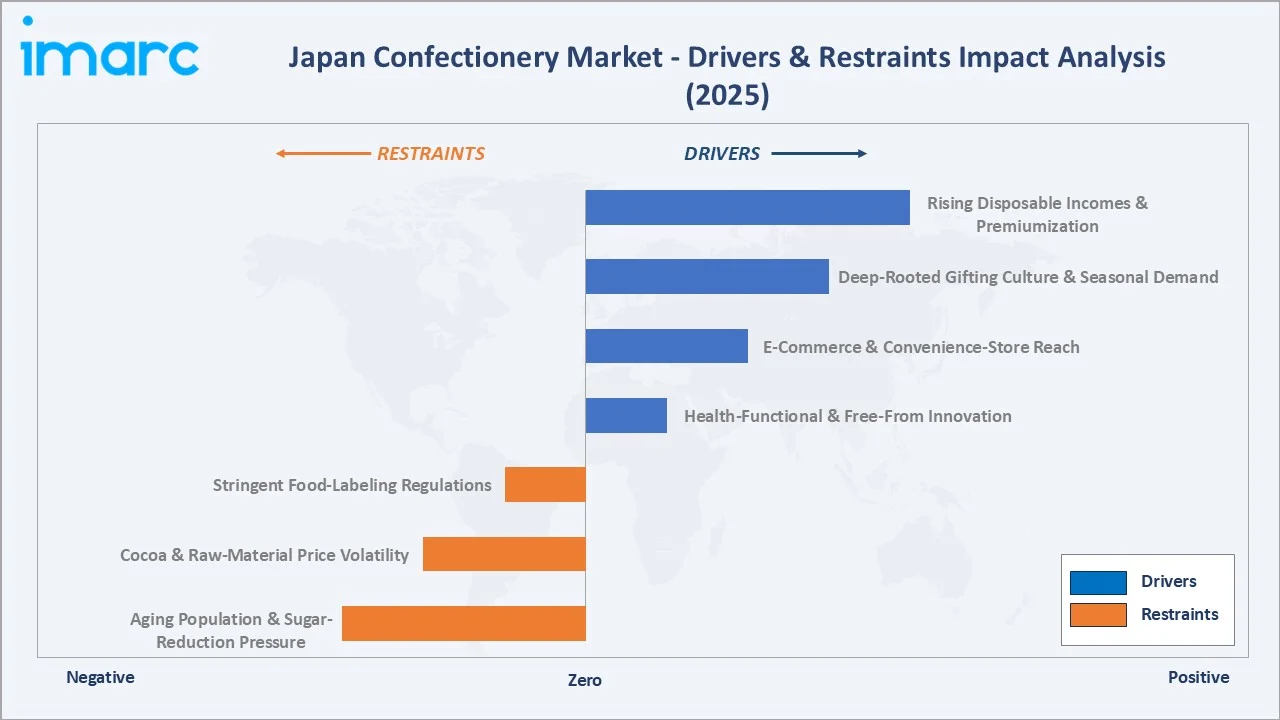

Market Drivers

- Rising Disposable Incomes and Premiumization: Steady wage growth is encouraging Japanese consumers to upgrade to premium chocolate, single-origin cacao, and artisanal patisserie, lifting average per-purchase value across both gifting and self-consumption occasions.

- E-commerce and Convenience-Store Reach: The combination of dense convenience store coverage and rapid e-commerce growth is broadening category access. As per IMARC Group, the Japan e-commerce market size was valued at USD 286.5 Billion in 2025.

- Deep-Rooted Gifting Culture and Seasonal Occasions: Valentine's Day, White Day, Christmas, Obon, and year-end corporate gifting sustain steady demand for premium boxed assortments, while seasonal limited editions encourage repeat purchase across calendar events.

- Health-Functional and Free-From Innovation: Functional chocolate with high-cacao polyphenols, reduced-sugar gummies, and gluten-free or dairy-free formats are creating new growth pockets, particularly among older and wellness-focused consumers.

Market Restraints

- Cocoa and Raw-Material Price Volatility: In early April 2026, Cocoa prices elevated to 3391.00 USD/T, the highest since March 2026, amid the Israel–Iran–USA conflict, prompting major Japanese makers to raise retail prices, compressing volumes in price-sensitive categories.

- Aging Population and Sugar-Reduction Pressure: Japan's rapidly aging population and rising prevalence of lifestyle diseases are limiting per-capita consumption of sugar-rich confectionery, pushing manufacturers toward lower-sugar reformulations that often carry thinner margins.

- Stringent Food-Labeling Regulations: Strict labeling rules under the Food Labeling Act, including allergen, nutrition, and country-of-origin requirements, increase compliance costs and slow product launch cycles, especially for smaller brands.

Market Opportunities

- Inbound Tourism and Souvenir Demand: Japan's recovery in inbound tourist arrivals is driving demand for regional specialties, omiyage gift boxes, and matcha-flavored sweets, creating premium-price opportunities in airports, train stations, and tourist hubs.

- Digital and Pop-Culture Collaborations: Anime, gaming, and character collaborations are creating limited-edition collectible confectionery formats that drive both volume spikes and brand premium, with strong cross-generational appeal.

Market Challenges

- Saturated Domestic Market: With high per-capita consumption already established, growth must come from premiumization, exports, and new occasions rather than volume gains, putting innovation pressure on incumbents.

- Competitive Intensity and Shelf Space: Convenience-store shelves are tightly contested, making it difficult for smaller domestic players and new entrants to secure listing without significant trade promotion investment.

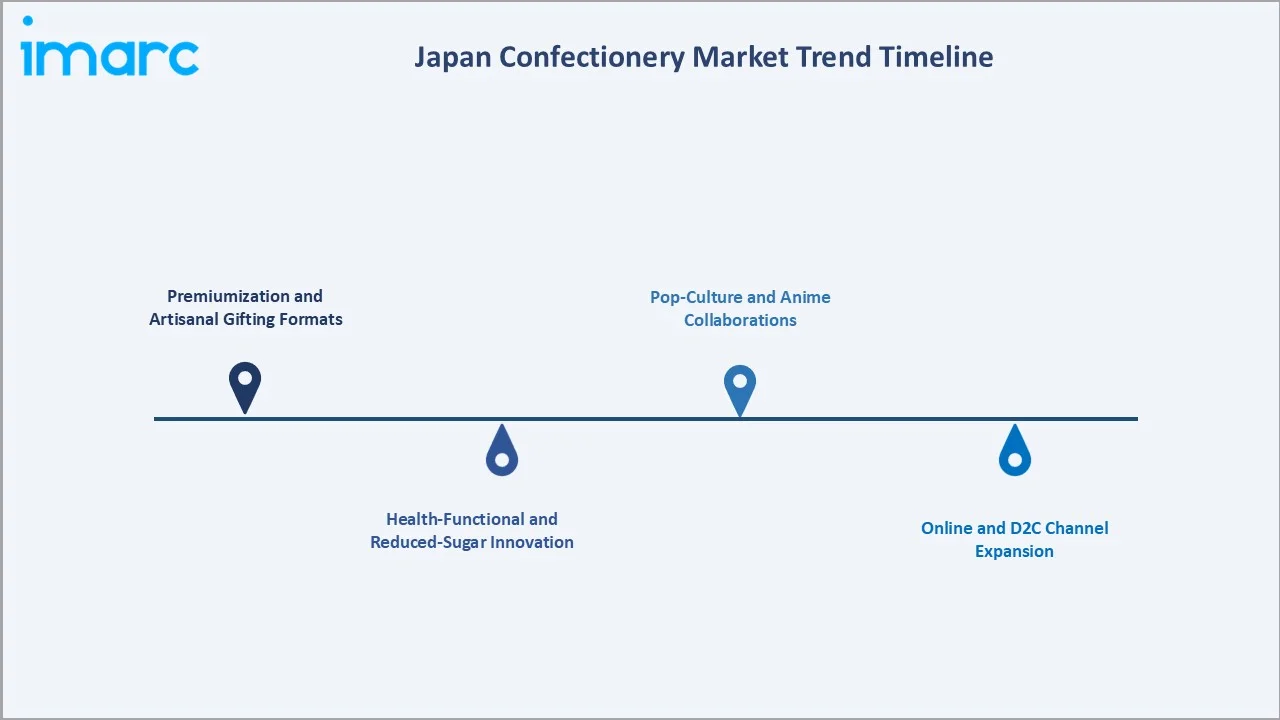

Emerging Market Trends

1. Premiumization and Artisanal Gifting Formats

Premium and artisanal confectionery is gaining ground as Japanese consumers trade up for special occasions, with department-store food halls and specialty boutiques anchoring single-origin chocolates, hand-crafted wagashi, and small-batch patisserie. Brands are responding with elevated packaging, limited annual editions, and seasonal collections aligned to festivals and gifting calendars.

2. Health-Functional and Reduced-Sugar Innovation

Functional and reduced-sugar formats are reshaping shelves as makers respond to wellness-conscious consumers. In June 2024, Meiji Holdings Co., Ltd. introduced a new chocolate line that used fructooligosaccharides (FOS) as a sugar substitute, positioning the launch as a gut-friendly indulgence. Adoption of high-cacao polyphenol formats and reduced-sugar gummies is broadening the daily-consumption base. The trend is particularly relevant for older consumers and dieters, encouraging manufacturers to invest in clean-label reformulations.

3. Pop-Culture and Anime Collaborations

Confectionery brands are increasingly partnering with anime, gaming, and entertainment franchises to create limited-edition packaging, collectible wrappers, and themed flavors. Such collaborations drive volume spikes, social-media traction, and cross-generational appeal, attracting both younger consumers and adult fans. Augmented reality (AR) wrappers and digital collectibles are extending the experience beyond consumption.

4. Online and D2C Channel Expansion

Online stores are emerging as a high-growth channel, offering access to regional specialties, limited editions, and curated gifting hampers that are not stocked nationwide. Brand-owned websites and live-commerce platforms are reshaping shopper journeys, especially for premium, niche, and occasion-driven products.

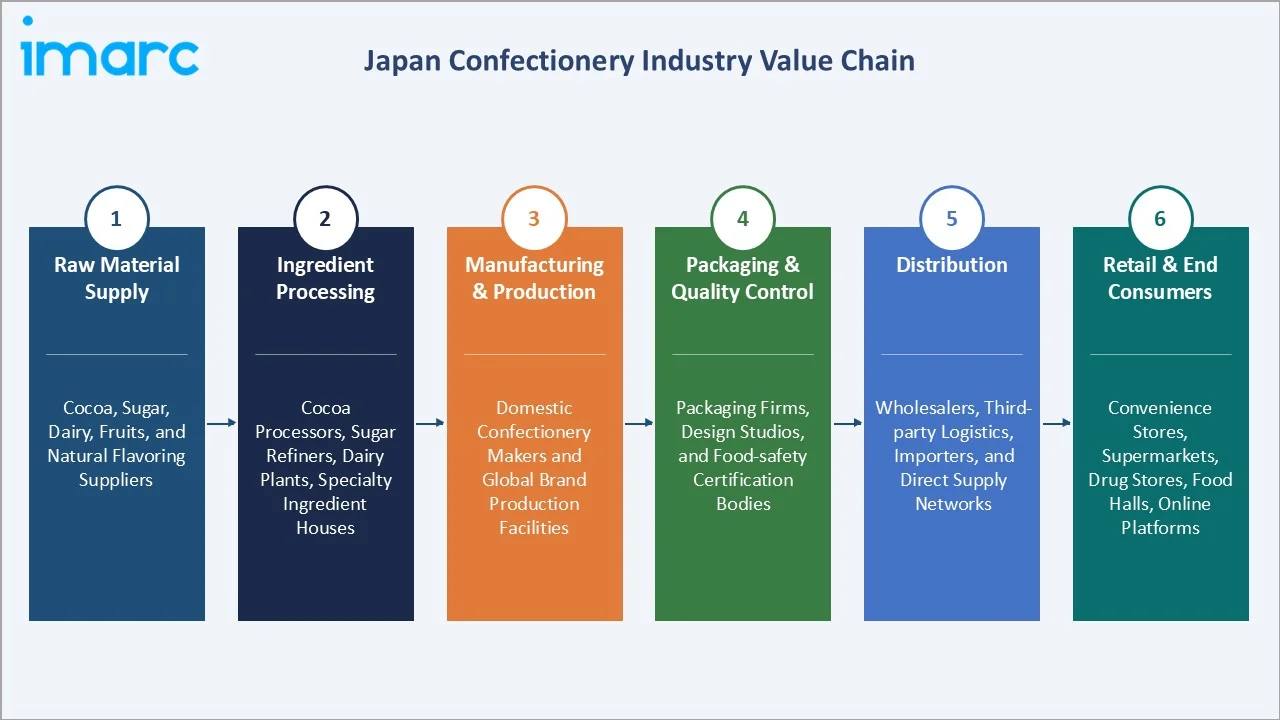

Industry Value Chain Analysis

The Japan confectionery value chain runs from upstream cocoa, sugar, and dairy sourcing through manufacturing, packaging, and distribution to a dense omnichannel retail network. Brand equity, channel relationships, and limited-edition execution capabilities create the strongest competitive advantage in this category.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of cocoa beans, sugar, dairy ingredients, fruits, and natural flavorings sourced from domestic and international markets |

|

Ingredient Processing |

Cocoa processors, sugar refiners, dairy plants, and specialty ingredient houses providing inputs for chocolate, biscuits, and gummies |

|

Manufacturing & Production |

Domestic confectionery makers and global brands operating production facilities for chocolates, gummies, hard candies, and baked sweets across Japan |

|

Packaging & Quality Control |

Packaging firms, design studios, and certification bodies that ensure compliance with Japan Agricultural Standards and food-labeling laws |

|

Distribution |

Wholesalers, third-party logistics partners, importers, and company-direct supply networks reaching urban and regional retailers |

|

Retail & End Consumers |

Convenience stores, supermarkets, drug stores, department-store food halls, online platforms, and household consumers across Japan |

Vertically integrated leaders, which manage in-house cocoa processing and dairy operations, achieve superior cost control and supply security versus smaller players reliant on third-party sourcing.

Technology Landscape in the Japan Confectionery Industry

Ingredient and Flavor Innovation

Reduced-sugar formulations, plant-based alternatives, and functional ingredients, such as high-polyphenol cacao, prebiotic fibers, and GABA, are reshaping new product development. Japanese makers are pairing traditional flavors like matcha, yuzu, and sakura with modern functional claims, creating differentiated portfolios for both domestic and export markets.

Packaging and Sustainability

Lightweight, recyclable, and biodegradable packaging is gaining traction as Japanese retailers and consumers respond to plastic-reduction targets. Brands are also investing in resealable formats, single-portion gift wraps, and limited-edition collectible designs that combine convenience with premium presentation, supporting both gifting and on-the-go consumption.

Smart Manufacturing and Artificial Intelligence (AI)-Driven NPD

Major confectionery firms are deploying automation, predictive demand forecasting, and AI-assisted flavor development to compress innovation cycles. Convenience-store partners are integrating these capabilities into joint NPD programs, enabling rapid limited-edition launches and tighter alignment with shifting consumer preferences across regions.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | 🔒 | 🔒 | 2025 |

| Age Group | 🔒 | 🔒 | 2025 |

| Price Point | Mid-Range | 46.8% | 2025 |

| Distribution Channel | Convenience Stores | 34.6% | 2025 |

| Region | Kanto Region | 37.8% | 2025 |

By Price Point

Mid-range commands a 46.8% share in 2025, supported by trusted local brands, frequent product rotation, and broad availability across convenience stores and supermarkets. The tier captures everyday consumption, school-related purchases, and routine self-treats, anchored by enduring favorites, such as branded chocolates, biscuits, and gummies.

To access detailed market analysis, Request Sample

Economy at 34.2% in 2025 captures price-sensitive households and younger consumers, with multi-pack formats, promotional pricing, and private-label alternatives anchoring repeat purchase. Luxury holds 19.0% of the market share.

By Distribution Channel

Convenience stores dominate with 34.6% share in 2025, leveraging Japan's extensive store network, frequent product rotation, and exclusive limited-edition launches that drive impulse purchase. The channel is also the primary route to market for new product introductions and seasonal campaigns, sustaining its leadership across both indulgence and gifting occasions.

Supermarkets and hypermarkets hold 26.8% share, anchoring weekly grocery missions and family-format purchases. Their dominance is reinforced by wide product assortments, promotional pricing strategies, and the ability to offer bulk discounts that appeal to value-conscious households.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.8% |

Dense urban consumer base, strong gifting culture, premium retail concepts, and high tourist footfall |

|

Kansai/Kinki Region |

18.6% |

Rich culinary heritage, established confectionery brands, and vibrant department-store food hall ecosystems |

|

Central/Chubu Region |

13.4% |

Industrial wage base, strong convenience store penetration, and growing demand for premium and seasonal products |

|

Kyushu-Okinawa Region |

8.5% |

Tourism-driven souvenir demand, regional specialties, and rising health-functional confectionery adoption |

|

Tohoku Region |

6.9% |

Locally inspired flavors, fresh ingredients, and steady demand for traditional and seasonal sweet products |

|

Chugoku Region |

5.3% |

Traditional rice-based confectionery heritage, regional gifting, and growing online channel penetration |

|

Hokkaido Region |

4.8% |

High-quality dairy ingredients, premium chocolate brands, and strong tourism-led specialty purchases |

|

Shikoku Region |

4.7% |

Steady household consumption, regional confectionery specialties, and gradual modern retail expansion |

Kanto Region at 37.8% in 2025 leads the market, anchored by Tokyo's dense retail network, premium gifting demand, and consistently high tourist footfall. Mature flagship store concepts, department-store food halls, and a concentration of corporate gifting sustain leadership in both volume and value across confectionery categories.

Kansai/Kinki Region at 18.6% is anchored by Osaka, Kyoto, and Kobe, offering a strong mix of traditional wagashi, premium imports, and modern confectionery innovation. Hokkaido Region at 4.8% is the fastest-growing region through 2034, supported by high-quality dairy ingredients, premium chocolatier brands, and tourism-led specialty purchases.

Competitive Landscape

The Japan confectionery market is moderately concentrated, with leading domestic players such as Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., and Morinaga & Co., Ltd. dominating brand awareness and shelf space. Global players including Nestlé Japan Ltd. and Mondelez Japan Ltd. compete through established global brands and frequent limited-edition launches, while smaller specialists serve niche premium and regional segments.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Meiji Holdings Co., Ltd. |

Meiji Milk Chocolate, Hello Panda |

Leader |

Product innovation, brand expansion, and strengthening distribution networks |

|

Lotte Co., Ltd. |

Xylitol Gum, Yukimi Daifuku |

Leader |

Portfolio diversification, premium positioning, and expansion across new consumer segments |

|

Ezaki Glico Co., Ltd. |

Pocky, Pretz |

Leader |

Continuous product innovation, global brand expansion, and strategic partnerships |

|

Morinaga & Co., Ltd. |

Hi-Chew, Chocoball, Choco Monaka Jumbo |

Challenger |

Heritage brand strengthening, international expansion, and health-oriented innovation |

|

Nestlé |

KitKat, Aero |

Challenger |

Localized product innovation, premiumization, and channel diversification |

Key players include Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., Morinaga & Co., Ltd., and Nestlé, among others.

Key Company Profiles

Meiji Holdings Co., Ltd.

Meiji Holdings Co., Ltd., headquartered in Tokyo, is the leading Japanese confectionery and dairy company. The group is a long-standing leader in chocolate and gummy confectionery in Japan. It continues to strengthen its position through continuous product innovation and expansion into health-focused and functional confectionery segments.

- Product Portfolio: Meiji Milk Chocolate, Chocolate Kouka high-cacao range, Hello Panda biscuits, Yan Yan, and a broad gummy and dairy portfolio.

- Recent Developments: The company has expanded its portfolio with limited-edition, regionally inspired chocolate variants and introduced new formulations using alternative sweeteners to cater to growing health-conscious demand.

- Strategic Focus: Vertical integration across cocoa processing and dairy, broad innovation across health-functional and premium chocolate, and deep convenience store and supermarket relationships nationwide.

Ezaki Glico Co., Ltd.

Ezaki Glico Co., Ltd., headquartered in Osaka, is a major Japanese confectionery and food company best known for its Pocky and Pretz snack-confectionery platforms. The company sells products in several countries across North America, Asia-Pacific, and Europe.

- Product Portfolio: Pocky chocolate-coated pretzel sticks, Pretz savory pretzel sticks, Almond Chocolate, and a range of GABA-functional chocolates.

- Recent Developments: Ezaki Glico has continued to expand its global Pocky franchise, while rolling out limited-edition flavors aligned with Japanese seasons and tourism trends. The company is also strengthening its overseas presence through localized product adaptations and wider distribution partnerships across key international markets.

- Strategic Focus: Snack-confectionery crossover positioning, global Pocky and Pretz platforms, functional health innovation through GABA chocolate, and partnership-led international growth.

Morinaga & Co., Ltd.

Morinaga & Co., Ltd., headquartered in Tokyo and established in 1899, is one of Japan's oldest confectionery companies, with a heritage anchored in milk caramel and chocolate. The Hi-Chew chewy candy brand is sold in many countries, including the United States.

- Product Portfolio: Hi-Chew chewy candy, Milk Caramel, Choco Ball, Choco Monaka Jumbo, and Angel Pie marshmallow biscuit products.

- Recent Developments: Morinaga has continued to expand the international footprint of Hi-Chew with new flavors targeted at the United States and Asian markets, while investing in functional and amazake-based products in Japan to address health-conscious consumers.

- Strategic Focus: Heritage-led brand portfolio, leadership in caramel and chewy candy, international Hi-Chew expansion, and growing presence in functional and reduced-sugar formats.

Market Concentration Analysis

The Japan confectionery market is moderately concentrated, with the top five companies, including Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., Morinaga & Co., Ltd., and Nestlé, estimated to hold a substantial portion of total retail value share in 2025.

Barriers to entry include scale-driven manufacturing economics, established convenience store and supermarket relationships, strict Japan Agricultural Standards compliance, and the high marketing cost of building brand recognition in a heavily contested category.

Consolidation pressures continue through international expansion of domestic brands, joint ventures, and selective acquisitions of artisanal or premium players. Scale advantages in production, distribution, and trade-marketing further reinforce the position of established leaders in the Japan confectionery market share.

Investment & Growth Opportunities

Fastest-Growing Segments

Online stores expand faster than the overall 4.65% market CAGR through 2034, driven by D2C brand sites and curated gifting. Luxury price point is the fastest-growing price segment, fueled by premium gifting, artisanal patisserie, and imported chocolatiers.

Emerging Markets

Hokkaido Region is the fastest-growing regional market through 2034, supported by premium dairy-based confectionery and tourism-led specialty purchases. Kyushu-Okinawa offers strong tourism-driven growth, while Chugoku and Tohoku represent regional opportunities driven by local heritage flavors and gradual modern retail expansion.

Investment Trends

Investment is concentrated in functional and reduced-sugar formulations, premium gifting brands, sustainable packaging, and digital D2C platforms. Strategic interest is also building in regional artisans, international Hi-Chew-style brand expansion, and pop-culture-driven limited-edition partnerships.

Future Market Outlook (2026-2034)

The Japan confectionery market is forecast to expand from USD 30.10 Billion in 2025 to USD 45.31 Billion by 2034 at a CAGR of 4.65%, adding approximately USD 15.21 Billion in incremental annual market value over the forecast period.

Four forces will shape the market through 2034: continued premiumization and gifting-led growth; rising adoption of health-functional and reduced-sugar formats; rapid expansion of online and D2C channels; and pop-culture-driven limited-edition launches that command price premiums.

By 2034, premium and luxury tiers are expected to capture a meaningfully larger share of value, online channels are likely to exceed one-fifth of total sales, and functional confectionery is expected to anchor everyday-consumption growth across both urban hubs and regional cities.

Research Methodology

Primary Research

Primary research included interviews with senior product, marketing, and supply-chain leaders at confectionery manufacturers, convenience-store and supermarket category buyers, online platform operators, and packaging specialists, validating market sizing, channel splits, and price-point evolution.

Secondary Research

Secondary sources included the Ministry of Agriculture, Forestry and Fisheries, the Consumer Affairs Agency, the All Nippon Kashi Association, company annual reports, investor presentations, press releases of listed manufacturers, and reputable trade publications covering the Japanese food and confectionery industry.

Forecasting Models

Market forecasts use top-down and bottom-up models combining household expenditure patterns, channel-level growth rates, average per-unit price, and demographic adjustments. Scenario analysis addresses cocoa input cost variation, foreign-exchange movement, and shifts in tourist arrivals.

Japan Confectionery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Hard-Boiled Sweets, Mints, Gums and Jellies, Chocolate, Caramels and Toffees, Medicated Confectionery, Fine Bakery Wares, Others |

| Age Groups Covered | Children, Adult, Geriatric |

| Price Points Covered | Economy, Mid-Range, Luxury |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Pharmaceutical and Drug Stores, Online Stores, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., Morinaga & Co., Ltd., Nestlé, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan confectionery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan confectionery market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan confectionery industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Confectionery Market Report

The Japan confectionery market was valued at USD 30.10 Billion in 2025, supported by gifting culture, convenience store reach, and premium chocolate and biscuit demand.

The market is projected to grow at 4.65% CAGR from 2026 to 2034, reaching USD 45.31 Billion, driven by premiumization, e-commerce, and health-functional innovation.

Mid-range leads at 46.8% in 2025, anchored by branded chocolates, biscuits, and gummies sold widely through convenience stores and supermarkets across Japan.

Convenience stores lead at 34.6% in 2025, supported by their dense footprint, 24/7 access, and fast product rotation. Online stores at 14.7% are expanding fastest through brand-direct websites.

Kanto Region commands 37.8% in 2025, led by Tokyo's premium retail, corporate gifting, and inbound tourism, with Hokkaido Region emerging as the fastest-growing region at 4.8%.

Leading players include Meiji Holdings Co., Ltd., Lotte Co., Ltd., Ezaki Glico Co., Ltd., Morinaga & Co., Ltd., and Nestlé.

Premiumization is driven by gifting traditions, rising disposable income, tourist demand, department-store food halls, and growing interest in artisanal and single-origin chocolate.

Gifting culture sustains demand across Valentine's Day, White Day, Obon, year-end occasions, and corporate exchanges, anchoring premium boxed assortments year-round.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade