Japan Construction Equipment Market Size, Share, Trends and Forecast by Solution Type, Equipment Type, Type, Application, Industry, and Region, 2026-2034

Japan Construction Equipment Market Size, Share, Trends & Forecast (2026-2034)

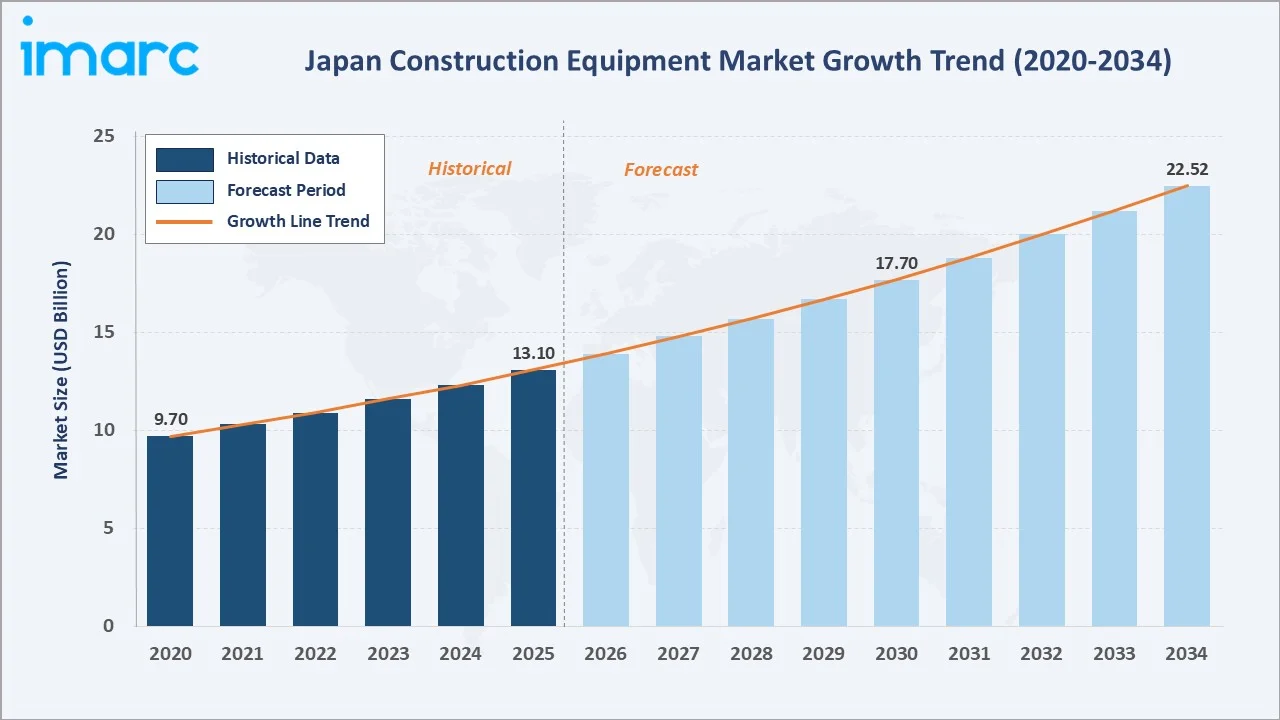

The Japan construction equipment market size reached USD 13.10 Billion in 2025 and is projected to reach USD 22.52 Billion by 2034, exhibiting a CAGR of 6.20% during the forecast period 2026-2034. Rising government investment in infrastructure - roads, bridges, railways, and urban renewal - alongside post-disaster reconstruction programs and the integration of smart ICT construction technologies are the primary catalysts driving Japan construction equipment market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.10 Billion |

|

Forecast Market Size (2034) |

USD 22.52 Billion |

|

CAGR (2026-2034) |

6.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

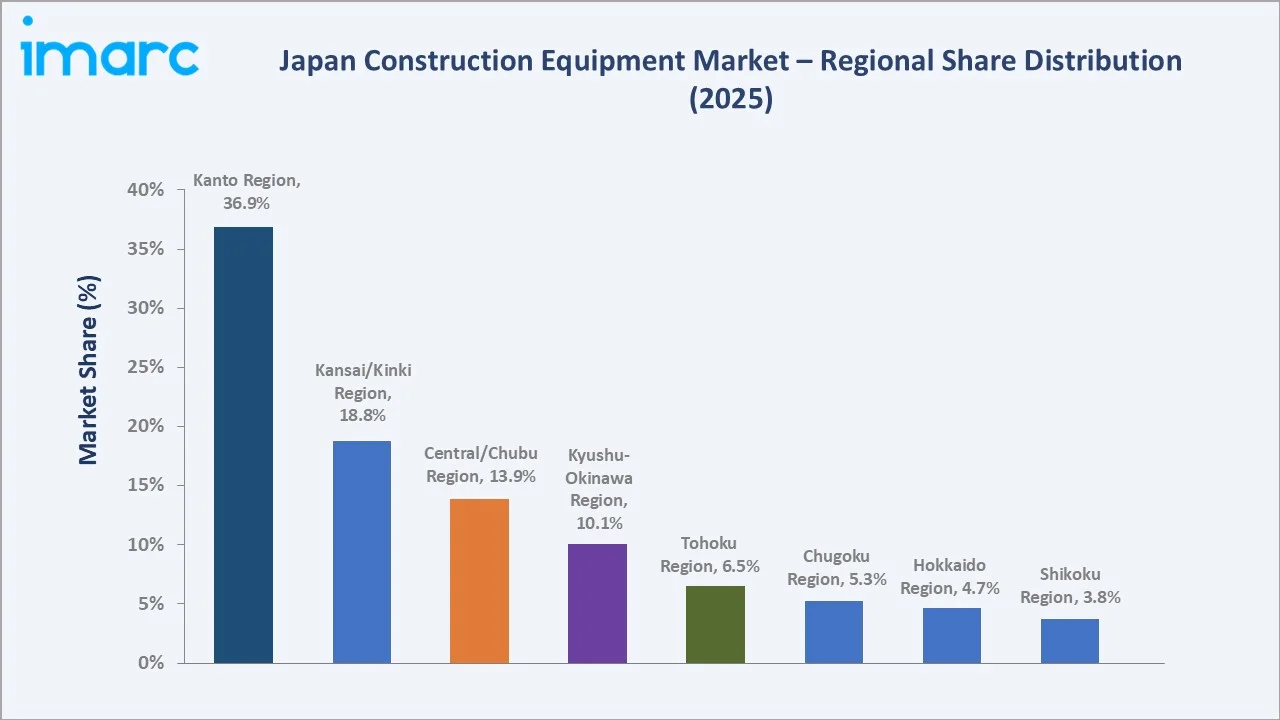

Kanto Region (36.9% share, 2025) |

|

Fastest Growing Region |

Kanto Region (largest absolute demand) |

|

Leading Equipment Type |

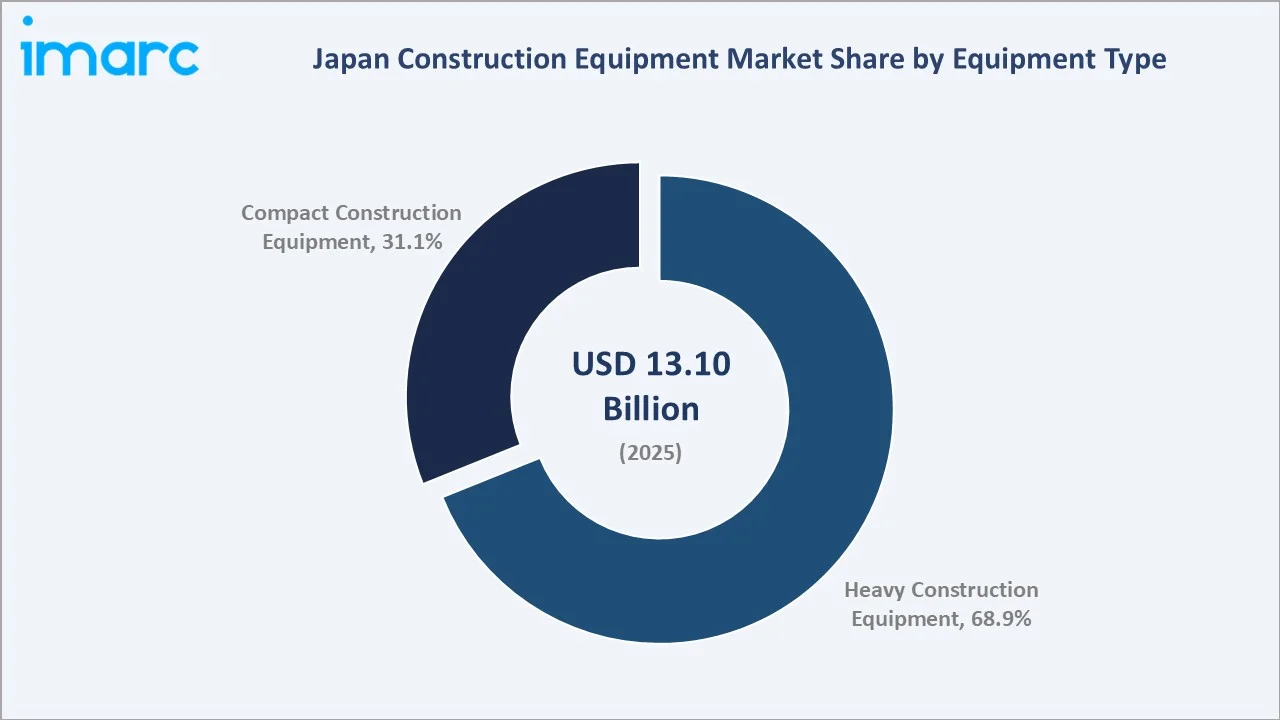

Heavy Construction Equipment (68.9%, 2025) |

|

Leading Solution Type |

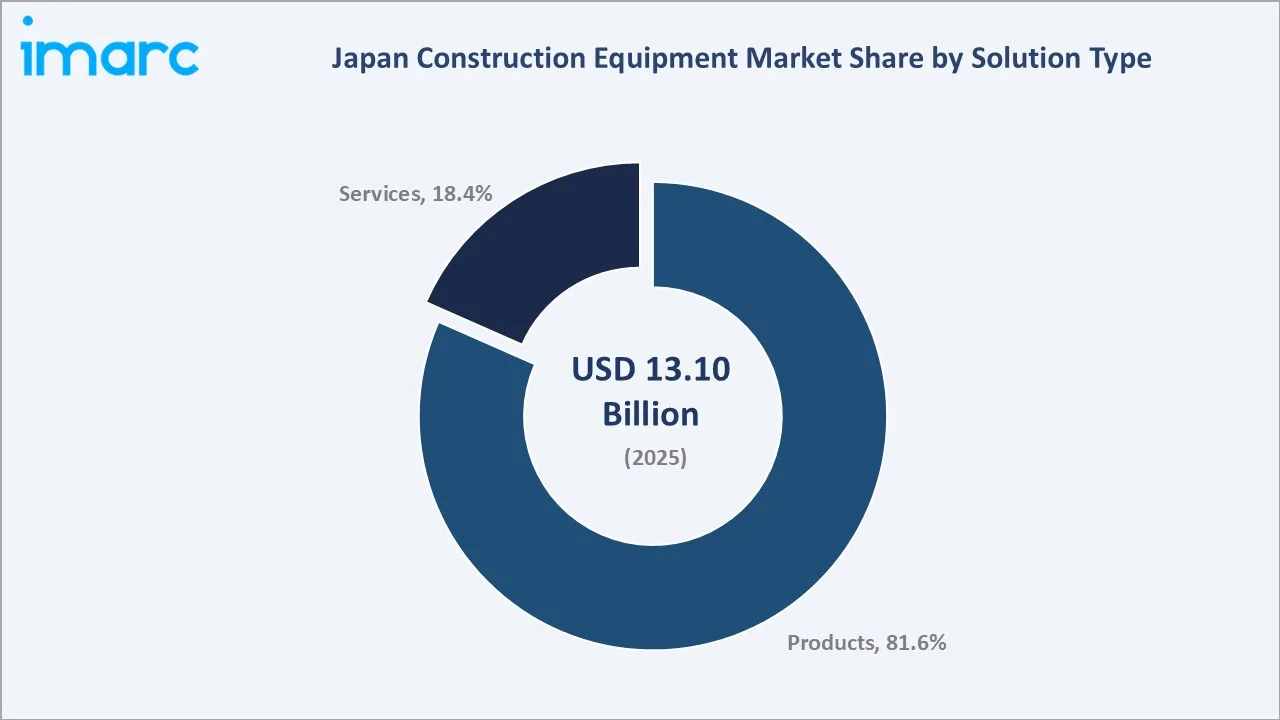

Products (81.6%, 2025) |

The chart below illustrates the Japan construction equipment market growth trajectory from 2020 through 2034, contrasting historical expansion against a robust forecast curve powered by infrastructure investment, urbanization, and technology-driven productivity gains.

To get more information on this market, Request Sample

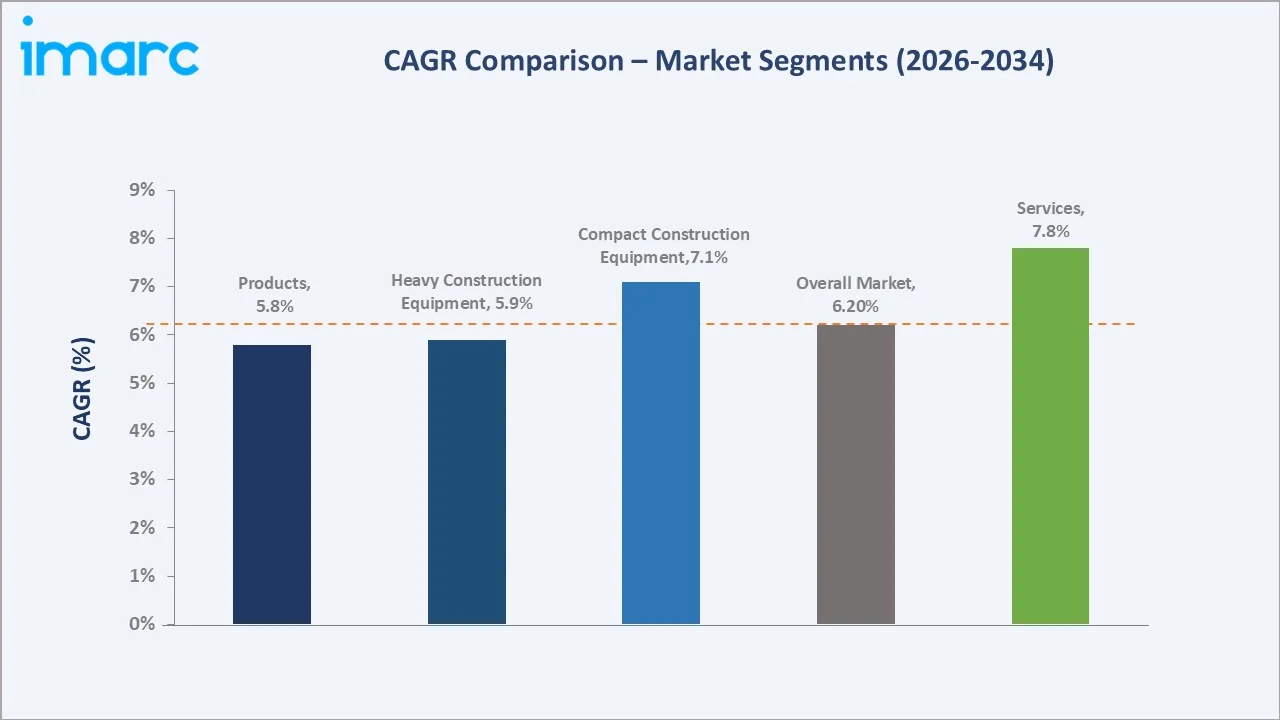

Segment-level CAGR comparisons below highlight the compact equipment and services sub-segments as the fastest-growing categories within the Japan construction equipment market forecast through 2034, driven by urban site constraints and rental fleet expansion.

Executive Summary

The Japan construction equipment market is undergoing sustained structural growth. Valued at USD 13.10 Billion in 2025, the market is forecast to reach USD 22.52 Billion by 2034 at a CAGR of 6.20%, up from USD 9.70 Billion in 2020. Government-led capital expenditure programs, including Japan's Fifth National Resilience Plan targeting disaster-resilient infrastructure, represent the primary institutional demand driver.

Heavy construction equipment commands 68.9% share in 2025, driven by excavator and crane procurement across mega-projects, road widening, and offshore wind installation works. Compact construction equipment represents 31.1%, growing faster at an estimated CAGR of 7.1% through 2034, supported by urban site constraints and increased adoption by small contractors. Products dominate at 81.6%, while services - including telematics-enabled maintenance and fleet management - are expanding at approximately 7.8% CAGR.

The Kanto region maintains its 36.9% leadership as the largest market, anchored by Tokyo's commercial real estate pipeline and transport infrastructure. The Kyushu-Okinawa region is a notable emerging driver, spurred by TSMC's semiconductor fab construction in Kumamoto. The Japan construction equipment market outlook remains positive, supported by automation adoption, hydrogen-powered equipment trials, and sustained government infrastructure allocations through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Equipment Type |

Heavy Construction Equipment – 68.9% share (2025) |

|

Second Equipment Type |

Compact Construction Equipment – 31.1% share (2025) |

|

Largest Solution Type |

Products – 81.6% share (2025) |

|

Services Share |

Services – 18.4% share (2025) |

|

Leading Region |

Kanto Region – 36.9% revenue share (2025) |

|

Second Region |

Kansai/Kinki Region – 18.8% revenue share (2025) |

|

Top Companies |

Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., Tadano Ltd., Takeuchi Global, Caterpillar, KUBOTA Corporation |

|

Market Opportunity |

Electric, autonomous & ICT equipment adoption |

Key Analytical Observations Supporting the Above Data:

- Heavy equipment's 68.9% dominance in 2025 reflects large-scale civil infrastructure procurement, including the Chuo Shinkansen maglev construction, coastal sea-wall reinforcement programs, and Tokyo waterfront redevelopment projects.

- Compact equipment at 31.1% is growing faster than the overall market at ~7.1% CAGR, driven by narrow urban construction sites, residential renovation demand, and contractor preference for versatile mini excavators and compact loaders.

- Products segment at 81.6% dominates as OEMs Komatsu and Hitachi continue rolling out ICT-enabled equipment with integrated GPS, telematics, and automated grade-control systems commanding premium unit prices.

- Services at 18.4% represent a high-growth area, with fleet management, predictive maintenance, and telematics-as-a-service gaining traction among Tier-1 contractors seeking lifecycle cost reduction.

- Kanto Region's 36.9% share is underpinned by JPY multi-trillion Tokyo 2040 infrastructure plans, ongoing Olympics legacy works, and commercial redevelopment in Shinjuku, Shibuya, and Toranomon districts.

- Kyushu-Okinawa at 10.1% is experiencing above-average growth momentum, with TSMC's JPY 2-trillion Kumamoto fab investment stimulating road, utilities, and industrial park construction across the region.

Japan Construction Equipment Market Overview

Construction equipment encompasses a broad range of heavy machinery, vehicles, and tools used for earthmoving, material handling, lifting, paving, and demolition. The Japan market includes excavators, hydraulic cranes, loaders, forklifts, bulldozers, and compact equipment, supported by an advanced domestic manufacturing ecosystem led by global OEMs Komatsu and Hitachi Construction Machinery.

Japan's construction equipment industry operates at the convergence of government infrastructure mandates, technological innovation, and demographic-driven urbanization. The country's aging infrastructure stock - over 50% of bridges and tunnels require repair or replacement by 2030 per Ministry of Land, Infrastructure, Transport and Tourism (MLIT) data - creates a structural, long-cycle replacement demand cycle that underpins the Japan construction equipment industry analysis.

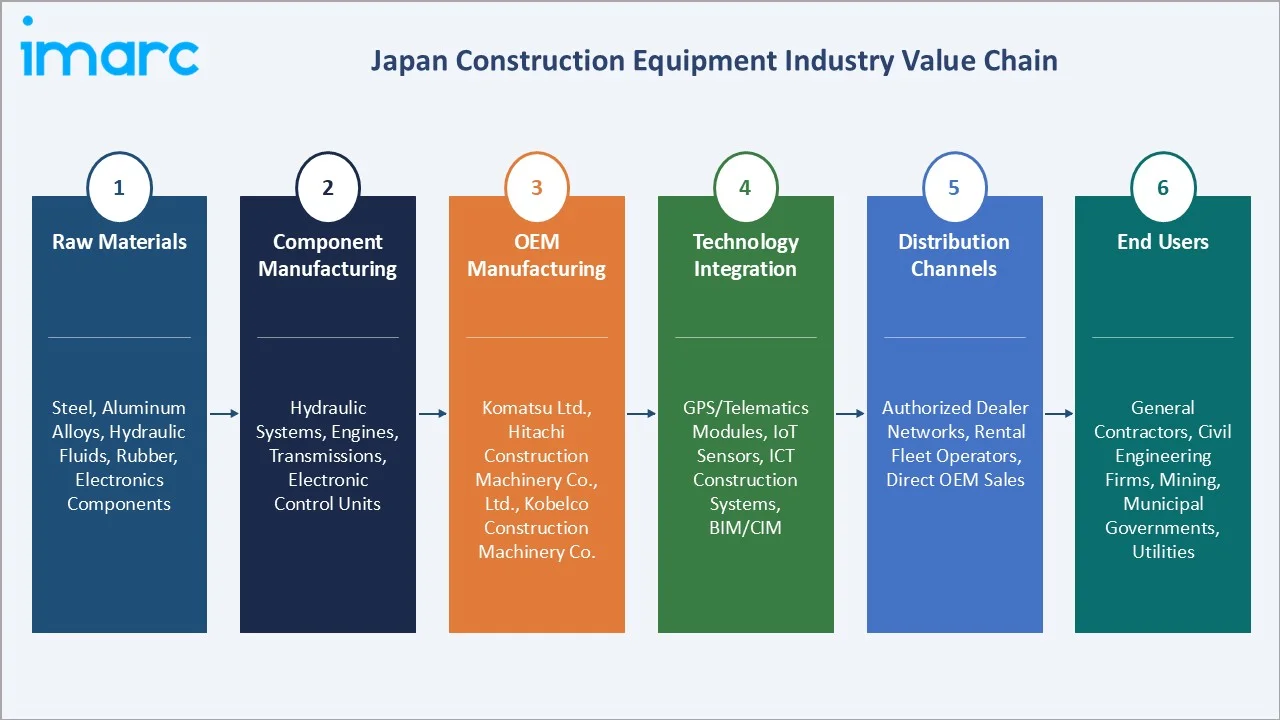

The diagram below illustrates the Japan construction equipment industry ecosystem from raw material supply through end-user deployment.

Market Dynamics

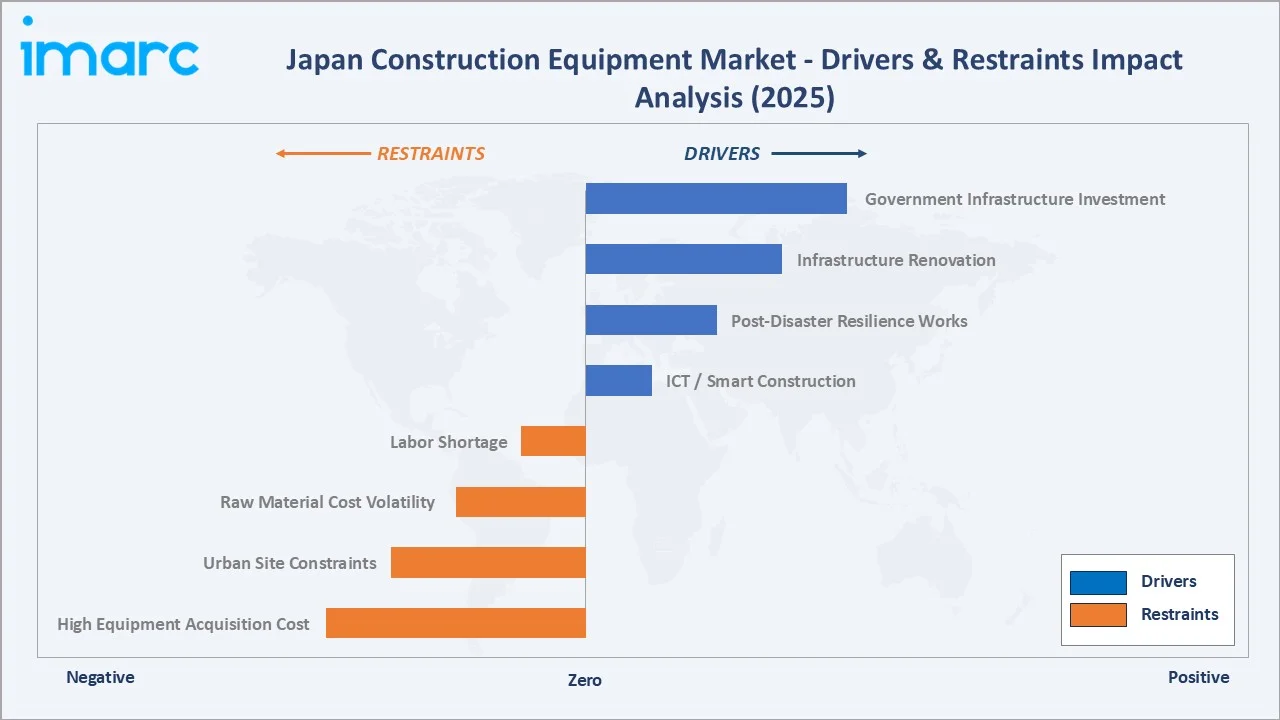

The chart below maps the primary growth drivers and key restraints shaping the Japan construction equipment market in 2025.

To evaluate market opportunities, Request Sample

Market Drivers

- Government Infrastructure Investment: Japan’s government has committed substantial funding under the Economic Security Promotion Act and the Fifth National Resilience Plan. Ongoing highway expansion, new Shinkansen extensions, port modernization, and urban expressway developments are sustaining long-term equipment procurement pipelines across Tier-1 contractors.

- Post-Disaster Reconstruction and Resilience Works: Japan’s seismic vulnerability drives continuous demand for coastal sea-wall construction, river reinforcement, and urban retrofitting. The government’s national disaster mitigation program sustains elevated demand for excavators, cranes, and earthmoving equipment across Pacific-coast prefectures.

- ICT and Smart Construction Adoption: The MLIT i-Construction initiative mandates BIM/CIM adoption and promotes automated, ICT-equipped machinery on public projects. A majority of new public works projects now require ICT-compatible equipment, driving equipment upgrades and accelerating fleet replacement cycles.

- Aging Infrastructure Replacement: MLIT estimates a significant share of Japan’s road bridges, tunnels, and sewer infrastructure will exceed 50 years of age by 2030. This creates a structurally large, government-funded repair and replacement pipeline, sustaining demand for specialized lifting and maintenance equipment through 2034.

Market Restraints

- Acute Labor Shortage: Japan’s construction sector faces a significant shortage of skilled workers by 2030, according to the Japan Federation of Construction Contractors. While automation partially offsets this gap, the labor deficit continues to constrain overall project execution and throughput.

- High Equipment Acquisition Costs: ICT-equipped and hybrid construction equipment commands a substantial price premium over conventional models. Smaller regional contractors face capital constraints in fleet renewal, which slows technology adoption outside major metropolitan markets.

- Raw Material Cost Volatility: Steel and copper price fluctuations directly influence OEM production costs and aftermarket parts pricing, compressing margins and creating procurement cost uncertainty for fleet owners.

Market Opportunities

- Electric and Hydrogen-Powered Equipment: Japan's Green Growth Strategy targets carbon neutrality by 2050. Komatsu and Hitachi have committed to commercial electric mini-excavator launches by 2026 and hydrogen fuel cell prototype testing. Carbon-neutral construction mandates create first-mover procurement advantages for OEMs with certified zero-emission equipment.

- Rental Market and Fleet-as-a-Service: Japan's equipment rental market is expanding at above-market rates. OEMs offering integrated rental-plus-maintenance packages can capture incremental recurring revenue.

- Digital Twin and Remote Monitoring: Advanced telematics platforms enabling real-time equipment health monitoring, predictive maintenance scheduling, and automated billing are creating high-margin aftermarket revenue streams for Komatsu (KomConnect) and Hitachi (ConSite).

Market Challenges

- Site Constraint in Urban Markets: Tokyo, Osaka, and other dense urban areas impose strict dimensional and noise restrictions on construction equipment, limiting deployable equipment types and requiring costly traffic management protocols.

- Regulatory Compliance Complexity: Japan's construction safety regulations, emission standards aligned with MLIT guidelines, and municipal-level noise ordinances require manufacturers to maintain complex, differentiated product certification portfolios.

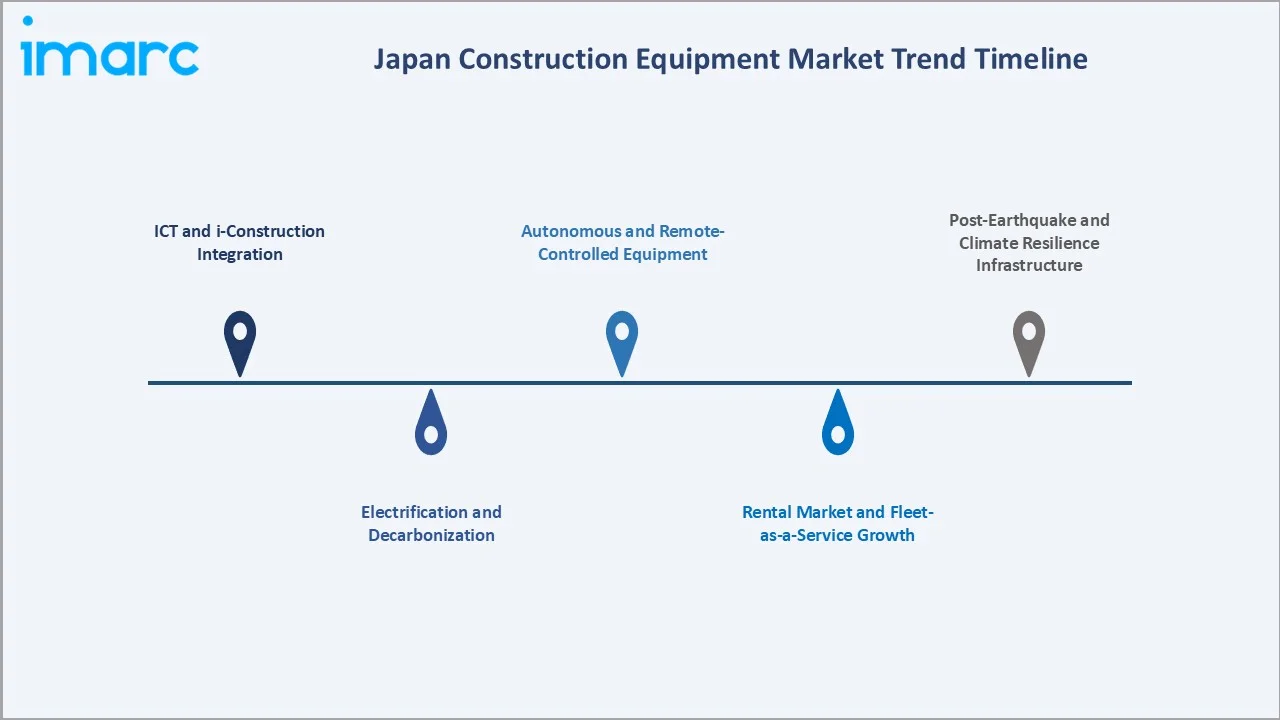

Emerging Market Trends

The Japan construction equipment market is being reshaped by five structural trends that will define competitive positioning and procurement patterns through 2034. The timeline below illustrates key milestones across the forecast horizon.

1. ICT and i-Construction Integration

MLIT's i-Construction initiative has fundamentally transformed procurement specifications for public works projects. Public contracts require ICT-compatible equipment, including GPS-guided excavators, automated compaction rollers, and drone survey integration. Komatsu's Intelligent Machine Control (IMC) platform and Hitachi's Solution Linkage system are the market-defining platforms, each supporting fully automated blade and bucket control without skilled operator input.

2. Electrification and Decarbonization

Japan's 2050 carbon neutrality commitment is accelerating OEM investment in battery-electric and hydrogen fuel cell construction equipment. Komatsu launched its PC30E-6 electric mini-excavator in 2023. Tokyo Metropolitan Government's 2025 construction emission zone requirements for major procurement projects are creating pull-through demand for certified zero-emission equipment.

3. Rental Market and Fleet-as-a-Service Growth

Japan's construction equipment rental penetration is rising steadily, with leading operators expanding managed service models that bundle equipment, telematics, operator training, and predictive maintenance into recurring monthly fee structures.

4. Autonomous and Remote-Controlled Equipment

Japan’s severe construction labor shortage is accelerating the deployment of autonomous and tele-operated construction equipment. Leading OEMs and contractors are piloting remote and autonomous systems for earthmoving and infrastructure projects, with early commercial applications already emerging.

5. Post-Earthquake and Climate Resilience Infrastructure

The January 2024 Noto Peninsula earthquake reinforced Japan's commitment to accelerated infrastructure resilience investment. The revised national resilience plan for the 2026–2030 period maintains dedicated disaster mitigation funding, ensuring sustained equipment demand for sea-wall, bridge, and underground utility construction through 2034.

Industry Value Chain Analysis

The Japan construction equipment industry value chain spans six integrated stages from raw material supply through end-user deployment. Each stage involves distinct competitive dynamics and margin structures relevant to the overall Japan construction equipment industry analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Steel, aluminum alloys, hydraulic fluids, rubber, electronics |

|

Component Manufacturing |

Hydraulic systems, engines, transmissions, control units |

|

OEM Manufacturing |

Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., – full assembly & certification |

|

Technology Integration |

GPS/telematics modules, IoT sensors, ICT construction systems |

|

Distribution Channels |

Authorized dealer networks, rental fleet operators, direct OEM sales |

|

End Users |

General contractors, civil engineering firms, mining operators, municipal governments, utilities |

OEMs hold the highest strategic value by integrating components, advanced control systems, and telematics platforms into certified, market-ready equipment. Japan's domestic OEM ecosystem. Rental operators and dealer networks are gaining influence as fleet-as-a-service models expand, enabling OEMs to maintain equipment utilization data and extend customer lifecycle relationships beyond initial sale.

Technology Landscape in the Japan Construction Equipment Industry

ICT Construction and Automated Machine Control

Japan leads globally in ICT construction adoption, driven by MLIT's i-Construction policy framework. Automated machine control systems - including GPS-guided blade control, automated compaction feedback, and real-time 3D design integration - are now standard on new excavators and dozers procured for public works. Komatsu's IMC2 enables fully automated excavation without skilled operator input, addressing the labor shortage while improving construction precision.

Telematics and Predictive Maintenance

Advanced telematics platforms are transforming aftermarket revenue models. Komatsu's KOMTRAX system provides real-time operational data, fuel consumption analytics, and predictive maintenance alerts. These platforms generate recurring SaaS revenue that complements equipment sales and strengthens customer retention.

Electrification and Alternative Fuels

Battery-electric and hydrogen fuel cell equipment development is accelerating. Komatsu's PC30E-6 battery excavator and Kubota's electric compact equipment lineup represent the first commercial wave. OEMs are targeting 2026-2028 for commercial launches of battery-electric mid-size excavators. Hydrogen fuel cell feasibility studies are underway for large equipment where battery energy density remains insufficient.

Autonomous and Remote Operation Technologies

Japan's construction sector is a global testbed for autonomous equipment. Komatsu's Smart Construction solution integrates drone surveying, 3D design modeling, and autonomous dozer operation into a unified jobsite management platform.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Solution Type | Products | 81.6% | 2025 |

| Equipment Type | Heavy Construction Equipment | 68.9% | 2025 |

| Type | 🔒 | 🔒 | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Industry | 🔒 | 🔒 | 2025 |

| Region | Kanto Region | 36.9% | 2025 |

By Equipment Type

To access detailed market analysis, Request Sample

Heavy Construction Equipment leads the Japan construction equipment market with a 68.9% share in 2025, equivalent to approximately USD 9.03 Billion. Demand is driven by large-scale civil infrastructure projects including expressway construction, port expansion, dam rehabilitation, and high-speed rail corridor works.

By Solution Type

Products dominate the market at 81.6% of total revenue in 2025, approximately USD 10.69 Billion. This segment encompasses new equipment sales and spare parts. ICT-integrated product launches are expanding average selling prices, with fully automated ICT excavators.

Regional Market Insights

The Japan construction equipment market is analyzed across eight primary regional markets, each presenting distinct demand profiles shaped by infrastructure programs, industrial activity, and disaster reconstruction requirements.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

36.9% |

Tokyo metro development, Olympic legacy infrastructure, commercial real estate, logistics hubs |

|

Kansai/Kinki Region |

18.8% |

Osaka Expo 2025 legacy works, Umeda redevelopment, industrial zone expansion |

|

Central/Chubu Region |

13.9% |

Nagoya industrial clusters, Chuo Shinkansen construction, auto sector infrastructure |

|

Kyushu-Okinawa Region |

10.1% |

TSMC Kumamoto fab construction, energy infrastructure, tourism facilities |

|

Tohoku Region |

6.5% |

Post-disaster reconstruction, coastal sea-wall projects, renewable energy installations |

|

Chugoku Region |

5.3% |

Port upgrades, industrial plant maintenance, road network improvement programs |

|

Hokkaido Region |

4.7% |

Shinkansen extension to Sapporo, tourism resort development, agricultural infrastructure |

|

Shikoku Region |

3.8% |

Bridge and tunnel maintenance, regional highway upgrades, disaster prevention works |

The chart below illustrates the regional distribution of Japan construction equipment market revenue in 2025.

Competitive Landscape

The Japan construction equipment market is moderately concentrated at the top tier, with Komatsu and Hitachi Construction Machinery holding dominant positions. Competition intensifies in compact equipment and services segments.

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Komatsu Ltd. |

Komatsu |

Leader |

Largest Japan OEM; ICT/Smart Construction leadership; global scale |

|

Hitachi Construction Machinery Co., Ltd. |

Hitachi |

Leader |

Hydraulic excavator dominance; ConSite IoT platform |

|

Kobelco Construction Machinery Co., Ltd. |

Kobelco |

Leader |

Excavator fuel efficiency; strong domestic dealer network |

|

Tadano Ltd. |

Tadano |

Challenger |

Mobile crane leadership; Faun acquisition; lifecycle services |

|

Takeuchi Global |

Takeuchi |

Challenger |

Compact equipment specialist; mini excavators; global reach |

|

Caterpillar |

CAT |

Challenger |

Global technology platform; strong rental fleet; Cat Financial |

|

KUBOTA Corporation |

Kubota |

Challenger |

Mini excavators; compact tractors; decarbonization focus |

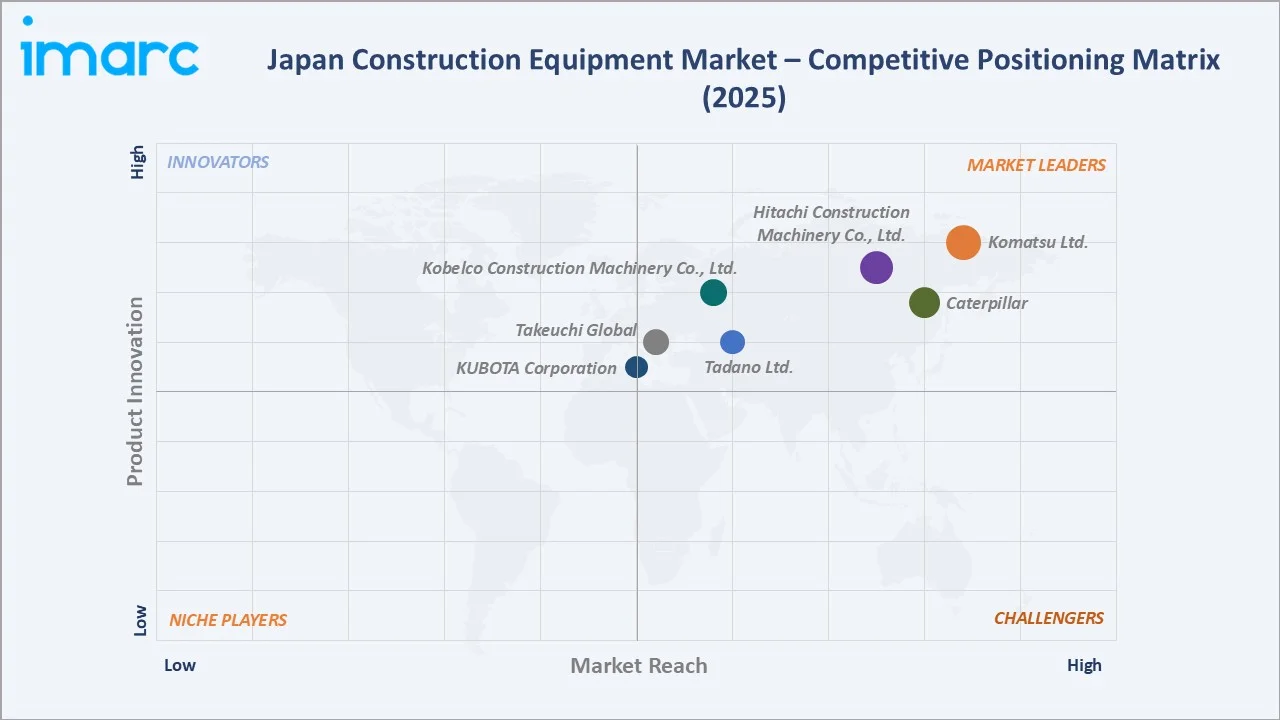

The competitive positioning matrix below maps key Japan construction equipment players on product innovation capability versus market presence dimensions in 2025.

Key Company Profiles

Komatsu Ltd.

Komatsu Ltd. is Japan's largest construction equipment manufacturer, headquartered in Tokyo, Japan. Founded in 1921, with a strong global footprint across Asia, North America, Europe, and emerging markets, Komatsu generates a significant portion of its revenue from overseas operations.

- Product & Platform Portfolio: Komatsu's Japan product range includes hydraulic excavators (PC series), ICT bulldozers (D series IMC), wheel loaders, mining dump trucks, and compact equipment. The Smart Construction platform integrates drones, ICT machinery, and cloud-based data management into a unified digital construction workflow.

- Recent Developments: In 2023, Komatsu Ltd. announced the launch of a new 3-ton class electric mini excavator in 2023 for the Japanese market, equipped with a lithium-ion battery. The model is a fully redesigned version of its earlier electric mini excavator, featuring zero exhaust emissions, lower noise, and improved efficiency through a more compact and lightweight battery system, supporting Komatsu’s broader electrification and carbon neutrality goals.

- Strategic Focus: Komatsu's strategy centers on digitalization through Smart Construction, decarbonization via electric and hydrogen product development, and expansion of service-based revenue through telematics and predictive maintenance platforms.

Kobelco Construction Machinery Co., Ltd.

Kobelco Construction Machinery is a specializing in hydraulic excavators. Kobelco holds a strong domestic market position in the mid-size excavator segment and is recognized for fuel efficiency leadership and operator comfort design.

- Product & Platform Portfolio: Kobelco's range is centered on SK-series hydraulic excavators spanning the 1.5-500 ton range, with particular strength in the 13-35 ton urban and civil construction segments.

- Recent Developments: In 2023, Kobelco’s announcement highlights the launch of new short-radius excavators under its “Performance x Design” concept, focusing on combining compact design, high productivity, and strong lifting performance. The new SK230SRLC-7 and SK270SR(N)LC-7 models are designed for urban and confined job sites such as roadworks and utility construction.

- Strategic Focus: Kobelco's strategy focuses on fuel efficiency leadership in mid-size excavators, urban site optimization features for Japan's constrained construction environments, and selective international market expansion in Southeast Asia and Europe.

Tadano Ltd.

Tadano Ltd. is a Japan-based global manufacturer specializing in lifting equipment, particularly cranes and aerial work platforms. Founded in 1948 and headquartered in Takamatsu, Japan, the company is recognized as one of the world’s leading crane manufacturers.

- Product & Platform Portfolio: Tadano's portfolio includes all-terrain cranes (ATF/GR series), rough terrain cranes, truck cranes, and aerial work platforms. The HELLO-NET telematics system provides crane management and remote diagnostic services.

- Recent Developments: In 2025, Tadano announced that it will showcase its expanded portfolio of lifting equipment at CONEXPO-CON/AGG. The company is highlighting its transformation into a broader lifting and access solutions provider, including cranes, aerial work platforms, and electric pick-and-carry systems.

- Strategic Focus: Tadano's strategy focuses on global crane market leadership through the Faun integration, lifecycle service expansion, and electrification roadmap development for aerial work platforms.

Market Concentration Analysis

The Japan construction equipment market exhibits moderate concentration, with significant differentiation by equipment category. The overall top-5 players - Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., Tadano Ltd., Takeuchi Global - account for approximately 70-75% of total market revenue.

The market is experiencing bifurcated competitive dynamics. In the large equipment and ICT construction segment, consolidation is occurring around platform capabilities - Smart Construction (Komatsu), ConSite (Hitachi). OEMs without proprietary digital platforms face risk of displacement in government procurement, where ICT capability is increasingly a selection criterion.

Investment & Growth Opportunities

Fastest-Growing Segments

Services - encompassing telematics, fleet management, predictive maintenance, and operator training - represent the highest CAGR segment at approximately 7.8% through 2034. Compact construction equipment is the fastest-growing equipment type at approximately 7.1% CAGR, driven by urban site constraints, residential renovation demand, and agricultural machinery convergence. The ICT construction enablement technology market is growing at double-digit rates.

Emerging Market Expansion

Within Japan, Kyushu represents the most compelling near-term growth region, with TSMC semiconductor fab construction sustaining elevated demand through 2026-2027. Hokkaido offers medium-term growth opportunity via Shinkansen extension infrastructure, resort development, and renewable energy installations. Internationally, Japan's OEMs are expanding in Southeast Asia and India, where construction activity mirrors Japan's early growth phase.

Venture and Strategic Investment Trends

Corporate R&D investment in Japan's construction technology sector is focused on autonomous operation AI, battery and hydrogen fuel cell systems, digital twin platforms, and advanced telematics analytics.

Future Market Outlook (2026-2034)

The Japan construction equipment market forecast projects expansion from USD 13.10 Billion in 2025 to USD 22.52 Billion by 2034 at a CAGR of 6.20%. Infrastructure spending provides a structural demand floor that insulates the market from cyclical economic downturns.

Three structural shifts will reshape the market through 2034. First, ICT and autonomous construction will transition from competitive differentiator to baseline requirement in public works procurement by 2028-2030. Second, electrification will gain commercial scale in compact and mid-size equipment by 2027-2028, with battery-electric models achieving total cost of ownership parity with diesel equivalents.

Third, the services segment will structurally gain share from products, with predictive maintenance and fleet management contracts becoming standard engagement models for Tier-1 contractors.

Demographic constraints - Japan's declining and aging construction workforce - will sustain demand for automation and ICT-enabled productivity enhancement, structurally differentiating Japan's market growth from pure volume-driven emerging market expansion.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with Japan construction equipment industry stakeholders, including product directors at OEM manufacturers, procurement managers at Tier-1 general contractors, fleet managers at rental equipment operators (Nishio Rent All, Kanamoto), and institutional investors in Japanese infrastructure and industrials sectors.

Secondary Research

Secondary sources include MLIT construction investment data, Japan Construction Equipment Manufacturers Association (CEMA) shipment statistics, Japan Federation of Construction Contractors industry reports, Cabinet Office economic data, company annual reports, and trade publications including Kensetsu Kikaika (Construction Mechanization).

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth trajectories, government infrastructure expenditure plans, construction output data, equipment fleet age distribution, and historical market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty.

Japan Construction Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solution Types Covered | Products, Services |

| Equipment Types Covered | Heavy Construction Equipment, Compact Construction Equipment |

| Types Covered | Loader, Cranes, Forklift, Excavator, Dozers, Others |

| Applications Covered | Excavation and Mining, Lifting and Material Handling, Earth Moving, Transportation, Others |

| Industries Covered | Oil and Gas, Construction and Infrastructure, Manufacturing, Mining, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., Tadano Ltd., Takeuchi Global, Caterpillar, KUBOTA Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan construction equipment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan construction equipment market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan construction equipment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Construction Equipment Market Report

The Japan construction equipment market was valued at USD 13.10 Billion in 2025, driven by government infrastructure investment, ICT construction adoption, and post-disaster reconstruction programs across Japan.

The market is projected to reach USD 22.52 Billion by 2034, growing at a CAGR of 6.20% during 2026-2034, supported by sustained infrastructure spending, electrification, and autonomous equipment adoption.

Heavy construction equipment leads with a 68.9% share in 2025, driven by large civil infrastructure projects including expressways, Shinkansen extensions, sea-wall construction, and port development.

Services is the fastest-growing solution type, expanding at approximately 7.8% CAGR through 2034, driven by telematics fleet management, predictive maintenance, and rental fleet expansion.

The Kanto region dominates with 36.9% share in 2025, underpinned by Tokyo metropolitan infrastructure renewal, commercial real estate development, and concentration of Tier-1 contractors.

Key drivers include government infrastructure investment, ICT i-Construction mandates, post-earthquake resilience programs, aging infrastructure replacement, Shinkansen extensions, and semiconductor fab construction in Kyushu.

Major players include Komatsu Ltd., Hitachi Construction Machinery Co., Ltd., Kobelco Construction Machinery Co., Ltd., Tadano Ltd., Takeuchi Global, Caterpillar, and KUBOTA Corporation.

ICT automated machine control and autonomous operation systems are fastest-growing, advancing at double-digit rates driven by MLIT i-Construction mandates and Japan's construction labor shortage crisis.

Japan's construction labor deficit is accelerating adoption of automated, ICT-enabled, and autonomous equipment, structurally driving premium equipment demand.

Key opportunities include electric and hydrogen equipment development, ICT construction platform services, compact equipment expansion, rental fleet-as-a-service models, and Kyushu regional infrastructure driven by TSMC investment.

The Japan construction equipment market was valued at approximately USD 9.70 Billion in 2020, representing the market base prior to the accelerated post-COVID infrastructure investment and ICT construction adoption cycle.

The Japan construction equipment market is expected to reach approximately USD 17.70 Billion in 2030, representing sustained 6.20% CAGR growth driven by national infrastructure programs and technology adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade