Japan Consumer Finance Market Size, Share, Trends and Forecast by Product Type, Application, Loan Purpose, Credit Score, Term Length, and Region, 2026-2034

Japan Consumer Finance Market Summary:

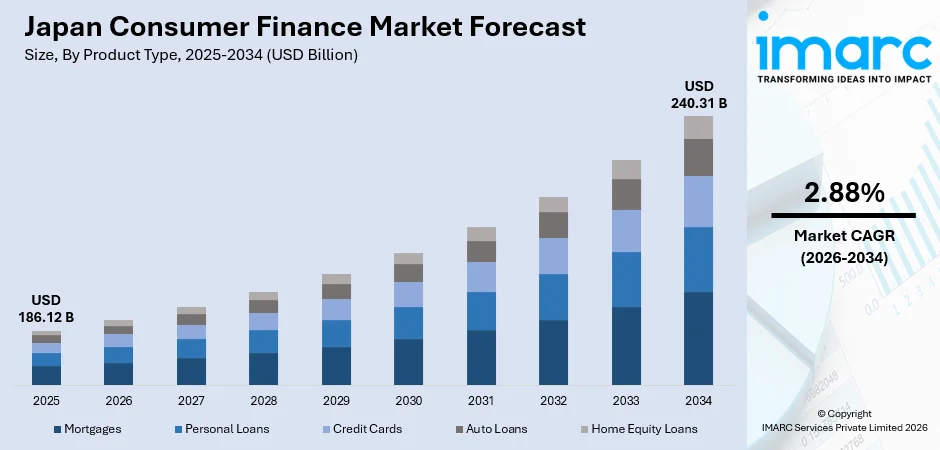

The Japan consumer finance market size was valued at USD 186.12 Billion in 2025 and is projected to reach USD 240.31 Billion by 2034, growing at a compound annual growth rate of 2.88% from 2026-2034.

The Japan consumer finance market is witnessing sustained expansion as evolving consumer spending patterns, rising demand for diversified lending products, and growing financial literacy reshape borrowing behaviors nationwide. Increasing urbanization, shifting demographic profiles, and preference for flexible repayment structures are driving adoption across multiple consumer segments. The expanding digital financial ecosystem, supportive regulatory frameworks, and integration of advanced credit assessment methodologies are further strengthening market fundamentals, positioning Japan as a mature and innovation-driven consumer finance landscape with significant long-term growth potential across the Japan consumer finance market share.

Key Takeaways and Insights:

- By Product Type: Mortgages dominate the market with a share of 42.6% in 2025, driven by the sustained demand for residential and commercial property financing supported by historically favorable lending conditions and long-term asset accumulation preferences.

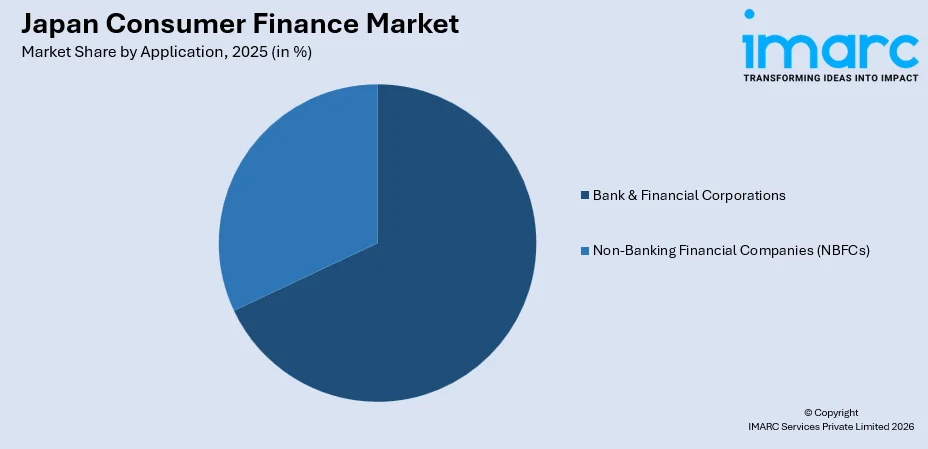

- By Application: Bank & financial corporations lead the market with a share of 68.4% in 2025, owing to their wide branch networks, strong consumer trust, substantial capital, and diverse lending product offerings.

- By Loan Purpose: Debt consolidation holds the largest share of 31.8% in 2025, reflecting increasing popularity of consumers to consolidate various debts into one manageable facility with lower interest rates.

- By Credit Score: Good dominates the market with a share of 39.5% in 2025, as the majority of Japanese borrowers maintain strong creditworthiness through disciplined financial behavior and comprehensive credit reporting systems.

- By Term Length: Long-term loans represent the largest segment with a share of 46.7% in 2025, as consumers increasingly favor extended repayment horizons to manage larger financial commitments while maintaining affordable monthly obligations.

- By Region: Kanto Region dominates with a share of 37.9% in 2025, supported by the concentration of economic activity, higher disposable incomes, and the dense population base centered around the Greater Tokyo metropolitan area.

- Key Players: The Japan consumer finance market exhibits a moderately consolidated competitive landscape, with established banking institutions and specialized lending companies competing across product categories through digital innovation, diversified service portfolios, and strategic partnerships.

To get more information on this market Request Sample

The Japan consumer finance market is evolving in response to shifting macroeconomic conditions and changing consumer financial behaviors. As the country transitions toward a normalized interest rate environment after decades of ultra-low borrowing costs, lenders are recalibrating their product offerings to address evolving demand patterns. According to reports, in Q3 2025, Japan’s consumer credit outstanding increased to 57202.60 JPY Billion from 56452.60 JPY Billion in Q2 2025, reflecting continued growth in household credit uptake amid improving economic activity. The growing integration of digital technologies into lending processes is transforming how consumers access and manage credit, with online platforms and mobile applications enabling faster approvals and greater convenience. Meanwhile, demographic shifts, including an aging population and changing household structures, are creating new demand for tailored financial products such as reverse mortgages and senior-focused lending solutions.

Japan Consumer Finance Market Trends:

Accelerated Digital Transformation in Consumer Lending

The consumer finance sector in Japan is undergoing rapid digital transformation as lenders increasingly adopt online application platforms, mobile-first interfaces, and automated credit evaluation systems. According to sources, in 2025, Japanese fintech firm Finatext reported that its SaaS‑based personal lending service, powered by its “Crest” system, surpassed 50,000 cumulative credit applicants, underscoring strong uptake of digital lending channels and consumer engagement. This shift is enabling faster loan processing, improved accessibility for underserved populations, and enhanced customer experiences across the lending value chain.

Expansion of Embedded Finance and Platform-Based Lending

Embedded finance is gaining significant traction across Japan as non-financial platforms integrate lending solutions directly into e-commerce, retail, and service ecosystems. In March 2025, Japan’s fintech firm Smartpay, in partnership with Chubb Insurance Japan, announced the launch of the country’s first embedded insurance products within its BNPL (Buy‑Now‑Pay‑Later) offerings, enabling consumers to access insurance at the point of sale alongside credit services. This trend allows consumers to access credit seamlessly at the point of purchase, promoting financial inclusion and diversifying borrowing channels beyond traditional banking institutions.

.webp)

Growing Demand for Flexible and Personalized Credit Products

Japanese consumers are increasingly seeking customized lending solutions that align with their unique financial circumstances and life stages. According to reports, in 2025, an Ad‑Advisor Navi survey showed that borrowers choosing card loans prioritized ease of repayment and loan flexibility, with a majority selecting products based on how well terms matched their needs, highlighting demand for tailored offerings. Furthermore, lenders are responding with flexible repayment structures, tiered interest rate models, and purpose-specific loan products designed to accommodate diverse borrower profiles.

Market Outlook 2026-2034:

The Japan consumer finance market is poised for steady expansion over the forecast period, supported by the ongoing modernization of lending infrastructure, strengthening wage growth, and the progressive normalization of monetary policy. Increasing consumer confidence, coupled with the growing adoption of technology-driven credit assessment tools, is expected to broaden the addressable borrower base. The continued evolution of regulatory frameworks promoting responsible lending and financial transparency will further reinforce market stability, while emerging product categories and digital distribution channels will unlock new growth avenues across diverse consumer segments. The market generated a revenue of USD 186.12 Billion in 2025 and is projected to reach a revenue of USD 240.31 Billion by 2034, growing at a compound annual growth rate of 2.88% from 2026-2034.

Japan Consumer Finance Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Mortgages |

42.6% |

|

Application |

Bank & Financial Corporations |

68.4% |

|

Loan Purpose |

Debt Consolidation |

31.8% |

|

Credit Score |

Good |

39.5% |

|

Term Length |

Long-Term |

46.7% |

|

Region |

Kanto Region |

37.9% |

Product Type Insights:

- Personal Loans

- Credit Cards

- Mortgages

- Auto Loans

- Home Equity Loans

Mortgages dominate with a market share of 42.6% of the total Japan consumer finance market in 2025.

Mortgages represent the cornerstone of Japan's consumer finance market, driven by the deeply rooted cultural emphasis on homeownership and long-term asset building. The availability of extended repayment periods, including loans spanning up to fifty years, has expanded accessibility for younger borrowers navigating rising urban property prices. According to sources, in 2025, Japan’s Housing Finance Agency reported Flat 35 mortgage applications rose 50.7% year-on-year to 14,223 units, with completed loans up 27.7% and total loan value at 277.6 billion yen.

The evolving interest rate environment has prompted a dynamic shift between fixed-rate and variable-rate mortgage products, as borrowers reassess their financing strategies in response to monetary policy changes. Increasing digitization of the mortgage application process, along with enhanced credit evaluation methodologies, continues to streamline access and improve the overall borrower experience. The introduction of innovative lending structures, including reverse mortgage options tailored for the aging population, is further diversifying the mortgage product landscape and broadening the addressable borrower base.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Bank & Financial Corporations

- Non-Banking Financial Companies (NBFCs)

Bank & financial corporations lead with a share of 68.4% of the total Japan consumer finance market in 2025.

Bank & financial corporations maintain a commanding position in Japan's consumer finance landscape, leveraging their extensive nationwide branch networks, deep capital reserves, and established consumer trust. In February 2026, Japan’s Mitsubishi UFJ Financial Group reported a 6% rise in third-quarter net profit to 520.6 billion yen, achieving 86% of its annual forecast amid strong loan demand. These institutions offer comprehensive product portfolios spanning mortgages, personal loans, and credit-based services, supported by robust risk management frameworks.

The growing emphasis on digital banking infrastructure is enabling these institutions to enhance service delivery through online platforms and mobile applications, broadening customer reach beyond traditional branch-based interactions. Ongoing strategic partnerships with technology providers and fintech firms are further strengthening their competitive positioning and operational efficiency across diverse consumer lending categories. The integration of advanced data analytics and artificial intelligence into credit assessment processes is also improving loan approval speed and accuracy, elevating the overall consumer experience.

Loan Purpose Insights:

- Debt Consolidation

- Home Renovations

- Education

- Car Purchase

- Medical Expenses

Debt consolidation dominates with a market share of 31.8% of the total Japan consumer finance market in 2025.

Debt consolidation has emerged as a prominent loan purpose category as Japanese consumers increasingly seek to simplify their financial obligations by combining multiple debt instruments into single, streamlined repayment arrangements. This approach offers potential benefits including reduced overall interest burden and improved household budget management. As per sources, the Japanese Financial Services Agency launched the “Multidebt Counsellor Support Campaign 2025,” providing free consultations and advisory services nationwide for consumers struggling with multiple debts, including guidance on consolidation and repayment strategies.

The rising awareness of financial planning tools and responsible borrowing practices is encouraging more consumers to pursue consolidation options as a pathway to improved creditworthiness. Financial institutions are actively developing dedicated consolidation products with competitive terms, recognizing the growing demand for solutions that help borrowers achieve greater financial stability and long-term debt management efficiency. Enhanced digital advisory platforms and automated eligibility assessments are further simplifying the consolidation process, making these products more accessible across diverse income levels and borrower demographics.

Credit Score Insights:

- Excellent

- Good

- Fair

- Poor

Good leads with a share of 39.5% of the total Japan consumer finance market in 2025.

Good represents the largest borrower segment in Japan's consumer finance market, reflecting the country's well-established credit reporting infrastructure and the generally disciplined financial behavior of Japanese consumers. Borrowers within this segment benefit from favorable lending terms, including competitive interest rates and broader product accessibility. The strong representation of this category underscores the effectiveness of Japan's financial education initiatives and prudent borrowing culture, which collectively foster a reliable and creditworthy consumer base for lending institutions.

The prevalence of comprehensive credit information systems, including integration with national identification frameworks, enables lenders to accurately assess and serve this segment with tailored offerings. The ongoing expansion of credit scoring methodologies incorporating alternative data sources is further refining risk assessment capabilities and improving lending outcomes for this dominant borrower category. Advanced analytics and machine learning tools are increasingly being deployed to enhance scoring precision, allowing financial institutions to offer more personalized products that align with the specific repayment capacities and financial goals of borrowers.

Term Length Insights:

- Short-Term

- Medium-Term

- Long-Term

Long-term dominates with a market share of 46.7% of the total Japan consumer finance market in 2025.

Long-term constitute the largest segment by term length, driven predominantly by the significant volume of mortgage lending and other substantial financial commitments that necessitate extended repayment periods. The cultural preference for gradual, manageable repayment schedules aligns with the risk-averse borrowing tendencies characteristic of Japanese consumers. In 2025, SBI Shinsei Bank began offering variable‑rate housing loans with repayment periods up to 50 years, expanding long‑term borrowing options for Japanese homebuyers seeking lower monthly payments.

The availability of ultra-long-term loan products, including repayment periods extending beyond traditional timeframes, is further expanding this segment as borrowers seek to manage rising property costs while maintaining affordable monthly obligations. Lenders continue to innovate within this category, offering flexible rate structures and customizable terms to meet diverse long-term financing needs. The introduction of hybrid repayment models that combine fixed and adjustable-rate components is also attracting a broader spectrum of borrowers seeking predictability alongside long-term cost optimization.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region leads with a share of 37.9% of the total Japan consumer finance market in 2025.

Kanto region commands the largest share of Japan's consumer finance market, anchored by the economic prominence of the Greater Tokyo metropolitan area, which serves as the nation's primary financial, commercial, and population center. High urbanization rates, elevated property values, and concentrated corporate activity generate substantial demand for mortgage, personal, and credit-based financial products. The region's dense population base and higher average disposable incomes further reinforce its position as the dominant consumer lending market across all product categories.

The region benefits from an advanced financial services infrastructure, with a high density of banking institutions, fintech companies, and digital lending platforms facilitating broad consumer access to diversified credit offerings. Rising living costs and dynamic real estate markets within the Kanto Region continue to sustain robust demand for consumer finance products across all borrower categories and loan purposes. The ongoing urban redevelopment initiatives and expanding commercial zones are also creating additional financing requirements that drive sustained lending activity throughout the region.

Market Dynamics:

Growth Drivers:

Why is the Japan Consumer Finance Market Growing?

Rising Consumer Financial Awareness and Credit Accessibility

The increasing financial literacy among Japanese consumers is playing a pivotal role in driving the adoption of diverse consumer finance products. Educational initiatives introduced across the national curriculum have strengthened foundational financial knowledge, empowering individuals to make more informed borrowing decisions. As per sources, in March 2025, 11 Japanese financial technology and services firms formed the “Financial Education Future Alliance,” collaborating to promote nationwide financial literacy through tech‑driven education programs and public outreach. Furthermore, this growing awareness, combined with the expansion of comprehensive credit reporting systems and national identification integration, has improved credit accessibility for a wider demographic base.

Progressive Monetary Policy Normalization and Evolving Interest Rate Environment

The ongoing transition toward a normalized monetary policy framework in Japan is fundamentally reshaping the consumer finance landscape. After an extended period of historically low borrowing costs, the gradual adjustment of policy rates is prompting significant recalibration across lending product categories. According to sources, in December 2025, the Bank of Japan raised its key policy rate to 0.75% from 0.5%, the highest since 1995, marking a major shift away from ultra-easy monetary conditions. This evolving environment is stimulating demand for fixed-rate products as borrowers seek to secure favorable terms, while also driving refinancing activity among existing loan holders. The resulting increase in banking sector profitability through improved net interest margins is enabling institutions to invest further in lending infrastructure and product innovation.

Digital Transformation and Fintech Integration in Lending Services

The rapid digitization of Japan’s financial services sector is significantly expanding the reach and efficiency of consumer lending operations. The proliferation of digital application platforms, artificial intelligence-powered credit scoring systems, and mobile-first banking interfaces is removing traditional barriers to credit access while reducing processing times and operational costs. The emergence of embedded finance models, where lending services are integrated directly into e-commerce and retail platforms, is creating new consumer touchpoints and borrowing opportunities. Additionally, strategic collaborations between established financial institutions and technology-focused firms are accelerating innovation in areas such as automated underwriting, personalized product recommendations, and real-time portfolio management, collectively broadening the addressable consumer finance market.

Market Restraints:

What Challenges the Japan Consumer Finance Market is Facing?

Demographic Headwinds from Population Aging and Decline

Japan's rapidly aging population and declining birth rates present structural challenges for the consumer finance market. A shrinking working-age population reduces the pool of active borrowers, while increasing longevity necessitates more conservative lending approaches for older demographics. These demographic dynamics constrain overall market expansion potential and require lenders to continuously adapt their product strategies.

Stringent Regulatory Caps on Lending Rates and Borrowing Limits

Japan's strict regulatory framework governing maximum interest rates and individual borrowing thresholds constrains the profitability and reach of consumer lending operations. While these regulations protect consumers from over-indebtedness, they limit the ability of lenders to serve higher-risk borrower segments and compress margins, particularly for specialized and non-banking financial institutions operating in the unsecured lending space.

Rising Borrowing Costs in a Tightening Monetary Environment

The gradual increase in benchmark interest rates is elevating borrowing costs for consumers, particularly those with variable-rate loan products. Higher monthly repayment obligations may dampen demand for new credit among price-sensitive borrowers and could increase default risks in certain segments. This cost pressure poses challenges for sustained lending volume growth, especially in mortgage and long-term financing categories.

Competitive Landscape:

The Japan consumer finance market is characterized by a moderately consolidated competitive structure, where established banking groups and specialized consumer lending institutions operate alongside a growing ecosystem of digital-native financial service providers. Market participants are increasingly prioritizing technological innovation, investing in artificial intelligence-driven credit assessment platforms, mobile-first customer interfaces, and seamless digital onboarding processes to enhance operational efficiency and consumer engagement. Strategic alliances between traditional lenders and technology-focused firms are reshaping competitive dynamics, enabling broader product diversification and improved service delivery.

Recent Developments:

-

In November 2024, Tokyo-based startup SmartBank raised $26 million to expand its personal finance management app, B/43. The platform offers prepaid cards, AI-driven financial advisory, and integrated credit management, targeting young adults and couples, while aiming to become a comprehensive fintech platform in Japan’s consumer finance market.

Japan Consumer Finance Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Personal Loans, Credit Cards, Mortgages, Auto Loans, Home Equity Loans |

|

Applications Covered |

Bank & Financial Corporations, Non-Banking Financial Companies (NBFCs) |

|

Loan Purposes Covered |

Debt Consolidation, Home Renovations, Education, Car Purchase, Medical Expenses |

|

Credit Scores Covered |

Excellent, Good, Fair, Poor |

|

Term Length’s Covered |

Short-Term, Medium-Term, Long-Term |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Consumer Finance Market Report

The Japan consumer finance market size was valued at USD 186.12 Billion in 2025.

The Japan consumer finance market is expected to grow at a compound annual growth rate of 2.88% from 2026-2034 to reach USD 240.31 Billion by 2034.

Mortgages, holding the largest revenue share of 42.6%, remain the dominant product type in Japan’s consumer finance market, driven by sustained homeownership demand, extended repayment options, and the cultural emphasis on long-term asset accumulation.

Key factors driving the Japan consumer finance market include rising financial literacy, progressive monetary policy normalization, accelerating digital transformation in lending services, expanding embedded finance ecosystems, and growing demand for flexible and personalized credit products.

Major challenges include demographic headwinds from population aging and decline, stringent regulatory caps on lending rates and borrowing limits, rising borrowing costs in a tightening monetary environment, and the need for continuous technological investment to serve evolving consumer expectations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)