Japan Cosmetics Market Size, Share, Trends and Forecast by Product Type, Category, Gender, Distribution Channel, and Region, 2026-2034

Japan Cosmetics Market Size, Share, Trends & Forecast (2026-2034)

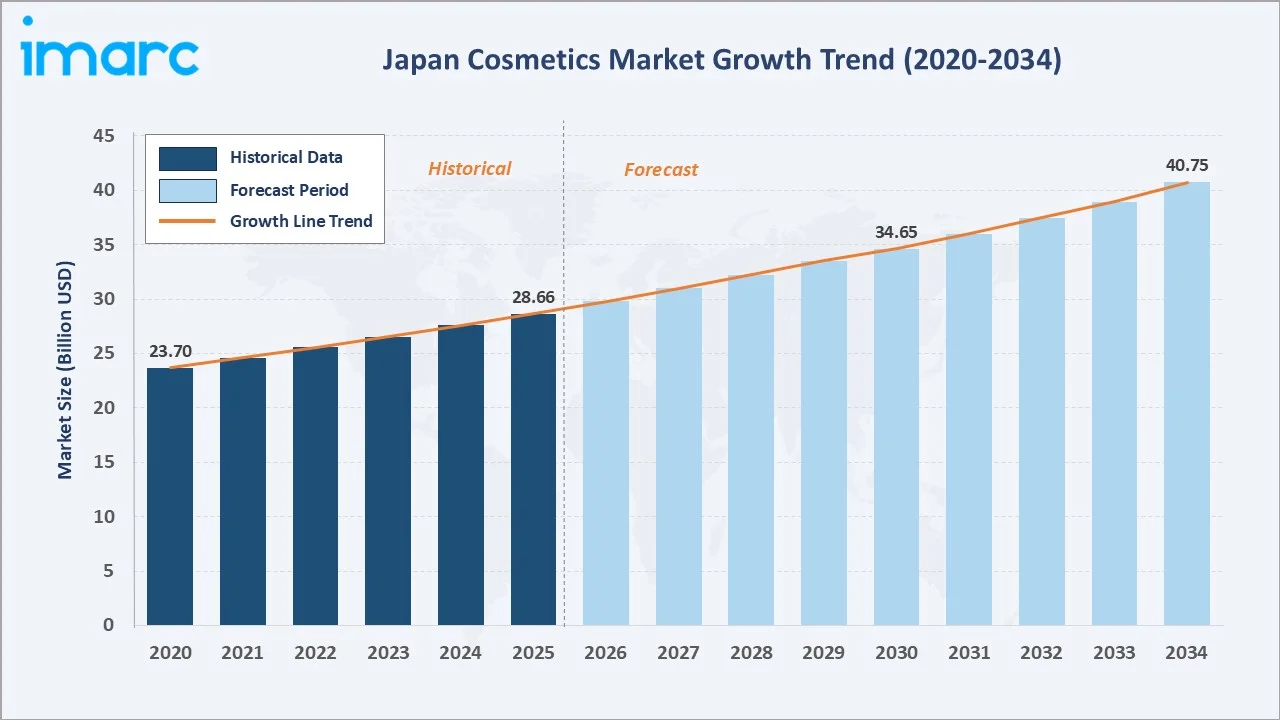

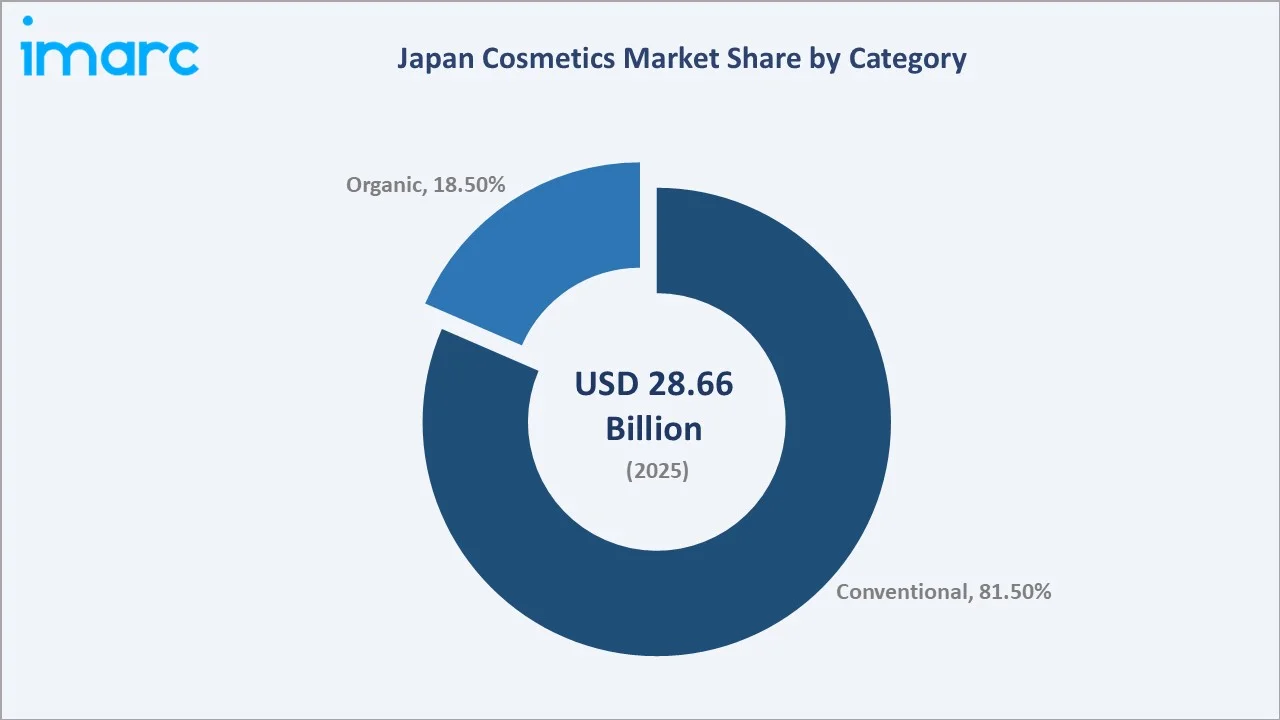

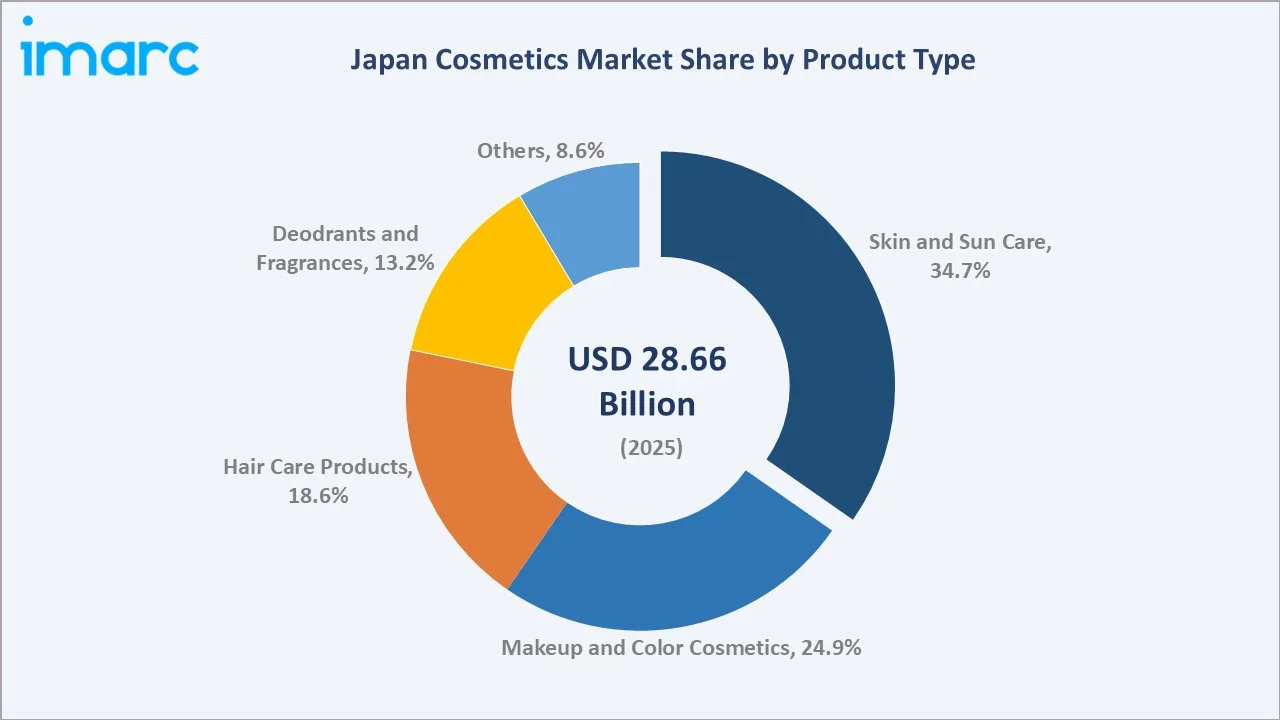

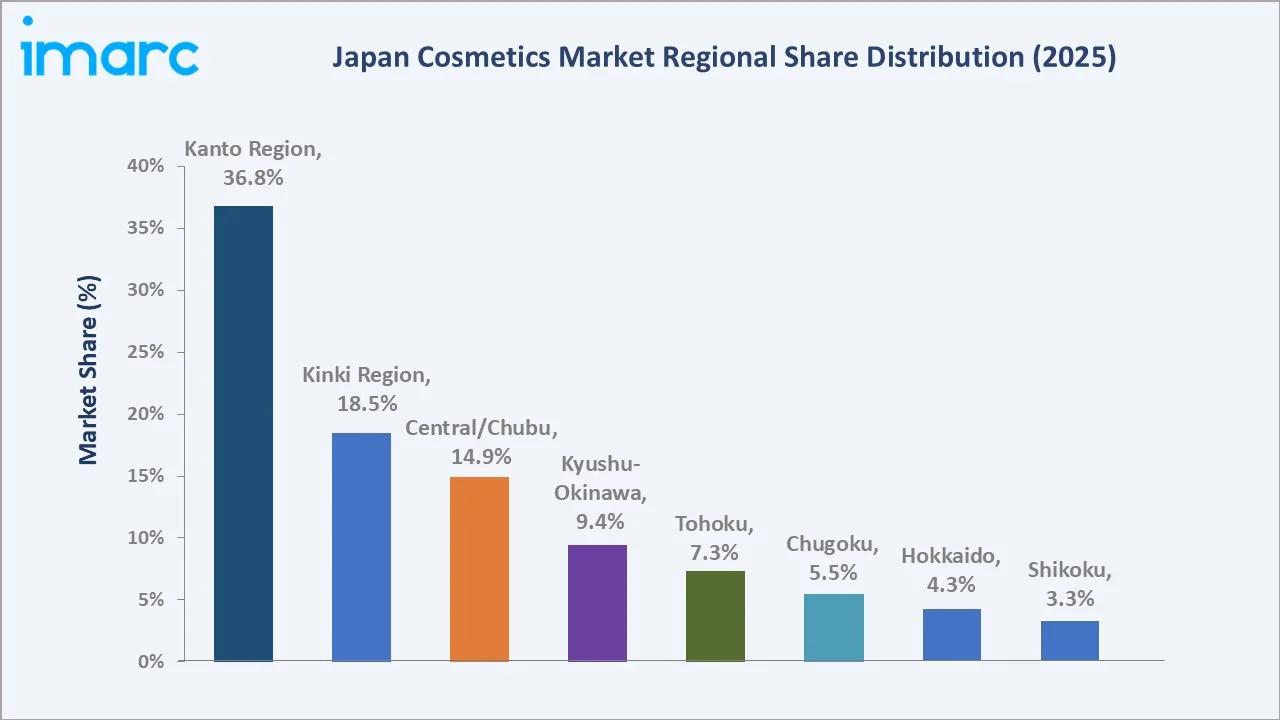

The Japan cosmetics market was valued at USD 28.66 Billion in 2025 and is projected to reach USD 40.75 Billion by 2034, growing at a CAGR of 3.87% during 2026-2034. Japan ranks among Asia’s top three beauty markets, driven by an aging population’s heightened skincare demand, a booming inbound tourism sector, and deep-rooted consumer culture around premium personal care. Skin and sun care products lead at 34.7% segment share (2025), while conventional products dominate the category mix at 81.5%. The Kanto region accounts for 36.8% of total market revenue, anchoring the market’s geographic concentration in Greater Tokyo.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 28.66 Billion |

|

Forecast Market Size (2034) |

USD 40.75 Billion |

|

CAGR (2026-2034) |

3.87% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

Kanto Region – 36.8% |

|

Fastest Growing Region |

Kanto Region (urbanization & tourism) |

The market grew from USD 23.70 Billion in 2020 to USD 28.66 Billion in 2025. It is anchored at USD 34.65 Billion in 2030 and is forecast to reach USD 40.75 Billion by 2034. Post-pandemic recovery in domestic consumption, a record-high inbound tourism influx in 2024, and expanding clean beauty preferences underpin this trajectory.

To get more information on this market, Request Sample

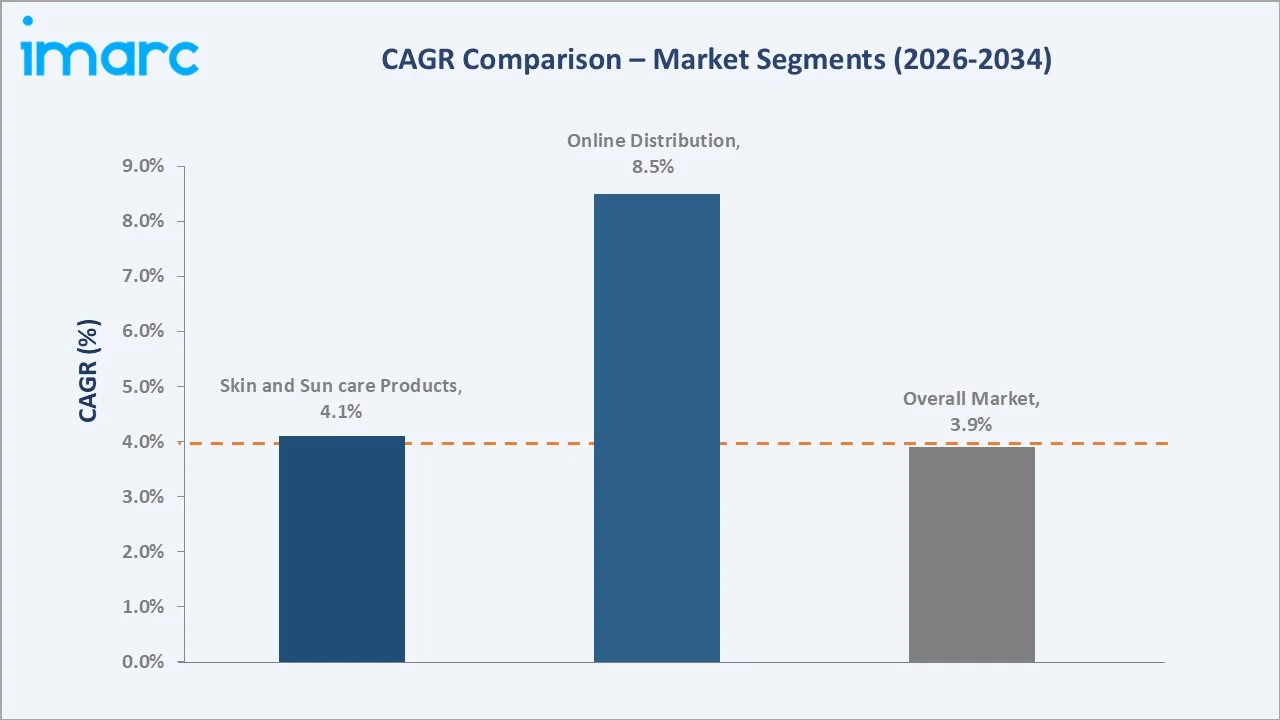

Online distribution is the fastest-growing channel at approximately 8.5% CAGR (2026-2034), driven by expanding e-commerce penetration and social commerce. Organic cosmetics grow at approximately 6.2% CAGR, outpacing conventional products at 3.1%, as consumer preference shifts toward clean, sustainable formulations.

Executive Summary

The Japan cosmetics market reached USD 28.66 Billion in 2025, solidifying its position as Asia’s third-largest beauty and personal care market. Japan’s unique consumer profile, characterized by a high-aging demographic, deep-seated skincare culture, and premium brand loyalty, creates a structurally stable yet innovation-driven market. Universal demand for functional beauty, anti-aging skincare, and multi-step routines support consistent per-capita spending that is among the highest in Asia. Japan’s cosmetics industry benefits from a sophisticated domestic manufacturing base and regulatory framework under the Pharmaceutical and Medical Device Act (PMDA), sustaining strong brand trust.

Market growth at 3.87% CAGR through 2034 reflects steady, sustainable expansion driven by aging population skincare demand, inbound tourism at record volumes (36.87 million foreign visitors in 2024 per JNTO), digital commerce adoption, and the K-beauty-influenced premiumization trend. Skin and sun care products lead at 34.7% of 2025 revenue, supported by Japan’s year-round UV awareness culture. Makeup and color cosmetics hold 24.9%, recovering post-pandemic with social event normalization.

The Kanto Region commands 36.8% of market revenue, anchored by the Greater Tokyo urban cluster’s retail density and flagship beauty stores. Specialty stores and pharmacies remain primary dispensing channels, while online retail grows fastest at approximately 8.5% CAGR. Key players Shiseido, Kao Corporation, and KOSE Holding Corporation dominate the domestic landscape, collectively accounting for a significant portion of market revenue.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Product Type) |

Skin and Sun Care Products - 34.7% share (2025) |

|

Largest Category |

Conventional - 81.5% share (2025) |

|

Fastest Growing Category |

Organic - ~6.2% CAGR (2026-2034) |

|

Leading Region |

Kanto Region - 36.8% share (2025) |

|

Top Companies |

Shiseido Company, Limited, Kao Corporation, KOSE Holding Corporation, L'Oreal S.A. |

|

Market Opportunity |

Men’s grooming, organic cosmetics, AI-personalized skincare |

Key Analytical Observations Supporting The Above Data:

- Skin and sun care products at 34.7% (2025) reflect Japan’s deeply entrenched UV protection culture. Japan’s National Institute of Infectious Diseases data indicates over 65% of Japanese consumers apply SPF products daily, creating a structurally high baseline demand for sun care formulations year-round.

- Conventional cosmetics dominate at 81.5% due to their established distribution footprint across pharmacies and mass retail. However, organic cosmetics at 18.5% are gaining ground, supported by younger millennial and Gen Z consumers prioritizing clean ingredient lists, as noted by Japan’s Consumer Affairs Agency (2024) green product preference survey.

- Organic cosmetics growing at 6.2% CAGR outpace the overall market, driven by government sustainability initiatives and METI’s Green Innovation Fund supporting eco-friendly formulation R&D.

- Kanto Region at 36.8% reflects Tokyo’s cosmopolitan retail density, with Shinjuku and Shibuya districts housing flagship stores for all major domestic and international cosmetics brands.

Japan Cosmetics Market Overview

Japan’s cosmetics market encompasses skincare, color cosmetics, hair care, fragrances, deodorants, and personal care products sold through retail, pharmacy, specialty, and online channels. The ecosystem integrates domestic raw material suppliers, leading Japanese and multinational manufacturers, MHLW-regulated product approval pathways, and multi-tier distribution through cosmetics specialty chains (Cosme Kitchen, @cosme store), pharmacy chains (Matsumoto Kiyoshi, Sundrug), department stores, and e-commerce platforms (Amazon Japan, Rakuten, brand-owned DTC sites).

Japan’s macroeconomic environment is characterized by modest but positive GDP growth, a weakening yen boosting inbound tourist spending power in 2024-2025, and a structural aging dynamic where 34.9% of the population was aged 65 or older in 2020 (Ministry of Internal Affairs and Communications). The Pharmaceutical and Medical Device Act (PMDA framework) governs cosmetic product registration, ensuring consumer safety and elevating market entry standards that favor established players.

Market Dynamics

To evaluate market opportunities, Request Sample

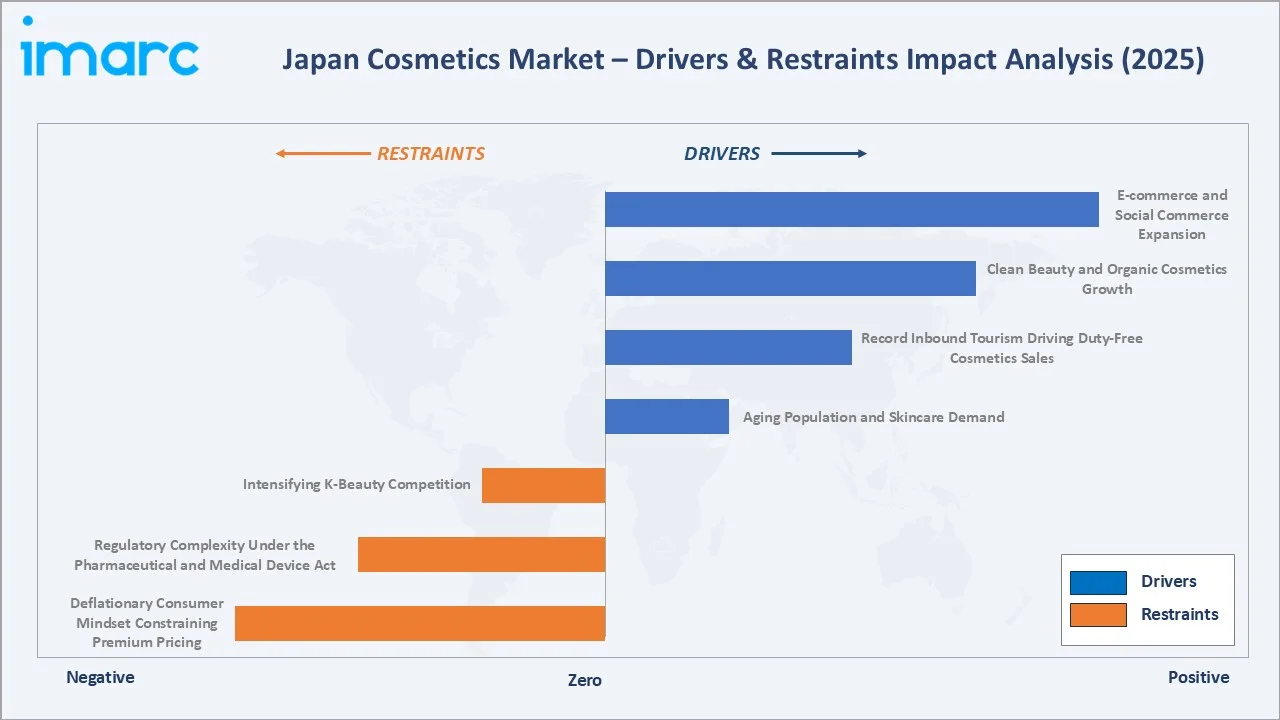

Market Drivers

- Aging Population and Skincare Demand: Japan’s population aged 65 or older is projected to reach 47% by 2050. Elderly consumers allocate disproportionately high spending to anti-aging skincare, moisturizers, and UV protection. Japan recorded 10.8 million adults with diabetes-related skin sensitivity requiring specialized derma-cosmetic products (2024), further deepening functional skincare demand.

- Record Inbound Tourism Driving Duty-Free Cosmetics Sales: JNTO reported 37 million inbound visitors in 2024, generating substantial cosmetics purchases at duty-free stores, airports, and urban specialty retailers. Chinese, Korean, and Southeast Asian visitors specifically target premium Japanese cosmetics brands as high-value souvenirs.

- Clean Beauty and Organic Cosmetics Growth: Japan’s Consumer Affairs Agency (2024) green product preference survey identified over 60% of urban female consumers aged 25-44 prioritizing natural ingredient lists in new cosmetics purchases, directly driving organic segment expansion at 6.2% CAGR.

- E-commerce and Social Commerce Expansion: In 2024, the scale of the domestic B-to-C e-commerce market increased to 26.1 trillion yen, driven by @cosme beauty platform integration, TikTok-driven product discovery, and premium brand DTC site expansion.

Market Restraints

- Deflationary Consumer Mindset Constraining Premium Pricing: Japan’s decades-long deflation psychology leads consumers to resist price increases despite inflationary raw material costs. Shiseido, Kao, and KOSE Holding Corporation implemented price hikes in April 2024 in response to rising costs, but cautious consumer sentiment moderated volume uptake in Q4 2024.

- Regulatory Complexity Under the Pharmaceutical and Medical Device Act: Japan’s PMDA framework requires extensive ingredient registration and efficacy substantiation for quasi-drug cosmetics, creating 12–24-month market entry timelines for new formulations and limiting rapid product iteration common in K-beauty competitors.

- Intensifying K-Beauty Competition: Korean cosmetics brands including Innisfree, Laneige, and Sulwhasoo have captured an estimated 8–10% of Japan’s mid-premium skincare market by 2025, appealing to younger consumers with innovative textures, competitive pricing, and viral social media presence.

Market Opportunities

- Men’s Grooming Mainstream Adoption: Japan’s men’s cosmetics market was valued at approximately 4.5% of total cosmetics sales in 2024, with Kao’s KATE brand and Shiseido’s UNO line reporting accelerating growth. The Men’s Non-No magazine survey (2024) found 58% of Japanese men aged 18–35 using skincare products regularly, signaling strong market expansion potential.

- AI-Personalized Beauty Solutions: Shiseido launched its Beauty AR Navigation app in January 2024, partnering with dermatologists to provide personalized product recommendations. Similar platforms by POLA Orbis and Fancl create premium subscription revenue streams with higher customer lifetime value.

- Sustainable Packaging and Refill Economy: Japan’s Ministry of Environment’s Plastic Resource Circulation Act (effective 2022) incentivizes cosmetic brands to adopt refillable packaging. Kao’s MERIT shampoo refill pack achieved 92% adoption rate among repeat purchasers by 2024, demonstrating strong consumer acceptance.

Market Challenges

- Declining Domestic Birth Rate Reducing Youth Consumer Base: Japan's total fertility rate fell further to a record-low of 1.15 in 2024, continuing its decline from 1.20 in 2023 (Ministry of Health, Labour and Welfare), the lowest on record, shrinking the future youth consumer pipeline that drives color cosmetics and trend-sensitive beauty segments.

- Supply Chain Pressures from JPY Weakness: The Japanese yen’s depreciation to multi-decade lows in 2024 increased import costs for essential raw materials including synthetic fragrances, specialty oils, and packaging materials, compressing margins for brands without fully domestic supply chains.

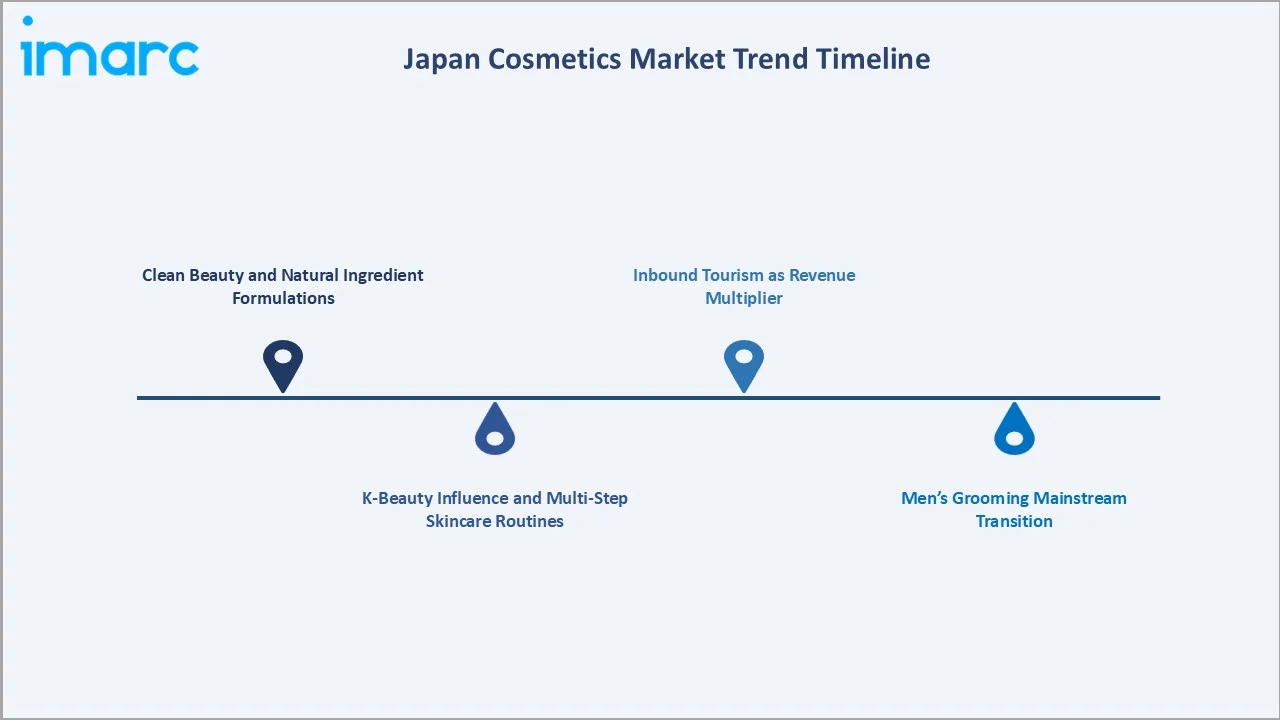

Emerging Market Trends

1. Clean Beauty and Natural Ingredient Formulations

Japan’s clean beauty movement accelerated post-2020 as consumers became more ingredient conscious. Brands reformulating with Japanese botanical actives, including yuzu, sake ferment, camellia oil, capturing premium positioning.

2. K-Beauty Influence and Multi-Step Skincare Routines

Korean beauty’s influence reshaped Japan’s mass skincare market from 2021 onward. Essence layers, sheet mask integration, and ceramide-first formulation approaches migrated into mainstream Japanese product ranges. @cosme’s 2024 Bestseller Awards showed K-beauty products capturing 6 of the top-20 skincare spots, indicating sustained consumer appetite for Korean-style innovation.

3. Inbound Tourism as Revenue Multiplier

Japan’s record 37 million inbound visitors in 2024 (JNTO) created a dual-revenue dynamic: domestic consumption plus tourist spending at flagship stores and duty-free channels. Shiseido reported Japan business growth in the low teens in Q4 2024, with ELIXIR serum and Foundation Serum launches contributing to inbound consumer purchases above baseline.

4. Men’s Grooming Mainstream Transition

Japan’s men’s grooming market is transitioning from niche to mainstream, driven by K-beauty’s normalization of male skincare and workplace diversity acceptance. Kao’s KATE brand announced strategic initiatives in 2025 to promote Japanese makeup culture globally, with men’s lines as a key growth pillar. The men’s skincare segment is estimated to grow at approximately 7% CAGR through 2034.

5. AI and Technology-Driven Personalization

AI-powered skin analysis tools are transforming Japan’s beauty retail landscape. AS Watson Group launched Skinfie Lab, an innovative skin analysis tool generating personalized product recommendations from customer selfies, in October 2022. Shiseido’s Foundation Serum launch in May 2024 incorporated skin diagnosis data to deliver customized coverage levels, representing the convergence of technology and beauty at scale.

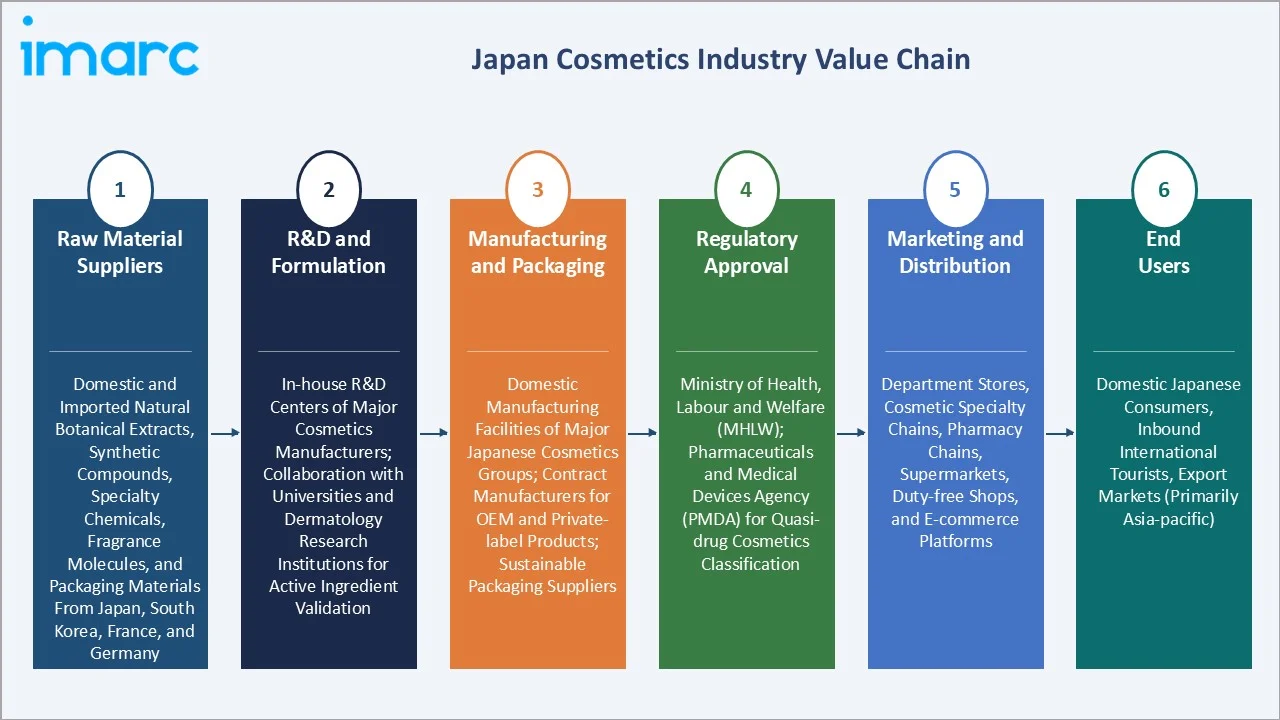

Industry Value Chain Analysis

Japan’s cosmetics market value chain integrates raw material supply through formulation R&D, PMDA-regulated manufacturing, multi-tier distribution, and end consumer delivery across retail, pharmacy, specialty, and online channels.

|

Stage |

Key Participants |

|

Raw Material Suppliers |

Domestic and imported natural botanical extracts, synthetic compounds, specialty chemicals, fragrance molecules, and packaging materials from Japan, South Korea, France, and Germany |

|

R&D and Formulation |

In-house R&D centers of major cosmetics manufacturers; collaboration with universities and dermatology research institutions for active ingredient validation |

|

Manufacturing and Packaging |

Domestic manufacturing facilities of major Japanese cosmetics groups; contract manufacturers for OEM and private-label products; sustainable packaging suppliers |

|

Regulatory Approval |

Ministry of Health, Labour and Welfare (MHLW); Pharmaceuticals and Medical Devices Agency (PMDA) for quasi-drug cosmetics classification |

|

Marketing and Distribution |

Department stores, cosmetic specialty chains, pharmacy chains, supermarkets, duty-free shops, and e-commerce platforms |

|

End Users |

Domestic Japanese consumers, inbound international tourists, export markets (primarily Asia-Pacific) |

Technology Landscape in the Japan Cosmetics Industry

AI and Digital Skin Analysis

Japan’s cosmetics industry leads globally in AI-driven skin diagnosis applications. KOSE Holding Corporation collaborated with biotech firms in 2024 to develop beauty products using iPS cell-based skin modeling, marking a convergence of regenerative medicine and cosmetics.

Biomimetic and Biotechnology Ingredients

Japan’s cosmetic ingredient innovation focuses on biomimetic peptides, fermented actives, and skin microbiome-supporting formulations. Fancl’s proprietary nano-encapsulation technology delivers active ingredients at 50-nanometer particle sizes for enhanced dermal penetration.

Sustainable Formulation and Green Chemistry

In response to the Plastic Resource Circulation Act and consumer sustainability preferences, Japan’s cosmetics R&D is shifting toward waterless formulations, biodegradable packaging, and cold-process manufacturing reducing energy consumption. Kao’s MERRIES and skincare lines achieved 30% reduction in CO2 emissions per product unit by 2024, as reported in the Kao Integrated Report 2024.

E-commerce Technology and Virtual Try-On

Japan’s beauty e-commerce integrates augmented reality (AR) virtual try-on tools pioneered by @cosme and individual brand apps. L’Oréal Japan’s ModiFace AR platform drives online color cosmetics conversion rates 3x above industry baseline. Real-time social commerce through LINE and TikTok Shop is expanding impulse purchase channels for beauty products.

Market Segmentation Analysis

The report covers the following segment:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Category |

Conventional |

81.5% |

2025 |

|

Product Type |

Skin and Sun Care Products |

34.7% |

2025 |

|

Gender |

🔒 |

🔒 |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Kanto |

36.8% |

2025 |

By Category

Conventional cosmetics lead at 81.5% market share (2025). Japan’s established pharmacy distribution infrastructure, mass-market pricing, and consumer brand familiarity anchor conventional cosmetics dominance. The segment grows at approximately 3.1% CAGR, driven by core replenishment purchasing across moisturizers, shampoos, and color cosmetics. Price increases implemented by major manufacturers in April 2024 were absorbed without significant volume decline, confirming conventional cosmetics’ inelastic demand profile.

To access detailed market analysis, Request Sample

Organic cosmetics at 18.5% are the market’s fastest-growing category at approximately 6.2% CAGR. Premium organic brands including NATURAGLACE, ETVOS, and Pañpuri (acquired by KOSE Holding Corporation in 2024) are capturing the 25-44 urban female demographic at higher price points.

By Product Type

Skin and sun care products dominate at 34.7% share (2025). Japan’s year-round UV awareness, supported by the Japanese Dermatological Association’s public health campaigns on UV-related skin damage, drives among the world’s highest per-capita SPF product consumption rates. The segment is projected to grow at approximately 4.1% CAGR through 2034, supported by innovation in lightweight, tinted SPF foundations and reef-safe mineral sunscreen formulations.

Makeup and color cosmetics at 24.9% are recovering strongly post-pandemic as social events, workplace return, and inbound tourist demand normalize. Hair care products at 18.6% are driven by premium scalp care and treatment innovation, with Kao’s melt and THE ANSWER premium brands exceeding sales plan in 2024. Deodorants and fragrances at 13.2% show stable growth, benefiting from Japan’s outdoor summer culture and increasing fragrance adoption among younger consumers.

Regional Market Insights

|

Region |

Share (2025) |

Major Growth Drivers |

|

Kanto |

36.8% |

Inbound tourism, urban premium retail, e-commerce HQ concentration |

|

Kinki |

18.5% |

Domestic tourism, luxury beauty demand, Kyoto botanical brand heritage |

|

Central/Chubu |

14.9% |

Industrial workforce personal care, growing e-commerce adoption |

|

Kyushu-Okinawa |

9.4% |

Sun care demand, local botanical ingredient brands, inbound Asian tourists |

|

Tohoku |

7.3% |

Aging population skincare needs, rural pharmacy chain expansion |

|

Chugoku |

5.5% |

Stable mass-market cosmetics demand, pharmacy chain consolidation |

|

Hokkaido |

4.3% |

Cold-climate skincare formulations, tourist duty-free purchases |

|

Shikoku |

3.3% |

Pharmacy-centered distribution, anti-aging product demand |

Competitive Landscape

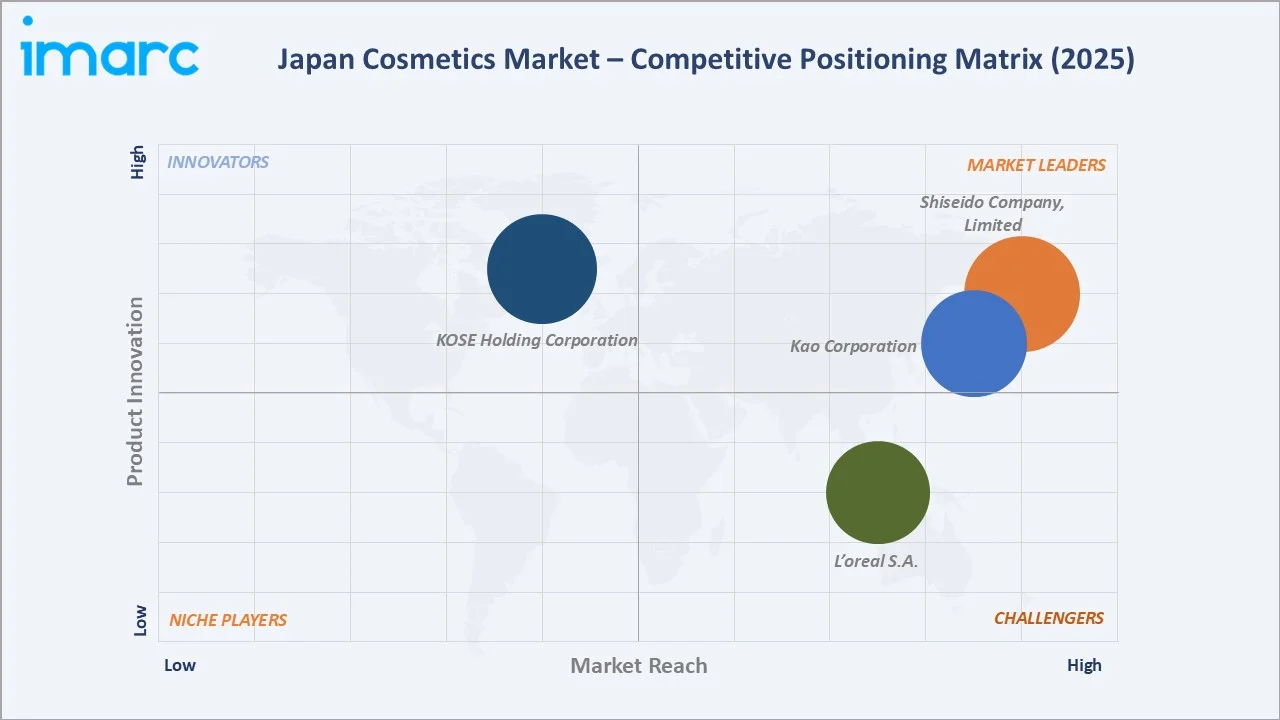

Japan’s cosmetics market is moderately concentrated at the domestic branded premium level. Shiseido, Kao Corporation, and KOSE Holding Corporation collectively hold an estimated 45–50% of the domestic market by value (2025). International brands including L’Oréal, Estée Lauder, and Procter & Gamble maintain significant presence, particularly in imported premium skincare and fragrances. The competitive landscape is intensifying through K-beauty brand entries and niche DTC digital-native brands.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Shiseido Company, Limited |

ELIXIR, Clé de Peau Beauté, NARS |

Market Leader |

Japan’s largest cosmetics company; premium and prestige positioning across all segments |

|

Kao Corporation |

KANEBO, KATE, SOFINA iP, Curél, SENSAI |

Market Leader |

RNA-based skin analysis technology for differentiated product development |

|

KOSE Holding Corporation |

Sekkisei, Cosme Decorté, JILL STUART |

Established Player |

Prestige skincare heritage; acquired Thai brand Pañpuri in 2024; AI-driven formulation R&D with hospital partnerships |

|

L'Oreal S.A. |

Lancôme, Maybelline |

Global Challenger |

Operates through its regional subsidiary L'Oréal Japan (Nihon L'Oréal K.K.). Largest international cosmetics group in Japan |

Shiseido’s quasi-drug skincare lines add complexity to competitive dynamics, blending pharmaceutical and cosmetics categories in Japan’s unique regulatory environment where quasi-drug products (including whitening and anti-acne actives) command premium pricing.

Key Company Profiles

Shiseido Company, Limited

Shiseido is Japan’s largest and oldest cosmetics company, founded in 1872, and ranks among the top 10 global beauty manufacturers by revenue. Shiseido operates across prestige skincare, color cosmetics, fragrances, and personal care, serving over 120 countries.

- Product Portfolio: ELIXIR, Clé de Peau Beauté, NARS

- Recent Developments: In October 2025, Shiseido conducted a study with the Tohoku University Hospital Department of Dermatology, to strengthen sensitive skin science through research and development in cooperation with dermatologists in Japan and apply this to value development in areas such as cosmetics and services with the aim of realizing healthy beauty throughout each person's life.

- Strategic Focus: Selection and concentration around core brands; Japan domestic profit recovery targeting JPY 50 billion in 2025; AI-powered personalization tools for premium consumer engagement.

Kao Corporation

Kao Corporation is Japan’s second-largest cosmetics and personal care group. It operates across prestige skincare (KANEBO), mass makeup (KATE), dermacare (Curél), science-driven skincare (SOFINA), and other brands.

- Product Portfolio: KANEBO, KATE, SOFINA iP, Curél, SENSAI

- Recent Developments: In July 2025, Kao Corporation announced the launch of SENSAI TOTAL FORM EXPERT CREAM, an anti-ageing cream, which combines Koishimaru Silk EX*1, SENSAI’s signature moisturizing ingredient, with the Total Form CPX*2 complex.

- Strategic Focus: Premium cosmetics strategy; KATE brand expansion; RNA-based skin analysis technology for differentiated product development; OMO (online-merges-with-offline) channel integration in Asia.

Market Concentration Analysis

Japan’s cosmetics market exhibits moderate-to-high concentration at the premium branded segment, with Shiseido, Kao Corporation, and KOSE Holding Corporation collectively holding an estimated 45–50% of total market revenue in 2025. At the mass-market level, competition from private labels, K-beauty imports, and DHC’s DTC model is more fragmented, reducing concentration in the sub-JPY 1,500 price tier.

Consolidation trends are reshaping the mid-market. KOSE Holding Corporation’s acquisition of Pañpuri (2024) reflects a broader M&A strategy of acquiring premium niche brands to diversify beyond domestic mass cosmetics. Similarly, Shiseido’s brand portfolio rationalization, retaining 8 core brands and divesting underperformers, signals intentional concentration of investment behind fewer, higher-return brand assets. The entry of Activist investor Oasis Management urging Kao to unlock cosmetics brand value globally in 2024 further indicates institutional pressure for strategic consolidation around high-growth segments.

International players L’Oréal and Estée Lauder hold an estimated 10-12% of Japan’s total cosmetics market combined, competing primarily in the luxury and prestige segment rather than the mass-market where domestic brands have overwhelming advantages through distribution depth and brand heritage.

Investment & Growth Opportunities

Fastest Growing Segments

Online distribution channel (approximately 8.5% CAGR), organic cosmetics category (approximately 6.2% CAGR), men’s grooming (approximately 7% CAGR), AI-personalized skincare platforms (high double-digit CAGR), and premium sun care formulations (approximately 5% CAGR) represent Japan’s highest-growth cosmetics investment vectors through 2034. Sustainable refillable packaging solutions are emerging as a differentiated revenue stream as the Plastic Resource Circulation Act matures.

Emerging Market Opportunities

Japan’s rural prefectures (Tohoku, Chugoku, Shikoku) represent underserved cosmetics markets where pharmacy chains are the primary beauty retail channel and digital commerce penetration lags urban centers by 5-7 years. Targeted digital-first brand strategies, pharmacy-partnership DTC models, and subscription refill programs offer growth vectors in these lower-competition geographies. The men’s grooming segment’s transition from niche to mainstream creates a USD 1-2 billion incremental opportunity by 2034 if current adoption rates in the 18-34 demographic continue accelerating.

Investment Themes

- Japan Cosmetics Brand Acquisition: International beauty groups seeking premium Asia-Pacific positioning can acquire mid-size domestic Japanese brands with strong pharmacy and specialty channel distribution at attractive multiples compared to global cosmetics M&A benchmarks.

- Technology Platform Investment: AI-skin analysis, AR try-on, and personalized formulation platforms are in early growth stages in Japan, with beauty tech companies raising Series B and C rounds. Japan’s high smartphone penetration (approximately 96% in 2024 per MIC Japan) and tech-savvy consumer base support rapid platform adoption.

- Organic Ingredient Supply Chain: Japan’s growing organic cosmetics segment creates opportunities for domestic botanical ingredient suppliers aligned with Japan’s clean-label and traceability preferences.

Future Market Outlook (2026-2034)

The Japan cosmetics market is projected to grow from USD 28.66 Billion in 2025 to USD 40.75 Billion by 2034 at a steady 3.87% CAGR. This trajectory reflects Japan’s unique market economics, an aging domestic consumer base continuously deepening skincare spending, offset by a declining youth demographic, with net positive growth anchored by premiumization, organic category expansion, and digital commerce scaling.

Japan’s USD 34.65 Billion market in 2030 will consolidate its position as Asia’s third-largest cosmetics market, with Kanto Region maintaining its dominant 36.8%+ share driven by Tokyo’s role as a global beauty retail destination. Three structural forces anchor this growth with high predictability: Japan’s irreversible demographic aging deepening anti-aging skincare penetration; the digital transformation of beauty retail through AI personalization, AR try-on, and social commerce; and the premium sustainability transition as organic cosmetics approach 25% market share by 2034.

Technological disruption will reshape competitive dynamics through 2034. AI-powered skin analysis platforms will commoditize basic skincare consultation, shifting competitive advantage toward proprietary active ingredient innovation and brand heritage. Biotechnology-derived cosmetic actives (iPS cell-based formulations, microbiome-targeting probiotics) represent Japan’s next differentiation frontier, with commercial applications expected by 2027-2030. Japan’s cosmetics industry is well-positioned to lead this innovation wave given its academic research infrastructure, regulatory sophistication, and consumer openness to technology-integrated beauty.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including senior executives from Shiseido Company, Limited, Kao Corporation, KOSE Holding Corporation, L'Oreal S.A.; dermatologists from Keio University Hospital and Osaka University Hospital; beauty retail chain executives from Matsumoto Kiyoshi, @cosme, and Cosme Kitchen; MHLW regulatory specialists; and independent cosmetics industry consultants. Primary insights informed market driver validation, competitive landscape mapping, and regional market characterization.

Secondary Research

Secondary research encompassed Japan Cosmetics Industry Association (JCIA) trade statistics 2020-2024; Ministry of Economy, Trade and Industry (METI) e-commerce market surveys; Japan Tourism Agency inbound visitor data; Cabinet Office demographic aging projections; Pharmaceutical and Medical Device Act regulatory database; annual reports and investor presentations Shiseido Company, Limited, Kao Corporation, KOSE Holding Corporation, L'Oreal S.A.; @cosme Bestseller Award data; and independent market intelligence. Over 120 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up consumer spending modeling by product segment and region, cross-validated against industry association revenue data, company annual report segment disclosures, and macroeconomic demographic projections. Key inputs include JCIA category-level growth rates, Cabinet Office aging population projections through 2034, METI e-commerce growth scenarios, organic market adoption S-curve modeling, and inbound tourism revenue contribution analysis.

Japan Cosmetics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Product Types Covered | Skin and Sun Care Products, Hair Care Products, Deodorants and Fragrances, Makeup and Color Cosmetics, Others |

| Categories Covered | Conventional, Organic |

| Genders Covered | Men, Women, Unisex |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Pharmacies, Online Stores, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, and Shikoku Region |

| Companies Covered | Shiseido Company Limited, Kao Corporation, KOSE Holding Corporation, L'Oreal S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan cosmetics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan cosmetics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan cosmetics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Cosmetics Market Report

The Japan cosmetics market was valued at USD 28.66 Billion in 2025, covering skincare, makeup, hair care, fragrances, and deodorants across all distribution channels serving domestic and inbound international consumers.

The market is projected to grow at a CAGR of 3.87% during 2026-2034, reaching USD 40.75 Billion by 2034, driven by aging population skincare demand, organic cosmetics expansion, digital commerce growth, and premium tourism purchasing.

Skin and sun care products lead at 34.7% market share (2025), driven by Japan’s deep-rooted UV protection culture and high per-capita spending on moisturizers, serums, and SPF formulations across all age demographics.

Conventional cosmetics dominate at 81.5% share (2025), anchored by established distribution infrastructure, mass-market pricing, and strong domestic brand loyalty. Organic cosmetics at 18.5% are the fastest-growing segment at approximately 6.2% CAGR.

Kanto Region leads at 36.8% share (2025), driven by Greater Tokyo’s cosmopolitan retail density, flagship beauty stores, high-income urban consumers, and Japan’s highest concentration of inbound tourist spending.

Leading companies include Shiseido Company, Limited, Kao Corporation, KOSE Holding Corporation, L'Oreal S.A.

Japan’s cosmetics market is projected to reach approximately USD 34.65 Billion by 2030, driven by premium skincare expansion, organic cosmetics category growth, and continued e-commerce channel scaling.

Key drivers include Japan’s aging population driving anti-aging skincare demand, record inbound tourism (37 million visitors in 2024) boosting duty-free purchases, growing organic beauty preference, and rapid e-commerce channel expansion at approximately 8.5% CAGR.

Online distribution is growing fastest at approximately 8.5% CAGR (2026–2034), driven by social commerce adoption, AR try-on technology, DTC brand expansion, and post-pandemic normalization of e-pharmacy and beauty subscription models.

Inbound tourism significantly amplifies Japan cosmetics revenue. Japan’s record 37 million visitors in 2024 (JNTO) generated disproportionate duty-free cosmetics purchases, particularly at airport shops and Shinjuku flagship stores, contributing to Shiseido’s Japan business double-digit growth in 2024.

K-beauty has captured an estimated 8-10% of Japan’s mid-premium skincare market by 2025, driving domestic brands to innovate faster in essence formulations, sheet masks, and ceramide-focused products. @cosme’s 2024 awards showed K-beauty capturing 6 of the top-20 skincare spots.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)