Japan Data Monetization Market Size, Share, Trends and Forecast by Method, Organization Size, End Use, and Region 2026-2034

Japan Data Monetization Market Size, Share, Trends & Forecast (2026-2034)

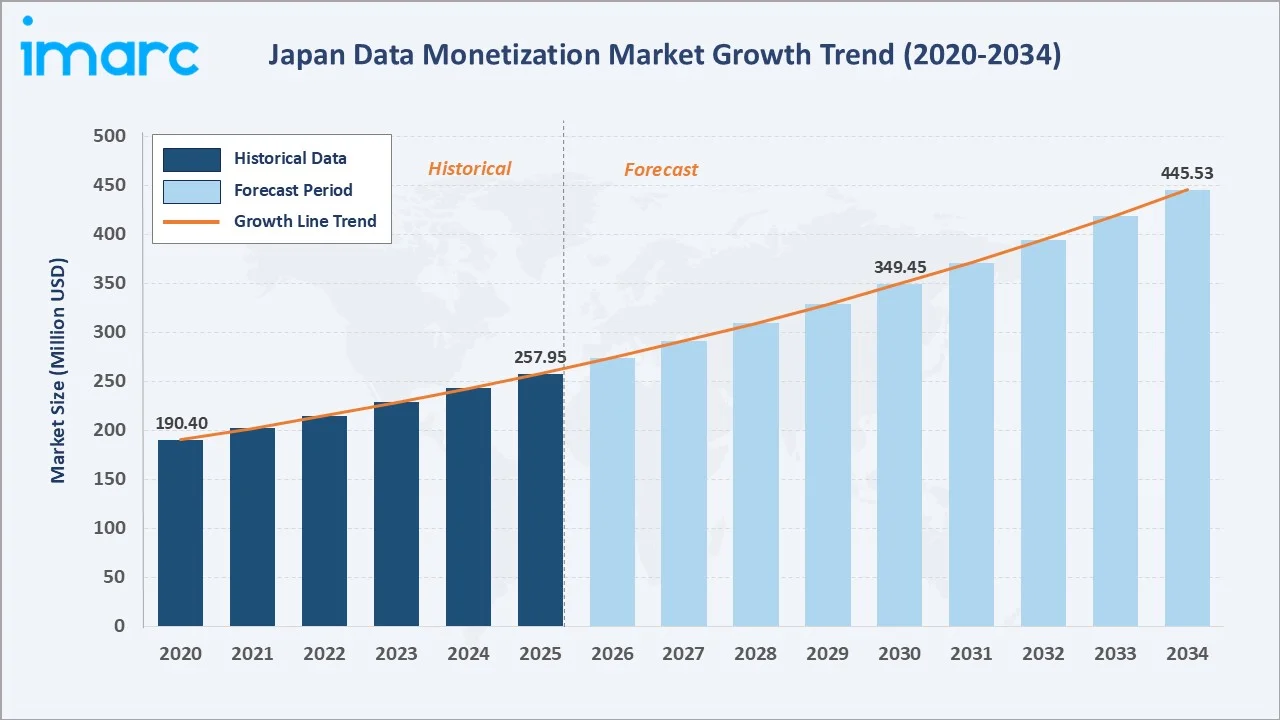

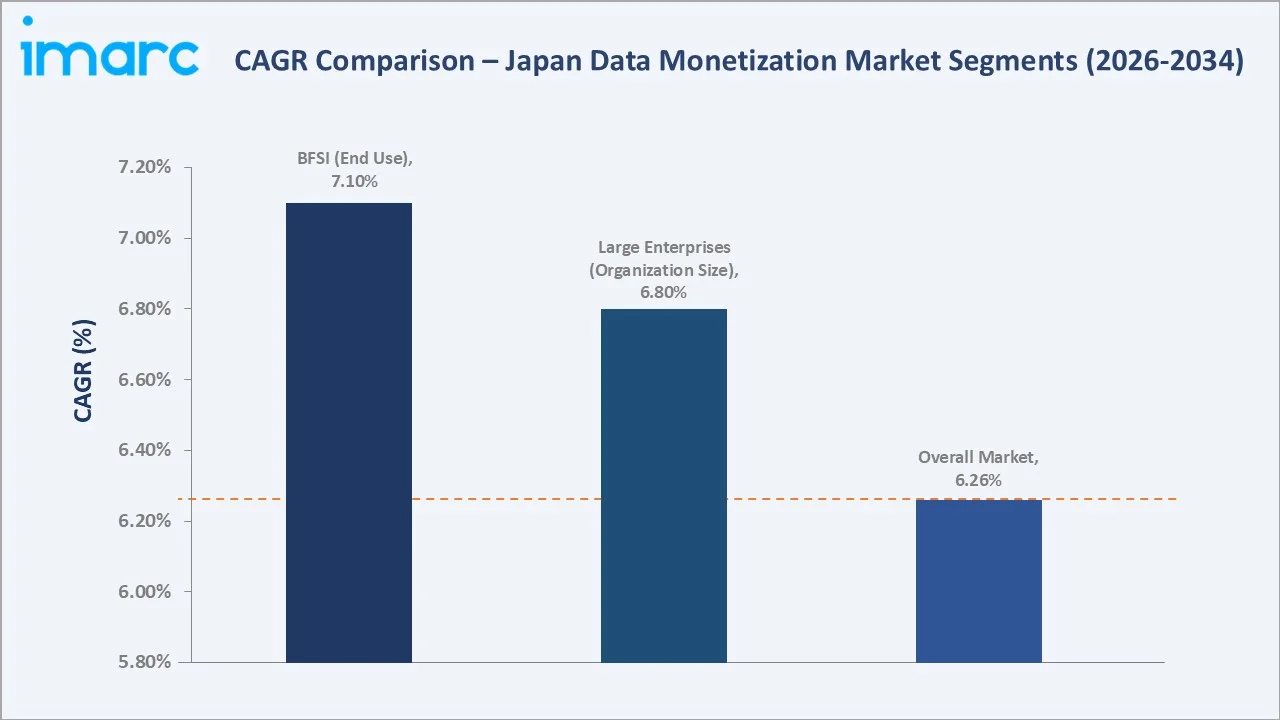

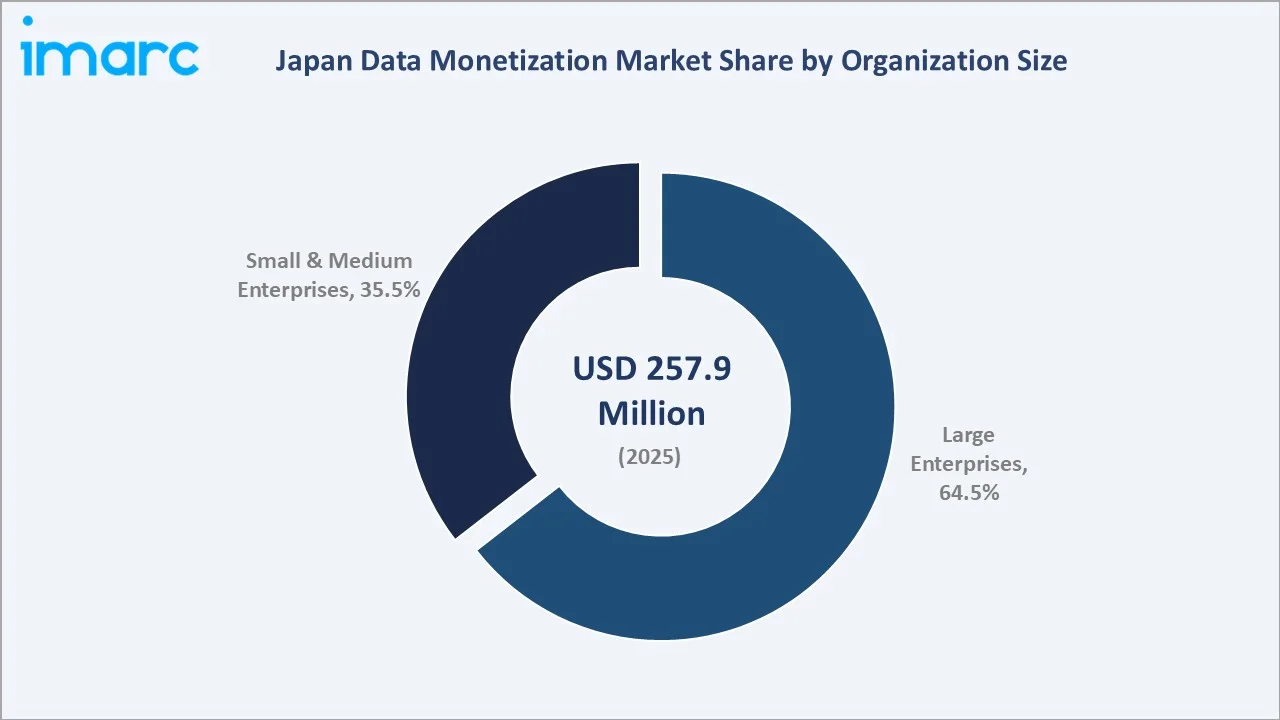

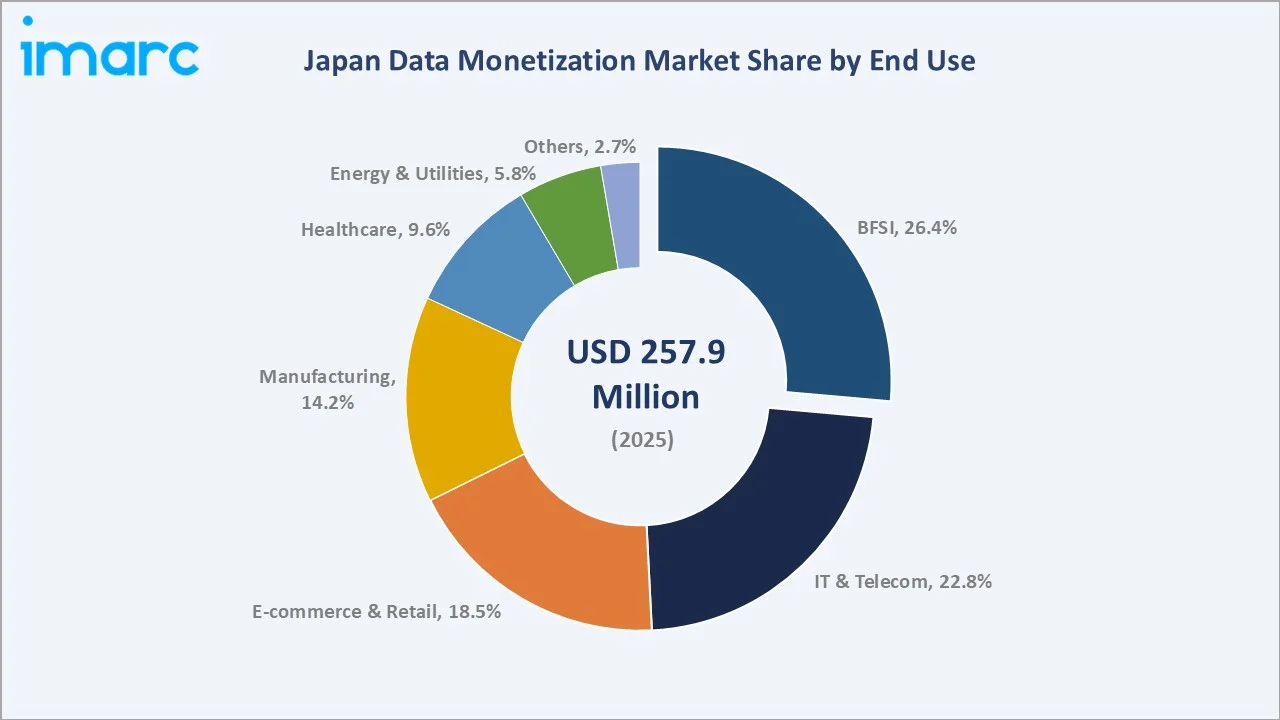

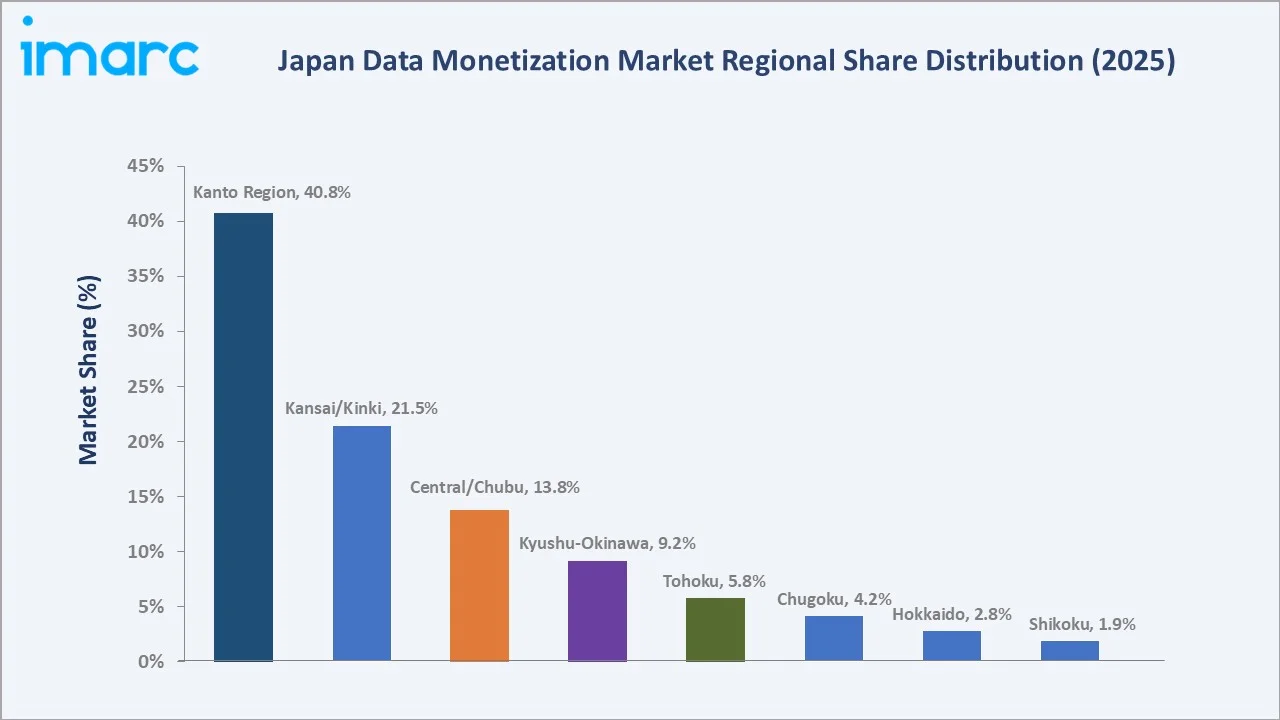

The Japan data monetization market size reached USD 257.95 Million in 2025 and is projected to reach USD 445.53 Million by 2034, growing at a CAGR of 6.26% during 2026-2034. Growing enterprise demand for AI-driven analytics platforms, accelerating digital transformation across key industries, and government-led data economy initiatives are the primary factors propelling the data monetization market growth in Japan.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 257.95 Million |

|

Forecast Market Size (2034) |

USD 445.53 Million |

|

CAGR (2026-2034) |

6.26% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (40.8% share, 2025) |

|

Fastest Growing Region |

Kansai/Kinki Region |

The Kanto region dominates, holding a 40.8% market share in 2025, supported by Tokyo's concentration of financial institutions, IT multinationals, and digital-native enterprises driving large-scale data asset commercialization initiatives. Large enterprises account for 64.5% of market revenue, while BFSI leads end-use demand at 26.4%.

Data monetization encompasses the strategies and technologies organizations deploy to generate measurable economic value from data assets, through direct data sales, analytics-driven product intelligence, or data-enhanced service delivery, creating new revenue streams and operational efficiencies across Japan's economy.

To get more information on this market, Request Sample

With adoption spanning BFSI, e-commerce, IT, manufacturing, healthcare, and energy, the Japan data monetization market is positioned for sustained expansion, supported by advancing AI and machine learning infrastructure, Japan's evolving data economy policy framework, and the proliferation of cross-industry data exchange platforms.

Executive Summary

The Japan data monetization market is on a consistent upward trajectory, driven by enterprise digital transformation mandates, AI platform proliferation, and a national policy environment increasingly supportive of open data and data-driven business models. The market reached USD 257.95 Million in 2025 and is forecast to reach USD 445.53 Million by 2034, reflecting a CAGR of 6.26% over the forecast period.

The Kanto region leads nationally at 40.8% revenue share in 2025, underpinned by Tokyo's unparalleled concentration of enterprise data producers and consumers across financial services, technology, and retail. Kansai/Kinki follows at 21.5%, while Central/Chubu accounts for 13.8%, driven by automotive and industrial data monetization use cases centered on Nagoya's manufacturing cluster.

Large Enterprises dominate at 64.5%, leveraging mature data infrastructure and dedicated data strategy functions, while BFSI commands the largest end-use share at 26.4%, monetizing transaction data, credit intelligence, and behavioral analytics across banking, insurance, and fintech verticals.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Organization Size) |

Large Enterprises – 64.5% share (2025) |

|

Largest Segment (End Use) |

BFSI – 26.4% share (2025) |

|

Leading Region |

Kanto Region – 40.8% revenue share (2025) |

|

Fastest Growing Region |

Kansai/Kinki Region (Osaka smart city + industrial data exchange growth) |

|

Top Companies |

NTT Data Corporation, Fujitsu Limited, NEC Corporation, Hitachi, Ltd. |

|

Market Opportunity |

SME-targeted analytics-as-a-service platforms projected at USD 95 Million by 2034 |

Key Analytical Observations Supporting the Above Data:

- Large enterprises account for 64.5% of the Japan data monetization market in 2025, leveraging established data governance frameworks, centralized data lakes, and dedicated data monetization strategy teams to commercialize operational data.

- BFSI leads end-use demand at 26.4% (2025), driven by banks, insurers, and fintech platforms monetizing transaction histories, credit behavior analytics, and real-time payment intelligence for internal risk management optimization, third-party data product sales, and regulatory intelligence services.

- The Kanto region holds 40.8% of the Japanese data monetization market in 2025, anchored by Tokyo's role as Japan's primary financial and technology hub, housing the highest density of data-rich enterprises across banking, e-commerce, and telecommunications.

- Kansai/Kinki is the fastest-growing regional market, with Osaka's Data Free Flow with Trust (DFFT) pilot programs, manufacturing data exchange initiatives, and smart city infrastructure investments generating new data monetization opportunities beyond the Kanto enterprise cluster.

- AI and advanced analytics integration is the primary technology driver differentiating competitive data monetization offerings in Japan, with vendors embedding predictive modelling, natural language querying, and automated insight generation into platform services to increase data product value and stickiness.

Japan Data Monetization Market Overview

Data monetization refers to the process by which organizations derive measurable economic value from data assets, either through direct data sales or through using data to optimize internal operations, enhance products, and improve decision-making. In Japan's context, data monetization encompasses Data as a Service (DaaS), Insight as a Service, Analytics-enabled Platform as a Service, and Embedded Analytics delivery models, which collectively transform raw organizational data into structured, commercially valuable intelligence products.

Japan's data monetization ecosystem spans data infrastructure providers (cloud platforms, data lakes), analytics software vendors, data marketplace operators, management consulting firms providing data strategy advisory, and corporate end users across all major industry verticals.

Japan's Society 5.0 national vision, which frames data as a foundational infrastructure for a human-centered, technology-integrated society, provides a powerful government-level mandate for data economy development. This policy backdrop, combined with the Ministry of Economy, Trade and Industry's (METI) data strategy frameworks and Japan's leadership in DFFT international data governance initiatives, creates a uniquely supportive institutional environment for enterprise data monetization investment.

Market Dynamics

To evaluate market opportunities, Request Sample

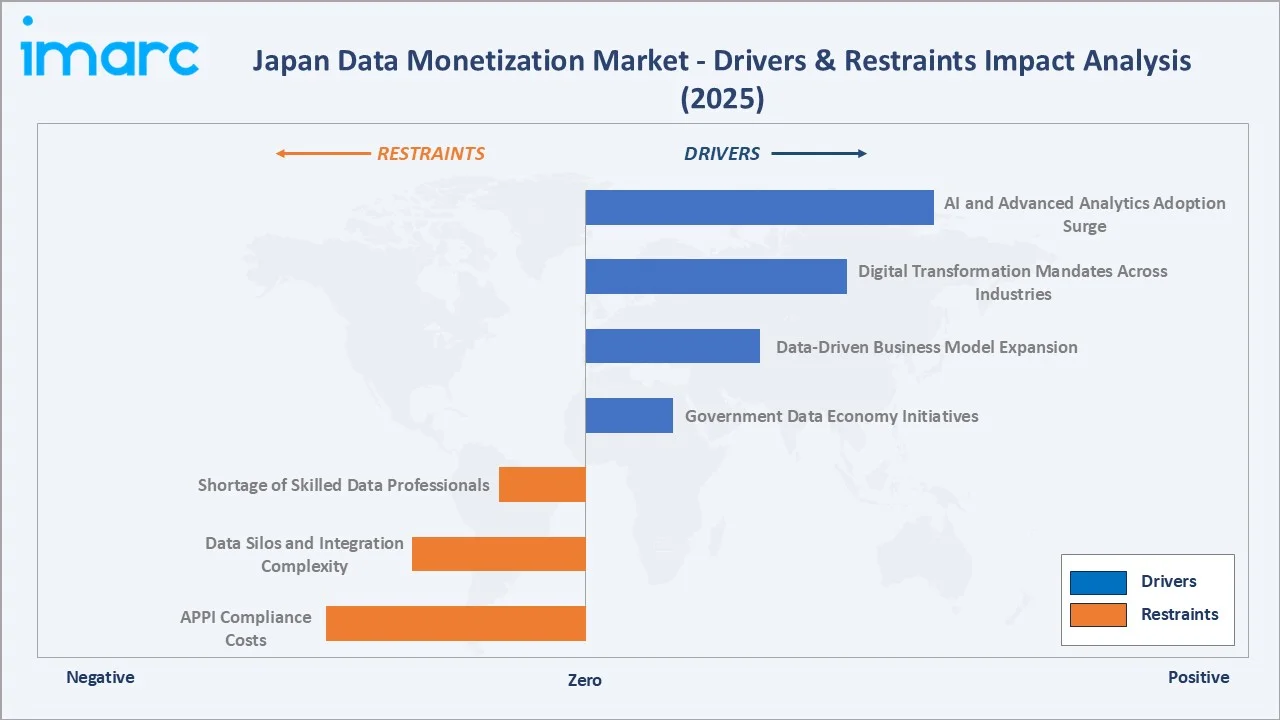

Market Drivers

- AI and Advanced Analytics Adoption Surge: Japan's AI investment reached approximately USD 8.9 Billion in 2024 and is expected to reach USD 27.9 Billion by 2029, with data analytics and insight generation platforms representing the single largest AI application category, directly expanding the commercial infrastructure underpinning data monetization strategies across BFSI, manufacturing, and retail.

- Digital Transformation Mandates Across Industries: Japan's DX (Digital Transformation) corporate mandate compels organizations to digitize operations and commercialize resulting data assets, creating a top-down organizational imperative for data monetization strategy development and platform investment.

- Data-Driven Business Model Expansion: The proliferation of subscription analytics products, API-based data services, and embedded intelligence platforms is enabling organizations across BFSI, e-commerce, and healthcare to build new data-native revenue streams.

- Government Data Economy Initiatives: Japan's METI data strategy, the Digital Agency's interoperability frameworks, and active participation in international DFFT governance are creating institutional infrastructure that lowers cross-organizational data sharing barriers.

These drivers create a compounding growth dynamic: DX mandates generate richer organizational data assets, AI investment creates tools to extract value from those assets, and government policy reduces friction in cross-organizational data exchange, collectively expanding market size from both supply and demand sides simultaneously.

Market Restraints

- APPI Compliance Costs: Japan's revised Act on Protection of Personal Information imposes detailed requirements on data handling, cross-border transfer, third-party sharing consent, and data breach notification that create significant legal compliance investment for organizations seeking to commercialize customer-linked data assets.

- Data Silos and Integration Complexity: Many Japanese large enterprises operate fragmented legacy IT architectures with data distributed across incompatible systems, requiring substantial data integration investment before monetization-ready data products can be developed and deployed commercially.

- Shortage of Skilled Data Professionals: By 2030, Japan is expected to face a shortage of up to 790,000 IT professionals, based on estimates from the country's Ministry of Economy, Trade and Industry (METI), constraining organizational capacity to execute data monetization strategies at scale.

Market Opportunities

- SME Data Monetization Platforms: Japan's over 3.36 million SMEs represent a largely untapped data monetization opportunity, with cloud-native, affordable DaaS and analytics platforms specifically designed for smaller data estates, potentially addressing an incremental USD 95 Million market opportunity by 2034.

- Cross-Industry Data Marketplace Development: B2B data exchange platforms enabling anonymized data sharing between non-competing industries, such as mobility data from manufacturers monetized by insurers, represent a structurally growing market segment aligned with Japan's DFFT policy framework.

- Embedded Analytics in SaaS Products: Integrating monetization-ready data analytics layers within existing enterprise SaaS platforms delivers data product value without requiring standalone customer investment, enabling faster adoption and lower sales friction across mid-market enterprise segments.

Market Challenges

- Cultural Reluctance to Share Proprietary Data: Japan's corporate culture of data confidentiality and competitive information protection creates organizational resistance to external data monetization initiatives, requiring significant internal governance and culture change management investment before data commercialization programs can launch.

- Regulatory Complexity Across Data Categories: Different data types in Japan are governed by distinct and evolving regulatory frameworks, creating complex compliance landscapes for organizations seeking to monetize multi-source data assets across industry verticals.

Emerging Market Trends

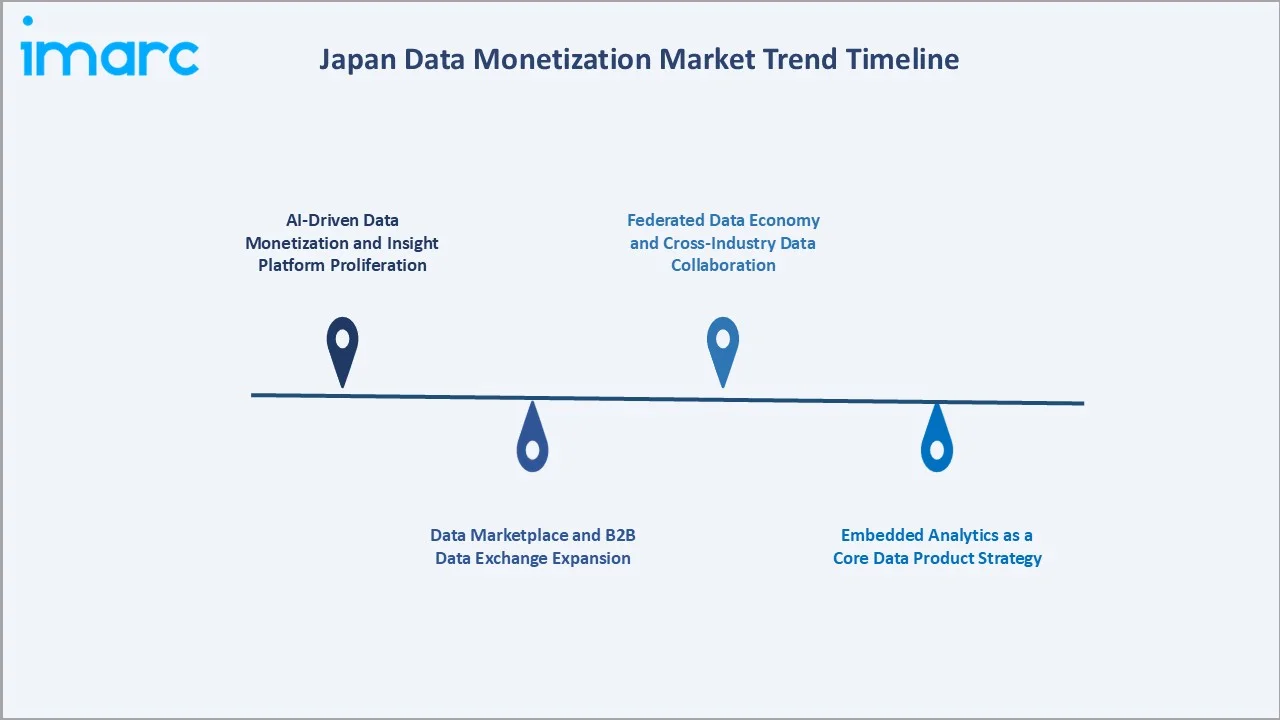

1. AI-Driven Data Monetization and Insight Platform Proliferation

Japan's leading DaaS providers embedded generative AI query interfaces in their analytics platforms from 2024, enabling non-technical business users to generate actionable insights from complex data assets without specialist data science resources, substantially expanding internal monetization use cases.

2. Data Marketplace and B2B Data Exchange Expansion

METI's promotion of the Integrated Innovation Strategy 2025 has catalyzed investment in data broker infrastructure, API standardization, and trust frameworks enabling enterprises to sell data assets to verified B2B buyers without compromising competitive or regulatory sensitivities.

3. Embedded Analytics as a Core Data Product Strategy

Japanese SaaS vendors and enterprise software providers are increasingly differentiating through embedded analytics, integrating intelligence layers within core business applications that expose monetization-ready insights to end users within existing workflow contexts. This embedded approach lowers customer adoption barriers, increases product stickiness, and enables vendors to introduce analytics-premium subscription.

4. Federated Data Economy and Cross-Industry Data Collaboration

Federated data architectures enabling secure, privacy-preserving cross-organizational data collaboration are gaining adoption in Japan's healthcare, manufacturing, and financial services sectors. Federated learning frameworks allow multiple organizations to collectively train analytics models on combined data without sharing raw data.

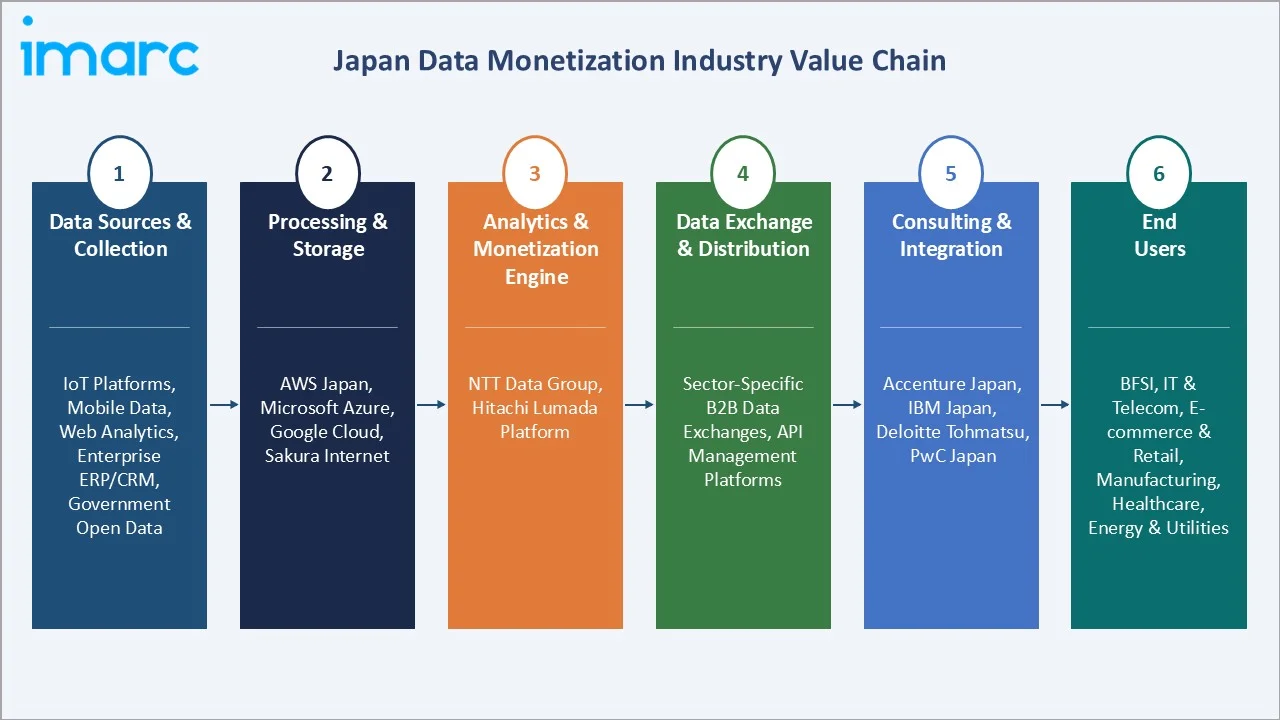

Industry Value Chain Analysis

The Japan data monetization value chain spans data generation and collection infrastructure through end-user consumption and ROI realization, with each stage populated by specialized operators whose capabilities directly determine the quality, compliance, and commercial viability of data products.

|

Stage |

Key Players / Examples |

|

Data Sources & Collection |

IoT platforms, mobile data, web analytics, enterprise ERP/CRM, government open data |

|

Processing & Storage |

AWS Japan, Microsoft Azure, Google Cloud, Sakura Internet |

|

Analytics & Monetization Engine |

NTT Data Group, Hitachi Lumada Platform |

|

Data Exchange & Distribution |

Sector-specific B2B data exchanges, API management platforms |

|

Consulting & Integration |

Accenture Japan, IBM Japan, Deloitte Tohmatsu, PwC Japan |

|

End Users |

BFSI, IT & Telecom, E-commerce & Retail, Manufacturing, Healthcare, Energy & Utilities |

Technology Landscape in the Japan Data Monetization Industry

AI and Machine Learning Analytics Platforms

Fujitsu's Zinrai AI platform, NEC's AI portfolio, and Hitachi's Lumada IoT platform represent flagship domestic AI-data monetization integrations, supplemented by global cloud AI services from AWS, Azure, and Google Cloud Japan serving multinational enterprise buyers.

Cloud Data Infrastructure and Data Lake Architecture

Japan's major cloud providers offer dedicated data compliance configurations aligned with APPI requirements, enabling organizations to build monetization-ready data products within Japan's data residency framework without compromising regulatory standing.

Data Marketplace and API Management Technology

API-first data marketplace platforms enabling authenticated, usage-metered B2B data product sales are gaining traction in Japan's financial services, mobility, and healthcare sectors. These platforms provide the commercial infrastructure required to operate data products as commercial-grade digital services with defined SLAs and compliance guarantees.

Privacy-Enhancing Technologies (PETs) and Compliance Automation

Differential privacy, synthetic data generation, and homomorphic encryption technologies are enabling Japanese organizations to monetize data assets that would otherwise be restricted by APPI consent or competitive sensitivity constraints. PET integration within data monetization pipelines is becoming a competitive differentiator for enterprise DaaS vendors serving healthcare, financial services, and public sector buyers with heightened data protection obligations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Method |

🔒 |

🔒 |

2025 |

|

Organization Size |

Large Enterprises |

64.5% |

2025 |

|

End Use |

BFSI |

26.4% |

2025 |

|

Region |

Kanto Region |

40.8% |

2025 |

By Organization Size

Large Enterprises dominate the organization size segment with a 64.5% share in 2025. Japan's large enterprises, including leading banks, telecommunications carriers, automotive manufacturers, and retail conglomerates, possess the data volume, governance maturity, and financial resources to execute structured data monetization strategies encompassing dedicated data product teams, enterprise data marketplace participation, and external DaaS offerings.

To access detailed market analysis, Request Sample

Small and medium-sized enterprises account for 35.5%, representing a growing adoption cohort as affordable cloud-based analytics platforms and no-code data product tools lower the technical and capital barriers to data commercialization.

By End Use

BFSI leads end-use demand at 26.4% in 2025, driven by banks, insurers, securities firms, and fintech platforms that operate Japan's richest per-customer data assets. BFSI organizations monetize transactional behavior data, credit intelligence, fraud pattern analytics, and market sentiment signals through DaaS products sold to regulated third parties.

IT and Telecommunications follows at 22.8%, leveraging network usage data, mobility intelligence, and connectivity behavior analytics. E-commerce and retail account for 18.5%, driven by purchase behavior, supply chain, and customer journey data products.

Regional Market Insights

Kanto Region's market leadership (40.8%, 2025) is anchored by Tokyo's structural position as Japan's primary data economy hub, home to Japan's largest banks, e-commerce platforms, telecommunications carriers, and technology companies, all of which generate, consume, and commercially exchange data products at the highest per-capita intensity in the country.

|

Region |

Share |

Key Growth Drivers |

Major Industries |

Data Monetization Focus |

|

Kanto Region |

40.8% |

Financial hub, IT concentration, e-commerce density |

BFSI, IT & Telecom, E-commerce |

DaaS, Embedded Analytics, Insight APIs |

|

Kansai/Kinki |

21.5% |

DFFT pilot programs, industrial data exchange, Osaka Expo legacy |

Manufacturing, Pharma, Retail |

B2B Data Marketplaces, PaaS Analytics |

|

Central/Chubu |

13.8% |

Automotive IoT data, manufacturing intelligence |

Automotive, Electronics, Manufacturing |

Industrial IoT Monetization, Connected Vehicle Data |

|

Kyushu-Okinawa |

9.2% |

Semiconductor data, tourism analytics, and data center growth |

Semiconductor, Tourism, IT |

Operational Intelligence, Edge Data Products |

|

Tohoku |

5.8% |

Agriculture data monetization, reconstruction analytics |

Agriculture, Public Sector |

Open Data Products, Agri-Intelligence |

|

Chugoku |

4.2% |

Port logistics data, steel/chemical operational analytics |

Logistics, Manufacturing, Chemicals |

Supply Chain Data Products, Industrial Analytics |

|

Hokkaido |

2.8% |

Food & agri data, tourism intelligence, data center expansion |

Agriculture, Tourism, Data Infra |

Agricultural Data Exchange, Climate Analytics |

|

Shikoku |

1.9% |

Regional SME digitalization, public sector data sharing |

SMEs, Public Sector |

SME Data Products, Open Government Data |

Kansai/Kinki is the fastest-growing regional market, with Osaka's designation as Japan's DFFT pilot region enabling cross-border and cross-industry data flow experiments that are generating new data monetization use cases in pharmaceutical, logistics, and smart city domains.

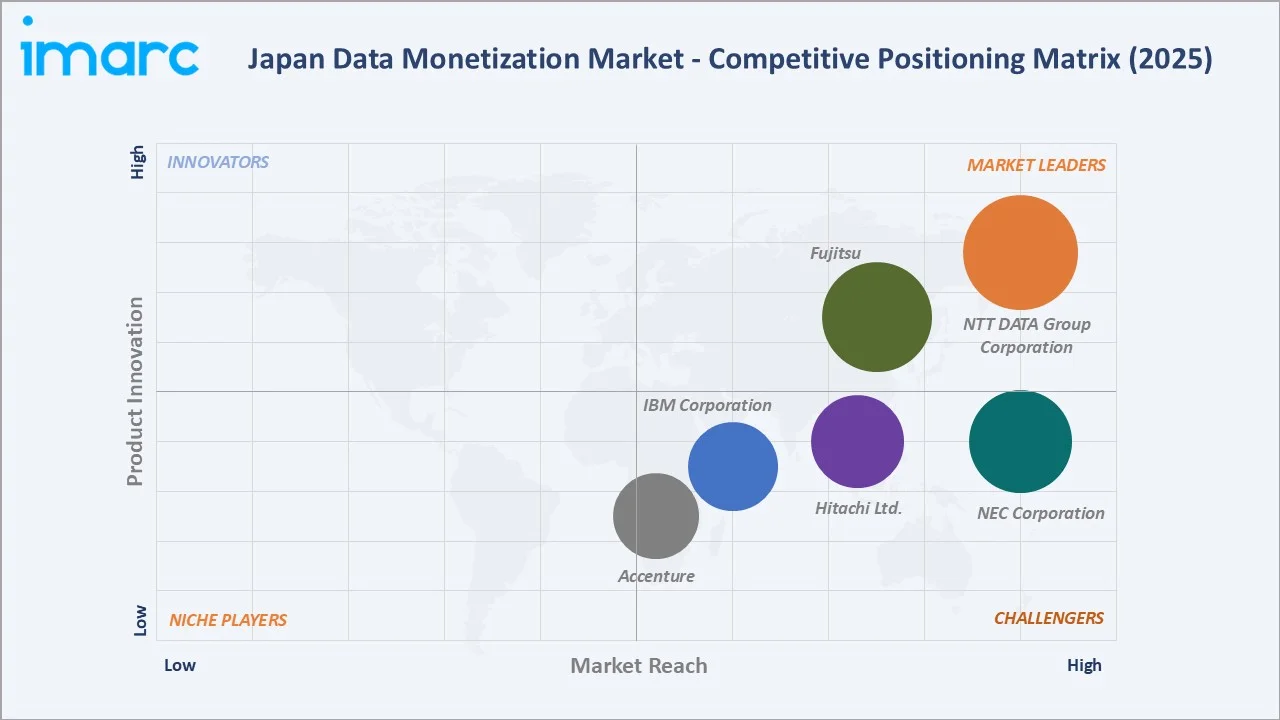

Competitive Landscape

The Japan data monetization market exhibits a moderately concentrated competitive structure dominated by Japan's major IT services conglomerates, which leverage existing enterprise relationships, deep industry vertical expertise, and integrated data infrastructure capabilities to deliver end-to-end data monetization platform solutions.

|

Company Name |

Platform/Brand |

Market Position |

Core Strength |

|

NTT DATA Group Corporation |

GenAI TechHub accelerator |

Market Leader |

Largest Japanese IT services group; enterprise DaaS platform across all verticals |

|

Fujitsu |

Fujitsu Uvance / Fujitsu Kozuchi |

Market Leader |

Japan's largest tech company, an AI-powered insight monetization platform |

|

NEC Corporation |

NEC Advanced Analytics Platform (AAPF) |

Strong Challenger |

AI and biometrics data products; government and public sector data monetization |

|

Hitachi, Ltd. |

Lumada (Lumada 3.0) |

Strong Challenger |

IoT and industrial data monetization; OT/IT convergence analytics leadership |

|

IBM Corporation |

IBM Cloud Pak for Data |

Challenger |

Enterprise data fabric; AI-embedded data product development for BFSI and healthcare |

|

Accenture |

Data & AI Services |

Challenger |

Strategy-to-implementation data monetization consulting; cross-industry data exchange design |

NTT DATA Group Corporation, Fujitsu, NEC Corporation, and Hitachi, Ltd. collectively account for approximately 55–60% of market revenue in 2025, supplemented by international management consulting firms and global cloud providers operating specialized data monetization practices.

Key Company Profiles

NTT DATA Group Corporation

NTT DATA Group Corporation, headquartered in Tokyo and operating as the IT services arm of the NTT Group, is Japan's largest domestic IT services company and the primary market leader in enterprise data monetization platform deployment across BFSI, government, healthcare, and telecommunications sectors.

- Service Portfolio: GenAI TechHub, the Ouranos Ecosystem data-space platform, and tsuzumi LLM.

- Recent Developments: In April 2025, the company successfully demonstrated interoperability between Japan’s Battery Traceability Platform and the Catena‑X network, marking a key milestone in cross‑industry digital integration under a government‑led initiative.

- Strategic Focus: AI-native DaaS platform scaling; cross-industry data marketplace expansion; global enterprise data monetization consulting growth.

Fujitsu

Fujitsu, headquartered in Kanagawa, is one of Japan's largest technology companies by revenue and a pioneer in AI-driven data product development, deploying its Kozuchi and Uvance sustainable transformation framework across Japan's largest enterprise customers.

- Service Portfolio: Fujitsu Data Intelligence PaaS, Fujitsu Kozuchi, Industry-specific Insight APIs, Hybrid Cloud Data Platform.

- Recent Developments: In February 2024, Fujitsu unveiled a strengthened AI strategy centered around its Fujitsu Data Intelligence PaaS platform, aimed at enhancing data integration and generative AI capabilities across the enterprise.

- Strategic Focus: Uvance platform ecosystem expansion; AI data monetization for manufacturing and healthcare; sustainability data product development.

NEC Corporation

NEC Corporation, headquartered in Tokyo, is a global technology leader with deep expertise in AI, biometrics, and public safety analytics, deploying data monetization solutions primarily across government, public safety, telecommunications, and financial services verticals.

- Service Portfolio: NEC Advanced Analytics Platform (AAPF), AI Facial Recognition Analytics, Telecom Data Intelligence Services, Government Open Data Products.

- Recent Developments: In February 2026, NEC Corporation demonstrated an Agentic AI–driven autonomous network operation technology in collaboration with AWS that can automatically manage the full lifecycle of a 5G/6G network User Plane Function (UPF).

- Strategic Focus: Biometric and behavioral data monetization; smart city intelligence products; government data marketplace participation.

Market Concentration Analysis

The Japan data monetization market exhibits moderate concentration at the platform and advisory services level, with the top four domestic IT conglomerates, NTT DATA Group Corporation, Fujitsu, NEC Corporation, and Hitachi, Ltd., collectively controlling approximately 55–60% of professional services and managed platform revenue in 2025.

The broader market is considerably more fragmented across specialized data product vendors, industry-specific data marketplace operators, and international cloud analytics providers, collectively serving a diverse long tail of enterprise and mid-market buyers with varied data monetization objectives and budgets.

Consolidation is accelerating, driven by the economics of AI platform investment that favor scale operators capable of amortizing model development costs across large enterprise customer portfolios. Private equity investment in data infrastructure and marketplace platforms is also increasing, targeting companies with proprietary data assets, API-first architectures, and demonstrable B2B data exchange revenue streams.

Investment & Growth Opportunities

Fastest Growing Segments

AI-embedded Insight-as-a-Service platforms (estimated CAGR 8.5% through 2034), industrial IoT data monetization solutions for manufacturing (7.8% CAGR), and SME-targeted analytics-as-a-service offerings (7.5% CAGR) represent the three highest-growth investment vectors within the Japan data monetization market, addressing a combined incremental opportunity of approximately USD 95 Million by 2034.

Emerging Opportunities

Japan's DFFT-aligned cross-border data exchange infrastructure represents an emerging high-value opportunity, enabling organizations to commercialize anonymized data assets internationally within trusted data governance frameworks. Healthcare data monetization, leveraging Japan's aging population's rich longitudinal health datasets for pharmaceutical R&D, insurance analytics, and public health intelligence, represents a structurally growing segment with strong institutional demand and evolving regulatory enablement.

Venture and Institutional Investment Trends

- Japan's data economy startup ecosystem attracted over USD 680 Million in venture funding between 2022 and 2025, with data marketplace platforms, synthetic data vendors, and privacy-enhancing technology providers representing the most active funding categories.

- Corporate venture arms of NTT, Fujitsu, and Hitachi are actively co-investing in data monetization infrastructure startups to accelerate platform ecosystem expansion beyond organic development timelines.

Future Market Outlook (2026-2034)

The Japan data monetization market is positioned for sustained, broad-based growth through 2034. From a base of USD 257.95 Million in 2025, the market is projected to reach USD 445.53 Million by 2034, representing cumulative incremental value creation of USD 187.58 Million at a CAGR of 6.26%.

Regulatory evolution will progressively lower data sharing barriers while maintaining consent and privacy standards, expanding the addressable market for legitimate data monetization across healthcare, financial services, and government sectors. Vendors delivering APPI-native compliance automation, Japanese-language AI analytics, and seamless integration with Japan's domestic IT ecosystem will capture disproportionate market share in the forecast period.

Long-term, Japan's data monetization market trajectory converges with three structural forces: the demographic-driven urgency to maximize productivity from every organizational resource, including data, the international competitiveness imperative to build AI-ready data infrastructure at scale, and the government's strategic commitment to positioning Japan as a global leader in trusted, high-value data economy development.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 95 industry participants in 2024–2025, including data platform vendors, management consulting firms, corporate chief data officers, IT procurement managers, and data economy policy advisors across Japan's major industry verticals and regional markets.

Secondary Research

Secondary research encompassed a systematic review of vendor annual reports, METI data economy policy documents, Digital Agency strategic publications, Japan IT Market Research (ITR) databases, Nikkei corporate financial data, trade publications including IT Leaders and CIO Online Japan, and international data economy benchmarking studies.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting, incorporating Japan's enterprise IT spend growth trajectories, data platform adoption rates by industry vertical, AI investment acceleration data, and regional corporate digital maturity indices. A base-case CAGR of 6.26% reflects consensus estimates validated against major vendor-reported ARR growth and analyst consensus data from ITR and IDC Japan.

Japan Data Monetization Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Methods Covered | Data as a Service, Insight as a Service, Analytics-enabled Platform as a Service, Embedded Analytics |

| Organization Sizes Covered | Large Enterprises, Small and Medium-sized Enterprises |

| End Uses Covered | BFSI, E-commerce and Retail, IT and Telecommunications, Manufacturing, Healthcare, Energy and Utilities, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | NTT DATA Group Corporation, Fujitsu, NEC Corporation, Hitachi, Ltd., IBM Corporation, Accenture, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan data monetization market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan data monetization market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan data monetization industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Data Monetization Market Report

The Japan data monetization market reached USD 257.95 Million in 2025. It is projected to reach USD 445.53 Million by 2034.

The Japan data monetization market is expected to grow at a CAGR of 6.26% during the forecast period from 2026 to 2034, supported by AI platform adoption, enterprise DX mandates, and government data economy initiatives.

Kanto region leads the market with a 40.8% revenue share in 2025, driven by Tokyo's concentration of data-rich enterprises across BFSI, IT, e-commerce, and telecommunications verticals.

Large enterprises dominate with a 64.5% share in 2025, leveraging mature data governance infrastructure, dedicated data strategy resources, and enterprise-grade monetization platform investments.

BFSI holds the largest end-use share at 26.4% in 2025, driven by the high commercial value of transaction, credit, and behavioral data assets across banking, insurance, and fintech organizations.

Key players include NTT DATA Group Corporation, Fujitsu, NEC Corporation, Hitachi, Ltd., IBM Corporation, and Accenture.

AI is the primary technology multiplier in Japan's data monetization landscape, enabling organizations to transform raw data into commercially valuable predictive intelligence products, embedded analytics services, and automated insight APIs that generate new revenue streams from existing data assets with reduced specialist resource requirements.

Key challenges include APPI compliance costs for customer data commercialization, data silo integration complexity in legacy enterprise IT architectures, a structural shortage of data science and data product management talent, and cultural reluctance to share proprietary data externally in Japan's competitive business environment.

Significant opportunities exist in AI-embedded insight platform development, SME-targeted analytics-as-a-service products, industrial IoT data monetization for manufacturing, DFFT-aligned cross-border data exchange infrastructure, and healthcare data monetization for pharmaceutical and insurance analytics.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade