Japan Digital Health Market Size, Share, Trends and Forecast by Type, Component, and Region, 2026-2034

Japan Digital Health Market Size, Share, Trends & Forecast (2026-2034)

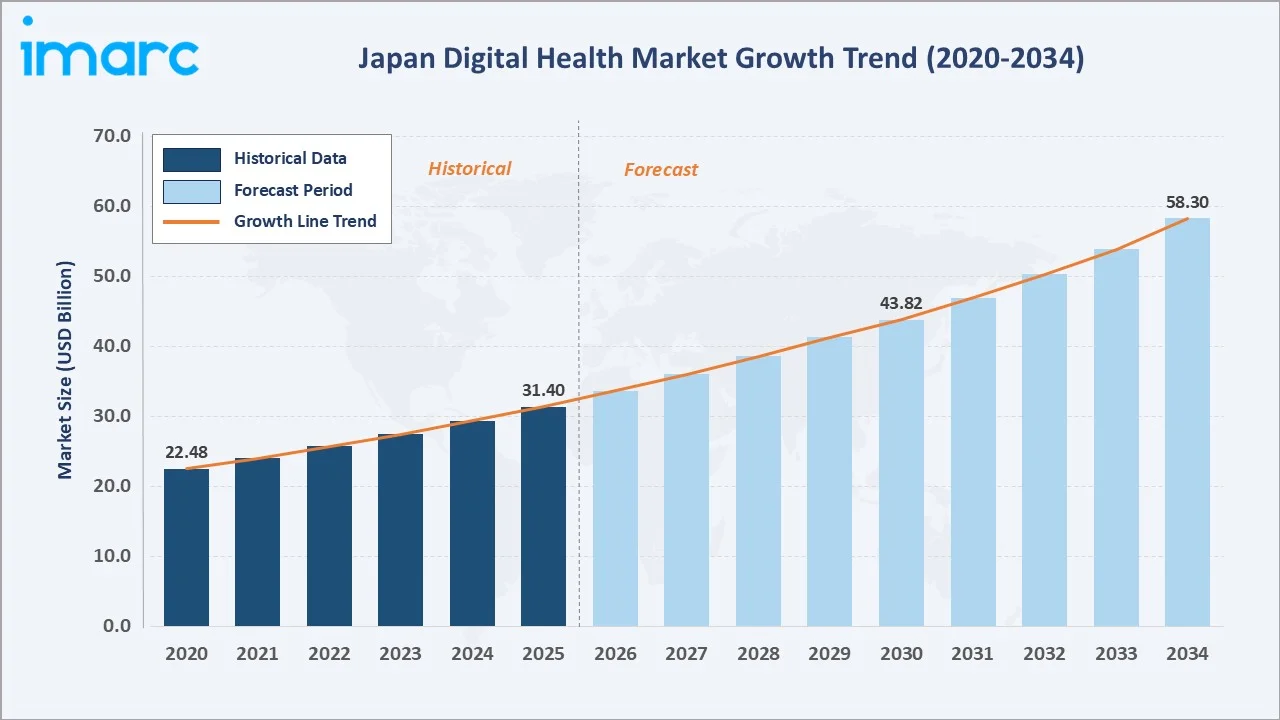

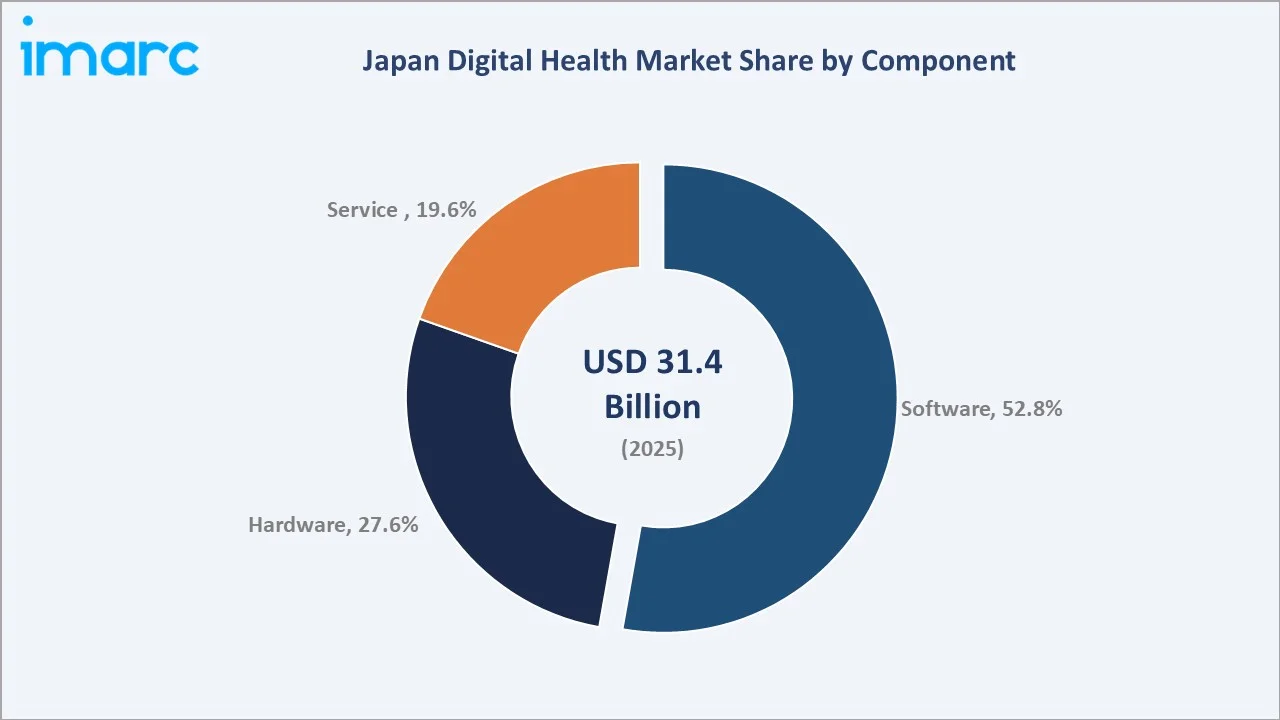

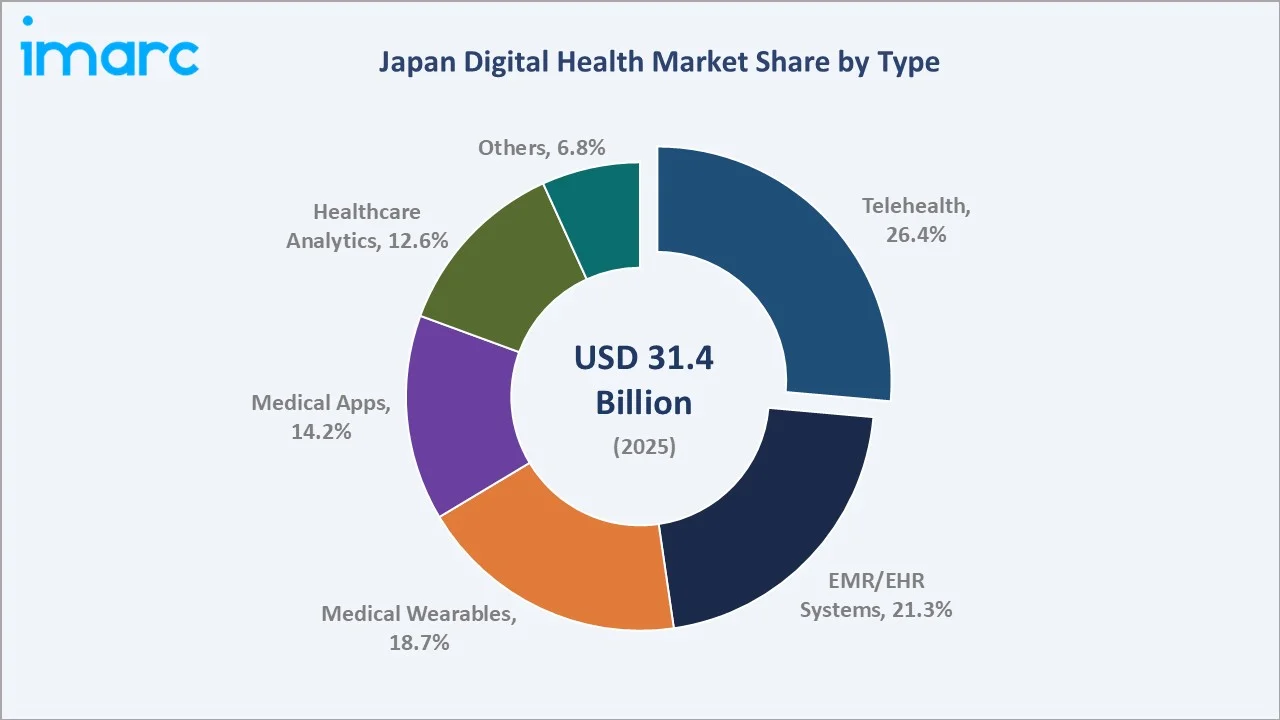

The Japan digital health market size was valued at USD 31.4 Billion in 2025 and is projected to reach USD 58.3 Billion by 2034, exhibiting a CAGR of 6.9% during the forecast period 2026-2034. The market is fueled by a super-aged population alongside robust government Medical DX mandates and surging adoption of telehealth, AI diagnostics, and EMR/EHR platforms. Software dominates by component at 52.8% in 2025, while Telehealth is the leading type segment at 26.4%. The Kanto Region commands the largest regional share at 38.5%, anchored by Tokyo's concentration of hospitals, digital health ventures, and public sector DX investment.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 31.4 Billion |

|

Forecast Market Size (2034) |

USD 58.3 Billion |

|

CAGR (2026-2034) |

6.9% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (38.5% share, 2025) |

|

Leading Component |

Software (52.8% share, 2025) |

|

Largest Type Segment |

Telehealth (26.4% share, 2025) |

To get more information on this market, Request Sample

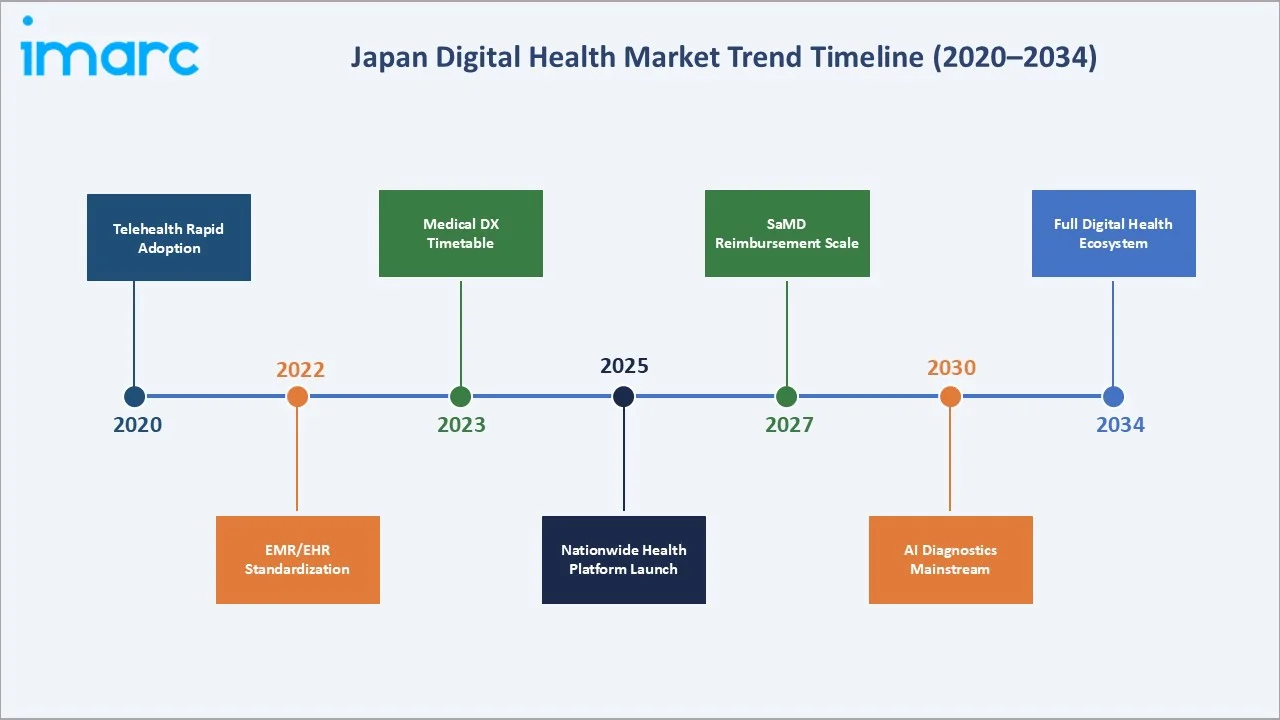

The Japan digital health market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast growth curve powered by government Medical DX mandates, aging population dynamics, and AI-driven clinical adoption, is depicted below.

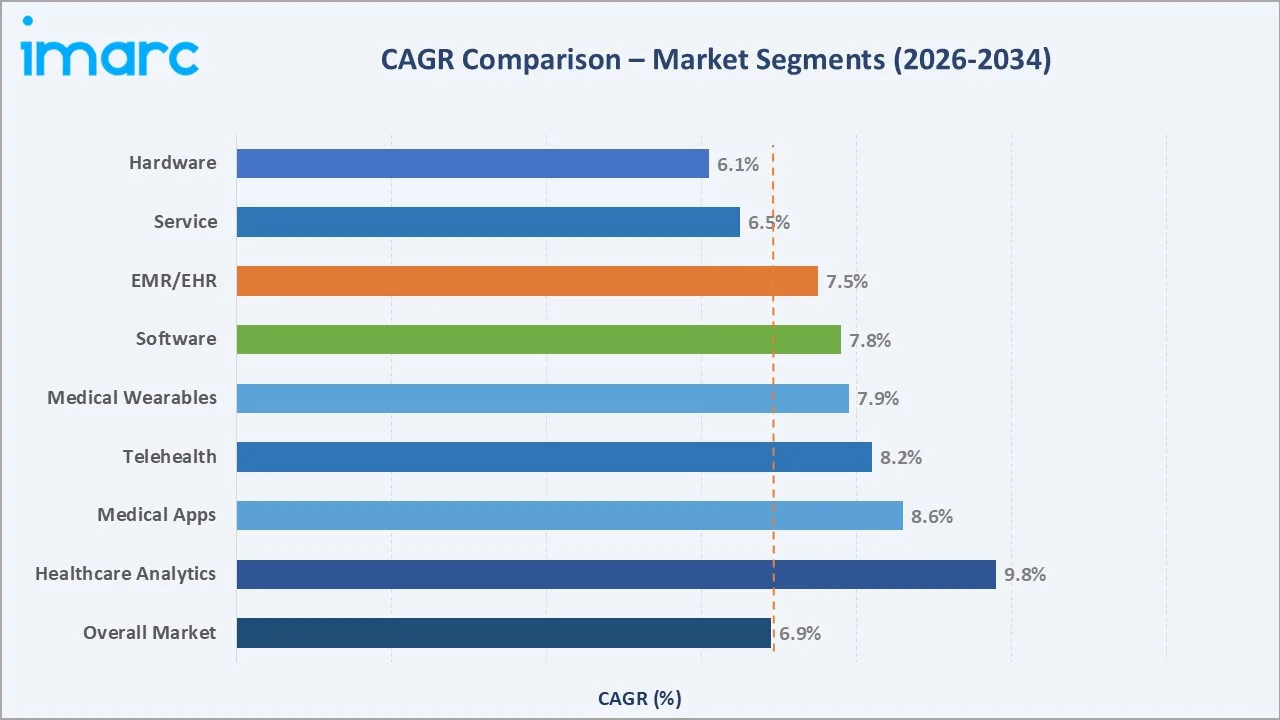

Segment-level CAGR comparisons highlighting Healthcare Analytics and Telehealth as the two fastest-growing type sub-categories within the Japan digital health market during the 2026-2034 forecast period are shown below.

Executive Summary

Japan's digital health market is undergoing a structural transformation driven by the convergence of demographic imperatives, government policy mandates, and accelerating technology adoption. The nation's super-aged society is generating unprecedented demand for scalable, remote, and AI-augmented healthcare solutions.

Software solutions captured 52.8% of market revenue in 2025, reflecting strong enterprise adoption of EMR/EHR platforms, hospital management systems, and AI diagnostics tools. Telehealth emerged as the dominant type segment at 26.4% in 2025 following MHLW regulatory liberalization of first-visit online consultations. EMR/EHR Systems held 21.3% in 2025, driven by the Nationwide Medical Information Platform mandate. Medical Wearables at 18.7% are supported by OMRON's dominant healthcare device portfolio and Google's Suica-integrated Fitbit tracker launched in August 2025.

Geographically, the Kanto Region commands 38.5% of national market share in 2025, hosting the highest concentration of digital health start-ups, academic medical centers, and government DX investment pools. The market outlook is strongly positive, with a CAGR of 6.9% projected through 2034 as digital therapeutics gain reimbursement pathways, 5G rural coverage matures, and AI diagnostics achieve clinical validation in major imaging modalities.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Component) |

Software - 52.8% share (2025) |

|

Leading Type Segment |

Telehealth - 26.4% share (2025) |

|

Second Largest Type Segment |

EMR/EHR Systems - 21.3% share (2025) |

|

Leading Region |

Kanto Region - 38.5% revenue share (2025) |

|

Top Companies |

OMRON Corp., CureApp, LINE Healthcare, Ubie, M3 Inc. |

Key analytical observations supporting the data points above:

- Software's 52.8% dominance in 2025 reflects the rapid rollout of cloud-based EMR/EHR platforms under Japan's Medical DX agenda, with over 80% of acute-care hospitals targeted for full digitization by 2026 under the Nationwide Medical Information Platform.

- Telehealth commands 26.4% of type share in 2025, driven by MHLW regulatory amendments enabling first-visit online consultations, and the ubiquity of LINE Doctor across 95+ million active LINE users in Japan, with online consultation visits exceeding 12 million in FY2024.

- EMR/EHR Systems at 21.3% in 2025 reflect mandatory adoption of standardized electronic records, with AWS Japan selected in September 2025 to host parts of Japan's government health cloud infrastructure.

- Kanto Region's 38.5% dominance in 2025 is reinforced by Tokyo Metropolitan Government's JPY 50 Billion Digital Innovation Fund (2024-2028) and the production of 40+ digital health start-ups receiving Series A or above funding in 2024.

- Healthcare Analytics is positioned as the fastest-growing type sub-segment, driven by AI adoption and the national health data lake emerging from the Nationwide Medical Information Platform, with Ubie's AI symptom checker deployed across 3,000+ Japanese clinics as of 2025.

- Medical Wearables at 18.7% reflect strong OMRON healthcare device penetration across primary care and the August 2025 Fitbit/Google Suica-compatible health tracker launch, integrating health monitoring with Japan's dominant transit payment system.

Japan Digital Health Market Overview

Digital health in Japan integrates software, connected devices, telemedicine, and AI analytics into healthcare delivery, patient management, and wellness. The ecosystem includes EMR/EHR platforms, mHealth apps, clinical dashboards, wearables, smart diagnostic tools, remote monitoring kits, telehealth services, and data management consulting.

Key applications cover primary care, chronic disease management, mental health, preventive wellness, post-operative monitoring, and elderly care. Growth drivers include Japan’s aging population, public-private Medical DX investments under Society 5.0, and a near-universal health insurance system enabling reimbursable digital therapeutics and telehealth. Government agencies—MHLW, PMDA, METI, and the Digital Agency—coordinate the national healthcare digitization roadmap through 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

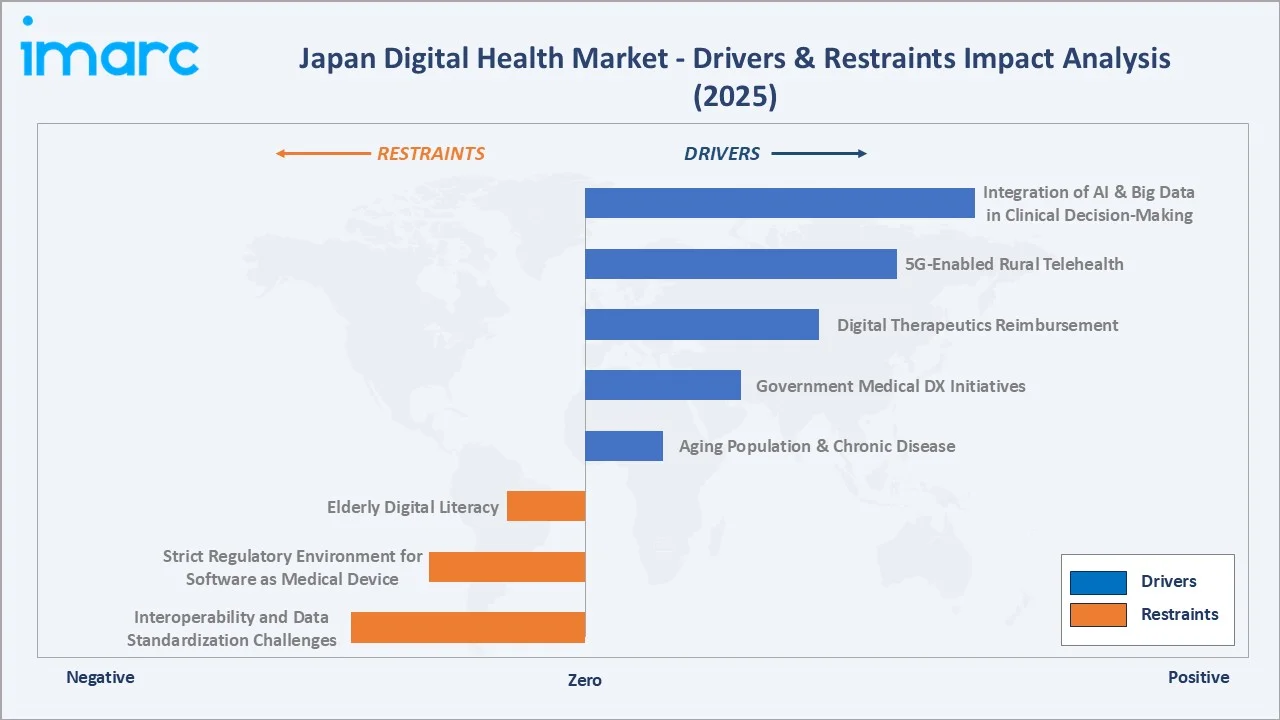

Market Drivers

- Aging Population & Chronic Disease: Japan’s rapidly aging population is driving strong demand for remote patient monitoring, telehealth, and AI-powered elder care, while chronic conditions like diabetes create a growing market for digital therapeutics and EMR-integrated care solutions.

- Government Medical DX Initiatives: Japan’s Medical DX policies and nationwide EMR platform are removing barriers to online consultations and standardizing medical data, laying the foundation for a connected digital health ecosystem.

Market Restraints

- Interoperability and Data Standardization Challenges: Despite government mandates, Japan's healthcare IT landscape remains fragmented. Legacy hospital systems operate on proprietary data formats, limiting seamless data exchange.

- Strict Regulatory Environment for Software as Medical Device: Japan's PMDA applies rigorous clinical evidence requirements to SaMD approvals, extending go-to-market timelines. CureApp's alcohol addiction app received approval only in February 2025, underscoring the lengthy development-to-market cycle. Post-approval reimbursement negotiation adds further delay before commercial scale.

Market Opportunities

- Digital Therapeutics Reimbursement: Japan offers clear regulatory and reimbursement pathways for digital therapeutics (SaMD), supporting approved apps for chronic conditions and behavioral health under national insurance.

- 5G-Enabled Rural Telehealth: Expansion of 5G networks by NTT and KDDI enables high-quality remote consultations and diagnostics, improving healthcare access in rural and underserved regions.

Market Challenges

- Elderly Digital Literacy: Low smartphone and app adoption among Japan’s oldest adults limits digital health uptake, requiring user-friendly designs and offline-integrated care.

- Healthcare Workforce Resistance: Many physicians remain cautious of AI-assisted workflows due to liability and accuracy concerns, slowing adoption in traditional hospital networks.

Emerging Market Trends

1. AI-Powered Diagnostics and Symptom Pre-Screening at Scale

AI‑driven platforms like Ubie’s AI symptom checker are being adopted by healthcare providers in Japan to support patient triage and workflow efficiency, reflecting broader uptake of AI in clinical settings. Ubie has been highlighted internationally for its AI symptom checker tool used by clinics.

2. Digital Therapeutics as a Mainstream Clinical Treatment Modality

Japan’s regulatory framework for digital therapeutics (SaMD) has enabled market entry and reimbursement for treatment apps such as CureApp’s therapeutic apps, and recent approvals include an ADHD‑focused digital therapeutic licensed to Shionogi.

3. Nationwide EMR Standardization and Cloud Infrastructure Buildout

Japan’s Nationwide Healthcare Information Platform aims to integrate EMRs, vaccination histories, electronic prescriptions, and other core health data into a unified, interoperable network to support clinical information exchange across institutions.

4. Consumer Platform Integration as Telehealth Access Layer

Telehealth services embedded in mass‑market consumer platforms (e.g., LINE Healthcare/LINE Doctor) leverage Japan’s existing digital communication channels to lower barriers to virtual care adoption.

5. Wearable Health Devices Integrating With Daily Life Infrastructure

Wearable health devices are increasingly integrating with consumer infrastructure and daily life, helping embed monitoring into routine behaviours and broadening the reach of digital health engagement, particularly among working‑age adults.

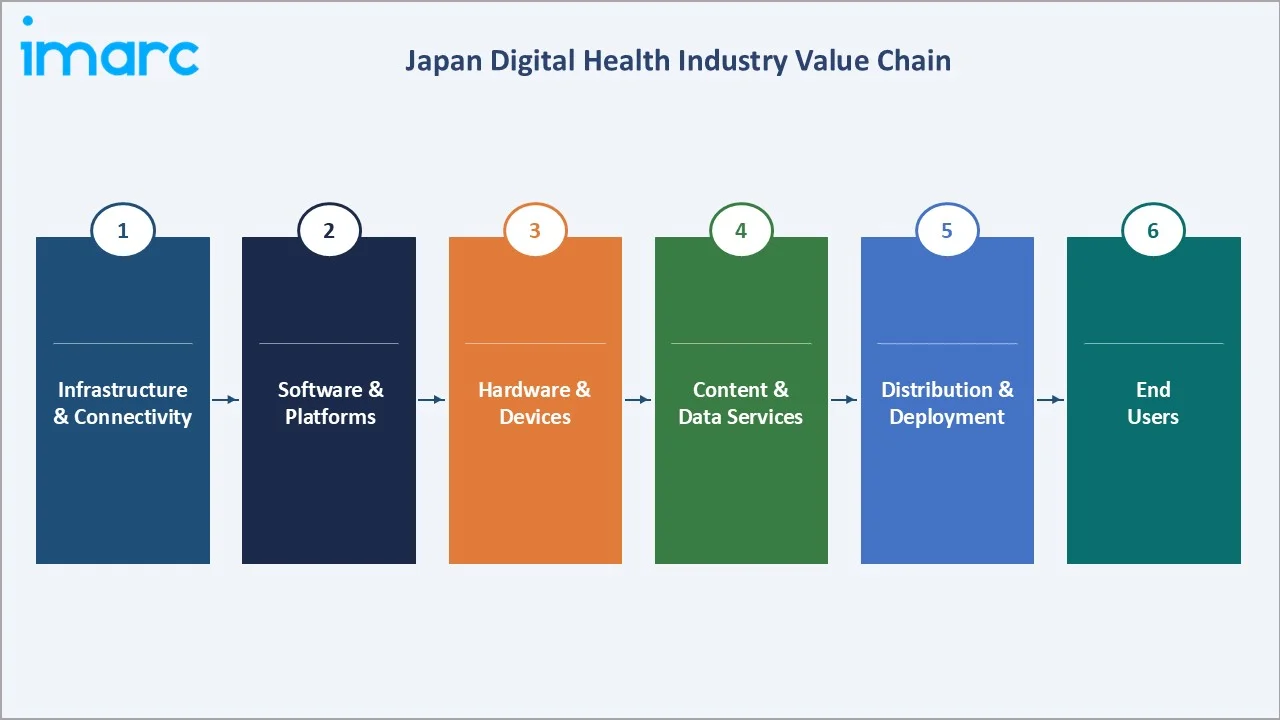

Industry Value Chain Analysis

The Japan digital health value chain spans six integrated stages from telecommunications infrastructure through end-user care delivery. Each stage involves distinct players with specialized competencies, and the structure is rapidly evolving under cloud migration pressure and government interoperability mandates.

|

Stage |

Key Players / Examples |

|

Infrastructure & Connectivity |

NTT Docomo, KDDI, SoftBank (5G), AWS Japan, Microsoft Azure Healthcare |

|

Software & Platform Development |

NEC Corp., NTT Data, CureApp, Ubie, LINE Healthcare, M3 Inc. |

|

Hardware & Device Manufacturing |

OMRON Corp., Sony, Murata Manufacturing, Hitachi |

|

Content & Data Services |

Allm Inc., HealthNode, Dai-ichi Life Holdings, Shionogi DTx |

|

Distribution & Deployment |

Hospitals, Clinics, National Health Insurance Network, Pharmacies |

|

End Users |

Patients, Elderly Care Recipients, Corporate Wellness Programs, Clinicians |

Platform developers and SaMD companies occupy the highest strategic value positions, as software margins and recurring subscription models generate superior economics compared to hardware manufacturing. The shift toward cloud-native architectures and government-mandated interoperability is reshaping the distribution layer, with established hospital management system vendors being disrupted by agile health-tech ventures including Ubie, CureApp, and LINE Healthcare.

Technology Landscape in Japan's Digital Health Industry

Artificial Intelligence and Machine Learning in Clinical Diagnostics

AI and ML are the foundational technology layer for Japan's next-generation digital health platforms. Applications span diagnostic imaging analysis (CT, MRI, fundus photography), natural language processing for clinical documentation, predictive analytics for hospital readmission risk, and real-time anomaly detection in wearable sensor streams. Japan is advancing AI-driven healthcare through AMED-led funding programs supporting diagnostics, medical devices, and data infrastructure, though total AI-specific investment is not disclosed as a single consolidated figure.

Cloud Infrastructure and Interoperability Platforms

Cloud migration of hospital IT systems is accelerating under the Nationwide Medical Information Platform mandate. AWS, Microsoft Azure, and Fujitsu's healthcare cloud are the dominant platforms. HL7 FHIR (Fast Healthcare Interoperability Resources) is the mandated data exchange standard for the national platform, driving EMR vendors to rebuild their data layers for compliance.

5G Connectivity and Remote Patient Monitoring

5G enables real-time transmission of high-definition diagnostic imaging, continuous vital-sign streams from wearables, and low-latency teleconsultation for remote areas. NTT Docomo and KDDI are expanding 5G healthcare use cases, accelerating connected care delivery.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Telehealth |

26.4% |

2025 |

|

Component |

Software |

52.8% |

2025 |

|

Region |

Kanto Region |

38.5% |

2025 |

By Component

To access detailed market analysis, Request Sample

Software commands the largest share at 52.8% in 2025, driven by enterprise EMR/EHR deployments, hospital management systems, and SaaS-based telehealth platforms scaling rapidly under the government's 2025 EMR standardization mandate. Cloud-based delivery models are improving scalability and reducing upfront implementation costs, compelling even smaller clinics of 200 beds and below to adopt certified software systems. The software segment is further boosted by the SaMD sub-category, where CureApp and Shionogi's approved digital therapeutics generate recurring reimbursement-driven revenue streams.

Hardware accounts for 27.6% in 2025, supported by OMRON's dominant position in blood pressure monitors, connected glucose meters, and CPAP devices. Clinical-grade remote monitoring kits and the emerging wearable biosensor category are expanding hardware revenue. Service represents 19.6% in 2025, comprising telehealth platform managed services, EMR migration consulting, cybersecurity compliance services, and government-subsidized digital health outreach programs in rural regions.

By Type

Telehealth leads at 26.4% in 2025, benefiting from MHLW regulatory liberalization and LINE Doctor's platform-embedded expansion. EMR/EHR Systems hold 21.3% share driven by the Nationwide Medical Information. Medical Wearables represent 18.7%, anchored by OMRON's ubiquitous connected blood pressure monitor fleet and the rising adoption of consumer smartwatches with clinical-grade health monitoring features.

Medical Apps account for 14.2% in 2025, with over 2,800 health applications holding MHLW approval spanning chronic disease management, mental wellness, maternity care, and dietary health. Healthcare Analytics holds 12.6%, growing rapidly as hospitals leverage accumulated EMR data through AI prediction models. Others (6.8%) include digital therapeutics (SaMD), e-pharmacy platforms, and health insurance-linked wellness management services.

Regional Market Insights

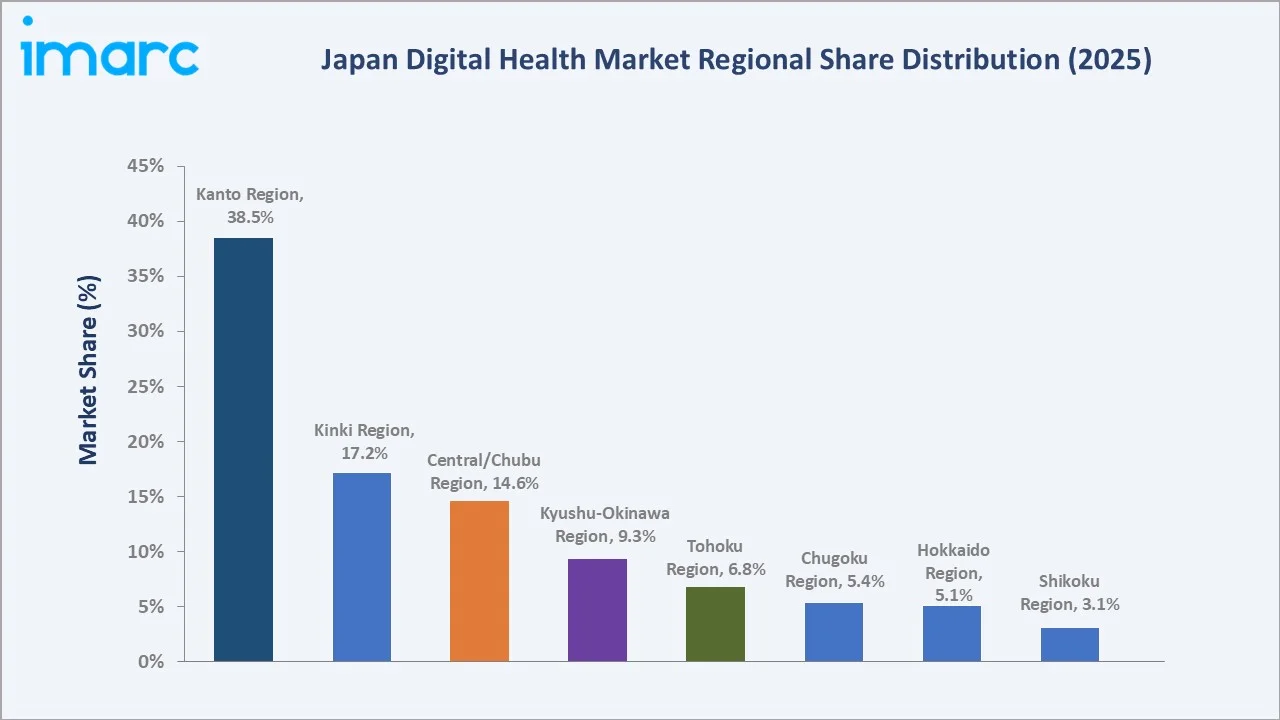

Japan's digital health market is geographically concentrated, with the Kanto Region accounting for over one-third of national revenues in 2025. Regional disparities reflect differences in population density, hospital infrastructure concentration, start-up ecosystem maturity, and government DX investment allocation across Japan's eight major prefectural regions.

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

38.5% |

Tokyo hospital concentration, JPY 50B DX fund, 40+ digital health start-up Series A rounds in 2024 |

|

Kinki Region |

17.2% |

Osaka-Kyoto pharmaceutical hub, Kyoto University AI Medical Centre, strong SaMD R&D |

|

Central/Chubu Region |

14.6% |

Toyota Group corporate wellness digitization, Nagoya University AI radiology initiative |

|

Kyushu-Okinawa Region |

9.3% |

Aging population density, government-led rural telehealth programs, 5G rural expansion |

|

Tohoku Region |

6.8% |

Post-2011 reconstruction digital health infrastructure, 5G remote monitoring pilots |

|

Chugoku Region |

5.4% |

SME healthcare digitization, phased rural EMR rollout under MHLW mandate |

|

Hokkaido Region |

5.1% |

Cold-climate remote care demand, wearable sensor adoption in elderly communities |

|

Shikoku Region |

3.1% |

Smallest regional market; accelerating via national DX grant programs through 2026 |

The Kanto Region's 38.5% dominance in 2025 reflects Tokyo's dual role as Japan's administrative capital and venture capital hub, hosting the highest concentration of National University Hospitals and government-affiliated digital health innovation programs. Kinki's 17.2% reflects Osaka's position as Japan's pharmaceutical capital, with Takeda Pharmaceutical and Shionogi both headquartered in the region and investing in digital-pharmaceutical convergence. Central/Chubu's 14.6% is supported by Toyota's employee wellness platform rollout and Nagoya University Hospital's AI diagnostics deployment in 2024-2025.

Competitive Landscape

Japan's digital health competitive landscape is characterized by a blend of established healthcare device manufacturers commanding hardware market dominance, pharmaceutical-adjacent digital therapeutics developers, consumer platform operators extending into healthcare services, and venture-backed AI health-tech platforms. The market is moderately concentrated at the hardware level but highly fragmented at the software and platform level.

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

OMRON Corporation |

OMRON Healthcare Devices |

Leader |

Connected health hardware, BP monitors, cardiac monitoring |

|

CureApp Inc. |

CureApp SC, CureApp HT |

Challenger |

SaMD pioneer, MHLW-approved digital therapeutics |

|

Shionogi & Co., Ltd. |

ADHD Therapeutic App |

Innovator |

Pharma-digital convergence, paediatric SaMD approval |

|

LINE Healthcare (LY Corp.) |

LINE Doctor |

Emerging Leader |

Platform telehealth, 95M+ user base distribution |

|

Ubie Inc. |

Ubie AI Symptom Checker |

Fast-Growing |

AI pre-diagnosis in 3,000+ clinics, Series D funded |

|

M3 Inc. |

MedPeer, AskDoctors |

Key Player |

Physician network, consumer health apps, 300K+ MDs |

|

Allm Inc. |

Join (clinical comms) |

Established |

In-hospital digital communication, 1,600+ hospitals |

|

NTT Data Corporation |

Healthcare Cloud Platform |

Infrastructure Leader |

EMR/EHR cloud, national platform integration |

Key Company Profiles

OMRON Corporation

OMRON Corporation is a leading Japanese healthcare technology company specializing in connected medical devices for home and clinical use. Its healthcare division focuses on blood pressure monitors, respiratory devices, and digital health solutions, supported by integrated platforms for remote patient monitoring and preventive care.

-

Product & Platform Portfolio: Connected blood pressure monitors (HEM series), wearable ECG patch, CPAP device with cloud connectivity, AI-enabled activity tracker.

-

Recent Developments: In July 2025, OMRON Corporation announced today that it has entered into a strategic partnership agreement with Japan Activation Capital, Inc. to accelerate sustainable growth and enhance long-term corporate value at OMRON.

-

Strategic Focus: OMRON's strategy centers on clinical-grade connectivity, integrating device data into hospital EMR systems and the national health cloud platform, positioning its hardware as infrastructure rather than consumer electronics.

CureApp Inc.

CureApp is Japan's pioneer in Software as Medical Device, having obtained MHLW approval for Japan's first prescription digital therapeutic for nicotine addiction in 2020.

- Product & Platform Portfolio: CureApp SC (smoking cessation DTx), CureApp HT (hypertension management, in clinical trials), alcohol addiction DTx (approved 2025).

- Recent Developments: In February 2025, CureApp received MHLW marketing approval for its alcohol addiction management digital therapeutic - Japan's third approved SaMD. The company is targeting five additional SaMD approvals by 2028 across hypertension, NAFLD, and sleep disorders.

- Strategic Focus: CureApp's strategy focuses on building Japan's broadest SaMD evidence base and reimbursement portfolio, positioning the company as a platform for pharmaceutical co-development of software complements to drug therapies.

LINE Healthcare (LY Corporation)

LINE Healthcare operates Japan's largest consumer-facing telehealth platform, leveraging the 95+ million monthly active users of the LINE messaging application. The LINE Doctor service enables patients to consult licensed physicians via video call within the existing LINE app interface, requiring no separate download or registration.

- Product & Platform Portfolio: LINE Doctor (video teleconsultation), LINE prescription delivery integration, LINE Health Checkup Reminder service.

- Recent Developments: In December 2020, LINE Healthcare Corporation launched its telemedicine service LINE Doctor, available with select medical clinics in the Greater Tokyo Area.

- Strategic Focus: LINE Healthcare's strategy leverages zero-friction distribution - no new app required - to democratize access to teleconsultations, particularly targeting demographics resistant to standalone medical applications including elderly users and rural residents.

Market Concentration Analysis

The Japan digital health market exhibits moderate concentration at the aggregate level, with the top 5 players (OMRON, NTT Data, M3 Inc., LINE Healthcare, and CureApp) estimated to collectively account for approximately 28-33% of total market revenue in 2025. However, concentration varies significantly by segment, ranging from high in connected hardware to highly fragmented in mHealth applications.

Japan’s digital health market features strong hardware leadership by OMRON and enterprise EMR dominance by NTT Data and Fujitsu, while software segments such as mHealth and SaMD remain highly fragmented with no clear leader. The telehealth space is beginning to consolidate around platforms like LINE Healthcare, M3 (AskDoctors), and Medley. Overall, the market is transitioning from fragmentation toward consolidation, driven by increasing M&A activity, global strategic interest, and the rollout of the Nationwide Medical Information Platform, which is expected to create winner-takes-most dynamics in EMR interoperability and platform services.

Investment & Growth Opportunities

Fastest-Growing Segments

Healthcare analytics is a high-growth segment in Japan, driven by expanding health data integration and AI adoption for clinical decision support, including risk prediction and disease management. Teleconsultation platforms—especially those integrated into consumer digital ecosystems—are also emerging as a key growth area, supported by increasing adoption of virtual care models.

Emerging Market Expansion

Digital therapeutics (SaMD) represent a key emerging opportunity in Japan, supported by a progressive regulatory framework, national reimbursement pathways, and strong pharmaceutical participation. At the same time, rural telehealth expansion—backed by government initiatives and improving connectivity—is enabling broader access to care and creating new growth avenues for digital health solutions.

Venture & Private Investment Trends

Japan’s digital health sector is seeing strong venture and strategic investment, particularly across AI diagnostics, digital therapeutics (SaMD), and telehealth platforms. Activity is driven by both domestic players and increasing interest from global companies, positioning Japan as a key entry point into the Asia-Pacific digital health market.

Future Market Outlook (2034)

The Japan digital health market is forecast to grow from USD 31.4 Billion in 2025 to USD 58.3 Billion by 2034, at a CAGR of 6.9% during 2026-2034. This trajectory reflects a mature-market digitization cycle where Japan's well-resourced but structurally conservative healthcare system undergoes systematic digital transformation driven by demographic necessity, policy mandate, and technology cost reduction.

Near-term outlook (2026-2028): Japan’s Nationwide Medical Information Platform is expected to drive EMR/EHR upgrades and interoperability across healthcare providers. Expansion of digital therapeutics (SaMD) reimbursement and growing adoption of 5G-enabled remote monitoring will support improved chronic disease management and accelerate demand for healthcare analytics solutions.

Long-term outlook (2029-2034): Japan is positioned to become a leading market for digital therapeutics and advanced regulatory frameworks, attracting global health-tech players. Over time, AI-driven monitoring and integrated elder care solutions are expected to play a central role in supporting the country’s aging population.

Research Methodology

Primary Research

Primary data collection involved structured interviews with 80+ stakeholders across Japan's digital health ecosystem, including hospital CIOs and digital transformation officers, telehealth platform executives, MHLW and PMDA regulatory affairs officers, clinical informaticians, digital therapeutics developers, health insurance executives, and digital health venture investors.

Secondary Research

Secondary research encompassed MHLW policy documents, PMDA regulatory filings, Japan Medical Association publications, Cabinet Office Digital Agency reports, AMED research program disclosures, academic journals (JMIR, Lancet Digital Health, Journal of Medical Internet Research Japan), and corporate financial disclosures and investor presentations from publicly listed digital health companies.

Forecasting Models

Market sizing employs a bottom-up methodology: segment-level revenue estimation (software licenses, hardware device sales, telehealth service fees, SaMD reimbursements) aggregated to total market size, validated against top-down macroeconomic indicators including Japan's healthcare GDP share (11.1% in 2024), digital health investment data, and insurance reimbursement claim volumes. CAGR projections are derived from multi-scenario regression models incorporating policy implementation timelines, technology adoption S-curves, and demographic projection data from Japan's National Institute of Population and Social Security Research.

Japan Digital Health Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, Others |

| Components Covered | Software, Hardware, Service |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | OMRON Corporation, CureApp Inc., Shionogi & Co., Ltd., LINE Healthcare (LY Corp.), Ubie Inc., M3 Inc., Allm Inc., NTT Data Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan digital health market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan digital health market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan digital health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Digital Health Market Report

The Japan digital health market was valued at USD 31.4 Billion in 2025 and is projected to reach USD 58.3 Billion by 2034, growing at a CAGR of 6.9% during 2026-2034.

The market is projected to exhibit a CAGR of 6.9% during 2026-2034, driven by government Medical DX mandates, aging population dynamics, and AI-powered clinical adoption.

Software leads with 52.8% share in 2025, driven by EMR/EHR platform deployments and SaaS-based telehealth solutions under the Nationwide Medical Information Platform mandate.

Telehealth leads at 26.4% in 2025, followed by EMR/EHR Systems (21.3%) and Medical Wearables (18.7%), reflecting regulatory liberalization and government digitization priorities.

Kanto Region leads with 38.5% share in 2025, driven by Tokyo's hospital concentration, digital health start-up ecosystem, and JPY 50 Billion government DX innovation fund.

Key drivers include Japan's super-aged population (28%+ aged 65), MHLW Medical DX mandates, Nationwide Medical Information Platform rollout, AI diagnostics, and telehealth regulatory liberalization.

Leading companies include OMRON Corporation, CureApp Inc., Shionogi & Co., Ltd., LINE Healthcare (LY Corp.), Ubie Inc., M3 Inc., Allm Inc., NTT Data Corporation.

Healthcare Analytics is the fastest-growing type sub-segment at 9-11% CAGR through 2034, driven by AI adoption and the national health data lake from the Nationwide Medical Information Platform.

Key challenges include EMR interoperability barriers, low digital literacy among the 80+ age cohort, cybersecurity compliance costs under APPI, and physician resistance to AI-assisted clinical tools.

High-potential opportunities include SaMD pipeline investment, rural telehealth infrastructure, healthcare analytics platforms leveraging the national data lake, and corporate wellness digital platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)