Japan Digital Oilfield Market Size, Share, Trends and Forecast by Solution, Process, Application, and Region, 2026-2034

Japan Digital Oilfield Market Size, Share, Trends & Forecast (2026-2034)

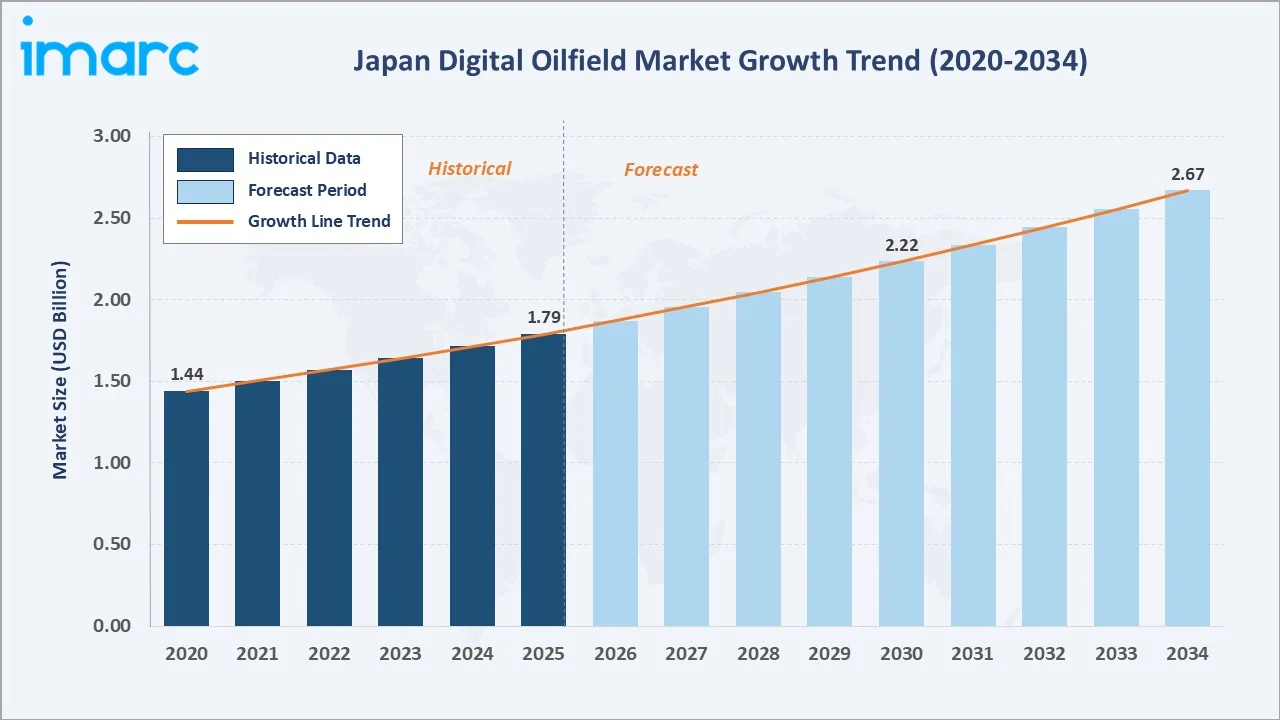

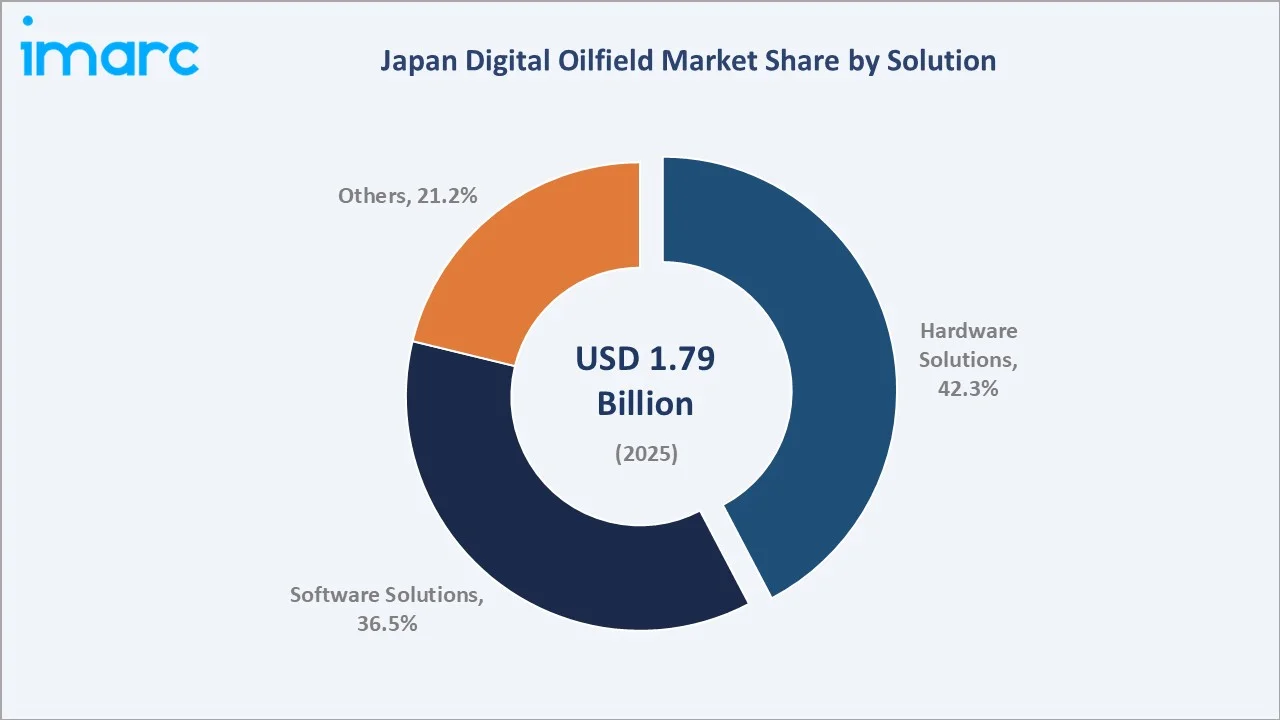

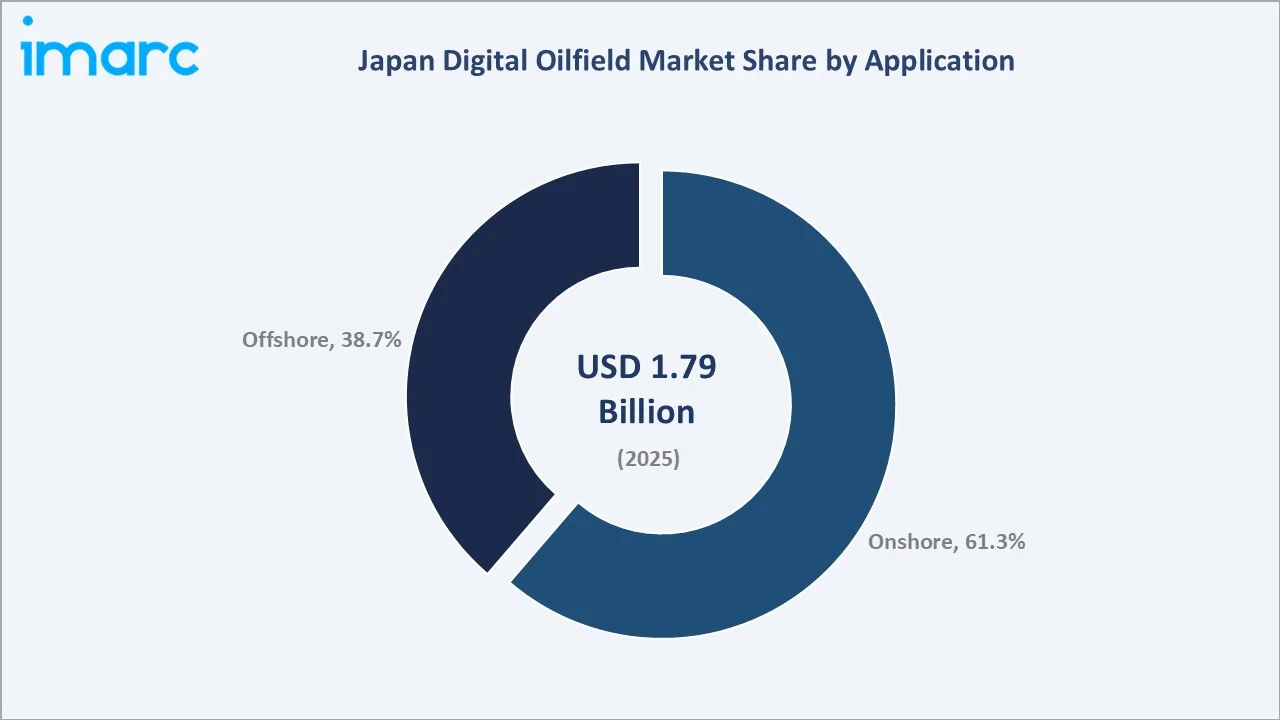

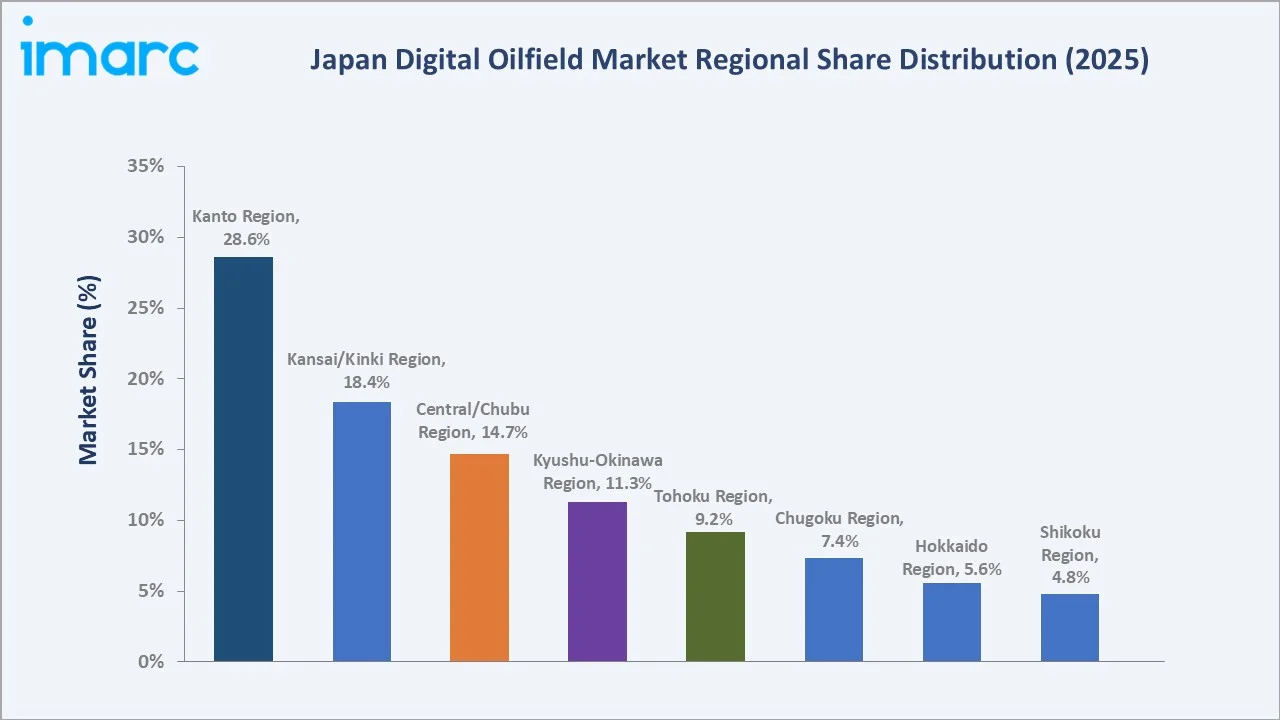

The Japan digital oilfield market was valued at USD 1.79 Billion in 2025 and is projected to reach USD 2.67 Billion by 2034, expanding at a CAGR of 4.39% during 2026-2034. Growth is driven by Japan’s GX (Green Transformation) carbon-neutral 2050 mandate requiring digital efficiency in upstream operations, chronic labor shortages accelerating unmanned remote well monitoring, and Japan’s strategic energy security investment in domestic and overseas digital E&P capabilities. Hardware solutions lead with 42.3% share, onshore dominates at 61.3%, and the Kanto Region commands 28.6% of the market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.79 Billion |

|

Forecast Market Size (2034) |

USD 2.67 Billion |

|

CAGR (2026-2034) |

4.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

Kanto Region (28.6%, 2025) |

|

Fastest Growing Region |

Tohoku Region (CAGR ~5.1%, 2026-2034) |

The Japan digital oilfield market expanded from USD 1.44 Billion in 2020 to USD 1.79 Billion in 2025, reflecting steady investment in automation, remote operations, and predictive maintenance across upstream oil and gas assets. Anchored at USD 2.22 Billion in 2030, the market is forecast to reach USD 2.67 Billion by 2034, supported by Japan's Society 5.0 digital vision, METI-driven energy sector technology roadmaps, and increasing adoption of cloud-based oilfield analytics among domestic operators.

To get more information on this market, Request Sample

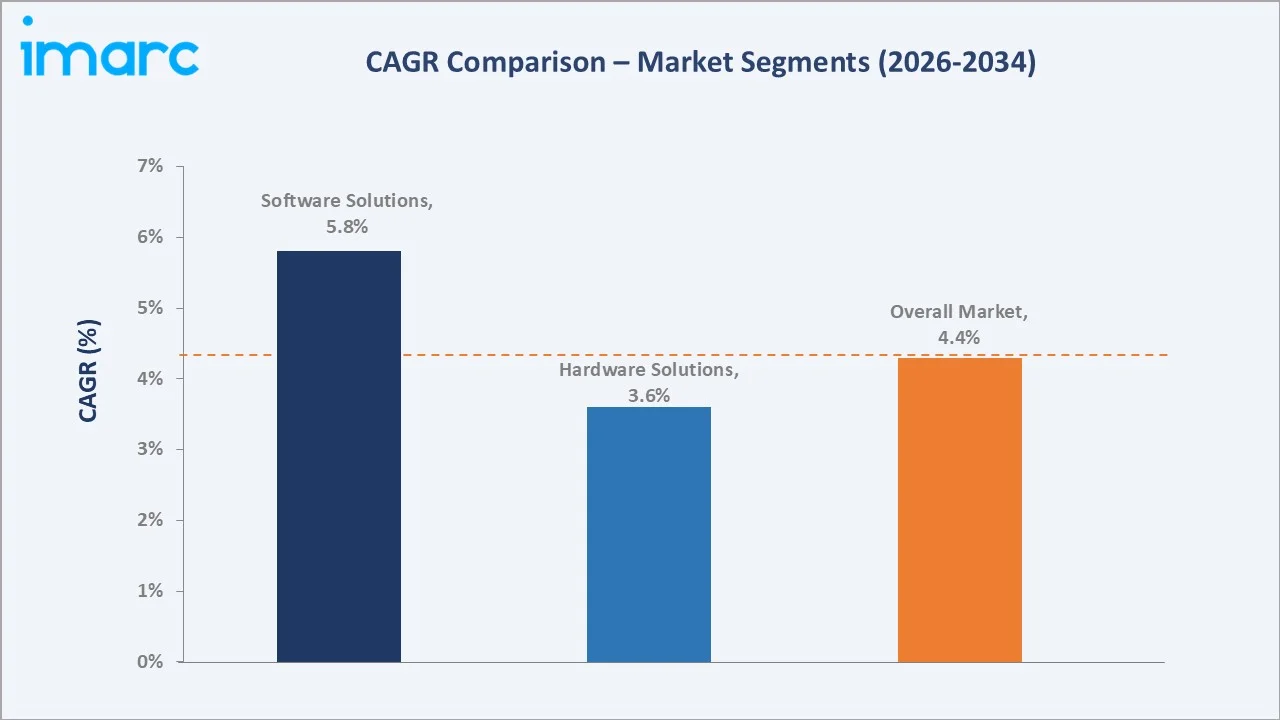

The CAGR comparison across key segments underlines the divergent growth dynamics. Software solutions, growing at 5.8%, remain the largest contributor, driven by cloud analytics and AI-powered production optimization tools.

Executive Summary

The Japan digital oilfield market expanded from USD 1.44 Billion in 2020 to USD 1.79 Billion in 2025, driven by post-COVID remote monitoring adoption, and METI’s GX strategy progressively mandating digital efficiency monitoring across Japan’s upstream operations. Japan’s digital oilfield market is defined by a unique combination of factors: a highly mature, technology-oriented operator base, a world-class domestic industrial automation industry, and Japan’s national strategic imperative to maximize domestic energy production efficiency and extend the productive life of aging Akita and Niigata onshore fields through digital enhancement rather than new development.

Hardware solutions lead at 42.3%, comprising DCS systems, SCADA networks, smart well completions, safety systems, and wireless IoT sensor networks deployed across onshore fields and Japan Sea offshore platforms. Onshore dominates at 61.3%, reflecting Japan’s history of Akita and Niigata basin production. Kanto Region’s 28.6% dominance reflects Tokyo’s role as the corporate headquarters of Japan’s oil and gas operators and digital solution vendors, making Kanto the central procurement and investment decision node for digital oilfield spending nationally.

Key Market Insights

|

Insight |

Data |

|

Dominant Solution |

Hardware Solution – 42.3% share (2025) |

|

Dominant Application |

Onshore – 61.3% share (2025) |

|

Leading Region |

Kanto Region – 28.6% share (2025) |

|

Fastest Growing Region |

Tohoku Region (CAGR ~5.1%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Hardware at 42.3% reflecting Japan’s operational technology foundation: Japan’s oil and gas digital oilfield hardware spending is dominated by Yokogawa’s Centum VP DCS, FAST/TOOLS SCADA networks, and wireless sensor network infrastructure.

- Onshore at 61.3% anchored by Japan’s historic Akita and Niigata basin operations: Japan’s onshore oil and gas production, with the onshore Nakajo oil and gas field in Niigata Prefecture has produced over 5 billion standard cubic meters of natural gas since the first production in 1959, is strategically critical for energy security.

- Kanto at 28.6% as Japan’s digital oilfield procurement headquarters: Tokyo’s dominance reflects Japan’s corporate centralization and all major digital oilfield vendors’ Japan offices are concentrated within a 30 km radius in the Tokyo metropolitan area.

Japan Digital Oilfield Market Overview

Japan’s digital oilfield market encompasses the full spectrum of hardware, software, and data management technologies deployed to optimize upstream oil and gas exploration, development, and production operations across Japan’s domestic onshore fields and offshore Japan Sea structures, as well as the digital technology programs of Japanese operators’ extensive international asset portfolios.

The ecosystem integrates hardware and sensor manufacturers, oilfield services digital platform providers, Japanese IT and AI companies, EPC digital solution providers, and E&P operators themselves, under regulatory and policy oversight from METI (Ministry of Economy, Trade and Industry) and JOGMEC.

Applications span production optimization (real-time reservoir management, artificial lift optimization, production allocation), drilling optimization (automated formation evaluation, wellbore trajectory optimization, real-time drilling analytics), reservoir optimization (AI-powered history matching, decline curve analysis, EOR digital management), safety management (emergency shutdown system monitoring, HSE compliance digital reporting), and Others (digital supply chain management, enterprise asset management). Japan’s macroeconomic and policy context, Japan’s demographic labor shortage requiring autonomous field operations, and the JPY depreciation driving import energy cost consciousness, create the multi-dimensional structural demand environment for steady digital oilfield market growth through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

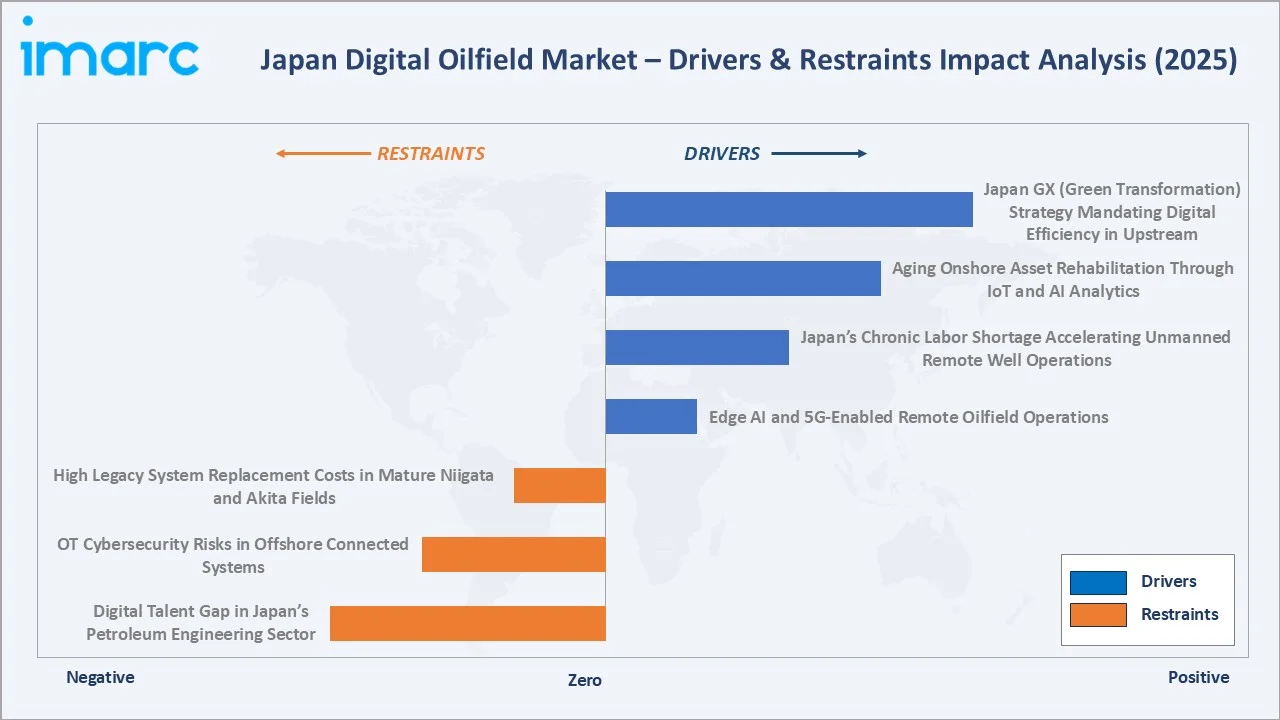

Market Drivers

- Japan GX (Green Transformation) Strategy Mandating Digital Efficiency in Upstream: Japan’s GX Strategy (launched 2023, JPY 150 trillion private-public investment over 10 years) explicitly identifies digital optimization of fossil fuel production as a key pathway to meeting Japan’s carbon neutral 2050 target while maintaining energy security during the transition.

- Aging Onshore Asset Rehabilitation Through IoT and AI Analytics: Japan’s onshore oil and gas fields are among the world’s most mature with the onshore Nakajo oil and gas field in Niigata Prefecture has produced over 5 billion standard cubic meters of natural gas since the first production in 1959, creating a uniquely large aging asset base where digital EOR (Enhanced Oil Recovery) and production optimization can economically extend field life by 10–20 years beyond natural decline timelines.

- Japan’s Chronic Labor Shortage Accelerating Unmanned Remote Well Operations: Japan’s petroleum engineering and field operator workforce is aging critically. This creates an existential pressure to deploy autonomous and remote monitoring systems that enable fewer, younger operators to manage the same well count.

Market Restraints

- High Legacy System Replacement Costs in Mature Niigata and Akita Fields: Japan’s onshore digital oilfield modernization faces the paradox of legacy: while Akita and Niigata fields have SCADA connectivity, the existing systems are 1990s–early 2000s era platforms that require complete replacement rather than incremental upgrade.

- OT Cybersecurity Risks in Offshore Connected Systems: METI’s 2024 industrial cybersecurity assessment found that Japan’s offshore oil and gas platforms are among the country’s highest-risk critical infrastructure assets for cyber attacks targeting OT (Operational Technology) systems.

Market Opportunities

- Methane Hydrate Digital Development as Japan’s Long-Term Resource Program: Japan’s methane hydrate development program represents a potential transformative resource for Japan’s energy security and the single largest long-term digital oilfield opportunity in the Japan market.

- Edge AI and 5G-Enabled Remote Oilfield Operations: Japan’s world-leading 5G network deployment, with over 150,000 5G base stations as of 2023, creates the connectivity infrastructure for edge AI processing at the wellhead level, enabling real-time anomaly detection, automated well control, and unmanned field operations at quality levels previously requiring on-site engineers.

Market Challenges

- Digital Talent Gap in Japan’s Petroleum Engineering Sector: Japan’s petroleum engineering and data science intersection, the critical skill set for digital oilfield implementation, is severely understaffed.

- Vendor Lock-In Risks from Proprietary Digital Platform Adoption: Japan’s largest digital oilfield platforms are proprietary architectures with limited interoperability, creating vendor lock-in risks that Japan’s cautious procurement culture intensely dislikes.

Emerging Market Trends

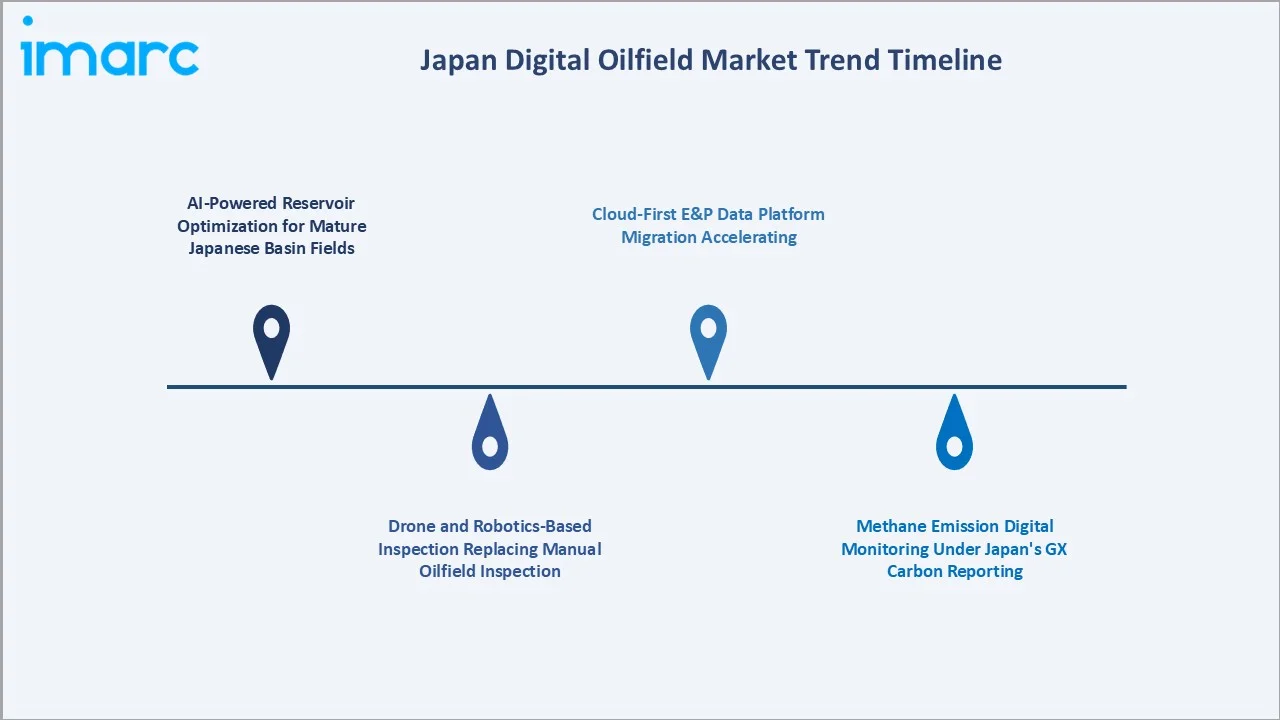

1. AI-Powered Reservoir Optimization for Mature Japanese Basin Fields

Japan’s world-uniquely challenging reservoir engineering problem, maximizing recovery from 100+ year-old Akita and Niigata fields with complex, heterogeneous geology and declining reservoir pressure, is driving Japan-specific AI reservoir optimization development.

2. Drone and Robotics-Based Inspection Replacing Manual Oilfield Inspection

Japan’s Industrial Safety and Health Act mandatory inspection requirements for oilfield facilities, combined with Japan’s severe labor shortage in qualified inspection engineers, are driving rapid adoption of drone-based visual inspection, crawler robots for pipeline inspection, and AI-powered corrosion detection from video analytics.

3. Methane Emission Digital Monitoring Under Japan’s GX Carbon Reporting

Japan’s GX Strategy and the Ministry of the Environment’s updated Greenhouse Gas Reporting Guidelines require all upstream oil and gas operators to implement continuous methane emission monitoring at well sites and processing facilities, replacing annual estimation-based reporting with real-time continuous monitoring data. This regulatory mandate creates systematic demand for methane detection sensor networks, satellite-based methane monitoring data services, and AI-powered leak detection analytics across Japan’s producing well sites.

4. Cloud-First E&P Data Platform Migration Accelerating

Japan’s E&P operators are executing multi-year cloud migration programs that convert decades of on-premise geological and engineering data to secure cloud platforms enabling global collaboration, advanced AI analytics, and disaster recovery unavailable from aging Tokyo data centers.

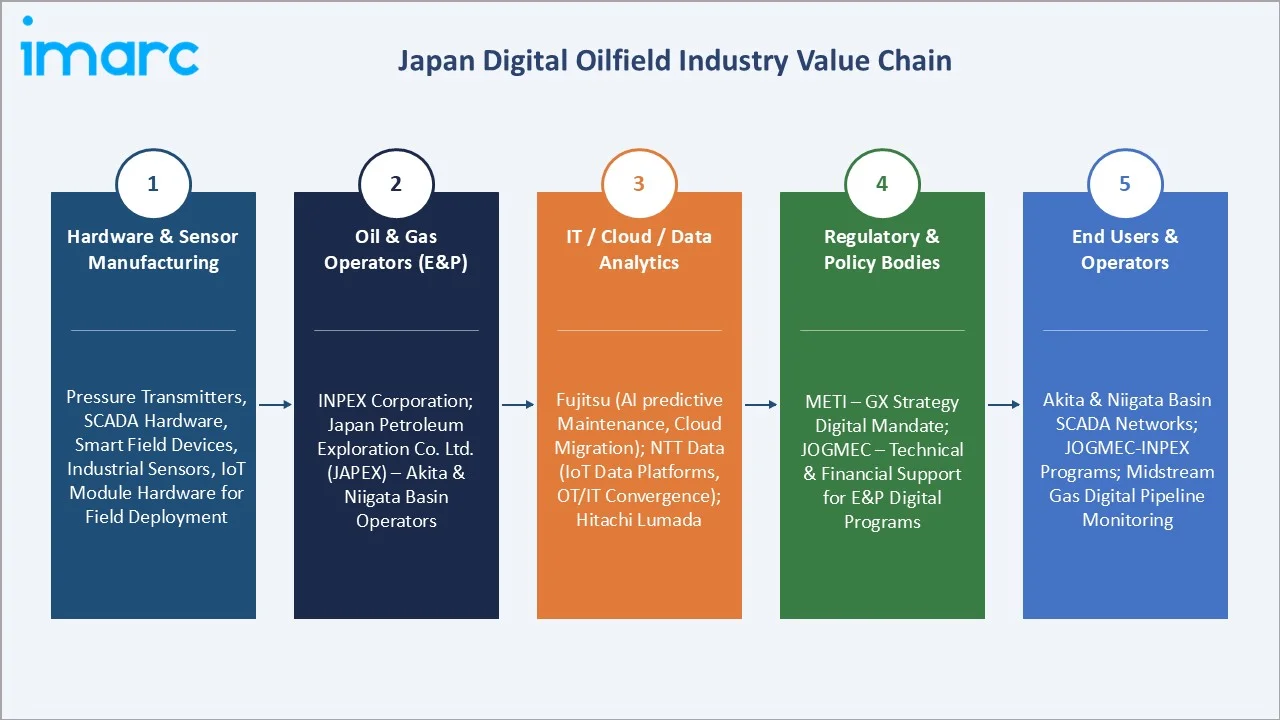

Industry Value Chain Analysis

Japan’s digital oilfield value chain integrates hardware manufacturing, software development, IT services delivery, E&P operator deployment, and regulatory compliance across six distinct stages reflecting Japan’s uniquely industrial-automation-dominated upstream ecosystem.

|

Stage |

Key Participants |

|

Hardware & Sensor Manufacturing |

Pressure transmitters, SCADA hardware, smart field devices, industrial sensors, IoT module hardware for field deployment |

|

Oil & Gas Operators (E&P) |

INPEX Corporation; Japan Petroleum Exploration Co. Ltd. (JAPEX) – Akita and Niigata onshore field operator deploying digital reservoir management |

|

IT / Cloud / Data Analytics |

Fujitsu Limited Energy & Utilities Division (AI predictive maintenance for upstream equipment, cloud migration for E&P data platforms); NTT Data Corporation (digital transformation consulting for oil & gas clients, IoT data management); Hitachi, Ltd. (Digital Systems & Services / Lumada 3.0) |

|

Regulatory & Policy Bodies |

Ministry of Economy, Trade and Industry (METI) – Japan’s GX (Green Transformation) strategy mandating digital efficiency in fossil fuel operations through 2050; Japan Organization for Metals and Energy Security (JOGMEC) – technical and financial support for Japanese E&P companies’ digital oilfield programs |

|

End Users & Operators |

Akita Basin onshore wells using SCADA and wireless sensor networks, Niigata gas field digital production optimization; JOGMEC-INPEX joint field development programs; midstream natural gas distribution with digital leak detection, digital pipeline monitoring network |

Yokogawa’s installed base of Centum VP DCS and FAST/TOOLS SCADA across Japan’s upstream creates recurring hardware maintenance and software update revenue from oil and gas clients alone. Fujitsu and NTT Data’s digital transformation consulting engagements represent the emerging high-margin service layer, with multi-year digital oilfield transformation contracts.

Technology Landscape in the Japan Digital Oilfield Industry

DCS, SCADA, and Industrial IoT Infrastructure

Yokogawa Electric Corporation revealed that its subsidiary, Yokogawa Saudi Arabia, secured a contract from the Royal Commission for Riyadh City to supply the required systems and services for the primary command and control center of the Green Riyadh project, utilizing unified DCS, SCADA, advanced process control, and enterprise data integration, is Japan’s most comprehensively deployed digital oilfield hardware-software platform, covering most of Japan’s LNG terminal DCS deployments and refinery SCADA.

Cybersecurity for OT/IT Convergence

METI’s 2024 Cybersecurity Guidelines for Industrial Control Systems specifically address oil and gas upstream OT environments. NTT Data’s OT security operations center, represents Japan’s emerging OT cybersecurity service market, as METI compliance deadlines concentrate attention on previously unmonitored control system vulnerabilities.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

| Solution | Hardware Solution | 42.3% |

2025 |

| Process | 🔒 | 🔒 |

2025 |

| Application | Onshore | 61.3% |

2025 |

| Region | Kanto Region | 28.6% |

2025 |

By Solution

Hardware solutions lead at 42.3% market share (2025). Japan’s hardware dominance reflects its industrial automation market maturity across Japan’s entire upstream and refining sector, representing systematic hardware deployment, creating a massive installed base requiring maintenance, upgrade, and replacement investment.

To access detailed market analysis, Request Sample

Software at 36.5% growing at ~5.8% CAGR encompasses E&P geoscience platforms, production optimization software, IT outsourcing services for digital oilfield infrastructure management, and collaborative product management tools. Others at 21.2% covers hosted and on-premise data storage solutions, including cloud migration of E&P seismic and well log databases and legacy on-premise storage management.

By Application

Onshore dominates at 61.3%, representing Japan’s extensive mature onshore production portfolio across Akita, Niigata, Hokkaido, Kyushu, and Central regions. Japan’s onshore digital oilfield market is distinctive globally, the combination of very mature fields, dense SCADA legacy infrastructure, Japan’s highest oilfield safety culture standards, and METI’s methane monitoring mandate creates a systematic digitalization demand that is less dependent on oil price cycles than most global onshore markets.

Offshore at 38.7% is growing faster at ~5.2% CAGR, driven by Japan Sea offshore platform structural integrity monitoring and METI’s methane hydrate program digital infrastructure. Japan’s offshore digital oilfield market commands the highest per-unit solution value nationally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

28.6% |

The Tokyo headquarters of major digital oilfield solution vendors is concentrating procurement decision-making, R&D investment, and corporate digital transformation programs in a single metropolitan cluster |

|

Kansai/Kinki Region |

18.4% |

Osaka-Kobe industrial corridor’s heavy chemical and refining industries require digital process optimization and environmental monitoring systems |

|

Central/Chubu Region |

14.7% |

Nagoya’s industrial automation and automotive technology ecosystem provides digital oilfield hardware cross-application synergies |

|

Kyushu-Okinawa Region |

11.3% |

Fukuoka’s proximity to the East China Sea offshore exploration blocks is driving offshore digital monitoring deployment |

|

Tohoku Region |

9.2% |

Akita Prefecture, Japan’s most active onshore oil and gas production region, hosts JAPEX’s primary domestic production operations across Akita Basin wells, deploying legacy SCADA system modernization programs under Japan’s largest onshore digital oilfield transformation initiative |

|

Chugoku Region |

7.4% |

Hiroshima and Okayama’s petrochemical refining cluster requires digital process optimization at the refinery-upstream interface |

|

Hokkaido Region |

5.6% |

Hokkaido’s offshore exploration potential requires remote digital monitoring, given Hokkaido’s harsh winter operational conditions, driving investment in unmanned digital monitoring systems |

|

Shikoku Region |

4.8% |

Ehime Prefecture’s Niihama Chemical and Industrial Complex requires digital process and energy monitoring systems with upstream gas supply digital traceability |

The Kanto Region’s 28.6% dominance is structural and likely permanent. Tokyo’s role as the corporate headquarters of Japan’s entire oil and gas industry means that even physical production located in Tohoku, Kyushu, or overseas is managed digitally from Kanto, concentrating procurement, IT services, and software licensing revenue in the Greater Tokyo metropolitan area.

Tohoku Region’s 9.2% share belies its strategic significance as the location of Japan’s actual domestic production operations. Akita Basin and Niigata’s Minami Nagaoka field collectively generate most of Japan’s domestic oil and gas output. The Kansai/Kinki Region’s 18.4% captures Japan’s industrial automation industry concentration.

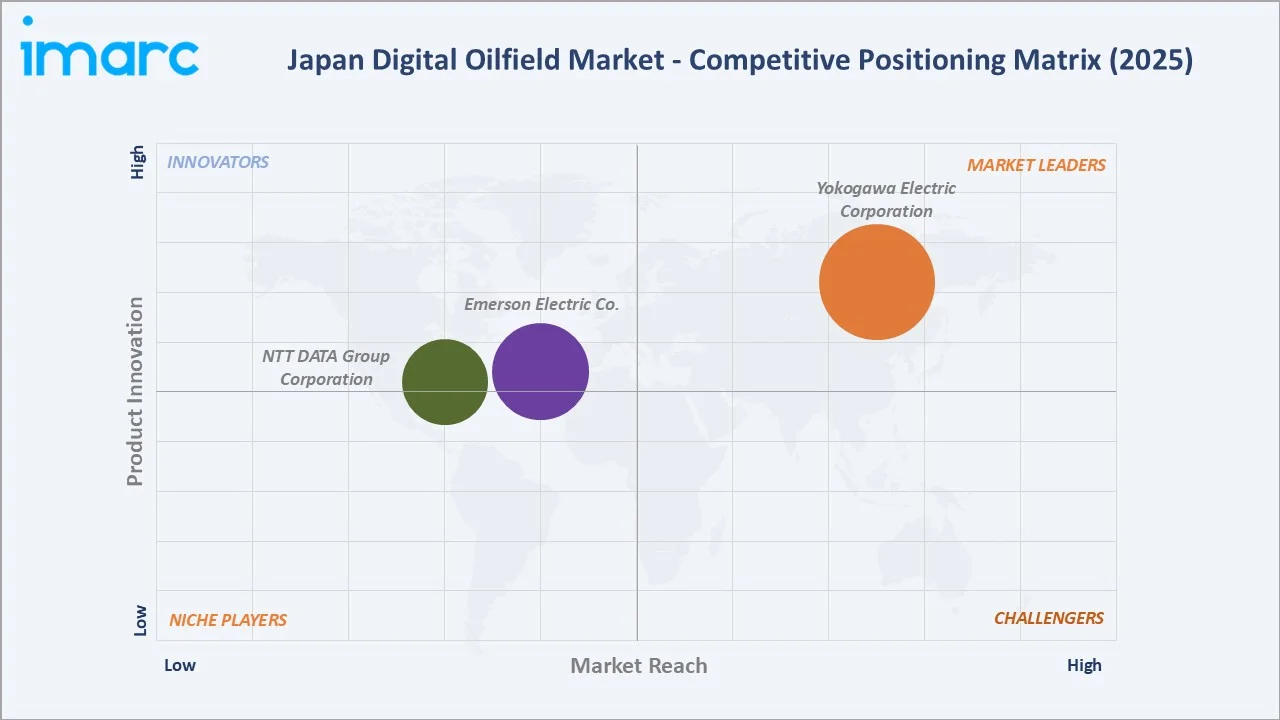

Competitive Landscape

Japan’s digital oilfield market exhibits moderate concentration at the software platform tier and fragmented competition at the hardware and IT services tiers. Yokogawa and NTT Data collectively capture approximately 45–50% of Japan’s organized digital oilfield revenue, reflecting the global oilfield services duopoly’s dominance in E&P software combined with Yokogawa’s unmatched installed base in Japan’s upstream and refining DCS/SCADA.

|

Company Name |

Services / Product Line |

Market Position |

Core Strength |

|

Yokogawa Electric Corporation |

RTUs, SCADA, DCS, Safety Systems |

Market Leader |

Japan’s leading industrial automation company with the strongest domestic market position in DCS, SCADA, and safety systems for oil and gas operations |

|

Emerson Electric Co. |

DeltaV DCS, Rosemount measurement, Micro Motion flow, Fisher control valves, AspenTech, Plantweb/AMS |

Established |

Emerson’s Japan operations serve oil and gas automation through Rosemount measurement products (the world’s most widely deployed pressure and temperature transmitter brand) |

|

NTT DATA Group Corporation |

Cloud migration, IoT data platforms, OT/IT convergence, Edge AI, digital fuel retail (COE Oil Station) |

Established |

NTT Data’s energy and utility digital transformation division providing Japanese upstream operators with cloud migration consulting, IoT data platform integration, and OT/IT convergence services |

The IT services and Japanese technology company tier represents 15–20% of market revenue and is growing faster than the global oilfield services tier as Japanese operators increase domestic IT spending relative to international oilfield services contracts.

Key Company Profiles

Yokogawa Electric Corporation

Yokogawa Electric Corporation is Japan’s largest industrial automation company and the dominant domestic supplier of DCS, SCADA, and safety systems to Japan’s oil and gas refining and petrochemicals sector.

- Product Portfolio: RTUs, SCADA, DCS, Safety Systems.

- Recent Developments: In December 2023, Cosmo Oil Co., Ltd. and Yokogawa Electric Corporation announced a collaboration between Cosmo Oil and Yokogawa Electric subsidiaries, Yokogawa Solution Service Corporation and Yokogawa Digital Corporation, to advance the digitalization of operations at Cosmo Oil’s refineries.

- Strategic Focus: Unmanned and remote oilfield operations as core growth offering addressing Japan’s engineer shortage; AI-powered advanced process control for aging domestic field production optimization.

NTT DATA Group Corporation

NTT DATA Group Corporation is a global IT services and digital transformation company, operating through its energy and utility division to serve Japanese upstream operators with advanced cloud, IoT, and OT/IT integration solutions. The company has established a dedicated practice focused on the oil and gas upstream sector in Japan.

- Product Portfolio: Private 5G, Cloud migration, IoT data platforms, OT/IT convergence, Edge AI, digital fuel retail (COE Oil Station).

- Recent Developments: NTT DATA established its energy and utility digital transformation division with a focused mandate to serve Japanese upstream operators, delivering cloud migration consulting alongside IoT data platform integration and OT/IT convergence services.

- Strategic Focus: Positioning as an end-to-end digital transformation partner for Japan's upstream oil and gas sector; Private 5G network deployment as a core connectivity enabler for field operations; OT/IT convergence as a key growth offering to bridge legacy operational technology with modern IT infrastructure; cloud migration consulting to modernize upstream data environments.

Market Concentration Analysis

Japan’s digital oilfield market is moderately concentrated at the E&P software platform tier, where Yokogawa and NTT Data collectively control approximately 45–50% of the organized market by revenue. The hardware tier is highly concentrated: Yokogawa holds an estimated 60–70% of Japan’s upstream DCS installed base, with Emerson and NTT data sharing the remaining 30–40%, a hardware concentration reflecting Yokogawa’s 50+ year Japan oil and gas incumbent relationship that is unlikely to be disrupted in the forecast period. The IT services tier is the most fragmented.

Japan’s digital oilfield market’s concentration is reinforced by Japan’s “keiretsu” business culture, long-term preferred supplier relationships that resist open competitive tendering for established solution providers. The most significant market share shift risk is from Japanese IT companies expanding into traditional oilfield services territory through AI and cloud capabilities that global oilfield services companies lack in Japanese language and government relationship terms.

Investment & Growth Opportunities

Fastest Growing Segments

Software solutions (~5.8% CAGR), offshore application (~5.2% CAGR), Tohoku Region digital oilfield (~5.1% CAGR), methane emission digital monitoring (~15–20% CAGR from 2025 base), and methane hydrate digital systems (long-term from 2028 commercialization) represent Japan’s highest-growth digital oilfield vectors.

Emerging Technology Opportunities

Japan’s methane hydrate program represents a potential Japan-specific digital oilfield sub-market by 2030 as METI moves toward pilot commercial production. Edge AI and 5G connected wellheads in Akita and Niigata represent a hardware and software opportunity as NTT Docomo and KDDI extend 5G to Japan’s producing regions. Drone-based inspection robotics for Japan Sea offshore platforms represents a market growing at 20‑25% annually as Japan’s offshore inspection labor shortage drives mandatory automation adoption.

Investment Themes

METI’s GX investment roadmap, JOGMEC’s technology development grants, and INPEX’s digital investment collectively create Japan’s digital oilfield investment landscape.

- Government program investment: JOGMEC methane hydrate digital program, METI GX digital efficiency mandate, NEDO energy digital innovation grants, and Agency for Natural Resources and Energy upstream digitalization support collectively create a government-linked digital oilfield investment annually.

- Vendor investment: SLB’s Japan-specific DELFI customization investment, Yokogawa’s OpreX R&D and NTT Data’s Connected Field platform for Japan E&P collectively represent a vendor Japan market investment annually.

Future Market Outlook (2026-2034)

Japan’s digital oilfield market is approaching its most technically sophisticated phase. From USD 1.79 Billion in 2025, the market will reach USD 2.67 Billion by 2034, at a measured 4.39% CAGR that reflects Japan’s combination of steady institutional digital investment and the structural limitations of a declining domestic reserve base.

The 4.39% CAGR, moderate by global digital industry standards but robust for Japan’s mature industrial sector, is anchored by three structurally reliable demand drivers: METI’s GX strategy creating regulatory obligation for digital efficiency in upstream operations that cannot be deferred without compliance consequences; INPEX’s global asset portfolio generating increasing digital oilfield investment that flows through Japan’s market statistics; and Japan’s chronic labor shortage creating existential pressure for unmanned and autonomous oilfield operations that has no non-digital solution.

Research Methodology

Primary Research

Primary research included structured interviews with 110+ industry stakeholders in 2025, comprising digital oilfield technology managers, METI Agency for Natural Resources and Energy digital policy officers, JOGMEC technology development program managers, energy sector leads, and independent Japan petroleum engineering specialists.

Secondary Research

Secondary research encompassed METI Agency for Natural Resources and Energy upstream digital policy documents, JOGMEC technology development annual reports, Yokogawa Electric Annual Report FY2024, NTT Data Annual Report, IMARC digital oilfield industry database, Japan Petroleum Engineering Society technical publications, METI GX Strategy documents, and NEDO energy digital technology R&D program reports. Over 130 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up solution-type × application × region disaggregated model validated against top-down Japan upstream capital expenditure models. Key inputs include INPEX 5-year capital program, JAPEX domestic digitalization budget, METI upstream digital policy investment trajectory, SLB and Halliburton Japan revenue trajectory analysis, and Yokogawa energy division revenue growth history.

Japan Digital Oilfield Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Solutions Covered |

|

| Processes Covered | Production Optimization, Drilling Optimization, Reservoir Optimization, Safety Management, Others |

| Applications Covered | Onshore, Offshore |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Yokogawa Electric Corporation, Emerson Electric Co., NTT DATA Group Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan digital oilfield market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan digital oilfield market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan digital oilfield industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Digital Oilfield Market Report

The Japan digital oilfield market was valued at USD 1.79 Billion in 2025 and is projected to reach USD 2.67 Billion by 2034.

The Japan digital oilfield market is forecast to grow at a CAGR of 4.39% during 2026-2034, driven by Japan’s GX carbon-neutral strategy, INPEX’s global digital E&P portfolio, aging asset rehabilitation, and Japan’s engineer shortage mandating autonomous operations.

Hardware solutions lead with 42.3% revenue share (2025), with Yokogawa’s Centum VP DCS and FAST/TOOLS SCADA installed across all INPEX LNG terminals and Japan’s refineries.

Onshore leads with 61.3% revenue share (2025), driven by Akita Basin and Minami Nagaoka digital programs, Japan’s most mature producing region requiring continuous SCADA modernization.

Kanto Region leads with 28.6% share (2025) as Tokyo’s corporate headquarters of INPEX, JAPEX, and all major digital oilfield vendors concentrates digital procurement decision-making in the Greater Tokyo area.

Key companies include Yokogawa Electric Corporation, Emerson Electric Co., and NTT DATA Group Corporation.

Key drivers include METI’s GX Green Transformation strategy mandating upstream digital efficiency, INPEX’s global asset portfolio digital investment, aging Akita/Niigata field rehabilitation using IoT and AI, Japan’s engineer shortage driving autonomous operations adoption, and mandatory methane emission monitoring requirements.

Key trends include INPEX Ichthys LNG digital twin deployment, AI-powered reservoir optimization for mature Japanese basin fields, drone and robot inspection replacing manual oilfield inspection, methane emission GX-mandated continuous monitoring, cloud-first E&P data platform migration, and 5G edge AI for unmanned Akita wellhead operations.

Key challenges include high legacy SCADA system replacement costs in mature Akita and Niigata fields, OT cybersecurity risks in offshore connected systems, Japan’s limited domestic reserve base constraining investment scale, digital-petroleum engineering talent shortage, and vendor lock-in risks from proprietary platform adoption.

Top opportunities include METI methane hydrate digital systems, INPEX Abadi FLNG digital twin, edge AI and 5G unmanned wellhead operations, GX-mandated methane emission monitoring across well sites, Akita/Niigata legacy SCADA replacement, and Fujitsu/NTT Data AI reservoir analytics services for INPEX and JAPEX.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)