Japan Elevator and Escalator Market Size, Share, Trends and Forecast by Type, Service, End Use, and Region, 2026-2034

Japan Elevator and Escalator Market Size, Share, Trends & Forecast (2026-2034)

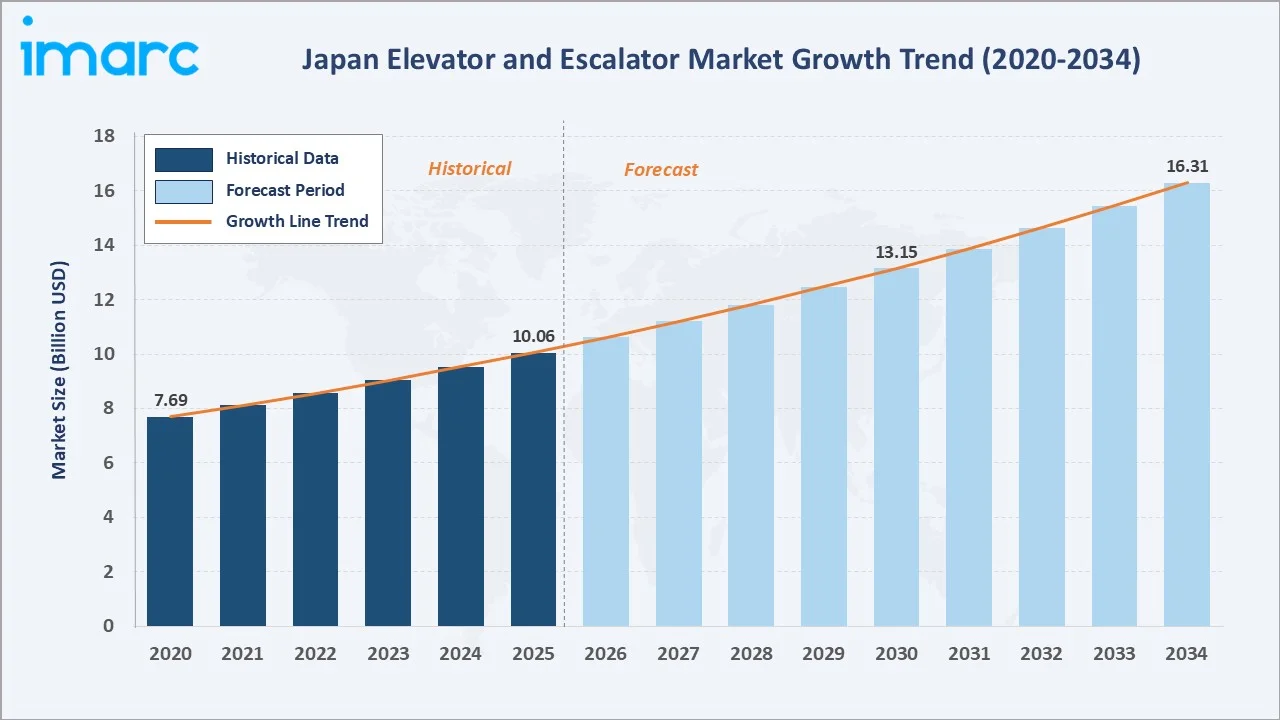

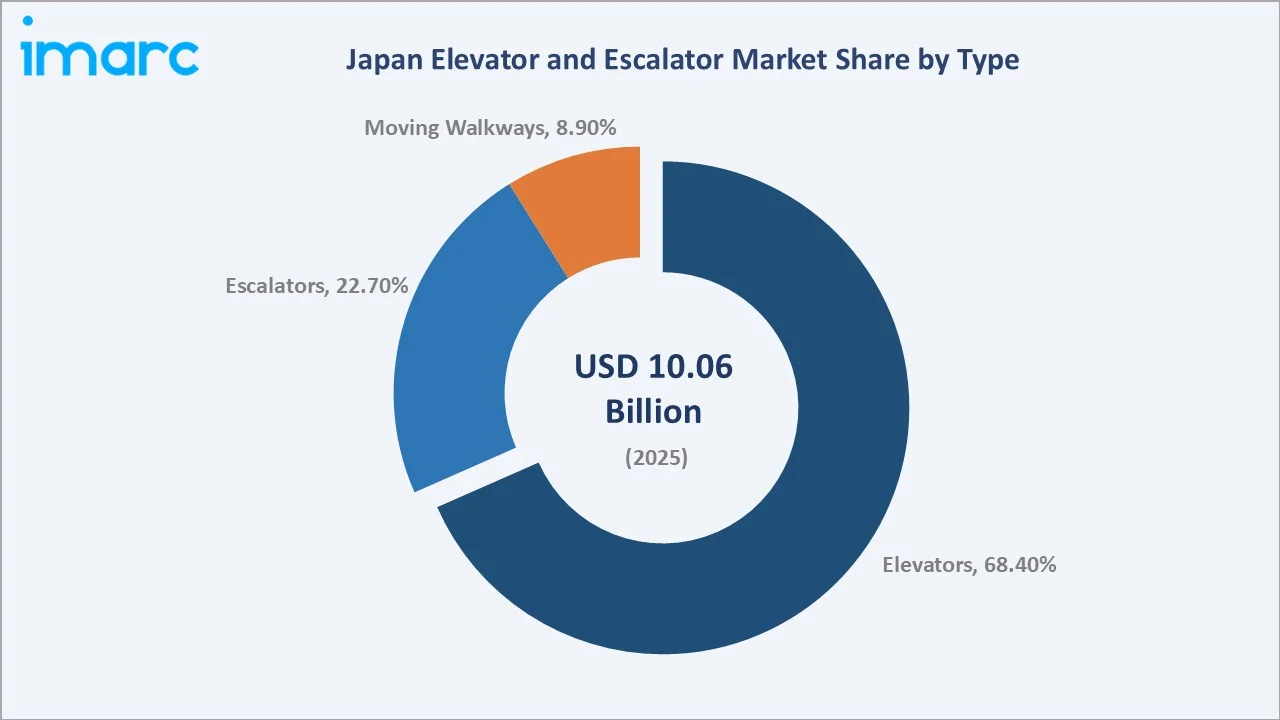

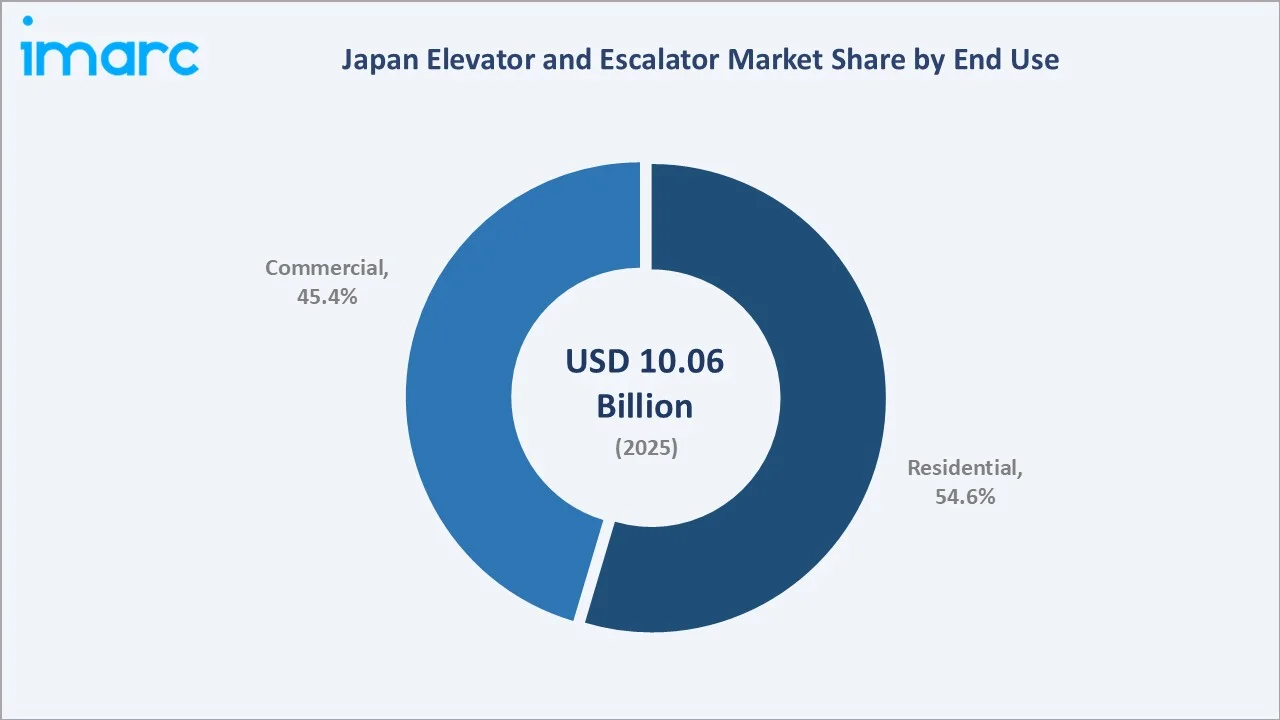

The Japan elevator and escalator market size reached USD 10.06 Billion in 2025 and is projected to reach USD 16.31 Billion by 2034, exhibiting a CAGR of 5.51% during 2026-2034. Rapid urban redevelopment, an aging population requiring barrier-free accessibility, and smart building IoT integration are the primary forces driving market growth.

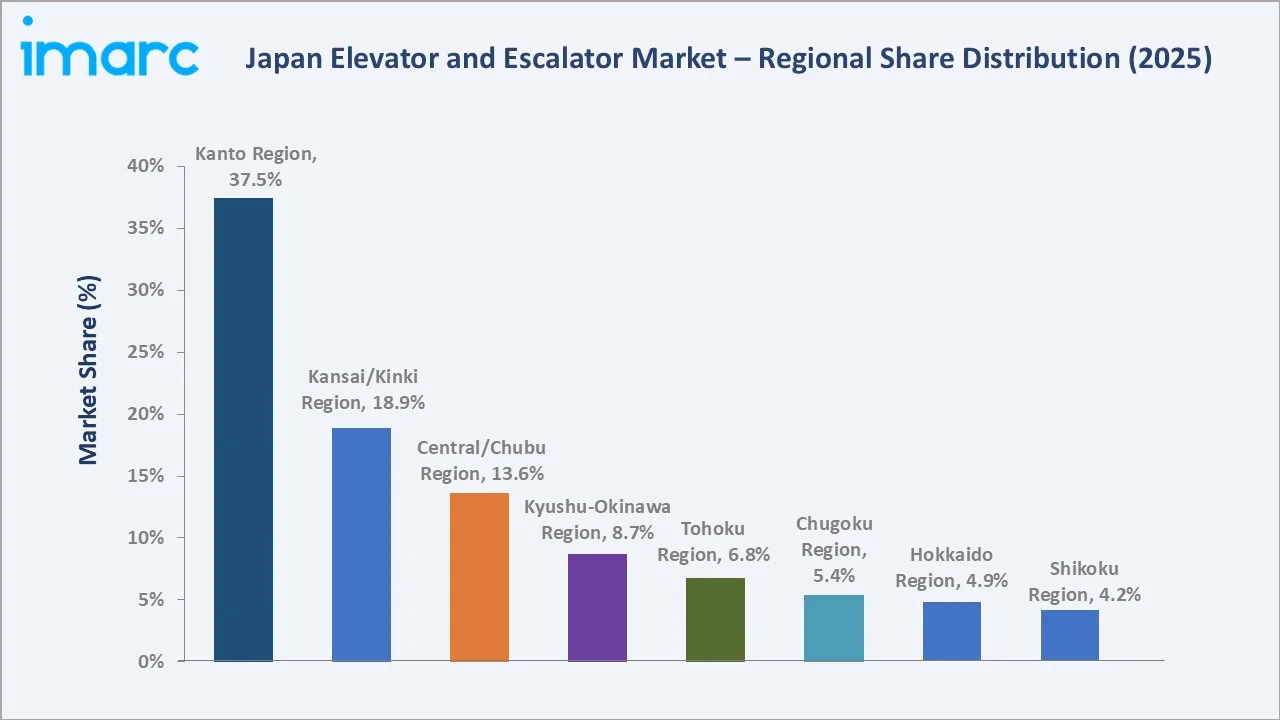

Elevators dominate the type mix at 68.4% in 2025, while the residential end-use segment leads at 54.6%. The Kanto Region commands a dominant 37.5% regional share in 2025, reflecting Tokyo's unparalleled construction and urban redevelopment activity across residential, commercial, and transit infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.06 Billion |

|

Forecast Market Size (2034) |

USD 16.31 Billion |

|

CAGR (2026-2034) |

5.51% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Type |

Elevators (68.4% share, 2025) |

|

Second Type |

Escalators (22.7% share, 2025) |

|

Leading End Use |

Residential (54.6%, 2025) |

|

Leading Region |

Kanto Region (37.5% share, 2025) |

The Japan elevator and escalator market growth trajectory from 2020 through 2034, with historical expansion to USD 10.06 Billion in 2025, reflects consistent infrastructure-driven demand. The forecast to USD 16.31 Billion captures accelerating smart building investment, aging population-driven accessibility demand, and Kanto Region urbanization-led growth.

To get more information on this market, Request Sample

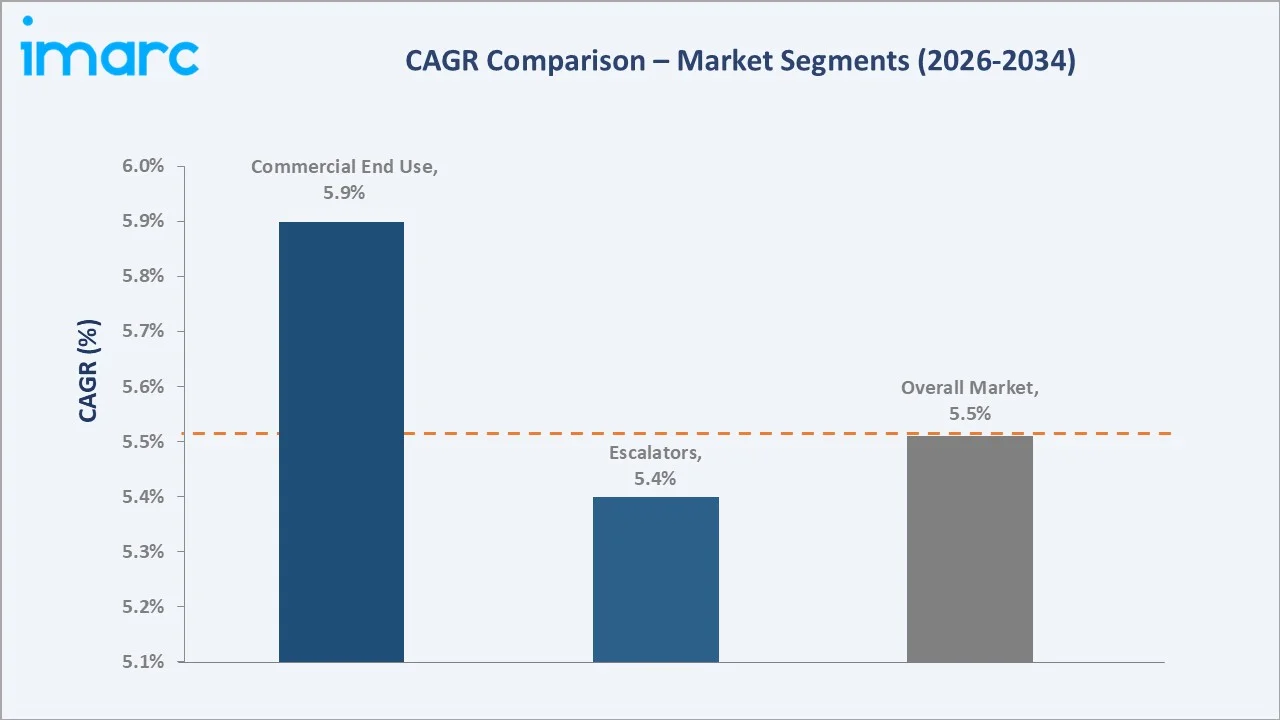

The CAGR trajectories across key type and end-use sub-segments, with the commercial end-use at ~5.9% CAGR and escalators at ~5.4% CAGR, are the fastest-growing categories within the Japan elevator and escalator industry analysis through 2034.

Executive Summary

The Japan elevator and escalator market is on a sustained growth trajectory from USD 10.06 Billion in 2025 to USD 16.31 Billion by 2034. Elevators, escalators, and moving walkways are essential vertical mobility systems deployed across residential towers, commercial complexes, transit hubs, hospitals, and public facilities, benefiting from Japan's structural demographic and urbanization drivers.

Elevators dominate type at 68.4% in 2025, driven by high-rise residential construction in Tokyo, Osaka, and Nagoya, and mandated barrier-free access for Japan's rapidly aging population. Escalators at 22.7% serve dense commercial and transit environments. Moving walkways at 8.9% are concentrated in airports and major public venues.

Residential end use leads at 54.6% in 2025, reflecting condominium and apartment tower expansion in major metropolitan areas. Commercial end use at 45.4% is driven by office complexes, shopping malls, hotels, and transit infrastructure upgrading vertical mobility systems for efficiency and IoT connectivity.

Kanto Region dominates at 37.5% in 2025, reflecting Tokyo's position as Japan's largest construction market. Kansai/Kinki Region (18.9%) benefits from Osaka's commercial expansion and Expo 2025 infrastructure. Central/Chubu Region (13.6%) is driven by manufacturing zone investment and mixed-use development in Nagoya.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Elevators – 68.4% share (2025) |

|

Leading End Use |

Residential – 54.6% share (2025) |

|

Leading Region |

Kanto Region – 37.5% share (2025) |

|

Second Region |

Kansai/Kinki Region – 18.9% share (2025) |

|

Top Companies |

Fujitec Co. Ltd., Hitachi Ltd., KONE Corporation, Mitsubishi Electric Building Solutions Corporation, Toshiba Elevator and Building Systems Corporation |

Key Analytical Observations Expanding on the Above Data:

- Elevators at 68.4% in 2025 dominate because Japan's urbanization concentrates demand in high-rise residential and commercial buildings, where elevator installation is mandated under the Building Standards Act for structures above five floors.

- Residential end use at 54.6% in 2025 leads due to Japan's continuous condominium construction in major cities, combined with government-mandated barrier-free upgrades to existing residential buildings for elderly and disabled occupants.

- Kanto Region's 37.5% dominance reflects Tokyo's position as the most densely developed real estate market in Japan, generating the highest volume of new elevator and escalator installations across commercial, residential, and public building categories.

- Commercial end use at 45.4% is underpinned by robust hotel construction linked to inbound tourism growth, office tower redevelopment programs in central Tokyo, and large-scale retail complex expansion across Japan's major urban centers.

Japan Elevator and Escalator Market Overview

Elevators, escalators, and moving walkways are critical vertical and horizontal mobility infrastructure deployed across Japan's residential, commercial, institutional, and transportation sectors. Systems encompass traction elevators, hydraulic lifts, machine-room-less (MRL) units, conventional escalators, high-speed transit escalators, and airport moving walkways.

The Japan ecosystem integrates component manufacturers, OEM system assemblers, certified installation contractors, real estate developers, government regulators, building owners, and after-sales service providers. Japan's strict Building Standards Act and seismic safety standards create a compliance environment that favors established domestic manufacturers with deep regulatory expertise.

Market Dynamics

To evaluate market opportunities, Request Sample

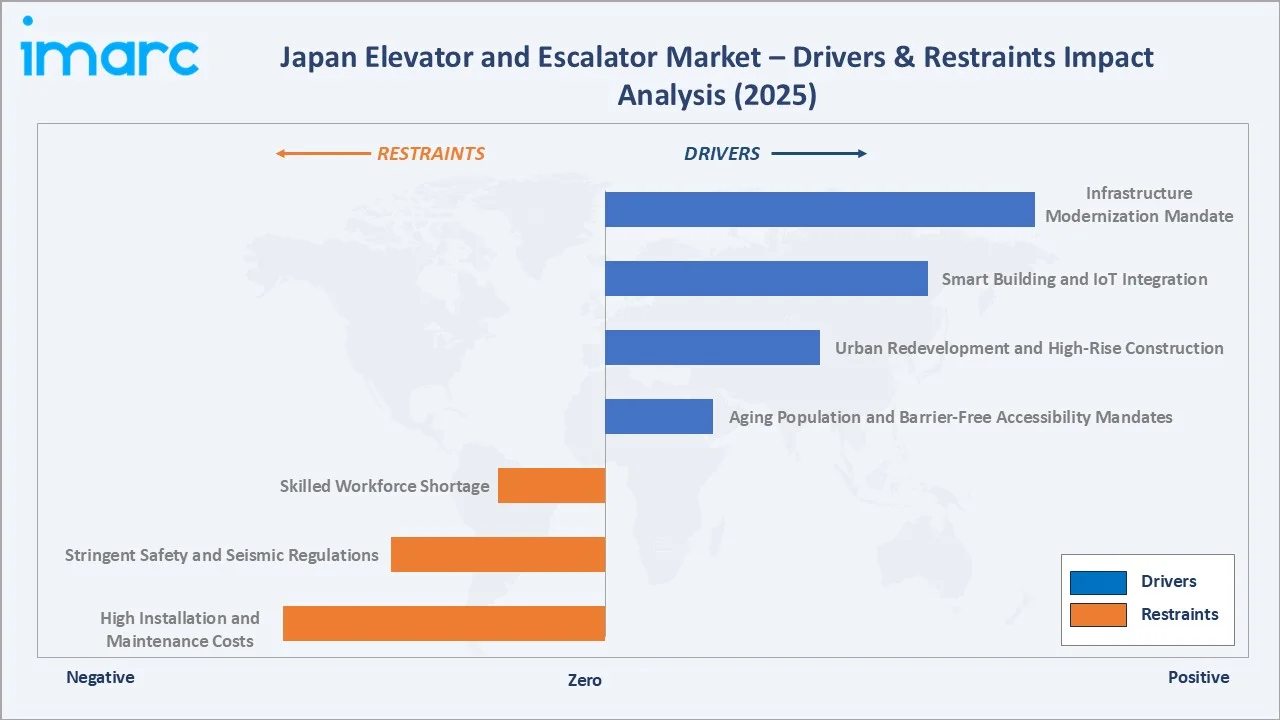

Market Drivers

- Aging Population and Barrier-Free Accessibility Mandates: Japan's elderly population (aged 65+) reached 29.3% of total population in 2024, the highest globally. Government subsidies under the Barrier-Free Act mandate elevator installation in public buildings, hospitals, and residential complexes, creating non-discretionary institutional procurement demand across all regions.

- Urban Redevelopment and High-Rise Construction: Japan's national government has designated over 50 large-scale urban redevelopment zones in Tokyo, Osaka, and Nagoya through 2035. Landmark developments including Tokiwabashi Area Redevelopment and Shibuya Station Redevelopment each deploy hundreds of new elevators and escalators.

- Smart Building and IoT Integration: Japan's Smart Cities Initiative and ESG-driven ZEB building certifications require IoT-connected elevator systems with predictive maintenance, energy consumption monitoring, and remote diagnostics, generating a premium product upgrade cycle across commercial properties.

- Infrastructure Modernization Mandate: There are approximately 900,000 elevators and escalators in use in Japan as of 2020, generating a mandatory replacement and modernization cycle driven by seismic upgrade requirements and energy efficiency standards from Japan's Ministry of Land, Infrastructure, Transport and Tourism (MLIT).

Market Restraints

- High Installation and Maintenance Costs: Seismic-resistant systems, energy-efficient regenerative drives, and IoT-enabled platforms add cost premiums over standard installations. This limits replacement pace in older, low-income residential buildings and smaller municipal facilities with constrained capital budgets.

- Stringent Safety and Seismic Regulations: Japan's post-2011 earthquake revisions to elevator safety standards require enhanced P-wave sensor, automatic braking, and earthquake recovery capabilities in all new and replacement elevators, increasing compliance complexity and overall project cost significantly.

Market Opportunities

- Smart City Development and Connected Elevators: Japan's Woven City project, digital transformation investment under Society 5.0, and new town development programs are creating greenfield smart building environments with embedded IoT elevator and escalator infrastructure generating premium product demand.

- Green and Energy-Efficient Elevators: Sustainability goals and green building standards are increasingly influencing elevator specifications, driving the adoption of energy-efficient systems such as regenerative drive technology that can recover a portion of braking energy. This shift is contributing to the emergence of a premium segment within the market, where advanced, eco-friendly elevator solutions command higher pricing compared to conventional installations due to their efficiency and long-term energy savings.

Market Challenges

- Aging Infrastructure Replacement Costs: Japan's stock of over 900,000 aging elevators represents a massive capital replacement requirement. Building owners in older residential cooperatives and rural municipalities face financing constraints that slow the modernization cycle despite strong regulatory pressure.

- Supply Chain Disruptions and Component Shortages: Global semiconductor shortages have impacted elevator control system delivery, extending lead times from 8-12 weeks to 20-28 weeks for advanced IoT-enabled elevator controllers, creating installation delays for new commercial and residential projects throughout Japan.

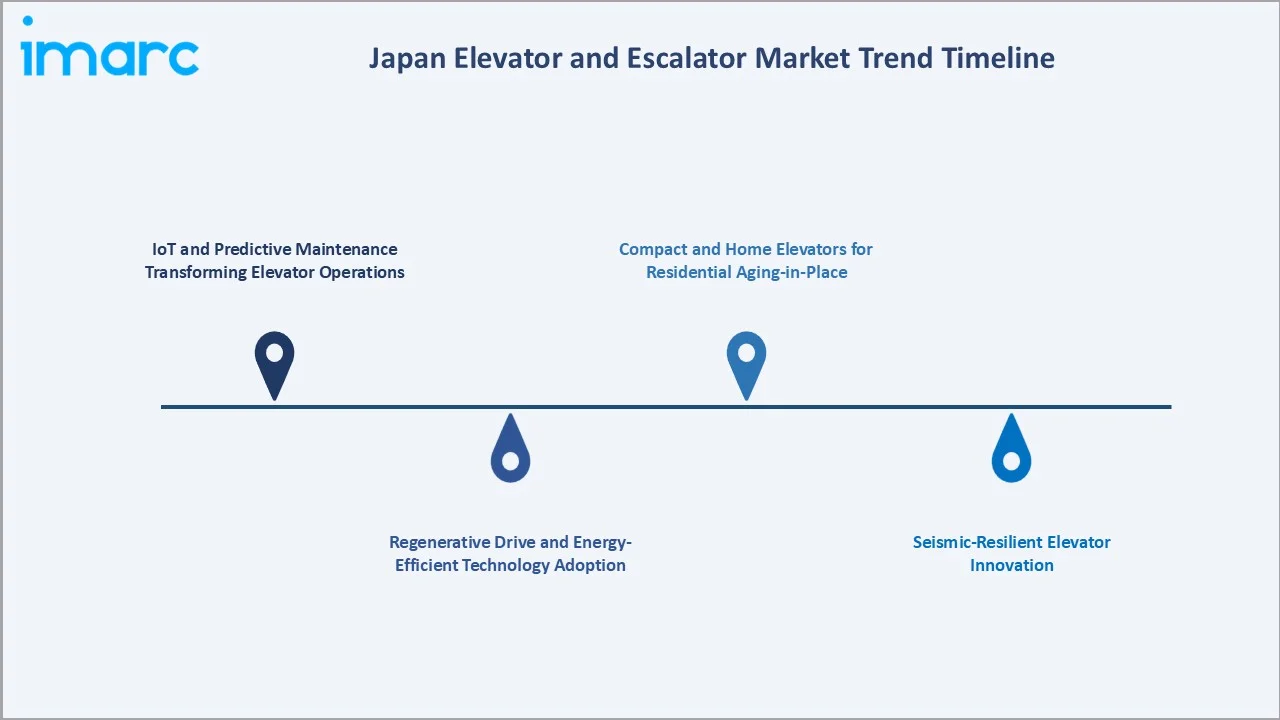

Emerging Market Trends

1. IoT and Predictive Maintenance Transforming Elevator Operations

IoT-integrated elevator systems with real-time diagnostic sensors, remote monitoring platforms, and AI-driven predictive maintenance are achieving 30-50% reduction in unplanned downtime across Japan's commercial elevator installed base. Leading OEMs are deploying cloud-connected maintenance platforms across high-volume building portfolios.

2. Regenerative Drive and Energy-Efficient Technology Adoption

Regenerative drive adoption is accelerating in ZEB-certified commercial buildings, where energy recovery from elevator braking reduces building energy consumption by 2-5%. MLIT energy efficiency guidelines for new buildings are mandating these systems in Class-A commercial construction as standard specifications.

3. Seismic-Resilient Elevator Innovation

Japan's seismic environment requires continuous innovation in earthquake-safe elevator systems. Advanced P-wave sensor integration, automatic rescue operation to nearest floor, and post-earthquake self-diagnostic return-to-service capabilities are now standard specifications across all new commercial and residential elevator installations.

4. Compact and Home Elevators for Residential Aging-in-Place

Japan's Silver Economy demand is driving rapid growth in compact residential elevators and platform lifts for single-family homes and low-rise apartments. Government subsidy programs covering up to 50% of installation costs for certified accessibility equipment are accelerating adoption among elderly homeowners nationwide.

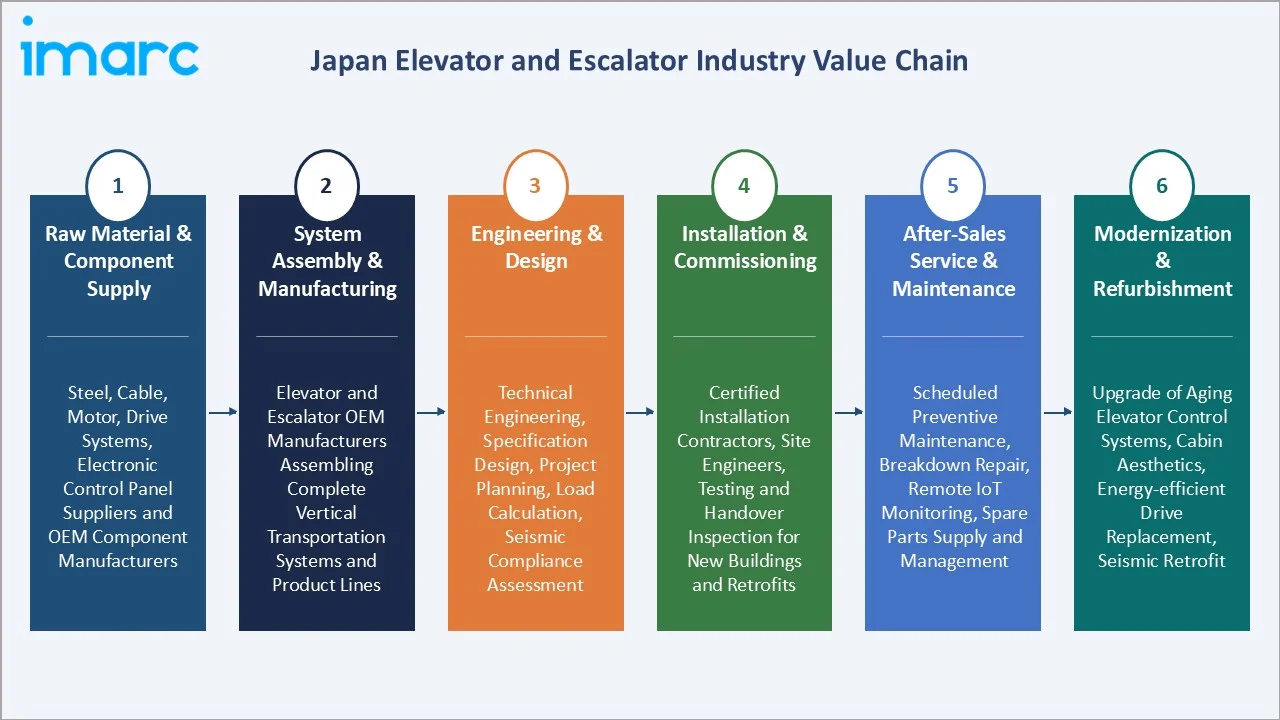

Industry Value Chain Analysis

The Japan elevator and escalator value chain spans six stages from raw component supply through modernization services. System assembly and after-sales maintenance capture the highest value-add margins, while IoT monitoring and modernization services generate the fastest growing revenue streams as Japan's large installed base continues to age.

|

Stage |

Description |

|

Raw Material & Component Supply |

Steel, cable, motor, drive systems, electronic control panel suppliers and OEM component manufacturers |

|

System Assembly & Manufacturing |

Elevator and escalator OEM manufacturers assembling complete vertical transportation systems and product lines |

|

Engineering & Design |

Technical engineering, specification design, project planning, load calculation, seismic compliance assessment |

|

Installation & Commissioning |

Certified installation contractors, site engineers, testing and handover inspection for new buildings and retrofits |

|

After-Sales Service & Maintenance |

Scheduled preventive maintenance, breakdown repair, remote IoT monitoring, spare parts supply and management |

|

Modernization & Refurbishment |

Upgrade of aging elevator control systems, cabin aesthetics, energy-efficient drive replacement, seismic retrofit |

Vertically integrated manufacturers with captive component supply chains and proprietary maintenance platforms achieve lower lifecycle cost structures compared to competitor’s dependent on third-party service networks, creating a meaningful competitive advantage in the price-sensitive modernization segment.

Technology Landscape in the Japan Elevator and Escalator Industry

Traction and Machine-Room-Less Technology

Machine-Room-Less (MRL) traction elevators have become the dominant installation technology in Japan's residential and low-to-mid-rise commercial construction. MRL systems eliminate the dedicated machine room, reducing building footprint by 5-10%, and are mandated for ZEB-certified buildings due to their superior energy efficiency profiles.

AI-Powered Predictive Maintenance and Remote Monitoring

Japan's major OEMs have invested in proprietary AI maintenance platforms utilizing machine learning on multi-sensor data to predict component failures 2-4 weeks in advance. These systems reduce unplanned maintenance costs by 20-30% and extend system lifecycle to 35-40 years, creating strong recurring digital service revenue.

Seismic Detection and Earthquake Response Systems

Japan's seismic environment has driven world-leading innovation in earthquake response elevator technology. P-wave detection systems trigger pre-emptive floor landing before S-wave arrival, reducing entrapment incidents by over 90%. Active vibration control in high-rise applications further reduces seismic structural loading on elevator systems.

Destination Dispatch and Smart Access Control

Destination dispatch systems group passengers traveling to similar floors before cab assignment, achieving 20-30% reduction in elevator wait times in high-traffic commercial buildings. Integration with building access control, visitor management, and IoT platforms is driving adoption across Japan's premium commercial real estate sector.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Elevators | 68.4% | 2025 |

| Service | 🔒 | 🔒 | 2025 |

| End Use | Residential | 54.6% | 2025 |

| Region | Kanto Region | 37.5% | 2025 |

By Type

Elevators command a 68.4% majority share in 2025 due to their fundamental role in Japan's dense urban high-rise residential and commercial construction. The Barrier-Free Act mandates elevator installation in all public buildings and housing complexes above three stories, making elevator demand structurally non-discretionary across Japan's property market.

To access detailed market analysis, Request Sample

Escalators at 22.7% in 2025 are irreplaceable in Japan's high-traffic transit infrastructure, including subway stations, shopping malls, and airports, where moving large pedestrian volumes between levels is essential for operational efficiency. Moving walkways at 8.9% serve Japan's major international airports and large exhibition centers.

By End Use

Residential end use leads at 54.6% in 2025, driven by Japan's continuous condominium tower construction in Tokyo, Osaka, and Nagoya, where mandatory elevator installation in buildings above three floors generate consistent demand. Aging population-related barrier-free retrofits in existing housing add further non-discretionary procurement volume.

Commercial end use at 45.4% in 2025 encompasses office towers, hospitality, retail complexes, and mixed-use developments. Japan's hospitality sector expansion, with new luxury hotel construction tied to inbound tourism growth exceeding 42.7 million international visitors in Japan in 2025, is a meaningful incremental driver of commercial elevator procurement.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.5% |

Tokyo high-rise construction; transit hub expansion; corporate office redevelopment |

|

Kansai/Kinki Region |

18.9% |

Commercial redevelopment; tourism facilities |

|

Central/Chubu Region |

13.6% |

Manufacturing zone expansion; Toyota ecosystem; Nagoya urban development |

|

Kyushu-Okinawa Region |

8.7% |

Tourism resort development; aging population accessibility mandates |

|

Tohoku Region |

6.8% |

Seismic-resilient upgrade programs |

|

Chugoku Region |

5.4% |

Port and industrial facility investment; mixed-use building projects |

|

Hokkaido Region |

4.9% |

Tourism and hospitality infrastructure; barrier-free public facility upgrades |

|

Shikoku Region |

4.2% |

Public facility modernization; aging residential building retrofits |

Kanto Region's 37.5% market dominance in 2025 is driven by the structurally exceptional combination of Tokyo's real estate investment scale, urban redevelopment programs, and the highest concentration of aging elevator infrastructure requiring mandatory modernization. Tokyo alone accounts for the majority of Japan's annual elevator installation and replacement volume.

Kansai/Kinki Region at 18.9% in 2025 is experiencing accelerated growth driven by Osaka's World Expo 2025 infrastructure investment, the Umeda Kita Yard mega-development, and direct rail link expansion to Kansai Airport generating substantial hotel and transit elevator procurement demand across the region.

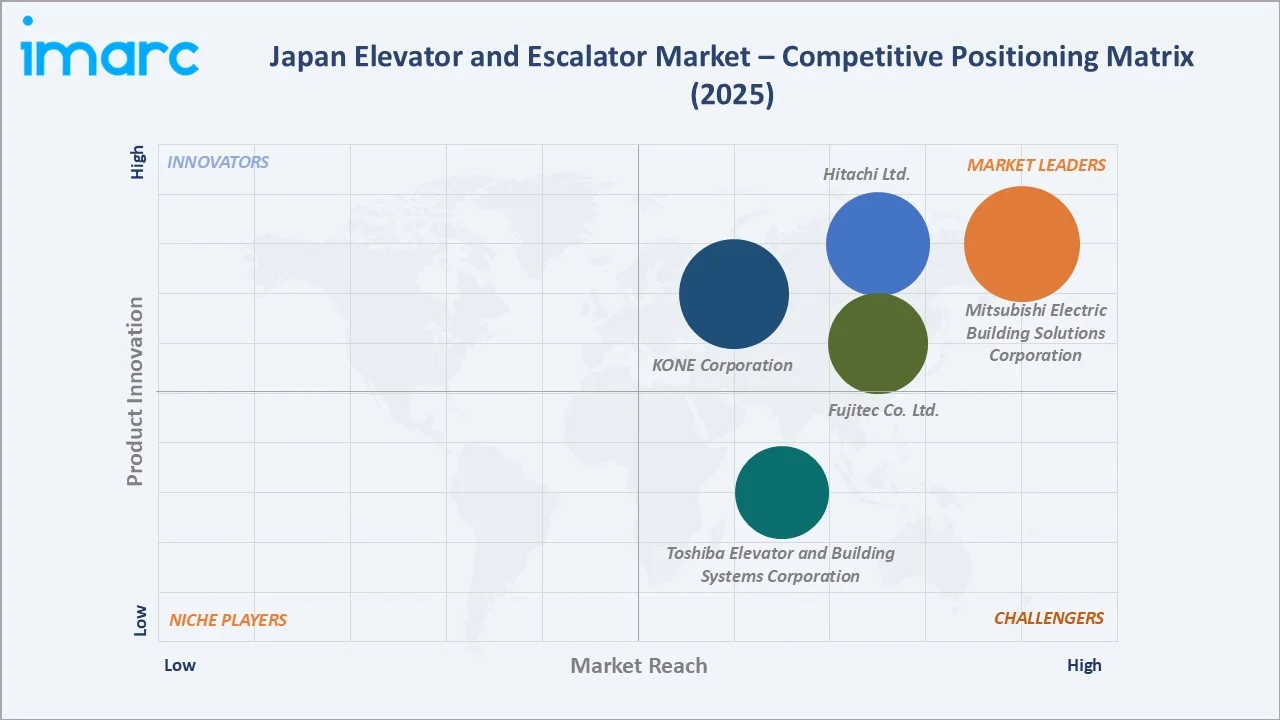

Competitive Landscape

The Japan elevator and escalator market is moderately concentrated, with domestic manufacturers commanding majority market share.

| Company Name | Key Products | Position | Strategic Focus |

|---|---|---|---|

| Fujitec Co. Ltd. | Elevators, Escalators, Moving Walks | Leader | Japan domestic leader; full product range; Asia-Pacific export presence |

| Hitachi Ltd. | Elevators, Escalators & Moving Sidewalks | Leader | IoT-integrated smart elevators; seismic technology; Japan and global presence |

| KONE Corporation | Elevators, Escalators and Autowalks | Leader | Energy-efficient solutions; ZEB-aligned; strong presence in Japan commercial and hospitality sectors |

| Mitsubishi Electric Building Solutions Corporation | Elevators, Escalators | Leader | Largest Japanese elevator manufacturer; high-speed and high-rise elevator leadership |

| Toshiba Elevator and Building Systems Corporation | Elevators, Escalators, Moving Walks | Challenger | Japan residential and commercial focus; hospital-grade systems; seismic specialist |

Key players include Fujitec Co. Ltd., Hitachi Ltd., KONE Corporation, Mitsubishi Electric Building Solutions Corporation, Toshiba Elevator and Building Systems Corporation, and others.

Key Company Profiles

Hitachi Ltd.

Hitachi Ltd., is one of Japan's largest elevator and escalator manufacturers, operating through its Mito Works development and manufacturing base, delivering vertically integrated solutions combining proprietary elevator technology with IoT-enabled smart building platforms across residential, commercial, and high-rise infrastructure segments.

- Product Portfolio: Elevators, Escalators & Moving Sidewalks

- Recent Developments: In June 2024, Hitachi Ltd. has secured its largest-ever order in Japan for elevators and escalators, including the installation of some of the country’s highest outdoor escalators, which will connect upper floors to a rooftop observation area at a significant height above ground.

- Strategic Focus: Hitachi's strategy is anchored on two growth pillars, its core elevator and escalator business spanning the full lifecycle from new installation through maintenance and modernization, and its Green & Smart Building business expanding the BuilMirai building IoT solution. The company leverages its frontline OT data from maintenance operations combined with AI and digital engineering to deliver smart, energy-efficient building systems, targeting Japan's premium high-rise commercial and public infrastructure segments.

Mitsubishi Electric Building Solutions Corporation

Mitsubishi Electric Building Solutions Corporation competes across Japan's commercial, high-rise, residential, and public infrastructure segments as the largest Japanese elevator manufacturer, leveraging its seismic engineering expertise, world-class high-speed elevator technology, and expanding digital maintenance platform to maintain domestic market leadership while accelerating international growth.

- Product Portfolio: Elevators, Escalators

- Recent Developments: In April 2026, Mitsubishi Electric Building Solutions Corporation (MEBS) completed the acquisition of all shares of Mitsubishi Hitachi Home Elevator from Hitachi, making it a wholly owned subsidiary as of April 15, 2026. As part of this transition, the company has been renamed Mitsubishi Electric Home Elevator Corporation, strengthening MEBS’s integrated building systems portfolio.

- Strategic Focus: Mitsubishi Electric Building Solutions Corporation targets domestic leadership and global scale through its NEXIEZ elevator platform supplied from its Inazawa Works and Thailand manufacturing bases, using M's BRIDGE, its global remote maintenance service providing continuous AI and IoT-driven monitoring, inspection, and data analytics, as its primary service differentiator.

Market Concentration Analysis

The Japan elevator and escalator market is moderately concentrated, with the top five domestic manufacturers collectively holding approximately 60-70% of total market revenue. This concentration reflects the structural advantage of established domestic OEMs in navigating Japan's complex regulatory, seismic compliance, and service network requirements.

Domestic manufacturers benefit from deep regulatory expertise in Japan's seismic compliance framework, established service networks with dense maintenance technician coverage, and long-standing relationships with Japan's major real estate developers and construction contractors that create high barriers to entry for new market participants.

Investment & Growth Opportunities

Fastest-Growing Segments

Commercial end use at ~5.9% CAGR through 2034 is the highest-growth end-use segment, driven by hotel construction, office tower redevelopment, and transit infrastructure expansion. IoT-connected elevator systems growing at premium pricing multiples represent the highest value-per-unit growth opportunity in the forecast period.

Emerging Markets

The Tohoku and Hokkaido regions are the fastest-growing regional markets for elevator and escalator investment through 2034, driven by post-disaster reconstruction programs and tourism infrastructure development respectively, generating new installation demand from relatively underpenetrated regional building stock.

Venture & Investment Trends

Japan's major elevator OEMs are investing in AI maintenance platform development and IoT service business models, transitioning from capital equipment sales to recurring digital service revenue. Private real estate investment funds are financing large-scale urban redevelopment projects that generate bundled elevator and escalator procurement demand.

Future Market Outlook (2026-2034)

The Japan elevator and escalator market is forecast to expand from USD 10.06 Billion in 2025 to USD 16.31 Billion by 2034 at a CAGR of 5.51%, adding USD 6.25 Billion in incremental annual market value. This sustained growth reflects the market's aging population-linked, infrastructure-driven demand characteristics with structural non-discretionary demand underpinning.

Three structural forces will most significantly shape the Japan elevator and escalator industry landscape through 2034. Japan's Society 5.0 smart city initiatives will embed IoT-connected elevator platforms as standard infrastructure in new urban development zones, creating premium specification requirements across the commercial sector.

The residential modernization segment, serving Japan's 800,000+ aging elevator installed base, will become the largest growth contributor by 2030 as regulatory enforcement of post-2011 seismic standards accelerates replacement of non-compliant systems, creating a substantial annual modernization opportunity alongside new installation demand.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Japan elevator and escalator industry stakeholders including senior commercial managers at domestic OEMs, building developers, EPC project managers, and government building standards officials from MLIT. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Japan Ministry of Land, Infrastructure, Transport and Tourism Building Statistics, Japan Elevator Association Annual Reports, Statistics Bureau Japan, Japan Building Owners and Managers Association data, Ministry of Economy Trade and Industry manufacturing statistics, and specialist industry trade publications.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating Japan GDP growth rates, urbanization indices, building permit data, and historical market evolution patterns. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

Japan Elevator and Escalator Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Elevators, Escalators, Moving Walkways |

| Services Covered | New Installation, Maintenance and Repair, Modernization |

| End Uses Covered |

|

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Fujitec Co. Ltd., Hitachi Ltd., KONE Corporation, Mitsubishi Electric Building Solutions Corporation, Toshiba Elevator and Building Systems Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan elevator and escalator market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan elevator and escalator market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan elevator and escalator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Elevator and Escalator Market Report

The Japan elevator and escalator market reached USD 10.06 Billion in 2025, reflecting consistent demand from urban redevelopment, aging population accessibility requirements, and smart building infrastructure investment across residential, commercial, and public sectors.

The market is projected to reach USD 16.31 Billion by 2034, growing at a CAGR of 5.51% during 2026-2034, driven by residential construction, commercial infrastructure modernization, seismic upgrade programs, and IoT-connected smart elevator adoption.

Elevators lead with a 68.4% type share in 2025, driven by their essential role in Japan's high-rise residential and commercial buildings, where the Barrier-Free Act mandates installation in multi-story structures above three floors.

Residential end use leads at 54.6% in 2025, supported by continuous condominium construction and government-mandated barrier-free residential upgrades for Japan's rapidly growing elderly population segment.

Kanto Region commands a dominant 37.5% market share in 2025, driven by Tokyo's unparalleled real estate investment scale, urban redevelopment programs, and the highest concentration of aging elevator stock requiring mandatory seismic modernization.

Commercial end use is the fastest-growing segment at ~5.9% CAGR through 2034, driven by hotel construction, office tower redevelopment, and IoT-connected building automation requirements in Japan's premium commercial real estate sector.

Leading companies include Fujitec Co. Ltd., Hitachi Ltd., KONE Corporation, Mitsubishi Electric Building Solutions Corporation, Toshiba Elevator and Building Systems Corporation, and others.

Key applications include high-rise residential apartments, commercial office towers, retail complexes, hotels, hospitals, railway stations, airports, and public institutional buildings, each with distinct specifications for speed, capacity, seismic resistance, and aesthetic requirements.

Japan's 29.1% elderly population (2024) is the primary structural driver of residential and public building elevator demand, mandating barrier-free access upgrades under the Barrier-Free Act and supported by government subsidies for home lift and platform lift installations.

Machine-Room-Less (MRL) traction elevators eliminate the dedicated machine room above the elevator shaft, reducing building footprint, improving energy efficiency, and lowering installation cost by 10-15%, making them the preferred specification for new residential and mid-rise commercial buildings.

Japan's seismic environment mandates earthquake-resistant elevator specifications including P-wave sensors, automatic braking, emergency floor landing, and post-seismic self-diagnostic systems, creating premium specification requirements that favor technically advanced domestic manufacturers with deep seismic engineering expertise.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)