Japan Fintech Market Size, Share, Trends and Forecast by Deployment Mode, Technology, Application, End User, and Region, 2026-2034

Japan Fintech Market Size, Share, Trends & Forecast (2026-2034)

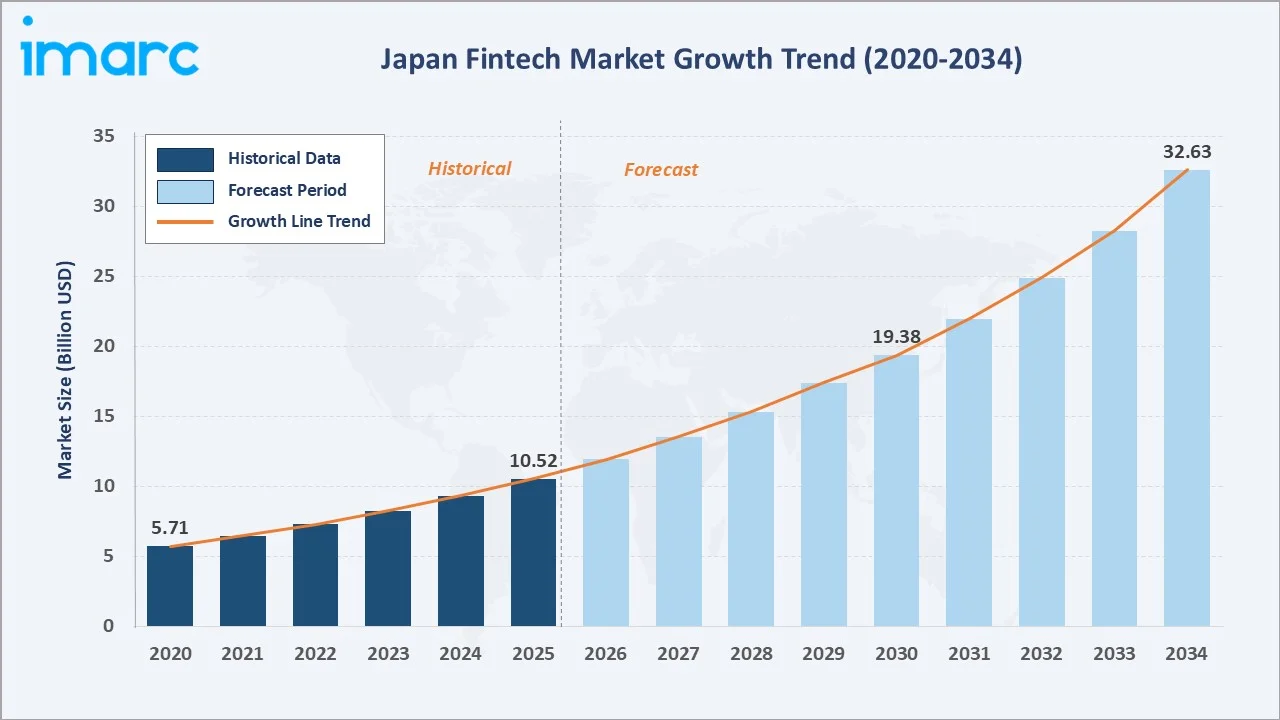

The Japan fintech market reached USD 10.52 Billion in 2025 and is projected to reach USD 32.63 Billion by 2034, growing at a CAGR of 13.0% during 2026-2034. The market is propelled by supportive regulatory frameworks, rising consumer demand for digital financial services, and rapid advances in AI, blockchain, and API-driven open banking.

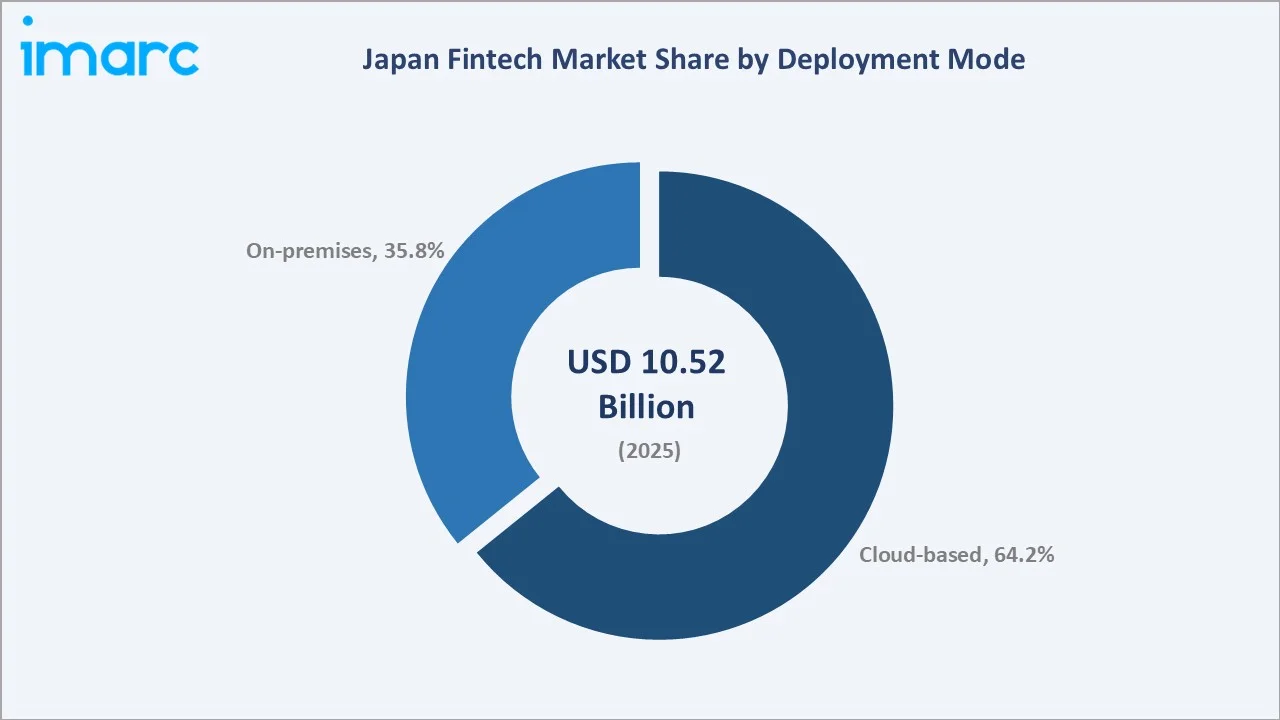

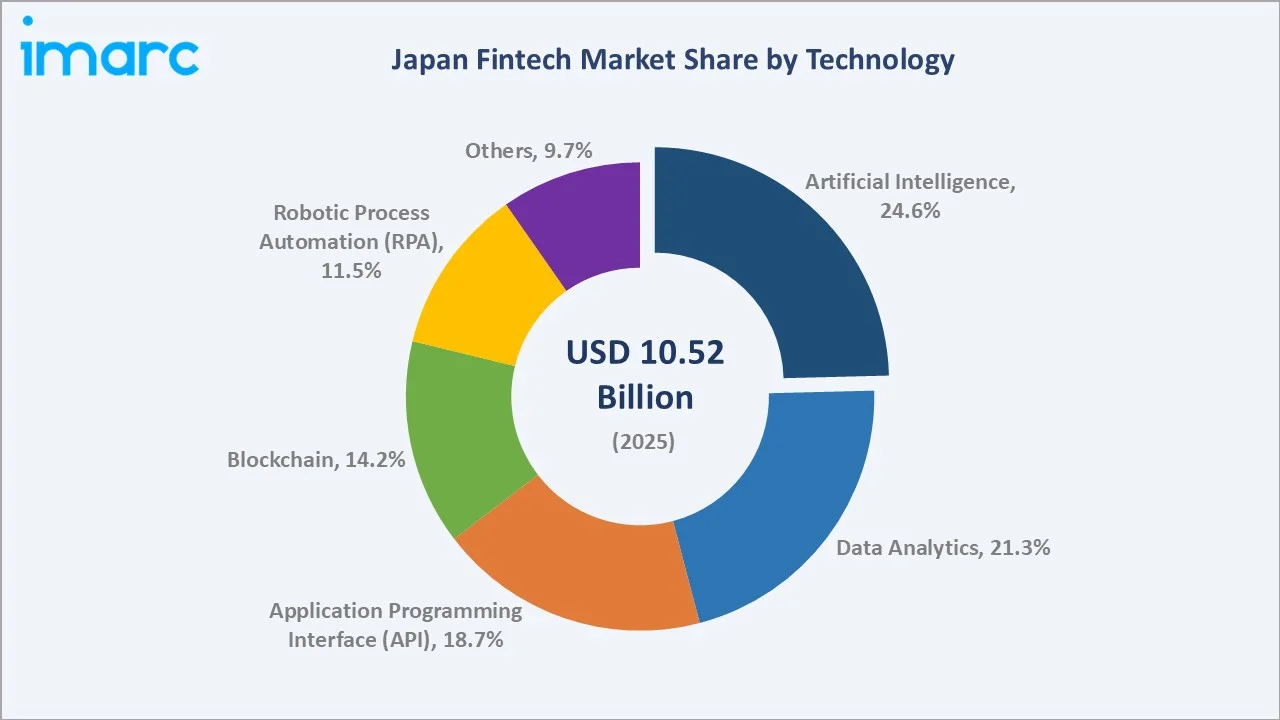

Cloud-based deployment dominates at 64.2%, reflecting fintech firms' preference for scalable cloud infrastructure. Artificial Intelligence leads the technology segment at 24.6%, enabling fraud detection, credit scoring, and personalized wealth advisory.

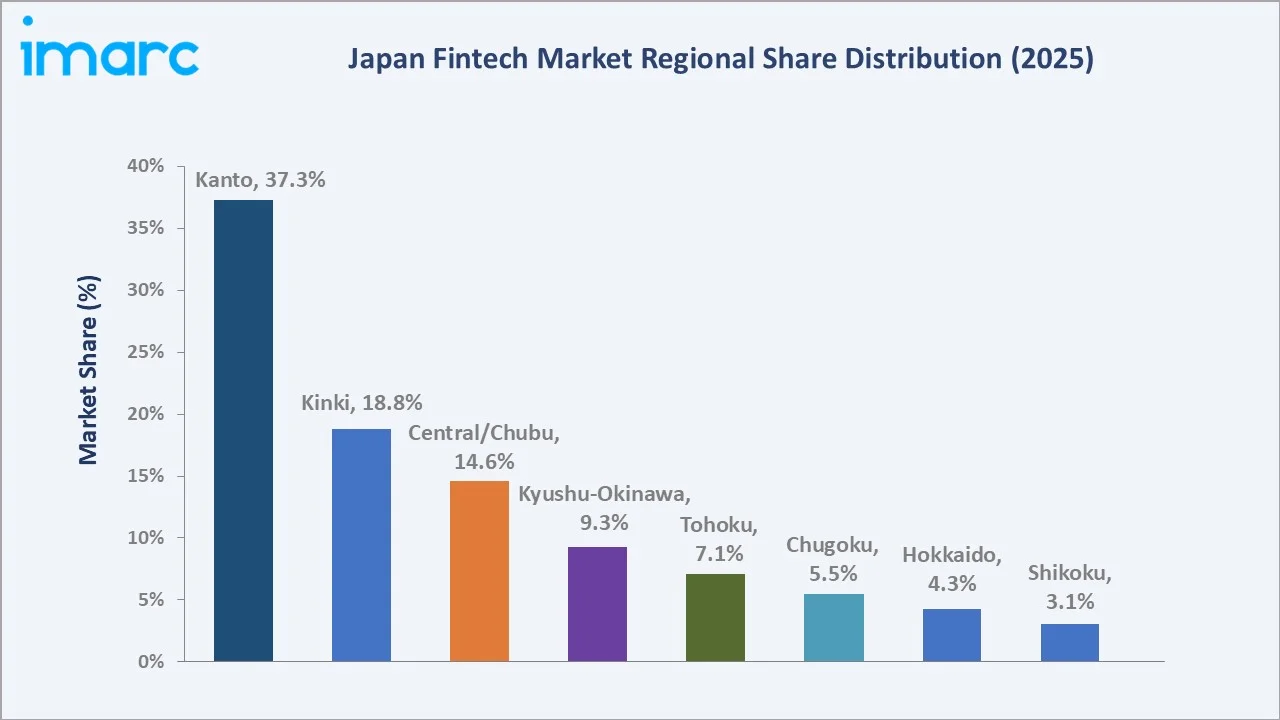

The Kanto Region commands 37.3% of total market share, anchored by Tokyo's position as Japan's primary financial hub.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 10.52 Billion |

|

Forecast Market Size (2034) |

USD 32.63 Billion |

|

CAGR (2026-2034) |

13.0% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Deployment Mode |

Cloud-based (64.2%, 2025) |

|

Leading Technology |

Artificial Intelligence (24.6%, 2025) |

|

Leading Region |

Kanto Region (37.3%, 2025) |

The Japan fintech market expanded from USD 5.71 Billion in 2020 to USD 10.52 Billion in 2025, nearly doubling in five years, anchored at USD 19.38 Billion in 2030 and forecast to reach USD 32.63 Billion by 2034. The COVID-19 pandemic compressed multi-year digital adoption into a single cycle, with government cashless society initiatives and post-pandemic fintech investment inflows sustaining structural growth momentum through 2024-2025.

To get more information on this market, Request Sample

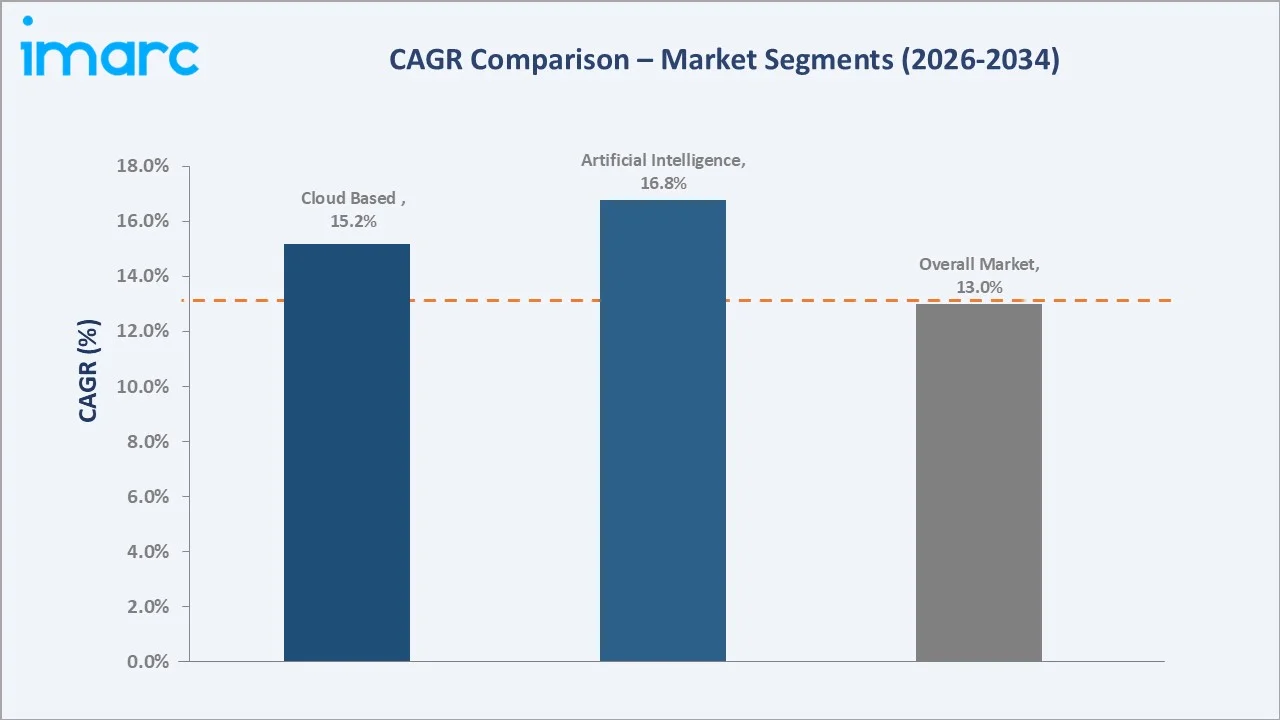

Cloud-based fintech platforms grow fastest at approximately 15.2% CAGR, driven by SaaS business models, Banking-as-a-Service adoption, and Japanese financial institutions migrating to cloud-native core banking architectures. AI technology grows at approximately 16.8% CAGR as banks and insurers scale AI-driven underwriting, compliance automation, and customer analytics deployments across their operations.

Executive Summary

The Japan fintech market reached USD 10.52 Billion in 2025, representing one of Asia's most structurally dynamic financial technology markets, underpinned by Japan's sophisticated financial ecosystem, leading global technology capabilities, and active regulatory innovation under the Financial Services Agency. The market is projected to reach USD 32.63 Billion by 2034, growing at 13.0% CAGR.

Cloud-based deployment at 64.2% dominates by enabling rapid product launches, scalable infrastructure, and cost-efficient operations. Artificial Intelligence at 24.6% leads technology by enabling personalized financial services, automated compliance, and intelligent fraud detection. The Kanto Region at 37.3% leads through Tokyo's fintech ecosystem concentration of startups, major financial institutions, and venture capital investment.

Key Market Insights

|

Insight |

Data |

|

Dominant Deployment Mode |

Cloud-based - 64.2% share (2025) |

|

Leading Technology |

Artificial Intelligence - 24.6% market share (2025) |

|

Fastest-Growing Technology |

Blockchain - 17.4% CAGR (2026-2034) |

|

Leading Region |

Kanto Region - 37.3% market share (2025) |

|

Market Opportunity |

CBDC pilots; embedded finance; AI-driven wealth management; cross-border payments |

Key Analytical Observations Supporting the Above Data:

- Cloud-based at 64.2%: Cloud deployment dominates as fintech firms require elastic, scalable, and rapidly deployable infrastructure unavailable in legacy on-premises architectures. Major cloud providers, including AWS Japan, Microsoft Azure, and Google Cloud Japan, support fintech workloads with FSA-compliant data residency and security frameworks.

- Artificial Intelligence at 24.6%: AI leads technology adoption through its cross-sector applicability across banking, insurance, and capital markets, enabling fraud detection, credit scoring, regulatory reporting automation, and robo-advisory wealth management services at a commercially viable scale across Japan's financial institutions.

- Kanto Region at 37.3%: The Kanto Region leads through Tokyo's position as Asia's second-largest financial centre, hosting Japan's three mega-banks, the Tokyo Stock Exchange, major global bank branches, and Japan's highest density of fintech venture capital investment and startup accelerator programmes.

Japan Fintech Market Overview

The Japan fintech market encompasses the design, deployment, and commercialization of technology-enabled financial products and platforms across digital payments, open banking, AI-driven wealth management, blockchain-based asset settlement, InsurTech, and regulatory technology spanning retail consumers, SMEs, and institutional clients nationwide.

The ecosystem integrates cloud infrastructure providers, API gateway and open banking platform operators, payment network processors, AI technology vendors, blockchain infrastructure firms, traditional financial institutions undergoing digital transformation, fintech startups, regulatory bodies including the FSA and Bank of Japan, and end users across all consumer and corporate segments.

Market Dynamics

To evaluate market opportunities, Request Sample

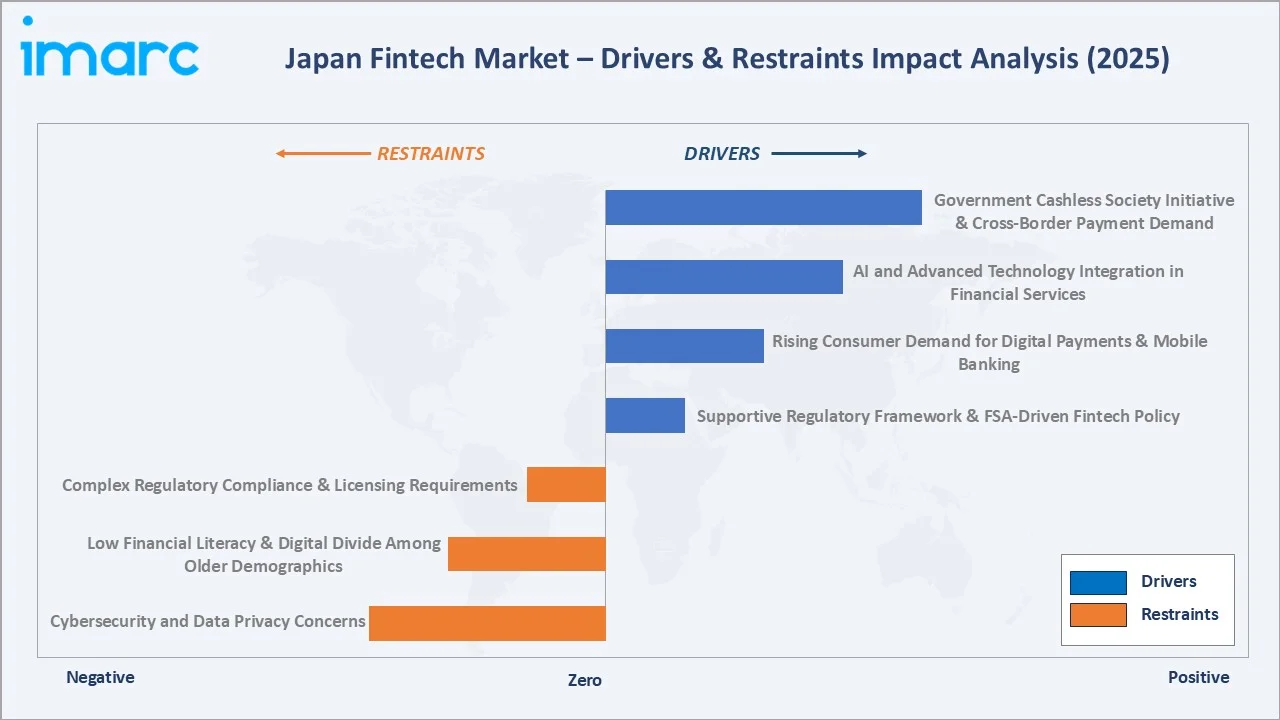

Market Drivers

- Supportive Regulatory Framework and FSA-Driven Fintech Policy: Japan's Financial Services Agency has actively promoted fintech innovation through regulatory sandbox programmes and Payment Services Act amendments facilitating digital payment licensing. This regulatory clarity encourages fintech investment and accelerates ecosystem development and market expansion across all financial service verticals.

- Rising Consumer Demand for Digital Payments and Mobile Banking: Japan's rapid pivot toward cashless payments, accelerated by the 2019 government cashless promotion campaign and the COVID-19 pandemic, has embedded digital payment habits across consumer demographics. Mobile payment penetration grew significantly during 2020-2022, creating sustained structural demand for fintech payment, wallet, and banking applications nationwide.

- AI and Advanced Technology Integration in Financial Services: Continuous advancement in artificial intelligence, machine learning, and data analytics enables Japanese financial institutions and fintech startups to deploy personalized financial services, automated credit decisioning, AI-driven fraud prevention, and intelligent robo-advisory wealth management platforms at a commercially viable scale.

- Government Cashless Society Initiative and Cross-Border Payment Demand: In 2024, the cashless payment ratio steadily increased to 42.8% in the country, backed by infrastructure investments and merchant incentive programmes. Japan's globalized economy and significant inbound tourism simultaneously create structural demand for cross-border payment, remittance, and multi-currency fintech solutions.

Market Restraints

- Cybersecurity and Data Privacy Concerns: Rising cyber threats and stringent data protection requirements under Japan's Act on the Protection of Personal Information create compliance complexity and security investment burdens for fintech operators. High-profile financial data breaches increase consumer distrust and regulatory scrutiny, creating adoption friction and significant operational cost pressures for fintech providers.

- Low Financial Literacy and Digital Divide Among Older Demographics: Japan's aging population represents a significant segment of potential fintech users with limited digital financial literacy. This demographic digital divide restricts mass-market adoption of mobile banking, digital wallets, and robo-advisory services, particularly outside major urban centres.

- Complex Regulatory Compliance and Licensing Requirements: Japan's multi-layered financial regulatory environment, spanning the FSA, Bank of Japan, and sector-specific regulators, creates significant compliance overhead for fintech entrants. Licensing timelines, capital requirements, and evolving data residency rules increase operational costs and market entry barriers, particularly for international fintech firms.

Market Opportunities

- Central Bank Digital Currency Pilot Infrastructure: The Bank of Japan's advancing CBDC pilot programme creates foundational infrastructure demand for digital currency wallet providers, payment processors, and settlement technology firms. CBDC deployment represents a structural new market for fintech technology providers and creates adjacent opportunities in digital identity and programmable finance applications.

- Embedded Finance and Banking-as-a-Service Expansion: Japan's open banking regulations and API-enabled financial infrastructure enable embedded finance use cases where non-financial companies integrate financial services into their customer journeys. BaaS platforms create new recurring revenue streams for technology-enabled banking infrastructure providers serving Japan's large e-commerce and retail conglomerates.

Market Challenges

- Legacy Core Banking System Replacement Complexity: Japan's major banks operate some of the world's largest and most complex legacy core banking systems developed over several decades. Migrating to cloud-native architectures while maintaining operational continuity represents a significant technical and financial challenge, slowing digital transformation and limiting third-party fintech integration opportunities.

- Intense Competition from Global Fintech Platforms Entering Japan: Global fintech platforms, have established Japanese operations, creating competitive pressure on domestic fintech providers. Their scale advantages, international brand recognition, and advanced technology capabilities challenge domestic incumbents' market positioning and pricing power across key product segments.

Emerging Market Trends

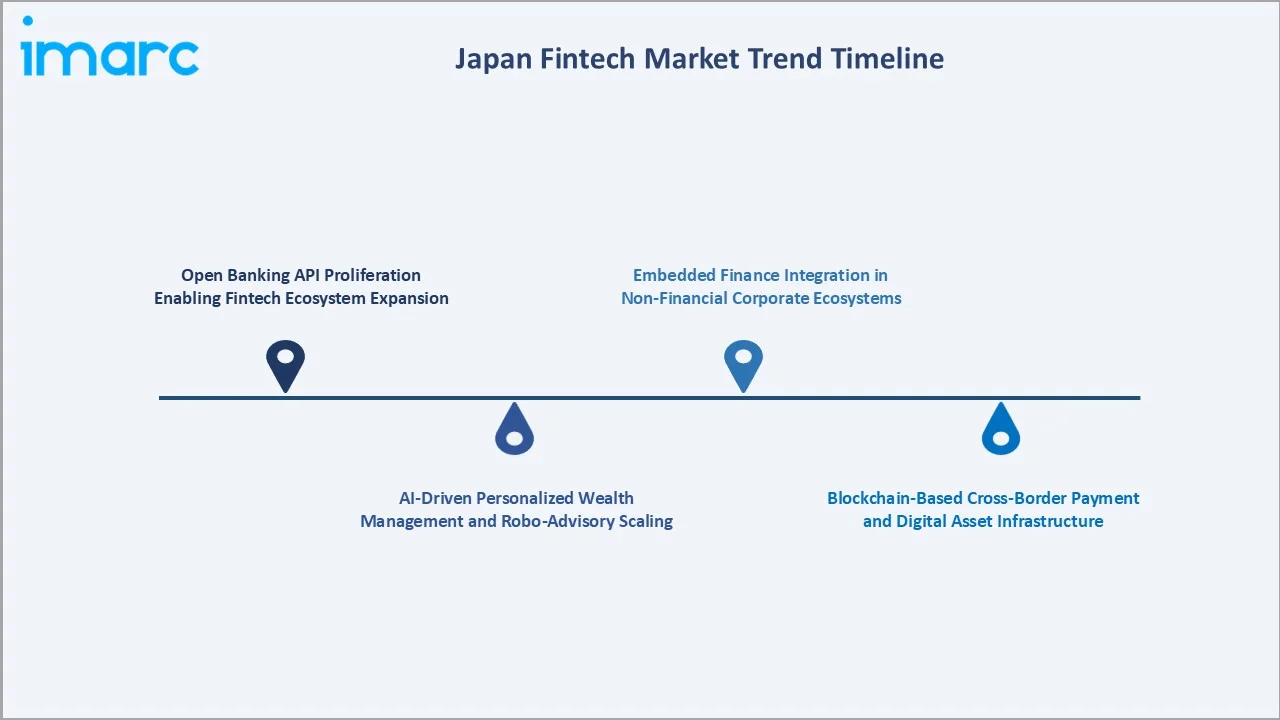

1. Open Banking API Proliferation Enabling Fintech Ecosystem Expansion

Japan's revised Banking Act mandates major banks to provide open API access, enabling third-party fintech providers to build financial management, payment, and investment applications on top of existing banking infrastructure. This structural shift accelerates a multi-layered fintech ecosystem where specialised fintech applications complement traditional financial institutions, creating compounding service innovation and new revenue models.

2. AI-Driven Personalized Wealth Management and Robo-Advisory Scaling

AI-powered robo-advisory platforms are gaining commercial traction in Japan's large retail investment market, offering automated portfolio construction, tax-loss harvesting, and personalized financial planning at significantly lower costs than traditional wealth advisors. Japan's aging population and large household savings pool represent a structurally attractive market for AI-enabled wealth management fintech platforms.

3. Blockchain-Based Cross-Border Payment and Digital Asset Infrastructure

Japan's progressive cryptocurrency regulatory framework and significant remittance market are driving blockchain-based cross-border payment platform adoption. Stablecoin issuance regulations and advancing CBDC pilot programmes are creating infrastructure for blockchain-based payment settlement, expanding the addressable market for digital asset fintech providers across institutional and retail segments.

4. Embedded Finance Integration in Non-Financial Corporate Ecosystems

Japan's large e-commerce and retail conglomerates are embedding financial services, including payments, lending, and insurance, within their consumer ecosystems. This embedded finance model creates captive financial service channels with lower customer acquisition costs, driving rapid fintech adoption outside traditional banking channels and expanding the addressable market for fintech infrastructure providers.

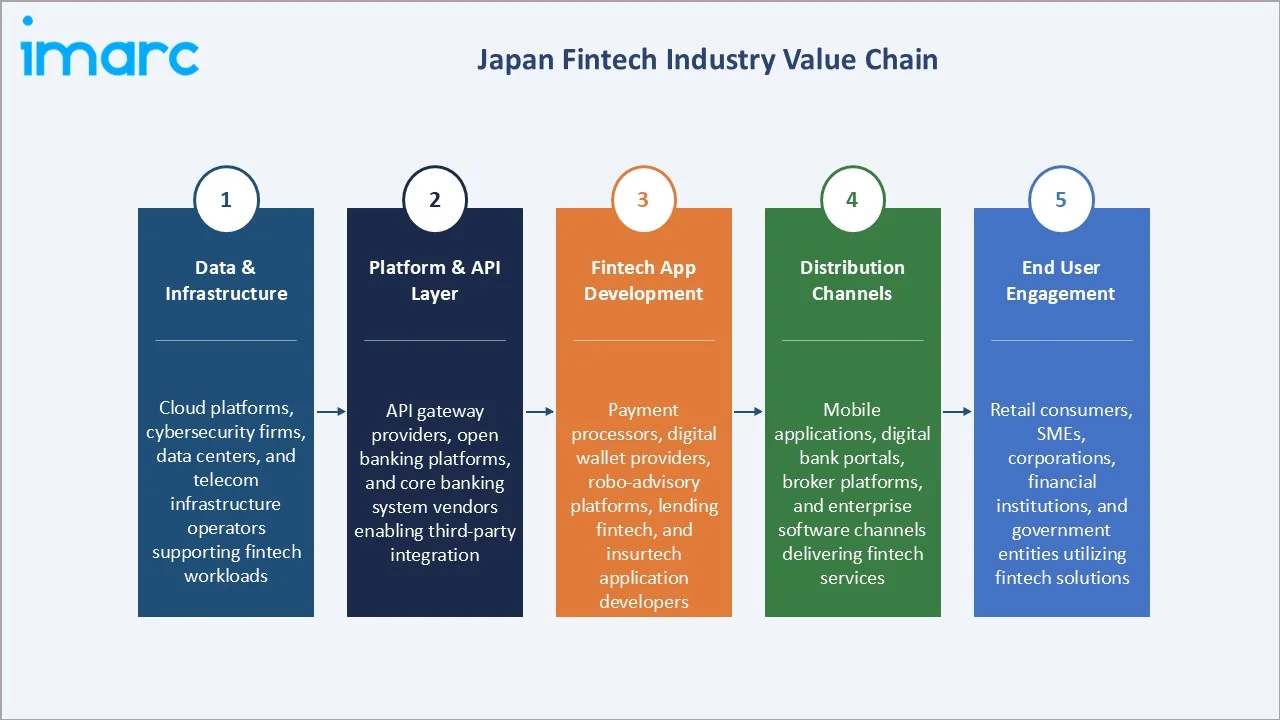

Industry Value Chain Analysis

The Japan fintech value chain integrates cloud and data infrastructure provisioning, API and platform layer development, fintech application creation, multi-channel distribution, and end-user engagement across retail and institutional segments. The commercial architecture is consolidating toward platform-based models where API layers enable fintech application ecosystems, replacing the former separation between infrastructure and application layers.

|

Stage |

Description |

|

Data & Infrastructure |

Cloud platforms, cybersecurity firms, data centers, and telecom infrastructure operators supporting fintech workloads |

|

Platform & API Layer |

API gateway providers, open banking platforms, and core banking system vendors enabling third-party integration |

|

Fintech Application Development |

Payment processors, digital wallet providers, robo-advisory platforms, lending fintech, and insurtech application developers |

|

Distribution Channels |

Mobile applications, digital bank portals, broker platforms, and enterprise software channels delivering fintech services |

|

End User Engagement |

Retail consumers, SMEs, corporations, financial institutions, and government entities utilizing fintech solutions |

The data and infrastructure tier forms the fintech value chain's most commercially critical foundation, encompassing cloud platform operators and cybersecurity firms enabling compliant fintech deployments at scale. The platform and API layer tier is experiencing the most rapid commercial expansion as open banking mandates drive API adoption across Japan's major financial institutions and third-party fintech operators.

Technology Landscape in the Japan Fintech Industry

Artificial Intelligence and Machine Learning Technology

Artificial intelligence and machine learning technology enables real-time fraud detection, automated credit scoring, personalized financial product recommendations, and intelligent regulatory compliance automation across Japan's fintech industry. AI-driven applications reduce operational costs, improve risk management accuracy, and enable scalable personalization across millions of customer interactions simultaneously.

Application Programming Interface Technology

Open API technology forms the technical backbone of Japan's open banking ecosystem, enabling secure data exchange between financial institutions and third-party fintech providers. RESTful API standards and OAuth security protocols allow fintech applications to access account data, initiate payments, and offer financial management services within a regulated, consent-based framework supporting innovation.

Blockchain and Distributed Ledger Technology

Blockchain technology is applied in Japan across cross-border payment settlement, security token issuance, digital asset custody, and trade finance documentation. Japan's progressive regulatory stance on cryptocurrency and digital assets has enabled commercial blockchain fintech deployment at institutional scale, with leading financial conglomerates operating blockchain infrastructure for digital asset and payment applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Deployment Mode |

Cloud-based |

64.2% |

2025 |

|

Technology |

Artificial Intelligence |

24.6% |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

37.3% |

2025 |

By Deployment Mode

Cloud-based deployment leads at 64.2% in 2025, encompassing the dominant fintech operational model in Japan as technology firms and financial institutions migrate from legacy on-premises infrastructure to cloud-native architectures enabling elastic scaling, rapid feature deployment, and reduced capital expenditure across all fintech service categories.

To access detailed market analysis, Request Sample

On-premises deployment at 35.8% persists among large financial institutions subject to strict data residency requirements, legacy core banking system constraints, and internal IT governance policies mandating on-premises data processing. Regulatory compliance complexity and institutional risk aversion sustain on-premises deployment despite cloud's operational cost and agility advantages for fintech workloads.

By Technology

Artificial Intelligence leads at 24.6%, capturing the broadest cross-sector application scope across banking, insurance, securities, and wealth management. AI's direct linkage to core financial risk, compliance, and customer experience functions makes it the highest-investment technology priority for Japan's financial institutions and fintech firms entering the market.

Data Analytics at 21.3% enables customer behaviour modelling, risk assessment, and operational efficiency optimisation across all financial service segments. Application Programming Interface (API) at 18.7% underpins open banking infrastructure and third-party fintech integration. Blockchain at 14.2% drives digital asset, cross-border payment, and security token applications. Robotic Process Automation (RPA) at 11.5% automates compliance, reporting, and back-office financial workflows at scale.

Regional Market Insights

|

Region |

Share (2025) |

Key Fintech Market Drivers & Characteristics |

|

Kanto Region |

37.3% |

Anchored by Tokyo, Japan's financial capital; highest concentration of fintech startups, major bank headquarters, venture capital clusters, and digital payment infrastructure nationally |

|

Kinki Region |

18.8% |

Osaka-Kobe financial corridor driving insurtech, regional banking digitization, and enterprise payment innovation as Japan's second-largest economic centre |

|

Central/Chubu Region |

14.6% |

Manufacturing-linked supply chain finance, SME digital lending, and industrial IoT payment integration fuelling steady regional fintech expansion |

|

Kyushu-Okinawa Region |

9.3% |

Regional bank digital transformation programmes, tourism-linked cashless payment expansion, and agricultural fintech adoption driving incremental growth |

|

Tohoku Region |

7.1% |

Post-disaster reconstruction initiatives driving public-sector fintech, digital governance platforms, and community-focused mobile banking solutions |

|

Chugoku Region |

5.5% |

Rural digital payment adoption, SME working capital lending digitization, and local bank core banking modernization programmes supporting growth |

|

Hokkaido Region |

4.3% |

Agricultural fintech solutions, inbound tourism QR payment expansion, and regional bank digital service rollouts emerging as primary growth drivers |

|

Shikoku Region |

3.1% |

Smallest share; mobile payment infrastructure expansion and basic digital banking adoption across regional institutions driving incremental market development |

The Kanto Region at 37.3% leads through Tokyo's fintech ecosystem concentration of startup accelerators, major bank innovation labs, venture capital investment clusters, and global technology firm regional headquarters. The Kinki Region at 18.8% reflects Osaka's position as Japan's second-largest financial centre with growing insurtech and SME lending fintech clusters providing a strong regional foundation.

Central/Chubu at 14.6% reflects manufacturing-linked supply chain finance and SME digital lending growth in Japan's industrial heartland. Kyushu-Okinawa at 9.3% benefits from regional bank digital transformation and tourism-driven cashless payment expansion.

Tohoku, Chugoku, Hokkaido, and Shikoku together represent 20.0% of the market, with mobile payment adoption and digital banking infrastructure driving incremental growth across these regions.

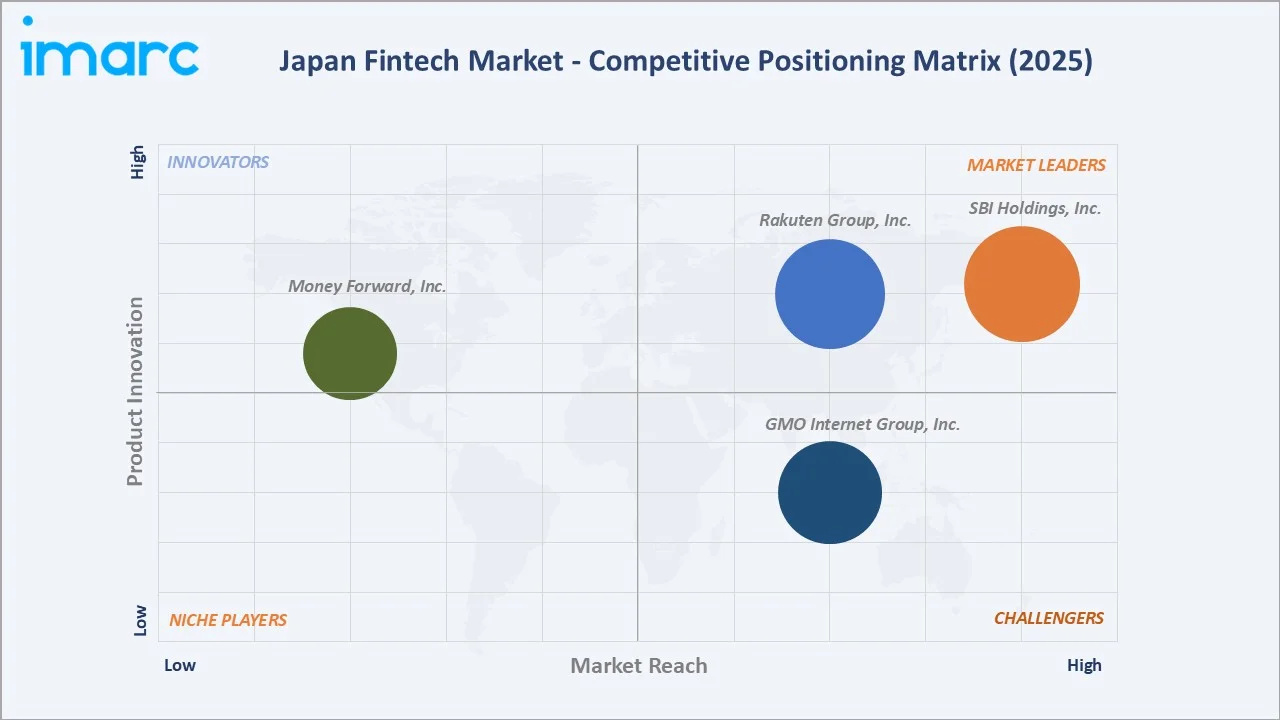

Competitive Landscape

The Japan fintech market's competitive landscape is moderately concentrated with three distinct competitive tiers: large diversified financial conglomerates with captive fintech operations, technology-enabled financial infrastructure specialists, and emerging pure-play fintech platforms with vertical-specific market positions competing across payment, lending, and wealth management segments.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

SBI Holdings, Inc. |

SBI Neo Banking System, SBI FinTech Solutions |

Market Leader |

Diversified financial conglomerate integrating blockchain, digital banking, and cryptocurrency services across Japan |

|

Rakuten Group, Inc. |

Rakuten Pay App, Rakuten Edy, Rakuten Check, Rakuten Card, Rakuten Bank, Rakuten Wallet |

Market Leader |

Ecosystem-driven fintech leveraging Japan's largest loyalty platform for payments, banking, and investment services |

|

GMO Internet Group, Inc. |

GMO Aozora Net Bank, GMO Payment Gateway |

Strong Challenger |

Internet-native financial infrastructure specialist providing BaaS platforms, digital assets, and payment processing |

|

Money Forward, Inc. |

Money Forward Cloud, Money Forward ME |

Emerging Leader |

Leading SaaS platform for personal and business financial management with AI-driven accounting and analytics |

Key players include SBI Holdings, Inc., Rakuten Group, Inc., GMO Internet Group, Inc., Money Forward, Inc., and others.

Key Company Profiles

SBI Holdings, Inc.

SBI Holdings, Inc. is a Tokyo-based diversified financial services conglomerate with a dominant presence in Japan's fintech market through integrated digital banking, blockchain infrastructure, cryptocurrency trading, and cross-border payment operations spanning retail, institutional, and venture capital financial service segments.

- Key Products: SBI Neo Banking System, SBI FinTech Solutions

- Recent Developments: In November 2025, SBI Holdings agreed with the Global Finance & Technology Network (GFTN), an organization established by the Monetary Authority of Singapore (MAS), to establish a joint venture fund focused on investing in global growth-stage fintech companies and related technology sectors.

- Strategic Focus: Expanding an integrated digital finance ecosystem combining cryptocurrency, open banking, robo-advisory, and cross-border payment capabilities within a single conglomerate fintech platform targeting retail and institutional segments.

Rakuten Group, Inc.

Rakuten Group, Inc. is a Tokyo-based digital commerce and services conglomerate operating one of Japan's most expansive consumers fintech ecosystems through integrated payments, digital banking, investment, and insurance services connected by Japan's largest customer loyalty programme.

- Key Products: Rakuten Pay App, Rakuten Edy, Rakuten Check, Rakuten Card, Rakuten Bank, Rakuten Wallet

- Strategic Focus: Deepening financial service integration within the Rakuten ecosystem, leveraging cross-selling opportunities between e-commerce, travel, content, and financial service divisions to drive fintech product adoption and increase average revenue per user.

Market Concentration Analysis

The Japan fintech market is moderately concentrated at the platform ecosystem tier, with the top 2-3 key players collectively commanding an estimated 25-35% of consumer fintech revenue through their multi-product financial ecosystems.

Pure-play fintech platforms hold strong positions in their respective verticals of financial management SaaS and accounting software, operating at smaller revenue scales compared to conglomerate-backed fintech ecosystems. Market concentration is declining at the application layer as vertical fintech specialists gain traction across payments, insurtech, and wealth management segments.

Investment & Growth Opportunities

Highest Growth Segments

Cloud-based deployment at approximately 15.2% CAGR, AI technology at approximately 16.8% CAGR, Blockchain at approximately 17.4% CAGR, CBDC infrastructure, BaaS platforms, AI-powered wealth management, and embedded finance solutions represent the highest-growth investment vectors in Japan's fintech market through 2034. Japan's aging population and large household savings pool create a particularly large addressable market for AI-driven personalized financial planning.

Emerging Investment Opportunities

Cross-border payment fintech represents a high-value emerging opportunity, as Japan's large outbound and inbound remittance market, combined with growing inbound tourism and foreign worker populations, creates structural demand for real-time, low-cost international payment solutions. Blockchain-based stablecoin and CBDC payment infrastructure represents the most structurally transformative fintech investment theme through 2034.

Investment Themes

- AI-native financial services platform investment capturing Japan's large institutional AI deployment cycle: Japan's three mega-banks are each investing significant capital in AI-driven core banking, risk, and compliance transformation. AI fintech platforms providing modular, API-accessible AI capabilities represent high-value enterprise technology investments with recurring SaaS revenue structures and long institutional contract durations.

- Open banking API infrastructure investment capturing the BaaS market enabled by Japan's open banking mandate: Japan's open banking API framework creates a structural BaaS market where regulated deposit-taking institutions expose banking capabilities to non-bank fintech applicants. BaaS platform operators providing FSA-compliant banking infrastructure as a cloud service represent a structurally defensible investment category with growing demand.

Future Market Outlook (2026-2034)

The Japan fintech market is projected to grow from USD 10.52 Billion in 2025 to USD 32.63 Billion by 2034, delivering a 13.0% CAGR over the forecast period. The market reaches approximately USD 19.38 Billion by 2030, representing Japan's fintech industry at its most transformative commercial inflection, with CBDC pilots transitioning to commercial deployment and embedded finance achieving mainstream consumer and institutional adoption.

Three structural forces define Japan fintech market growth through 2034. The regulatory innovation cycle under FSA's fintech promotion strategy creates a continuously expanding addressable market for new financial technology categories including CBDC, digital securities, and programmable finance applications. The demographic-driven demand shift from branch-based to digital-first financial services creates compounding adoption tailwinds as digitally native generations represent a growing share of Japan's financial services consumers.

The enterprise AI investment super-cycle creates a multi-year technology procurement expansion as Japan's financial institutions allocate growing portions of their technology budgets to AI-enabled financial intelligence platforms, automated compliance systems, and AI-driven customer experience transformation programmes targeting retail banking, wealth management, and insurance service delivery.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50 or more industry stakeholders in 2025, including Chief Digital Officers of major Japanese banks, fintech startup Chief Executive Officers, FSA-regulated payment institution executives, AI platform technology leads, and open banking API integration specialists operating across Japan's financial services ecosystem.

Secondary Research

Secondary research encompassed company annual reports, Bank of Japan digital finance reports, FSA fintech regulatory guidance documents, Japan Fintech Association market surveys, METI digital economy statistics, IMF and World Bank Japan financial sector assessments, and over 60 secondary industry sources reviewed to develop comprehensive market intelligence.

Forecasting Models

Market revenue forecasts were developed using a bottom-up segment construction model incorporating technology segment revenue forecasts by deployment mode and technology category, regional revenue allocation based on financial institution concentration and digital payment infrastructure maturity, and competitive pricing dynamics and platform monetization model adjustments for the 2026-2034 forecast period.

Japan Fintech Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Deployment Modes Covered | On-premises, Cloud-based |

| Technologies Covered | Application Programming Interface, Artificial Intelligence, Blockchain, Robotic Process Automation, Data Analytics, Others |

| Applications Covered | Payment and Fund Transfer, Loans, Insurance and Personal Finance, Wealth Management, Others |

| End Users Covered | Banking, Insurance, Securities, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | SBI Holdings, Inc., Rakuten Group, Inc., GMO Internet Group, Inc., Money Forward, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan fintech market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan fintech market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan fintech industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Fintech Market Report

The Japan fintech market reached USD 10.52 Billion in 2025, driven by cloud-based deployment leading at 64.2%, Artificial Intelligence technology at 24.6%, and the Kanto Region commanding 37.3% of total market share through Tokyo's concentration of fintech startups, major financial institutions, and venture capital investment infrastructure.

The Japan fintech market grows at 13.0% CAGR during 2026-2034, reaching USD 32.63 Billion by 2034. This growth reflects digital payment expansion, AI integration across banking and insurance, API-enabled open banking proliferation, government cashless society initiatives, and increasing cross-border payment and remittance service demand nationally.

Cloud-based deployment leads at 64.2%, reflecting fintech firms' preference for scalable, cost-efficient, and rapidly deployable cloud infrastructure over legacy on-premises architectures. Major cloud platform providers support FSA-compliant fintech workloads with data residency and enterprise security frameworks suited to Japan's regulated financial services environment.

Artificial Intelligence leads at 24.6%, enabling fraud detection, credit scoring, robo-advisory wealth management, and personalized financial service delivery across banking, insurance, and capital markets. AI's broad cross-sector applicability makes it the highest-priority technology investment for Japan's financial institutions and fintech platform operators.

The Kanto Region leads at 37.3%, anchored by Tokyo's position as Japan's financial capital. The region hosts the headquarters of Japan's three mega-banks, the Tokyo Stock Exchange, major global financial institution branches, the highest density of fintech venture capital investment, and Japan's largest concentration of fintech startup accelerator programmes.

Leading companies include SBI Holdings, Inc., Rakuten Group, Inc., GMO Internet Group, Inc., Money Forward, Inc., and others.

The Japan fintech market is projected to reach approximately USD 19.38 Billion by 2030, with CBDC programmes advancing toward commercial deployment, embedded finance achieving mainstream adoption across Japan's major e-commerce and retail conglomerates, and AI-powered wealth management platforms scaling across Japan's large retail investment market.

Key investment opportunities include AI-native financial services platforms, cross-border payment and stablecoin infrastructure, CBDC-adjacent technology providers, Banking-as-a-Service platform operators, embedded finance enablers for non-financial corporates, and cloud-native lending and insurtech platforms targeting Japan's large SME and retail consumer financial services markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)