Japan Foreign Exchange Market Size, Share, Trends and Forecast by Counterparty, Type, and Region, 2026-2034

Japan Foreign Exchange Market Size, Share, Trends & Forecast (2026-2034)

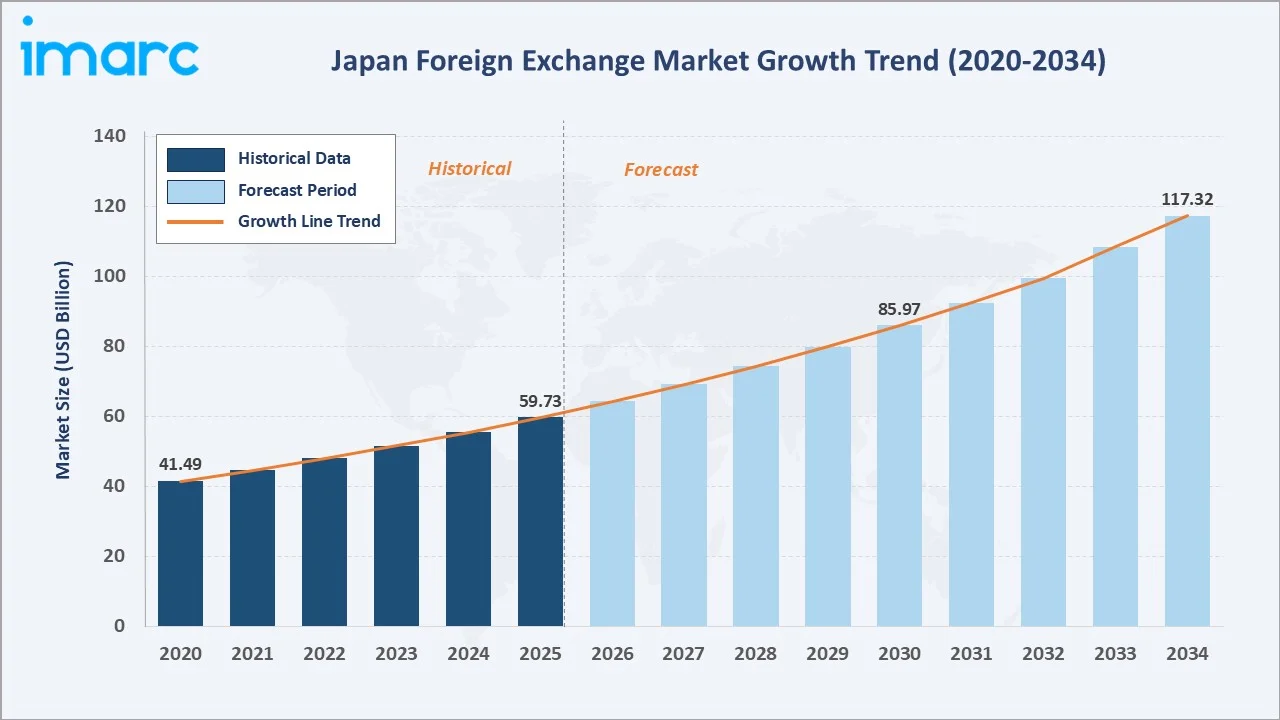

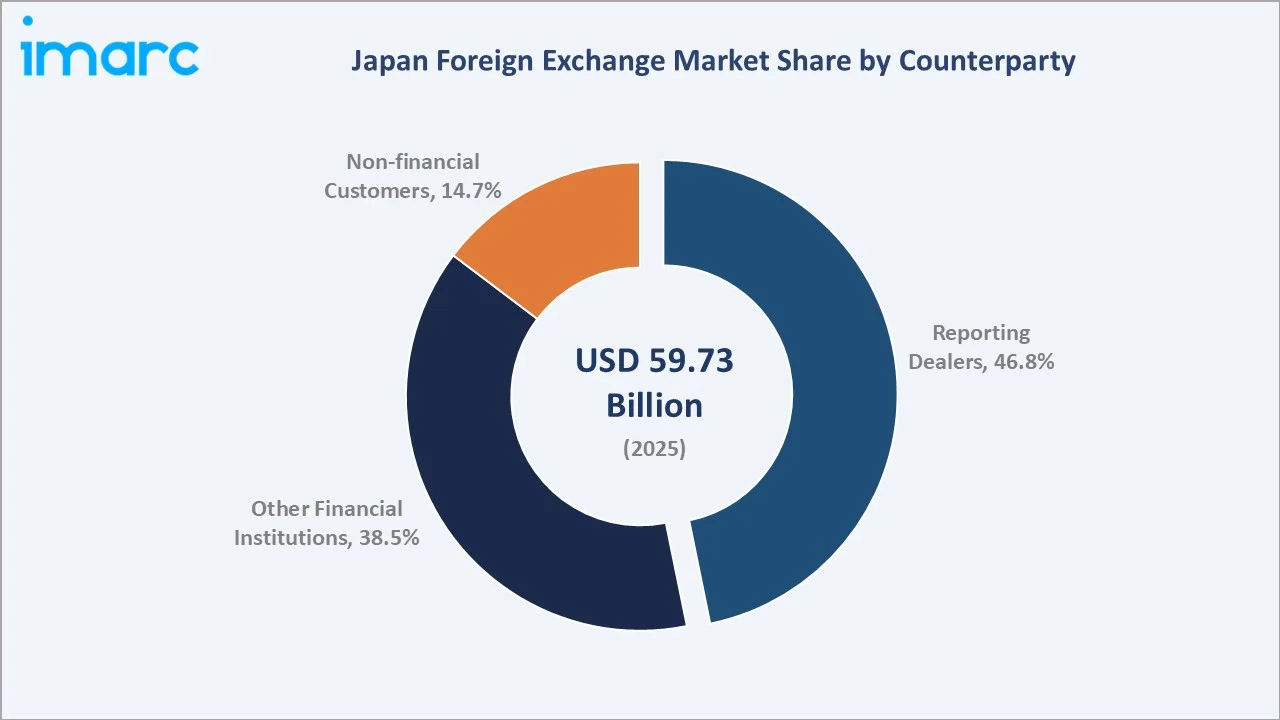

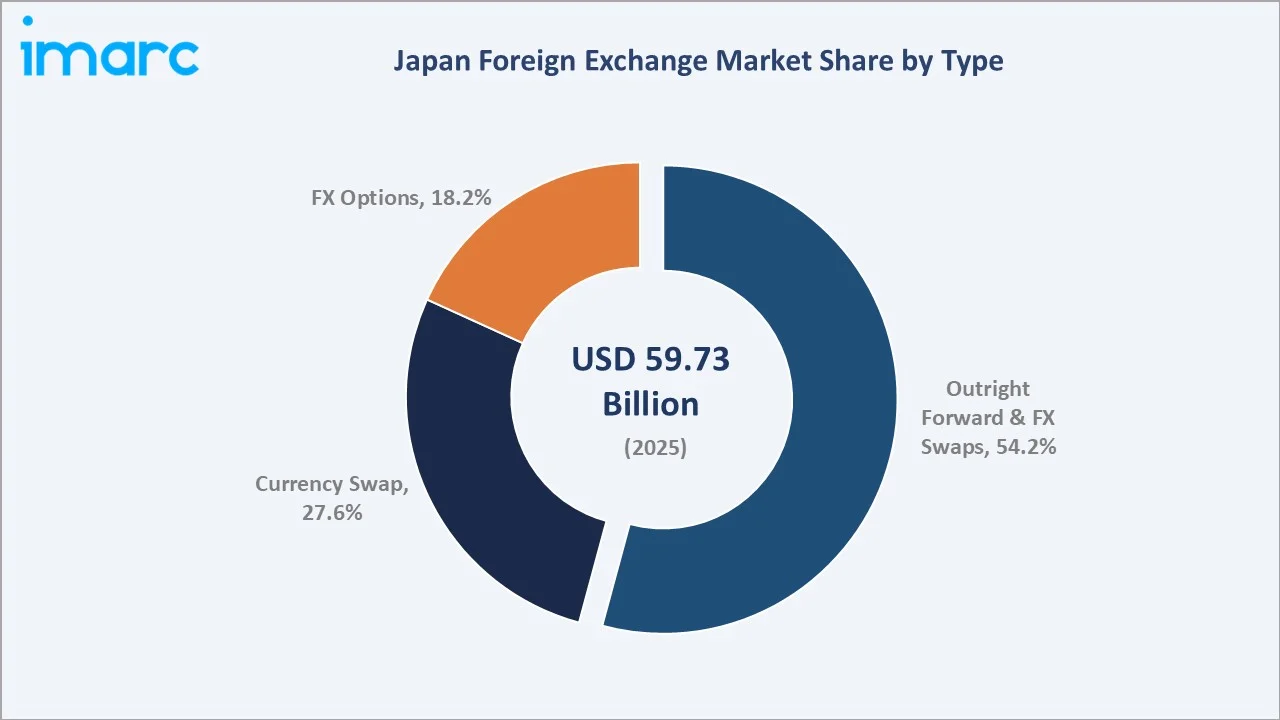

The Japan foreign exchange market size was valued at USD 59.73 Billion in 2025 and is projected to reach USD 117.32 Billion by 2034, exhibiting a CAGR of 7.56% during 2026-2034. Heightened yen volatility, expanding cross-border trade settlement, faster electronic platform adoption, and rising hedging demand from corporate and institutional investors are collectively driving market growth. Reporting Dealers account for 46.8% of trading flow in 2025, while Outright Forwards and foreign exchange Swaps lead the instrument mix at 54.2%. The Kanto region, anchored by Tokyo, commands the largest regional share at 39.6% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 59.73 Billion |

|

Forecast Market Size (2034) |

USD 117.32 Billion |

|

CAGR (2026-2034) |

7.56% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (39.6% share, 2025) |

|

Fastest Growing Region |

Kinki Region |

|

Leading Counterparty |

Reporting Dealers (46.8%, 2025) |

|

Leading Type |

Outright Forward & FX Swaps (54.2%, 2025) |

The chart below tracks Japan foreign exchange market growth from 2020-2034, capturing post-pandemic recovery and structural demand from yen volatility, cross-border investment flows, and corporate hedging activity.

To get more information on this market, Request Sample

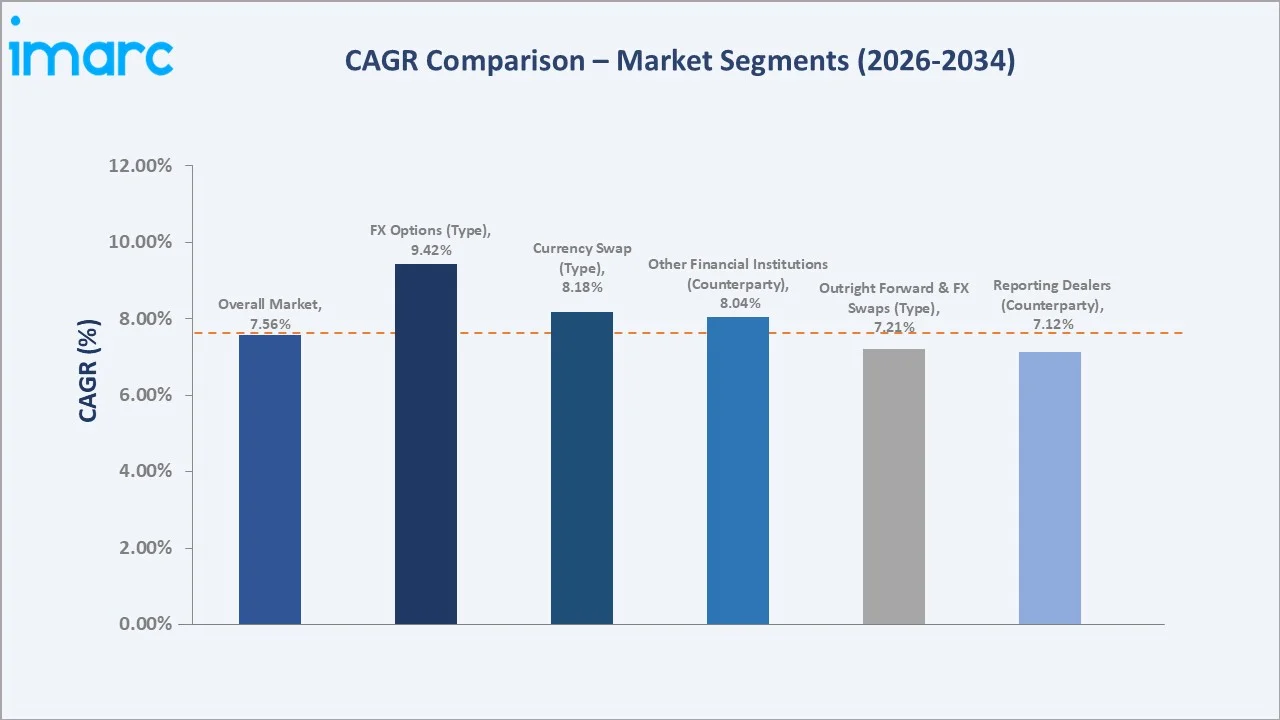

CAGR analysis identifies foreign exchange Options and Currency Swap instruments as the fastest-growing segments through 2034, reflecting deeper hedging needs from Japanese corporates and rising institutional demand for tail-risk protection.

Executive Summary

The Japan foreign exchange market is being reshaped by structural yen volatility, electronic platform consolidation, and broader institutional adoption of derivative hedging. Valued at USD 59.73 Billion in 2025, the market is projected to reach USD 117.32 Billion by 2034 at a CAGR of 7.56%. Tokyo is among the top global foreign exchange trading centres but now ranks outside the top four, behind London, New York, Singapore, and Hong Kong.

Reporting Dealers lead the counterparty mix with a 46.8% share in 2025, supported by major Japanese banks including MUFG Bank, Mizuho Bank, and SMBC, alongside global investment banks operating in Tokyo. Other Financial Institutions contribute 38.5%, reflecting growing foreign exchange activity from asset managers, pension funds, and life insurers such as Japan Post Insurance and Nippon Life. Non-financial Customers account for 14.7%, driven by exporters, importers, and multinationals managing yen exposure.

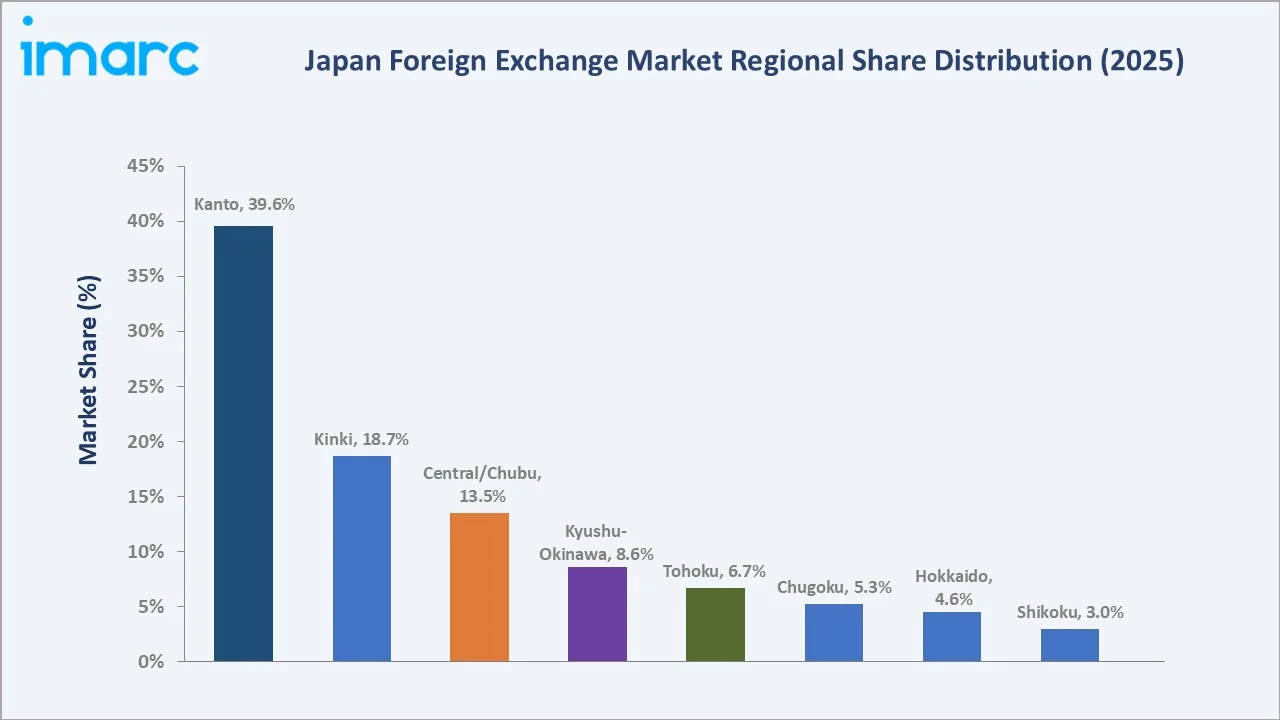

Outright Forwards and foreign exchange Swaps dominate the type of segment with a 54.2% share in 2025, largely due to short-dated funding swaps used by Japanese banks to source US dollar liquidity. Currency Swaps follow at 27.6%, while foreign exchange Options account for 18.2% as volatility-driven hedging gains traction. Regionally, Kanto leads with 39.6% in 2025, anchored by Tokyo's institutional concentration, followed by Kinki at 18.7% and Central/Chubu at 13.5%.

Key Market Insights

|

Insight |

Data |

|

Largest Counterparty Segment |

Reporting Dealers - 46.8% (2025) |

|

Second Counterparty Segment |

Other Financial Institutions - 38.5% share (2025) |

|

Leading Type Segment |

Outright Forward & FX Swaps - 54.2% share (2025) |

|

Leading Region |

Kanto Region - 39.6% (2025) |

|

Second Region |

Kinki Region - 18.7% (2025) |

|

Top Companies |

MUFG Bank, Ltd., Mizuho Bank, Ltd., SMBC Group, and Nomura Holdings, Inc. |

Key Analytical Observations Supporting the Above Data:

- Reporting Dealers' 46.8% dominance in 2025 reflects the central role of major Japanese banks and global investment banks in providing two-way liquidity, with MUFG, Mizuho, and SMBC handling the bulk of interbank flow.

- Other Financial Institutions at 38.5% in 2025 represent rising foreign exchange activity from asset managers, pension funds, life insurers, and hedge funds, particularly in cross-border yen carry trades and portfolio hedging.

- Outright Forwards and foreign exchange Swaps at 54.2% in 2025 reflect heavy short-dated swap usage by Japanese banks for USD funding, given the yen's role as a major funding currency in global carry strategies.

- Currency Swaps at 27.6% in 2025 are driven by long-dated cross-currency hedging from Japanese life insurers hold around JPY 100 trillion (USD 691 billion) in foreign securities.

- Kanto's 39.6% lead is anchored by Tokyo's status as Japan's primary financial center, hosting the headquarters of major banks, the Bank of Japan, and the Tokyo foreign exchange Market Committee.

Japan Foreign Exchange Market Overview

The Japan foreign exchange market encompasses trading in Japanese yen and other global currencies through instruments such as spot, forwards, swaps, and options. It involves a network of reporting dealers, central authorities like the Bank of Japan, regulators including the Financial Services Agency and Ministry of Finance, electronic platforms such as EBS and Refinitiv FX all, and settlement systems like CLS Bank that help reduce settlement risk.

Applications span trade settlement, capital flow management, portfolio hedging, speculation, and monetary policy operations. Demand is reinforced by rising cross-border M&A activity, sustained yen carry trade flows, BOJ policy normalization, and expanding electronic execution that improves price transparency for both institutional and corporate end users.

Market Dynamics

To evaluate market opportunities, Request Sample

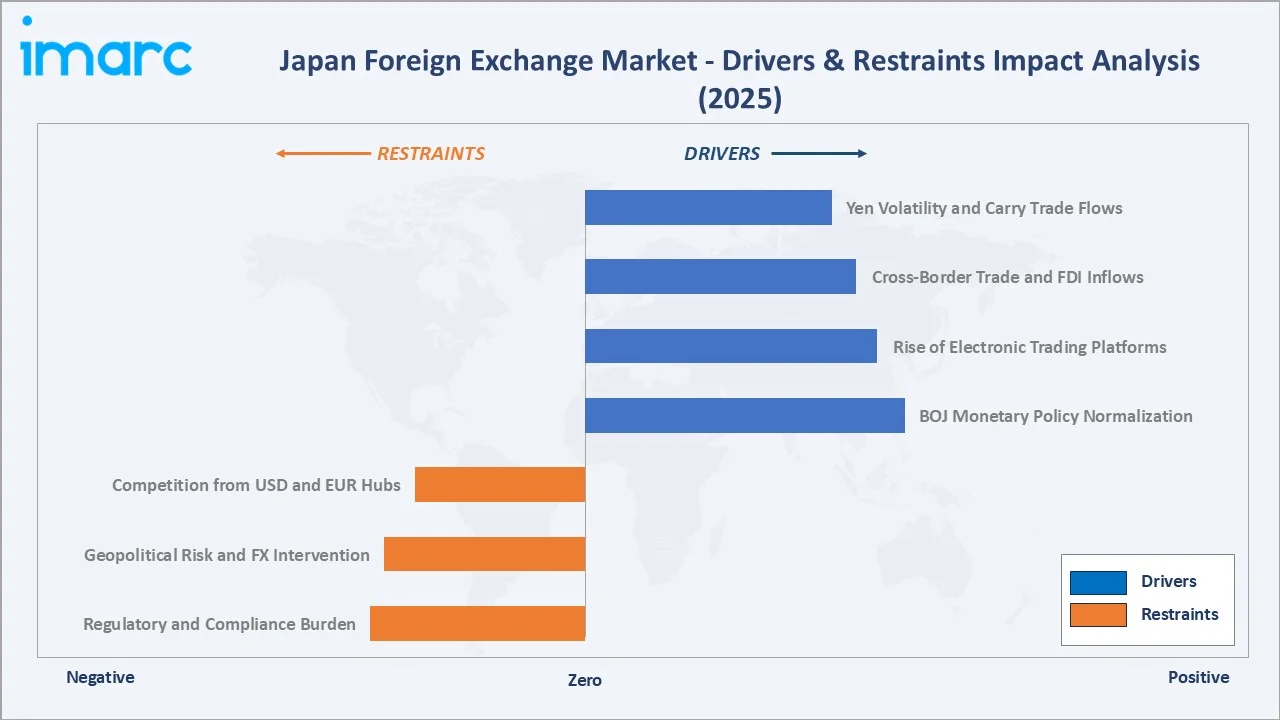

Market Drivers

- Yen Volatility and Carry Trade Flows: Persistent USD/JPY volatility, with the yen weakening past the 150 level on multiple occasions in 2024-2025, has significantly increased hedging demand from Japanese exporters, importers, and offshore investors deploying yen-funded carry trades.

- Cross-Border Trade and FDI Inflows: Japan’s total goods trade (exports + imports) in 2023 was about USD 1.50 trillion, while inbound and outbound FDI flows remain robust, supporting continuous demand for spot, forward, and swap transactions across major currency pairs including USD/JPY, EUR/JPY, and AUD/JPY.

- Rise of Electronic Trading Platforms: Electronic execution via EBS, Refinitiv FXall, single-dealer platforms operated by MUFG, Mizuho, and SMBC, and aggregator venues now accounts for most of the foreign exchange volume, lowering transaction costs and expanding access for mid-tier institutions.

- BOJ Monetary Policy Normalization: The Bank of Japan's exit from negative interest rates in March 2024 and gradual policy tightening have introduced new yield differentials, attracting heightened foreign exchange market activity as participants reposition portfolios and recalibrate hedging strategies.

Market Restraints

- Regulatory and Compliance Burden: Stringent oversight from the Financial Services Agency, including margin requirements for non-cleared derivatives and Best Execution rules, increases operational costs for foreign exchange dealers and may limit participation by smaller firms.

- Geopolitical Risk and FX Intervention: Japan’s Ministry of Finance Japan intervened multiple times to support the yen, creating episodic volatility that complicates risk management for dealers and end users.

- Competition from USD and EUR Hubs: London and New York continue to dominate global foreign exchange volumes, capturing roughly 38% and 19% respectively per BIS Triennial Survey, which constrains Tokyo's share of global yen trading despite local advantages.

Market Opportunities

- Foreign Exchange Options and Volatility Products: With yen realized volatility elevated, demand for vanilla and structured foreign exchange options is expanding among Japanese corporate and institutional investors, supporting growth in the highest-margin segment of the foreign exchange value chain.

- CLS Settlement and T+1 Migration: Adoption of CLS multilateral netting and the global migration toward T+1 settlement create operational opportunities for Japanese dealers to enhance liquidity provision and reduce settlement risk on yen-denominated trades.

- Algorithmic and AI-Driven Execution: Japanese banks are deploying machine-learning algorithms for order routing and liquidity aggregation, mirroring practices at global peers; this opens scope for proprietary execution products targeted at Japanese institutional clients.

Market Challenges

- Yen Funding Stress and USD Liquidity Gaps: Persistent USD funding pressure for Japanese banks, visible in cross-currency basis spreads, raises hedging costs and creates periodic liquidity strain, particularly around fiscal year-end and quarter-end reporting dates.

- Cyber and Operational Resilience Risk: Growing reliance on electronic platforms has elevated cyber risk; the FSA has intensified supervisory expectations on incident reporting and operational resilience for foreign exchange market infrastructure providers.

- Talent and Quant Capability Gap: Japanese banks face structural shortages of quantitative and electronic trading talent versus global peers, slowing the rollout of advanced algorithmic and AI-driven foreign exchange products in domestic markets.

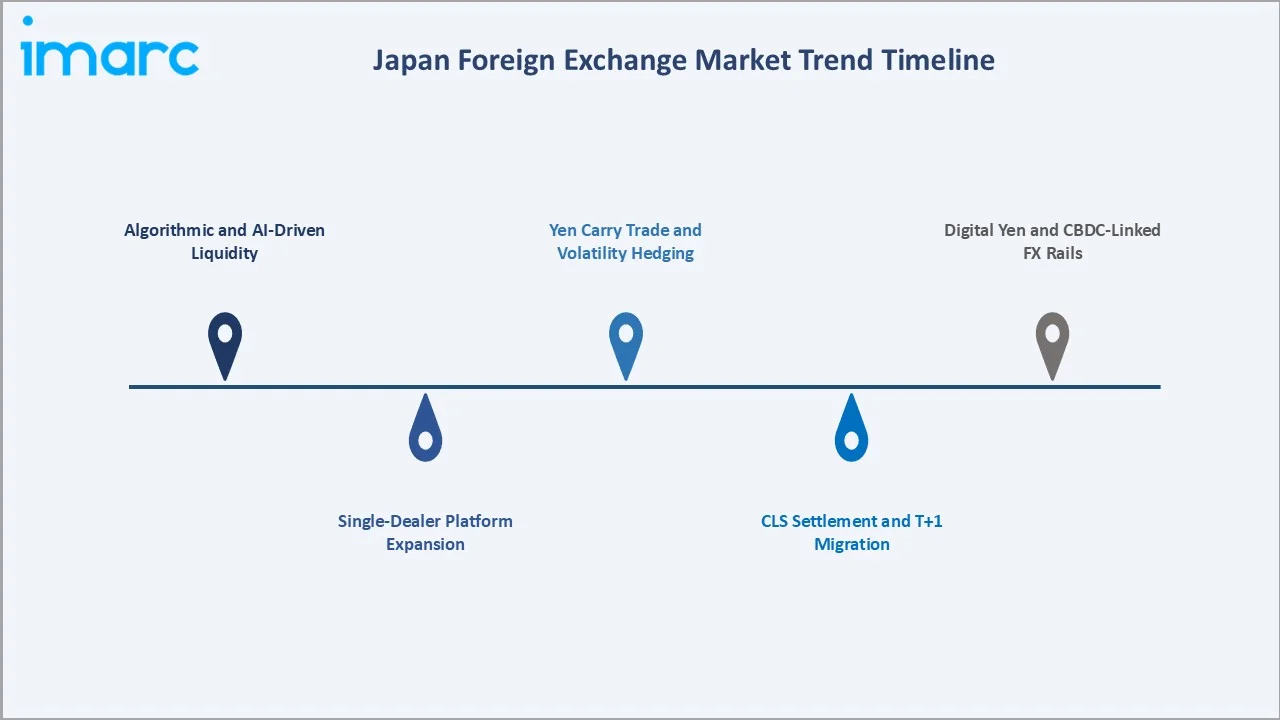

Emerging Market Trends

1. Algorithmic and AI-Driven Liquidity

Japanese banks are accelerating algorithmic execution and AI-based price formation. MUFG, Mizuho, and SMBC have all expanded e-FX desks, deploying machine-learning models to optimize spread, internalize flow, and reduce reliance on third-party liquidity providers.

2. Single-Dealer Platform Expansion

Single-dealer platforms operated by major Japanese banks now offer real-time pricing, post-trade analytics, and integrated risk management. These platforms increasingly compete with multi-dealer venues, capturing flow from corporates seeking customized execution.

3. CLS Settlement and T+1 Migration

CLS Bank settles a substantial share of yen foreign exchange volumes, mitigating Herstatt risk. With major markets moving to T+1 securities settlement, Japanese foreign exchange desks are upgrading post-trade infrastructure to ensure timely matching, confirmation, and funding.

4. Yen Carry Trade and Volatility Hedging

Interest rate differentials continue to support yen carry trades, while periodic unwind episodes have increased volatility, boosting demand for foreign exchange options and hedging strategies.

5. Digital Yen and CBDC-Linked Foreign Exchange Rails

The Bank of Japan's ongoing CBDC pilots could reshape long-term foreign exchange settlement architecture. Cross-border CBDC initiatives such as Project Agorá involve the BOJ and may eventually enable atomic foreign exchange settlement, reducing intraday liquidity needs.

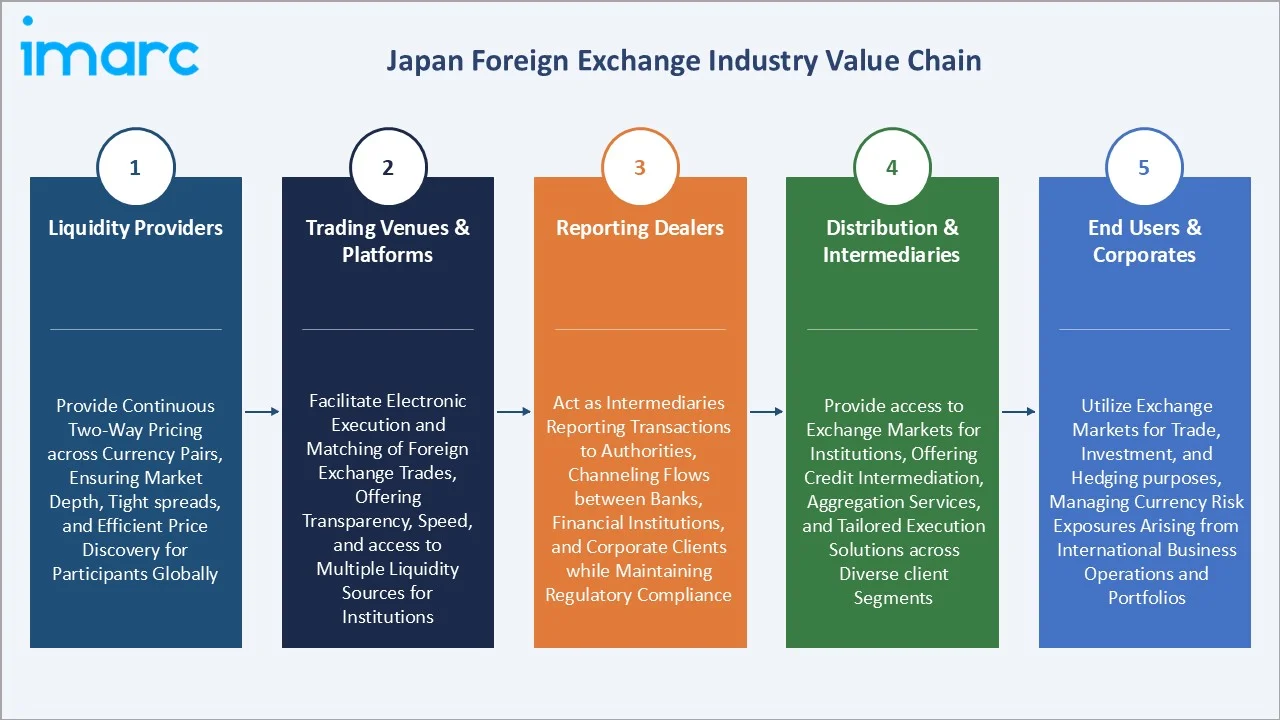

Industry Value Chain Analysis

The Japan foreign exchange value chain spans five stages, from liquidity provision to end-user execution, with each stage carrying distinct margin profiles, regulatory obligations, and competitive dynamics.

|

Stage |

Key Players / Examples |

|

Liquidity Providers |

Provide continuous two way pricing across currency pairs, ensuring market depth, tight spreads, and efficient price discovery for participants globally. |

|

Trading Venues & Platforms |

Facilitate electronic execution and matching of foreign exchange trades, offering transparency, speed, and access to multiple liquidity sources for institutions. |

|

Reporting Dealers |

Act as intermediaries reporting transactions to authorities, channeling flows between banks, financial institutions, and corporate clients while maintaining regulatory compliance. |

|

Distribution & Intermediaries |

Provide access to exchange markets for institutions, offering credit intermediation, aggregation services, and tailored execution solutions across diverse client segments |

|

End Users & Corporates |

Utilize exchange markets for trade, investment, and hedging purposes, managing currency risk exposures arising from international business operations and portfolios |

Reporting dealers capture the largest revenue share through bid-ask spread and balance-sheet financing, while platforms generate fees and brokerage. Settlement infrastructure providers operate on tight margins but underpin the entire ecosystem's risk profile.

Technology Landscape in the Japan Foreign Exchange Industry

Electronic Execution Infrastructure

Japan's foreign exchange market relies on a layered electronic execution stack including EBS Market for spot interbank, Refinitiv FXall and Bloomberg FXGO for institutional RFQ, and proprietary single-dealer platforms operated by MUFG, Mizuho, and SMBC, each offering algorithmic order types and pre-trade analytics.

Algorithmic Trading and AI

Japanese dealers are scaling AI-driven liquidity and execution algorithms. Machine-learning models optimize internalization rates, predict short-term price moves, and reduce market impact, narrowing the gap with global e-FX leaders.

Settlement and Clearing

CLS Bank provides multilateral netting for yen foreign exchange trades, reducing settlement risk substantially. Japan's clearing infrastructure also includes JSCC for OTC interest-rate derivatives and is being upgraded to support T+1 timelines for global cross-asset alignment.

Cybersecurity and Resilience

FSA-mandated operational resilience standards have prompted Japanese banks to implement zero-trust architecture, real-time anomaly detection, and tabletop incident exercises, given the systemic importance of foreign exchange market infrastructure to global yen liquidity.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Outright Forward and FX Swaps |

54.2% |

2025 |

|

Counterparty |

Reporting Dealers |

46.8% |

2025 |

|

Region |

Kanto Region |

39.6% |

2025 |

By Counterparty

Reporting dealers account for 46.8% of the Japan foreign exchange market in 2025, broadly aligned with BIS evidence showing dealer-to-dealer activity forms a major share of foreign exchange turnover, with large banks and securities firms acting as core liquidity providers across spot, forward, swap, and derivatives markets.

To access detailed market analysis, Request Sample

Other financial institutions contribute 38.5% in 2025, reflecting growing activity from asset managers, hedge funds, life insurers including Nippon Life and Japan Post Insurance, and pension funds such as GPIF. Non-financial customers represent 14.7%, encompassing exporters, importers, multinational corporates, and a sizable retail margin foreign exchange community.

By Type

Outright forwards and foreign exchange Swaps lead the type of segment at 54.2% in 2025, driven by short-dated USD funding swaps used by Japanese banks and by corporate forwards hedging trade receivables and payables. The yen's role as a major funding currency reinforces this dominance.

Currency swaps account for 27.6% in 2025, reflecting long-dated cross-currency hedging by Japanese life insurers and pension funds managing foreign bond holdings exceeding USD 2 trillion. Foreign exchange options hold 18.2%, fueled by elevated yen volatility, structured product issuance, and growing demand for tail-risk hedging instruments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

39.6% |

Tokyo financial hub, headquarters of MUFG, Mizuho, SMBC; concentration of BOJ, FSA, MOF; majority of e-foreign exchange volume |

|

Kinki Region |

18.7% |

Osaka manufacturing exporters (Panasonic, Daikin); regional banking hubs; trade-led foreign exchange hedging demand |

|

Central/Chubu Region |

13.5% |

Nagoya auto export cluster (Toyota, Denso, Aisin); strong corporate foreign exchange hedging; supplier-network treasury operations |

|

Kyushu-Okinawa Region |

8.6% |

Semiconductor and tourism flows; Fukuoka regional bank growth; expanding cross-border ASEAN trade settlement |

|

Tohoku Region |

6.7% |

Reconstruction-linked FDI flows, agri-export hedging, regional bank consolidation supporting foreign exchange product expansion |

|

Chugoku Region |

5.3% |

Hiroshima auto and steel exports; Mazda treasury hedging activity; mid-size corporate forward usage |

|

Hokkaido Region |

4.6% |

Tourism and food exports to Asia; Sapporo financial services; growing cross-border e-commerce flows |

|

Shikoku Region |

3.0% |

Mid-sized exporters, regional bank foreign exchange desks, specialty manufacturing hedging needs across Tokushima and Ehime |

Kanto commands a 39.6% share in 2025, reflecting Tokyo's status as Japan's primary financial center and home to the Bank of Japan, the Tokyo Foreign Exchange Market Committee, the headquarters of MUFG, Mizuho, and SMBC, and the Japanese branches of all major global investment banks.

Kinki at 18.7% is anchored by Osaka's manufacturing exporter base, while Central/Chubu at 13.5% benefits from Nagoya's automotive cluster. Kyushu-Okinawa (8.6%), Tohoku (6.7%), Chugoku (5.3%), Hokkaido (4.6%), and Shikoku (3.0%) collectively reflect Japan's geographically distributed industrial base and regional banking depth.

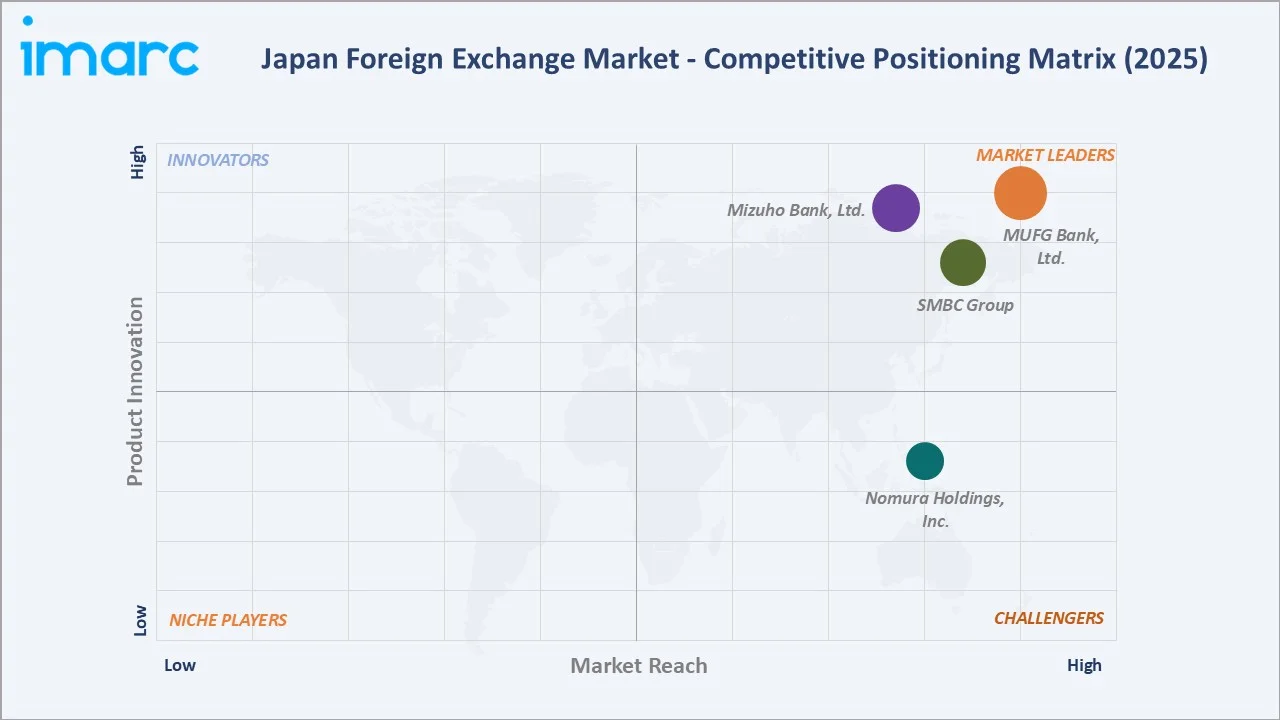

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

MUFG Bank, Ltd. |

MUFG |

Leader |

Largest Japanese FX flow franchise, deep yen liquidity, global branch network |

|

Mizuho Bank, Ltd. |

Mizuho e-FX |

Leader |

Strong corporate client base, integrated treasury solutions, e-FX scale |

|

SMBC Group |

SMBC FX |

Leader |

Cross-border trade finance integration, expanding APAC footprint |

|

Nomura Holdings, Inc. |

Nomura FX |

Challenger |

Securities-linked FX, structured products |

The Japan foreign exchange market is led by MUFG Bank, Ltd., Mizuho Bank, Ltd., and SMBC Group, with strong international competition from JP Morgan Chase, Citibank, Goldman Sachs, and Deutsche Bank. MUFG reported FY2023 group net income exceeding Yen 1,490.7 Bn, with its global markets business contributing meaningfully to foreign exchange flow.

Key Company Profiles

MUFG Bank, Ltd.

MUFG Bank, headquartered in Tokyo, is the core banking arm of Mitsubishi UFJ Financial Group, one of the world’s largest financial groups. It is a leading FX liquidity provider in Japan, supported by global operations, strong corporate relationships, and advanced electronic trading capabilities.

- Product & Service Portfolio: MUFG provides comprehensive FX services including spot, forwards, swaps, and options, supported by electronic trading platforms, structured hedging solutions, and global liquidity distribution through its corporate and institutional banking network.

- Latest Recent Developments: In 2025, MUFG was awarded “FX House of the Year – Japan” at the FX Markets Asia Awards 2025, recognizing its strong domestic FX franchise and growing electronic trading capabilities. In 2023, MUFG announced its FX collaboration with Morgan Stanley under the “Alliance 2.0” initiative, enabling integration of trading capabilities and use of Morgan Stanley’s advanced FX technology and infrastructure to enhance execution and client services.

- Strategic Focus: MUFG is focused on scaling its global FX franchise by enhancing electronic trading capabilities, leveraging the Morgan Stanley alliance, and strengthening yen and Asian currency liquidity for institutional and corporate clients.

Mizuho Bank, Ltd.

Mizuho Bank, headquartered in Tokyo, is a core subsidiary of Mizuho Financial Group and one of Japan’s three megabanks. It maintains a strong global FX presence, supported by corporate banking relationships, international network coverage, and ongoing investment in electronic trading infrastructure.

- Product & Service Portfolio: Mizuho provides FX products including spot, forwards, swaps, and options, delivered through electronic trading platforms and multi-dealer connectivity, alongside structured hedging and treasury solutions for corporate and institutional clients globally.

- Latest Recent Developments: In 2025, Mizuho Bank joined the Singapore Exchange’s FX platform (SGX FX) as a liquidity provider, beginning price streaming in June 2025. This move strengthens its electronic FX distribution across Asia, improves institutional client access to diversified liquidity pools, and enhances its role in regional FX market-making as electronification accelerates.

- Strategic Focus: Mizuho is focused on expanding its electronic FX capabilities, strengthening Asian market liquidity distribution, and enhancing client-centric treasury solutions through advanced pricing technology and global platform integration.

SMBC Group

Sumitomo Mitsui Banking Corporation (SMBC), headquartered in Tokyo, is a core unit of Sumitomo Mitsui Financial Group and one of Japan’s leading megabanks. It maintains a strong global FX presence, supported by international operations, corporate banking relationships, and expanding electronic trading capabilities.

- Product & Service Portfolio: SMBC offers FX products including spot, forwards, swaps, and options, alongside structured hedging, non-deliverable forwards (NDFs), and trade-linked FX solutions delivered through electronic trading platforms and its global corporate and institutional banking network.

- Latest Recent Developments: In 2024, SMBC became the first Japanese megabank to stream FX prices directly to Singapore Exchange (SGX FX) clients and extended connectivity to SGX CurrencyNode, enhancing electronic liquidity distribution. The move deepened Asian currency liquidity, improved institutional access to Japan’s FX markets, and reinforced SMBC’s regional eFX market-making role.

- Strategic Focus: SMBC is focused on expanding its Asia-Pacific electronic FX liquidity footprint, integrating FX with trade finance solutions, and strengthening its global derivatives and swap-dealer capabilities to support increasing outbound investment by Japanese corporates.

Market Concentration Analysis

The Japan foreign exchange market is moderately concentrated. The top three Japanese banks (MUFG Bank, Ltd., Mizuho Bank, Ltd., SMBC Group) together with the Tokyo branches of leading global investment banks account for an estimated 70-75% of reporting-dealer foreign exchange flow in 2025. The remaining share is distributed across mid-tier banks, securities firms, and electronic market makers.

The middle tier includes Nomura, Daiwa, Resona, regional banks such as Bank of Yokohama and Chiba Bank, and Japanese branches of Asian and European banks. These participants compete for niche segments including retail margin foreign exchange, corporate hedging, and structured product distribution.

Consolidation trends include continued integration of Japanese megabanks' securities and foreign exchange operations, alongside global bank rationalization of regional foreign exchange desks. M&A activity in the sector remains modest but partnerships, such as Morgan Stanley MUFG Securities, illustrate the importance of joint platforms for scale economics. Electronic market makers including XTX and Citadel Securities are also expanding their Tokyo footprint, intensifying competition on price.

Investment & Growth Opportunities

Fastest-Growing Segments

Foreign exchange Options represent the fastest-growing instrument segment, supported by elevated yen volatility, growing structured-product issuance, and rising tail-risk hedging demand from Japanese asset managers and corporates. Currency Swaps follow, driven by long-dated foreign-bond hedging by life insurers managing portfolios exceeding USD 2 trillion in aggregate.

Emerging Market Segments

Foreign exchange trading involving Asian currencies, particularly INR, IDR, VND, and offshore CNH, is expanding rapidly as Japanese corporates deepen Indo-Pacific investment. Asian currency pairs against the yen are also gaining liquidity on Tokyo single-dealer platforms, opening commercial opportunities for dealers with regional balance sheet capacity.

Venture & Strategic Investment Trends

Strategic investment is concentrated in e-foreign exchange infrastructure, AI-driven liquidity, and post-trade automation. Japanese megabanks have committed multi-hundred-million-dollar technology programs to upgrade foreign exchange execution stacks, while fintech investment in retail margin foreign exchange continues, with SBI Group and DMM.com Securities expanding mobile-first platforms.

Future Market Outlook (2026-2034)

The Japan foreign exchange market forecast projects sustained value expansion from USD 59.73 Billion in 2025 to USD 117.32 Billion by 2034, growing at a CAGR of 7.56%, representing nearly USD 58 billion in incremental annual revenue. Growth will be driven by continued yen volatility, deeper electronic execution, and expanded hedging by Japanese institutional investors.

Three transformational shifts will reshape the industry through 2034. First, AI-driven execution will become standard, with machine-learning models handling order routing, internalization, and price formation across major Japanese dealers. Second, T+1 foreign exchange settlement and broader CLS adoption will reduce intraday liquidity needs and operational risk. Third, CBDC-linked foreign exchange rails, including BOJ pilots and cross-border initiatives such as Project Agorá, may eventually enable atomic settlement, transforming post-trade economics.

By 2034, the Japan foreign exchange market is expected to evolve into a fully digital, AI-augmented ecosystem combining institutional liquidity, retail margin platforms, and emerging tokenized foreign exchange rails. Dealers investing in e-foreign exchange infrastructure, quantitative talent, and Asian currency depth are positioned to capture the highest-growth segments across institutional, corporate, and retail channels.

Research Methodology

Primary Research

Primary research involved structured interviews and surveys conducted in 2024-2025 with Japan foreign exchange market stakeholders including reporting-dealer trading heads, corporate treasury executives, asset managers, retail brokers, regulators, and electronic platform providers operating across Tokyo, Osaka, and Nagoya.

Secondary Research

Secondary sources include Bank of Japan Tokyo foreign exchange Market Committee turnover surveys, BIS Triennial Central Bank Survey of foreign exchange activity, Financial Services Agency rulemaking, Ministry of Finance intervention disclosures, company annual reports, peer-reviewed publications, and industry trade journals such as Risk.net and foreign exchange Markets.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models, incorporating BOJ turnover trends, BIS global foreign exchange growth, Japanese GDP and trade flows, electronic platform adoption curves, and yen volatility scenarios under base, optimistic, and conservative cases.

Japan Foreign Exchange Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Counterparties Covered | Reporting Dealers, Other Financial Institutions, Non-financial Customers |

| Types Covered | Currency Swap, Outright Forward and FX Swaps, FX Options |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | MUFG Bank, Ltd., Mizuho Bank, Ltd., SMBC Group, Nomura Holdings, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan foreign exchange market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan foreign exchange market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan foreign exchange industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Foreign Exchange Market Report

The Japan foreign exchange market was valued at USD 59.73 Billion in 2025, supported by yen volatility, cross-border trade, electronic execution, and rising hedging demand.

The market is projected to reach USD 117.32 Billion by 2034, expanding at a CAGR of 7.56% during 2026-2034.

Reporting Dealers lead with a 46.8% share in 2025, supported by MUFG Bank, Ltd., Mizuho Bank, Ltd., SMBC Group, and global investment banks operating in Tokyo.

Outright Forwards and foreign exchange Swaps dominate with a 54.2% share in 2025, driven by short-dated USD funding swaps and corporate trade hedging.

The Kanto Region leads with a 39.6% share in 2025, anchored by Tokyo's status as Japan's primary financial and foreign exchange trading center.

Key drivers include yen volatility, cross-border trade, electronic platform adoption, BOJ policy normalization, and rising institutional hedging demand.

Kinki Region is among the fastest growing, supported by Osaka's exporter base, expanding regional banking activity, and corporate foreign exchange hedging needs.

Leading companies include MUFG Bank, Ltd., Mizuho Bank, Ltd., SMBC Group, and Nomura Holdings, Inc.

Foreign exchange Options hold an 18.2% share in 2025, supported by elevated yen volatility, structured product issuance, and rising institutional tail-risk hedging.

Electronic foreign exchange growth is fueled by single-dealer platforms, multi-dealer venues, AI-driven algorithms, and tighter spreads from internalized liquidity.

AI execution, single-dealer platforms, CLS settlement, T+1 migration, and CBDC pilots are transforming Japan foreign exchange into an integrated digital ecosystem.

Reporting dealers and other financial institutions form the largest combined end-user base, while corporates and retail margin investors drive incremental growth.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade