Japan Frozen Foods Market Size, Share, Trends and Forecast by Product Type and Region, 2026-2034

Japan Frozen Foods Market Size, Share, Trends & Forecast (2026-2034)

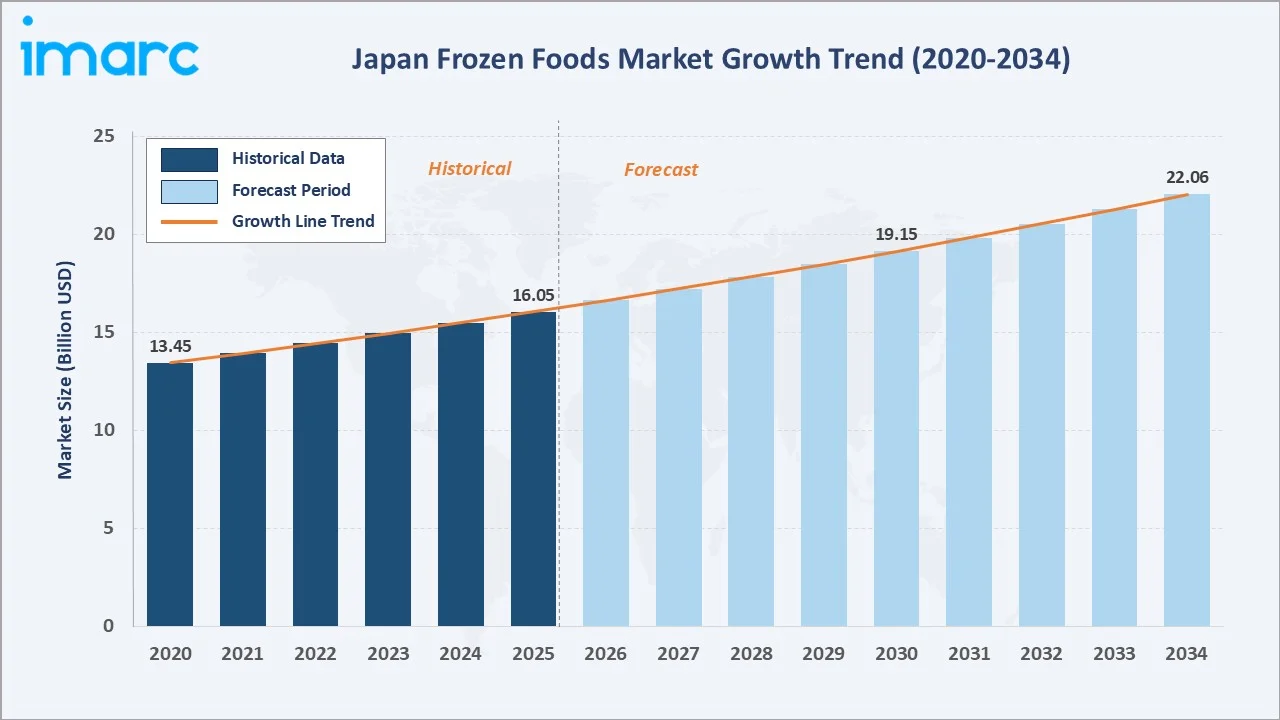

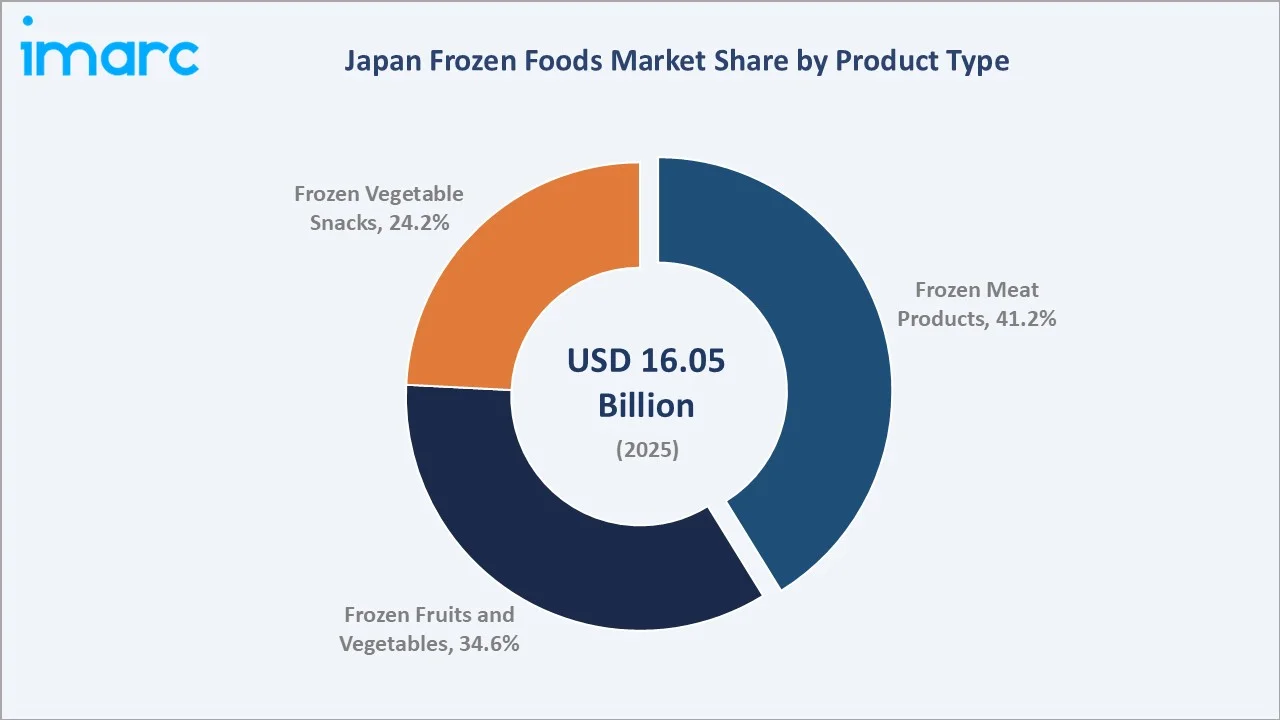

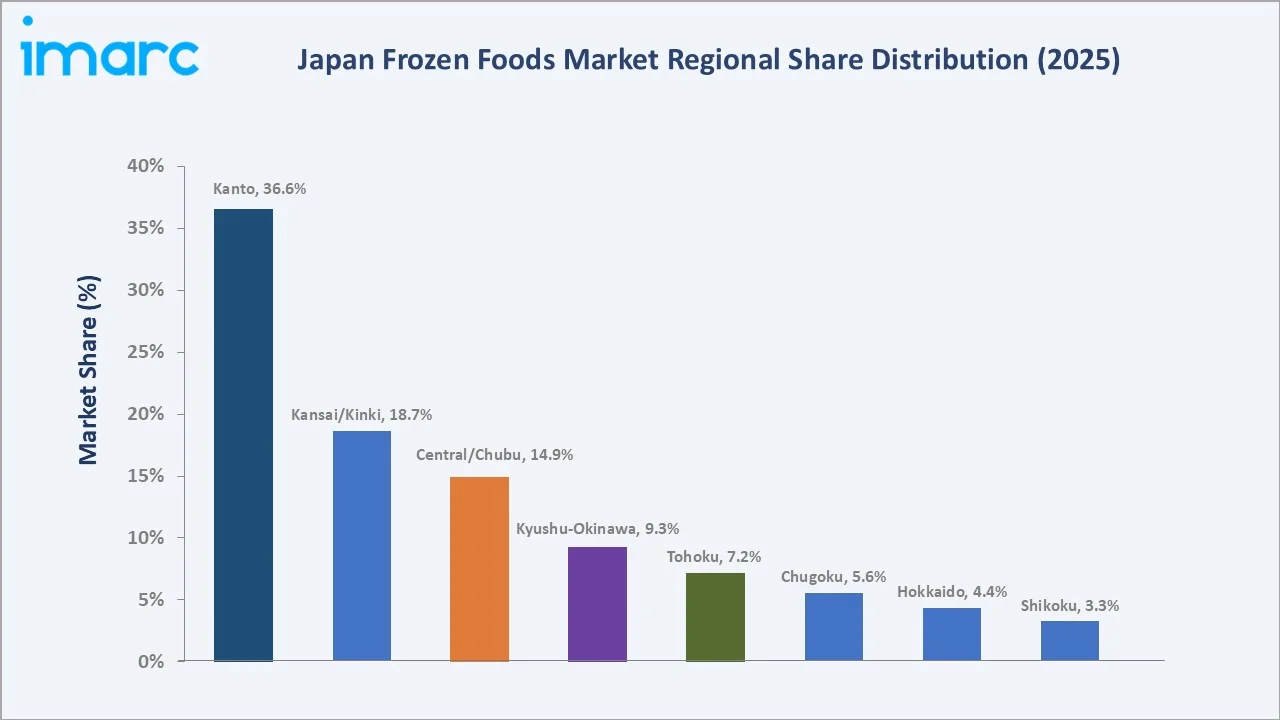

The Japan frozen foods market reached USD 16.05 Billion in 2025 and is projected to reach USD 22.06 Billion by 2034, growing at a CAGR of 3.59% during 2026-2034. The market is primarily driven by the growing demand for convenient and time-saving meal solutions amid busy lifestyles, an aging population, and increasing workforce participation. According to the Japan Frozen Food Association, imported frozen foods represented 37.5% of Japan’s total market in 2023, of which frozen vegetables accounted for 65% and prepared frozen foods made up 35%. This strong import base is driving market growth by improving product availability, diversifying consumer choices, and supporting demand for convenient, ready-to-cook and ready-to-eat frozen food options. Frozen meat products lead at 41.2%. The Kanto region leads at 36.6%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.05 Billion |

|

Forecast Market Size (2034) |

USD 22.06 Billion |

|

CAGR (2026-2034) |

3.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Product Type |

Frozen Meat Products (41.2%, 2025) |

|

Leading Region |

Kanto Region (36.6%, 2025) |

Japan frozen foods market expanded from USD 13.45 Billion in 2020 to USD 16.05 Billion in 2025, anchored at USD 19.15 Billion in 2030, and forecast to reach USD 22.06 Billion by 2034. Japan frozen food culture is uniquely characterized by bento culture, the practice of preparing packed lunches incorporating frozen food components, creating Japan's most commercially distinctive above-convenience-only single frozen food application, generating Japan's high per-household frozen food purchase frequency.

To get more information on this market, Request Sample

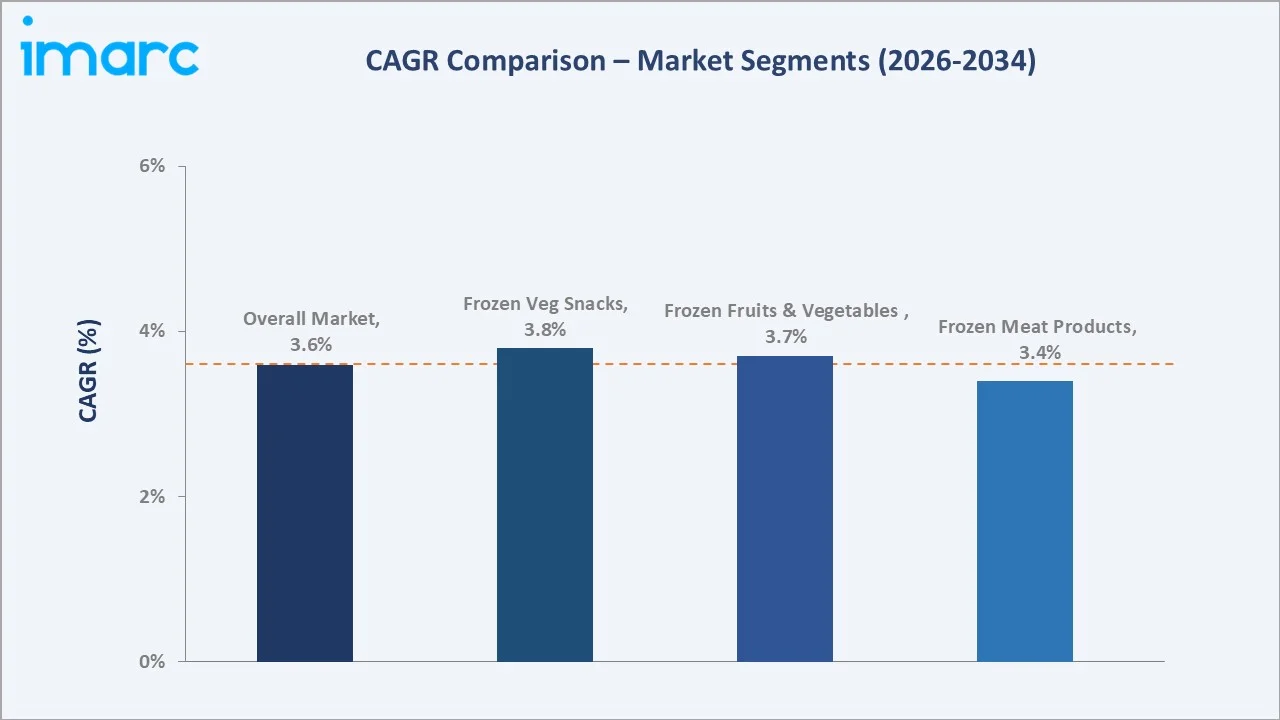

Frozen vegetable snacks grow fastest at ~3.8% CAGR through health-conscious consumer demand for convenient vegetable consumption, bento-suitable portion-packaged frozen vegetable snack, and Japan's growing plant-based food movement, creating the above-meat-product snack category growth. Frozen fruits and vegetables grow at ~3.7% CAGR through household convenience cooking, smoothie and food service demand, and expanding import frozen fruit availability.

Executive Summary

Japan frozen foods market at USD 16.05 Billion in 2025 represents the most commercially quality-demanding and culturally sophisticated single national frozen food market. Japan frozen food market's commercial uniqueness is the bento culture intersection, Japan's homemakers using frozen food components as bento lunch box components, creating the most commercially unique above-meal-replacement single frozen food application where frozen food is a cooking ingredient rather than a convenience substitute. The market is projected to reach USD 22.06 Billion by 2034.

Frozen meat products at 41.2% leads through Japan's above-average demand for frozen gyoza, karaage, hamburger steak, and frozen shumai as Japan's most commercially culturally embedded above-Western-frozen-product single frozen food category, creating Japan's most commercially familiar above-imported frozen food domestic product cultural heritage. Kanto leads regionally at 36.6% through Tokyo's concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Product Type |

Frozen Meat Products - 41.2% share (2025) |

|

Leading Region |

Kanto Region - 36.6% share (2025) |

|

Market Opportunity |

Premium ethnic frozen meal expansion; plant-based protein frozen product; senior-friendly portion control frozen meal; export-quality frozen meat; functional vegetable frozen snack for health-conscious consumers |

Key Analytical Observations Supporting the Above Data:

- Frozen Meat Products at 41.2%: The frozen meat products segment dominates due to strong demand for convenient protein-rich meal solutions, including frozen chicken, beef, pork, and processed meat items. Its growth is further supported by busy lifestyles, foodservice demand, and the longer shelf life offered by frozen meat products.

- Kanto Region at 36.6%: Kanto Region is dominant due to its large urban population, high concentration of supermarkets, convenience stores, foodservice outlets, and busy working consumers. Strong cold chain infrastructure and higher demand for convenient, ready-to-eat meals further support regional growth.

Japan Frozen Foods Market Overview

Japan frozen foods market operates within the broader Japan food and beverage market as the most commercially technology-advanced above-any-other-product-category single food processing category through Japan's leading IQF freezing technology and Japan's cold chain standard, creating the most quality-assured frozen food market. The market's commercial uniqueness is Japan's frozen food cultural integration, frozen food components embedded in Japan's most culturally-significant above-Western food preparation ritual (bento making), creating Japan's most commercially culturally-accepted above-meal-replacement single frozen food application where frozen is an ingredient rather than a shortcut, creating Japan's above-stigma-free above-any-major-Western-market single frozen food consumer perception.

Japan frozen foods ecosystem integrates overseas and domestic raw material supply, food processing and IQF freezing, cold chain logistics, multi-channel retail distribution, food service, and home consumer final preparation. Macroeconomic factors include rising workforce participation, urbanization, higher disposable incomes, and busy consumer lifestyles.

Market Dynamics

To evaluate market opportunities, Request Sample

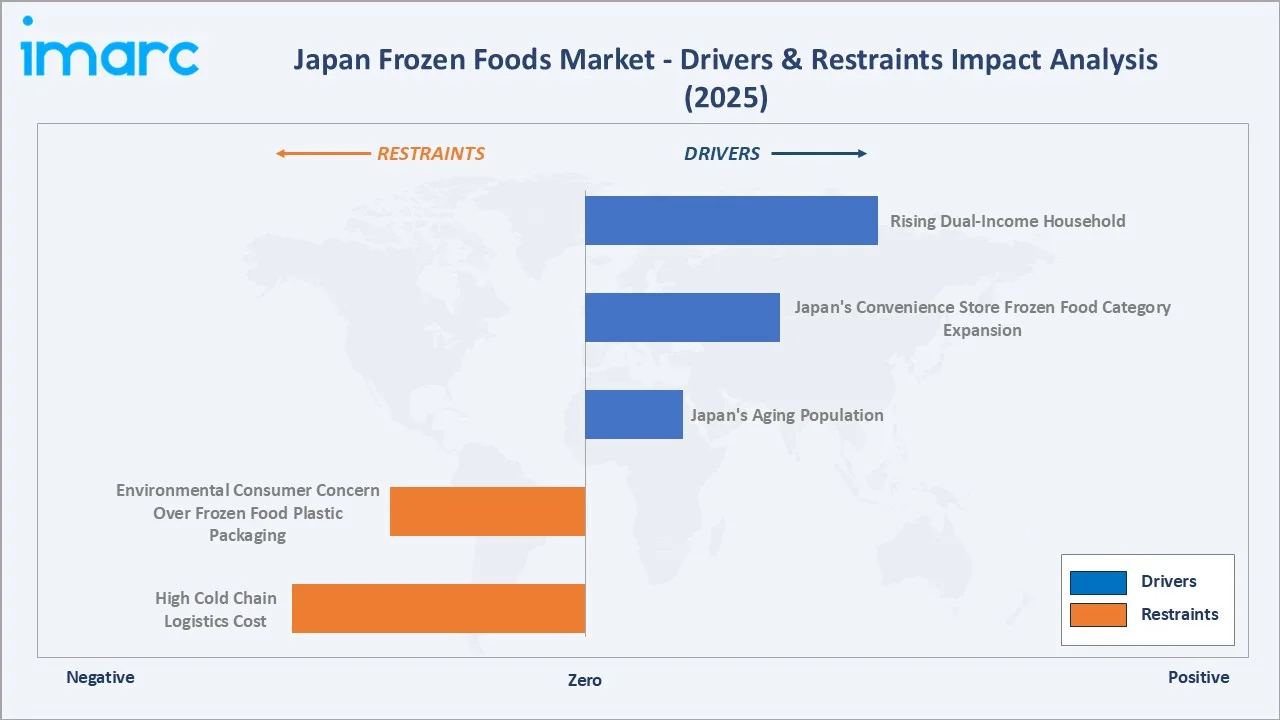

Market Drivers

- Rising Dual-Income Household: Rising dual-income households in Japan are driving demand for frozen foods as consumers seek quick, convenient, and easy-to-prepare meal options. With less time available for daily cooking, working families increasingly prefer frozen ready meals, vegetables, meat products, and snacks that reduce preparation time. Frozen foods also help households manage meal planning efficiently while minimizing food waste. According to the 2025 annual Labour Force Survey by Japan’s Statistics Bureau, dual-income households in Japan increased to 13 million, an increase of 220,000 from 12.78 million in the previous year. This reflects ongoing changes in the country’s labour market structure and household dynamics. This trend is further supported by the availability of high-quality, nutritious, and restaurant-style frozen products across supermarkets and convenience stores.

- Japan's Convenience Store Frozen Food Category Expansion: Japan’s convenience store frozen food category expansion is driving the market by making frozen meals, snacks, desserts, and ready-to-cook items more accessible to urban consumers. Major convenience stores are widening freezer sections and adding premium, private-label frozen products to meet demand for quick meals. This supports impulse purchases and repeat buying among office workers, students, and small households. As convenience stores operate across dense residential and commercial areas, they are strengthening last-mile availability and boosting frozen food consumption.

- Japan's Aging Population: According to Japan’s Ministry of Internal Affairs and Communications, the number of people aged 65 and above reached a record 36.25 million in 2024, representing 29.3% of the total population. This proportion is expected to increase to 34.8% by 2040 and 36.3% by 2045. This rising Japan’s aging population is driving demand for frozen foods as elderly consumers prefer convenient, portion-controlled, and easy-to-prepare meal options. Frozen products help reduce cooking effort while offering longer shelf life and less food waste for smaller households. Demand is also rising for nutritious, soft-textured, and ready-to-eat frozen meals suited to senior dietary needs. This is encouraging manufacturers to expand healthier and single-serve frozen food offerings.

Market Restraints

- High Cold Chain Logistics Cost: High cold chain logistics costs increase expenses for temperature-controlled storage, refrigerated transport, and last-mile delivery. These higher operating costs raise product prices and reduce margins for manufacturers and retailers. Small and regional players may face difficulty expanding distribution due to the need for advanced freezer infrastructure. This can limit product affordability and restrict wider market penetration.

- Environmental Consumer Concern Over Frozen Food Plastic Packaging: Environmental concerns over plastic packaging are hampering the market as consumers increasingly prefer sustainable and low-waste food options. Frozen foods often require multilayer plastic packaging to maintain quality, prevent freezer burn, and extend shelf life, which raises recyclability concerns. This can reduce appeal among eco-conscious buyers and pressure brands to adopt costlier sustainable packaging. As a result, manufacturers may face higher compliance and packaging innovation costs.

Market Opportunities

- Premium Ethnic Frozen Cuisine: Premium ethnic frozen cuisine meeting rising consumer interest in global flavors such as Korean, Chinese, Thai, Indian, and Western meals. These products offer restaurant-style taste with home convenience, appealing to busy urban consumers and younger households. Expanding premium frozen ranges also helps brands command higher margins. In March 2026, Pepizo Foods launched MORUBY, a new frozen potato brand in Japan, in collaboration with ABCD Company. This partnership supports Pepizo Foods’ global expansion strategy and strengthens its position in Japan’s frozen food industry. This supports the premium ethnic frozen cuisine opportunity by introducing differentiated international-style frozen products to Japanese consumers. Such launches expand product variety, encourage demand for inspired frozen foods, and help brands target premium, convenience-focused buyers.

- Plant-Based Protein Frozen Product: Plant-based protein frozen products address the rising demand for healthier, sustainable, and flexitarian meal options. Frozen plant-based burgers, nuggets, dumplings, and ready meals offer convenience while appealing to consumers seeking alternatives to meat. Their longer shelf life supports retail expansion and reduces food waste. This segment also allows manufacturers to target premium, wellness-focused consumers with innovative frozen offerings.

Market Challenges

- Japan's Import Frozen Food Trade Disruption Risk: Japan's import frozen food trade disruption risk is challenging the market because a significant share of frozen vegetables, seafood, and prepared foods is sourced from overseas suppliers. Geopolitical tensions, shipping delays, port congestion, and rising freight costs can disrupt supply availability and increase procurement expenses. Such disruptions may lead to inventory shortages and price volatility across retail channels. This creates uncertainty for manufacturers, distributors, and consumers, potentially affecting market growth.

- Fluctuating Raw Material and Seafood/Meat Prices: Fluctuating raw material and seafood/meat prices increase production and procurement costs for manufacturers. Variations in commodity prices, fishing yields, livestock feed costs, and import expenses can make it difficult to maintain stable pricing. These cost pressures may reduce profit margins or lead to higher retail prices for consumers. As a result, demand growth can be affected, particularly in price-sensitive product categories.

Emerging Market Trends

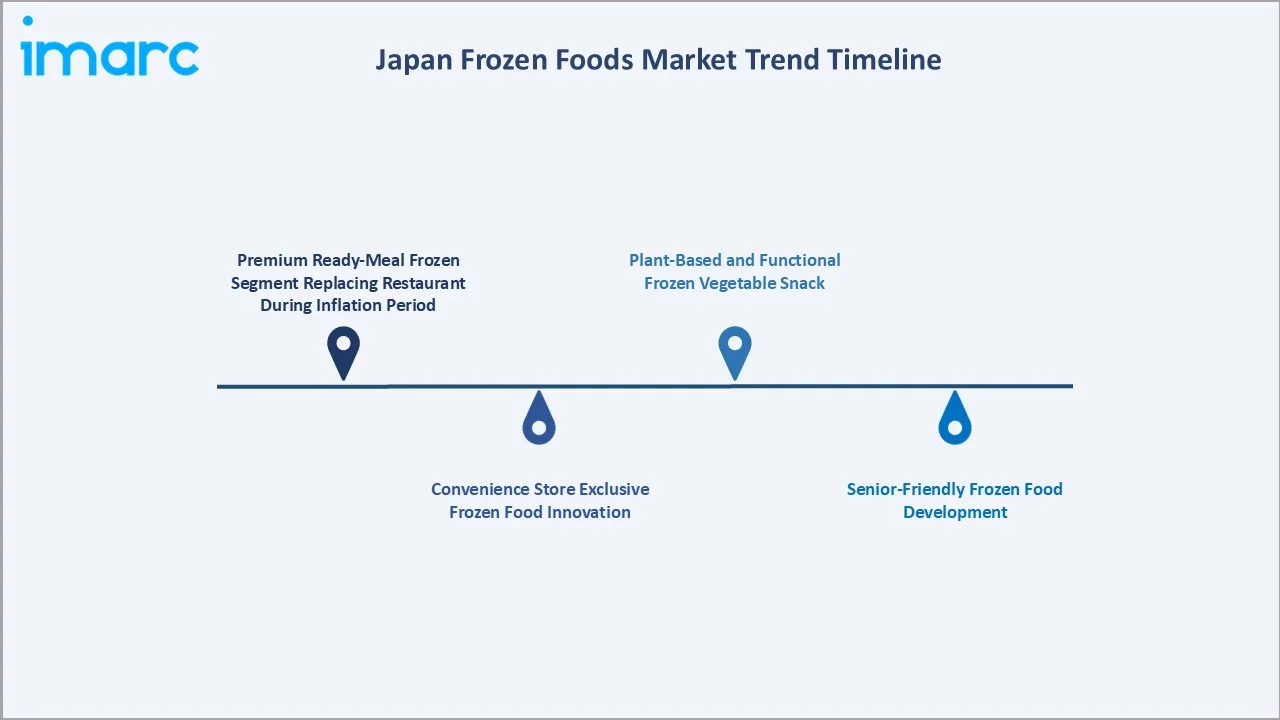

1. Premium Ready-Meal Frozen Segment Replacing Restaurant During Inflation Period

Premium ready-meal frozen products are emerging as consumers seek cost-effective alternatives to dining out during periods of inflation. These products offer restaurant-quality taste, convenience, and variety at a lower overall cost than eating at restaurants. Manufacturers are introducing premium frozen meals featuring high-quality ingredients and authentic flavors to attract value-conscious consumers. In April 2025, AEON Co., Ltd. launched three new frozen one-plate meals under its private label “TOPVALU BestPrice”. Available across about 2,900 AEON, AEON Style, and MaxValu stores nationwide, the lineup includes Gomoku Rice with Chicken in Black Vinegar Sauce, Cheese Curry with Hamburger Steak, and Peperoncino with Tomato Sauce Hamburger Steak. This shift is boosting demand for upscale frozen foods and expanding the market’s premium segment.

2. Convenience Store Exclusive Frozen Food Innovation

Convenience store-exclusive frozen food innovation is emerging as retailers develop unique, high-quality frozen products that cannot be found elsewhere. Major convenience store chains are expanding their private-label portfolios with premium ready meals, snacks, desserts, and ethnic cuisine options. These exclusive offerings help differentiate stores, increase customer loyalty, and drive repeat purchases. The trend is also accelerating product innovation and broadening consumer acceptance of frozen foods as everyday meal solutions.

3. Senior-Friendly Frozen Food Development

Senior-friendly frozen food development is emerging in Japan as brands target the country’s aging population with convenient, nutritious, and easy-to-eat meals. Products with soft textures, smaller portions, balanced nutrition, and simple heating instructions are gaining demand among elderly consumers. This trend also supports independent living by reducing daily cooking effort. As a result, manufacturers are expanding frozen meals tailored to senior dietary and lifestyle needs.

4. Plant-Based and Functional Frozen Vegetable Snack

Plant-based and functional frozen vegetable snacks are emerging in Japan as consumers seek healthier, convenient, and nutrient-rich snack options. These products appeal to flexitarian, wellness-focused, and busy consumers looking for quick alternatives to fried or processed snacks. Frozen formats help preserve freshness, taste, and nutritional value while extending shelf life. In July 2023, Konscious Foods broadened its plant-based seafood portfolio with frozen sushi rolls, poke bowls, and stuffed onigiri rice snacks. Made with clean-label ingredients such as konjac, pea fiber, and organic red quinoa, the new range targets health-conscious and sustainability-driven consumers with convenient Japanese-inspired frozen meal options. This trend is encouraging brands to launch vegetable-based nuggets, bites, dumplings, and protein-enriched frozen snacks.

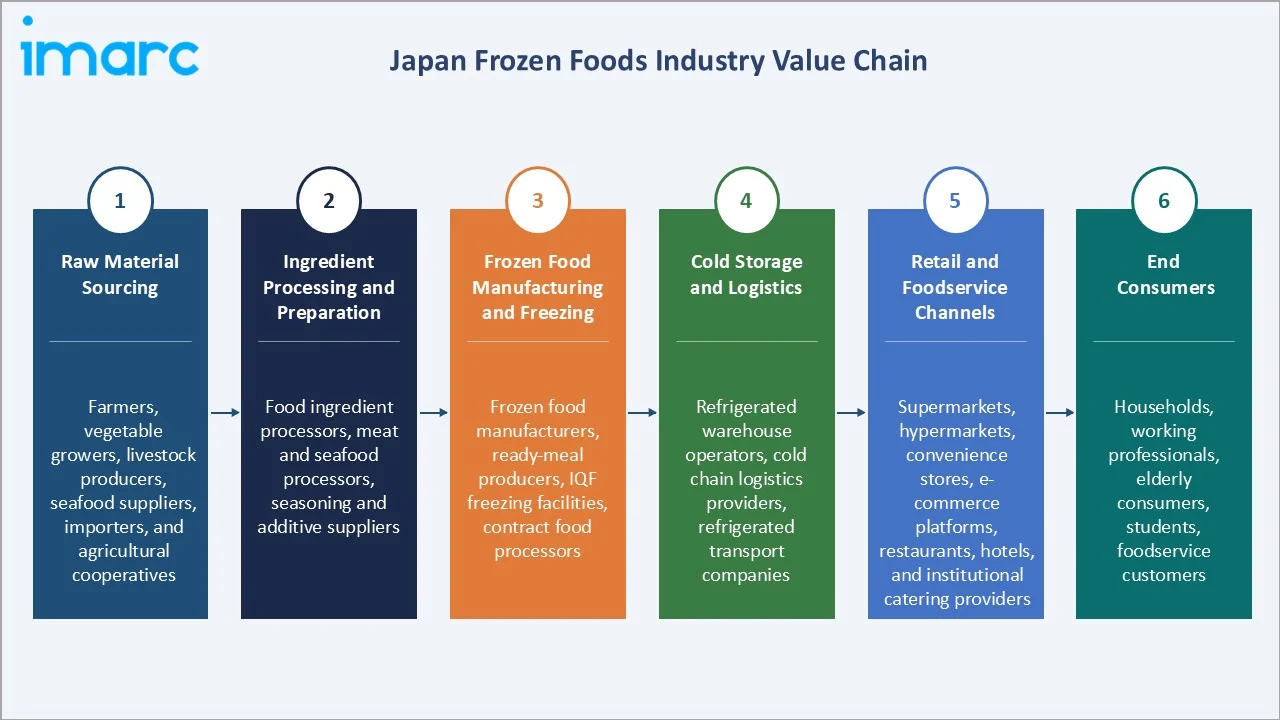

Industry Value Chain Analysis

Japan frozen foods value chain integrates raw material sourcing, ingredient processing & preparation, frozen food manufacturing & freezing, cold storage & logistics, retail & foodservice channels, and end consumers.

|

Stage |

Key Participants |

| Raw Material Sourcing |

Farmers, vegetable growers, livestock producers, seafood suppliers, importers, and agricultural cooperatives |

|

Ingredient Processing & Preparation |

Food ingredient processors, meat and seafood processors, seasoning and additive suppliers |

|

Frozen Food Manufacturing & Freezing |

Frozen food manufacturers, ready-meal producers, IQF freezing facilities, contract food processors |

|

Cold Storage & Logistics |

Refrigerated warehouse operators, cold chain logistics providers, refrigerated transport companies |

|

Retail & Foodservice Channels |

Supermarkets, hypermarkets, convenience stores, e-commerce platforms, restaurants, hotels, and institutional catering providers |

|

End Consumers |

Households, working professionals, elderly consumers, students, foodservice customers |

Cold chain logistics maintenance is Japan's most commercially distinctive value chain stage due to the country's stringent food quality standards and extensive distribution network for frozen products. Advanced temperature-controlled storage and transportation systems ensure product freshness, safety, and quality throughout the supply chain, minimizing spoilage and enabling nationwide availability of frozen foods.

Technology Landscape in the Japan Frozen Foods Industry

IQF (Individually Quick Frozen) Technology

IQF (Individually Quick Frozen) technology enables the rapid freezing of individual food items while preserving their texture, flavor, nutritional value, and appearance. The technology prevents products from clumping together, improving convenience and portion control for consumers. It is widely used for frozen vegetables, seafood, fruits, and ready-to-cook meals, supporting demand for premium-quality frozen foods. As manufacturers focus on quality differentiation and reducing food waste, IQF adoption continues to expand across the industry.

Advanced Freezing Technologies

Advanced freezing technologies are improving the preservation of taste, texture, appearance, and nutritional value across a wide range of products. Innovations such as blast freezing, cryogenic freezing, and multi-stage freezing systems enable faster and more uniform freezing while minimizing cellular damage. These technologies support the development of premium frozen meals, seafood, meat, and vegetable products with near-fresh quality. At SusHi Tech Tokyo 2024, DayBreak Co., Ltd. partnered with traditional fishery specialists from Toyama Prefecture to showcase advanced freezing technology that preserves the fresh taste of locally sourced fish, demonstrating how innovation can make frozen foods both high-quality and delicious. As consumer expectations for high-quality convenience foods rise, manufacturers are increasingly investing in advanced freezing solutions to enhance product differentiation and operational efficiency.

Temperature Tracking and Traceability Platforms

Temperature tracking and traceability platforms are strengthening Japan’s frozen foods technology landscape by enabling real-time monitoring of storage and transport conditions. These systems help maintain product quality, reduce spoilage, and ensure compliance with strict food safety standards. Traceability tools also allow companies to track products from sourcing to retail, improving transparency and recall management. As frozen food distribution expands, such platforms are becoming essential for reliable cold chain operations.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Frozen Meat Products |

41.2% |

2025 |

|

Region |

Kanto Region |

36.6% |

2025 |

By Product Type

Frozen meat products lead at 41.2% (2025). Japan's frozen meat product category encompasses frozen gyoza, karaage, shumai, hamburger steak, frozen yakitori, frozen pork belly, frozen teba (chicken wing), and frozen minced meat set, creating Japan's most commercially Western-frozen-meat single product category portfolio unlike any other developed market's frozen meat category.

To access detailed market analysis, Request Sample

Frozen fruits and vegetables at 34.6% serve household cooking convenience, smoothie ingredients, and food service frozen vegetables. Frozen vegetable snacks at 24.2% encompass portioned frozen edamame pods, frozen corn snack packs, frozen sweet potato, and emerging functional vegetable frozen snack growing at Japan's fastest above-category single frozen product segment CAGR.

Regional Market Insights

|

Region |

Share (2025) |

Key Japan Frozen Foods Market Drivers & Characteristics |

|

Kanto |

36.6% |

Driven by its large urban population, high workforce participation, dense convenience store network, and strong demand for ready-to-eat and ready-to-cook meals. |

|

Kansai/Kinki |

18.7% |

Strong retail infrastructure, a vibrant foodservice sector, and increasing preference for convenience foods support regional demand. |

|

Central/Chubu |

14.9% |

Demand is supported by busy consumers seeking convenient meal solutions and frozen food products. |

|

Kyushu-Okinawa |

9.3% |

Driven by its strong seafood industry, expanding retail sector, and growing acceptance of frozen prepared foods. |

|

Tohoku |

7.2% |

Supported by agricultural and seafood production, which provides a strong supply base for frozen food manufacturers. |

|

Chugoku |

5.6% |

Growing consumer preference for convenient and long-shelf-life food products is contributing to the frozen food market expansion. |

|

Hokkaido |

4.4% |

Hokkaido plays an important role in the frozen foods market due to its strong agricultural, dairy, and seafood industries. |

|

Shikoku |

3.3% |

Represents a smaller but steadily growing market, supported by expanding retail availability, changing consumer lifestyles, and increasing adoption of frozen meals and convenience-oriented food products. |

Kanto's 36.6% market dominance reflects the Tokyo metropolitan area's consumer concentration, CVS and supermarket frozen food channel density, and corporate headquarters concentration. Kansai/Kinki's 18.7% reflects Osaka's food culture intensity, culinary heritage, and Kansai's above-national per-capita food expenditure. Chubu's 14.9% reflects Nagoya's manufacturing worker bento demand and above-average frozen food industrial catering.

Kyushu-Okinawa's 9.3% reflects regional frozen food IP and premium Kurobuta frozen pork. Tohoku's 7.2% reflects Japan's most commercially productive above-prefecture single fishery frozen product source region above consumer market size. Hokkaido's 4.4% reflects Japan's most commercially frozen food production-concentrated above-consumer-proportional single above-production-origin region, creating Japan's largest frozen food production-to-consumption geographic separation above other prefectures. Shikoku's 3.3% reflects frozen national distribution and frozen yuzu specialty market above conventional regional frozen food volume.

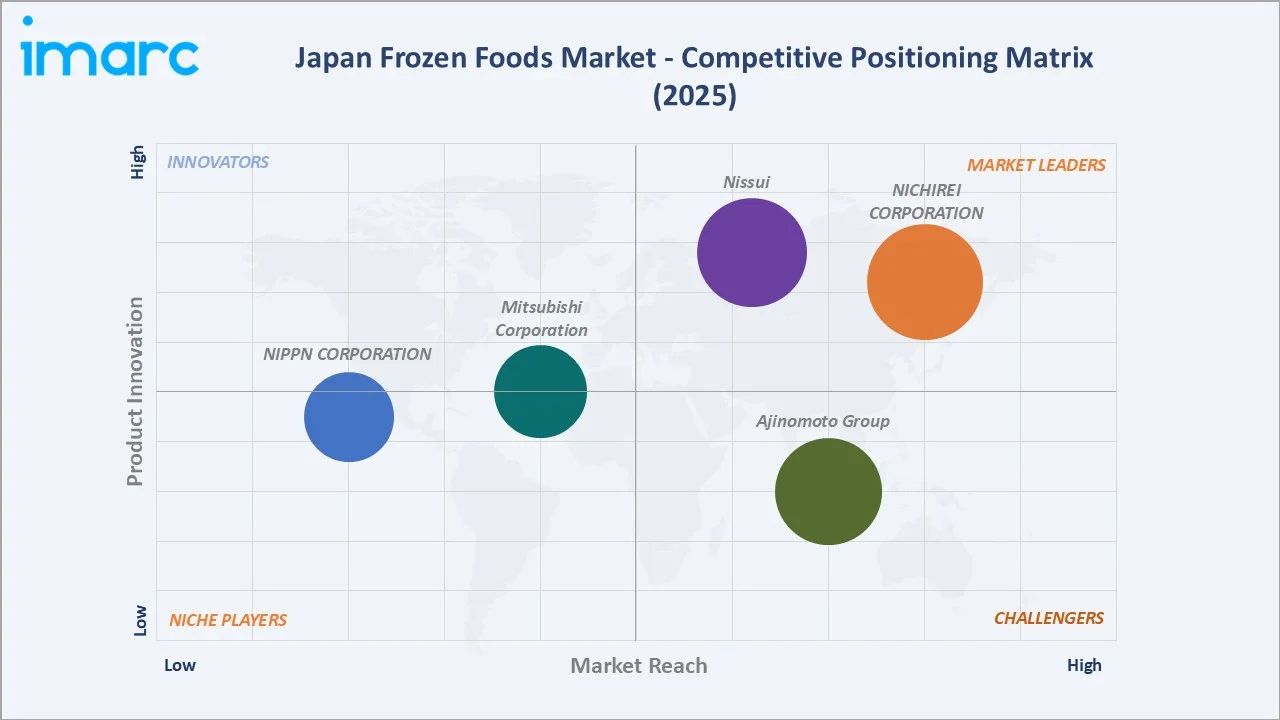

Competitive Landscape

Japan frozen foods competitive landscape is commercially stratified between large, diversified food companies with dedicated frozen food divisions, diversified food company frozen extension, niche frozen food specialists, and international-origin frozen food companies.

| Company | Key Products |

Market Position |

Core Strength |

|

NICHIREI CORPORATION |

Honkaku-Itame Cha-Han (frozen fried rice), Yaki-onigiri (frozen grilled rice balls), Toku-kara (frozen fried chicken), Imagawayaki (frozen Classical Japanese snacks) |

Market Leader |

NICHIREI CORPORATION holds the top market share in Japan's frozen foods sector. As a market leader, it manufactures, processes, and sells a wide range of household and commercial products. |

|

Nissui |

Frozen Foods, Chilled Foods (Including Surimi-Based Products), and Shelf-Stable Foods (Fish Sausages, Canned and Bottled Products) |

Market Leader |

Nissui is a dominant leader in Japan's frozen food sector, specializing in high-quality, processed seafood, household meals, and commercial-use products. |

|

Ajinomoto Group |

Seafood Gyoza Family Pack, Shrimp Shumai Tray, Yakitori Chicken with Japanese-Style Fried Rice |

Strong Challenger |

The Ajinomoto Group is a dominant leader in Japan’s frozen food market. Leveraging expertise in umami and amino acids, AJINOMOTO FROZEN FOODS CO., INC. offers high-quality, convenient products. |

|

Mitsubishi Corporation |

Frozen Rice Balls and Kimbap |

Established Player |

Mitsubishi Corporation plays a foundational, integrated role in Japan's frozen food sector, spanning from raw material procurement and manufacturing to wholesale distribution and retail. |

|

NIPPN CORPORATION |

Frozen Pasta and Pasta Sauce, Cooked Rice, Meals for Boxed Lunches, Snacks, Desserts, Frozen Dough |

Established Player |

NIPPN CORPORATION is a leading Japanese food manufacturer, playing a pivotal role in the frozen food market. They specialize in frozen pasta, ready-made meals, and frozen dough. |

Japan frozen food competitive landscape is evolving through three forces: product premiumization above economy, sustainability packaging innovation, and functional ingredient differentiation.

Key Company Profiles

NICHIREI CORPORATION

NICHIREI CORPORATION is one of Japan’s leading frozen food companies and a pioneer in the country’s frozen foods industry. Through its core subsidiary, Nichirei Foods Inc., the company manufactures and markets a wide range of frozen foods for both household and commercial customers, including frozen fried rice, grilled rice balls, fried chicken, and snacks.

- Key Products: Honkaku-Itame Cha-Han (frozen fried rice), Yaki-onigiri (frozen grilled rice balls), Toku-kara (frozen fried chicken), Imagawayaki (frozen Classical Japanese snacks).

- Strategic Focus: Expanding high-quality, convenient, and ready-to-eat frozen meal solutions for households and foodservice customers.

Ajinomoto Group

Ajinomoto Group is one of Japan’s leading food manufacturers and a major participant in the country's frozen foods market. The company offers a broad portfolio of frozen products, including frozen dumplings (gyoza), fried rice, prepared meals, and convenience-oriented food solutions for both retail and foodservice channels.

- Key Products: Seafood Gyoza Family Pack, Shrimp Shumai Tray, Yakitori Chicken with Japanese-Style Fried Rice.

- Strategic Focus: Expanding premium ready-to-eat and ready-to-cook meal offerings that combine convenience, taste, and nutrition.

Market Concentration Analysis

Japan frozen food market is moderately concentrated, with a few large domestic players holding significant market shares through strong brand recognition, extensive distribution networks, and advanced manufacturing capabilities. However, the market also includes numerous regional manufacturers, private-label brands, and imported frozen food suppliers, creating a competitive landscape. Continuous product innovation, convenience store partnerships, and premium frozen meal development remain key competitive differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Frozen vegetable snacks (~3.8% CAGR through health-conscious and bento demand), premium ethnic frozen cuisine above conventional Japanese frozen food (~5-7% CAGR from small base), plant-based frozen protein product (~8-12% CAGR from near-zero base), senior-friendly frozen meal (~6-8% CAGR through silver market expansion), single-serve convenience rice (~4-5% CAGR through single-person household growth), and Japan-origin frozen food overseas export to Japanese restaurant market (~7-10% CAGR) represent Japan's highest-growth frozen food investment vectors through 2034.

Investment Themes

- Premium ethnic frozen meal creating above-standard margin new category: Investment in authentic Thai curry, Indian masala, Vietnamese pho, and Korean bibimbap premium frozen meal creates Japan's most commercially above-standard Japan frozen single price point premium frozen category for Japan's most food-adventure receptive above-other-country single national consumer market above conventional Japanese frozen food category saturation. Japan's food inflation-driven restaurant substitution is creating peak timing for premium frozen ethnic meal market entry above the pre-inflation lower restaurant-vs-frozen value gap.

- Plant-based frozen protein product: Leveraging Japan's existing consumer plant-based food familiarity to introduce a plant-based frozen protein product above the Western market's above-resistance single plant-based adoption challenge. Investment in frozen plant-based gyoza, frozen soy-protein karaage, and frozen tofu-based hamburger steak creates Japan's most commercially above-skepticism above-Western-plant-based-adoption single plant-based frozen product launch opportunity through Japan's most commercially plant-protein-culturally-familiar above-other-developed-market single consumer geography.

Future Market Outlook (2026-2034)

Japan frozen foods market is projected to grow from USD 16.05 Billion in 2025 to USD 22.06 Billion by 2034, delivering a 3.59% CAGR over the forecast period. The market's anchor value of USD 19.15 Billion in 2030 represents Japan's frozen food industry at steady-state maturity. Dual-income household normalization reaching full penetration of frozen food component purchase, CVS frozen food premium tier achieving mainstream adoption, and senior-friendly frozen food creating Japan's most commercially silver-market above standard frozen consumer above previous older-consumer frozen food use demographic.

Three structural forces define Japan's frozen food market through 2034: demographic inevitability creates Japan's most commercially guaranteed above-discretionary structural demand driver, Japan's single-person household growth, creating Japan's most commercially single-serve-oriented above-family-pack single frozen food packaging format demand shift that creates above-current-packaging SKU proliferation for single-serve portion frozen product, and premium and functional frozen food value creation above pure volume growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with Japan frozen food industry stakeholders (2025), including senior managers, product development directors, category managers, Japan Frozen Food Association secretariat representatives, and a consumer survey from Japan frozen food buyers.

Secondary Research

Secondary research encompassed the Japan Frozen Food Association Annual Survey, the Ministry of Agriculture, Forestry and Fisheries Japan food production statistics, the Ministry of Health, Labour and Welfare food safety annual report, and the company annual reports. Over 40 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a product category expenditure model: Japan frozen food total market estimated from published frozen food shipment data, extrapolated with CAGR adjustment based on product category growth rate differentiation.

Japan Frozen Foods Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Frozen Vegetable Snacks, Frozen Fruits and Vegetables, Frozen Meat Products |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | NICHIREI CORPORATION, Nissui, Ajinomoto Group, Mitsubishi Corporation, NIPPN CORPORATION, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan frozen foods market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan frozen foods market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan frozen foods industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Frozen Foods Market Report

The Japan frozen foods market reached USD 16.05 Billion in 2025, driven by rising demand for convenient, time-saving meal solutions among dual-income households, aging consumers, and urban populations. Expanding convenience store frozen sections, premium ready-meal launches, and advanced cold chain infrastructure are further supporting market growth.

The Japan frozen foods market grows at 3.59% CAGR during 2026-2034, reaching USD 22.06 Billion by 2034. The overall growth is sustained by dual-income household time-scarcity, aging and single-person household demographic structure, IQF technology quality advancement, and CVS frozen food premium category expansion.

Frozen meat products lead at 41.2% through Japan's high culturally-embedded frozen gyoza, karaage, shumai, and hamburger steak category, creating Japan's most commercially domestic-culinary-IP above-Western-concept single frozen meat product portfolio.

Kanto region leads at 36.6% through Tokyo's residents, creating the most commercially concentrated single metropolitan consumer frozen food market, Japan's highest CVS-per-capita density, creating Tokyo's most commercially accessible cold food distribution infrastructure.

Leading companies include NICHIREI CORPORATION, Nissui, Ajinomoto Group, Mitsubishi Corporation, and NIPPN CORPORATION, among others.

The Japan frozen foods market is projected to reach approximately USD 19.15 Billion by 2030, with senior-friendly frozen meals, plant-based frozen protein creating commercial scale above the current niche, premium ethnic frozen meals achieving CVS mainstream distribution above the current specialty retail access, and single-serve frozen food proliferation.

Three priority investment opportunities: Premium ethnic frozen meal creating above-standard margin, a new category for Japan's food-adventure-receptive above-other-country single consumer market, plant-based frozen protein through Japan's existing plant food familiarity, and regional frozen food IP national distribution and international Japanese restaurant market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade