Japan Generative AI Market Size, Share, Trends and Forecast by Offering Type, Technology Type, Application, and Region, 2026-2034

Japan Generative AI Market Size, Share, Trends & Forecast (2026-2034)

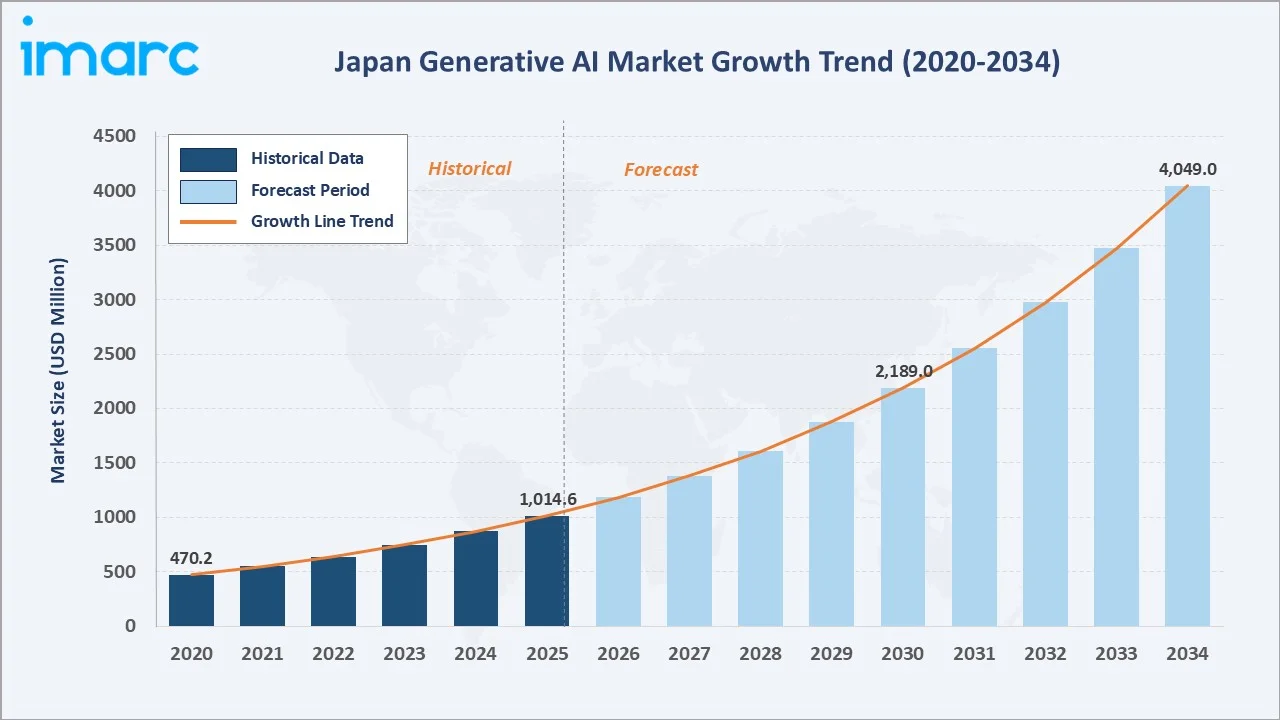

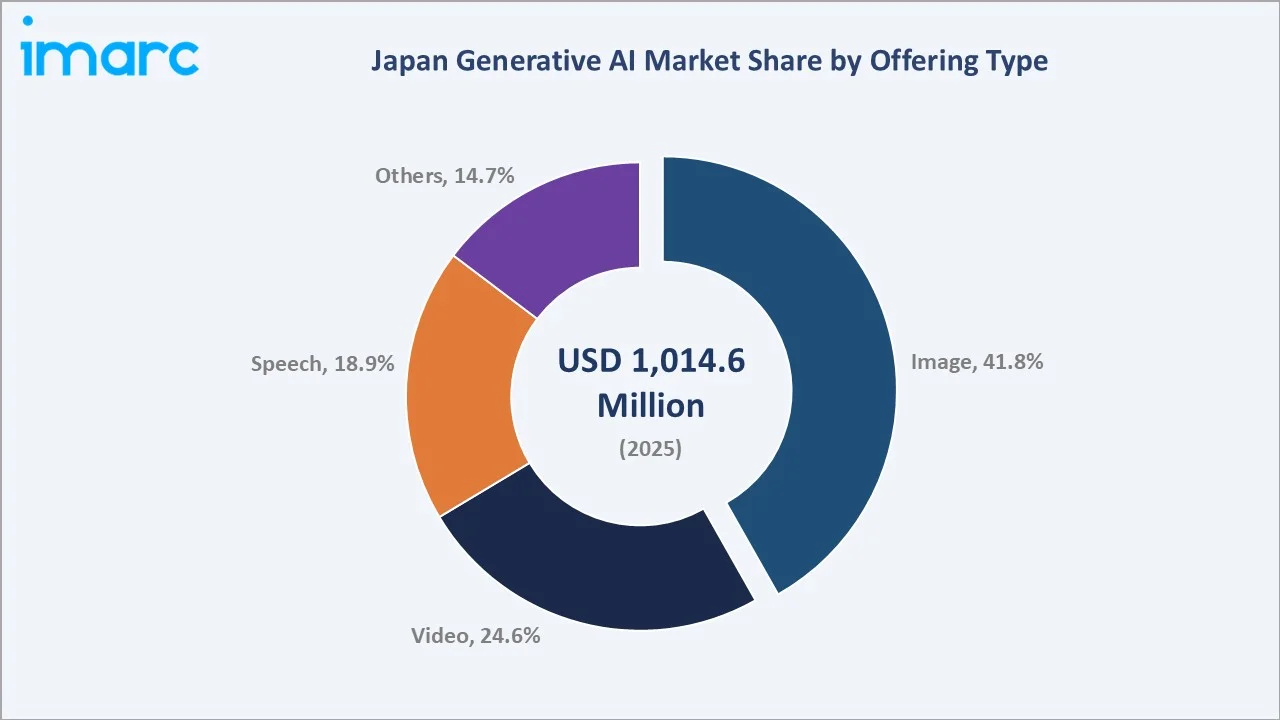

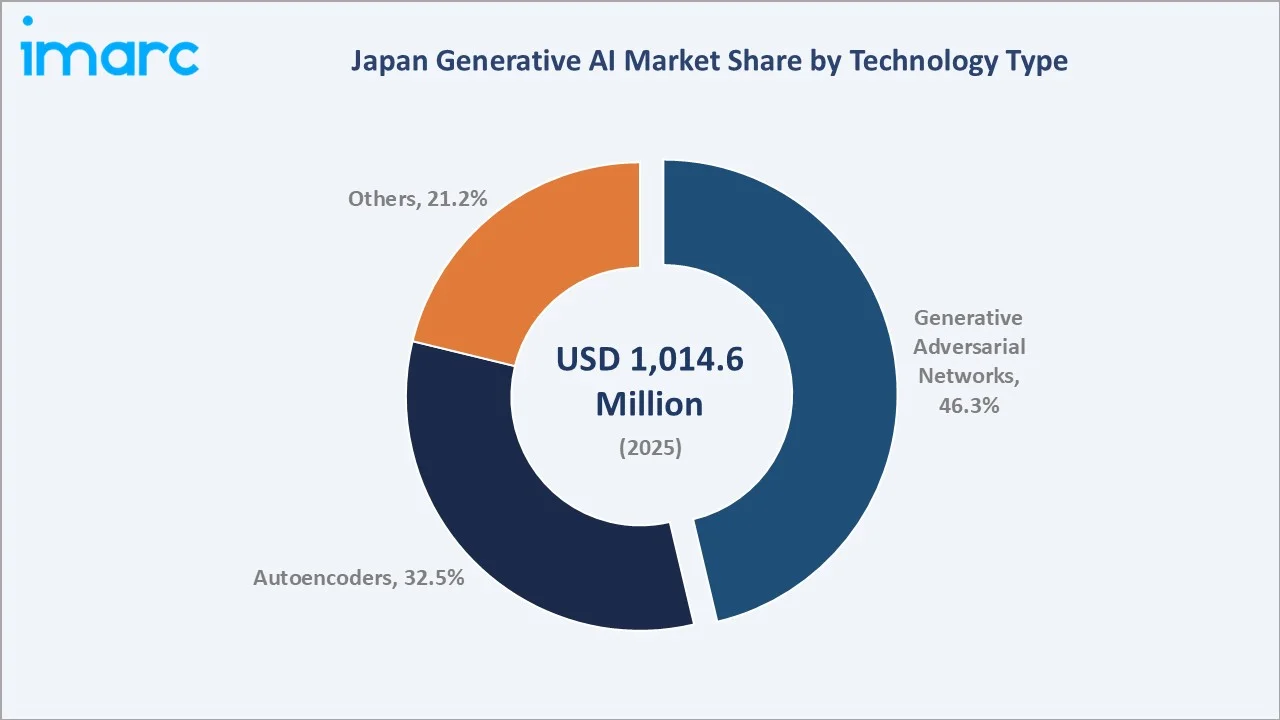

The Japan generative AI market size was valued at USD 1,014.6 Million in 2025 and is projected to reach USD 4,049.5 Million by 2034, exhibiting a CAGR of 16.63% during the forecast period 2026-2034. Rapid enterprise AI adoption, the government-led Society 5.0 initiative, expanding healthcare digitization, and growing demand for AI-driven content creation are driving the Japan generative AI market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,014.6 Million |

|

Forecast Market Size (2034) |

USD 4,049.5 Million |

|

CAGR (2026-2034) |

16.63% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

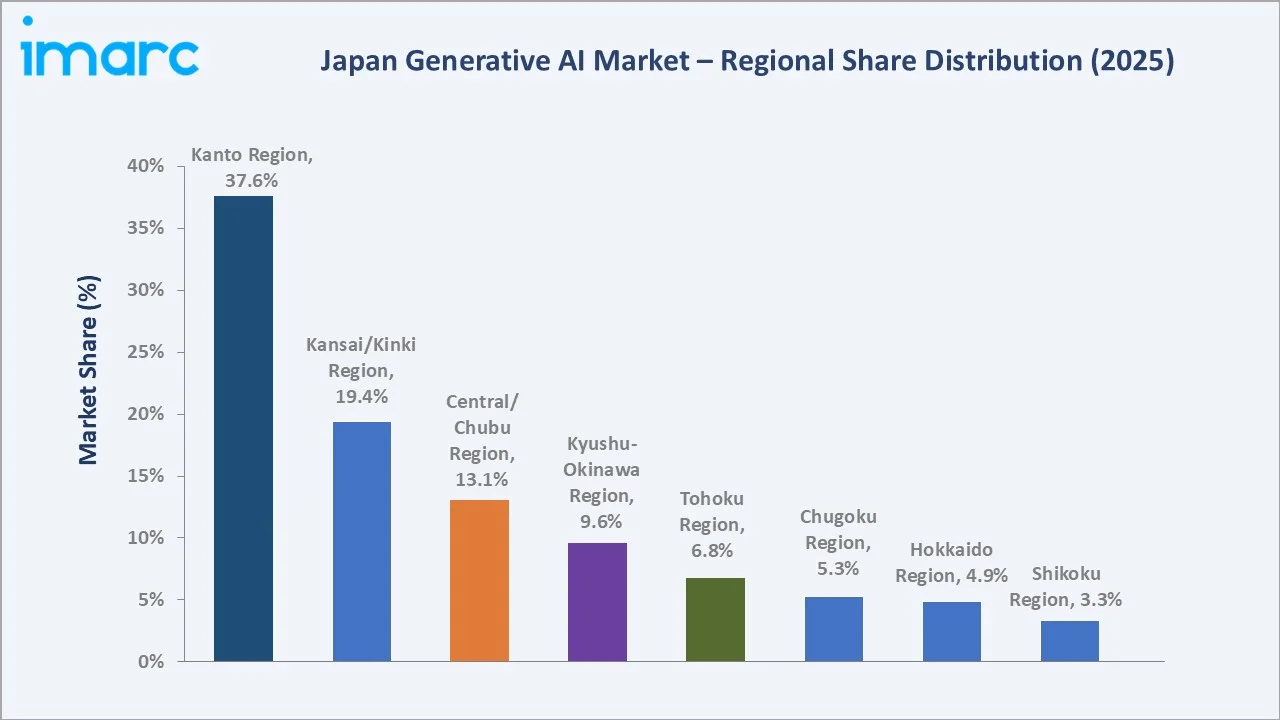

Largest Region |

Kanto Region (37.6% share, 2025) |

|

Fastest Growing Region |

Kanto Region (CAGR ~17.8%) |

|

Leading Offering Type |

Image (41.8%, 2025) |

|

Leading Technology |

Generative Adversarial Networks (46.3%, 2025) |

The Japan generative AI market growth trajectory from 2020 through 2034 shows a steady acceleration powered by enterprise AI integration, healthcare digitization, and rising adoption across media and entertainment verticals.

To get more information on this market, Request Sample

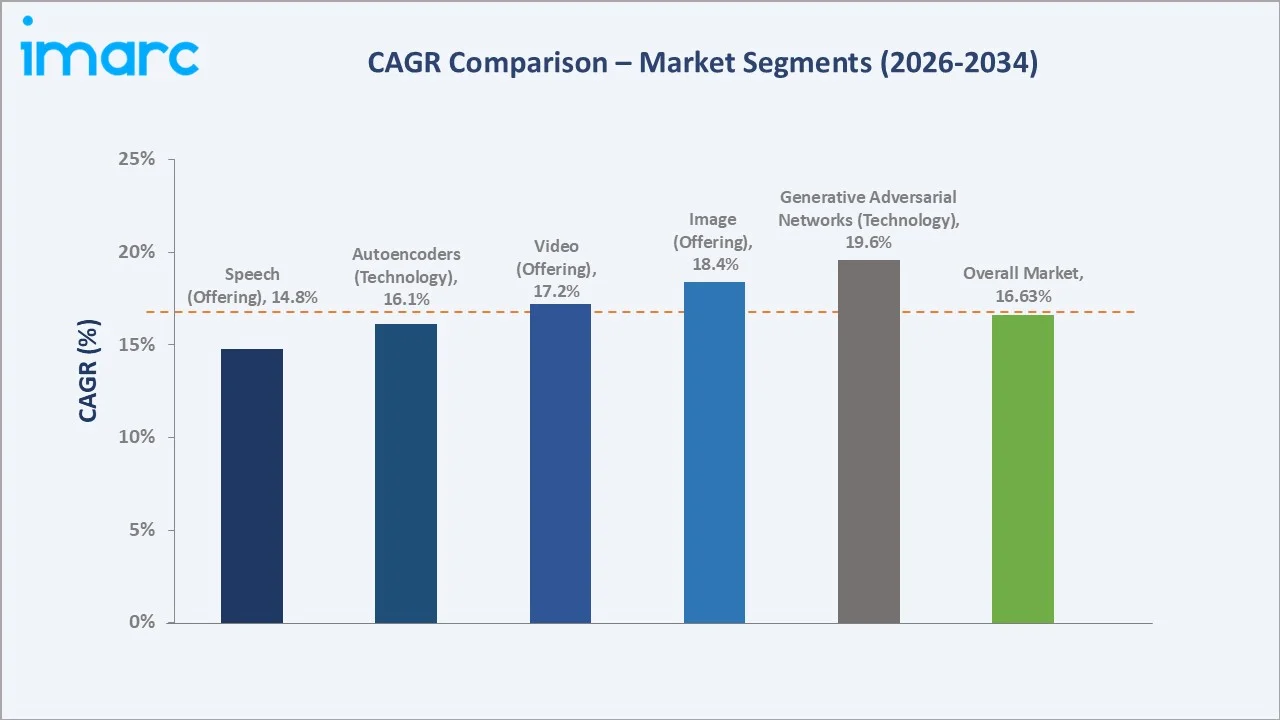

Segment-level CAGR comparisons highlight Generative Adversarial Networks and image-based offerings as the fastest-growing sub-categories within the Japan generative AI market forecast through 2034.

Executive Summary

The Japan generative AI market is undergoing rapid transformation. Growth is driven by enterprise digitization, the government-backed Society 5.0 initiative, and rising demand for AI-driven content creation. Valued at USD 1,014.6 Million in 2025, the market is projected to reach USD 4,049.5 Million by 2034 at a CAGR of 16.63%.

Image generation commands a 41.8% share in 2025, propelled by anime studios, advertising platforms, and design automation tools. Video generation accounts for 24.6%, while speech models hold 18.9%. Among technology architectures, Generative Adversarial Networks lead with 46.3% of revenue, followed by autoencoders at 32.5%.

The Kanto region dominates with 37.6% national revenue share in 2025, anchored by Tokyo's enterprise hub and venture funding density. Kansai/Kinki holds 19.4% and Central/Chubu 13.1%. The Japan generative AI market outlook remains strong as multimodal AI deployment, regulatory clarity, and cross-industry partnerships converge.

Key Market Insights

|

Insight |

Data |

|

Largest Offering Type |

Image – 41.8% share (2025) |

|

Second Offering Type |

Video – 24.6% share (2025) |

|

Largest Technology |

Generative Adversarial Networks – 46.3% share (2025) |

|

Second Technology |

Autoencoders – 32.5% share (2025) |

|

Leading Region |

Kanto Region – 37.6% revenue share (2025) |

|

Top Companies |

SoftBank Corp., NEC Corporation, Fujitsu, Sony Group Corporation, NTT, Inc., Hitachi Ltd., and Preferred Networks, Inc. |

|

Market Opportunity |

Healthcare and Drug Discovery AI |

Key Analytical Observations Supporting the Above Data:

- Image generation's 41.8% dominance in 2025 reflects strong demand from Japan's anime, advertising, and gaming industries, where AI tools are streamlining concept art, character design, and marketing visuals.

- Video generation's 24.6% share is fueled by short-form content platforms and corporate marketing teams adopting AI for storyboarding, dubbing automation, and synthetic media production.

- GAN technology's 46.3% lead stems from its proven performance in photorealistic image synthesis and synthetic data generation, with Preferred Networks and Sony AI advancing research output.

- Kanto region's 37.6% dominance reflects Tokyo's role as the national AI epicenter, hosting more than 60% of Japan's AI-focused startups and a majority of corporate R&D centers.

- Healthcare AI emergence is gaining traction following the SoftBank, SB Intuitions, and Chugai Pharmaceutical MOU signed on January 30, 2025, focused on building a pharma-specific large language model.

- Autoencoders' 32.5% share is supported by their efficiency in anomaly detection and dimensionality reduction tasks, particularly in manufacturing quality control and financial fraud detection.

Japan Generative AI Market Overview

Generative AI refers to deep-learning systems capable of producing original content - including images, video, speech, code, and text - based on patterns learned from large training datasets. Japan's market spans foundation infrastructure providers, model developers, platform vendors, and downstream application creators across industries such as healthcare, media, manufacturing, automotive, and financial services.

The industry sits at the intersection of national AI policy, demographic shifts, and enterprise digital transformation. Growth is supported by macroeconomic drivers including a shrinking labor force pushing automation adoption, the government's Society 5.0 framework, robust cloud infrastructure investment, and increasing venture funding for domestic AI startups, with the broader Japan AI sector attracting record private capital through 2025.

Market Dynamics

To evaluate market opportunities, Request Sample

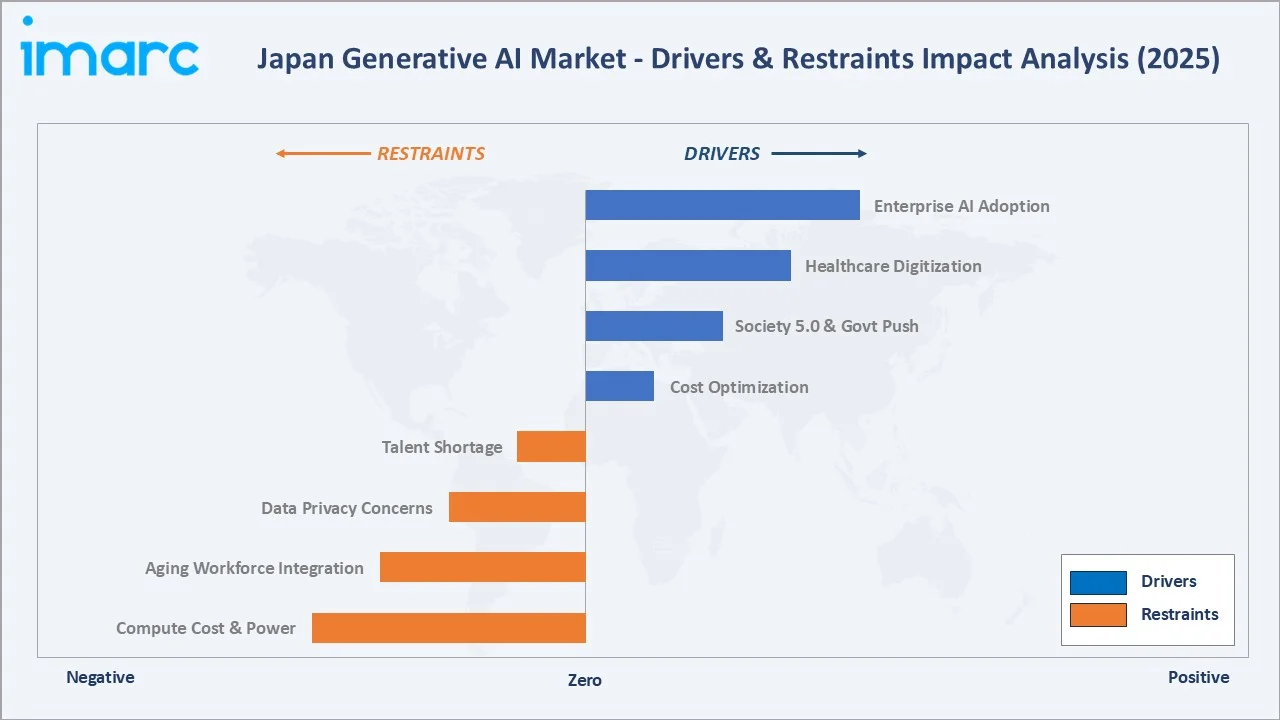

Market Drivers

- Enterprise AI Adoption: Japanese corporations are rapidly advancing the integration of generative AI across multiple functions, including customer service and product design. Across large enterprises, a significant share has already initiated generative AI pilot programs, with adoption continuing to increase steadily year over year.

- Society 5.0 and Government Push: The Cabinet Office's Society 5.0 vision and the AI Strategy 2025 program prioritize generative AI as foundational technology. Public-sector procurement and university research grants are channeling structured demand toward domestic vendors and consortia.

- Healthcare Digitization: Pharmaceutical and clinical AI applications are gaining traction. The SoftBank, SB Intuitions, and Chugai Pharmaceutical MOU announced on January 30, 2025, targets a pharma-specific large language model designed to compress drug development timelines and clinical trial throughput.

- Cost Optimization in a Tight Labor Market: Japan's working-age population is contracting steadily, and generative AI is increasingly used to automate routine knowledge work, including translation, document drafting, and customer support, helping firms preserve productivity despite workforce shortages.

Market Restraints

- Compute Cost and Power Constraints: Training and serving large generative models requires substantial GPU capacity, and Japan's data center power costs and supply tightness pressure unit economics, particularly for smaller domestic providers.

- Data Privacy and Regulatory Uncertainty: Evolving guidelines from the Personal Information Protection Commission and ongoing copyright debates around AI training data create compliance complexity, slowing some enterprise rollouts.

- Talent Shortage: Ministry of Economy, Trade and Industry highlights that Japan faces a structural shortfall in AI and machine-learning specialists. Projections indicate a significant gap in the availability of AI engineers through 2030, which is expected to constrain vendor expansion plans and slow large-scale deployment.

Market Opportunities

- Healthcare and Drug Discovery: Pharmaceutical AI partnerships and synthetic medical imaging applications represent a high-margin growth opportunity. Japan's aging population creates strong demand for AI-assisted diagnostics, radiology, and personalized treatment planning.

- Anime, Gaming, and Creative Media: Domestic content industries are increasingly integrating AI into production pipelines. Japan External Trade Organization initiatives such as the GDC Japan Pavilion have showcased AI-powered tools across numerous game titles, signaling growing mainstream adoption among mid-tier studios.

- Manufacturing and Industrial AI: Generative design, synthetic training data, and predictive maintenance applications are scaling across Japan's automotive, electronics, and precision-manufacturing base, opening enterprise contracts worth tens of billions of yen annually.

Market Challenges

- Foreign Hyperscaler Competition: U.S. providers including OpenAI, Anthropic, Google, and Microsoft hold strong enterprise mindshare in Japan, pressuring local vendors to differentiate through Japanese-language quality, on-premise deployment, and domain specialization.

- Aging Workforce Integration: Adoption rates remain uneven across firms, with smaller and mid-sized enterprises citing change-management friction and limited internal AI literacy as the top barriers to scaling proof-of-concepts into production.

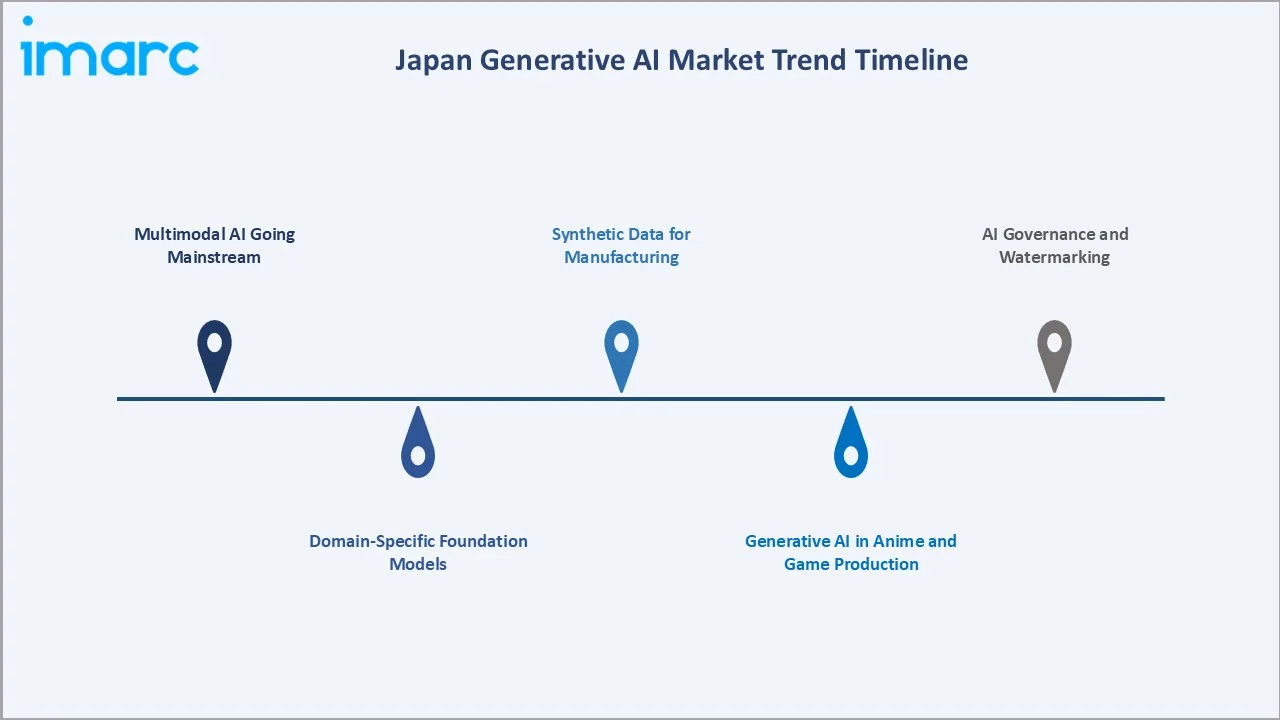

Emerging Market Trends

1. Multimodal AI Going Mainstream

Japanese enterprises are moving beyond text-only models toward multimodal systems that combine image, video, speech, and text. SoftBank, NEC, and Sony AI have all rolled out multimodal platforms in 2024-2025, supporting use cases such as automated video captioning and visual product search.

2. Domain-Specific Foundation Models

Japan's vendors are increasingly building specialized foundation models for finance, healthcare, manufacturing, and the Japanese language itself. SB Intuitions, NTT, and the National Institute of Informatics are advancing models tuned for industry-specific accuracy and Japanese-language fluency, reducing reliance on U.S. providers.

3. Generative AI in Anime and Game Production

Generative AI is transforming anime and game production workflows, with tools enabling AI-assisted character design, automated in-betweening, and storyboard generation. Mid-tier studios and gaming developers are increasingly adopting these solutions to enhance productivity, reduce manual effort, and accelerate content creation timelines while maintaining creative quality and visual consistency across projects.

4. Synthetic Data for Manufacturing

Automotive and electronics manufacturers are adopting GAN-based synthetic data to train computer vision systems where real-world labelled data is scarce. Toyota, Honda, and Sony Semiconductor have publicly disclosed synthetic-data pipelines for autonomous driving and quality inspection through 2025.

5. AI Governance and Watermarking

Following the AI Strategy 2025 update, Japanese platforms are deploying provenance markers and content-authentication tools. Major media outlets and stock-image providers are piloting watermarking standards aligned with the C2PA framework, addressing copyright and disinformation concerns.

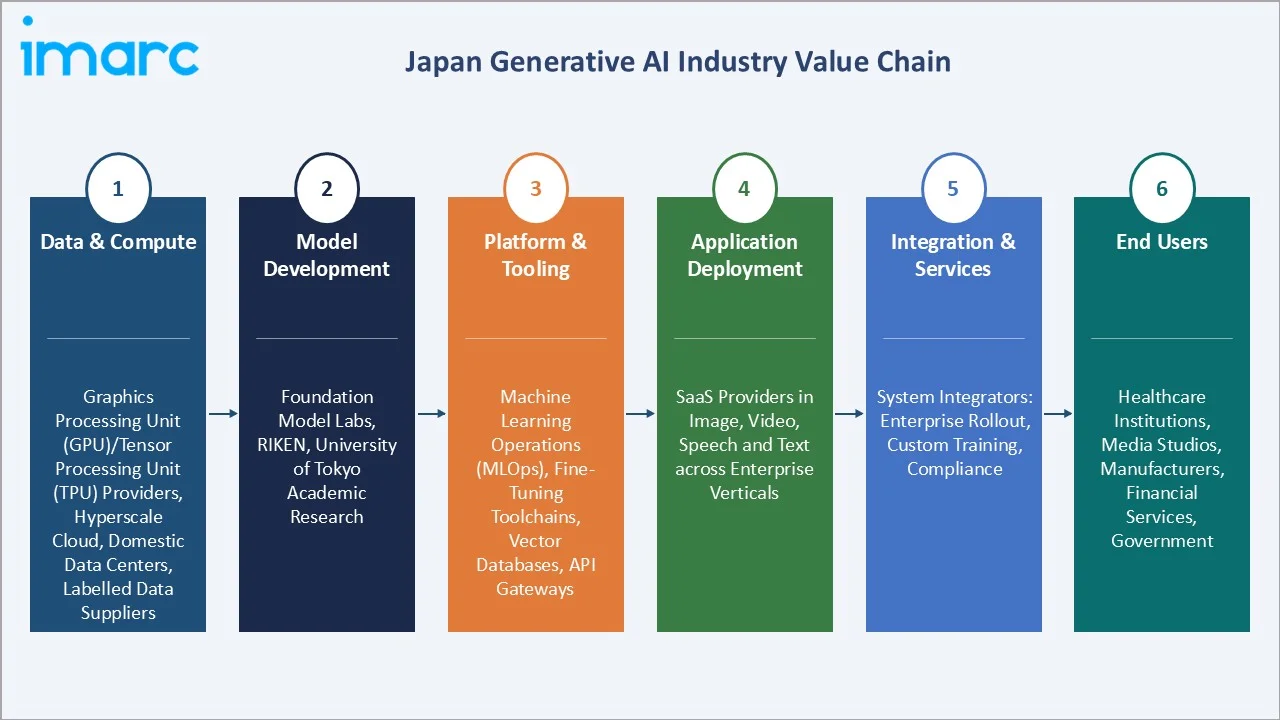

Industry Value Chain Analysis

The Japan generative AI value chain spans six integrated stages from data and compute infrastructure through end-user adoption. Each stage carries distinct competitive dynamics, capital intensity, and margin profiles relevant to the overall Japan generative AI market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Data & Compute |

Graphics Processing Unit (GPU) and Tensor Processing Units (TPU) providers, hyperscale cloud, domestic data centers, and labelled data suppliers |

|

Model Development |

Foundation model, academic research labs at RIKEN and University of Tokyo |

|

Platform & Tooling |

Machine Learning Operations (MLOps) and model orchestration vendors, fine-tuning toolchains, vector databases, and API gateways |

|

Application Deployment |

SaaS providers in image generation, video, speech, and text applications across enterprise verticals |

|

Integration & Services |

System integrators handling enterprise rollout, custom training, and compliance |

|

End Users |

Healthcare institutions, media studios, manufacturers, financial services firms, retailers, and government agencies |

Platform and tooling providers are emerging as the most strategically valuable layer, integrating compute, model access, and domain customization into turnkey enterprise solutions. Meanwhile, large system integrators continue to capture significant value through their existing client relationships and ability to deliver compliant, on-premise deployments tuned for Japanese-language workloads.

Technology Landscape in the Japan Generative AI Industry

Generative Adversarial Networks (GANs)

GANs lead the Japanese technology landscape with a 46.3% revenue share in 2025, supported by their proven track record in photorealistic image synthesis, anime-style character generation, and synthetic data creation.

Autoencoders and Diffusion Models

Autoencoders and their variants - including variational and diffusion architectures - account for 32.5% of revenue in 2025. They are widely deployed in anomaly detection for manufacturing quality control, financial fraud screening, and medical imaging enhancement, with adoption growing fastest in automotive and electronics verticals.

Large Language Models and Multimodal Architectures

Domestic LLM development is accelerating. SB Intuitions, NEC's cotomi, and NTT's tsuzumi are positioning Japanese-language foundation models against U.S. hyperscalers. Multimodal architectures combining vision, language, and speech are emerging as a differentiator, with Sony AI and Sakana AI investing heavily in next-generation model design.

Cloud Infrastructure and Edge Deployment

Generative AI workloads are split between hyperscale cloud GPUs and edge devices. NTT, and SoftBank are expanding domestic data center GPU capacity, while NEC corporation, and Fujitsu are advancing on-device inference for privacy-sensitive applications, particularly in healthcare and government deployments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Offering Type | Image | 41.8% | 2025 |

| Technology Type | Generative Adversarial Networks | 46.3% | 2025 |

| Application | 🔒 | 🔒 | 2025 |

| Region | Kanto Region | 37.6% | 2025 |

By Offering Type

To access detailed market analysis, Request Sample

Image generation leads the Japan generative AI market with a 41.8% share in 2025. Demand is driven by anime studios adopting AI-assisted character design, advertising agencies using generative tools for campaign creatives, and e-commerce platforms deploying synthetic product imagery. Adobe Firefly Japan, Sony's image-AI tools, and domestic startups including Rinna and Stability AI Japan partners are scaling rapidly across enterprise creative workflows.

By Technology Type

Generative Adversarial Networks dominate Japan's technology mix with a 46.3% share in 2025. GANs underpin the bulk of image and video applications, anime production tools, and synthetic data pipelines used in automotive and electronics manufacturing. Domestic research output from Preferred Networks, RIKEN AIP, and the University of Tokyo continues to advance GAN performance in low-data and Japanese-cultural-context tasks.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.6% |

Tokyo enterprise hub, AI startup density, government R&D, university research |

|

Kansai/Kinki Region |

19.4% |

Osaka manufacturing AI, Kyoto research labs, healthcare AI partnerships |

|

Central/Chubu Region |

13.1% |

Nagoya automotive AI (Toyota, Denso), industrial generative design |

|

Kyushu-Okinawa Region |

9.6% |

Fukuoka startup ecosystem, semiconductor industry, regional digital initiatives |

|

Tohoku Region |

6.8% |

Sendai academic AI hub, regional manufacturing automation |

|

Chugoku Region |

5.3% |

Hiroshima industrial AI, automotive supply chain digitization |

|

Hokkaido Region |

4.9% |

Sapporo data center investments, agricultural AI applications |

|

Shikoku Region |

3.3% |

SME digital transformation, regional government AI pilots |

Kanto commands 37.6% national revenue share in 2025. Tokyo is the country's undisputed AI capital, hosting headquarters for SoftBank, NEC, NTT, Hitachi, Sony AI, and the largest concentration of AI-focused startups including SB Intuitions, Sakana AI, and Preferred Networks. Government ministries, leading universities, and major venture funds are clustered in the region. Kanto is also the fastest-growing region, advancing at approximately 17.8% CAGR through 2034.

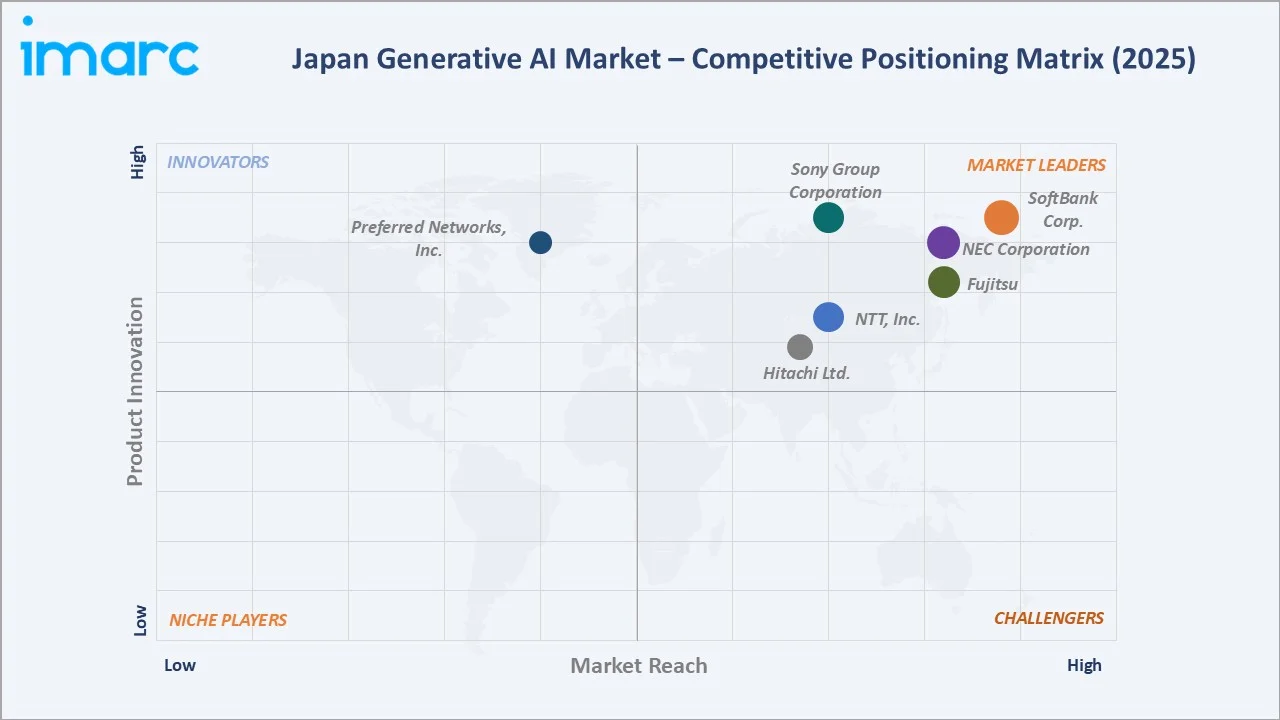

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

SoftBank Corp. |

Sarashina |

Leader |

Japanese LLM scale, telco-AI integration, healthcare partnerships |

|

NEC Corporation |

cotomi |

Leader |

Enterprise AI, public sector, on-premise deployment |

|

Fujitsu |

Takane |

Leader |

Supercomputing-backed models, Kozuchi platform, system integration |

|

Sony Group Corporation |

Sony AI |

Leader |

Multimodal AI, gaming, imaging, music generation |

|

NTT, Inc. |

tsuzumi |

Leader |

Lightweight LLMs, on-device inference, telecom data scale |

|

Hitachi Ltd. |

Lumada |

Challenger |

Industrial AI, healthcare informatics, social infrastructure |

|

Preferred Networks, Inc. |

PLaMo |

Challenger |

Deep-learning research depth, manufacturing AI partnerships |

Japan's generative AI competitive landscape is moderately concentrated, with established technology conglomerates competing alongside research-driven challengers and lean specialist startups. Leading players differentiate through Japanese-language model quality, on-premises deployment capabilities, vertical specialization, and partnership ecosystems.

Key Company Profiles

SoftBank Corp.

SoftBank Corp. is one of Japan's largest telecommunications and technology conglomerates, headquartered in Tokyo. Through its SB Intuitions subsidiary, the group is investing heavily in domestic foundation models and generative AI applications, with deep ties to enterprise customers and research institutions.

- Product & Platform Portfolio: SoftBank's AI portfolio includes the Sarashina large language model series developed by SB Intuitions, generative AI applications across customer service and enterprise automation, and a dedicated AI compute infrastructure backed by NVIDIA GPU partnerships.

- Recent Developments: In 2025, SoftBank Corp. is accelerating its generative AI push through in-house model development and large-scale ecosystem investments. In 2025, the company launched a domestic generative AI foundation model built on its proprietary LLM Sarashina, enabling secure, end-to-end AI deployment within Japan and improving network operations accuracy.

- Strategic Focus: SoftBank's strategy centers on building Japanese-language foundation models, partnering with vertical leaders in healthcare and finance, and leveraging its telecommunications scale to deliver generative AI services to enterprise customers and consumer applications.

NEC Corporation

NEC Corporation is a leading Japanese information technology and electronics company headquartered in Tokyo. Founded in 1899, NEC operates across IT services, network solutions, and AI platforms with a strong public-sector and enterprise customer base.

- Product & Platform Portfolio: NEC's generative AI offering centers on cotomi, its proprietary large language model platform, alongside the NEC the WISE AI suite covering image, video, and biometric generative applications. The company also delivers customized on-premise deployments for regulated industries.

- Recent Developments: In 2025, NEC Corporation announced a strategic collaboration with Anthropic focused on advancing enterprise generative AI in Japan. The partnership positions NEC as a global partner, enabling joint development of industry-specific AI solutions for sectors such as financial services, manufacturing, and government.

- Strategic Focus: NEC focuses on enterprise-grade generative AI with strong governance, on-premise deployment options for sensitive data, and Japanese-language accuracy, leveraging its long-standing relationships with government ministries and large corporations.

Fujitsu

Fujitsu is a global Japanese information and communication technology company headquartered in Tokyo. Founded in 1935, Fujitsu operates across cloud, AI, and digital transformation services with a presence in more than 100 countries.

- Product & Platform Portfolio: Fujitsu's generative AI portfolio includes the Kozuchi AI platform, the Takane Japanese-language large language model, and the Fugaku-LLM developed in collaboration with RIKEN and Tokyo Institute of Technology using the Fugaku supercomputer.

- Recent Developments: In 2026 Fujitsu announced the launch of a new platform enabling autonomous operation of generative AI within dedicated, in-house environments. The solution allows enterprises to manage the full AI lifecycle—from model development to continuous improvement—while ensuring secure, sovereign deployment of AI systems.

- Strategic Focus: Fujitsu's approach combines supercomputing-backed model development, system-integration depth, and a focus on responsible AI - including model transparency and data governance - to serve large enterprise and public-sector deployments.

Market Concentration Analysis

The Japan generative AI market exhibits moderate concentration. The top five players - SoftBank Corp., NEC Corporation, Fujitsu, Sony Group Corporation, NTT, Inc., - collectively account for approximately 55-62% of national revenue in 2025.

The market shows two distinct dynamics. At the foundation-model layer, consolidation is occurring around large conglomerates and well-funded startups capable of training Japanese-language models at scale. Simultaneously, the application layer remains highly fragmented, with hundreds of vertical specialists deploying generative AI across creative industries, healthcare, manufacturing, and financial services. This bifurcated structure is expected to persist through 2034 as platform economics favor scale while domain expertise continues to fragment downstream.

Investment & Growth Opportunities

Fastest-Growing Segments

Image generation is the highest revenue offering in Japan, and Generative Adversarial Networks lead the technology mix with 46.3% share in 2025. Healthcare-applied generative AI is the fastest-growing application vertical, advancing at an estimated 21-23% CAGR through 2030, driven by drug discovery, medical imaging, and clinical decision support. Multimodal AI platforms represent the premium technology growth opportunity, with adoption rising sharply across creative industries and enterprise automation.

Emerging Market Expansion

Beyond Tokyo, Osaka and Nagoya represent the highest-potential expansion territories given their concentration of healthcare and automotive manufacturing customers. Fukuoka is emerging as a startup hub backed by municipal incentives, while Sapporo's data center investments position Hokkaido as a future infrastructure node. International export of Japan-built generative AI models - particularly to Southeast Asia - is becoming a strategic growth lever for SoftBank Corp., NEC Corporation, and Fujitsu.

Venture and Strategic Investment Trends

Strategic acquisitions and partnerships are accelerating. SoftBank's January 2025 healthcare MOU, JETRO's GDC 2025 pavilion in March 2025 spotlighting AI-powered Japanese games, and ongoing investment from corporate venture arms at NEC, Fujitsu, and Sony are channeling capital into vertical AI startups.

Future Market Outlook (2026-2034)

The Japan generative AI market forecast projects sustained expansion from USD 1,014.6 Million in 2025 to USD 4,049.5 Million by 2034 at a CAGR of 16.63%. The Kanto region will retain its dominance through 2034 while Kansai/Kinki and Central/Chubu accelerate on healthcare and automotive AI demand respectively.

Three structural shifts will reshape the Japan generative AI market through 2034. First, multimodal foundation models will replace single-modality systems as the default enterprise standard by 2028. Second, domain-specialized models for healthcare, finance, and manufacturing will capture an increasing share of value as accuracy and compliance requirements intensify. Third, on-device and edge inference will scale rapidly, particularly through NTT's tsuzumi and similar lightweight Japanese-language models, supporting privacy-sensitive deployments across regulated industries.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with Japan generative AI industry stakeholders - including AI product directors at large Japanese conglomerates, machine-learning engineers at foundation-model startups, procurement leads at enterprise adopters, and venture investors active in domestic AI funding rounds. Primary insights validated market sizing, segmentation share estimates, and adoption-curve assumptions.

Secondary Research

Secondary sources include METI publications, Cabinet Office AI Strategy 2025 documents, Personal Information Protection Commission guidelines, JETRO trade reports, RIKEN AIP research output, company annual reports for SoftBank, NEC, Fujitsu, Sony, NTT, and Hitachi, trade publications, and university research databases. Funding and acquisition data were drawn from Japanese venture capital reports and corporate disclosure filings.

Forecasting Models

Market sizing and forecasting were derived through a combination of top-down and bottom-up models, incorporating GDP growth assumptions, ICT spending trajectories, AI adoption-curve modelling, and historical AI-spend patterns. Scenario analysis (base, optimistic, and conservative cases) was applied to account for regulatory and macroeconomic uncertainty across the 2026-2034 forecast horizon.

Japan Generative AI Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Offering Types Covered | Image, Video, Speech, Others |

| Technology Types Covered | Autoencoders, Generative Adversarial Networks, Others |

| Applications Covered | Healthcare, Generative Intelligence, Media and Entertainment, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, and Shikoku Region |

| Companies Covered | SoftBank Corp., NEC Corporation, Fujitsu, Sony Group Corporation, NTT, Inc., Hitachi Ltd., Preferred Networks, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan generative AI market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan generative AI market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan generative AI industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Generative AI Market Report

The Japan generative AI market reached USD 1,014.6 Million in 2025, supported by enterprise adoption, the Society 5.0 framework, and accelerating use across healthcare, media, and manufacturing applications.

The market is projected to reach USD 4,049.5 Million by 2034, growing at a CAGR of 16.63% during 2026-2034, supported by enterprise digitization, multimodal AI deployment, and government-backed innovation programs.

Image generation leads with a 41.8% share in 2025, driven by anime studios, advertising creatives, e-commerce visuals, and gaming asset generation across Japan's strong creative-industry ecosystem.

Generative Adversarial Networks dominate with 46.3% share in 2025, supported by their use in image synthesis, anime production, synthetic data generation, and growing applications in manufacturing quality control.

Kanto Region dominates with 37.6% national revenue share in 2025, anchored by Tokyo's enterprise base, AI startup density, government R&D, and the country's leading universities and venture funding networks.

Key drivers include enterprise AI adoption, the Society 5.0 framework, healthcare digitization, labor shortages pushing automation, expanding domestic LLMs, and government investment in foundation-model research and infrastructure.

Major players include SoftBank Corp., NEC Corporation, Fujitsu, Sony Group Corporation, NTT, Inc., Hitachi Ltd., and Preferred Networks, Inc.

Healthcare and drug discovery is among the fastest-growing applications, advancing at an estimated 21-23% CAGR through 2030, driven by pharmaceutical AI partnerships, medical imaging, and clinical decision support tools.

Opportunities include healthcare AI, manufacturing synthetic-data pipelines, anime and gaming AI tools, Japanese-language foundation models, on-premise enterprise deployment, and Southeast Asian export of Japan-built models.

Society 5.0 prioritizes generative AI as foundational national technology, channeling government procurement, university research grants, and structured demand toward domestic vendors, accelerating Japan's competitive positioning in foundation models and applied AI.

Key challenges include compute cost and power constraints, AI talent shortages, evolving data privacy and copyright regulations, and competitive pressure from established U.S. hyperscale providers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade