Japan Health and Wellness Market Size, Share, Trends and Forecast by Product Type, Functionality, and Region 2026-2034

Japan Health and Wellness Market Size, Share, Trends & Forecast (2026-2034)

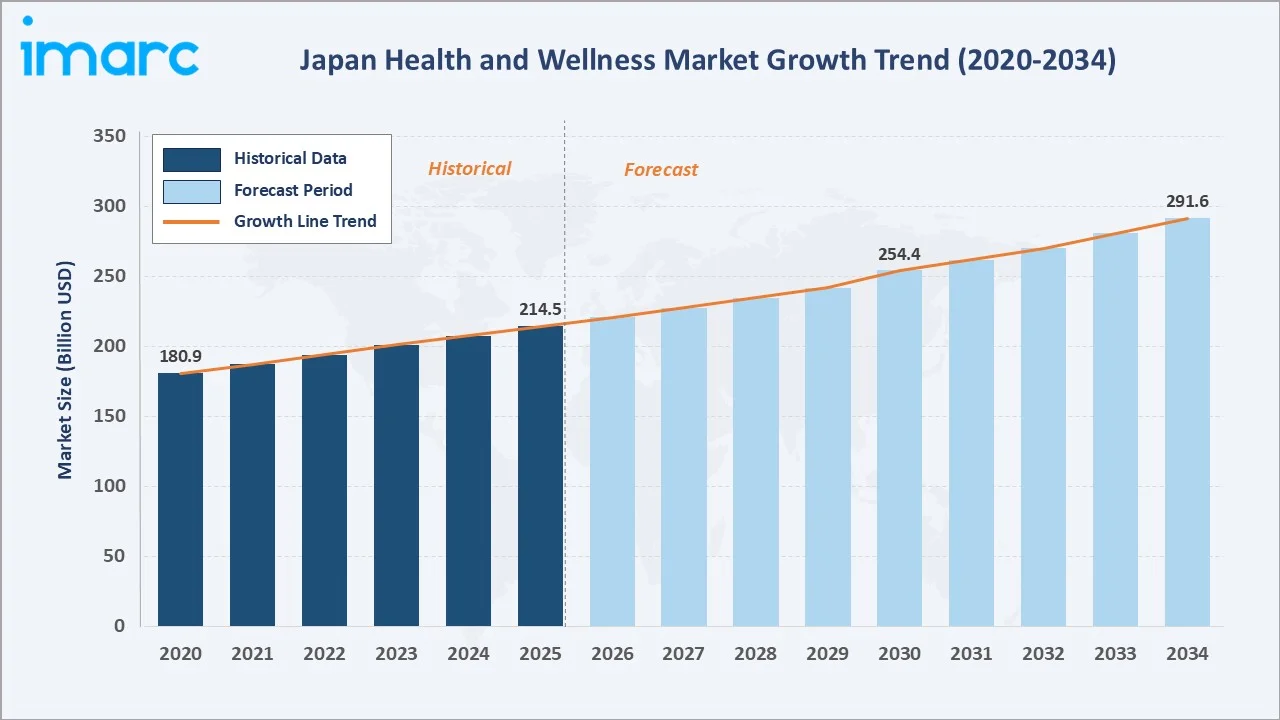

The Japan health and wellness market was valued at USD 214.5 Billion in 2025 and is projected to reach USD 291.6 Billion by 2034, exhibiting a CAGR of 3.47% during 2026-2034. Market growth is driven by Japan's aging population, rising preventive healthcare awareness, increasing demand for functional foods and dietary supplements, and the expanding adoption of personalized wellness solutions.

Functional foods and beverages lead product type at 38.6%, nutrition and weight management lead functionality at 24.8%, and Kanto Region commands 36.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 214.5 Billion |

|

Forecast Market Size (2034) |

USD 291.6 Billion |

|

CAGR (2026-2034) |

3.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (36.5%, 2025) |

|

Second Largest Region |

Kansai/Kinki Region (18.8%, 2025) |

|

Leading Product Type |

Functional Foods and Beverages (38.6%, 2025) |

|

Leading Functionality |

Nutrition and Weight Management (24.8%, 2025) |

The Japan health and wellness market expanded from USD 180.9 Billion in 2020 to USD 214.5 Billion in 2025, underpinned by deepening preventive health awareness and government-backed nutritional programs. Anchored at USD 254.4 Billion in 2030, the forecast to USD 291.6 Billion by 2034 is supported by rapid personalized nutrition growth, accelerating beauty-from-within trends, and the convergence of digital health monitoring with targeted supplement and beverage consumption.

To get more information on this market, Request Sample

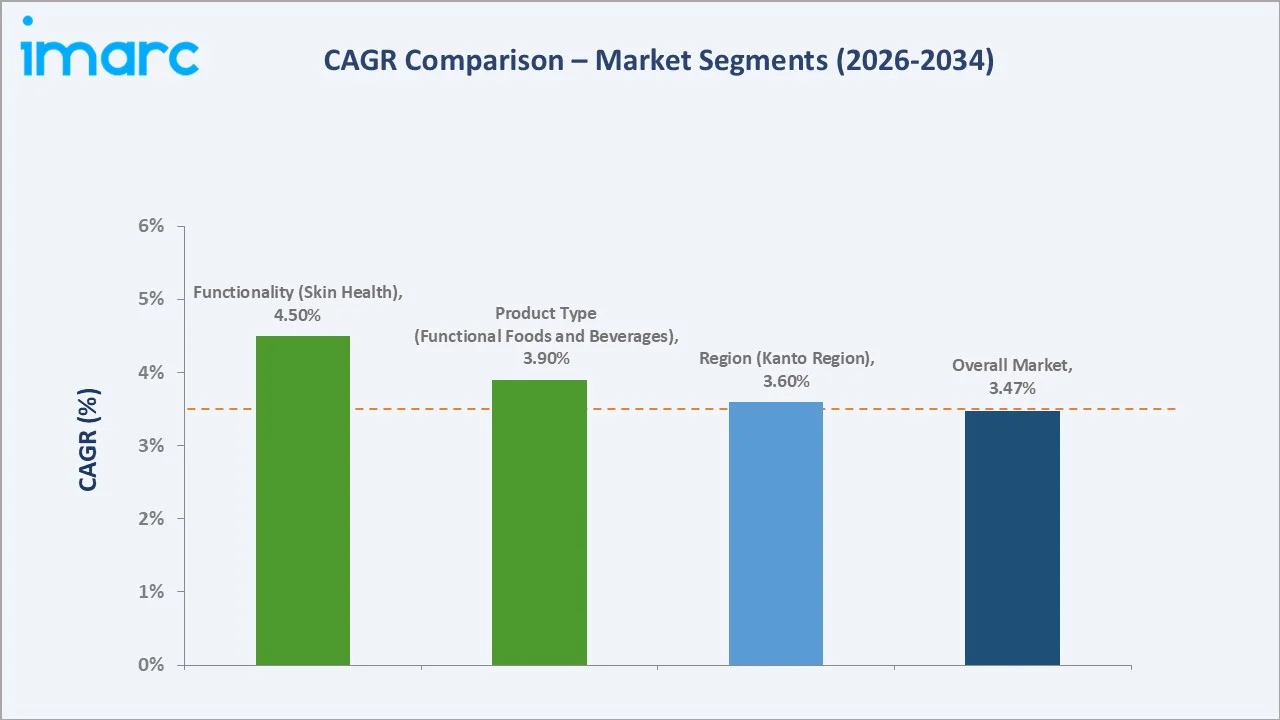

CAGR trajectories across product type and functionality sub-segments show preventive and personalized medicinal products and skin health expanding faster than the overall 3.47% market CAGR, driven by an aging consumer base, rising e-commerce penetration of health products, and the growing influence of healthcare professionals in consumer wellness decisions.

Executive Summary

The Japan health and wellness market is on a sustained growth trajectory from USD 180.9 Billion in 2020 to USD 291.6 Billion by 2034. The market has evolved from conventional food and pharmaceutical boundaries toward a broad, consumer-led wellness ecosystem encompassing functional foods and beverages, beauty and personal care, and preventive medicinal products. Japan's unique demographic structure, anchored by high life expectancy and one of the oldest median-age populations globally, is driving structural demand for health-optimizing, longevity-supporting, and disease-prevention products across all consumer cohorts.

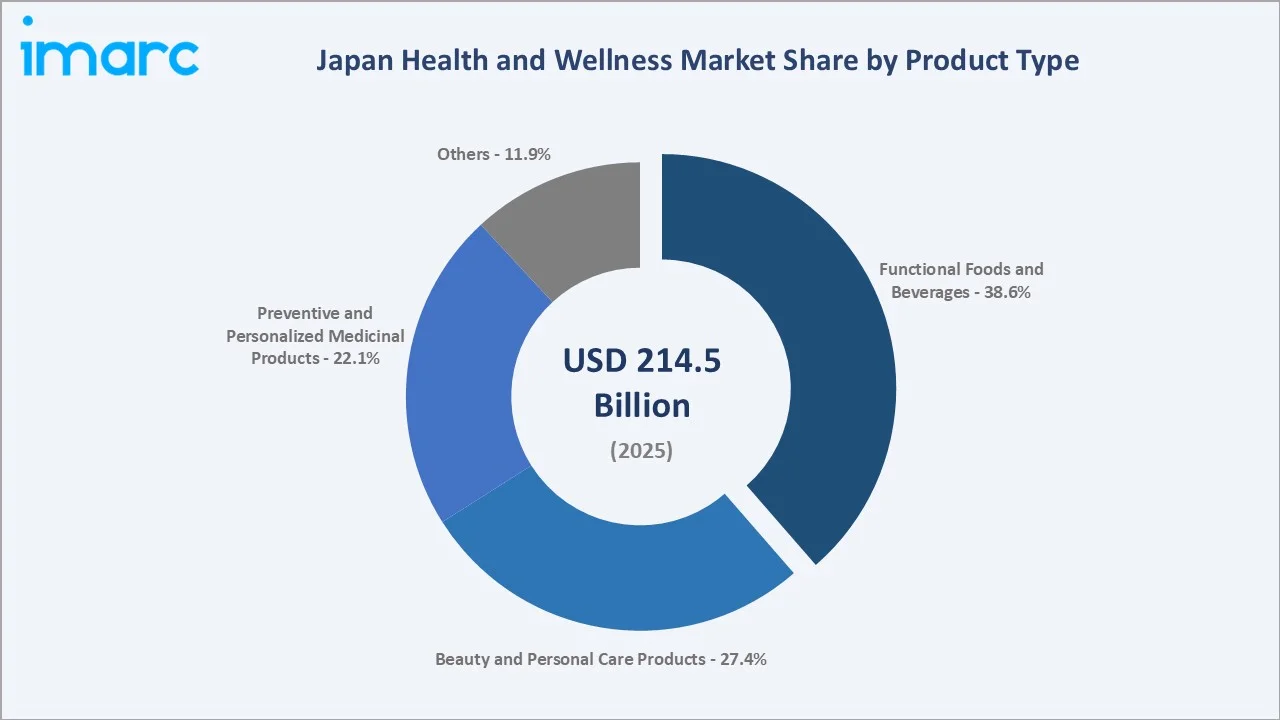

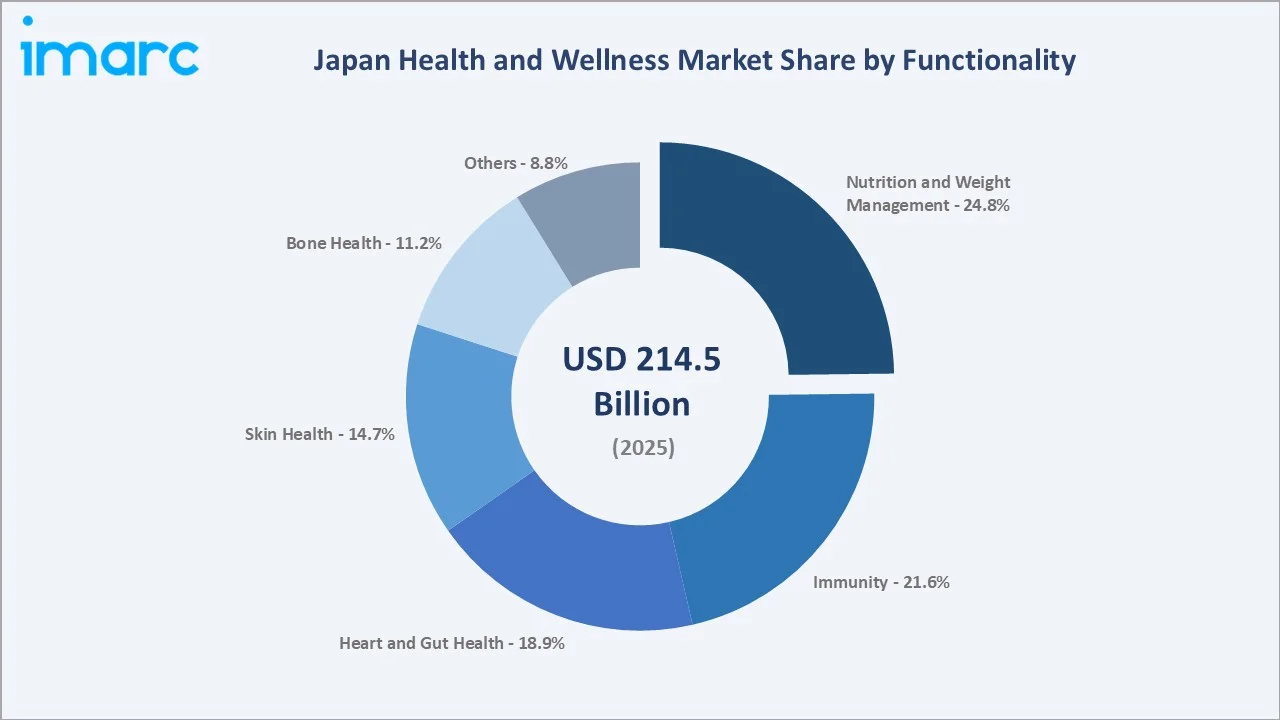

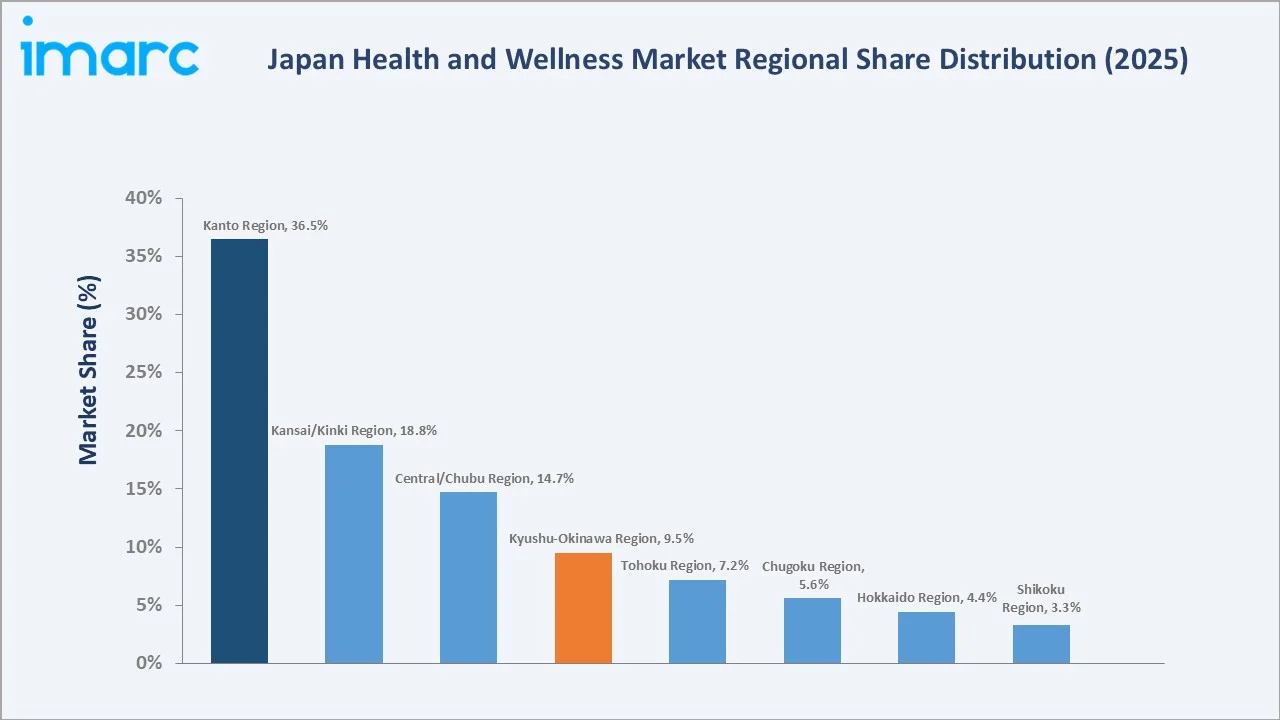

Functional foods and beverages dominate product type at 38.6% in 2025, supported by Japan's deeply embedded FOSHU regulatory framework, widespread consumer trust in functional ingredient science, and a mature distribution network spanning convenience stores, pharmacies, and e-commerce channels. As per IMARC Group, the Japan e-commerce market size was valued at USD 286.5 Billion in 2025. Nutrition and weight management prevail over the functionality segment with a 24.8% share, driven by growing consumer focus on balanced diets, weight control, and preventive health. Kanto Region commands 36.5% of the regional market, anchored by Tokyo's role as the national hub for product launches, retail innovation, and health-conscious urban consumption.

Key Market Insights

|

Insight |

Data |

|

Leading Product Type |

Functional Foods and Beverages – 38.6% share (2025) |

|

Second Largest Product Type |

Beauty and Personal Care Products – 27.4% share (2025) |

|

Leading Functionality |

Nutrition and Weight Management – 24.8% share (2025) |

|

Second Largest Functionality |

Immunity – 21.6% share (2025) |

|

Leading Region |

Kanto Region – 36.5% share (2025) |

|

Second Largest Region |

Kansai/Kinki Region – 18.8% share (2025) |

|

Top Companies |

Yakult Honsha Co., Ltd., Kao Corporation, Otsuka Holdings Co., Ltd., Meiji Holdings Co., Ltd., Shiseido Company, Limited |

Key Analytical Observations Supporting the Above Data:

- Functional foods and beverages at 38.6% represent the largest product type, powered by Japan's government-backed FOSHU and Food with Function Claims (FFC) labeling systems that institutionalize consumer trust in science-verified functional products across retail, pharmacy, and convenience channels.

- Beauty and personal care products at 27.4% are propelled by anti-aging demand from Japan's 50+ consumer cohort, the integration of active cosmeceutical ingredients, and the growing appeal of collagen-enriched, UV-protective, and microbiome-supporting formulations as a mainstream daily wellness ritual.

- Nutrition and weight management at 24.8% lead functionality, supported by rising metabolic syndrome awareness among the aging population, the growth of meal replacement and low-glycemic functional food formats, and active government anti-obesity initiatives in public health policy. As of September 2024, individuals aged 65 and older in Japan made up almost 30% of the population, according to government data.

- Immunity at 21.6% represents the second-largest functionality segment, driven by strong demand for probiotic, prebiotic, vitamin C, zinc, and elderberry formulations across food, beverage, and supplement products.

- Kanto Region at 36.5% dominates regional share, anchored by the Tokyo metropolitan area's dense retail ecosystem, advanced e-commerce infrastructure, and the concentration of leading wellness brand headquarters, innovation labs, and clinical research partnerships within the region.

Japan Health and Wellness Market Overview

Health and wellness encompass a holistic approach to maintaining physical, mental, nutritional, and preventive well-being through lifestyle choices, healthcare solutions, and consumer products designed to support long-term quality of life. The Japan health and wellness market includes products and services that support physical health, nutritional wellbeing, mental wellness, aesthetic health, and preventive disease management, while addressing growing consumer demand for healthy aging, functional nutrition, self-care, and long-term wellness maintenance.

The market ecosystem integrates raw material and active ingredient suppliers, domestic and international manufacturers, regulatory authorities, retail and pharmacy distribution networks, e-commerce platforms, and end consumers spanning all demographic segments with particularly concentrated demand among adults aged 50 and above.

Market Dynamics

To evaluate market opportunities, Request Sample

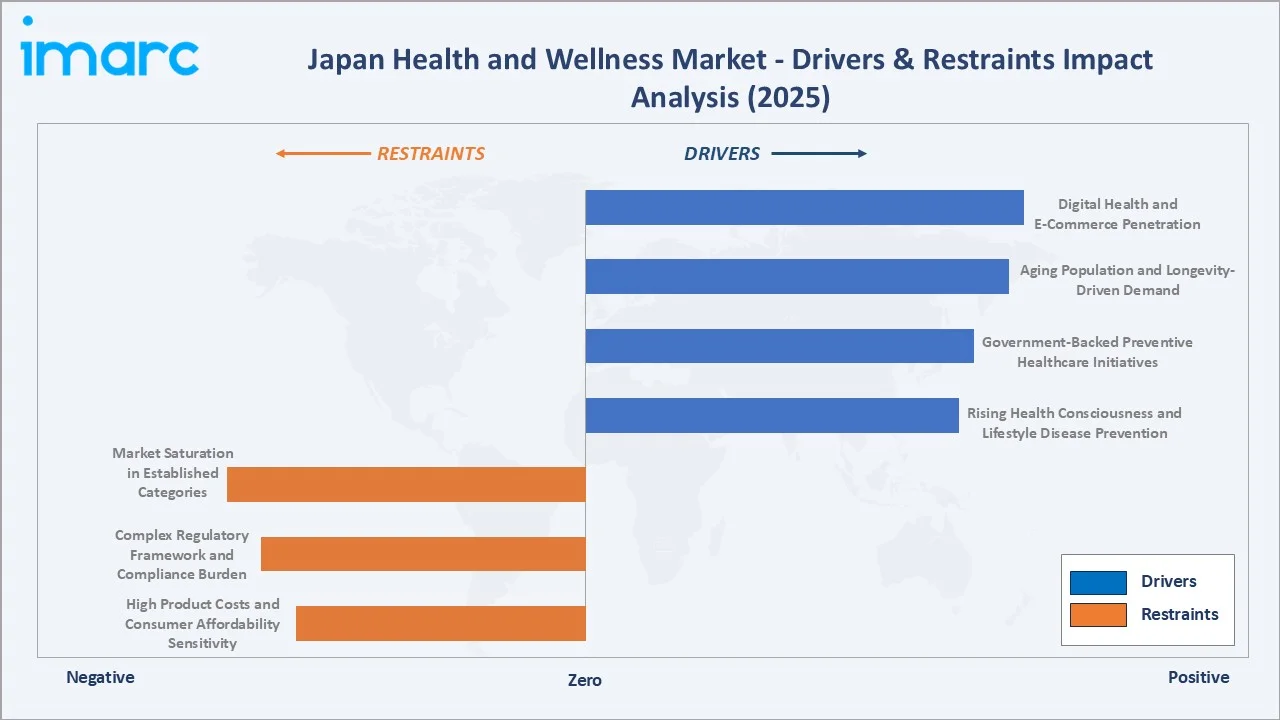

Market Drivers

- Aging Population and Longevity-Driven Demand: Japan's demographic structure is creating structurally elevated demand for products targeting bone health, joint mobility, cognitive function, cardiovascular wellness, and metabolic management. The elderly consumer segment in Japan spends disproportionately on preventive health products compared to younger cohorts, sustaining high per-capita wellness expenditure.

- Government-Backed Preventive Healthcare Initiatives: Japan's national health policy actively encourages functional food consumption and preventive supplementation. These programs reduce consumer skepticism, provide product differentiation through government-recognized health claims, and stimulate R&D investment by linking regulatory approval to commercial advantage.

- Rising Health Consciousness and Lifestyle Disease Prevention: Increasing prevalence of metabolic syndrome, hypertension, and type 2 diabetes among working-age Japanese adults is driving preventive product adoption across nutrition, weight management, and gut health categories. Consumer willingness to invest in health products as a cost-effective alternative to long-term pharmaceutical treatment is reinforcing category growth across functional foods, supplements, and personalized health solutions.

- Digital Health and E-Commerce Penetration: The rapid expansion of health-focused e-commerce platforms, subscription supplement services, and AI-driven personalization engines is lowering the barrier for consumer access to premium wellness products. Major retailers and brand-direct digital channels are increasingly the primary point of purchase for supplement, beauty, and functional food products among younger and middle-aged consumer segments.

Market Restraints

- High Product Costs and Consumer Affordability Sensitivity: Premium health and wellness products in Japan carry significant price premiums compared to conventional food and pharmaceutical alternatives, limiting category penetration among lower-income households and price-sensitive consumer segments. The cost differential is particularly pronounced for personalized nutrition programs, advanced cosmeceutical formulations, and evidence-based preventive supplementation regimens.

- Complex Regulatory Framework and Compliance Burden: Japan's multi-tier regulatory system, encompassing FOSHU approvals and FFC notifications, requires substantial investment in clinical evidence generation, regulatory filings, and ongoing compliance. These barriers disproportionately impact smaller domestic manufacturers and international brands seeking market entry.

- Market Saturation in Established Categories: Japan's functional food and supplement industry is among the most mature globally, with high SKU density, intense price competition, and compressed category growth rates in legacy segments, such as calcium supplementation, basic multivitamins, and conventional probiotic beverages. New entrants and growth-stage brands face significant shelf space and consumer attention competition in established segments.

Market Opportunities

- Precision and Personalized Nutrition Expansion: The convergence of genetic testing, microbiome analysis, and AI-driven dietary recommendation is creating a high-growth frontier in personalized wellness. Japanese consumers demonstrate strong receptivity to evidence-based personalization, and the regulatory environment is evolving to accommodate tailored supplement and functional food claims, creating early-mover advantage for brands investing in this segment.

- Premiumization of Beauty-From-Within Segment: The intersection of Japan's globally preeminent beauty culture with functional ingredient science is generating sustained premiumization in collagen peptide beverages, hyaluronic acid supplements, and ceramide-enriched functional foods. Export-led growth opportunities are equally compelling, as Japanese beauty wellness brands command premium positioning in China, South Korea, and Southeast Asian markets.

Market Challenges

- Consumer Trust and Scientific Substantiation Requirements: Japanese consumers are among the most scientifically literate and evidence-demanding in the world when evaluating health product claims. Brands must invest substantially in clinical studies, third-party verification, and transparent ingredient disclosure to earn and retain consumer trust, raising go-to-market costs and elongating product development timelines.

- Intensifying Competition from International Brands: The increasing availability of international health and wellness brands through e-commerce channels is intensifying competitive pressure on domestic manufacturers. North American, European, and Australian supplement and functional food brands are entering the Japanese market with differentiated ingredient profiles, competitive pricing, and global brand recognition.

Emerging Market Trends

1. Personalized Nutrition and Precision Supplementation

Japanese consumers are increasingly adopting individualized nutrition strategies informed by genetic profiling, gut microbiome analysis, and continuous blood glucose monitoring. Brands are offering subscription-based personalized supplement regimens and AI-curated dietary plans.

2. Beauty-From-Within and Cosmeceutical Convergence

The convergence of Japan's globally preeminent beauty culture with functional ingredient science is reshaping the beauty and personal care products segment. Collagen peptide beverages, hyaluronic acid supplements, and ceramide-enriched functional foods are increasingly prescribed by dermatologists and beauty professionals, elevating their credibility beyond cosmetic positioning.

3. Gut-Brain Axis and Psychobiotic Innovation

Scientific validation of the gut-brain connection is accelerating product development in psychobiotic foods, fermented functional beverages, and GABA-enriched products targeting stress, sleep quality, and cognitive function. Japan's deeply embedded cultural tradition of fermented food consumption, led by natto, miso, and yogurt, provides a favorable foundation for clinical-grade psychobiotic product development.

4. Digital Health Integration with Physical Wellness Products

Wearable health monitoring devices, smart nutrition apps, and AI-powered supplement recommendation platforms are increasingly integrated with physical product consumption in Japan. Companies are creating closed-loop ecosystems where biometric data from wearables triggers personalized dietary and supplementation recommendations delivered through subscription product services. This digital-physical integration is driving higher consumer engagement, increased product retention rates, and more favorable long-term health outcomes.

5. Sustainability and Clean Label Wellness

Japanese wellness consumers are demonstrating heightened sensitivity to ingredient transparency, sustainable sourcing, and minimal-processing product claims. Clean label functional foods, plant-based protein supplements, and sustainably certified botanical extracts are growing rapidly across both domestic consumption and export markets. Brands are responding by reformulating products to remove synthetic additives, investing in traceability certification, and communicating provenance through digital QR code labeling systems directly accessible to end consumers at point of purchase.

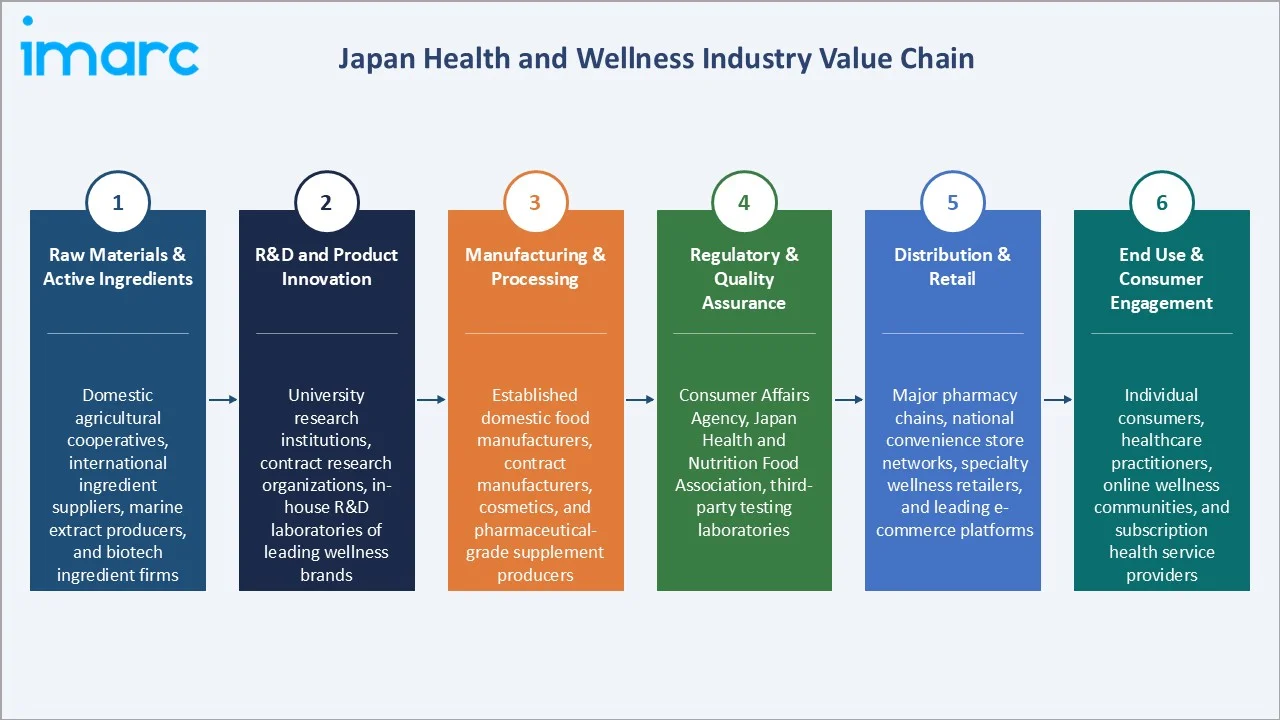

Industry Value Chain Analysis

The Japan health and wellness value chain spans six stages from raw material and active ingredient sourcing through end user engagement and long-term health management. Manufacturing, regulatory compliance, and direct-to-consumer digital distribution capture the highest value-add in the current market structure, while R&D investment increasingly determines sustainable competitive positioning as health claim substantiation requirements intensify.

|

Stage |

Key Players / Examples |

|

Raw Materials & Active Ingredients |

Domestic agricultural cooperatives, international ingredient suppliers, marine extract producers, and biotech ingredient firms |

|

R&D and Product Innovation |

University research institutions, contract research organizations, in-house R&D laboratories of leading wellness brands |

|

Manufacturing & Processing |

Established domestic food manufacturers, contract manufacturers, cosmetics production facilities, and pharmaceutical-grade supplement producers |

|

Regulatory & Quality Assurance |

Consumer Affairs Agency, Japan Health and Nutrition Food Association, third-party testing laboratories |

|

Distribution & Retail |

Major pharmacy chains, national convenience store networks, specialty wellness retailers, and leading e-commerce platforms |

|

End Use & Consumer Engagement |

Individual consumers, healthcare practitioners, corporate wellness programs, online wellness communities, and subscription health service providers |

Established brands supported by scientific validation, regulatory compliance, and extensive distribution networks achieve greater consumer trust and market penetration than smaller niche players.

Technology Landscape in the Japan Health and Wellness Industry

Functional Ingredient Science and Bioactive Compound Innovation

Japanese researchers and manufacturers are at the global forefront of bioactive compound identification, extraction optimization, and clinical efficacy verification. Advanced fermentation technologies, precision enzymatic processing, and nano-encapsulation techniques are enabling higher bioavailability of functional ingredients across food, beverage, and supplement matrices. Continuous investment in food biotechnology is producing new generations of clinically validated functional ingredients with enhanced stability, target specificity, and regulatory approvability under Japan's FOSHU and FFC frameworks.

AI and Personalized Health Recommendation

AI and machine learning (ML) models are increasingly deployed across supplement recommendation platforms, nutrition counseling applications, and consumer health monitoring ecosystems. These systems integrate dietary intake data, biometric signals from wearable devices, genetic profiles, and clinical biomarkers to generate individualized wellness protocols. AI-driven personalization is enabling brands to move beyond population-level health claims toward targeted, evidence-supported individual health outcomes.

Digital Health Monitoring and Connected Wellness Ecosystems

Wearable health devices, continuous glucose monitors, sleep tracking systems, and smart nutrition scales are creating rich real-time data streams that brands are integrating with subscription product services. Japan's high consumer technology adoption rate and advanced mobile connectivity infrastructure position the market as a global pioneer in connected wellness product ecosystems.

Advanced Cosmeceutical and Dermocosmetic Technologies

Japan's beauty and personal care products segment is deploying advanced technologies, including liposomal active delivery systems, biofermentation-derived beauty actives, microbiome-balancing probiotic cosmetics, and precision anti-aging formulations, validated through clinical dermatology studies. These technologies are elevating functional efficacy standards across the beauty wellness segment, creating significant barriers to entry for less technologically sophisticated competitors.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Functional Foods and Beverages |

38.6% |

2025 |

|

Functionality |

Nutrition and Weight Management |

24.8% |

2025 |

|

Region |

Kanto Region |

36.5% |

2025 |

By Product Type

Functional foods and beverages command a 38.6% majority share in 2025, underpinned by Japan's internationally unique regulatory framework for functional food claims, high consumer literacy regarding evidence-based health ingredients, and a distribution network that places functional beverages, probiotic dairy products, and fortified snacks within reach of virtually every Japanese consumer through dense convenience store and pharmacy networks.

To access detailed market analysis, Request Sample

Beauty and personal care products at 27.4% in 2025 represent Japan's globally distinctive contribution to the wellness category. Driven by anti-aging demands of an older consumer demographic, the scientific credibility of domestic cosmeceutical brands, and growing international export appeal, this segment integrates cosmetic functionality with bioactive health outcomes.

By Functionality

Nutrition and weight management dominate functionality at 24.8% in 2025, reflecting the structural demand from Japan's aging population for metabolic health management products, including meal replacements, protein supplements, low-glycemic functional foods, and clinical-grade dietary fiber formulations. Government anti-obesity initiatives and increasing physician recommendation of nutritional interventions are further institutionalizing this category within Japan's broader preventive healthcare ecosystem.

Immunity at 21.6% is the second-largest functionality segment, supported by sustained consumer interest in preventive health, immune resilience, and overall well-being. Demand remains strong for products containing probiotics, prebiotics, vitamins, minerals, and botanical ingredients that support daily health maintenance and wellness goals.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

36.5% |

Large urban population, dense retail and pharmacy network, high health consciousness, and concentration of leading wellness brand operations |

|

Kansai/Kinki Region |

18.8% |

Strong pharmaceutical and nutraceutical manufacturing base, rising preventive health adoption, and growing e-commerce wellness penetration |

|

Central/Chubu Region |

14.7% |

Expanding retail infrastructure, aging population health demand, growing functional food consumption, and increasing preventive healthcare awareness |

|

Kyushu-Okinawa Region |

9.5% |

Okinawa's internationally recognized longevity food culture, growing tourism-driven wellness demand, and expanding organic and traditional health product markets |

|

Tohoku Region |

7.2% |

Rising health awareness post-natural disasters, growing functional food adoption, expanding pharmacy networks, and government regional health investment |

|

Chugoku Region |

5.6% |

Steady demographic demand from aging population, expanding rural pharmacy access, and growing online wellness product penetration |

|

Hokkaido Region |

4.4% |

Strength in dairy-based functional food production, growing health tourism, and expanding natural and organic wellness product consumption |

|

Shikoku Region |

3.3% |

Niche longevity and pilgrimage-wellness culture, growing preventive health adoption among aging population, and expanding online retail access |

Kanto Region at 36.5% in 2025 leads the regional landscape, anchored by the Tokyo metropolitan area's role as Japan's primary hub for health and wellness brand launches, clinical nutrition research partnerships, premium retail experiences, and health-conscious urban consumer demand.

Kansai/Kinki Region at 18.8% represents the second-largest market, supported by Osaka and Kyoto's strong pharmaceutical and nutraceutical manufacturing heritage, growing preventive health adoption among urban and suburban consumers, and increasing e-commerce penetration of premium wellness product categories.

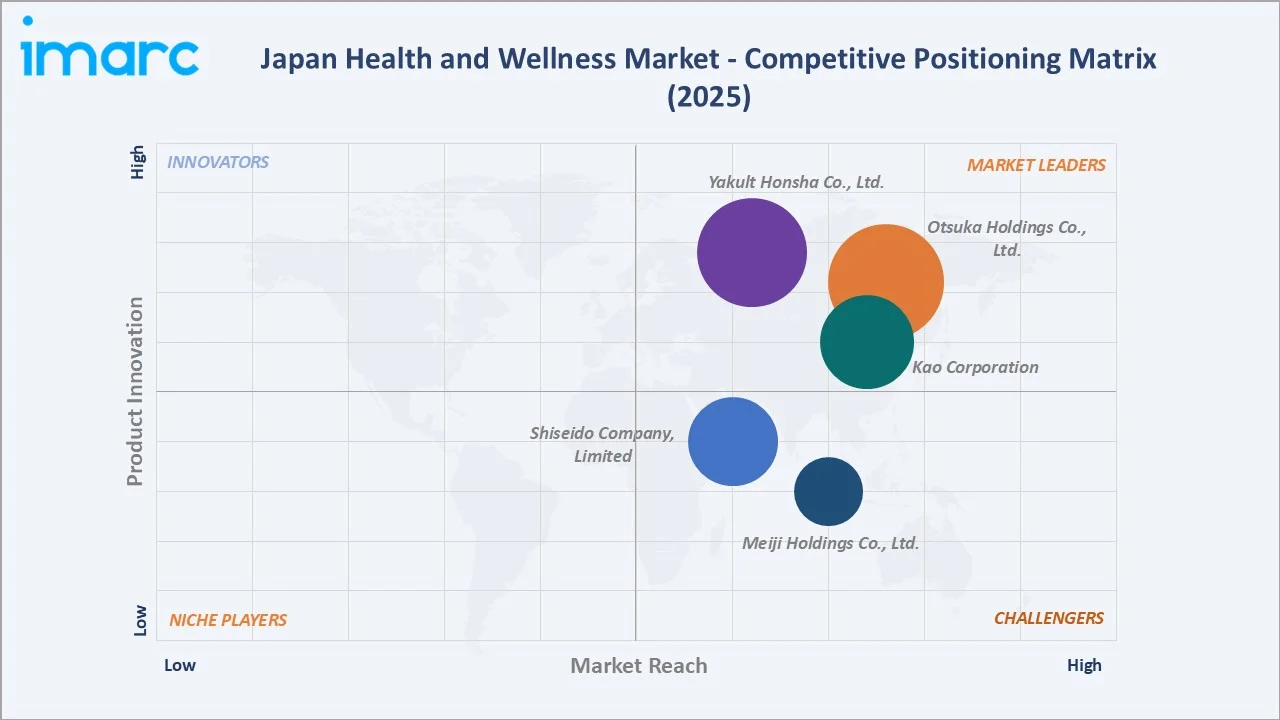

Competitive Landscape

The Japan health and wellness market is moderately concentrated, with established domestic conglomerates holding significant market positions across functional foods, personal care, and supplement categories, while emerging digital-native brands and international entrants compete in precision nutrition, premium cosmeceuticals, and specialty supplement segments. Brand equity built on scientific credibility, regulatory approval portfolios, and deep distribution networks forms the primary competitive moat in this high-trust, evidence-sensitive market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Yakult Honsha Co., Ltd. |

Yakult 1000 |

Leader |

Science-led probiotic innovation and global gut health brand leadership |

|

Kao Corporation |

Curel , Bioré |

Leader |

Beauty-health integration through skin science innovation and premium cosmetics brand development |

|

Otsuka Holdings Co., Ltd. |

Calorie Mate, POCARI SWEAT |

Leader |

Broad-spectrum health and nutrition solutions with pharmaceutical-wellness integration |

|

Meiji Holdings Co., Ltd. |

Meiji Probio Yogurt R-1 |

Challenger |

Dairy and protein-based functional food innovation with clinical health validation |

|

Shiseido Company, Limited |

ELIXIR, ANESSA |

Challenger |

Cosmeceutical leadership through science-backed beauty wellness and international brand expansion |

Key players include Yakult Honsha Co., Ltd., Kao Corporation, Otsuka Holdings Co., Ltd., Meiji Holdings Co., Ltd., and Shiseido Company, Limited, among others.

Key Company Profiles

Yakult Honsha Co., Ltd.

Yakult Honsha Co., Ltd. is a Japan-based food and health products company engaged in the research, manufacture, and sale of probiotic beverages, dairy products, pharmaceuticals, and cosmetics. The company operates across domestic and international markets, maintaining a significant presence in Asia, the Americas, Europe, and Oceania through retail and direct-to-consumer distribution channels.

- Product Portfolio: The company offers a range of probiotic beverages, fermented dairy products, health supplements, cosmetics, and pharmaceutical products. Its probiotic beverage portfolio includes products across standard, premium, and functional health claim formats targeting gut health, immunity, and overall wellness for consumers across age groups.

- Recent Developments: The company continues to expand its health and wellness offerings through product innovation, strategic partnerships, digital engagement initiatives, and investments in R&D to address evolving consumer preferences.

- Strategic Focus: The company focuses on advancing probiotic science and expanding its international footprint through science-backed product development, clinical research partnerships, and investment in distribution infrastructure across growth markets.

Kao Corporation

Kao Corporation is a Japan-based manufacturer of consumer products operating across hygiene and living care, health and beauty care, cosmetics, and specialty chemical segments. The company serves consumers across domestic and international markets through a portfolio of personal care, skincare, hair care, and household product brands.

- Product Portfolio: The company's health and beauty care portfolio includes skincare products for sensitive skin and cosmetic products across mass and premium segments. Its product range also encompasses fabric care, feminine hygiene, baby care, and professional hair care categories serving daily consumer needs.

- Recent Developments: The company has been concentrating investments in core beauty and skincare brands with strong global competitive positions. Consecutive market share gains have been achieved in key skincare categories in Japan.

- Strategic Focus: The company focuses on advancing skin science and beauty innovation through proprietary research in ceramide technology, UV protection, and bio-fermentation-derived actives, with investment concentrated in globally competitive premium and mass beauty brands.

Otsuka Holdings Co., Ltd.

Otsuka Holdings Co., Ltd. is a Japan-based total healthcare group operating across pharmaceutical, nutraceutical, and food science businesses. The company develops and markets science-based health products spanning functional beverages, nutritional foods, dietary supplements, and pharmaceutical products across domestic and international markets.

- Product Portfolio: The company's nutraceutical portfolio includes isotonic hydration beverages, balanced nutritional food products, protein-enriched snack formats, vitamin-enriched energy drinks, and dietary fiber products. Its functional beverage and nutritional food products are distributed across Japan and in multiple international markets.

- Recent Developments: The company has advanced its consumer health strategy through innovation in functional beverages, nutritional foods, and preventive wellness solutions supported by scientific research.

- Strategic Focus: The company focuses on bridging pharmaceutical-grade science with accessible consumer health products, developing evidence-based nutrition and hydration solutions that address everyday health maintenance needs across diverse demographic groups.

Market Concentration Analysis

The Japan health and wellness market exhibits moderate concentration at the product category level, with the top five companies collectively accounting for an estimated 35–40% of total market value. Market concentration is highest within specific functional food and beverage sub-segments, where FOSHU-approved brands benefit from regulatory differentiation and entrenched consumer trust, and lowest in the fragmented dietary supplement segment, where hundreds of domestic and international brands compete across multiple distribution channels.

Barriers to sustained competitive position are high in this market. They include the capital and time investment required for clinical evidence generation supporting FOSHU and FFC claims, the multi-year brand-building required to establish consumer trust for health product recommendations, and the continuous R&D investment required to maintain ingredient science leadership in rapidly evolving functionality segments.

Consolidation is progressing as mid-sized domestic players face increasing pressure from both large conglomerates expanding their wellness portfolios and digital-native challenger brands leveraging direct-to-consumer models to build specialized segment leadership. Strategic acquisitions of boutique supplement brands, ingredient technology start-ups, and digital health platforms are expected to accelerate throughout the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Preventive and personalized medicinal products represent the fastest-growing product type category, driven by expanding access to genetic health testing, growing consumer investment in evidence-based disease prevention, and the integration of AI-driven health monitoring with personalized supplement prescriptions. Within functionality, skin health is growing above-market CAGR, fueled by beauty-from-within product premiumization and the clinical validation of ingestible skincare actives.

Emerging Regional Markets

Kansai/Kinki Region is the fastest-growing major region, supported by investment in nutraceutical manufacturing capacity expansion, growing urban preventive health adoption, and increasing e-commerce wellness penetration. Kyushu-Okinawa Region at 9.5% represents a strategically compelling opportunity for longevity-positioned product brands, given Okinawa's globally recognized blue zone health culture and growing wellness tourism demand.

Venture & Investment Trends

Investment is concentrated in digital health and wellness platforms that integrate wearable data with product recommendation, personalized nutrition start-ups leveraging microbiome and genetic analysis, and direct-to-consumer premium supplement brands targeting specific health conditions with clinical-grade formulations.

Future Market Outlook (2026-2034)

The Japan health and wellness market is forecast to expand from USD 214.5 Billion in 2025 to USD 291.6 Billion by 2034 at a CAGR of 3.47%, adding approximately USD 77.1 Billion in incremental market value over the forecast period.

Four forces will define the market through 2034: the deepening integration of digital health monitoring with physical wellness product consumption; the rapid maturation of personalized nutrition as a mainstream consumer category; accelerating government investment in preventive healthcare infrastructure aligned with Japan's Society 5.0 health technology vision; and the global expansion of Japanese wellness brands leveraging the country's internationally recognized functional food science leadership and clean ingredient reputation.

By 2034, Kanto Region is expected to remain the dominant market force, supported by its high population density, concentration of healthcare infrastructure, strong purchasing power, and rapid adoption of premium health and wellness products and services.

Research Methodology

Primary Research

Primary research included structured interviews with functional food manufacturers, supplement brand executives, pharmacy chain buyers, healthcare professionals including registered dietitians and general physicians, and regulatory specialists in Japan's FOSHU and FFC framework.

Secondary Research

Secondary sources included publications from Japan's Ministry of Health, Labour and Welfare, Consumer Affairs Agency functional food claim databases, Japan Health and Nutrition Food Association industry reports, annual reports and investor presentations from key market participants, Japan National Health and Nutrition Survey data, and academic literature on functional food science and consumer health behavior published by Japanese and international research institutions.

Forecasting Models

Market forecasts were developed using top-down and bottom-up modeling approaches. Top-down analysis incorporated Japan's macroeconomic outlook, healthcare expenditure trends, and demographic projections from Statistics Japan. Bottom-up analysis aggregated segment-level demand projections across product type, functionality, and regional dimensions, validated against historical shipment data from industry associations and retail sell-through data from major distribution channels.

Japan Health and Wellness Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Functional Foods and Beverages, Beauty and Personal Care Products, Preventive and Personalized Medicinal Products, Others |

| Functionalities Covered | Nutrition and Weight Management, Heart and Gut Health, Immunity, Bone Health, Skin Health, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Yakult Honsha Co., Ltd., Kao Corporation, Otsuka Holdings Co., Ltd., Meiji Holdings Co., Ltd., Shiseido Company, Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan health and wellness market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan health and wellness market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan health and wellness industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Health and Wellness Market Report

The Japan health and wellness market was valued at USD 214.5 Billion in 2025, driven by Japan's aging population, government preventive healthcare initiatives, and deep functional food science culture.

The market is projected to grow at a CAGR of 3.47% from 2026-2034, reaching USD 291.6 Billion, supported by personalized nutrition adoption, beauty wellness expansion, and digital health integration.

Functional foods and beverages lead at 38.6% in 2025, supported by Japan's FOSHU and FFC regulatory frameworks and high consumer trust in science-backed functional ingredients.

Nutrition and weight management dominate at 24.8% in 2025, driven by metabolic health demand among Japan's aging population and government anti-obesity initiatives.

Kanto Region commands 36.5% in 2025, led by the Tokyo metropolitan area's concentration of premium retail, wellness brand operations, and health-conscious urban consumers.

Leading players include Yakult Honsha Co., Ltd., Kao Corporation, Otsuka Holdings Co., Ltd., Meiji Holdings Co., Ltd., and Shiseido Company, Limited, among others.

Growth is driven by expanding genetic health testing access, increasing physician endorsement of evidence-based supplements, and rising consumer investment in early-stage chronic disease prevention programs.

Key trends include personalized nutrition, gut-brain axis products, beauty-from-within cosmeceuticals, digital health-product integration, and sustainability-driven clean label wellness formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)