Japan Healthcare BPO Market Size, Share, Trends and Forecast by Service, and Region, 2026-2034

Japan Healthcare BPO Market Size & Forecast 2026-2034

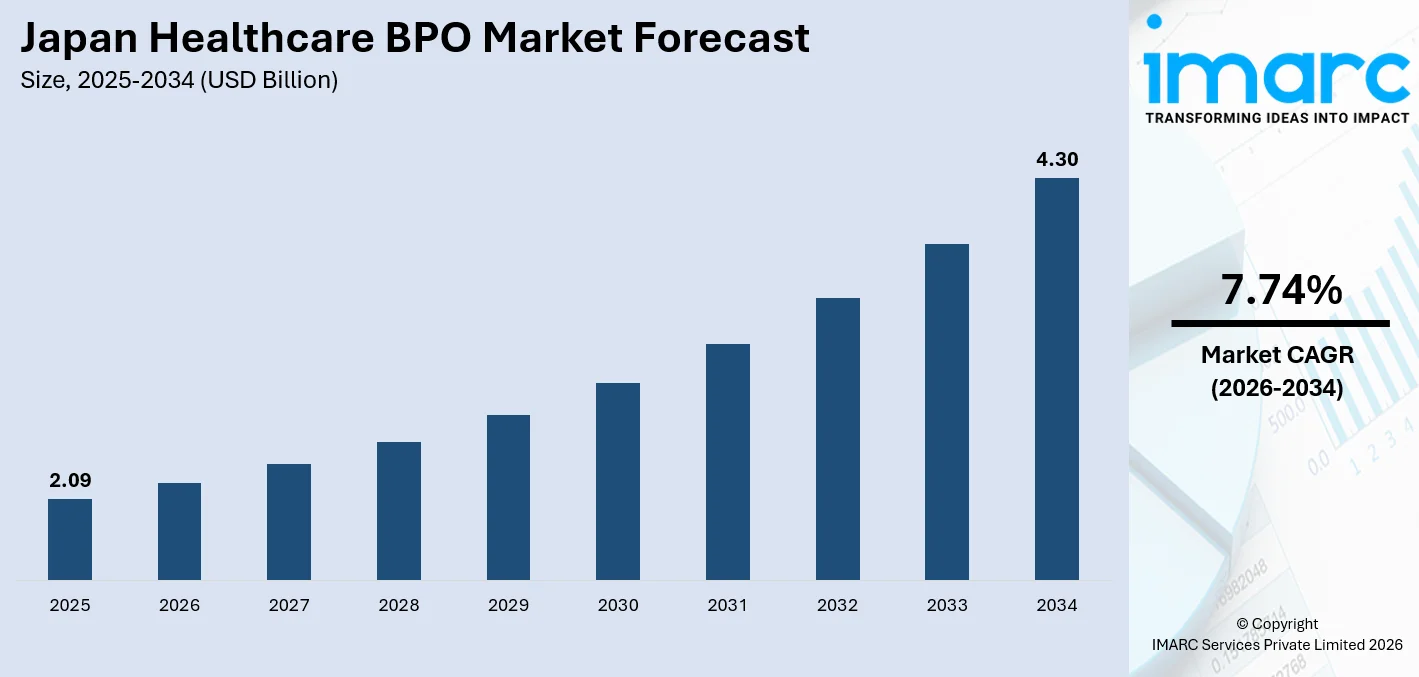

The Japan healthcare BPO market size, valued at USD 2.09 Billion in 2025, is projected to reach USD 4.30 Billion by 2034, growing at a CAGR of 7.74% from 2026-2034, driven by Japan's acute demographic pressures, advancing healthcare digitalization, and expanding pharmaceutical R&D outsourcing. Japan is home to approximately 30% of its population aged 65 or older, creating structural, long-term demand for outsourced administrative and clinical support services.

To get more information on this market Request Sample

Japan Healthcare BPO Industry Analysis - Key Insights

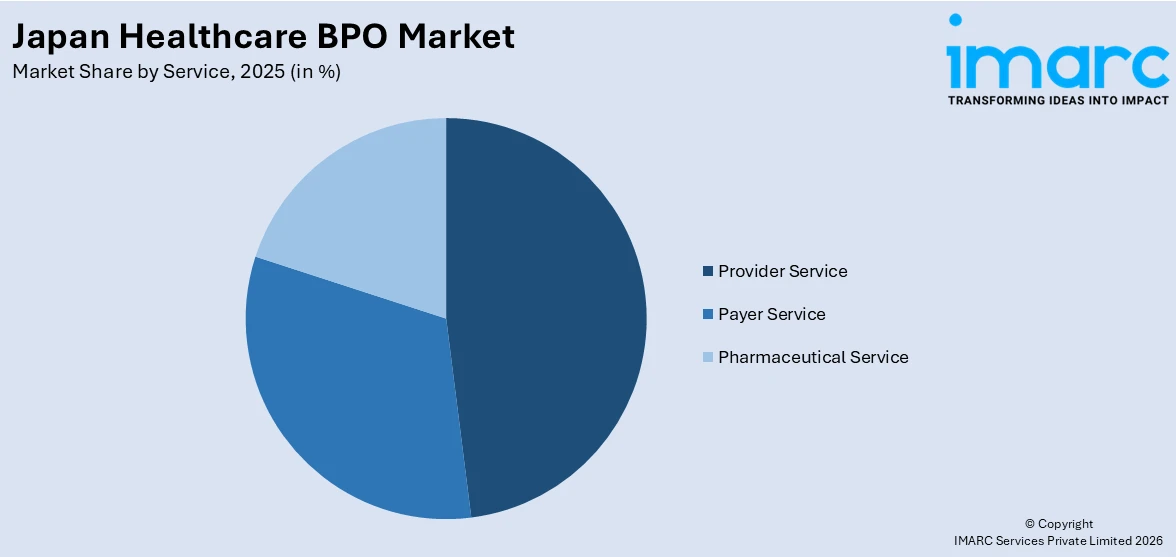

- Provider service commands the service at 44.7% in 2025- the revenue cycle management and patient care service sub-segments anchor this dominance, as Japan's hospitals and clinics outsource billing, coding, and patient enrolment to manage staff shortages and cost pressures.

- Kanto Region leads regionally at 42.3% in 2025- Tokyo's concentration of corporate hospital chains, national pharmaceutical headquarters, and leading IT/BPO vendors creates a self-reinforcing ecosystem for healthcare outsourcing, anchoring almost half of national market revenue in a single region.

Japan Healthcare BPO Market Trends and Dynamic 2026

Market Trends

AI-Powered Automation and Digital Health Integration Reshaping Administrative Workflows

Japan's healthcare institutions are rapidly adopting AI-driven tools to automate administrative and clinical support processes, a structural shift that is expanding the scope and sophistication of BPO mandates. In May 2025, Fujitsu and Tokai National Higher Education and Research System completed field trials using generative AI to process clinical data from approximately 1,800 patient records at Nagoya University and Gifu University, with the system demonstrating the capacity to structure unstructured doctor notes for clinical trial participant selection.

Government Healthcare DX Mandate Driving Cloud Migration and BPO Demand

Japan's MHLW Healthcare DX Promotion Plan formalizes nationwide cloud-based system migration for hospitals and pharmacies, directly creating demand for outsourced implementation, maintenance, and managed services. These Japan healthcare BPO market trends are compelling even the traditionally insourced public hospital network to seek external BPO partners for system management, data migration, and compliance administration.

Pharmaceutical Outsourcing Expansion Fueled by Drug Lag Mitigation and CRO Growth

Japan's pharmaceutical industry is accelerating clinical outsourcing as domestic companies face structural resource constraints and the pressure to resolve persistent drug lag. Direct and indirect employment in Japan's clinical trials sector is estimated at approximately 600,000 people, with CROs and domestic providers experiencing rising volumes of outsourced Phase I–III support from both domestic majors like Takeda, Daiichi Sankyo, and Eisai, and international sponsors entering the Japanese market.

- Revenue Cycle Outsourcing Acceleration: DPC-scheme hospital cost optimization pressures and staff shortages are driving rapid adoption of third-party revenue cycle management and coding services.

- Telehealth Administration Expansion: Telehealth administration expansion increases demand across patient scheduling, claims processing, and digital record management.

- RPA and Process Automation Integration: BPO vendors are embedding robotic process automation to manage Japan's complex multi-payer insurance claims environment, reducing manual processing cycles.

- Specialty-Specific BPO Services: Cardiology, oncology, and geriatric-specific billing and coding services are emerging as premium BPO categories, tailored to Japan's dominant chronic disease and aging patient profile.

Growth Drivers

Acute Healthcare Workforce Shortage and Aging Population Structural Pressure

Japan faces a shortage of healthcare workers, with the government indicating a shortage of 30,000–130,000 nursing personnel under various planning scenarios. With approximately 30% of Japan's population now aged 65 or older, the volume of inpatients with chronic and complex conditions is escalating while the working-age tax base contracts. These compounding demographic pressures have made BPO a structural necessity rather than a cost-efficiency option, as hospitals rely on outsourced administrative, patient care coordination, and claims processing functions to maintain service delivery standards.

Government Policy Support and Healthcare Digital Transformation Investment

Japan's Digital Agency, established in 2021 under Prime Minister Suga's government modernization initiative, embedded digital healthcare transformation as a national priority, accelerating market growth. AMED's ongoing R&D support programs and the 2025 pharmaceutical start-up fund create sustained demand for outsourced clinical data management, regulatory submission support, and manufacturing services across Japan's pharmaceutical services BPO sub-segment.

Rising Chronic Disease Burden Expanding Diagnostic and Care Management Outsourcing

The country's aging demographic structure is mostly aged 65 or older, with multi-morbidity and chronic conditions dominating care pathways. This creates sustained, high-frequency demand for outsourced care management, patient enrollment and strategic planning, and provider management services, particularly as Japan's universal National Health Insurance system imposes strict price controls that incentivise cost reduction through administrative outsourcing.

- National Health Insurance Cost Control Incentives: Japan's DPC bundled payment system structurally incentivises hospitals to reduce operational costs, making administrative and clinical BPO adoption a financially rational choice.

- Pharmaceutical R&D Pipeline Growth: Domestic majors, including Takeda, Astellas, and Eisai, are expanding outsourced clinical trial management for Phase I–III studies, supported by AMED's innovation ecosystem.

- EMR and EHR Adoption Mandates: MHLW's electronic prescription system expansion and standardised IVD validation protocols are generating sustained demand for outsourced health IT implementation and data management.

Market Restraints

Complex and fragmented regulatory landscape: Japan's healthcare regulatory environment encompasses multiple overlapping authorities, MHLW, PMDA, the Digital Agency, and prefectural-level Clinical Establishments Act implementation, creating inconsistent compliance requirements across geographies.

Cultural resistance to data outsourcing and deep-seated insourcing preferences: Japan's healthcare institutions, particularly public hospitals and academic medical centers, have historically maintained strong preferences for internal management of sensitive patient and operational data. Entrenched institutional cultures, concerns about data confidentiality, and a traditional reliance on in-house administrative staff create meaningful adoption barriers that limit the pace at which outsourcing relationships can be established and expanded across the national hospital network.

Data security concerns and cybersecurity compliance burden: Japan's healthcare sector handles highly sensitive patient records under strict privacy obligations, and outsourcing creates perceived vulnerabilities in data custody chains. BPO vendors must invest heavily in cybersecurity infrastructure and demonstrate compliance with MHLW information security guidelines, and any well-publicized data breach, which is increasing in healthcare settings globally, risks undermining institutional confidence and slowing adoption across the market.

Japan Healthcare BPO Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Service |

Provider Service |

44.7% |

2025 |

|

Region |

Kanto Region |

42.3% |

2025 |

Service Insights

Access the comprehensive market breakdown Request Sample

Provider Service - 44.7% Market Share (2025) | Leading Service

Provider service dominates the Japan healthcare BPO market, anchored by the country's vast network of hospitals and clinics that face simultaneous pressures of workforce shortages, cost containment under the DPC system, and accelerating digital mandates. Revenue cycle management is the highest-volume sub-segment, encompassing medical billing, claims processing, coding, and denial management.

|

Segment Breakdown Provider Service (Patient Enrollment and Strategic Planning, Patient Care Service, and Revenue Cycle Management) (44.7%) · Payer Service (Human Resource Management, Claims Management, Customer Relationship Management, Operational and Administrative Management, Care Management, Provider Management, and Others) · Pharmaceutical Service (Manufacturing Services, Research and Development Services, and Non-clinical Services) |

Regional Insights

Kanto Region - 42.3% Market Share (2025) | Leading Region

Kanto dominates Japan's healthcare BPO market, with Tokyo forming the commercial core of the country's healthcare outsourcing ecosystem. Tokyo hosts the headquarters of Japan's leading BPO providers, NTT DATA, Fujitsu, and NEC, as well as the national offices of international firms including Accenture, IBM Japan, and Genpact, giving the region unmatched vendor depth and delivery capability. Japan's AI Hospital initiative, a public-private program involving Hitachi, IBM Japan, and SoftBank, designated the Kanto corridor as the primary deployment zone for AI-powered hospital management and automated documentation systems.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 42.3% |

| Major Prefectures | Tokyo, Kanagawa, Chiba, Saitama, Ibaraki, Tochigi, and Gunma |

| Key Growth Drivers | BPO vendor headquarters concentration, AI hospital initiative rollout, national pharmaceutical company presence, DPC-scheme hospital density |

| Outlook | Sustained regional leadership through 2034, anchored by healthcare DX investment |

|

Regional Breakdown Kanto Region (42.3%) · Kansai/Kinki Region · Central/Chubu Region · Kyushu-Okinawa Region · Tohoku Region · Chugoku Region · Hokkaido Region · Shikoku Region |

Kansai/Kinki Region:

Kansai is Japan's second-largest healthcare BPO market, anchored by Osaka, Kyoto, and Kobe's dense private hospital networks, major pharmaceutical manufacturing clusters, and leading research institutions. Osaka University is a national leader in genomics-based diagnostics and AI healthcare applications, generating strong demand for outsourced clinical data management and research support services. In October 2024, Osaka Prefecture and Osaka City announced the Osaka Finance Forum, an event that will feature pitch sessions by life sciences and healthcare startups.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Osaka, Kyoto, Kobe, Nara, and Shiga |

| Key Growth Drivers | Pharmaceutical manufacturing cluster, Osaka University research ecosystem, private hospital network density, Kansai health-tech start-up activity |

| Outlook | Strong second-place position with pharmaceutical BPO growth |

Central/Chubu Region:

Chubu's healthcare BPO market is driven by Nagoya's industrial and manufacturing ecosystem and the regional hospital network anchored by Nagoya University Hospital and Gifu University Hospital, both key participants in Fujitsu's May 2025 clinical data AI field trials. The region's manufacturing economy sustains a concentrated occupational health and pharmaceutical manufacturing outsourcing market supported by established CRO partnerships.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Nagoya, Hamamatsu, Shizuoka, Kanazawa, Niigata, and Nagano |

| Key Growth Drivers | Automotive sector corporate health outsourcing, Nagoya University clinical trial ecosystem, pharmaceutical manufacturing cluster, AI wellness platform adoption |

| Outlook | Steady growth driven by industrial health outsourcing |

Kyushu-Okinawa Region:

Kyushu-Okinawa is driving with digital health programs and remote care adoption expanding rapidly across its aging communities. The region's focus on improving healthcare accessibility and providing timely services is creating strong demand for outsourced patient care services, telehealth administration, and remote monitoring support.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Fukuoka, Kitakyushu, Nagasaki, Kagoshima, and Kumamoto |

| Key Growth Drivers | Rural clinic AI adoption, remote patient monitoring expansion, aging community care outsourcing, telehealth administration growth |

| Outlook | Fastest regional growth rate from digital health expansion |

Tohoku Region:

Tohoku represents one of Japan's most underpenetrated BPO markets, with lower healthcare IT infrastructure density and heavier reliance on government-funded public health services. The region's relatively older and more rural population creates a structurally high need for outsourced care management and patient enrollment services as hospitals seek to manage growing caseloads with constrained administrative staffing.

|

Metric

|

Details

|

|---|---|

| Major Prefectures | Miyagi, Aomori, Iwaki, Akita, Yamagata, and Fukushima |

| Key Growth Drivers | Rural healthcare infrastructure investment, public hospital digital upgrade programmes, aging population care management demand |

| Outlook | Moderate growth with accelerating catch-up from low penetration base |

Market Outlook (2026-2034)

What is the future outlook of the Japan healthcare BPO market?

The Japan healthcare BPO market is expected to sustain steady revenue growth through 2034.

Japan's healthcare BPO sector is poised for sustained expansion, underpinned by irreversible demographic pressures, accelerating government-mandated digital transformation, and a deepening pharmaceutical R&D outsourcing culture. As NTT DATA, Fujitsu, and international entrants invest in Japan-specific healthcare outsourcing platforms, the Japan healthcare BPO market forecast reflects both the structural necessity of outsourcing in a demographically stressed system and the expanding technological sophistication of service offerings through 2034.

Japan Healthcare BPO Market - Leading Key Players

The Japan healthcare BPO market features a competitive landscape anchored by domestic technology conglomerates, multinational BPO specialists, and emerging AI-native service providers. Key players leverage deep institutional relationships with Japan's hospital networks, insurance payers, and pharmaceutical companies, combining regulatory expertise with advanced automation and AI capabilities to deliver compliant, cost-effective outsourcing solutions across provider, payer, and pharmaceutical service segments.

| Company | Leading Services/Products | Highlights |

|---|---|---|

|

EP-PharmaLine Co. Ltd. |

DI Contact Center Services, Healthcare BPO Services, Medical Device Support |

Provides BPO and contact center services for pharmaceutical, medical device, and healthcare companies, including drug information services and patient support programs. |

|

BELLSYSTEM24 Inc. |

Medical BPO Services, Healthcare Contact Center Solutions | Offers outsourcing for medical institutions including appointment scheduling, patient support, medical reception, and healthcare call center services. |

|

Prestige International Inc. |

BPO Support Services, Customer & Healthcare Support Solutions | Japanese outsourcing provider delivering BPO and customer support solutions offering operational assistance services. |

Some of the other key market players in Japan healthcare BPO market are NTT DATA Group Corporation, Fujitsu Limited, IBM Japan, NEC Corporation, etc.

Latest Development & News

- In September 2025, ITOCHU Corporation announced the launch of a joint business with BELLSYSTEM24, Inc. aimed at helping pharmaceutical companies modernize their marketing strategies and improve operational efficiency through IT and digital technologies. BELLSYSTEM24 will deliver BPO services centered on its contact center capabilities, combining advanced technologies with skilled personnel to support these initiatives.

- In May 2025, Fujitsu Limited and the Tokai National Higher Education and Research System (THERS) announced the successful completion of field trials that used generative AI to process clinical data for identifying suitable participants for clinical trials. During the trials, generative AI analyzed approximately 1,800 breast surgery patient records from Nagoya University and Gifu University, converting unstructured clinical information into structured data with about 90% accuracy.

Japan Healthcare BPO Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Services Covered |

|

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan healthcare BPO market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan healthcare BPO market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan healthcare BPO industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Healthcare BPO Market Report

The Japan healthcare BPO market was valued at USD 2.09 Billion in 2025.

The Japan healthcare BPO market is anticipated to reach a value of USD 4.30 Billion by 2034.

Provider service dominates the market with a share of 44.7% in 2025, driven by the extensive outsourcing of revenue cycle management, patient care services, and patient enrollment across Japan's approximately 1,700 DPC-scheme hospitals and tens of thousands of clinics seeking cost efficiency.

Kanto region currently leads the market, accounting for a share of 42.3% in 2025, underpinned by the concentration of BPO vendor headquarters, national pharmaceutical companies, and DPC-scheme hospital density across Tokyo, Kanagawa, and surrounding prefectures.

Some of the major players in the market include EP-PharmaLine Co., Ltd., BELLSYSTEM24, Inc., Prestige International Inc., NTT DATA Group Corporation, Fujitsu Limited, IBM Japan, NEC Corporation, etc.

Key trends include the MHLW's FY2026 cloud migration mandate for hospitals and pharmacies, AI-powered automation of revenue cycle and care coordination workflows, expanding pharmaceutical R&D outsourcing for clinical trials, RPA integration in claims management, and rapid growth of telehealth administration outsourcing.

Growth is driven by Japan's acute healthcare workforce shortage, the structural demand created by approximately 30% of the population being aged 65 or older, the MHLW's National Medical Information Platform rollout, national health insurance cost-containment pressures under the DPC system, and accelerating pharmaceutical R&D outsourcing through AMED-supported drug discovery programmes.

Key challenges include Japan's complex multi-layered regulatory environment spanning MHLW, PMDA, and prefectural authorities, strong institutional cultural resistance to data outsourcing in public hospitals, escalating cybersecurity compliance requirements under MHLW information security guidelines, and the difficulty of standardizing service delivery across eight highly differentiated regional markets with distinct healthcare infrastructure profiles.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)