Japan Industrial Engines Market Size, Share, Trends and Forecast by Fuel Type, Power, End Use, and Region, 2026-2034

Japan Industrial Engines Market Summary:

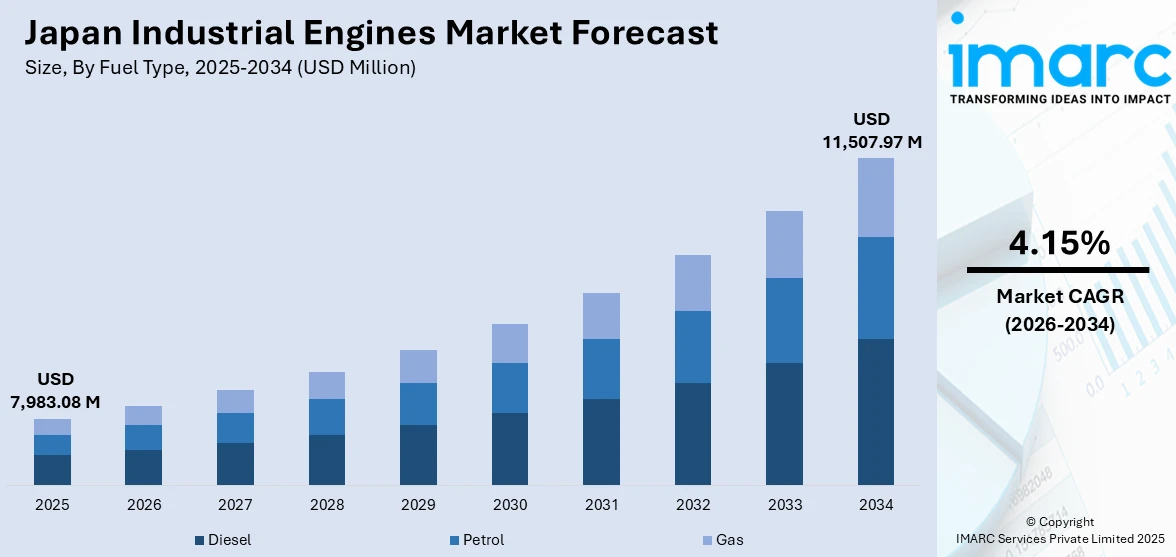

The Japan industrial engines market size was valued at USD 7,983.08 Million in 2025 and is projected to reach USD 11,507.97 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034.

The Japan industrial engines market is experiencing sustained momentum driven by accelerating infrastructure modernization, robust construction activity, and expanding demand for reliable power generation across industrial and commercial applications. Ongoing advancements in engine efficiency, the integration of digital monitoring technologies, and strategic collaborations among leading manufacturers are further strengthening market adoption. Supportive government investment in disaster resilience, transportation upgrades, and renewable energy infrastructure continues to create steady demand for high-performance industrial engines, reinforcing the Japan industrial engines market share.

Key Takeaways and Insights:

- By Fuel Type: Diesel dominates the market with a share of 62.7% in 2025, owing to its proven reliability, superior torque output, and extensive compatibility with heavy-duty construction, agricultural, and power generation equipment across Japan.

- By Power: 76–350 HP leads the market with a share of 39.5% in 2025, reflecting strong demand from mid-range construction machinery, agricultural equipment, and material handling applications that require a balance of power and operational efficiency.

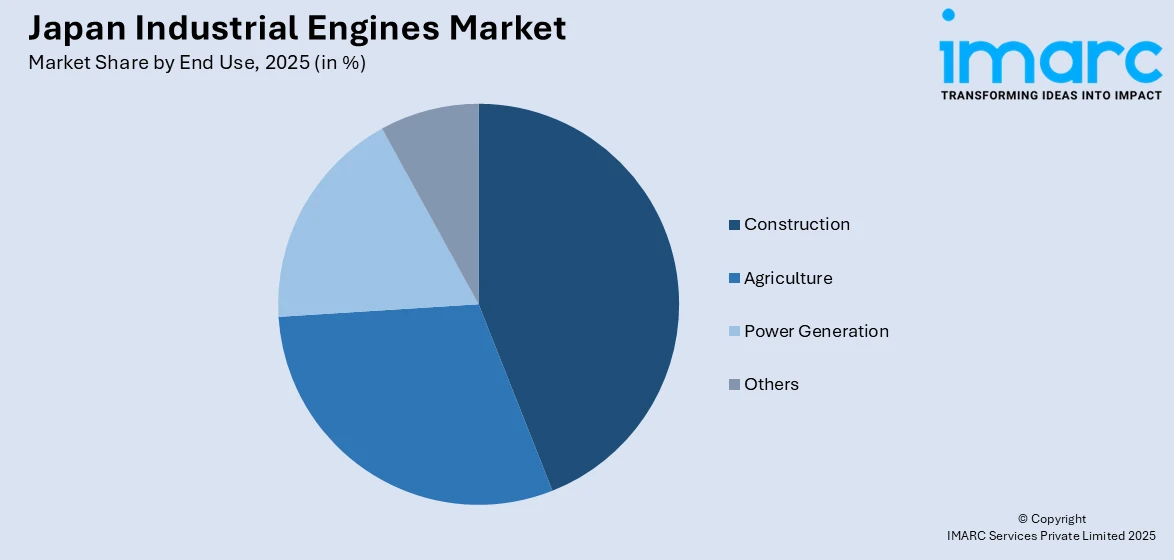

- By End Use: Construction dominates the market with a share of 44.3% in 2025, driven by sustained public infrastructure investment, large-scale urban redevelopment projects, and the ongoing national resilience program requiring heavy machinery powered by industrial engines.

- By Region: Kanto Region is the largest region with 36.9% share in 2025, fueled by the concentration of major construction projects, industrial manufacturing facilities, and logistics hubs across the greater Tokyo metropolitan area.

- Key Players: Leading manufacturers drive the Japan industrial engines market by investing in advanced powertrain technologies, expanding product portfolios across multiple fuel types, and forging strategic global partnerships to enhance engine performance and ensure reliable supply chains nationwide.

To get more information on this market Request Sample

The Japan industrial engines market is advancing steadily as manufacturers, government agencies, and end-use industries collectively pursue operational efficiency and environmental sustainability across diverse industrial applications. The construction sector remains the primary demand driver, supported by the Japanese government’s approval of a national resilience infrastructure plan worth over JPY 20 trillion (approximately USD 139 Billion) covering fiscal years 2026 through 2030, focused on earthquake-proofing, bridge reinforcement, and water infrastructure upgrades requiring heavy construction equipment powered by industrial engines. Meanwhile, the agricultural and power generation sectors continue to rely on dependable diesel and gas engines to maintain productivity in demanding and often remote operational environments. Strategic partnerships between domestic and international engine manufacturers are accelerating the introduction of next-generation powertrain solutions, including hydrogen-compatible and hybrid engines, positioning Japan as a global leader in sustainable industrial engine innovation and advanced technology development. The ongoing convergence of infrastructure investment, technological advancement, and regulatory compliance continues to expand the addressable market for industrial engines across all major segments and regional economies throughout the country, ensuring long-term demand stability and sustained revenue growth.

Japan Industrial Engines Market Trends:

Accelerating Development of Hydrogen and Alternative Fuel Engine Technologies

Japanese industrial engine manufacturers are intensifying research into hydrogen combustion and alternative fuel technologies as the nation pursues carbon neutrality by 2050. Hydrogen-powered engines are gaining traction as a viable pathway to decarbonize heavy-duty equipment that cannot easily transition to battery-electric systems. In October 2025, Kawasaki Heavy Industries, Yanmar Power Solutions, and Japan Engine Corporation completed the world’s first land-based operation of marine hydrogen engines at Japan Engine’s headquarters factors, demonstrating stable combustion in medium-speed four-stroke engines at rated output. This trend is reshaping the Japan industrial engines market growth.

Integration of Smart Monitoring and Digital Technologies in Engine Systems

Industrial engine manufacturers are increasingly embedding digital monitoring, telematics, and predictive maintenance capabilities into their engine platforms to enhance operational efficiency and minimize downtime. Connected engine systems enable real-time tracking of performance metrics, fuel consumption, and maintenance schedules, delivering significant value to fleet operators and industrial users. In 2024, Yanmar introduced its SmartAssist telematics system across multiple compact track loader models powered by its 4TN86CHT diesel engines, enabling remote monitoring of engine location, operating status, and diagnostic information for construction and landscaping applications.

Strategic Cross-Industry Powertrain Partnerships Reshaping Engine Supply

Major engine and vehicle manufacturers are forming strategic alliances to co-develop next-generation powertrain solutions that combine global engineering expertise with localized production capabilities. These partnerships are enabling faster deployment of advanced diesel engines while reducing development costs and expanding market reach across multiple vehicle and equipment categories. In May 2024, Cummins and Isuzu Motors launched the jointly developed 6.7-liter Isuzu DB6A diesel engine for medium-duty trucks, marking Cummins’ first entry into the Japanese on-highway market in its 105-year history, with assembly at Isuzu’s Tochigi Prefecture plant.

.webp)

Market Outlook 2026-2034:

The Japan industrial engines market is positioned for steady expansion over the forecast period, supported by sustained infrastructure investment, rising construction activity, and growing demand for efficient power generation solutions across industrial, commercial, and public sector applications. The government’s commitment to national resilience, renewable energy expansion, and industrial modernization ensures continued procurement of high-performance engines across multiple sectors. Simultaneously, evolving emission standards and the transition toward alternative fuels are compelling manufacturers to develop cleaner, more technologically advanced engine platforms that balance environmental compliance with operational performance. The market generated a revenue of USD 7,983.08 Million in 2025 and is projected to reach a revenue of USD 11,507.97 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034. The convergence of technological innovation, regulatory compliance, and sustained end-use demand across construction, agriculture, and power generation sectors positions the market for robust and sustained growth throughout the forecast period.

Japan Industrial Engines Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Fuel Type |

Diesel |

62.7% |

|

Power |

76–350 HP |

39.5% |

|

End Use |

Construction |

44.3% |

|

Region |

Kanto Region |

36.9% |

Fuel Type Insights:

- Diesel

- Petrol

- Gas

Diesel dominates with a market share of 62.7% of the total Japan industrial engines market in 2025.

Diesel engines remain the preferred choice across Japan's industrial landscape owing to their exceptional durability, high torque output, and fuel efficiency under sustained heavy-load conditions. The construction, agriculture, and power generation sectors depend extensively on diesel-powered equipment for excavation, material handling, and backup electricity supply, reinforcing the fuel type's leading market position. Ongoing advancements in common rail injection systems, exhaust aftertreatment technologies, and electronic engine management platforms are enhancing combustion efficiency while meeting progressively stricter emission standards. The extensive domestic fuel distribution infrastructure and well-established maintenance networks further support widespread diesel adoption across urban and regional operations.

The continued evolution of diesel engine technology toward lower emissions and improved fuel economy further supports sustained adoption across Japan’s industrial sectors. Manufacturers are incorporating advanced combustion systems, turbocharging, and exhaust aftertreatment technologies to meet stringent national emission standards while delivering enhanced performance. In April 2024, Toyota expanded its Land Cruiser lineup in Japan with the 250 series, offering a 2.8-liter direct injection turbo diesel engine paired with an eight-speed automatic transmission, reflecting ongoing investment in high-efficiency diesel powertrain development for both commercial and utility vehicle platforms.

Power Insights:

- 5–75 HP

- 76–350 HP

- 351–750 HP

- Above 751 HP

76–350 HP leads with a share of 39.5% of the total Japan industrial engines market in 2025.

The 76–350 HP segment serves as the backbone of Japan's industrial engine market, powering a diverse range of mid-size construction equipment, agricultural machinery, and material handling systems that demand a reliable balance between power output and operational versatility. This power range is ideally suited for excavators, wheel loaders, agricultural tractors, and generator sets that form the operational core of Japan's construction and farming sectors. Growing infrastructure renewal activity and rising mechanization in agriculture are sustaining consistent demand for engines within this category, reinforcing their dominant market position across multiple end-use applications.

Manufacturers are continuously refining engines in this power category to achieve greater fuel efficiency, reduced vibration, and improved emission compliance without compromising output. The integration of electronic fuel injection, turbocharging, and advanced cooling systems enables these engines to meet demanding operational requirements while adhering to Japan's stringent emission standards. Additionally, the rising adoption of telematics-enabled engine platforms with real-time performance monitoring and predictive maintenance capabilities is enhancing operational uptime and reducing total cost of ownership for fleet operators across the construction and agricultural sectors.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Agriculture

- Construction

- Power Generation

- Others

The construction exhibits a clear dominance with 44.3% share of the total Japan industrial engines market in 2025.

Japan's construction sector is the single largest consumer of industrial engines, driven by massive public investment in infrastructure modernization, urban redevelopment, and disaster resilience projects that require extensive deployment of engine-powered heavy machinery including excavators, cranes, bulldozers, and generators. The sector benefits from sustained government spending and rising construction orders across the country. Ongoing national programs targeting the rehabilitation of aging transportation networks, water distribution systems, and public facilities continue to generate strong demand for reliable, high-performance engines suited to demanding jobsite conditions throughout urban and regional areas.

The construction industry's reliance on industrial engines is further reinforced by Japan's comprehensive infrastructure strengthening initiatives aimed at improving seismic resilience, upgrading water pipelines, and modernizing transportation corridors across all prefectures. The government's long-term national resilience framework prioritizes extensive public works investment encompassing bridge retrofitting, tunnel reinforcement, and flood management infrastructure development. Additionally, the expansion of logistics and warehousing facilities driven by growing e-commerce activity is sustaining demand for material handling equipment powered by industrial engines, ensuring consistent market growth across both heavy construction and commercial infrastructure segments.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region represents the leading segment with 36.9% share of the total Japan industrial engines market in 2025.

The Kanto Region commands the largest share of Japan's industrial engines market, driven by the concentration of major construction projects, advanced manufacturing facilities, and logistics infrastructure across the greater Tokyo metropolitan area and surrounding prefectures. The region's dominance reflects sustained urban redevelopment activity, large-scale commercial construction, and robust industrial production that collectively generate significant demand for engine-powered equipment. The Kanto region's position as the country's primary economic hub ensures continuous and diversified consumption of industrial engines across construction, power generation, and material handling applications throughout the year.

Ongoing mega-projects and high-rise developments in the Kanto Region continue to sustain elevated demand for industrial engines across construction and logistics applications. Large-scale skyscraper developments, metropolitan rail network expansions, and commercial district modernization projects require extensive deployment of engine-powered cranes, excavators, and generators. Additionally, the region's role as Japan's primary economic and transportation hub ensures continuous demand for backup power generation systems and material handling equipment powered by industrial engines throughout commercial and industrial facilities, further reinforcing the Kanto Region's dominant position within the national market.

Market Dynamics:

Growth Drivers:

Why is the Japan Industrial Engines Market Growing?

Large-Scale Infrastructure Investment and National Resilience Programs

Japan's commitment to infrastructure modernization and disaster resilience is generating sustained demand for industrial engines across the construction and public works sectors. The government's multi-year investment programs encompass bridge reinforcement, water system upgrades, transportation network expansion, and seismic retrofitting of critical public infrastructure, all of which require extensive deployment of engine-powered heavy construction equipment. Recent devastating seismic events have exposed vulnerabilities in water and utility systems, prompting the government to approve comprehensive national resilience infrastructure plans allocating substantial funding for infrastructure strengthening across hundreds of projects over multi-year fiscal periods. This commitment ensures a sustained pipeline of construction projects demanding industrial engines for excavation, material transport, and on-site power generation. Furthermore, annual national budgets continue to support investment in transportation, energy, and disaster prevention infrastructure that collectively sustain robust demand for high-performance industrial engines across the country.

Expanding Construction Activity and Urban Redevelopment

Japan's construction industry is experiencing steady growth driven by rising construction orders, large-scale urban redevelopment projects, and investments in commercial, industrial, and renewable energy infrastructure that collectively increase demand for engine-powered construction machinery and on-site power generation systems. The expansion of data centers, semiconductor fabrication facilities, and commercial real estate across major metropolitan areas is further accelerating procurement of industrial engines. The construction market continues to demonstrate annual increases supported by robust private and public sector investment. Key mega-projects across Tokyo and Osaka are generating significant demand for cranes, excavators, generators, and other engine-dependent construction equipment. Government announcements of substantial aid packages for semiconductor and artificial intelligence infrastructure further expand the construction pipeline requiring industrial engine deployment across fabrication facility and data center projects nationwide.

Rising Demand for Reliable Backup Power and Disaster Preparedness

Japan's vulnerability to natural disasters including earthquakes, typhoons, and flooding has heightened the importance of reliable backup power generation across industrial, commercial, and public infrastructure facilities. Engine-powered generators serve as critical standby power sources for hospitals, data centers, telecommunications facilities, and essential public services that cannot tolerate power interruptions. The increasing frequency and intensity of natural disaster events in recent years has prompted both government agencies and private enterprises to invest in robust power generation contingency systems. Recent major seismic events causing prolonged water outages and power disruptions affecting large numbers of structures have underscored the critical need for dependable engine-powered backup generation systems. In response, government resilience plans specifically address strengthening electricity and water supply infrastructure, driving procurement of industrial engines for emergency power generation applications. This growing emphasis on disaster preparedness and business continuity planning across both public and private sectors creates sustained demand for reliable industrial engines in power generation applications throughout all Japanese regions.

Market Restraints:

What Challenges the Japan Industrial Engines Market is Facing?

High Costs of Advanced Emission-Compliant Engine Technologies

The increasing stringency of Japan's emission regulations requires manufacturers to incorporate advanced exhaust aftertreatment systems, electronic fuel injection, and sophisticated combustion technologies that significantly raise engine production and procurement costs. Compliance with stringent national emissions standards necessitates expensive components including diesel particulate filters and selective catalytic reduction systems. These elevated costs create financial barriers for smaller operators and end users, potentially slowing engine replacement cycles and limiting adoption of the latest compliant models across price-sensitive market segments.

Acute Skilled Labor Shortages in Key End-Use Industries

Japan's aging population and declining workforce participation are creating severe labor shortages in the construction, agriculture, and manufacturing sectors that directly impact the demand for and operation of industrial engines. The construction industry in particular has experienced declining construction starts, partly attributable to insufficient skilled labor availability. This workforce constraint can delay project timelines, reduce equipment utilization rates, and temper the pace of new engine procurement despite strong underlying demand from infrastructure investment programs.

Growing Competition from Electrification and Battery-Powered Equipment

The accelerating global transition toward electrification and battery-powered industrial equipment poses a growing competitive threat to conventional combustion-engine-powered machinery in Japan. Major construction equipment manufacturers are developing and deploying electric excavators, loaders, and other battery-powered alternatives that offer lower operating costs, reduced noise, and zero on-site emissions. As battery technology improves and charging infrastructure expands, electric equipment may gradually displace internal combustion engines in certain applications, particularly in urban construction environments where noise and emission restrictions are increasingly stringent.

Competitive Landscape:

The Japan industrial engines market features a highly competitive landscape characterized by the presence of established domestic manufacturers with deep engineering expertise and extensive distribution networks. Companies are actively investing in research and development to advance engine efficiency, reduce emissions, and develop alternative fuel technologies including hydrogen and hybrid powertrains. Competition is intensifying as manufacturers expand their product portfolios across multiple power ranges and fuel types to address diverse end-use requirements. Strategic partnerships between domestic and international engine producers are reshaping the competitive dynamics, enabling faster technology transfer and broader market coverage. The emphasis on after-sales service, parts availability, and digital monitoring capabilities is becoming an increasingly important differentiator as end users prioritize total cost of ownership and operational reliability.

Japan Industrial Engines Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Fuel Types Covered |

Diesel, Petrol, Gas |

|

Powers Covered |

5–75 HP, 76–350 HP, 351–750 HP, Above 751 HP |

|

End Uses Covered |

Agriculture, Construction, Power Generation, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Industrial Engines Market Report

The Japan industrial engines market size was valued at USD 7,983.08 Million in 2025.

The Japan industrial engines market is expected to grow at a compound annual growth rate of 4.15% from 2026-2034 to reach USD 11,507.97 Million by 2034.

Diesel dominated the market with a share of 62.7%, supported by its proven reliability, superior torque delivery, and widespread application across construction, agriculture, and power generation sectors in Japan.

Key factors driving the Japan industrial engines market include large-scale infrastructure investment under national resilience programs, expanding construction activity and urban redevelopment, rising demand for reliable backup power generation, and technological advancements in engine efficiency.

Major challenges include high costs of advanced emission-compliant engine technologies, acute skilled labor shortages in key end-use industries, growing competition from electrification and battery-powered equipment alternatives, and supply chain constraints affecting critical engine components.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)