Japan Industrial Robotics Market Size, Share, Trends and Forecast by Type, Function, End User, and Region 2026-2034

Japan Industrial Robotics Market Size, Share, Trends & Forecast (2026-2034)

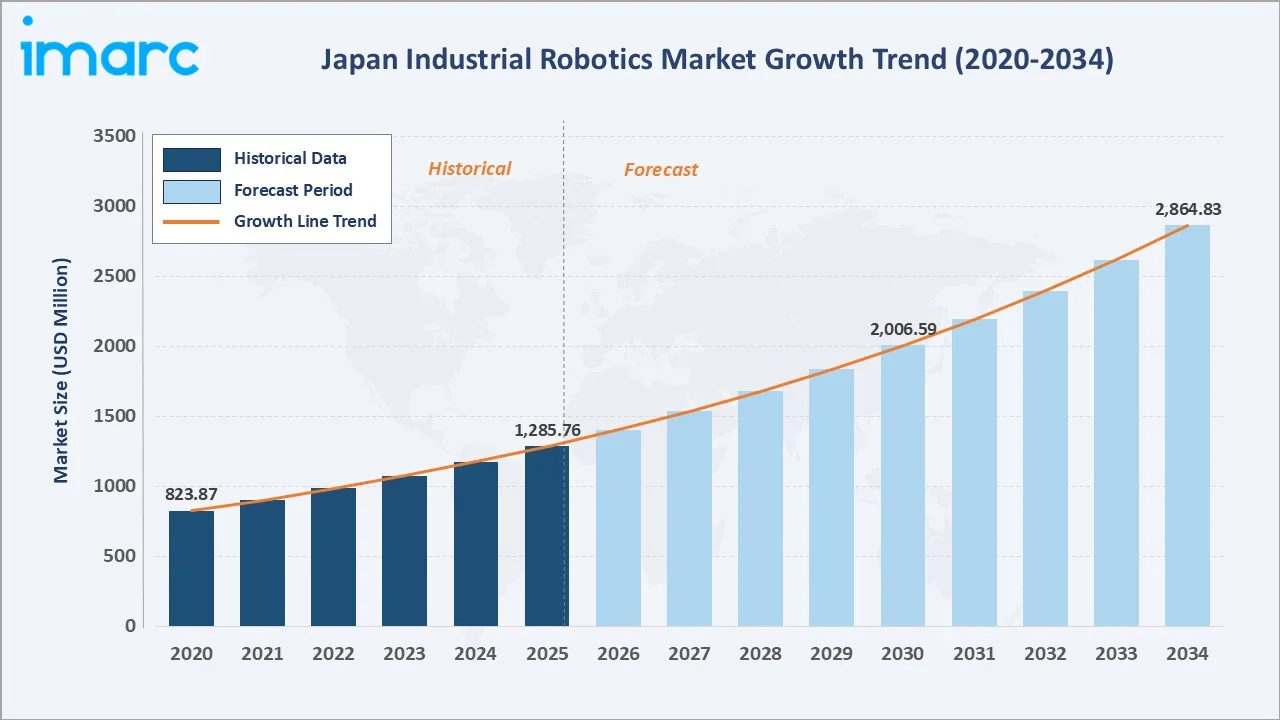

The Japan industrial robotics market size reached USD 1,285.76 Million in 2025 and is projected to reach USD 2,864.83 Million by 2034, exhibiting a CAGR of 9.31% during 2026-2034. Workforce shortages, automotive EV transition, government Society 5.0 initiatives, and electronics manufacturing expansion are primary forces driving Japan industrial robotics market growth.

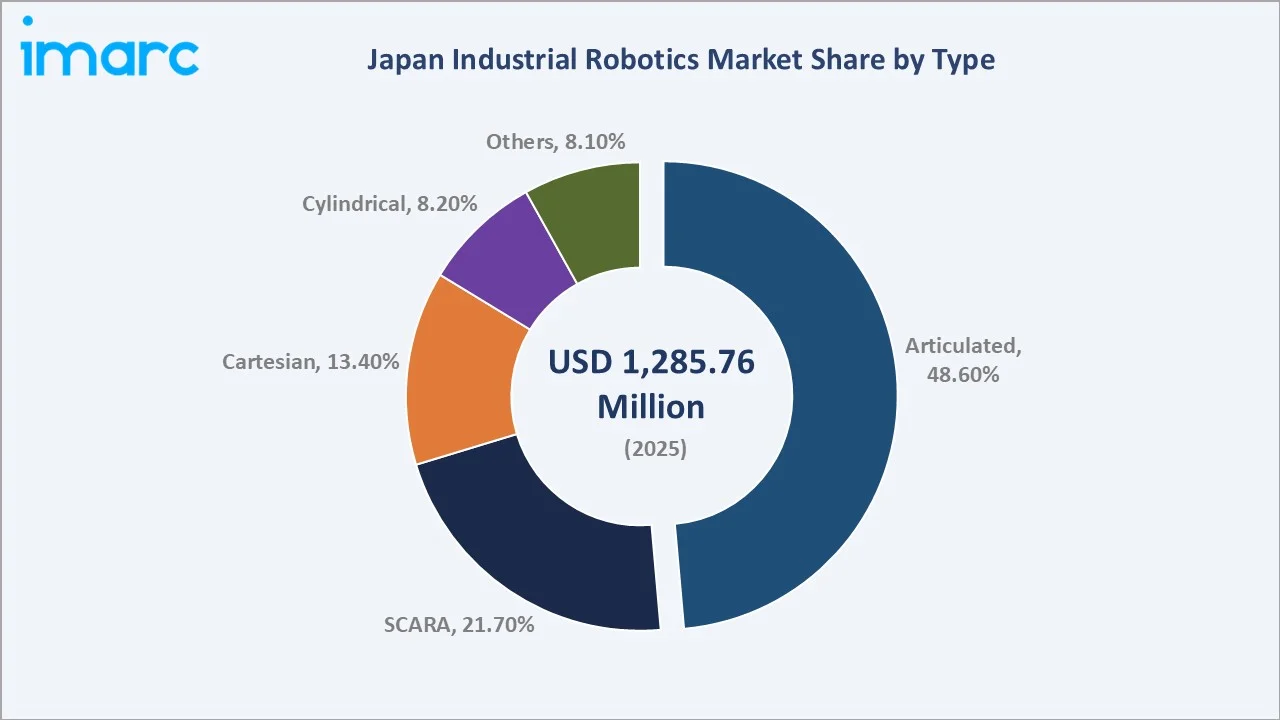

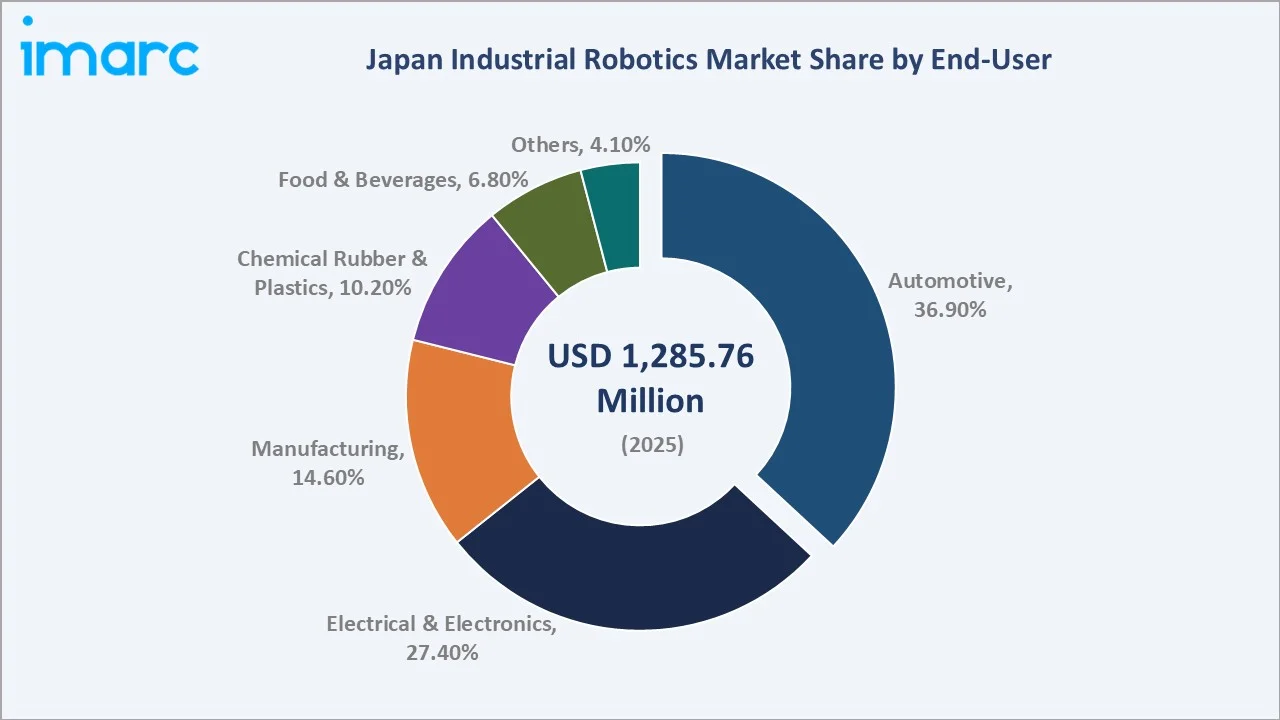

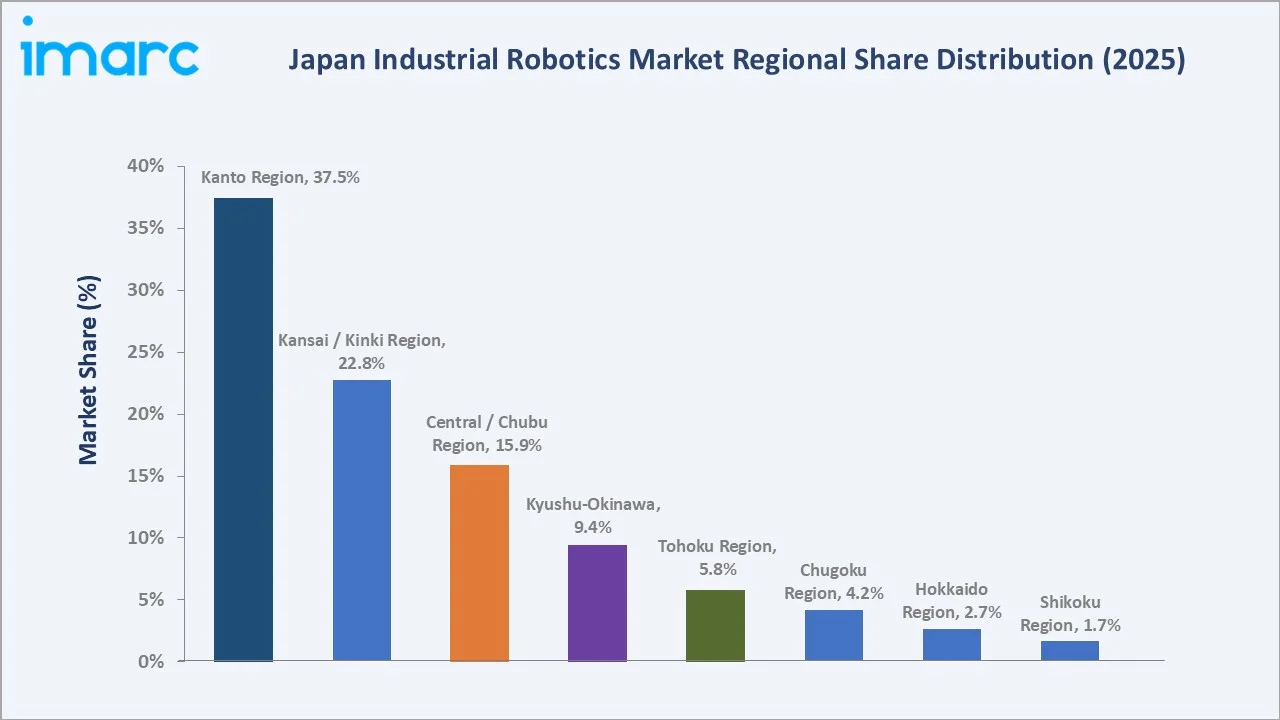

Articulated robots dominate at 48.6% in 2025, while automotive sector leads end-user share at 36.9%. Kanto Region commands a dominant 37.5% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1,285.76 Million |

|

Forecast Market Size (2034) |

USD 2,864.83 Million |

|

CAGR (2026-2034) |

9.31% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Kanto Region (37.5% share, 2025) |

|

Second Region |

Kansai/Kinki Region (22.8% share, 2025) |

|

Leading Robot Type |

Articulated (48.6%, 2025) |

|

Leading End-User |

Automotive (36.9%, 2025) |

To get more information on this market, Request Sample

The Japan industrial robotics market growth trajectory from 2020 through 2034 reflects accelerating demand from automotive modernization and electronics manufacturing. Historical expansion to USD 1,285.76 Million in 2025 and the forecast to USD 2,864.83 Million capture robotics investment driven by demographic-driven labor substitution and technology adoption.

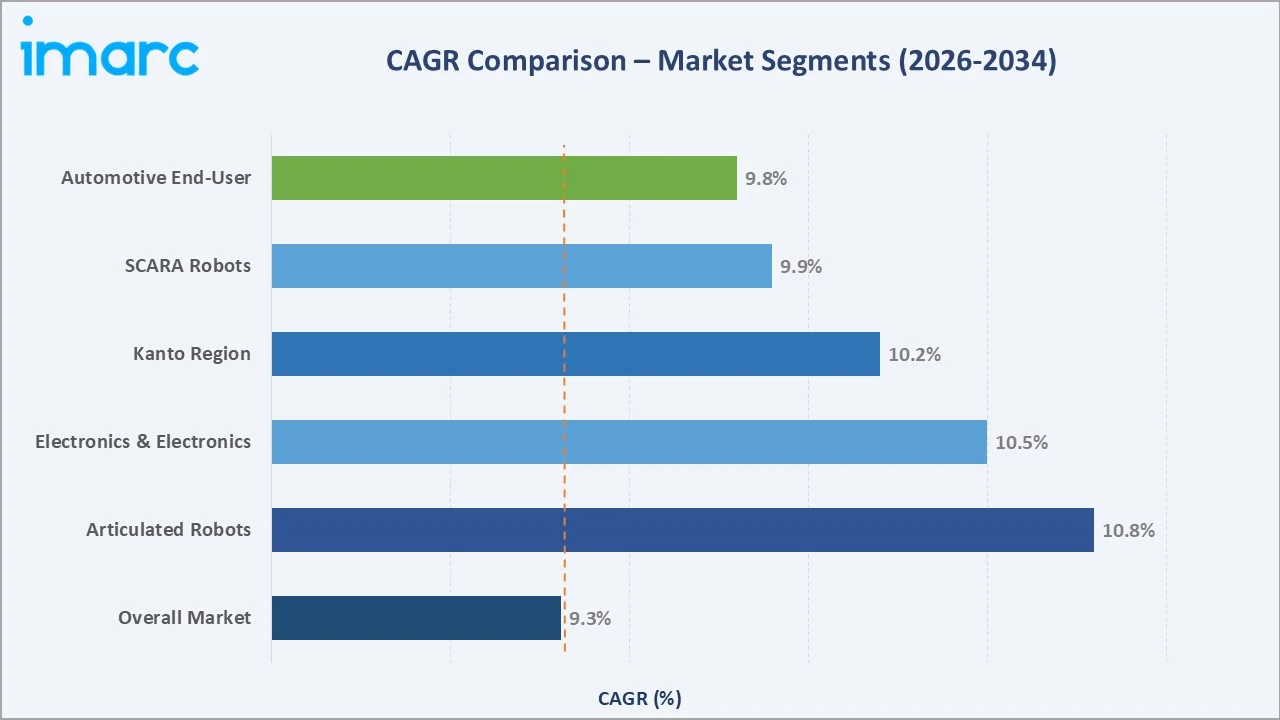

CAGR trajectories across key type and end-user sub-segments, with articulated robots at ~10.8% CAGR and electrical and electronics applications at ~10.5% CAGR, represent the fastest-growing categories within the Japan industrial robotics market analysis through 2034.

Executive Summary

The Japan industrial robotics market is on a sustained growth trajectory from USD 1,285.76 Million in 2025 to USD 2,864.83 Million by 2034. Industrial robots deliver precision automation across welding, assembly, painting, and materials handling, benefiting from non-discretionary demand driven by Japan's structural workforce shortage.

Articulated robots dominate robot type at 48.6% in 2025 owing to multi-axis flexibility across welding and assembly. Automotive sector commands 36.9% end-user share from high-density vehicle assembly line automation. Kanto Region leads regional contribution at 37.5%, reflecting Tokyo-Kanagawa industrial manufacturing concentration.

Japan's declining working-age population creates structural non-cyclical automation demand across manufacturing sectors. Government Society 5.0 and METI Connected Industries initiatives accelerate robotics adoption across SME manufacturers and large-scale automotive OEMs. High robot density validates continued upgrade and replacement investment cycles through 2034.

Key Market Insights

|

Metric |

Value |

|

Leading Robot Type |

Articulated – 48.6% share (2025) |

|

Dominant End-User |

Automotive – 36.9% revenue share (2025) |

|

Leading Region |

Kanto Region – 37.5% revenue share (2025) |

|

Second Region |

Kansai/Kinki Region – 22.8% revenue share (2025) |

|

Top Companies |

FANUC, Yaskawa Electric, Kawasaki Heavy Industries, Mitsubishi Electric, DENSO, Nachi-Fujikoshi, Panasonic |

Key Analytical Observations Expanding On The Above Data:

- Articulated robots, with 48.6% in 2025, dominate because their six-axis configuration enables the broadest application range across spot welding, arc welding, painting, and assembly. They cover the majority of automotive OEM and electronics manufacturing robotic automation requirements in a single platform architecture.

- Automotive sector, with 36.9% in 2025, leads because Japan's vehicle production ecosystem, Toyota, Honda, Nissan, Suzuki, and Mazda, maintains the world's highest robot density per worker in body-in-white welding, painting booths, and final assembly operations.

- Kanto Region's 37.5% dominance reflects concentration of automotive OEMs, Tier 1 suppliers, and electronics manufacturers within the Tokyo-Kanagawa industrial corridor, creating Japan's largest single-region robotics procurement market with the highest install base density.

- Electrical and Electronics sector, with 27.4% in 2025, reflects Japan's semiconductor and precision electronics manufacturing where SCARA and Cartesian robots perform high-speed pick-and-place, soldering, and micro-assembly operations with sub-millimeter precision tolerances.

Japan Industrial Robotics Market Overview

Industrial robotics comprises programmable multi-axis electromechanical systems designed to execute automated manufacturing tasks including welding, assembly, painting, material handling, and inspection. Robot configurations are defined by kinematic structure, articulated, SCARA, Cartesian, cylindrical, along with payload capacity, reach, speed, and precision specifications.

Japan's robotics ecosystem integrates servo motor and control system manufacturers, robot arm fabricators, end-of-arm tooling producers, systems integrators, software developers, and diverse end-use industries spanning automotive, electronics, food processing, pharmaceutical, and logistics sectors, underpinned by leading standards bodies JARA and ISO.

Market Dynamics

To evaluate market opportunities, Request Sample

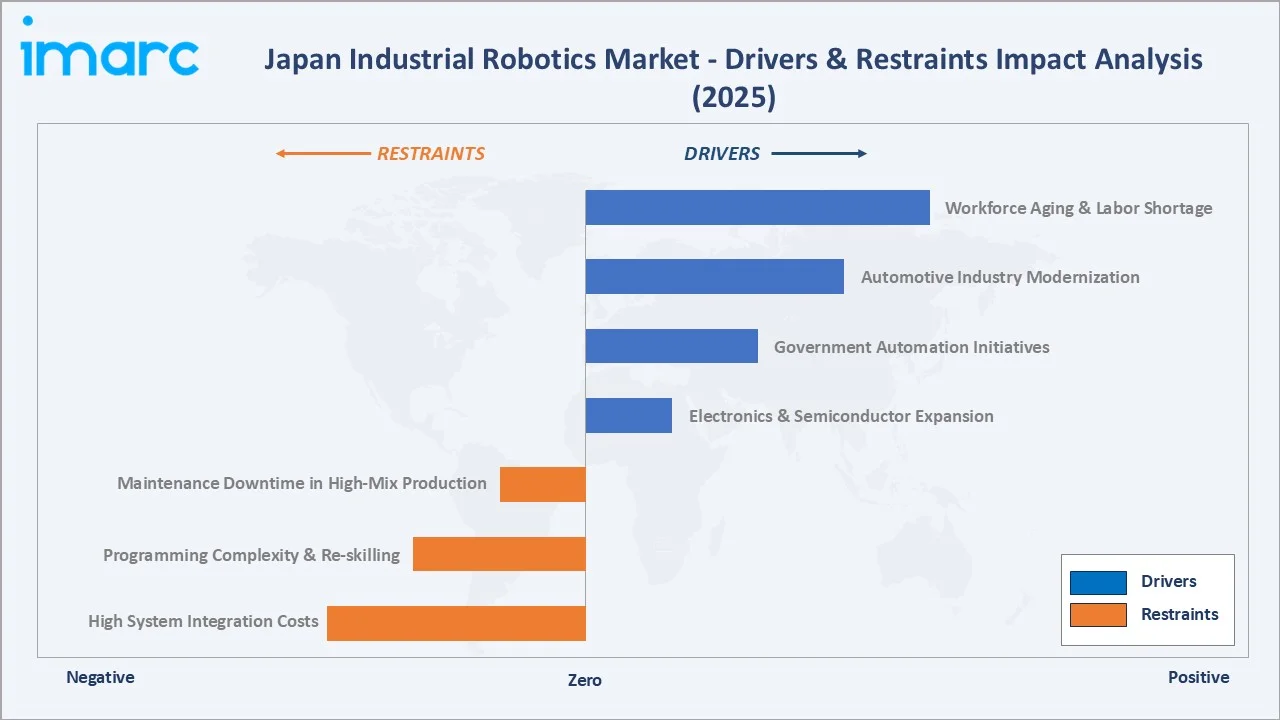

Market Drivers

- Workforce Aging and Labor Shortage: Japan faces the most acute demographic manufacturing challenge globally, with working age population projected to decline to 45 million by 2065. Robot deployment effectively substitutes skilled labor across welding, assembly, painting, and material handling, creating structural non-cyclical automation demand.

- Automotive Industry Modernization: Japan’s automotive industry is executing simultaneous EV transition and production line modernization. According to International Energy Agency, Japan and Korea accounted for the majority of the nearly 640 000 electric cars exported from the Asia Pacific region. New EV battery module assembly and electric motor winding processes require specialized robot configurations driving incremental procurement beyond standard replacement.

- Government Connected Industries Initiative: Japan has made industrial automation a national priority through coordinated government policies and funding programs. Significant public investment supports the adoption of advanced technologies such as robotics across both small and large manufacturing firms. Financial incentives, including subsidies, tax benefits, and development grants, help reduce implementation costs and encourage businesses to modernize their operations, improving productivity and competitiveness across the industrial sector.

Market Restraints

- High System Integration Costs: Implementing industrial automation systems often involves substantial upfront investment, including equipment setup, customization, safety compliance, and integration with existing processes. These high initial costs can slow adoption, particularly among smaller manufacturers with limited financial resources.

- Programming Complexity and Workforce Re-skilling: Legacy robot programming expertise requirements, combined with declining engineering graduate enrollment in Japan, create operational barriers. Re-skilling costs for existing technicians and limited availability of certified robot integrators constrain rapid deployment scale-up.

Market Opportunities

- Collaborative Robot Adoption in SMEs: Cobots with force-limiting safety systems enable smaller manufacturers to automate without expensive safety fencing, opening a USD 300+ Million addressable market within Japan's ~400,000 small and medium manufacturers currently below the robot adoption threshold.

- Semiconductor Fab Construction: Japan's semiconductor policy, including JPY 2.6 trillion in TSMC Kumamoto support and JPY 920 billion in Rapidus funding, drives precision robotics demand for cleanroom wafer handling, chip packaging, and automated inspection operations exceeding traditional automotive volumes by 2030.

Market Challenges

- Cybersecurity in Networked Robot Cells: Connected robot systems integrated with factory IoT and cloud platforms face cybersecurity vulnerabilities. Japanese manufacturers require additional security architecture investment exceeding standard robot cell budgets, slowing full IIoT integration timelines.

- ROI Demonstration for SME Adoption: Smaller manufacturers struggle to quantify return on investment for robotic cells when production volumes fluctuate seasonally. Variable order patterns common in Japan's high-mix low-volume manufacturing make standard payback period calculations unreliable.

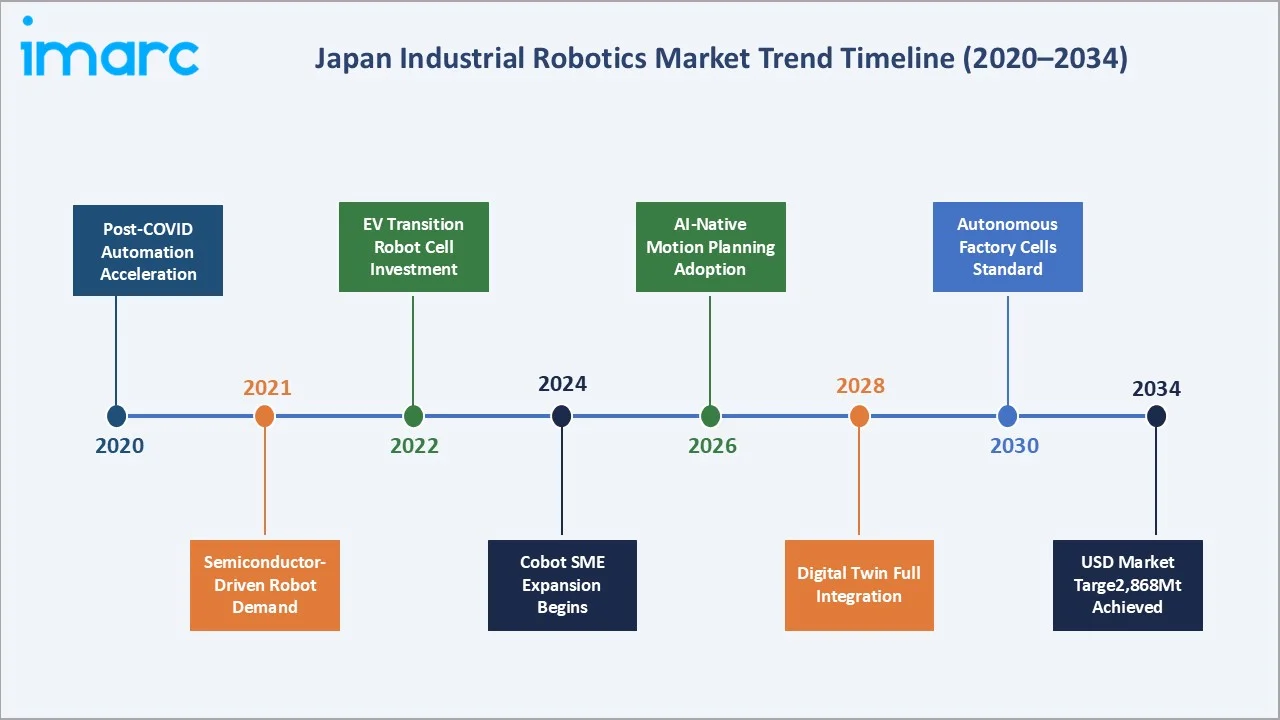

Emerging Market Trends

1. AI-Powered Adaptive Motion Planning Transforming Robot Versatility

AI-integrated motion planning enables robots to adapt trajectories dynamically to part variation and environmental changes. Adoption of vision-guided assembly and reinforcement learning motion systems reduces programming time by 60–70%, enabling faster deployment across high-mix manufacturing applications.

2. Collaborative Robots Enabling SME Factory Automation

Collaborative robot platforms with inherent force-torque safety systems eliminate expensive safety fencing requirements. Japan's SME manufacturers are adopting cobots for assembly, inspection, and palletizing.

3. Digital Twin Integration Accelerating Robot Deployment

Digital twin platforms compatible with FANUC's FIELD System, Yaskawa's i3-Mechatronics, and third-party simulation tools reduce physical commissioning time by 40–50%. Virtual robot cell validation eliminates production line disruption during integration, reducing total deployment costs significantly.

4. Green Manufacturing Driving Energy-Efficient Robot Design

Japan's carbon neutrality by 2050 targets are driving demand for energy-efficient servo motors and regenerative drive systems that recover braking energy. New-generation robots consume 20–30% less electricity than decade-old installed base, providing compelling energy cost reduction arguments for equipment refresh cycles.

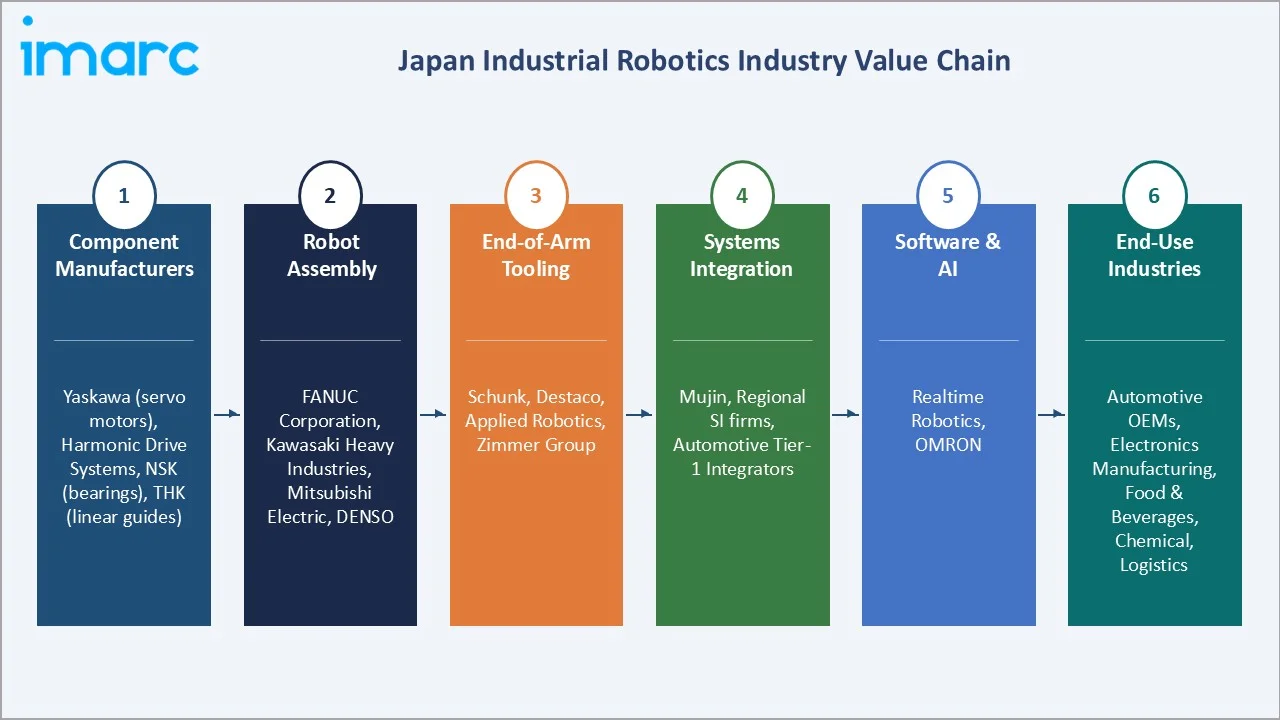

Industry Value Chain Analysis

The Japan industrial robotics value chain spans six stages from component manufacturing through end-use deployment. Robot assembly and systems integration capture the highest value-add margins, while software and AI platforms generate recurring revenue streams that favor IP-rich technology companies.

|

Stage |

Key Players / Examples |

Value-Add Focus |

|

Component Manufacturers |

Yaskawa (servo motors), Harmonic Drive Systems, NSK (bearings), THK (linear guides) |

Precision motion components |

|

Robot Assembly |

FANUC Corporation, Kawasaki Heavy Industries, Mitsubishi Electric, DENSO |

Kinematic systems & controllers |

|

End-of-Arm Tooling |

Schunk, Destaco, Applied Robotics, Zimmer Group |

Application-specific tooling |

|

Systems Integration |

Mujin, regional SI firms, automotive Tier 1 integrators |

Cell design & programming |

|

Software & AI |

Realtime Robotics, OMRON |

Motion AI & digital twin |

|

End-Use Industries |

Automotive OEMs, Electronics Mfg, F&B, Chemical, Logistics |

Production deployment |

Vertically integrated robot manufacturers with captive servo motor production, FANUC and Yaskawa, achieve lower component cost bases than assemblers relying on external servo procurement. This vertical integration is a durable competitive advantage in high-volume standardized robot segments where price competition is most intense.

Technology Landscape in the Japan Industrial Robotics Industry

Servo Control and Motion Technology: High-Speed Precision

Japan's servo motor technology, led by Yaskawa and FANUC, delivers sub-micron positioning repeatability through advanced encoder feedback systems achieving 26-bit resolution. High-speed communication protocols, EtherCAT, MECHATROLINK-III, enable microsecond-level synchronization across multi-axis robot cells.

Vision and Sensing: AI-Integrated Inspection Systems

AI-integrated 3D vision systems, combining structured light, time-of-flight, and deep learning inference, enable robots to identify, locate, and grasp unstructured parts without fixed fixtures. Keyence and Cognex vision platforms embedded in Japanese robot cells reduce fixture costs by 30–40% per assembly station.

Human-Robot Collaboration: Force-Sensing Cobot Platforms

Force-torque sensors integrated into cobot wrist designs enable compliant assembly operations previously requiring skilled human hand-feel. FANUC's CRX Series, Kawasaki's duAro, and Universal Robots' deployments in Japan's electronics manufacturing demonstrate sub-5-minute safety certification for new tasks.

Digital Twin and Simulation Platforms

Robot simulation platforms, FANUC ROBOGUIDE, Yaskawa MotoSim, and Siemens Process Simulate, enable full virtual commissioning of robot cells before physical installation. Japanese automotive OEMs mandate digital twin validation for all new robot cells, reducing physical commissioning time by 40–50%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Articulated |

48.6% |

2025 |

|

Function |

🔒 |

🔒 |

2025 |

|

End User |

Automotive |

36.9% |

2025 |

|

Region |

Kanto Region |

37.5% |

2025 |

By Type

Articulated robots command a 48.6% majority share in 2025 owing to their six-axis multi-directional reach capability. Versatility across welding, painting, and assembly operations makes articulated robots the default configuration across automotive OEM production lines and precision electronics manufacturing facilities.

To access detailed market analysis, Request Sample

SCARA robots at 21.7% in 2025 serve high-speed, high-precision assembly and pick-and-place applications in electronics and pharmaceutical manufacturing. Their fast horizontal motion and vertical compliance provide unique performance advantages in printed circuit board assembly and component insertion operations.

Cartesian robots at 13.4% deliver cost-effective gantry-style loading, dispensing, and CNC machine tending with straightforward programming. Cylindrical robots at 8.2% provide efficient spot welding in constrained workspaces. Others category at 8.1% includes delta robots and collaborative robots gaining adoption in food and light assembly.

By End-User

Automotive sector commands 36.9% end-user share in 2025, driven by Japan's world-class vehicle production. Robot deployment spans body-in-white welding, coating systems, powertrain assembly, and EV battery module handling. Japan's automotive OEMs maintain among the world's highest robot-to-worker ratios in manufacturing operations.

Electrical and Electronics at 27.4% in 2025 leverages SCARA and Cartesian robots for printed circuit board assembly, component placement, and semiconductor wafer handling. Manufacturing sector at 14.6% reflects broad-based robot adoption across metalworking, plastics, and general factory automation applications.

Chemical Rubber and Plastics at 10.2% utilizes robots for injection molding machine tending, chemical mixing, and hazardous material handling. Food and Beverages at 6.8% applies hygienic-grade robots for packaging and palletizing. Others at 4.1% covers logistics, pharmaceutical, and emerging construction applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Kanto Region |

37.5% |

Tokyo-Kanagawa auto & electronics density; largest robot install base |

|

Kansai/Kinki Region |

22.8% |

Osaka-Kobe industrial zone; electronics; food processing automation |

|

Central/Chubu Region |

15.9% |

Nagoya automotive cluster; Toyota supply chain robot investment |

|

Kyushu-Okinawa Region |

9.4% |

Automotive clusters; semiconductor expansion; TSMC Kumamoto impact |

|

Tohoku Region |

5.8% |

Auto parts manufacturing; post-disaster reconstruction investment |

|

Chugoku Region |

4.2% |

Hiroshima automotive (Mazda); chemical industry robotics |

|

Hokkaido Region |

2.7% |

Food processing; agricultural automation growth |

|

Shikoku Region |

1.7% |

Chemical and pharmaceutical automation; emerging expansion |

Kanto Region's 37.5% dominance in 2025 reflects Japan's most concentrated industrial manufacturing geography. The region hosts Toyota's engineering headquarters, Nissan's Kanagawa plants, Honda R&D, Canon, Sony, and Hitachi manufacturing, creating the highest single-region robot procurement density in Japan.

Kansai/Kinki Region, with 22.8% in 2025, benefits from Osaka-Kobe industrial zone integrating Panasonic, Sharp, and Daikin manufacturing with major food processing, chemical, and pharmaceutical industries. Central/Chubu Region at 15.9% reflects Nagoya's world-class automotive cluster anchored by Toyota Group supply chain robotics investment.

Competitive Landscape

Japan industrial robotics market is highly concentrated among domestic manufacturers, with FANUC, Yaskawa Electric, Kawasaki Heavy Industries, and Mitsubishi Electric holding dominant positions. Domestic companies maintain structural advantages through proprietary servo technology, deep customer relationships, and Japan-specific integration expertise.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

FANUC Corporation |

CRX series, CR series, SCARA Robot, Delta Robot |

Leader |

Japan & global leader; broadest automation range; zero-downtime manufacturing |

|

Yaskawa Electric Corporation |

Arc Welding, Spot Welding, Biomedical, Palletizing robots |

Leader |

Global top-3; motion control integration; i3-Mechatronics platform |

|

Kawasaki Heavy Industries, Ltd. |

Palletizing, Picking, Medical, Arc Welding, Ceiling Robots |

Leader |

Japan & global; automotive & cleanroom; dual-arm robotics |

|

Mitsubishi Electric Corporation |

Vertical articulated robot, Horizontal articulated robot |

Leader |

Japan leader; electronics and automotive; factory automation integration |

|

DENSO Robotics |

LPH Series, HS-A1 Series, HSR Series, VLA Series, VM Series |

Leader |

Compact robot specialist; Toyota Group integration; electronics focus |

|

Nachi-Fujikoshi Corporation |

MZ07F/MZ07LF, MZ10LF |

Challenger |

Japan; machining and welding integration; hydraulic expertise |

|

Seiko Epson Corporation |

Horizontal articulated (SCARA) robot, Vertical articulated (6-axis) robot |

Challenger |

Japan; SCARA specialist; electronics and pharmaceutical precision |

|

DAIHEN Corporation |

FD Series |

Challenger |

Japan; arc welding robotics; integrated power supply solutions |

|

Panasonic Connect |

Arc Welding Robots |

Challenger |

Japan; welding and assembly robots; factory automation systems |

|

Comau SpA |

S-13, S-18, MyCo-3.5-0.95 |

Emerging |

European player; global automotive body shop automation; limited Japan market exposure |

The key players include FANUC Corporation, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, DENSO Robotics, Nachi-Fujikoshi Corporation, Seiko Epson Corporation, DAIHEN Corporation, Panasonic Connect, Comau SpA, and others.

The competitive positioning of key Japan industrial robotics market participants reflects FANUC and Yaskawa's leadership in both global market presence and strategic investment dimensions, while domestic challengers maintain strong Japan-specific positions across specialized welding, SCARA, and cobot application niches.

Key Company Profiles

FANUC Corporation

FANUC Corporation is Japan's largest and the world's leading industrial robotics manufacturer, headquartered in Yamanashi Prefecture. FANUC's yellow robots, CNC systems, and ROBODRILL machining centers integrate across automotive, electronics, and precision engineering sectors globally, with an installed base exceeding 750,000 robots.

- Product Portfolio: CRX series, CR series, SCARA Robot, Delta Robot

- Recent Developments: In March 2022, FANUC expanded its CRX collaborative robot portfolio by introducing new models that broaden its range of payload capacities and applications. This expansion enhances flexibility for manufacturers by offering a wider selection of easy-to-use cobots designed for safe human-robot collaboration, improved productivity, and simplified deployment across diverse industrial tasks.

- Strategic Focus: FANUC's strategy centers on zero-downtime manufacturing, leveraging its proprietary servo motor technology and IoT FIELD System platform to deliver predictive maintenance and digital factory integration across automotive and electronics customers globally.

Yaskawa Electric Corporation

Yaskawa Electric Corporation is Japan's largest servo motor manufacturer and a global top-3 industrial robot producer. Motoman robots serve automotive, food, pharmaceutical, and electronics sectors. Yaskawa's integrated AC drives, servo systems, and robot controllers provide competitive advantages in motion control precision and application versatility.

- Product Portfolio: Arc Welding, Spot Welding, Biomedical, Palletizing robots

- Recent Developments: In April 2020, Yaskawa introduced a new robotic solution designed to enhance automation capabilities by integrating advanced control technologies and digital data utilization. The system supports more flexible and intelligent manufacturing processes, enabling improved performance, adaptability, and value creation across a wide range of industrial applications.

- Strategic Focus: Yaskawa integrates robotics with its inverter and servo drive portfolio, offering full-motion control solutions and leveraging its i3-Mechatronics digital factory platform for connected manufacturing customers across Japan and globally.

Kawasaki Heavy Industries Ltd.

Kawasaki Heavy Industries' Robotics Division is a pioneer in Japan's industrial robotics, delivering arc welding, spot welding, painting, and assembly robots for automotive and general manufacturing. Kawasaki's dual-arm collaborative robot and agricultural automation systems extend into new application domains beyond traditional industrial use.

- Product Portfolio: Palletizing, Picking, Medical, Arc Welding, Ceiling Robots

- Recent Developments: In December 2024, Kawasaki announced a new initiative focused on advancing robotics and automation capabilities through the development of innovative technologies and solutions. The effort aims to strengthen its position in the robotics sector by enhancing product offerings, supporting more efficient manufacturing processes, and addressing evolving industry needs across a wide range of applications.

- Strategic Focus: Kawasaki's strategy focuses on integrating robotics with its broader aerospace and industrial systems portfolio, targeting high-precision and specialty applications including surgical robots and agricultural automation, while maintaining strength in automotive welding and assembly.

DENSO Robotics

DENSO Corporation’s robotics division is a global leader in small and medium payload industrial robots, particularly compact 4-axis and 6-axis platforms specialized for electronics assembly and pharmaceutical applications. DENSO robots are embedded in Toyota Group manufacturing systems globally across assembly, inspection, and material handling.

- Product Portfolio: LPH Series, HS-A1 Series, HSR Series, VLA Series, VM Series

- Recent Developments: In May 2024, DENSO Robotics introduced an advanced fully automated robotic system designed for agricultural harvesting, leveraging AI and sensing technologies to autonomously identify and process crops with minimal human intervention.

- Strategic Focus: DENSO's robotic strategy leverages its Toyota Group supply chain position to maintain captive automotive demand while expanding into electronics, pharmaceutical, and food processing applications where compact robot precision and hygienic design command premium pricing.

Market Concentration Analysis

Japan industrial robotics market is highly concentrated with domestic manufacturers controlling approximately 60–70% of the domestic installed base. FANUC and Yaskawa Electric together hold the largest combined revenue share, with deep integration into automotive and electronics manufacturing providing durable competitive protection against international entrants.

International competitors including ABB, KUKA, and Comau hold limited domestic Japan market shares, succeeding primarily in specialized applications or automotive transplant facilities where global supply agreements apply. Japan's unique programming standards and deep integrator networks create structural barriers that consistently favor domestic suppliers.

Investment & Growth Opportunities

Fastest-Growing Segments

Collaborative robots growing at ~12% CAGR represent the highest-growth sub-segment, driven by Japan's SME factory adoption. Electrical and Electronics end-user at ~10.5% CAGR reflects semiconductor and display panel automation expansion. Kyushu-Okinawa Region at ~11% CAGR is the fastest-growing regional market driven by TSMC-related investment.

Emerging Markets

Kyushu-Okinawa Region is the fastest-growing Japan robotics market driven by TSMC's Kumamoto semiconductor facility and associated supply chain automation. Semiconductor and electronics applications in Kyushu represent a concentrated investment target for robotics system integrators and precision equipment manufacturers through 2034.

Venture & Investment Trends

Japan government SBIR programs and METI Connected Industries grants fund robotics AI startups. Toyota, Panasonic, and SoftBank corporate venture arms invest in collaborative robot software. ABB and Universal Robots target Japan's SME automation market through local integrator partnerships, entering segments underserved by domestic large-robot specialists.

Future Market Outlook (2026-2034)

Japan industrial robotics market is forecast to expand from USD 1,285.76 Million in 2025 to USD 2,864.83 Million by 2034 at a CAGR of 9.31%, adding USD 1,579 Million in incremental annual market value. Deepening automotive EV transition, semiconductor expansion, and Society 5.0 policy create sustained non-cyclical demand characteristics.

Three forces will shape the Japan industrial robotics landscape through 2034: AI-native motion planning enabling faster deployment, collaborative robot cost reductions opening sub-100-person factory automation, and semiconductor fab construction creating precision robotics demand exceeding traditional automotive volumes in Kyushu and Tohoku regions.

Research Methodology

Primary Research

Primary research encompassed over 40 structured interviews in 2024–2025 with Japan robotics industry stakeholders including senior engineers at automotive OEMs, robotics procurement managers at electronics manufacturers, Japan Robot Association technical committee members, and systems integrators across Kanto, Kansai, and Chubu regions.

Secondary Research

Key secondary sources include Japan Robot Association (JARA) annual statistics, Ministry of Economy Trade and Industry (METI) factory automation white papers, IFR World Robotics Report, Nikkei Business industrial automation analysis, ISO 10218 and JIS B 8433 standards documentation, and peer-reviewed automation engineering journals.

Forecasting Models

Market size estimations and projections were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, robot density indices, labor cost escalation data, and historical Japan market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) accounts for macroeconomic and policy uncertainty.

Japan Industrial Robotics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Articulated, Cartesian, SCARA, Cylindrical, Others |

| Functions Covered | Soldering and Welding, Materials Handling, Assembling and Disassembling, Painting and Dispensing, Milling, Cutting, and Processing, Others |

| End Users Covered | Automotive, Electrical and Electronics, Chemical Rubber and Plastics, Manufacturing, Food and Beverages, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | FANUC Corporation, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, DENSO Robotics, Nachi-Fujikoshi Corporation, Seiko Epson Corporation, DAIHEN Corporation, Panasonic Connect, Comau SpA, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan industrial robotics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan industrial robotics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan industrial robotics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Industrial Robotics Market Report

The Japan industrial robotics market reached USD 1,285.76 Million in 2025, supported by automotive modernization, electronics manufacturing expansion, and structural workforce shortage driving non-discretionary automation investment across all major industry verticals.

The market is projected to reach USD 2,864.83 Million by 2034, growing at a CAGR of 9.31% during 2026-2034, driven by EV transition investment, semiconductor fab construction, and Society 5.0 automation policy implementation.

Articulated robots lead with 48.6% type share in 2025, valued for multi-axis versatility across welding, painting, and assembly. They serve as the default platform for automotive OEM and electronics production lines requiring flexible multi-step automation.

Automotive sector commands 36.9% in 2025, driven by Japan's vehicle assembly operations maintaining among the world's highest robot-to-worker ratios, with EV transition driving new cell configurations beyond traditional ICE assembly requirements.

Kanto Region commands 37.5% market share in 2025, driven by Tokyo-Kanagawa manufacturing concentration hosting Toyota, Nissan, Honda, Canon, Sony, and Hitachi's primary manufacturing operations with Japan's highest robot install base density.

Collaborative robots within the others segment represent the fastest-growing category at ~12% CAGR through 2034, enabling SME factory automation without expensive safety fencing and unlocking automation in manufacturers previously below the investment threshold.

Leading companies include FANUC Corporation, Yaskawa Electric Corporation, Kawasaki Heavy Industries, Ltd., Mitsubishi Electric Corporation, DENSO Robotics, Nachi-Fujikoshi Corporation, Seiko Epson Corporation, DAIHEN Corporation, Panasonic Connect, Comau SpA, and others.

Key applications include arc welding and spot welding, materials handling and palletizing, assembly and disassembly, painting and dispensing, and precision electronics component placement across automotive and electronics manufacturing sectors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)