Japan Internet of Things Market Size, Share, Trends and Forecast by Component, Application, Vertical, and Region, 2026-2034

Japan Internet of Things Market Size, Share, Trends & Forecast (2026-2034)

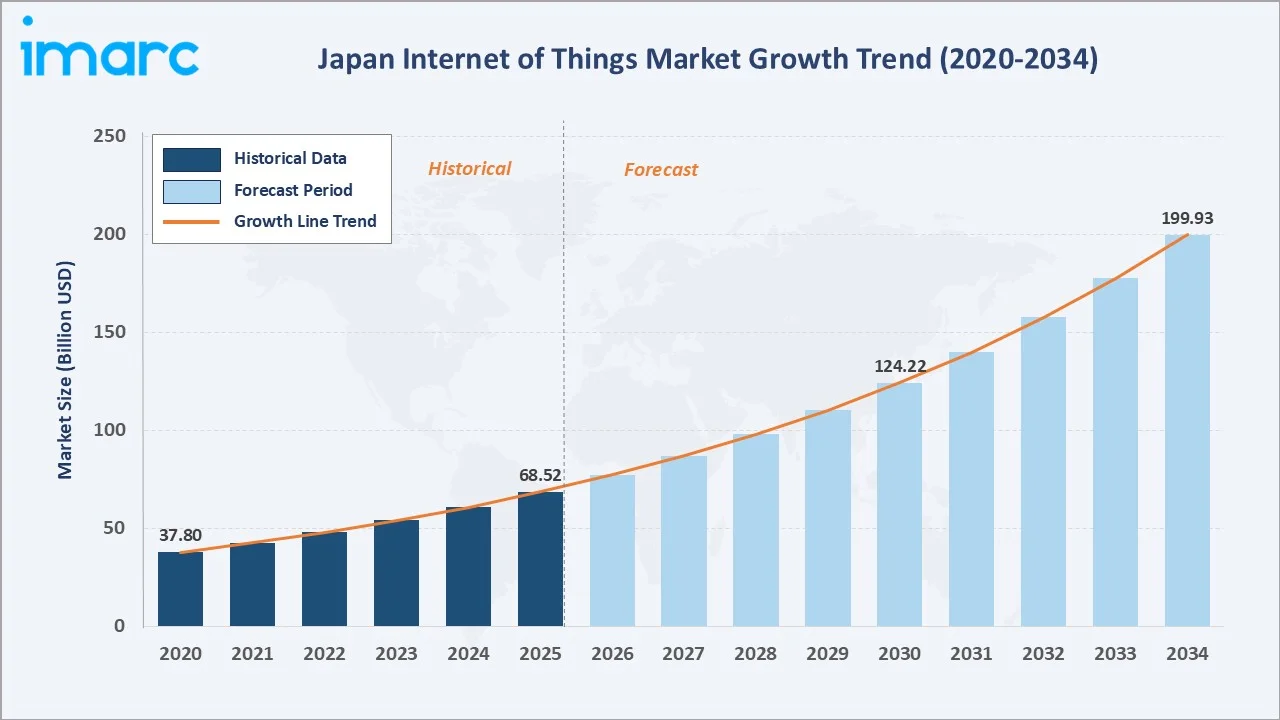

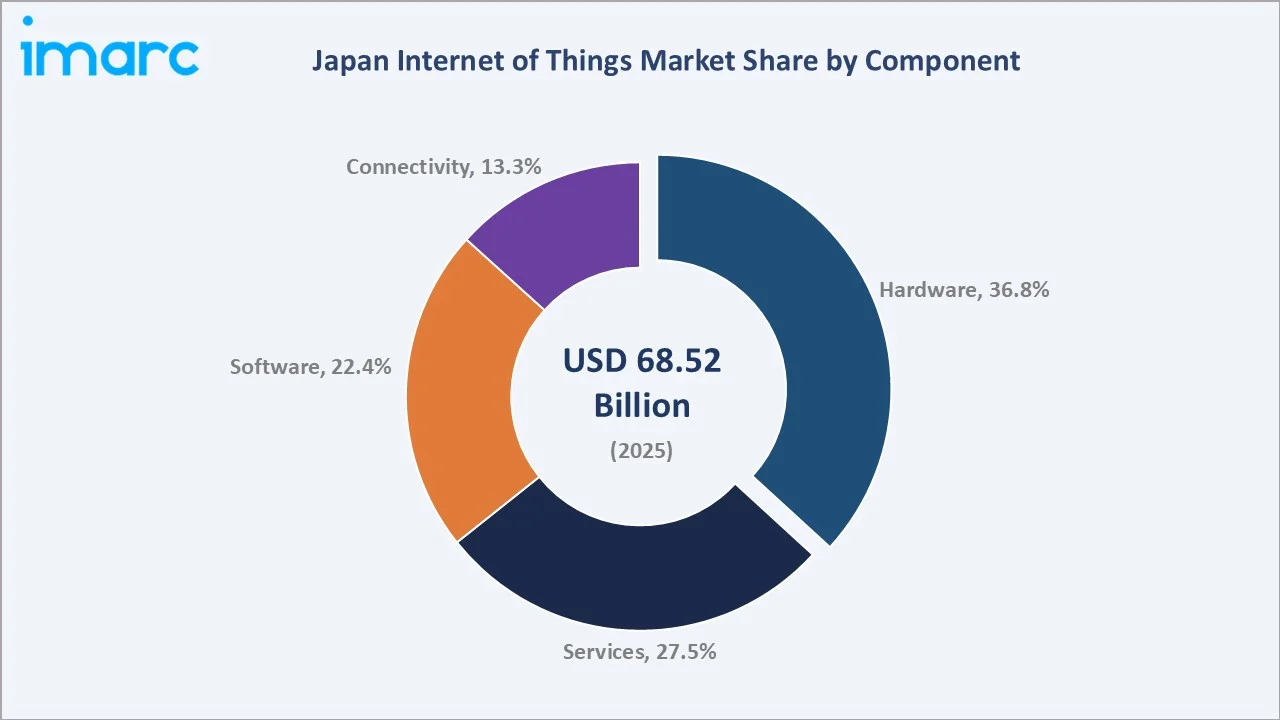

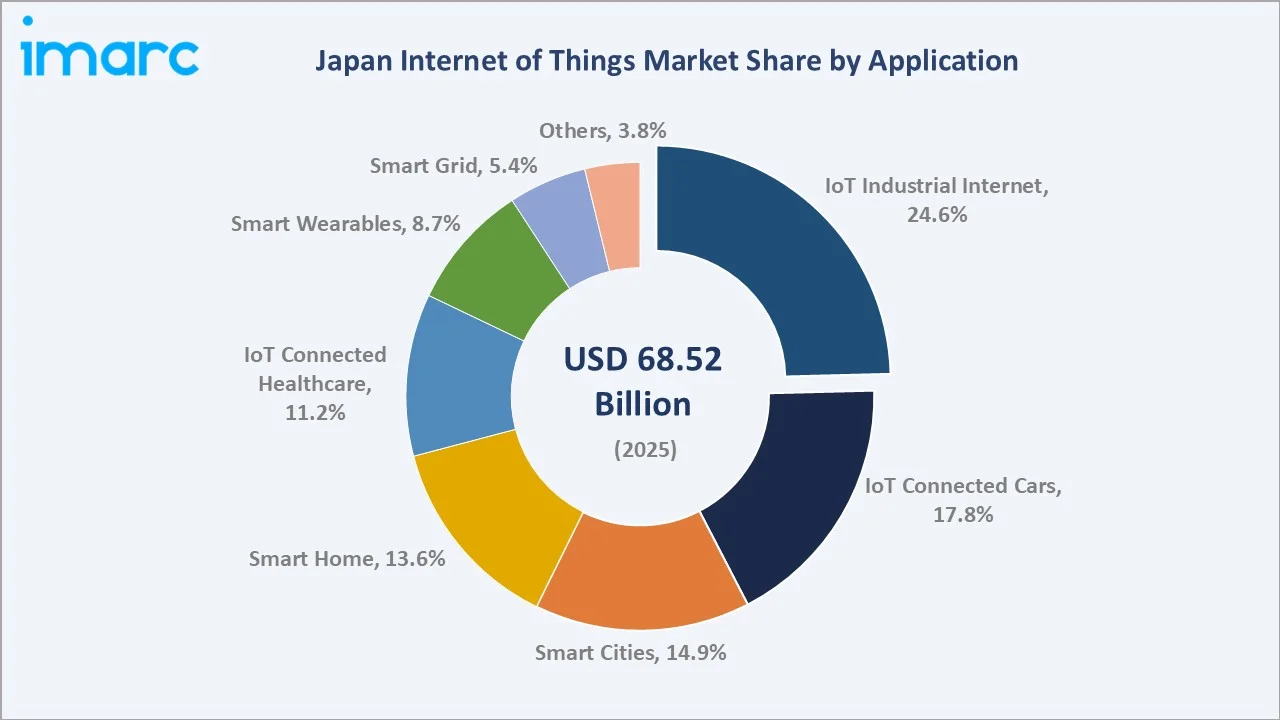

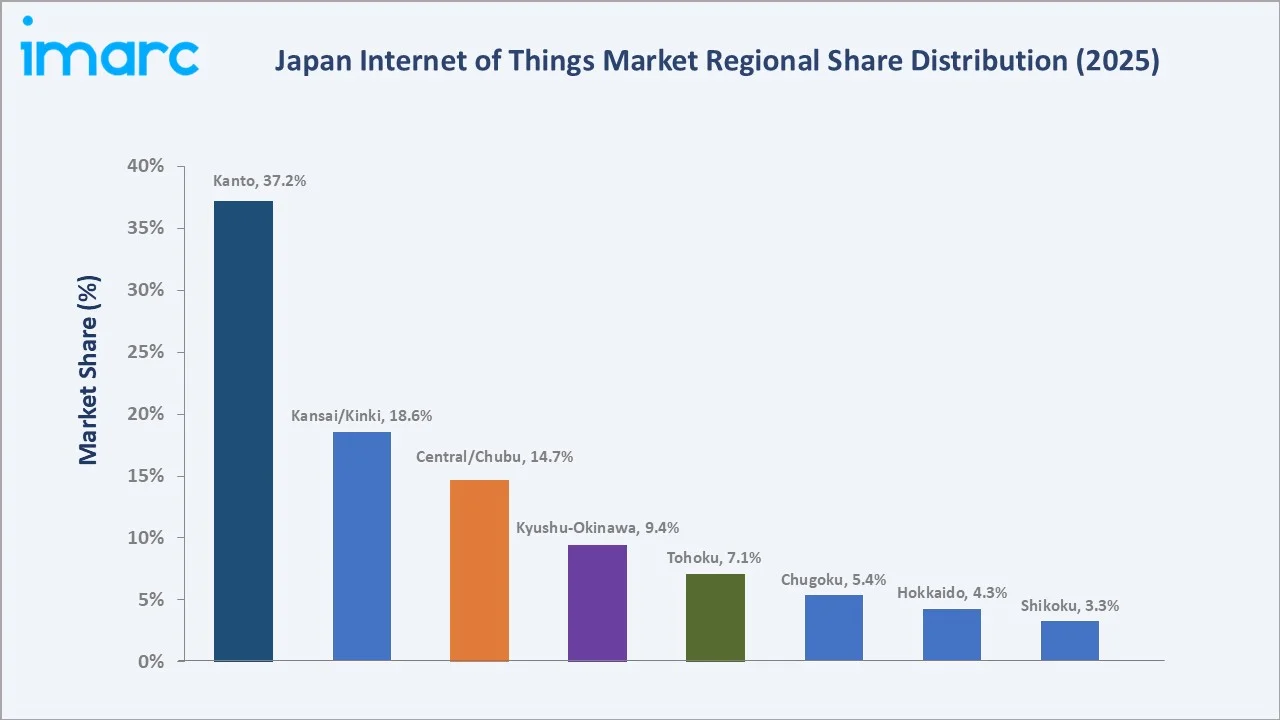

The Japan Internet of Things (IoT) market reached USD 68.52 Billion in 2025 and is projected to reach USD 199.93 Billion by 2034, growing at a CAGR of 12.64% during 2026-2034. The market is driven by the rapid adoption of smart manufacturing, connected devices, automation, and Industry 4.0 technologies across industries. In early 2025, Japan had 194 million active cellular mobile connections, equal to 157% of its population, while 109 million people were using the internet, representing 88.2% penetration. The country also recorded 97 million social media user identities in January 2025, equivalent to 78.6% of the population. This strong digital connectivity is driving Japan’s IoT market by creating a large base for connected devices, smart homes, wearables, industrial sensors, and mobile-based IoT applications. Hardware leads the component at 36.8%. IoT industrial internet leads application at 24.6%. Kanto leads regionally at 37.2%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 68.52 Billion |

|

Forecast Market Size (2034) |

USD 199.93 Billion |

|

CAGR (2026-2034) |

12.64% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Hardware (36.8%, 2025) |

|

Dominant Application |

IoT Industrial Internet (24.6%, 2025) |

|

Dominant Region |

Kanto Region (37.2%, 2025) |

Japan IoT market expanded from USD 37.80 Billion in 2020 to USD 68.52 Billion in 2025, anchored at USD 124.22 Billion in 2030, and forecast to reach USD 199.93 Billion by 2034. Japan's IoT market occupies a distinctive position in the global IoT landscape, shaped by Japan's Society 5.0 vision and manufacturing IoT demand from Japan's automobile, electronics, and precision machinery industries.

To get more information on this market, Request Sample

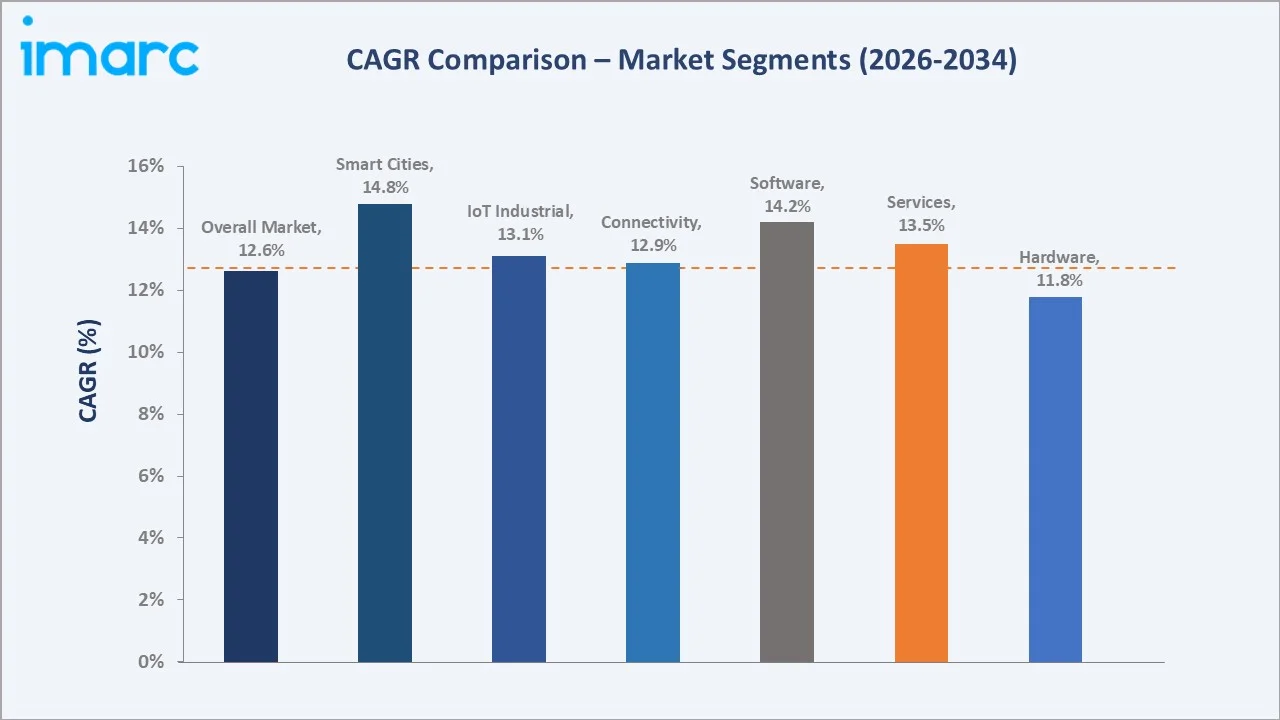

Software grows fastest at ~14.2% CAGR through AI-integrated IoT platform, digital twin, and edge analytics adoption, creating above-hardware-revenue value concentration as Japan's enterprises migrate from device-centric to platform-centric IoT investment. Smart cities grow at ~14.8% CAGR.

Executive Summary

Japan Internet of Things (IoT) market at USD 68.52 Billion in 2025 represents the most commercially technology-heritage-rich IoT market. Japan's IoT market's commercial uniqueness is the convergence of one of the largest economies' industrial demand, Japan's demographic imperative, and Japan's 5G infrastructure deployment, creating the most commercially connected IoT deployment environment. The market is projected to reach USD 199.93 Billion by 2034.

Hardware at 36.8% leads through Japan's world-class sensor, actuator, and embedded device manufacturing, creating above-software single component dominance. IoT industrial internet leads application at 24.6% through Japan's manufacturing sector. Kanto leads regionally at 37.2% through Tokyo's technology headquarters concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Hardware - 36.8% share (2025) |

|

Dominant Application |

IoT Industrial Internet - 24.6% (2025) |

|

Leading Region |

Kanto Region - 37.2% share (2025) |

|

Market Opportunity |

Connected factory AI-IoT integration; smart city infrastructure; connected car V2X platform; AgriTech IoT for rural automation; healthcare wearable IoT and remote patient monitoring |

Key Analytical Observations Supporting the Above Data:

- Hardware at 36.8%: The hardware dominates due to the widespread deployment of sensors, smart meters, connected devices, industrial equipment, and communication modules across manufacturing, automotive, healthcare, and smart city applications.

- IoT Industrial Internet at 24.6%: The IoT industrial internet dominates due to strong adoption of connected sensors, automation systems, robotics, and predictive maintenance solutions across manufacturing and industrial facilities.

- Kanto Region at 37.2%: The Kanto region dominates due to its concentration of major technology companies, manufacturing hubs, smart infrastructure projects, and enterprise headquarters in Tokyo and surrounding areas.

Japan Internet of Things Market Overview

Japan’s Internet of Things (IoT) market is expanding steadily, supported by strong digital connectivity, advanced manufacturing, smart infrastructure, and rising automation across industries. The market is driven by growing adoption of sensors, connected devices, industrial IoT platforms, smart homes, healthcare monitoring, and logistics solutions. Government-led digital transformation and the presence of major technology companies further strengthen IoT deployment across the country.

Japan's IoT ecosystem integrates hardware manufacturers, network operators, platform companies, system integrators, and government policy. Macroeconomic factors include advanced industrialization, high digital connectivity, rising automation needs, and labor shortages caused by an aging population.

Market Dynamics

To evaluate market opportunities, Request Sample

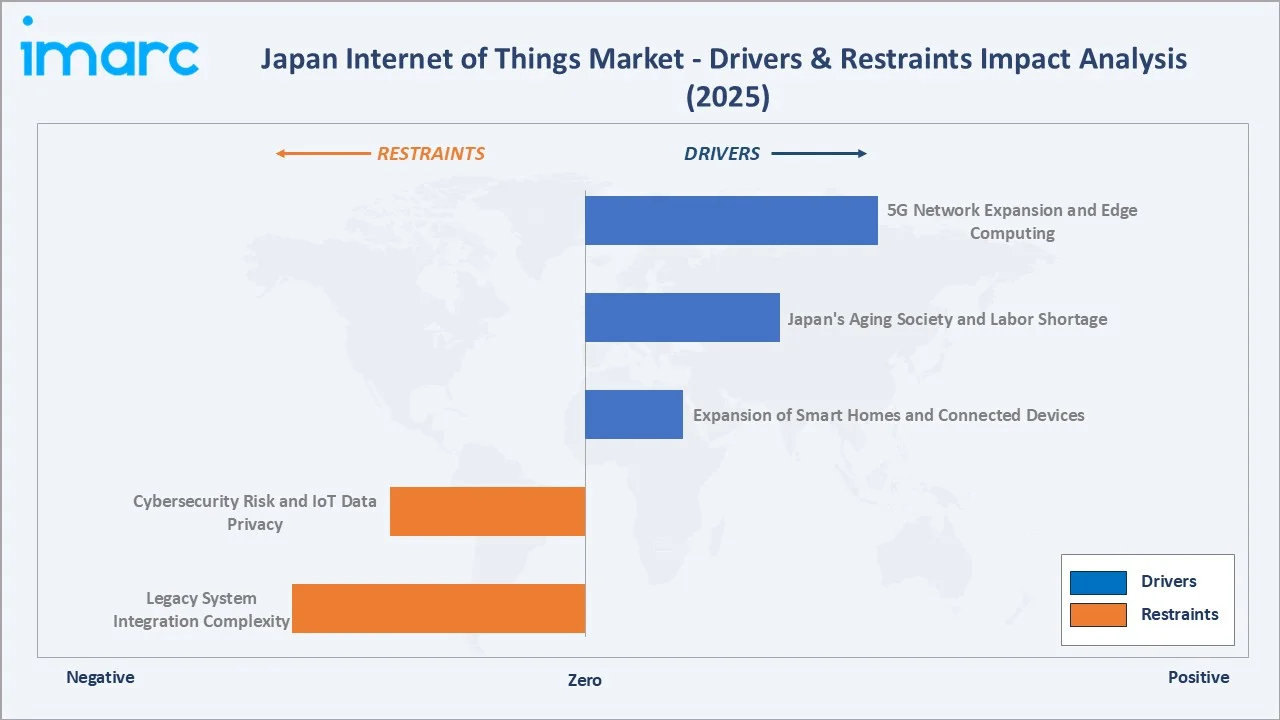

Market Drivers

- 5G Network Expansion and Edge Computing: Fitch projects that by 2029, Japan will have over 151 million 5G subscriptions. This 5G network expansion and edge computing enable faster, low-latency, and highly reliable connectivity for connected devices. These technologies support real-time data processing for industrial automation, autonomous systems, smart factories, and smart city applications. Edge computing reduces reliance on centralized cloud infrastructure by processing data closer to the source, improving operational efficiency and response times. As Japan accelerates 5G deployment, IoT adoption across manufacturing, healthcare, transportation, and logistics continues to expand.

- Japan's Aging Society and Labor Shortage: Japan’s Ministry of Internal Affairs and Communications reported that the population aged 65 and above reached a record 36.25 million in 2024, representing 29.3% of the total population. This share is expected to increase to 34.8% by 2040 and 36.3% by 2045. Japan’s aging society and labor shortage are driving IoT adoption as companies use connected devices, sensors, and automation to maintain productivity with fewer workers. IoT-enabled robotics, predictive maintenance, remote monitoring, and smart factory systems help reduce manual labor and improve operational efficiency. In healthcare, IoT supports elderly care through wearable devices, remote patient monitoring, and smart home solutions. This makes IoT a key technology for addressing Japan’s demographic and workforce challenges.

- Expansion of Smart Homes and Connected Devices: Expansion of smart homes and connected devices is driving the market as consumers increasingly adopt smart appliances, security systems, energy management tools, and voice-enabled devices. Rising demand for convenience, safety, and energy efficiency is encouraging households to integrate connected technologies. These devices generate continuous demand for sensors, connectivity modules, cloud platforms, and mobile applications. As urban households become more digitally connected, IoT adoption across the residential sector continues to grow.

Market Restraints

- Cybersecurity Risk and IoT Data Privacy: Cybersecurity risks and IoT data privacy concerns are hampering the market as connected devices generate large volumes of sensitive personal, industrial, and operational data. Weak device security, data breaches, and unauthorized access can reduce consumer and enterprise trust. These risks also increase compliance costs for IoT solution providers. As a result, companies may delay IoT adoption until stronger security frameworks and privacy safeguards are in place.

- Legacy System Integration Complexity: Legacy system integration complexity is hampering the market demand as many industries still rely on older machinery, IT platforms, and proprietary systems. Connecting these legacy assets with modern IoT sensors, cloud platforms, and analytics tools often requires high customization and technical expertise. This increases deployment time, cost, and operational risk for enterprises. As a result, some companies may delay or limit large-scale IoT adoption.

Market Opportunities

- Connected Car V2X and Mobility IoT: Connected car V2X and mobility IoT enabling real-time communication between vehicles, infrastructure, pedestrians, and traffic systems. This supports safer driving, autonomous mobility, smart traffic management, and efficient fleet operations. Japan’s strong automotive industry and smart city initiatives further encourage V2X deployment. As connected mobility expands, demand for IoT sensors, edge computing, 5G connectivity, and vehicle data platforms is expected to grow.

- Smart Agriculture IoT: Smart agriculture IoT helps farmers improve productivity amid labor shortages and an aging rural workforce. IoT sensors, drones, smart irrigation, and connected farm equipment enable real-time monitoring of soil, weather, crop health, and water usage. In November 2025, Internet Initiative Japan Inc. (IIJ) and Sony Semiconductor Solutions Corporation signed an agreement to form a joint venture focused on soil moisture sensors and irrigation guidance services for smart agriculture. Started operations in April 2026, the venture combined IIJ’s communications and smart farming expertise with Sony’s sensor technologies to improve farm efficiency, work quality, and climate-resilient agriculture. Such solutions can reduce manual work, improve resource efficiency, and strengthen IoT adoption in Japan’s agriculture sector.

Market Challenges

- Device Interoperability Issues: Device interoperability issues are a significant challenge for the market because connected devices often use different communication protocols, standards, and software platforms. This can make it difficult for organizations to integrate devices from multiple vendors into a unified IoT ecosystem. The lack of seamless compatibility increases deployment complexity, implementation costs, and maintenance requirements. As a result, enterprises may face delays in scaling IoT projects and realizing the full benefits of connected technologies.

- High Energy Consumption of Connected Devices: High energy consumption of connected devices is a challenge as the growing number of sensors, gateways, data centers, and connected systems increases electricity demand. Higher energy usage can raise operating costs for businesses and strain sustainability initiatives aimed at reducing carbon emissions. Battery-powered IoT devices also require frequent maintenance and replacement, particularly in large-scale deployments. These factors can impact the cost-effectiveness and long-term scalability of IoT solutions.

Emerging Market Trends

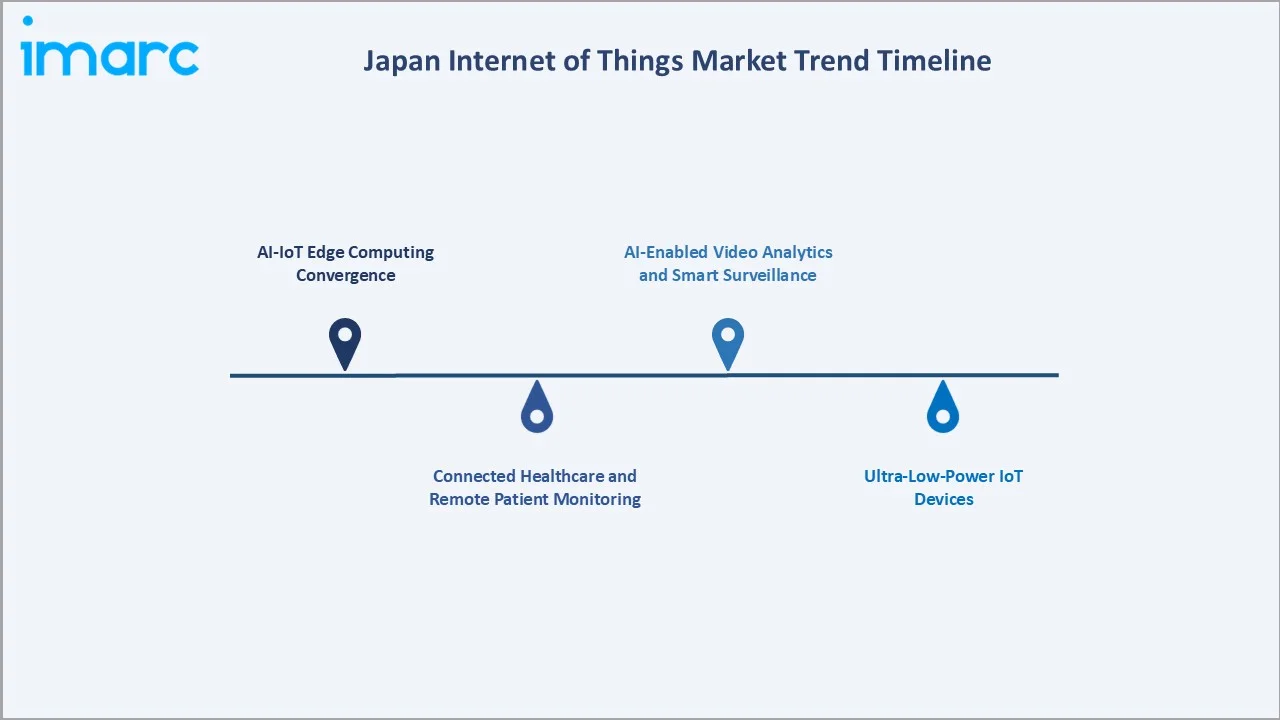

1. AI-IoT Edge Computing Convergence

AI-IoT edge computing convergence is emerging in Japan as companies increasingly combine connected sensors, real-time analytics, and AI processing at the device or network edge. This reduces latency and enables faster decision-making in smart factories, autonomous mobility, healthcare monitoring, and smart infrastructure. Edge-based AI also lowers cloud dependency and improves data privacy by processing sensitive information closer to the source. As Japan expands 5G and industrial automation, AI-enabled IoT edge solutions are gaining strong market relevance.

2. Connected Healthcare and Remote Patient Monitoring

Connected healthcare and remote patient monitoring are emerging as the country addresses rising elderly care needs and hospital capacity pressures. Wearables, smart sensors, and connected medical devices enable real-time tracking of vital signs, medication adherence, and patient activity. These solutions support early diagnosis, remote consultations, and continuous care outside hospitals. As healthcare providers adopt digital health tools, demand for secure IoT platforms and medical-grade connected devices is increasing.

3. Ultra-Low-Power IoT Devices

Ultra-low-power IoT devices are emerging in Japan as companies seek longer battery life, lower maintenance, and scalable sensor deployment across factories, homes, agriculture, and healthcare. These devices enable continuous monitoring in remote or hard-to-access locations without frequent battery replacement. They also support energy-efficient smart infrastructure and sustainability goals. In December 2025, Renesas Electronics Corporation launched its RA6W1 dual-band Wi-Fi 6 wireless MCU and RA6W2 MCU with integrated Wi-Fi 6 and Bluetooth Low Energy capabilities. The new devices target rising demand for always-connected, ultra-low-power IoT solutions across smart home, industrial, medical, and consumer applications, while integrated modules with antennas and validated RF connectivity help speed up product development. As IoT networks expand, low-power sensors and modules are becoming essential for cost-effective, large-scale deployment.

4. AI-Enabled Video Analytics and Smart Surveillance

AI-enabled video analytics and smart surveillance are emerging as cameras, sensors, and AI platforms are increasingly used for real-time monitoring. These solutions support public safety, traffic management, retail analytics, factory security, and elderly care monitoring. By analyzing video data at the edge, they reduce response time and improve operational efficiency. Rising smart city and smart building adoption is further accelerating demand for connected surveillance systems.

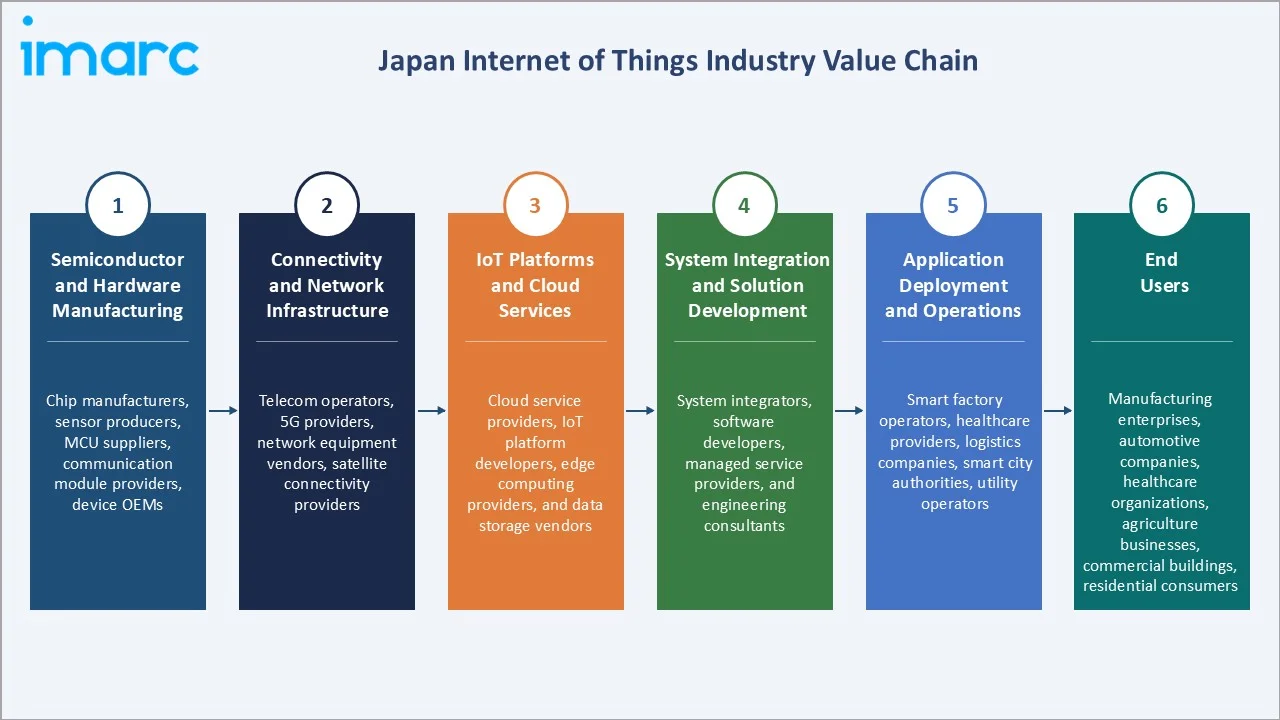

Industry Value Chain Analysis

Japan Internet of Things (IoT) value chain integrates semiconductor & hardware manufacturing, connectivity & network infrastructure, IoT platforms & cloud services, system integration & solution development, application deployment & operations, and end users.

|

Stage |

Key Participants |

|

Semiconductor & Hardware Manufacturing |

Chip manufacturers, sensor producers, MCU suppliers, communication module providers, device OEMs |

|

Connectivity & Network Infrastructure |

Telecom operators, 5G providers, network equipment vendors, satellite connectivity providers |

|

IoT Platforms & Cloud Services |

Cloud service providers, IoT platform developers, edge computing providers, and data storage vendors |

|

System Integration & Solution Development |

System integrators, software developers, managed service providers, and engineering consultants |

|

Application Deployment & Operations |

Smart factory operators, healthcare providers, logistics companies, smart city authorities, utility operators |

|

End Users |

Manufacturing enterprises, automotive companies, healthcare organizations, agriculture businesses, commercial buildings, residential consumers |

Japan's most commercially distinctive value chain characteristic is its highly advanced integration of connectivity, edge computing, and industrial automation technologies. The country combines strong semiconductor manufacturing capabilities, extensive 5G infrastructure, and a mature industrial base to support large-scale IoT deployments. This integrated ecosystem enables real-time data processing, predictive maintenance, and smart manufacturing applications, making Japan a leader in Industrial IoT and connected infrastructure solutions.

Technology Landscape in the Japan Internet of Things Industry

Edge AI and Semiconductor Innovation

Edge AI and semiconductor innovation enable real-time data processing directly on connected devices without relying heavily on cloud infrastructure. Advanced AI chips, microcontrollers, and low-power semiconductors improve processing speed, reduce latency, and enhance energy efficiency across industrial, automotive, healthcare, and smart city applications. These innovations support intelligent decision-making at the network edge while strengthening device performance and security. As Japan expands Industry 4.0 and 5G adoption, demand for AI-enabled semiconductor solutions continues to grow.

5G Private Network and Network Slicing

5G private networks and network slicing provide secure, low-latency, and highly reliable connectivity for industrial and enterprise applications. Private 5G networks enable manufacturers, logistics providers, and smart facilities to operate dedicated communication environments with greater control and security. Network slicing allows operators to allocate customized network resources for specific IoT use cases, ensuring optimal performance for critical applications. These capabilities are accelerating the adoption of smart factories, autonomous systems, and mission-critical IoT services across Japan.

Digital Twin Technology Integration

Digital twin technology integration enables virtual replicas of physical assets, production lines, buildings, and infrastructure to be monitored in real time through connected sensors. These digital models help organizations simulate operations, predict equipment failures, and optimize performance before issues occur. In May 2026, rFpro introduced an engineering-grade digital twin of Japan’s Hakone Turnpike, a 15 km toll road running through the mountainous forests of Kanagawa Prefecture. The route is commonly used by Japanese automakers for vehicle dynamics testing and development. This supports digital twin technology integration in Japan’s IoT industry by enabling realistic virtual testing of vehicles, road conditions, and mobility systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

36.8% |

2025 |

|

Application |

IoT Industrial Internet |

24.6% |

2025 |

|

Vertical |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

37.2% |

2025 |

By Component

Hardware leads at 36.8% (2025). Japan's IoT hardware ecosystem encompasses sensors, actuators, connectivity modules, embedded processors, IoT gateways, and edge computing devices, creating Japan's most commercially above-import-dependent single domestic component supply chain for IoT hardware.

To access detailed market analysis, Request Sample

Services at 27.5% encompass managed IoT services, system integration, security services, and consulting. Software at 22.4% grows fastest at ~14.2% CAGR through AI-IoT platform, digital twin, and edge analytics. Connectivity at 13.3% reflects 5G IoT and private network services.

By Application

IoT industrial internet leads at 24.6% (2025), through Japan's manufacturing sector's connected factory, predictive maintenance, and IoT investments, creating Japan's most commercially industrial IoT application concentration.

IoT connected cars at 17.8% reflect Japan's automotive IoT content. Smart cities at 14.9% grow fastest at ~14.8% CAGR. Smart home at 13.6%, IoT connected healthcare at 11.2%, smart wearables at 8.7%, smart grid at 5.4%, and others at 3.8% collectively represent Japan's above-industrial-only multi-application IoT market.

Regional Market Insights

|

Region |

Share (2025) |

Key Japan Internet of Things Market Drivers & Characteristics |

|

Kanto |

37.2% |

Driven by the concentration of technology companies, enterprise headquarters, data centers, and smart city initiatives. |

|

Kansai/Kinki |

18.6% |

Driven by its advanced manufacturing base, electronics industry, and smart factory deployments. |

|

Central/Chubu |

14.7% |

Supported by its automotive and industrial manufacturing ecosystem. |

|

Kyushu-Okinawa |

9.4% |

Benefits from its growing semiconductor industry, smart infrastructure projects, and expanding digital connectivity. |

|

Tohoku |

7.1% |

Supported by smart city initiatives, renewable energy projects, and digital infrastructure modernization. |

|

Chugoku |

5.4% |

Driven by industrial automation, connected logistics networks, and smart manufacturing investments. |

|

Hokkaido |

4.3% |

Emerging as an important market for IoT applications in agriculture, environmental monitoring, and smart energy management. |

|

Shikoku |

3.3% |

Represents a smaller but growing IoT market, supported by increasing digitalization, smart utility projects, and industrial modernization efforts. |

Kanto's 37.2% dominance reflects Tokyo's technology headquarters concentration, creating Japan's most commercially IoT-enterprise-procurement-dense single metropolitan area. Kansai's 18.6% reflects manufacturing IoT, component IoT, and medical IoT, creating Japan's second IoT commercial center. Chubu's 14.7% reflects automotive IoT concentration.

Kyushu-Okinawa's 9.4% reflects Japan's semiconductor investment and smart city leadership. Tohoku's 7.1% reflects disaster-resilience IoT and smart agriculture innovation. Chugoku's 5.4% reflects connected car and industrial IoT. Hokkaido's 4.3% reflects Japan's most commercially precision-agriculture-IoT-concentrated above-urban single regional IoT application. Shikoku's 3.3% reflects aquaculture IoT, creating Japan's most commercially rural-IoT-specialized above-urban-concentration single regional application.

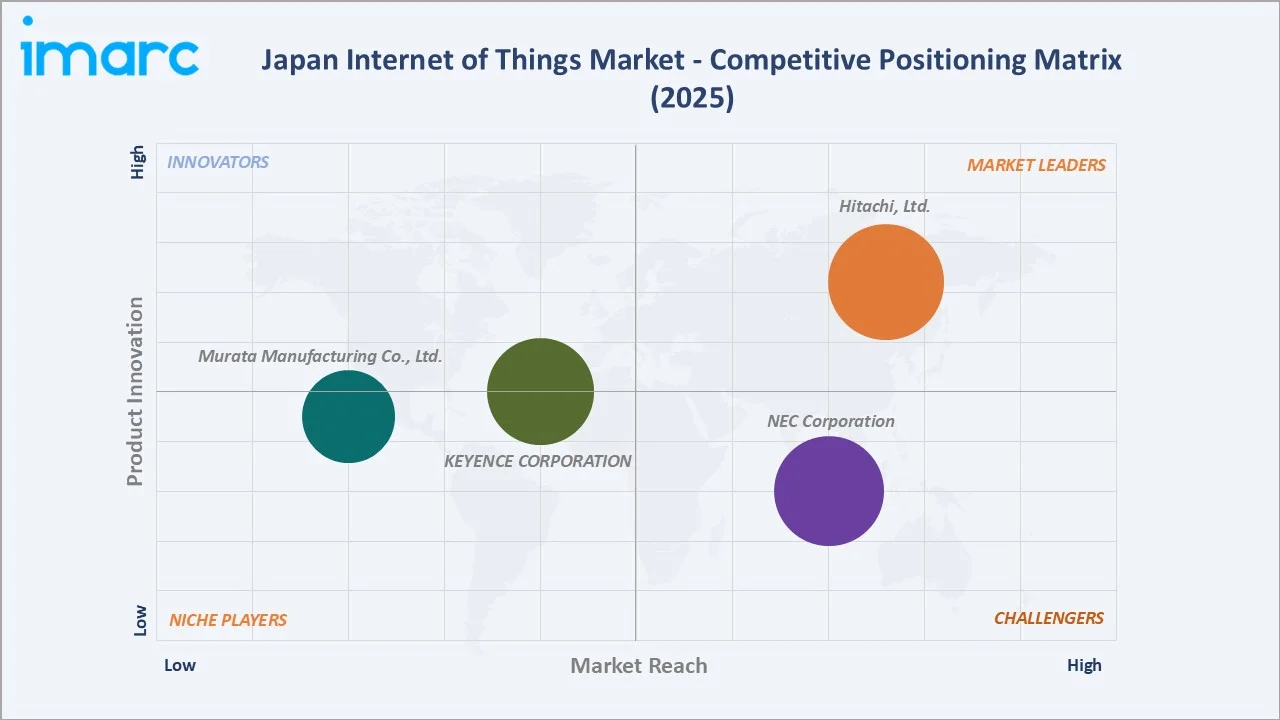

Competitive Landscape

Japan Internet of Things (IoT) competitive landscape is commercially stratified between Japan's most commercially dominant domestic IT giants, Japan's industrial IoT specialists, Japan's hardware IoT leaders, and telecom operator IoT platforms.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Hitachi, Ltd. |

Lumada |

Market Leader |

Hitachi, Ltd. plays a central role in Japan's Internet of Things (IoT) landscape by bridging Operational Technology (OT) with Information Technology (IT). |

|

NEC Corporation |

NEC Industrial IoT |

Strong Challenger |

NEC Corporation plays a foundational role in Japan's Internet of Things (IoT) landscape, serving as a key technology provider, systems integrator, and innovator in digital transformation for both public and private sectors. |

|

KEYENCE CORPORATION |

IoT and Sensors |

Established Player |

KEYENCE CORPORATION is a leading Japanese player in Industrial Internet of Things (IIoT) and factory automation (FA), acting as a crucial enabler of digital transformation in manufacturing. |

|

Murata Manufacturing Co., Ltd. |

IoT & Murata Sensors |

Established Player |

Murata Manufacturing Co., Ltd. plays a foundational role in Japan’s Internet of Things (IoT) ecosystem, transitioning from a component manufacturer to a comprehensive "one-stop solution provider". |

Japan's IoT competitive landscape is evolving through AI-IoT convergence, international cloud hyperscaler expansion, and hardware miniaturization leadership.

Key Company Profiles

Hitachi, Ltd.

Hitachi, Ltd. is one of Japan’s leading technology and industrial conglomerates and a prominent player in the Internet of Things (IoT) market. The company provides a broad portfolio of IoT solutions spanning industrial automation, smart manufacturing, transportation, energy, healthcare, smart cities, and digital infrastructure.

- Key Products: Lumada.

- Strategic Focus: Centered on expanding Industrial IoT, smart infrastructure, and digital transformation solutions.

NEC Corporation

NEC Corporation is a leading Japanese information technology and telecommunications company with a strong presence in the Internet of Things (IoT) market. The company provides end-to-end IoT solutions encompassing connectivity infrastructure, edge computing, AI, cloud platforms, cybersecurity, and system integration services.

- Key Products: NEC Industrial IoT.

- Strategic Focus: Centered on strengthening smart connectivity, 5G-enabled IoT ecosystems, and AI-driven digital transformation solutions.

Market Concentration Analysis

Japan Internet of Things market is moderately concentrated, served by Japan's largest IT companies with significant participation from international cloud providers, specialized hardware companies, and telecom operators. However, the presence of specialized IoT platform providers, semiconductor companies, telecom operators, and emerging technology firms creates a competitive environment. Innovation in AI, edge computing, 5G connectivity, and smart infrastructure remains a key differentiating factor among market participants.

Investment & Growth Opportunities

Highest Growth Segments

Smart cities (~14.8% CAGR), software/AI-IoT platform (~14.2% CAGR), connected healthcare (~13.5% CAGR through aging demographic), smart grid IoT (~12.8% CAGR), connected cars/V2X (~13.1% CAGR), and AgriTech IoT (~15-18% CAGR from small base) represent Japan's highest-growth IoT investment vectors through 2034.

Investment Themes

- AgriTech precision agriculture IoT: Investment in Hokkaido-specific precision agriculture IoT creates Japan's most commercially above-commercial single AgriTech IoT investment opportunity.

- Edge AI IoT semiconductor for Japan's precision manufacturing quality application: Japan's manufacturing sector's above-human single AI defect detection requirement, creating Japan's most commercial edge AI IoT quality inspection investment mandate through Japan's single zero-defect manufacturing quality standard, creating an edge AI vision sensor investment opportunity.

Future Market Outlook (2026-2034)

Japan Internet of Things market is projected to grow from USD 68.52 Billion in 2025 to USD 199.93 Billion by 2034, delivering a 12.64% CAGR over the forecast period, through the convergence of Japan's most commercially certain IoT investment drivers: demographic imperative, manufacturing quality competitiveness, and energy transition, creating Japan's most commercially multi-mandate IoT investment growth trajectory.

Three structural forces define Japan's IoT market growth through 2034: IoT investment demand through a digital transformation, AI-IoT convergence, creating Japan's most commercially above-connectivity-and-sensor single platform value migration, and demographics creating Japan's most commercially structural automation and healthcare IoT demand.

Research Methodology

Primary Research

Primary research comprised structured interviews with Japan IoT market stakeholders (2025), including IoT Platform Directors, Business Unit Managers, Partnership Managers, Product Managers, application engineers, manufacturing engineers, and enterprise IoT buyer survey from Japan large enterprises and SME manufacturers.

Secondary Research

Secondary research encompassed manufacturing white paper, information and communications white paper, Japan IoT initiative, company annual reports, Ministry of Internal Affairs and Communications 5G statistics, and Japan population forecast. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a component expenditure model: Japan IoT total market estimated from Japan IT investment statistics by sector, multiplied by IoT-specific share of IT investment and IoT-specific growth premium above general IT investment through IoT adoption acceleration.

Japan Internet of Things Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Hardware, Software, Services, Connectivity |

| Applications Covered | Smart Home, Smart Wearables, Smart Cities, Smart Grid, IoT Industrial Internet, IoT Connected Cars, IoT Connected Healthcare, Others |

| Verticals Covered | Healthcare, Energy, Public and Services, Transportation, Retail, Individuals, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central /Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Companies Covered | Hitachi, Ltd., NEC Corporation, KEYENCE CORPORATION, Murata Manufacturing Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan internet of things market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Japan internet of things market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan internet of things industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Internet of Things Market Report

The Japan Internet of Things market reached USD 68.52 Billion in 2025, driven by rising adoption of industrial automation, smart manufacturing, 5G connectivity, and edge computing across major industries. Growing demand for connected healthcare, smart homes, logistics tracking, and smart city infrastructure is further supporting IoT deployment. Japan’s aging population and labor shortages are also encouraging enterprises to use IoT-based monitoring, robotics, and predictive maintenance solutions.

The Japan IoT market grows at 12.64% CAGR during 2026-2034, reaching USD 199.93 Billion by 2034. The overall growth is sustained by 5G infrastructure, aging society labor automation demand, manufacturing IoT culture, and connected car V2X expansion, creating Japan's most commercially multi-driver above-single-factor IoT growth trajectory.

Hardware leads at 36.8% through Japan's IoT component manufacturing, creating an above-import-dependent single domestic IoT hardware supply.

IoT industrial internet leads at 24.6% through Japan's manufacturing sector's connected factory, predictive maintenance, and IoT investment, creating Japan's most commercially industrial IoT application concentration through Japan's manufacturing culture's quality obsession, aligning with IoT's real-time monitoring and AI analytics capability.

Kanto region leads at 37.2% through Tokyo's concentration of Japan's largest technology company headquarters, Japan's highest enterprise IoT procurement decision maker concentration, and Japan's most commercially 5G-dense above-other-prefecture single IoT connectivity infrastructure.

Leading companies include Hitachi, Ltd., NEC Corporation, KEYENCE CORPORATION, and Murata Manufacturing Co., Ltd., among others.

The Japan IoT market is projected to reach approximately USD 124.22 Billion by 2030, with connected cars expected to remain one of the fastest-growing IoT applications. The 2030 outlook will be supported by V2X deployment, smart city IoT, and progress in autonomous mobility.

Three priority investment opportunities: rural IoT investment, AgriTech precision agriculture IoT, and edge AI IoT semiconductor for Japan's precision manufacturing quality application.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade