Japan Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Japan Logistics Market Summary:

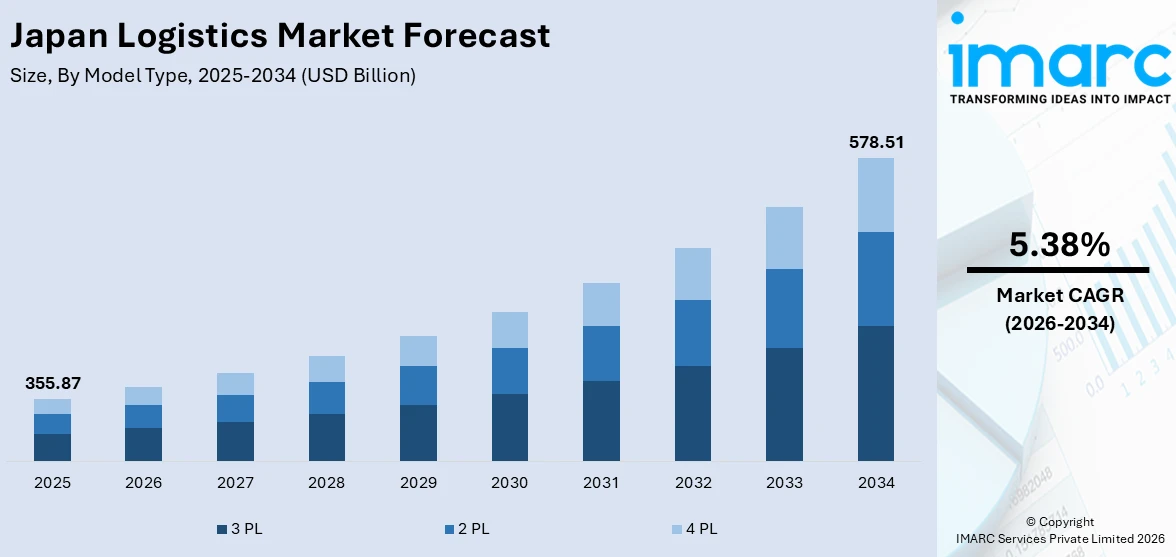

The Japan logistics market was valued at USD 355.87 Billion in 2025 and is anticipated to reach USD 578.51 Billion by 2034, growing at a compound annual growth rate of 5.38% during 2026-2034.

Japan's logistics sector is advancing on the back of rapid e-commerce expansion, increasing automation adoption, and the government's sustained focus on infrastructure modernization. Rising demand from manufacturing, healthcare, and retail end-use sectors is further reinforcing the Japan logistics market share, as operators invest in smart warehousing, last-mile delivery capabilities, and sustainable freight solutions to meet evolving supply chain requirements.

Key Takeaways and Insights:

- By Model Type: 3 PL dominates with a 44.6% share in 2025, driven by widespread outsourcing of integrated warehousing, order fulfillment, and supply chain management functions by manufacturing and retail companies.

- By Transportation Mode: Roadways hold the largest share at 48.2% in 2025, reflecting the dominance of truck-based freight movement across Japan's extensive domestic distribution networks.

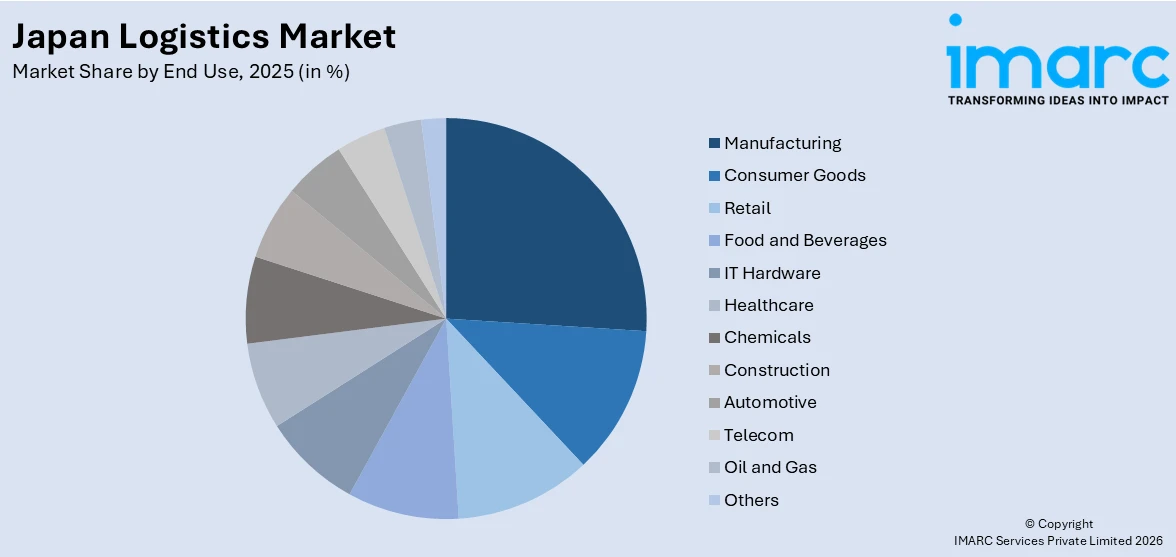

- By End Use: Manufacturing represents 26.3% share in 2025, underpinned by Japan's significant industrial base, particularly in the automotive and electronics sectors.

- By Region: Kanto Region leads with 35.4% share in 2025, supported by Tokyo's role as the nation's foremost commercial and logistics distribution hub.

- Key Players: The Japan logistics market features a mix of large domestic conglomerates and global express carriers competing through service diversification, digital investments, sustainable fleet development, and strategic partnerships to strengthen nationwide distribution capabilities.

To get more information on this market Request Sample

Japan's logistics market is undergoing a structural transformation shaped by technology integration, sustainability imperatives, and evolving regulatory norms. The government's active push for digital transformation, green logistics, and infrastructure modernization continues to attract fresh capital from both domestic and international players, reshaping competitive dynamics across the sector. Meanwhile, the "2024 Problem", a structural labor reform placing strict limits on truck driver overtime hours, has compelled operators to accelerate modal shifting, technology adoption, and last-mile innovation to sustain service reliability under tighter operating conditions. Leading logistics companies are spearheading investments in automation, AI-based routing, and sustainable fleets to offset workforce gaps and rising operational costs. The industry's decisive pivot toward digitally enabled, resilient supply chain operations is being reinforced by a broader ecosystem of technology providers, infrastructure developers, and logistics real estate investors recognizing Japan's long-term demand fundamentals. This convergence of regulatory pressure, workforce challenges, and technology-driven modernization is broadly expected to sustain strong and consistent market momentum throughout the forecast period, positioning Japan as a benchmark for intelligent and efficient supply chain management in the Asia-Pacific region.

Japan Logistics Market Trends:

E-Commerce-Driven Demand for Last-Mile Logistics

Japan's rapidly expanding e-commerce sector is catalyzing significant investment in last-mile delivery infrastructure. Consumer expectations for same-day and next-day delivery have prompted logistics operators to establish micro-fulfillment centers in urban areas and integrate AI-driven route optimization systems. In April 2025, Rakuten Group Inc. introduced autonomous delivery robots in Tokyo's Harumi district, marking a pivotal step toward extended last-mile logistics beyond warehouse environments. This trend is fundamentally reshaping distribution strategies and accelerating the deployment of advanced delivery technologies across the country.

Green Logistics and Sustainability Initiatives

Environmental priorities are reshaping Japan's logistics sector, with companies accelerating the adoption of eco-friendly transportation and warehousing solutions. Logistics firms are deploying electric and hydrogen-powered delivery vehicles, optimizing delivery routes for carbon reduction, and integrating renewable energy systems into distribution centers. In February 2024, DHL Express formed a long-term agreement with SCREEN Semiconductor Solutions Co. Ltd. to achieve carbon neutrality, utilizing sustainable aviation fuel under its GoGreen Plus program. Government-backed incentives for green logistics continue to deepen industry-wide sustainability commitments nationwide.

Digital Transformation and Automation in Warehousing

The integration of artificial intelligence, Internet of Things (IoT), and robotics is fundamentally transforming Japan's warehousing and distribution operations. Logistics operators are increasingly adopting warehouse management systems, automated guided vehicles, and AI-powered inventory management platforms to enhance operational efficiency and reduce growing labor dependencies. The widespread deployment of automated storage and retrieval systems across fulfillment centers is streamlining order processing, improving accuracy, and enabling round-the-clock operations with minimal human intervention. This accelerating shift toward intelligent warehousing reflects the sector's broader commitment to digital maturity, as companies recognize automation as a critical lever for sustaining competitiveness amid structural workforce constraints and rising consumer delivery expectations.

.webp)

Market Outlook 2026-2034:

The Japan logistics market is poised for robust expansion, supported by accelerating digital infrastructure investment, government-led automation initiatives, and growing end-use sector demand. Strategic investments in green logistics, including hydrogen-powered fleets, energy-efficient warehouses, and sustainable packaging, are expected to gain further traction as companies align with Japan's 2050 carbon neutrality goal. Concurrently, the government's planned automated cargo corridor between Tokyo and Osaka is anticipated to address long-standing transportation capacity gaps. The market will also benefit from rising demand for temperature-controlled and pharmaceutical logistics, as Japan's aging population increases healthcare delivery requirements. Collectively, these forces are expected to propel the Japan logistics market from USD 355.87 Billion in 2025 to USD 578.51 Billion by 2034, at a compound annual growth rate of 5.38%.

Japan Logistics Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Model Type |

3 PL |

44.6% |

|

Transportation Mode |

Roadways |

48.2% |

|

End Use |

Manufacturing |

26.3% |

|

Region |

Kanto Region |

35.4% |

Model Type Insights:

- 2 PL

- 3 PL

- 4 PL

3 PL leads the market with a 44.6% of the total Japan logistics market in 2025.

Third-party logistics has emerged as the dominant model type in Japan, driven by an increasingly complex and demand-intensive supply chain environment. Manufacturers, retailers, and e-commerce companies are progressively outsourcing warehousing, transportation, and inventory management functions to specialist 3PL providers to reduce capital investment, improve flexibility, and access advanced logistics infrastructure. The growing complexity of cross-border trade, coupled with heightened consumer expectations around delivery speed and accuracy, has made 3PL partnerships indispensable for businesses seeking to scale operations efficiently without expanding in-house logistics capabilities. Providers offer integrated services spanning inbound logistics, order fulfillment, returns management, and value-added operations, making them essential partners across diverse verticals including automotive, consumer electronics, pharmaceuticals, and fast-moving consumer goods.

The role of 3PL providers in Japan is also being redefined by the accelerating integration of technology within logistics operations. Major 3PL operators are investing heavily in automated warehouses, AI-powered demand forecasting, and real-time shipment tracking systems to enhance service quality and reduce error rates. Strategic joint ventures and partnerships are increasingly common, as companies recognize the value of combining complementary capabilities to deliver comprehensive, end-to-end logistics solutions spanning import and export management, warehousing, and packaging. This technology-led evolution is strengthening the overall value proposition of 3PL services and encouraging broader adoption across small and medium-sized enterprises seeking to compete more effectively in Japan's demanding and rapidly evolving logistics environment.

Transportation Mode Insights:

- Roadways

- Seaways

- Railways

- Airways

Roadways dominate the market, with a 48.2% of the total Japan logistics market in 2025.

Road-based freight transportation forms the backbone of Japan's domestic logistics network, offering unmatched reach and flexibility across the country's diverse geographic landscape. The trucking sector facilitates the movement of goods from manufacturing plants and distribution hubs to retail outlets, residential areas, and remote locations, making it the most operationally versatile mode of transport. Japan's well-developed road infrastructure, including expressway networks connecting major cities and regional centers, supports efficient freight movement across short and medium-haul distances. The sector serves as the primary mode for consumer goods delivery, manufacturing supply chains, food and beverage distribution, and e-commerce fulfillment, underpinning demand across virtually every end-use vertical covered in the report.

Despite its dominance, the road freight sector in Japan is navigating a period of significant structural change. The implementation of the government's Work Style Reform Act, which places strict limits on truck driver overtime hours, has introduced substantial capacity constraints across the domestic trucking network. Logistics operators are responding through modal shifting, fleet electrification, and the accelerating adoption of autonomous driving technology to sustain service reliability under tighter operating conditions. The industry's pivot toward automated freight solutions signals a broader and decisive shift away from labor-intensive operational models, as companies seek to offset deepening workforce shortages and support long-term efficiency across Japan's road freight landscape.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Manufacturing

- Consumer Goods

- Retail

- Food and Beverages

- IT Hardware

- Healthcare

- Chemicals

- Construction

- Automotive

- Telecom

- Oil and Gas

- Others

Manufacturing holds the largest segment, with a 26.3% of the total Japan logistics market in 2025.

Manufacturing represents the largest end-use segment within Japan's logistics market, anchored by the country's status as one of the world's foremost industrial producers. The automotive, electronics, and machinery sectors generate substantial logistics requirements spanning raw material inbound flows, intermediate component delivery, and finished goods outbound distribution. Japan's complex and time-sensitive manufacturing supply chains, particularly in the automotive sector where just-in-time production principles remain the operational norm, demand highly reliable, precision-managed logistics solutions. The dependence on integrated logistics for managing multi-tier supplier networks and coordinating production schedules across geographically dispersed facilities reinforces the manufacturing segment's position as the primary revenue contributor within the market.

The manufacturing segment's logistics requirements are also evolving in response to broader industrial restructuring and supply chain resilience priorities. Recent global supply disruptions have prompted Japanese manufacturers to diversify supplier bases, localize critical component sourcing, and strengthen domestic inventory buffers, all of which increase the complexity and volume of logistics activity. Export-oriented manufacturers are also investing in dedicated logistics corridors and advanced port connectivity to ensure seamless global supply chain integration. The continued expansion of Japan's industrial output, supported by the government's reindustrialization policies and foreign direct investment inflows, is expected to sustain strong logistics demand within the manufacturing segment over the forecast period.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region exhibits a clear dominance in the market, with a 35.4% share of the total Japan logistics market.

Kanto Regiondominates the Japanese logistics industry in terms of the largest share of the country's logistics market. This is due to the fact that it is the primary business and logistics center of Japan. It comprises a large concentration of industrial facilities, retail markets, distribution centers, and port facilities, including the Yokohama port and the Tokyo Bay logistics facilities. It has a large population density and a high level of consumer spending, which translates to a constant and high level of demand for logistics services of all kinds.

Kanto is the primary testing ground for the most advanced and cutting-edge logistics facilities and services, including the use of automation technology, underground conveyor systems, and the use of technology to improve the efficiency of the extensive logistics facilities of the region. Kanto has and will continue to attract the attention of investors due to its large concentration of quality logistics facilities and its ability to provide a constant and high level of demand for logistics services. This is due to the fact that it is the nerve center of the Japanese logistics industry.

Market Dynamics:

Growth Drivers:

Why is the Japan Logistics Market Growing?

E-Commerce Expansion and Rising Consumer Delivery Expectations

The rapid acceleration of e-commerce activity in Japan is one of the most powerful drivers reshaping the logistics market. Sustained growth in online shopping is generating substantial and rising demand for efficient parcel delivery, compelling logistics companies to invest in sophisticated last-mile infrastructure, including micro-fulfillment centers, autonomous delivery robots, and AI-driven route optimization platforms. Consumer expectations around same-day and next-day delivery continue to intensify, prompting third-party logistics providers to continuously upgrade their fulfillment capabilities and expand their distribution networks. Digital platforms connecting shippers and carriers are further enhancing end-to-end delivery efficiency, reducing friction across the supply chain and making logistics performance a key competitive differentiator for e-commerce operators seeking to retain and grow their customer base in Japan's increasingly demanding retail environment.

Government Infrastructure Investment and Modernization Initiatives

Government-led infrastructure investment is a significant catalyst for logistics market expansion in Japan. A series of strategic initiatives targeting port modernization, highway development, and freight corridor construction are enhancing connectivity between production centers and distribution networks across the country. The government's active pursuit of automated cargo transportation solutions is expected to optimize logistics operations, reduce transit delays, and streamline supply chains along the country's busiest freight corridors. Additionally, government subsidies supporting digital transformation in logistics — including IoT integration, AI-based route planning, and warehouse automation — are accelerating the modernization of Japan's logistics ecosystem. This sustained and multi-dimensional policy commitment is positioning Japan as a global benchmark for intelligent, technology-enabled supply chain infrastructure and reinforcing the country's long-term competitiveness in regional and international trade networks.

Expanding International Trade and Asia-Pacific Supply Chain Integration

Japan's deepening integration with regional and global trade networks is a key structural driver of logistics market growth. The country's strategic geographic position as a gateway to Asia-Pacific markets, combined with its advanced port infrastructure and air freight capabilities, positions it as a critical logistics hub for exports spanning automotive components, electronics, specialty chemicals, and pharmaceuticals. Major port facilities and international airports across Japan continue to handle substantial cargo volumes, while ongoing air freight network expansions are broadening reach for time-sensitive and high-value goods. Leading logistics operators are actively strengthening cross-border service capabilities to meet rising demand for reliable and efficient international freight solutions. The continued expansion of trade with Southeast Asian economies, coupled with evolving global supply chain realignment trends, is further amplifying demand for Japan-origin logistics services and reinforcing the country's role as an indispensable node in the broader Asia-Pacific supply chain ecosystem.

Market Restraints:

What Challenges the Japan Logistics Market is Facing?

Structural Labor Shortages and Aging Workforce

Japan's logistics sector faces a deepening structural workforce crisis, particularly in road freight, where the truck driver workforce is aging rapidly. A significant proportion of active drivers are approaching retirement age, while the influx of younger entrants remains insufficient to replenish the workforce at the required pace. The government's overtime reforms, while necessary to improve driver welfare and working conditions, have compounded short-term capacity constraints by limiting the hours available for freight movement. Long working hours and relatively low wages continue to discourage younger generations from entering the sector, making talent attraction and retention a core and persistent industry challenge that operators must urgently address to safeguard long-term logistics service reliability.

Rising Operational Costs and Fuel Price Volatility

Escalating operational costs pose a significant restraint on Japan's logistics market. Tightening labor regulations have further increased wage bills, while soaring construction costs for new logistics facilities are pushing rental rates higher in key metropolitan markets. These compounding cost pressures are squeezing margins for operators, particularly small and medium-sized logistics providers that lack the scale advantages of major players. The upward cost trajectory is also being passed on to shippers, potentially dampening demand in cost-sensitive segments and eroding competitive positioning.

Logistics Oversupply and Vacancy Rate Pressures

The rapid pace of large-scale logistics facility development in Japan's major metropolitan areas has created pockets of oversupply in key urban markets. While long-term demand fundamentals remain robust, the accelerated delivery of new logistics real estate has exceeded near-term absorption capacity in several regions, resulting in an imbalance between available supply and active tenant demand. This oversupply dynamic is lengthening tenant attraction periods and placing downward pressure on rental rates at non-prime locations, posing near-term revenue and yield challenges for logistics real estate operators and asset owners seeking to maintain stable occupancy levels across their portfolios.

Competitive Landscape:

The market for logistics in Japan has been defined as one that is competitive in nature, with both domestic conglomerates and international service providers being part of this market. The domestic market has been dominated by large conglomerates, with competition from these large conglomerates being in the form of service range, technology adoption, and geographical reach. The presence of international service providers has been felt in Japan, with these companies maintaining an active presence in the market, particularly in the area of cross-border and express freight services. The capacity to deliver integrated end-to-end services in the logistics market has been emerging as one of the key differentiators in this market, which has been evolving in nature.

Japan Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Logistics Market Report

The Japan logistics market reached a value of USD 355.87 Billion in 2025.

The Japan logistics market is projected to exhibit a compound annual growth rate of 5.38% during 2026-2034 to reach USD 578.51 Billion by 2034.

Key growth drivers include the rapid expansion of e-commerce, increasing automation adoption, government infrastructure investment, and growing demand from manufacturing and healthcare end-use sectors.

3 PL dominates the model type segment, reflecting the widespread outsourcing of warehousing, transportation management, and integrated supply chain operations by Japanese businesses across manufacturing, retail, and e-commerce verticals.

Some of the challenges faced by the Japan logistics market include labor shortages, aging workforce, rising operational costs, infrastructure oversupply, and strict driver overtime regulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)