Japan Luxury Furniture Market Size, Share, Trends and Forecast by Raw Material, Application, Distribution Channel, Design, and Region, 2026-2034

Japan Luxury Furniture Market Summary:

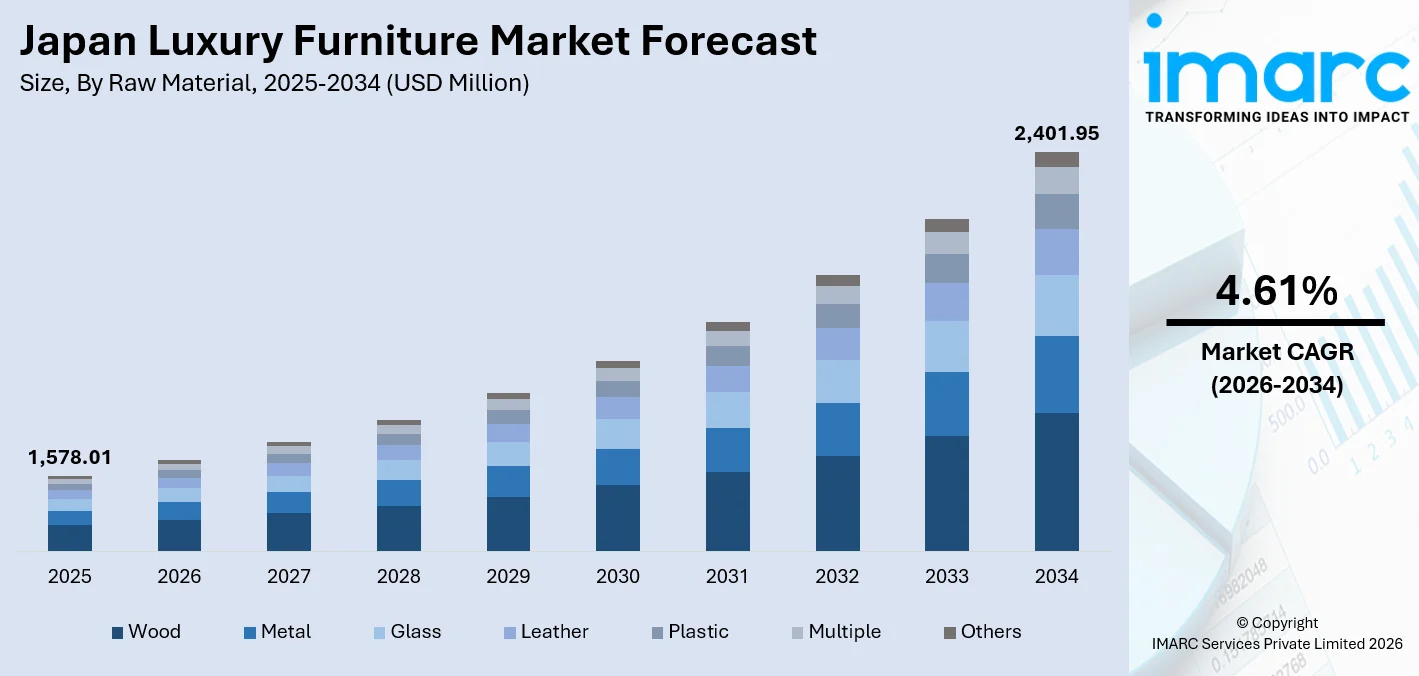

The Japan luxury furniture market size was valued at USD 1,578.01 Million in 2025 and is projected to reach USD 2,401.95 Million by 2034, growing at a compound annual growth rate of 4.61% from 2026-2034.

The Japan luxury furniture market is expanding steadily, fueled by rising consumer aspirations for premium residential interiors, a deepening cultural reverence for artisanal craftsmanship, and growing investments in high-end home renovation. Affluent urban consumers are increasingly prioritizing aesthetics and material quality in their purchasing decisions, while expanding demand from the luxury hospitality and commercial sectors adds further momentum, reinforcing the Japan luxury furniture market share across key applications and distribution channels.

Key Takeaways and Insights:

- By Raw Material: Wood dominates the market with a share of 38.4% in 2025, owing to its deep-rooted cultural resonance, natural aesthetic appeal, and enduring association with traditional Japanese craftsmanship and artisanal quality standards.

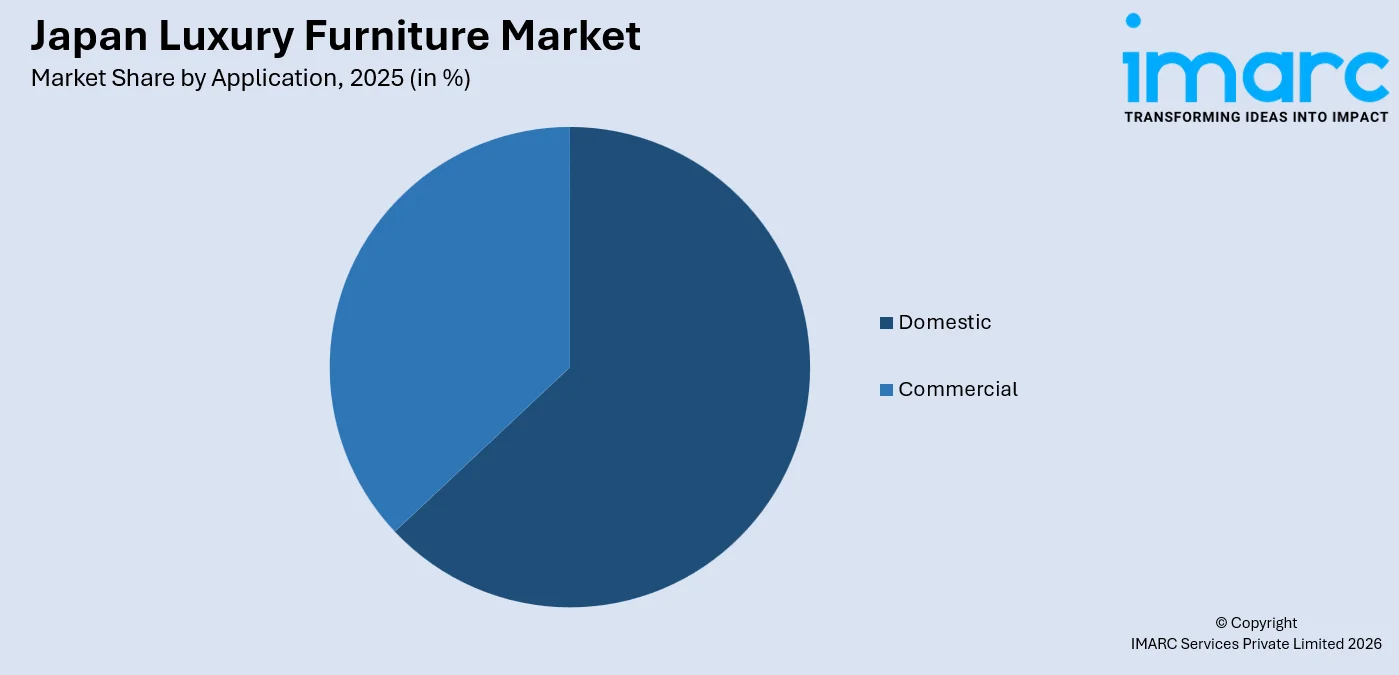

- By Application: Domestic leads the market with a share of 62.5% in 2025. This dominance is driven by elevated consumer spending on premium home interiors, growing preference for bespoke living spaces, and Japan's strong residential culture centered on quality and comfort.

- By Distribution Channel: Specialty stores represent the largest segment with a market share of 35.2% in 2025, reflecting affluent consumers' preference for curated, expert-guided purchasing experiences and premium product assortment available through dedicated luxury retail environments.

- By Design: Modern exhibits a clear dominance in the market with 52.3% share in 2025, driven by urban consumers' preference for clean lines, minimalist forms, and versatile aesthetics that complement contemporary Japanese residential and commercial interiors.

- By Region: Kanto Region represents the largest region with 41.6% share in 2025, driven by the high concentration of Japan's affluent population, well-established luxury retail infrastructure, and robust high-end interior design demand across Tokyo's metropolitan corridor.

- Key Players: Key players drive the Japan luxury furniture market by expanding product portfolios, forging collaborations with globally renowned designers, and enhancing premium retail experiences. Their investments in sustainable sourcing, bespoke customization capabilities, and strategic flagship store openings in prime urban locations strengthen brand positioning and accelerate adoption across diverse consumer segments.

To get more information on this market Request Sample

The Japan luxury furniture market is witnessing growth driven by various factors, which are converging in the market. Increasing household incomes, especially in key metropolitan cities such as Tokyo, Osaka, and Yokohama, are enabling end-users in these markets to purchase luxury home furnishing products that are not only aesthetically different but also showcase superior craftsmanship. Additionally, the Japanese culture of appreciating luxury living spaces and the value of understated elegance has continued to support the demand for luxury furniture that offers a perfect blend of form and functionality. At the same time, the Japan luxury furniture market is witnessing the emergence of international interior design styles, which are being driven by social media and international travel patterns, thus influencing the purchasing behavior of affluent consumers in the country. At the same time, the recovery of inbound tourism is supporting the growth of the luxury hotel sector in Japan. Sustainability has become another key factor, as affluent consumers are increasingly demanding wood and materials that are certified as sustainable, thus reflecting the value of aesthetics and sustainability.

Japan Luxury Furniture Market Trends:

Premiumization of Residential Interiors

Japan's residential luxury furniture segment is undergoing a notable premiumization shift as urban households prioritize personalized, aesthetically refined living environments. Consumers are investing in bespoke furniture pieces that reflect individual taste, artisanal quality, and the intersection of Japanese minimalism with global design influences. This trend is reinforced by the growing influence of interior design culture, particularly among affluent millennials who treat the home as a curated expression of identity, driving consistent Japan luxury furniture market growth and expanding demand for exclusive, design-led residential collections.

Expansion of Sustainable and Eco-Certified Luxury Offerings

Environmental consciousness is reshaping luxury furniture preferences in Japan, with consumers placing greater emphasis on sustainably sourced materials, eco-certified timber, and low-emission manufacturing processes. Brands are responding by adopting transparent supply chains and responsibly crafted product lines aligned with Japan's broader commitment to carbon neutrality. In 2025, Meuble, Mitsui & Co. Plastics, and Biomass Resin Holdings introduced RICEWAVE™, a next-generation sustainable material derived from recycled rice, exemplifying Japan's growing capacity for eco-aligned innovation within the luxury furniture production ecosystem.

Growth of Digital and E-Commerce Channels for Premium Furniture

Digital retail platforms are redefining the luxury furniture purchasing experience in Japan, enabling consumers to explore exclusive collections, access virtual visualization tools, and commission customized orders remotely. Leading brands are deploying augmented reality features and curated digital showrooms to replicate premium in-store experiences online. In October 2024, Sumitomo Corporation invested in Social Interior Inc., a digital platform offering furniture subscription services and office design solutions, reflecting the growing integration of technology within Japan's high-end home and commercial furnishings distribution ecosystem.

Market Outlook 2026-2034:

The Japan luxury furniture market is expected to continue its growth trajectory in the upcoming years, driven by the consistent demand for luxury residential furniture, growth in the luxury hospitality sector, and the continued trend of premiumizing residential space. The demand for luxury residential furniture has been driven by the consistent willingness of affluent consumers in Japan to spend on luxury products that offer unique designs, traditional craftsmanship, and modern styles, as reflected in the rise in disposable incomes in key cities in the country. Additionally, the growth in the luxury commercial sector, which includes luxury hotels, boutique offices, and luxury hospitality spaces, is expected to contribute significantly to the growth in the luxury furniture market in Japan, driven by the growth in the inbound tourism economy in the country. At the same time, the growth in digital channels is expected to increase the accessibility of the luxury market, offer greater customization options, and expand the luxury brand presence beyond traditional flagship store footprints. Sustainability products are expected to become a key differentiator for luxury brands, impacting brand strategies and consumer behavior throughout the forecast period. The market generated a revenue of USD 1,578.01 Million in 2025 and is projected to reach a revenue of USD 2,401.95 Million by 2034, growing at a compound annual growth rate of 4.61% from 2026-2034.

Japan Luxury Furniture Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Raw Material |

Wood |

38.4% |

|

Application |

Domestic |

62.5% |

|

Distribution Channel |

Specialty Stores |

35.2% |

|

Design |

Modern |

52.3% |

|

Region |

Kanto Region |

41.6% |

Raw Material Insights:

- Wood

- Metal

- Glass

- Leather

- Plastic

- Multiple

- Others

Wood leads the market with a share of 38.4% of the total Japan luxury furniture market in 2025.

Wood commands a dominant presence within Japan's luxury furniture market, underpinned by centuries of woodworking heritage that has elevated timber-based craftsmanship to a refined art form. Japanese consumers associate wooden furniture with warmth, natural beauty, and an authenticity that is difficult to replicate with alternative materials. High-quality hardwoods such as oak, walnut, hinoki cypress, and cedar are particularly valued for their visual richness and tactile depth. Artisan-crafted wooden pieces, characterized by precise joinery techniques and hand-applied finishes, continue to attract discerning buyers who prioritize longevity, understated luxury, and timeless aesthetic expression over transient design trends.

The sustained dominance of wood in the luxury segment is further reinforced by growing consumer demand for eco-certified and sustainably sourced timber products, a trend that resonates strongly among Japan's environmentally conscious affluent demographic. Furniture makers are increasingly adopting responsible supply chains and partnering with skilled artisans to produce distinctive, handcrafted pieces that reflect both environmental stewardship and premium material quality. This convergence of sustainability and craftsmanship has elevated Japanese timber-based furniture into a globally recognized expression of responsible luxury, appealing to discerning buyers who seek pieces that carry both aesthetic depth and ethical provenance.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Domestic

- Living Room and Bedroom

- Kitchen

- Bathroom

- Outdoor

- Lighting

- Commercial

- Office

- Hospitality

- Others

Domestic dominates with a market share of 62.5% of the total Japan luxury furniture market in 2025.

The domestic application segment commands the largest share of the Japan luxury furniture market, driven by consistent and broad demand for premium furnishings across residential settings. Japanese homeowners, particularly in high-income urban districts, are investing heavily in elevating the quality and design of their living spaces through carefully curated furniture selections. The living room and bedroom categories represent the most active purchasing areas within the domestic segment, with consumers seeking statement pieces that combine visual sophistication with ergonomic comfort and the spatial efficiency demanded by Japan's aspirational but compact urban residences.

Beyond core living spaces, growing consumer interest in premium kitchen fittings, designer bathroom furniture, and sophisticated outdoor collections is broadening the scope of domestic luxury demand. Affluent homeowners increasingly approach the home as an integrated luxury environment, extending premium furnishing investments to every functional zone rather than limiting expenditure to principal living areas. This holistic approach to residential luxury reflects a deeper cultural shift in which the quality, material distinction, and aesthetic coherence of every interior space, from the kitchen to the bathroom to the outdoor terrace, are regarded as essential components of an elevated domestic lifestyle.

Distribution Channel Insights:

- Conventional Furniture Stores

- Specialty Stores

- Online Retailers

- Others

Specialty stores hold the largest segment with a 35.2% share of the total Japan luxury furniture market in 2025.

Specialty stores occupy a dominant position in Japan's luxury furniture distribution landscape, offering affluent consumers an immersive, curated retail experience that aligns with the premium expectations of the segment. These dedicated environments are staffed by knowledgeable design consultants who assist buyers in navigating extensive collections and commissioning bespoke pieces, adding a personalized dimension to the purchasing journey. Major urban centers including Tokyo, Osaka, and Yokohama serve as hubs for high-end specialty showrooms, where flagship stores from domestic artisan brands and international luxury labels attract discerning clientele seeking premium, individualized furnishings.

The sustained prominence of specialty stores reflects a broader consumer behavior pattern in which luxury furniture buyers prioritize the tactile and experiential dimensions of purchasing, the ability to examine materials, evaluate proportions, and receive expert interior guidance. This preference is especially pronounced among high-net-worth consumer segments who associate the specialty retail environment with trust, exclusivity, and design authority. In October 2025, Danish luxury brand Fredericia opened its first Tokyo showroom in collaboration with local studio Flooat, featuring a refined minimalist interior that reinforced the growing importance of dedicated specialty retail experiences within Japan's premium furniture market.

Design Insights:

- Modern

- Contemporary

Modern holds the largest share with 52.3% of the total Japan luxury furniture market in 2025.

Modern design is the dominant aesthetic force within Japan's luxury furniture market, reflecting the strong preference of urban consumers for clean geometric forms, neutral palettes, and functional elegance. This design philosophy aligns naturally with Japan's cultural appreciation for simplicity and spatial efficiency, making it the favored choice for luxury residential and commercial interiors across major metropolitan regions. Modern luxury furniture balances visual restraint with material richness, combining premium woods, brushed metals, and refined upholstery in compositions that feel both timeless and expressive of contemporary sensibilities sought by Japan's discerning affluent consumers.

The sustained appeal of modern design within the luxury segment is reinforced by its versatility across diverse interior environments, from compact urban apartments to expansive villas and premium commercial spaces. Interior designers and affluent consumers alike gravitate toward modern luxury collections that can be layered and customized to achieve distinctive, personally expressive spaces. Japanese furniture brands have been particularly adept at translating modern design principles into globally acclaimed expressions, combining the precision of traditional craftsmanship with clean, contemporary forms that resonate with both domestic and international audiences seeking understated yet unmistakably refined luxury furnishings.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

Kanto Region is the largest region with a 41.6% share of the total Japan luxury furniture market in 2025.

The Kanto Region holds the leading position in Japan's luxury furniture market, anchored by the vast economic and consumer spending power concentrated in Tokyo, Kanagawa, Saitama, and surrounding prefectures. With the highest density of high-net-worth households and international residents in the country, the region sustains exceptional demand for premium residential furnishings. The concentration of luxury flagship stores, interior design studios, and high-end architectural projects in Tokyo's upscale districts further reinforces Kanto's commanding market dominance.

Kanto's luxury furniture demand is further propelled by the region's thriving high-end hospitality sector, active corporate real estate development, and the growing influx of international tourists frequenting Tokyo's premium retail and cultural destinations. Japan's expanding luxury travel economy, driven significantly by inbound visitor growth, is stimulating ongoing investment in premium commercial furnishings across upscale hotels, boutique offices, and high-end dining establishments concentrated throughout the greater Kanto metropolitan area.

Market Dynamics:

Growth Drivers:

Why is the Japan Luxury Furniture Market Growing?

Rising Consumer Affluence and Aspiration for Premium Home Environments

Japan's growing affluent consumer class is playing a central role in propelling the luxury furniture market forward. As household incomes rise, particularly in major urban centers such as Tokyo, Osaka, and Yokohama, consumers are dedicating increasing proportions of their discretionary spending to elevating the quality and aesthetic of their residential environments. This behavioral shift reflects a broader cultural evolution in which the home has transitioned from a purely functional space to an intentional statement of personal identity, refined taste, and material well-being. The deepening penetration of global interior design culture, facilitated through social media platforms, international design publications, and growing exposure to luxury hospitality environments, is significantly expanding consumer awareness of premium furniture as an expression of elevated living standards. Affluent homeowners are increasingly engaging professional interior designers and architects for residential projects, drawing inspiration from upscale hotel interiors and global design exhibitions. This aspiration-driven demand is reinforced by a generational shift among younger high-net-worth consumers who prioritize design-led purchasing, artisanal provenance, and long-term quality over transactional furnishing decisions, collectively establishing a durable foundation for sustained luxury furniture market growth across Japan's metropolitan and suburban affluent demographics.

Expanding Luxury Hospitality Sector and Commercial Interior Investment

Japan's thriving inbound tourism economy and the rapid expansion of its luxury hospitality infrastructure represent a powerful structural driver for the premium furniture market. Each new hospitality development requires extensive, carefully curated furniture procurement prioritizing design distinction, material quality, and alignment with the aspirational expectations of international luxury travelers. Beyond hospitality, Japan's corporate real estate sector is contributing meaningfully to luxury furniture demand through the renovation and development of premium office environments that reflect brand prestige and support employee well-being. High-end workspaces featuring carefully selected luxury furniture collections are increasingly deployed as tools for talent attraction and corporate image differentiation, particularly among financial services, technology, and creative industry firms operating in Tokyo and Osaka. The intersection of residential, hospitality, and commercial demand channels is creating a multi-dimensional growth architecture for Japan's luxury furniture market, ensuring stable and diversified expansion across multiple application categories throughout the forecast period.

Cultural Heritage of Craftsmanship and Growing Sustainability Emphasis

Japan's deeply ingrained cultural reverence for artisanal craftsmanship forms a foundational driver of the luxury furniture market. The country's woodworking traditions, including highly refined joinery techniques and handcrafted finishing methods developed over centuries, have cultivated generations of skilled artisans whose work commands premium valuations both domestically and internationally. This heritage distinguishes Japanese luxury furniture from mass-produced alternatives, resonating deeply with consumers who seek pieces that embody cultural meaning, technical precision, and enduring aesthetic value. Complementing this cultural foundation is the rapidly growing emphasis on sustainability, which has become an integral dimension of luxury purchasing decisions in Japan. Affluent consumers are increasingly prioritizing eco-certified materials, responsibly sourced timber, and low-emission manufacturing processes as part of a broader commitment to responsible consumption. The Japanese government's policy framework supporting domestic timber utilization, including grants from the Forestry Agency for firms transitioning toward domestic wood sources, has encouraged manufacturers to adopt sustainable practices, enabling them to position their offerings at the intersection of luxury and environmental stewardship, creating a compelling and differentiated market proposition that reinforces Japan's global standing as a leader in responsible, design-driven luxury furniture craftsmanship.

Market Restraints:

What Challenges the Japan Luxury Furniture Market is Facing?

Yen Depreciation and Rising Import Costs

The significant depreciation of the Japanese yen has substantially elevated the cost of imported raw materials, including tropical hardwoods, premium leathers, and specialty metals commonly used in luxury furniture production. Smaller and mid-sized manufacturers with limited hedging capacity face pronounced margin compression as the rising cost of imported inputs outpaces achievable retail price increases. This cost pressure undermines profitability across the supply chain, constraining investment in product innovation and new collection development at a time when competitive differentiation is increasingly critical to sustaining market share.

Demographic Decline and Aging Population Dynamics

Japan's well-documented demographic decline, characterized by a shrinking overall population, declining household formation rates, and a rapidly aging consumer base, presents a meaningful long-term structural challenge for the luxury furniture market. Declining new housing starts in rural prefectures and the gradual contraction of Japan's aspirational middle-income consumer segment are reducing the pipeline of prospective luxury furniture buyers, particularly in non-metropolitan regions. While major urban centers retain robust demand, sustaining broader market growth in the face of deteriorating demographic fundamentals requires brands to develop targeted strategies for senior-focused luxury products and internationally oriented consumer segments.

High Price Sensitivity Among Aspirational Consumer Segments

Despite strong demand from Japan's established high-net-worth demographic, the luxury furniture market faces limitations in penetrating broader aspirational consumer segments due to significant price differentials between premium and mid-range products. Many consumers who aspire to luxury furniture ownership are deterred by high upfront costs and the absence of accessible financing or rental options for premium pieces. This challenge constrains the addressable market and limits the ability of luxury furniture brands to expand volume, particularly as competitive pressure from high-quality mid-premium alternatives grows more intense across Japan's urban retail landscape.

Competitive Landscape:

The Japan luxury furniture market is characterized by a moderately concentrated competitive scenario, with prominent local artisan furniture brands, global luxury furniture and interior designers, and upscale international retailers competing with each other. Partnerships between Japanese furniture manufacturers and globally acclaimed designers are increasingly being utilized as a tool to enhance brand awareness and penetrate specific consumer segments. Digital retail and bespoke customization are emerging as important competitive factors, which are going to be utilized by luxury furniture retailers and manufacturers to cater to the growing need for customized luxury furniture solutions in the Japan market.

Recent Developments:

- In October 2025, Danish luxury furniture brand Fredericia opened its first showroom in Tokyo in collaboration with local design studio Flooat. The venue, positioned within a minimalist industrial concrete building, presented the brand's premium furniture collections in a setting that blended Scandinavian design heritage with Tokyo's refined contemporary aesthetic, marking a significant expansion of European luxury furniture's dedicated retail presence within Japan's premium market.

Japan Luxury Furniture Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Raw Materials Covered | Wood, Metal, Glass, Leather, Plastic, Multiple, Others |

| Applications Covered |

|

| Distribution Channels Covered | Conventional Furniture Stores, Specialty Stores, Online Retailers, Others |

| Designs Covered | Modern, Contemporary |

| Regions Covered | Kanto Region, Kansai/Kinki Region, Central/ Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Luxury Furniture Market Report

The Japan luxury furniture market size was valued at USD 1,578.01 Million in 2025.

The Japan luxury furniture market is expected to grow at a compound annual growth rate of 4.61% from 2026-2034 to reach USD 2,401.95 Million by 2034.

Wood dominated the market with a share of 38.4%, driven by Japan's cultural reverence for artisanal woodworking, the natural aesthetic appeal of premium timber, and a growing consumer preference for eco-certified, sustainably sourced luxury furnishings across residential and commercial settings.

Key factors driving the Japan luxury furniture market include rising consumer affluence and growing premium home investment, a deeply rooted culture of artisanal craftsmanship, expanding luxury hospitality demand, growing sustainability consciousness, and increasing integration of digital retail channels enabling wider premium product accessibility.

Major challenges include yen depreciation elevating import material costs, long-term demographic decline constraining household formation, high upfront product pricing limiting broader consumer segment penetration, and intensifying competition from high-quality mid-premium furniture alternatives across Japan's urban retail landscape.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)