Japan Meat Market Size, Share, Trends and Forecast by Type, Product, Distribution Channel, and Region, 2026-2034

Japan Meat Market Size, Share, Trends & Forecast (2026-2034)

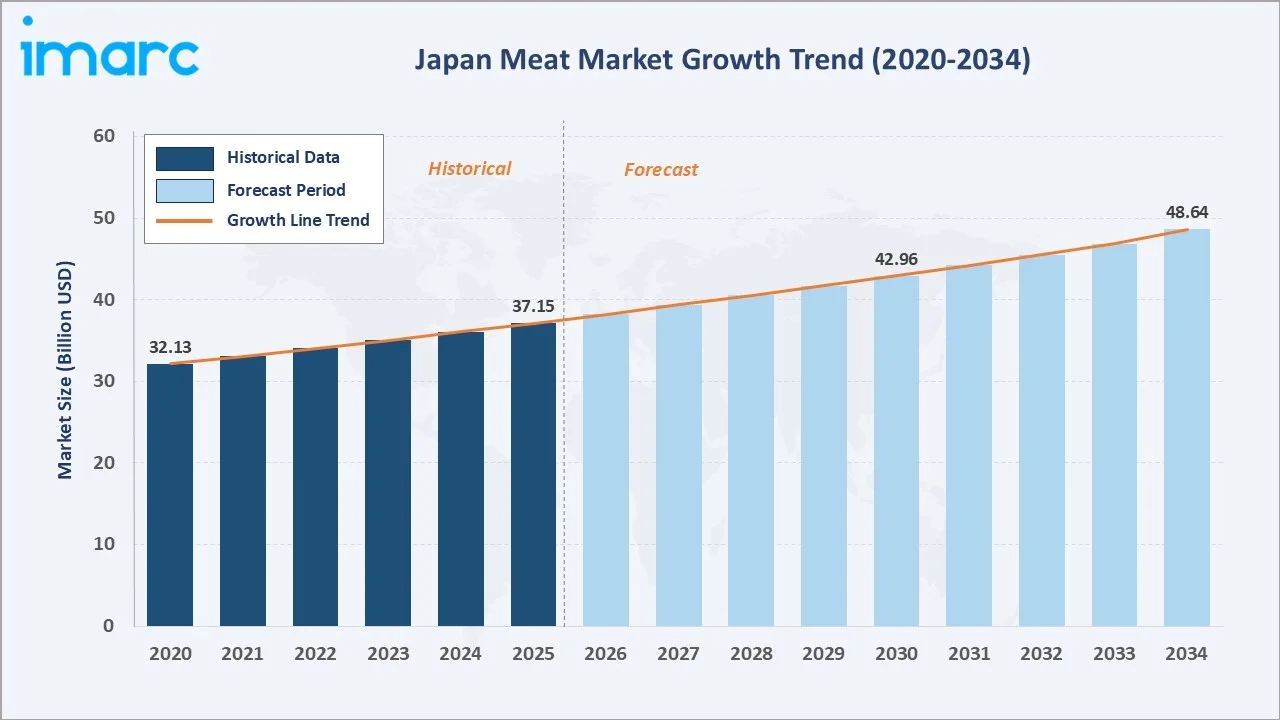

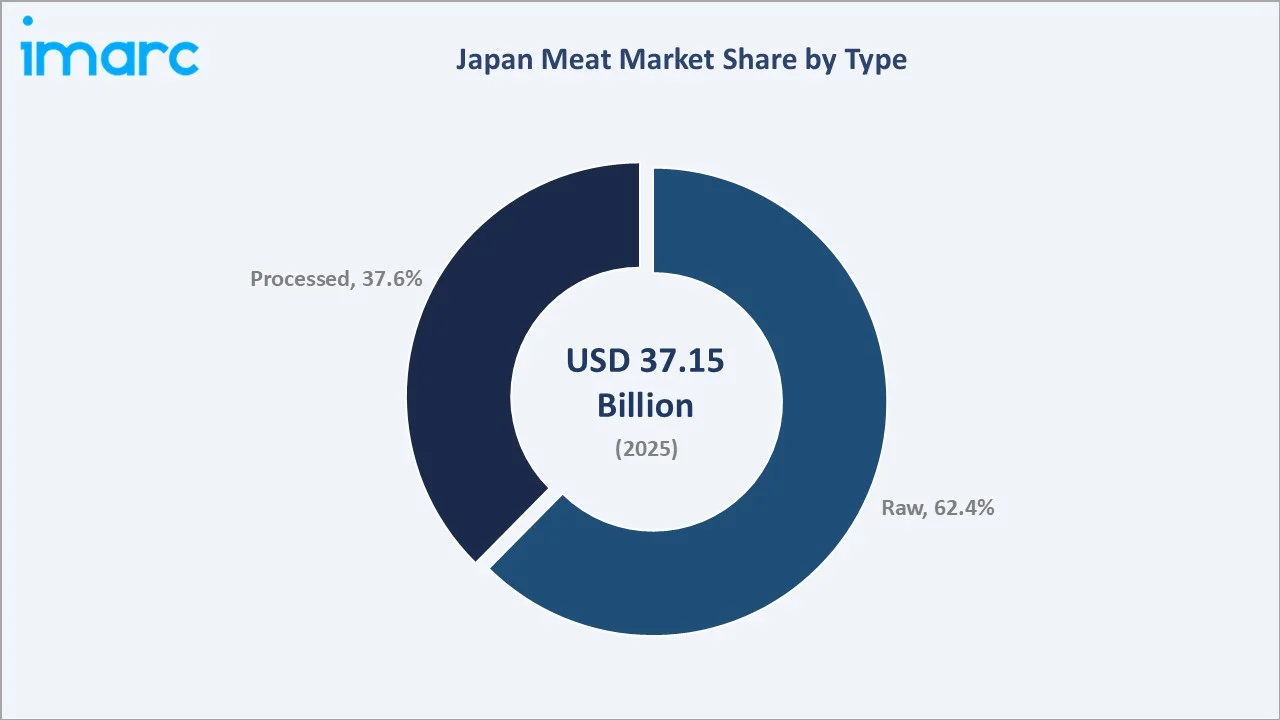

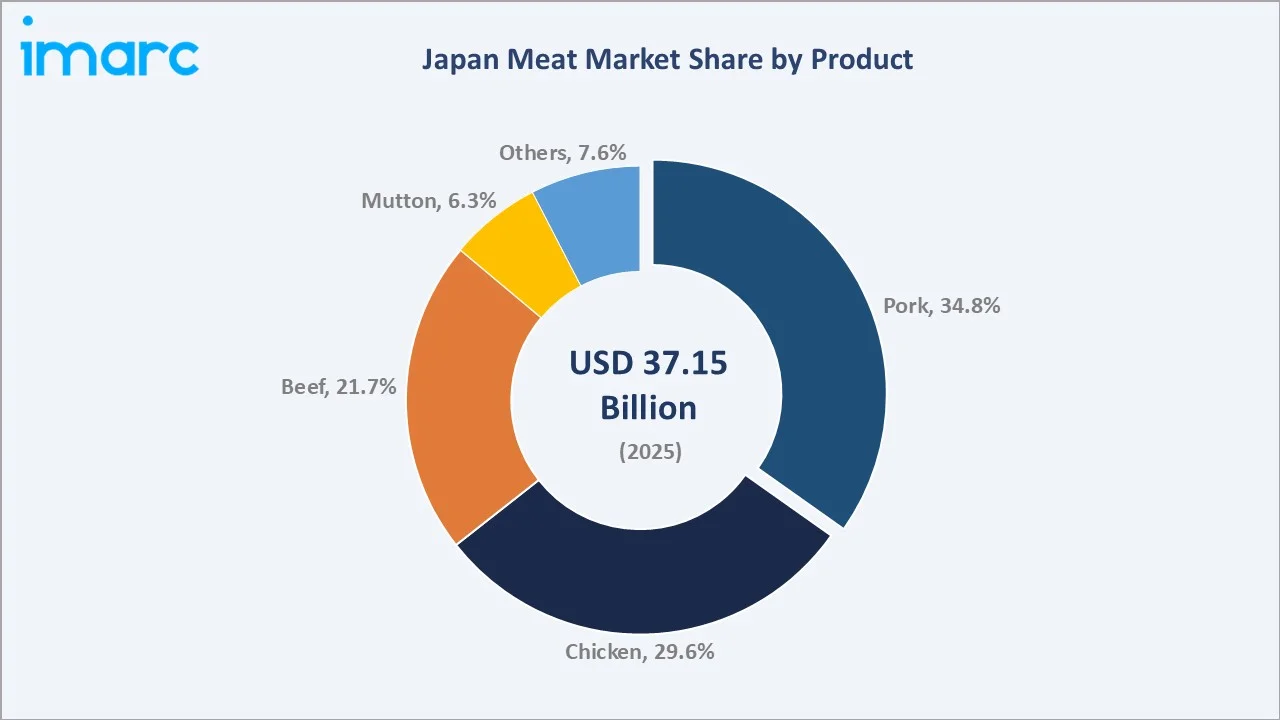

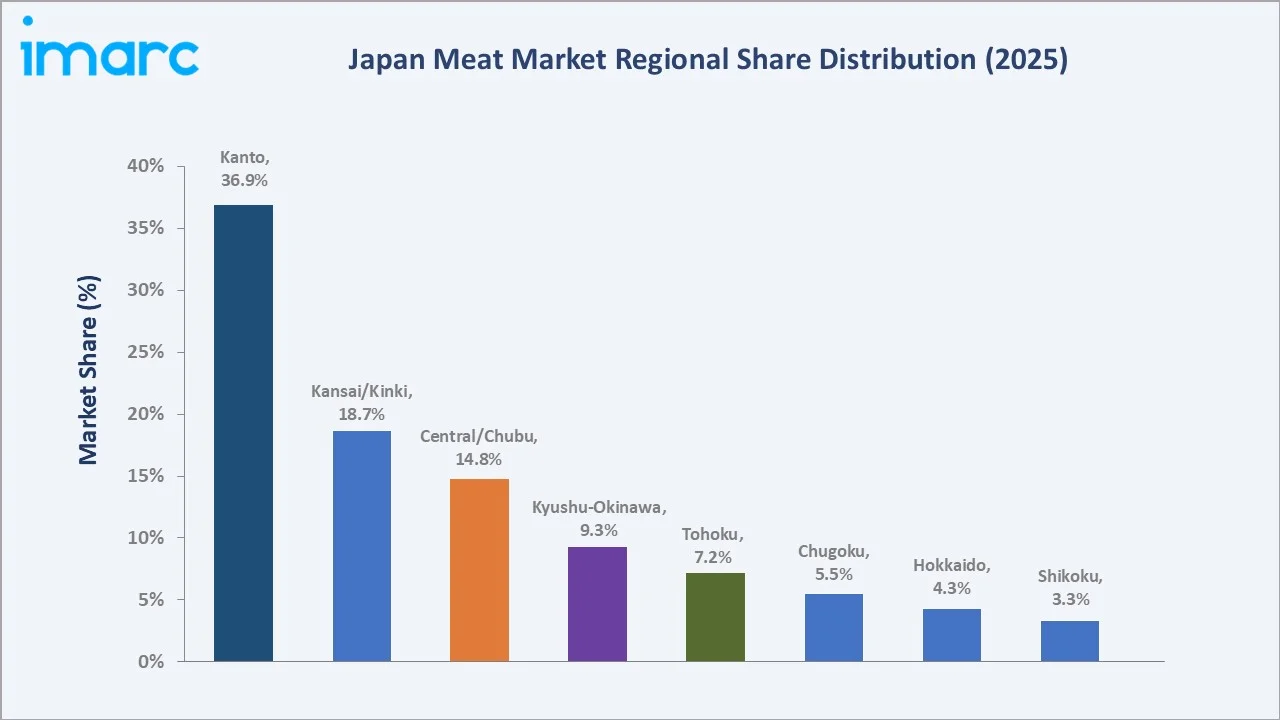

The Japan meat market reached USD 37.15 Billion in 2025 and is projected to reach USD 48.64 Billion by 2034, growing at a CAGR of 2.95% during 2026-2034. The market is driven by steady demand for high-quality protein, rising consumption of processed and ready-to-cook meat products, and strong foodservice demand. Japan’s per capita meat consumption is expected to rise steadily, increasing from 43.0 kilograms in 2021 to 47.8 kilograms by 2030. Premium beef, poultry, and imported meat products are further supporting market growth. Raw meat leads the type at 62.4%. Pork leads the product at 34.8%. Kanto leads regionally at 36.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 37.15 Billion |

|

Forecast Market Size (2034) |

USD 48.64 Billion |

|

CAGR (2026-2034) |

2.95% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Raw Meat (62.4%, 2025) |

|

Dominant Product |

Pork (34.8%, 2025) |

| Leading Region | Kanto Region (36.9%, 2025) |

Japan meat market expanded from USD 32.13 Billion in 2020 to USD 37.15 Billion in 2025, supported by increasing meat consumption and demand for processed and ready-to-cook products. The market is expected to reach USD 42.96 Billion by 2030 and USD 48.64 Billion by 2034, indicating sustained growth driven by premium meat demand, foodservice recovery, and import-based supply expansion.

To get more information on this market, Request Sample

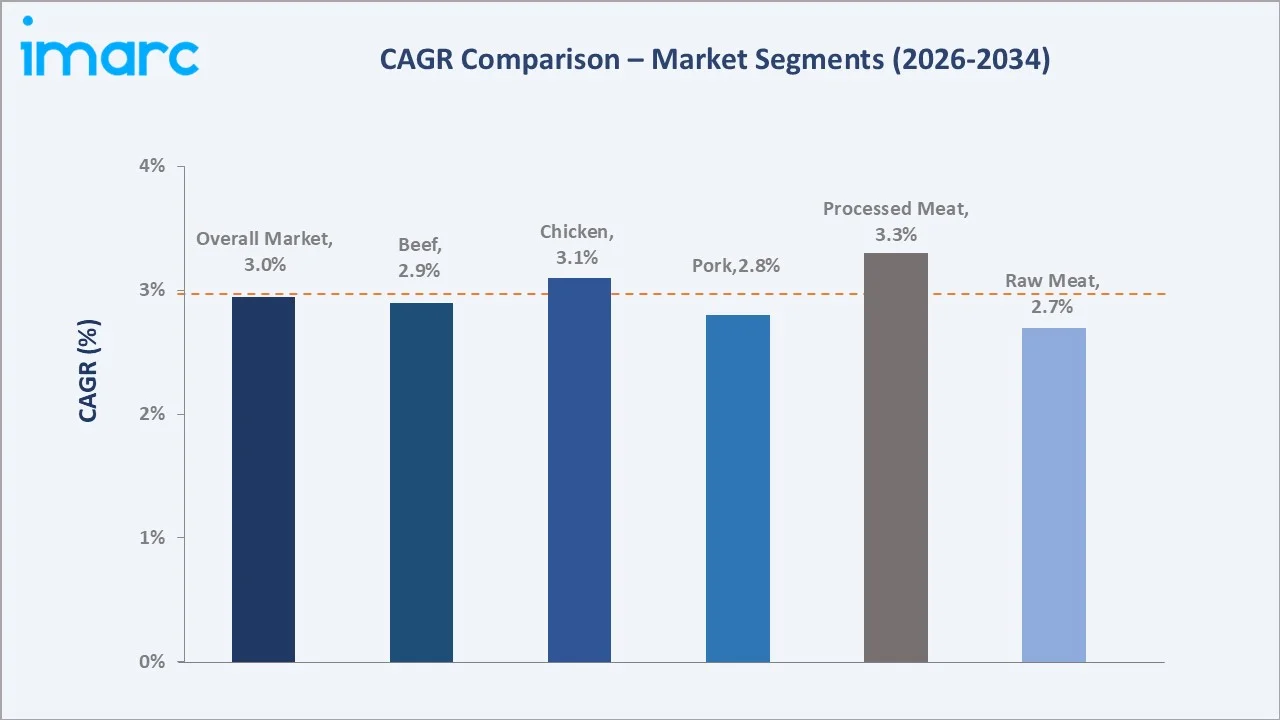

Processed meat grows fastest at ~3.3% CAGR through convenience food demand, chilled deli counter expansion in Japanese supermarkets, and premium charcuterie development above standard ham and sausage commodity category. Chicken grows at ~3.1% CAGR through karaage (Japanese fried chicken) convenience product expansion, health-conscious consumer shift toward below-pork single lower-fat protein, and bento lunch box chicken component demand.

Executive Summary

Japan meat market reached USD 37.15 Billion in 2025, driven by rising protein consumption, evolving dietary preferences, and increasing demand for convenient and premium meat products. Growing consumption of beef, pork, and poultry, supported by expanding retail distribution and foodservice channels, continues to strengthen market demand. Consumers are increasingly seeking high-quality, value-added, and ready-to-cook meat products that align with busy lifestyles and changing eating habits. The market is projected to reach USD 48.64 Billion by 2034.

Raw meat at 62.4% leads through Japan's fresh meat supermarket counter, restaurant fresh beef, and daily household cooking, creating Japan's most commercially fresh-oriented above-processed single consumer meat purchase preference. Pork at 34.8% leads the product through Japan's pork consumption cultural norm. Kanto leads at 36.9% through Tokyo's metropolitan consumer concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Raw Meat - 62.4% share (2025) |

| Dominant Product | Pork - 34.8% share (2025) |

|

Leading Region |

Kanto Region – 36.9% share (2025) |

|

Market Opportunity |

Export premium brand development; processed meat convenience product expansion; plant-based hybrid meat; school lunch and institutional processed meat supply; cold chain-enabled regional specialty meat nationwide distribution |

Key Analytical Observations Supporting The Above Data:

- Raw Meat at 62.4%: The raw meat segment dominates due to strong household and foodservice demand for fresh beef, pork, chicken, and seafood-based meat preparations. Its dominance is supported by Japanese consumers’ preference for cooking fresh meat at home and using raw meat in traditional and daily meals.

- Pork at 34.8%: The pork segment dominates due to its affordability, versatility, and widespread use in popular Japanese dishes. Strong household consumption and consistent demand from restaurants and foodservice establishments further reinforce its leading market position.

- Kanto Region at 36.9%: Kanto region dominates due to its large urban population, strong foodservice sector, and high concentration of supermarkets, restaurants, and convenience stores. Tokyo and the surrounding areas drive steady demand for fresh, processed, and premium meat products.

Japan Meat Market Overview

Japan meat market is growing steadily, supported by rising per capita meat consumption, strong demand for pork, poultry, beef, and processed meat products. The market is driven by household consumption, foodservice recovery, premium meat demand, and expanding ready-to-cook product availability. Imports also play an important role in ensuring a stable supply and meeting Japan’s diverse meat consumption needs.

Japan's meat market ecosystem integrates domestic livestock farming, import meat traders, slaughter and processing, wholesale distribution, and multi-channel retail distribution. Macroeconomic factors include rising disposable income, urbanization, strong foodservice demand, and increasing preference for protein-rich diets.

Market Dynamics

To evaluate market opportunities, Request Sample

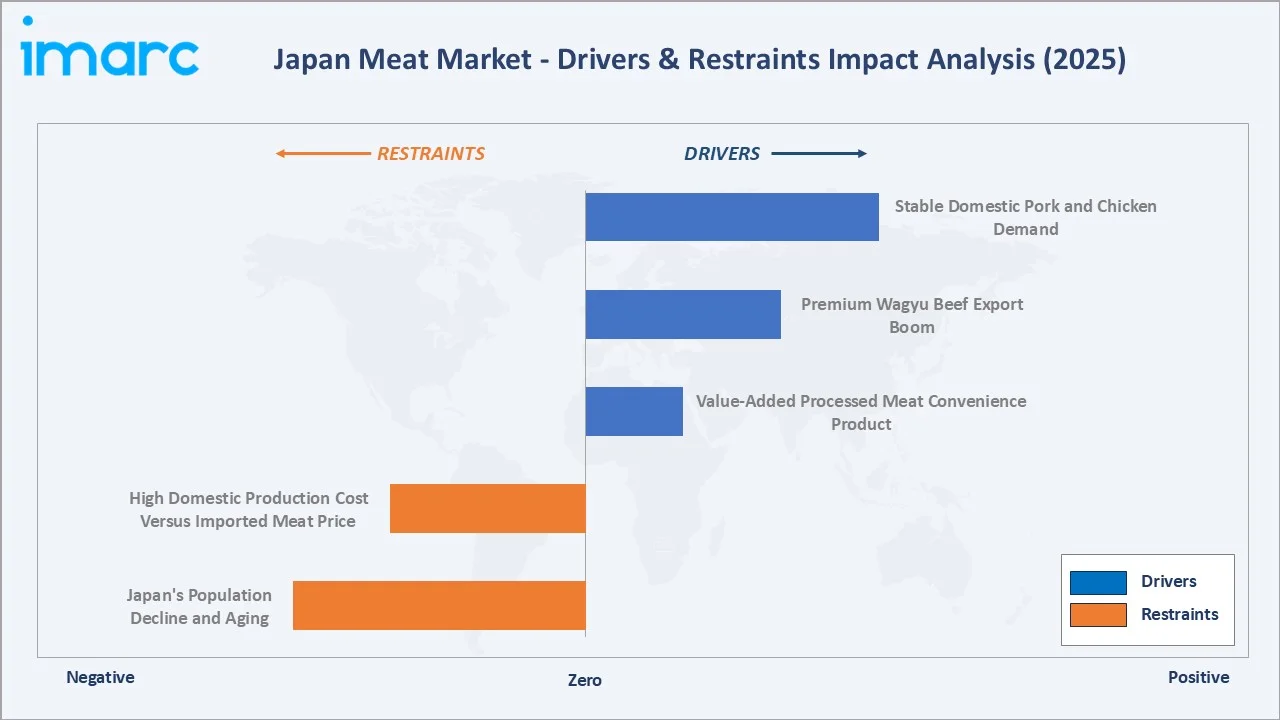

Market Drivers

- Stable Domestic Pork and Chicken Demand: Stable domestic pork and chicken demand is driving the market as these proteins remain affordable, widely available, and deeply integrated into everyday Japanese diets. Pork is a staple ingredient in popular dishes such as tonkatsu, ramen, and gyoza, while chicken is extensively consumed in home cooking and foodservice. Consistent consumer preference for these meats supports stable sales volumes across retail and restaurant channels. Their relatively lower prices compared to beef also help sustain demand during periods of economic uncertainty.

- Premium Wagyu Beef Export Boom: Japan exported 12,628 tons of beef in 2025, registering a 17% increase from the previous year, according to the ministry’s latest “Wagyu Supply and Demand Trends” report. Taiwan led export demand with a 21% share, followed by the United States at 20% and Hong Kong at 17%, with these three markets together accounting for nearly 60% of total exports, highlighting the rising global appeal of Japanese Wagyu beef. This premium Wagyu beef export growth is strengthening demand for high-value, specialty meat products. Rising global preference for authentic Japanese Wagyu supports premium pricing and improves revenue opportunities for producers and processors. It also encourages investment in quality control, branding, traceability, and export-oriented supply chains. This helps position Japan as a key supplier of premium meat in international markets.

- Value-Added Processed Meat Convenience Product: Value-added processed meat convenience products meet demand for quick, easy-to-cook, and ready-to-eat meal options. Products such as sausages, ham, bacon, marinated meats, meatballs, and packaged deli meats appeal to busy households and working consumers. These items offer longer shelf life, portion convenience, and consistent taste. Rising demand through supermarkets, convenience stores, and foodservice channels is further supporting market growth.

Market Restraints

- Japan's Population Decline and Aging: Japan’s births fell to 671,236 in 2025, decreasing by 14,937 from the previous year. According to demographic data from the Ministry of Health, Labor and Welfare, births remained below 700,000 for the second consecutive year and reached a record low for the tenth straight year since comparable records began in 1899. This population decline and aging are hampering the Japan meat market by reducing the overall consumer base and slowing long-term demand growth. Older consumers generally prefer smaller meal portions and may shift toward lighter diets with lower meat consumption. A shrinking working-age population also affects foodservice demand and labor availability across the meat supply chain. These demographic trends create challenges for sustained volume growth in the market.

- High Domestic Production Cost Versus Imported Meat Price: High domestic production costs are hampering the market as local producers face expensive feed, labor, land, and compliance costs. Imported meat is often available at more competitive prices, making it difficult for domestic suppliers to maintain price competitiveness. This puts pressure on margins and can shift consumer and foodservice demand toward lower-cost imported beef, pork, and poultry. As a result, domestic meat producers face challenges in scaling production and sustaining profitability.

Market Opportunities

- Wagyu Overseas Market Expansion: Wagyu overseas market expansion is increasing demand for premium Japanese beef. Growing consumer interest in high-quality, traceable, and luxury meat products in markets such as the United States, Taiwan, Hong Kong, and Southeast Asia is supporting export growth. Rising exports enable producers to command premium prices and invest further in breeding, branding, and quality assurance. This strengthens Japan’s position as a leading supplier of premium beef in the global market.

- Plant-Based Meat Hybrid Product: Plant-based meat hybrid products combine traditional meat with plant-based ingredients to offer healthier and more sustainable protein options. These products appeal to flexitarian consumers seeking to reduce meat consumption without compromising on taste and texture. They also help manufacturers address environmental concerns and diversify their product portfolios. As health awareness and sustainability preferences grow, demand for hybrid meat products is expected to increase across retail and foodservice channels.

Market Challenges

- Price Sensitivity Among Consumers: Price sensitivity among consumers is a challenging as rising food and living costs encourage shoppers to seek lower-cost protein options. Consumers may reduce purchases of premium meats such as Wagyu or switch to cheaper imported meat and alternative protein products. This can limit pricing flexibility for producers and retailers while putting pressure on profit margins. As a result, maintaining demand for higher-value meat products becomes increasingly difficult during periods of economic uncertainty.

- Disease Outbreak Risks in Livestock: Disease outbreak risks in livestock pose a significant challenge as outbreaks such as avian influenza and swine fever can disrupt production and reduce livestock populations. These incidents often lead to supply shortages, increased biosecurity costs, and higher meat prices. Trade restrictions and import-export disruptions may also occur, affecting market stability. As a result, producers and suppliers face operational uncertainty and pressure on profitability.

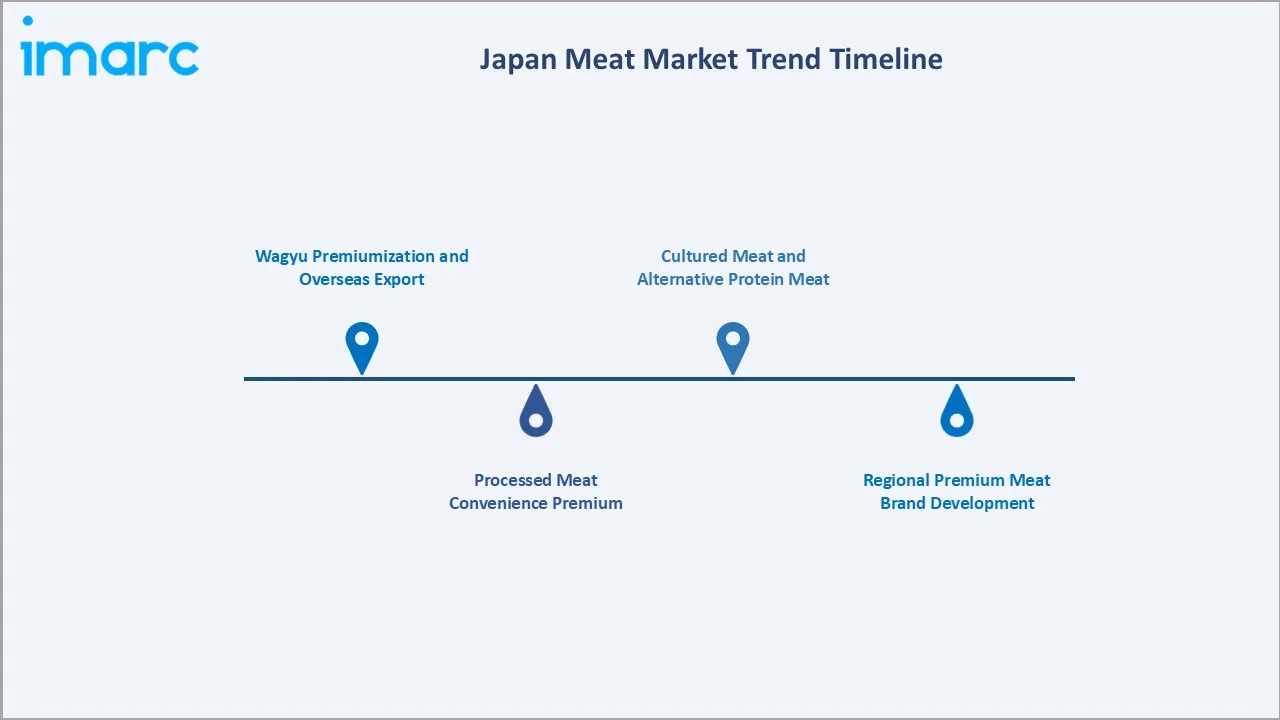

Emerging Market Trends

1. Wagyu Premiumization and Overseas Export

Wagyu premiumization and overseas export are emerging as global demand for high-quality, traceable, and luxury beef continues to increase. Producers are focusing on branding, quality certification, and premium product differentiation to capture higher-value international markets. Growing exports to regions such as North America, Asia, and the Middle East are strengthening revenue opportunities. This trend is encouraging investment in breeding programs, supply chain traceability, and premium meat production standards.

2. Processed Meat Convenience Premium

Processed meat convenience premium is emerging as consumers seek quick, high-quality, and ready-to-eat protein options. Premium sausages, ham, bacon, deli meats, marinated cuts, and frozen meat meals are gaining popularity among busy households and working consumers. These products offer convenience, consistent taste, and longer shelf life while supporting higher margins for brands. The trend is also encouraging innovation in packaging, portion control, and health-focused meat formulations.

3. Regional Premium Meat Brand Development

Regional premium meat brand development is emerging as local producers promote branded beef, pork, and poultry linked to specific prefectures and production methods. These regional brands highlight quality, traceability, freshness, and unique taste profiles to attract premium consumers. The trend supports higher product differentiation in both domestic retail and foodservice channels. It also helps rural producers improve margins and strengthen Japan’s premium meat identity.

4. Cultured Meat and Alternative Protein Meat

Cultured meat and alternative protein meat are emerging as consumers and companies explore sustainable protein sources beyond conventional livestock. Cultured meat, plant-based meat, and hybrid protein products can help address concerns over food security, emissions, and livestock production costs. These products also appeal to health-conscious and flexitarian consumers seeking a meat-like taste with lower environmental impact. In February 2025, YUKIGUNI FACTORY CO., LTD. launched a new “Mushroom Meat” product series made from maitake mushrooms. The range includes ready-to-cook Mushroom Meat, sauced variants in tomato, garlic oil, and sesame flavors, and Yukiguni Maitake Rice Seasoning, with each 50g pack offering 3.7g of dietary fiber along with ingredients such as rice protein, milk protein, and vegetable oil. Such launches help attract health-conscious and flexitarian consumers while offering sustainable, fiber-rich alternatives to conventional meat in Japan’s evolving protein market.

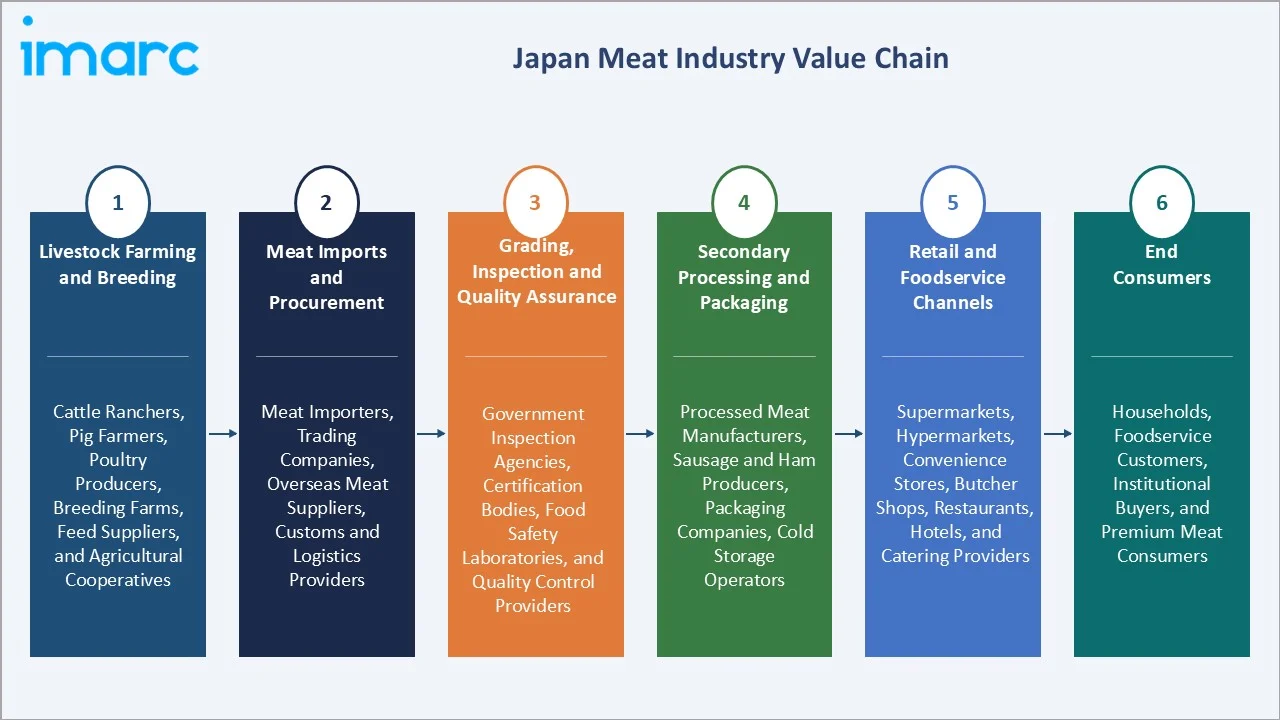

Industry Value Chain Analysis

Japan meat value chain integrates livestock farming & breeding, meat imports & procurement, grading, inspection & quality assurance, secondary processing & packaging, retail & foodservice channels, and end consumers.

|

Stage |

Key Participants |

| Livestock Farming & Breeding | Cattle ranchers, pig farmers, poultry producers, breeding farms, feed suppliers, and agricultural cooperatives |

| Meat Imports & Procurement | Meat importers, trading companies, overseas meat suppliers, customs and logistics providers |

| Grading, Inspection & Quality Assurance | Government inspection agencies, certification bodies, food safety laboratories, and quality control providers |

| Secondary Processing & Packaging | Processed meat manufacturers, sausage and ham producers, packaging companies, cold storage operators |

| Retail & Foodservice Channels | Supermarkets, hypermarkets, convenience stores, butcher shops, restaurants, hotels, and catering providers |

| End Consumers | Households, foodservice customers, institutional buyers, and premium meat consumers |

Grading is Japan's most commercially distinctive value chain stage because it determines the quality, marbling, yield, and market value of meat products, particularly Wagyu beef. Japan’s rigorous grading and traceability systems enhance consumer trust, support premium pricing, and strengthen the global reputation of Japanese meat in domestic and export markets.

Technology Landscape in the Japan Meat Industry

Grading Technology and AI Marbling Assessment

Grading technology and AI marbling assessment enable more accurate, consistent, and objective evaluation of meat quality, particularly for premium Wagyu beef. AI-powered imaging systems can analyze marbling patterns, color, texture, and yield characteristics with greater precision than traditional manual assessments. These technologies improve grading efficiency, enhance traceability, and support standardized quality control across the supply chain. As demand for premium and export-grade meat grows, AI-based grading solutions are becoming increasingly important for maintaining quality and market competitiveness.

Robotics in Meat Processing Plants

Robotics in meat processing plants automates labor-intensive tasks such as cutting, deboning, trimming, packaging, and quality inspection. This helps processors address labor shortages and improve operational efficiency while maintaining consistent product quality. In October 2025, a new collaboration was launched between Fatland Oslo, Japan-based MAYEKAWA, and Animalia to advance the development of CELLDAS, an innovative deboning robot. The technology is designed to make meat cutting safer and more efficient while reducing physical strain on slaughterhouse workers. MAYEKAWA’s automation expertise supports the processing of irregular and flexible pork, chicken, and turkey cuts, enabling tasks traditionally performed manually or through large-scale systems unsuitable for smaller production volumes. Robotic systems also enhance food safety by reducing direct human handling and minimizing contamination risks. As processing facilities seek higher productivity and precision, the adoption of advanced robotics continues to accelerate across the industry.

IoT-Based Livestock Health Monitoring

IoT-based livestock health monitoring using connected sensors, wearables, and farm management platforms to track animal health, movement, feed intake, and environmental conditions in real time. These systems help farmers detect illness early, reduce mortality, and improve productivity. They also support better traceability and quality control across the meat supply chain. As Japan faces labor shortages in livestock farming, IoT tools are becoming important for efficient and data-driven animal management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Raw |

62.4% |

2025 |

|

Product |

Pork |

34.8% |

2025 |

|

Distribution Channel |

🔒 |

🔒 |

2025 |

|

Region |

Kanto Region |

36.9% |

2025 |

By Type

Raw meat leads at 62.4% (2025). Japan's raw meat market encompasses fresh supermarket counter pork, beef, and chicken, restaurant thin-sliced beef and pork, and household cooking daily pork and chicken purchase, creating Japan's most commercially above-convenience-food single daily fresh protein procurement culture through Japan's above-other-developed-nation single fresh-first consumer food philosophy.

To access detailed market analysis, Request Sample

Processed meat at 37.6% grows fastest at ~3.3% CAGR through ham, sausage, convenience deli, premium charcuterie, school lunch supply, and value-added convenience products.

By Product

Pork leads at 34.8% (2025), through Japan's high pork consumption. Chicken at 29.6% grows fastest at ~3.1% CAGR through karaage, health-consciousness, and hot case expansion. Beef at 21.7% generates Japan's highest per-unit above-pork single revenue premium through wagyu's above-standard pricing.

Mutton at 6.3% serves traditional and cultural preferences. Others at 7.6% includes horse meat, duck, game meat, and processed meat components above the conventional four species.

Regional Market Insights

|

Region |

Market Share (2025) |

Key Japan Meat Market Drivers & Characteristics |

|

Kanto |

36.9% |

Driven by its large population base, strong foodservice industry, extensive retail network, and high consumption of beef, pork, poultry, and processed meat products. |

|

Kinki |

18.7% |

Strong restaurant activity, premium meat consumption, and well-developed distribution channels contribute to regional market growth. |

|

Central/Chubu |

14.8% |

Benefits from its large manufacturing workforce, growing urban population, and strong retail presence. |

|

Kyushu-Okinawa |

9.3% |

Plays an important role in Japan’s meat industry due to its significant livestock farming activities, particularly in beef and pork production. |

|

Tohoku |

7.2% |

Supported by agricultural and livestock production, along with growing demand for meat products through supermarkets and local foodservice channels. |

|

Chugoku |

5.5% |

Benefits from steady consumer demand, established food processing operations, and expanding distribution networks. |

|

Hokkaido |

4.3% |

Recognized for its livestock farming and high-quality meat production, particularly beef and dairy-related products. |

|

Shikoku |

3.3% |

Represents a smaller but stable market, supported by regional meat production, local consumption, and increasing availability of processed and convenience meat products through modern retail channels. |

Kanto's 36.9% dominance reflects Tokyo's metropolitan consumer concentration, the highest-density supermarket meat counter, and Japan's largest restaurant cluster. Kinki's 18.7% reflects Osaka's pork cultural intensity, beef premium brand, and above-national per-capita food expenditure. Chubu's 14.8% reflects chicken wing culture, beef premium, and worker institutional meal demand.

Kyushu-Okinawa's 9.3% reflects dual premium beef and pork production and Okinawa's above-mainland pork cultural intensity. Tohoku's 7.2% reflects Japan's most commercially livestock-production-concentrated above-consumer single regional meat supply geography. Hokkaido's 4.3% significantly understates production significance as Japan's most commercially significant livestock. Shikoku's 3.3% reflects Japan's smallest regional meat market served by chicken and cattle.

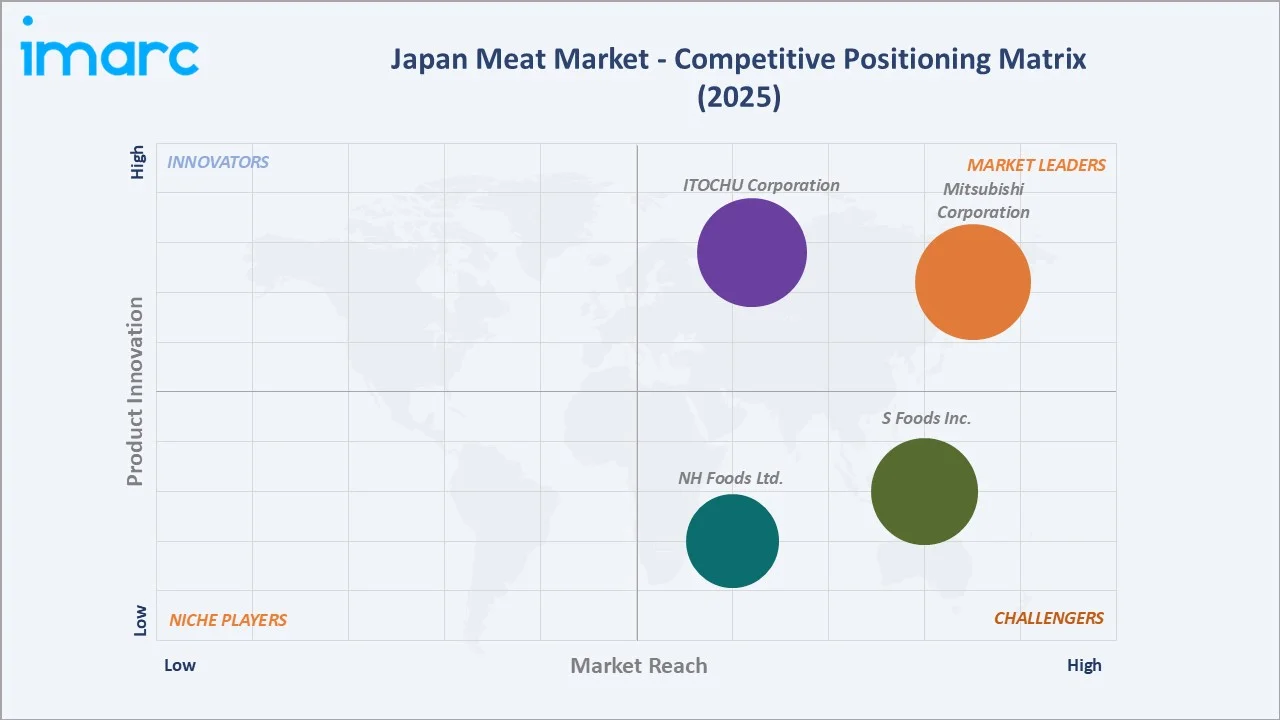

Competitive Landscape

Japan meat competitive landscape is commercially stratified between Japan's major integrated meat companies, import-specialist wholesalers, regional specialists, and institutional food service suppliers.

|

Company Name |

Key Products |

Market Position |

Core Strength |

| Mitsubishi Corporation | Chicken, Pork, Beef, Processed Meat Products |

Market Leader |

Mitsubishi Corporation plays a major role in Japan's meat industry through a comprehensive, end-to-end approach, ranging from traditional livestock production to the development of next-generation cultivated meat. |

| ITOCHU Corporation | Chilled And Frozen Pork, Beef, and Other Meats |

Market Leader |

ITOCHU Corporation plays a central role in Japan's meat industry, managing a comprehensive, vertically integrated value chain from global sourcing to domestic retail. |

| NH Foods Ltd. | Beef and Pork |

Strong Challenger |

NH Foods Ltd. is a dominant leader in Japan's meat industry, managing a comprehensive, vertically integrated system that spans farming, slaughtering, processing, and distribution. |

| S Foods Inc. | Multiple mobile titles, Nintendo mobile partnership | Strong Challenger | S Foods Inc. plays a comprehensive, integrated role in the Japanese meat industry, specializing in beef and pork meat. |

Japan's meat competitive landscape is evolving through three forces: wagyu premium export demand, plant-based hybrid development, and convenience processed meat premiumization.

Key Company Profiles

NH Foods Ltd.

NH Foods Ltd. is one of Japan’s largest meat processing and food manufacturing companies, with a strong presence across the domestic meat value chain. Its product portfolio includes fresh pork, beef, poultry, mutton, and value-added convenience foods.

- Key Products: Beef, Pork, Chicken Meat, Mutton.

- Strategic Focus: Strengthening its integrated meat value chain through livestock production, meat processing, premium product development, and nationwide distribution.

Mitsubishi Corporation

Mitsubishi Corporation is one of Japan’s largest trading and investment companies and a significant participant in the country’s meat market through its food industry operations. The company is involved in the procurement, import, processing, distribution, and sale of beef, pork, poultry, and processed meat products, leveraging its extensive global sourcing network and supply chain capabilities.

- Key Products: Chicken, Pork, Beef, Processed Meat Products.

- Strategic Focus: Securing a stable and diversified meat supply through its global procurement network, strategic investments in livestock and food processing businesses, and integrated distribution operations.

Market Concentration Analysis

Japan meat market is commercially concentrated at the branded processed meat tier and moderately fragmented at the fresh meat retail tier through independent butcher shops competing for daily fresh meat consumer purchases. Japan's processed ham and sausage market is Japan's most commercially concentrated above-fresh-meat single sub-category. The market benefits from strong vertical integration, particularly in livestock production, meat processing, cold chain logistics, and retail supply. However, regional meat producers, specialty Wagyu suppliers, and importers also contribute to competition. Product quality, traceability, branding, and value-added processed meat offerings remain key competitive differentiators.

Investment & Growth Opportunities

Highest Growth Segments

Processed meat premium convenience (~3.3% CAGR), chicken karaage convenience product (~3.1% CAGR), wagyu export to Middle East and Southeast Asia (~8-12% CAGR through luxury protein demand), plant-based hybrid processed meat (~8-15% CAGR from small base), senior institutional prepared meat for care facility (~6-8% CAGR), and online D2C wagyu gift (~10-15% CAGR through e-commerce premium food adoption) represent Japan's highest-growth meat investment vectors through 2034.

Investment Themes

- Wagyu export premium brand development: Japan's wagyu export record, creating Japan's most commercially above-domestic-ceiling single international premium beef revenue growth vector. Investment in wagyu processing and Singapore premium restaurant relationship creates Japan's most commercially above-domestic-price single export-premium wagyu revenue.

- Plant-based hybrid processed meat for Japan's health-conscious convenience consumer: Japan's established plant protein food culture, creating Japan's most commercially successful plant-hybrid processed meat consumer acceptance context. Investment in soy-protein and pea-protein hybrid processed meat creates demand for a health-enhanced processed meat category above pure animal protein competitors without equivalent plant-protein above-health single consumer appeal.

Future Market Outlook (2026-2034)

Japan meat market is projected to grow from USD 37.15 Billion in 2025 to USD 48.64 Billion by 2034, delivering a 2.95% CAGR over the forecast period. The market's anchor value of USD 42.96 Billion in 2030 represents Japan's meat industry at stable maturity. The Japan meat market is expected to witness steady growth in the coming years, supported by rising per capita meat consumption, increasing demand for premium Wagyu beef, and the expansion of value-added processed meat products. Continued innovation in meat processing, cold chain infrastructure, and traceability technologies will enhance product quality and supply chain efficiency. Export opportunities for high-quality Japanese meat, particularly Wagyu, are likely to strengthen market value.

Three structural forces define Japan's meat market through 2034: meat international commercial expansion, processed meat convenience premiumization, and plant-based hybrid meat's progressive Japan domestic market development.

Research Methodology

Primary Research

Primary research comprised structured interviews with Japan meat market stakeholders (2025), including directors, product managers, senior graders, fresh meat category buyers, and a consumer survey from Japan fresh and processed meat buyers.

Secondary Research

Secondary research encompassed Japan livestock production and trade statistics, Japan food safety recall database, Japan beef grading statistics, and company annual reports. Over 40 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using the protein expenditure model: Japan total household meat expenditure extrapolated with demographic adjustment, plus institutional and food service meat volume from food chain statistics.

Japan Meat Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Raw, Processed |

| Products Covered | Chicken, Beef, Pork, Mutton, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Departmental Stores, Specialty Stores, Online Stores, Others |

| Regions Covered | Kanto Region, Kinki Region, Central/Chubu Region, Kyushu/Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region. |

| Companies Covered | Mitsubishi Corporation, ITOCHU Corporation, NH Foods Ltd., S Foods Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Japan meat market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Japan meat market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Japan meat industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Japan Meat Market Report

The Japan meat market reached USD 37.15 Billion in 2025, driven by steady demand for pork, chicken, beef, and processed meat products across households and foodservice channels. Rising per capita meat consumption, premium Wagyu demand, and growth in ready-to-cook/value-added meat products are supporting market expansion. Strong imports and improved cold chain distribution further ensure a stable supply across the country.

The Japan meat market grows at 2.95% CAGR during 2026-2034, reaching USD 48.64 Billion by 2034. The moderate CAGR reflects Japan's mature market structure, where value premiumization through wagyu and premium processed meat sustains above-volume-only single revenue growth against Japan's structurally declining above-demographic-certain population base.

Raw meat leads at 62.4% through Japan's consumer food philosophy, creating the most commercially fresh-oriented above-convenience single developed-nation meat purchase culture through daily supermarket fresh counter shopping, restaurant table-grill fresh beef service, and Japan's traditional raw meat preparations.

Pork leads at 34.8% through Japan's pork consumption, creating Japan's most commercially dominant pork culture.

Kanto region leads at 36.9% through Tokyo's metropolitan population, creating the most commercially concentrated single urban meat consumption geography.

Leading companies include Mitsubishi Corporation, ITOCHU Corporation, NH Foods Ltd., and S Foods Inc., among others.

The Japan meat market is projected to reach approximately USD 42.96 Billion by 2030, with wagyu export demand, processed meat premium, and senior institutional prepared meat growth.

Three priority investment opportunities: Wagyu export premium brand development, plant-based hybrid processed meat for Japan's health-conscious convenience consumers, and senior institutional prepared meat for Japan's above-school single fastest-growing care facility meal service market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)