Japan Medical Automation Market Size, Share, Trends and Forecast by Application, End User, and Region, 2026-2034

Japan Medical Automation Market Summary:

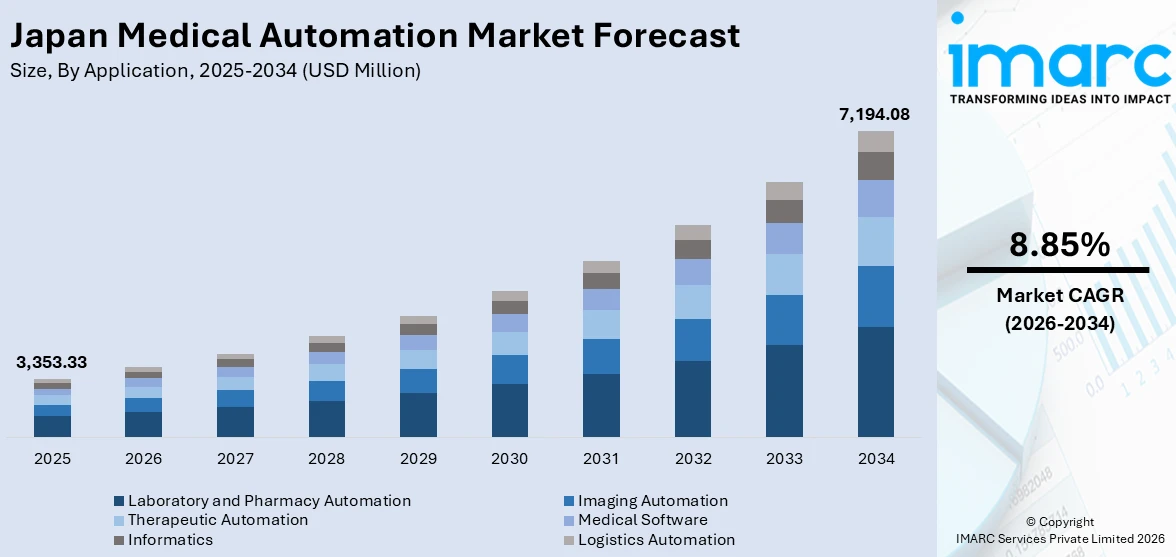

The Japan medical automation market size was valued at USD 3,353.33 Million in 2025 and is projected to reach USD 7,194.08 Million by 2034, growing at a compound annual growth rate of 8.85% from 2026-2034.

Japan’s medical automation market is experiencing strong expansion, propelled by the nation’s accelerating digital healthcare transformation, rising demand for precision diagnostics, and the integration of advanced robotics across clinical workflows. The convergence of artificial intelligence with laboratory systems, pharmacy dispensing solutions, and imaging platforms is reshaping care delivery. Increasing institutional investments in automated infrastructure and supportive regulatory frameworks continue to strengthen the Japan medical automation market share.

Key Takeaways and Insights:

- By Application: Laboratory and pharmacy automation dominates the market with a share of 38.6% in 2025, owing to the escalating need for high-throughput diagnostic testing, precision dispensing capabilities, and streamlined sample processing workflows across clinical and pharmaceutical settings. Growing adoption of robotic sample handlers is fueling the market expansion.

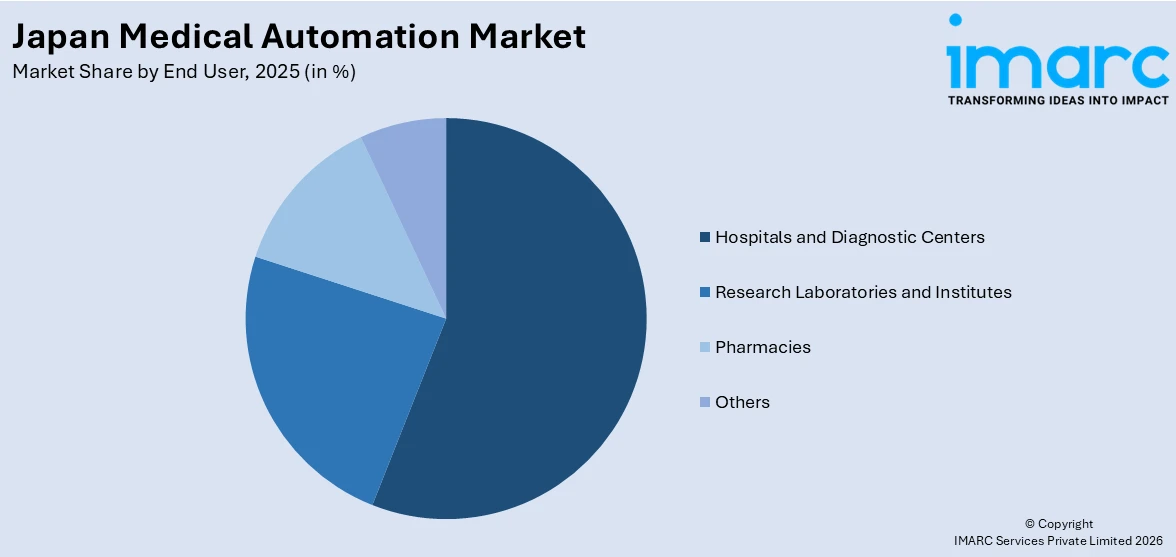

- By End User: Hospitals and diagnostic centers lead the market with a share of 56.2% in 2025. This dominance is driven by the concentration of advanced diagnostic equipment, large patient volumes requiring automated workflows, and institutional capacity to invest in integrated automation platforms that enhance operational efficiency and clinical accuracy.

- By Region: Kanto Region is the largest region with 34.8% share in 2025, driven by the concentration of leading tertiary hospitals, research institutions, and medical technology clusters within the Greater Tokyo metropolitan area, alongside higher healthcare expenditure and early adoption of digital infrastructure.

- Key Players: Key players drive the Japan medical automation market by expanding product portfolios, enhancing robotic precision and AI-driven diagnostic capabilities, and strengthening distribution networks. Their investments in research, strategic partnerships with healthcare institutions, and development of next-generation laboratory and pharmacy automation systems accelerate adoption and ensure consistent availability across diverse clinical settings.

To get more information on this market Request Sample

Japan’s medical automation landscape is fundamentally shaped by the nation’s demographic imperatives and technological ambitions. As the country contends with one of the world’s most rapidly aging populations, the healthcare sector is leveraging automation to sustain service quality amid mounting workforce pressures. Advanced laboratory systems, pharmacy dispensing robots, and AI-integrated imaging platforms are being deployed across hospitals and diagnostic centers to reduce manual intervention, enhance diagnostic accuracy, and optimize resource allocation. The government’s Medical Digital Transformation Promotion Plan, introduced to accelerate digitization of healthcare infrastructure, has catalyzed institutional investment in automated clinical workflows and interoperable data systems. From April 2025, medical institutions and pharmacies have been required to meet minimum thresholds for the utilization of the My Number Card as a health insurance card under the Medical DX Promotion Infrastructure Development Add-on, further incentivizing the adoption of digital infrastructure. The convergence of robotics, artificial intelligence, and informatics is creating comprehensive automation ecosystems that span diagnostics, therapeutics, and logistics, enabling healthcare facilities to deliver patient-centered care with unprecedented efficiency and precision across Japan’s diverse regional healthcare networks.

Japan Medical Automation Market Trends:

Integration of Artificial Intelligence in Clinical Diagnostic Workflows

Japan’s healthcare sector is witnessing accelerated integration of artificial intelligence into diagnostic processes, particularly in medical imaging and pathology analysis. The Pharmaceuticals and Medical Devices Agency is expanding its IDATEN framework, which permits pre-approved improvement plans for AI-based software as a medical device, removing the need for regulatory re-approval with each update. This streamlined approach is enabling rapid deployment of adaptive diagnostic algorithms across hospitals, enhancing detection accuracy for conditions ranging from gastrointestinal cancers to neurological disorders while reducing clinician workload.

Expansion of Robotic Automation in Pharmaceutical and Laboratory Settings

Pharmaceutical and clinical laboratories across Japan are increasingly deploying autonomous robotic systems to manage high-throughput screening, sample handling, and drug discovery processes. Mobile robots, dual-armed automated platforms, and AI-orchestrated software are being integrated into research facilities to minimize human error and accelerate data generation. The growing commitment of Japanese pharmaceutical firms to laboratory automation is evident through dedicated research facilities focused on robotics and sophisticated software development. This trend reflects the broader industry shift toward continuous autonomous operation and intelligent workflow orchestration in pharmaceutical research environments.

Government-Driven Healthcare Digitalization and Interoperability Mandates

Japan is advancing comprehensive digital health infrastructure through regulatory mandates and incentive frameworks designed to modernize healthcare delivery. The government is transitioning to unified digital health insurance identification systems, enabling seamless access to patient health information across institutions. National digitalization initiatives are standardizing electronic medical records and expanding the scope of shareable medical data, creating an interconnected digital ecosystem that supports automation-enabled clinical decision-making and population health management. These coordinated efforts are establishing the foundational architecture necessary for widespread medical automation deployment.

.webp)

Market Outlook 2026-2034:

The Japan medical automation market is positioned for sustained expansion throughout the forecast period, supported by structural demographic shifts, technological innovation, and policy-driven digitalization of healthcare systems. The continued integration of robotics, artificial intelligence, and advanced informatics across clinical, laboratory, and pharmacy settings is expected to drive efficiency gains and improve patient outcomes nationwide. The market generated a revenue of USD 3,353.33 Million in 2025 and is projected to reach a revenue of USD 7,194.08 Million by 2034, growing at a compound annual growth rate of 8.85% from 2026-2034. Rising institutional investments in automated diagnostic platforms, coupled with favorable reimbursement policies for robot-assisted procedures and government incentives for digital infrastructure upgrades, are anticipated to accelerate market penetration across both urban and regional healthcare facilities throughout Japan.

Japan Medical Automation Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Application |

Laboratory and Pharmacy Automation |

38.6% |

|

End User |

Hospitals and Diagnostic Centers |

56.2% |

|

Region |

Kanto Region |

34.8% |

Application Insights:

- Imaging Automation

- Therapeutic Automation

- Laboratory and Pharmacy Automation

- Medical Software

- Informatics

- Logistics Automation

Laboratory and pharmacy automation dominates with a market share of 38.6% of the total Japan medical automation market in 2025.

Laboratory and pharmacy automation holds the leading position in the Japan medical automation market, driven by the growing demand for high-throughput diagnostic testing, precision dispensing, and workflow optimization across clinical and pharmaceutical environments. Japanese healthcare facilities are increasingly deploying automated liquid handling systems, robotic sample processors, and AI-driven analytical platforms to reduce manual errors and improve turnaround times. The government has set ambitious targets for pharmacy automation adoption, reflecting the national commitment to enhancing operational efficiency through technological integration in medication management and diagnostic processing workflows.

The rapid advancement of robotics and software orchestration is transforming how laboratories and pharmacies operate in Japan, enabling continuous autonomous operation and real-time data management. Automated compound libraries, integrated screening platforms, and robotic dispensing systems are being widely adopted to streamline drug discovery and reduce operational costs. The growing commitment of Japanese pharmaceutical firms toward establishing dedicated automation-focused research facilities underscores the deepening synergy between pharmaceutical innovation and laboratory automation capabilities. This convergence of intelligent robotics with sophisticated data management solutions is accelerating market expansion across clinical and research settings.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals and Diagnostic Centers

- Research Laboratories and Institutes

- Pharmacies

- Others

Hospitals and diagnostic centers lead with a share of 56.2% of the total Japan medical automation market in 2025.

Hospitals and diagnostic centers constitute the dominant end-user segment in the Japan medical automation market, supported by their large-scale diagnostic operations, substantial patient volumes, and institutional capacity for capital-intensive technology investments. These facilities are at the forefront of adopting surgical robots, automated imaging systems, and intelligent pharmacy dispensing solutions to enhance clinical precision and operational throughput. The expanding insurance reimbursement scope for robot-assisted procedures across multiple surgical specialties is incentivizing broader hospital adoption of automated surgical platforms, further reinforcing institutional commitment to technological modernization.

The integration of AI-powered diagnostic tools and robotic logistics systems within hospitals is fundamentally reshaping care delivery models, enabling real-time clinical decision support and reducing administrative burdens on healthcare professionals. Hospitals are deploying automated transport robots, intelligent medication dispensing cabinets, and AI-assisted imaging analysis platforms to address persistent workforce constraints. These autonomous logistics solutions navigate clinical environments independently, handling specimen transport and supply delivery tasks that previously consumed significant staff time, thereby freeing clinical personnel for direct patient care and improving overall operational efficiency across healthcare institutions.

Regional Insights:

- Kanto Region

- Kansai/Kinki Region

- Central/Chubu Region

- Kyushu-Okinawa Region

- Tohoku Region

- Chugoku Region

- Hokkaido Region

- Shikoku Region

The Kanto Region exhibits a clear dominance with 34.8% share of the total Japan medical automation market in 2025.

The Kanto Region, encompassing the Greater Tokyo metropolitan area, leads Japan's medical automation market owing to its dense concentration of advanced tertiary hospitals, prestigious research universities, and medical technology headquarters. The region benefits from the highest healthcare expenditure per capita, robust digital infrastructure, and early adoption of AI-driven diagnostic and robotic surgical systems. Tokyo functions as the nation's primary medical cluster, housing numerous national medical centers and academic institutions that serve as early adopters of cutting-edge automation technologies across clinical specialties.

The region's leadership position is further reinforced by its well-established ecosystem of medical device manufacturers, technology startups, and research-driven pharmaceutical companies that collaborate closely with healthcare institutions to pilot and scale innovative automation solutions. Proximity to regulatory agencies and government policy centers facilitates faster adoption of emerging technologies and streamlined approval processes. The Kanto Region consistently serves as the trendsetter for nationwide automation deployment, with successful implementations in its hospitals and laboratories frequently becoming models replicated across other regions throughout Japan.

Market Dynamics:

Growth Drivers:

Why is the Japan Medical Automation Market Growing?

Rapidly Aging Population Intensifying Healthcare Demand

One of the strongest global drivers for the use of medical automation is the demographics of Japan. The percentage of senior persons in the country is the highest in the world. The extraordinary need for healthcare services, such as long-term care, surgery, chronic illness management, and diagnostic testing, is being caused by this demographic reality. Hospitals and diagnostic facilities are under increasing strain to handle more patients while preserving clinical quality as the number of older people rises. In order to address this growing need, medical automation technologies, such as robotic surgical systems, automated laboratory equipment, and intelligent pharmacy dispensing platforms are becoming increasingly important. Robotic assistants aid in patient mobility and rehabilitation, while automated imaging devices improve the early diagnosis of age-related disorders. The long-term demand for automation solutions that allow healthcare institutions to provide comprehensive, high-quality care to an older patient population is guaranteed by the structural permanence of Japan's aging trajectory.

Acute Healthcare Workforce Shortage Accelerating Automation Adoption

Healthcare facilities in Japan are being forced to use automation as an operational requirement due to a severe and growing manpower shortage. The working-age population of the country has been continuously declining. Hospitals are having difficulty hiring enough nurses, lab technicians, and pharmacists, making medical services one of the industries with the worst labor shortages. Medical automation is evolving from an efficiency boost to a basic necessity for preserving operational continuity due to this structural staffing shortfall. AI-powered diagnostic imaging, automated sample processing systems, and robotic drug distribution lessen reliance on manual labor while increasing precision and efficiency. Clinical personnel can provide direct patient care as logistics robots take care of supply delivery and specimen transportation. Workforce shortages will continue to be the key factor driving automation investment across all types of healthcare facilities due to Japan's ongoing population decrease.

Government-Led Digital Transformation and Regulatory Support

Through extensive legislative frameworks, financial incentives, and regulatory modernization measures, the Japanese government is aggressively promoting the implementation of medical automation. The nation's healthcare infrastructure is using more cloud-based electronic medical records, AI-driven patient care systems, and interoperable data platforms according to the Medical Digital Transformation Promotion Plan, which was implemented to standardize and expedite healthcare digitalization. By creating frameworks that allow adaptive AI-based software to develop without needing full reapproval for every update, regulatory bodies are expediting the approval process for automated medical devices. The time and expense restrictions related to implementing new automation technology are greatly decreased by these actions. Institutional investment is further encouraged by financial incentives, such as reimbursement policies for robot-assisted surgical operations and subsidies for upgrades to digital infrastructure. In order to create a supportive ecosystem that methodically encourages the development, deployment, and scaling of medical automation solutions nationwide, the government's Society 5.0 initiative specifically encourages the integration of robotics, artificial intelligence, and digital technologies across the healthcare and senior care sectors.

Market Restraints:

What Challenges the Japan Medical Automation Market is Facing?

High Implementation and Maintenance Costs Limiting Broader Adoption

The high cost of purchasing, setting up, and maintaining sophisticated medical automation systems is a major deterrent to their broad use, especially in smaller regional and rural healthcare institutions. Comprehensive laboratory automation systems, robotic surgical platforms, and integrated pharmacy dispensing solutions come with high initial expenditures in addition to continuing costs for software license, technical maintenance, and specialist training. Large-scale automation initiatives are financially difficult to finance without outside support systems because many public hospitals in Japan have tight budgets and medical care prices that have not kept up with growing operating expenses.

Cybersecurity Vulnerabilities in Interconnected Medical Systems

Healthcare organizations are more vulnerable to cybersecurity risks that might jeopardize patient safety and interfere with clinical operations due to the increased interconnectedness of automated medical equipment and healthcare information systems. Notable ransomware attacks on hospital electronic medical record systems have occurred in Japan; these attacks have resulted in the disruption of outpatient services and the prolonged use of paper-based processes. The potential attack surface grows significantly as medical automation systems become more networked and data-dependent, necessitating ongoing investments in security infrastructure, employee training, and adherence to changing cybersecurity standards set forth by the Ministry of Health, Labour, and Welfare.

Interoperability Challenges Across Healthcare Institutions

The full potential of medical automation is nevertheless constrained by the ongoing difficulty of achieving seamless data interchange and system integration across Japan's heterogeneous and fragmented healthcare sector. Disparate electronic medical record systems, diagnostic platforms, and automation technologies are often used by various hospitals, clinics, and labs without defined communication protocols. Data silos are produced by this fragmentation, which also makes it more difficult to establish linked automation ecosystems and prevents coordinated patient care. The difficulty of harmonizing disparate institutional IT designs and adapting outdated systems continues to impede the development of complete interoperability, despite government efforts to encourage standardization.

Competitive Landscape:

Established international medical technology companies coexist with creative local businesses in Japan's medical automation sector, which offers a varied competitive environment. In order to improve accessibility throughout metropolitan and regional markets, market participants compete via ongoing product innovation, strategic alliances with healthcare organizations, and service network growth. Businesses are making large investments in R&D to improve integrated automation platforms, robotic accuracy, and AI-driven diagnostic capabilities. Collaborations between government agencies, university research institutions, and technology companies to create next-generation medical automation solutions further influence the competitive landscape. To increase product portfolios and improve market positioning, mergers, acquisitions, and licensing agreements are often used tactics. Government initiatives that promote domestic innovation and lessen reliance on foreign technology have contributed to the growing emphasis on creating automation systems that are produced domestically.

Japan Medical Automation Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Applications Covered |

Imaging Automation, Therapeutic Automation, Laboratory and Pharmacy Automation, Medical Software, Informatics, Logistics Automation |

|

End Users Covered |

Hospitals and Diagnostic Centers, Research Laboratories and Institutes, Pharmacies, Others |

|

Regions Covered |

Kanto Region, Kansai/Kinki Region, Central/Chubu Region, Kyushu-Okinawa Region, Tohoku Region, Chugoku Region, Hokkaido Region, Shikoku Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Japan Medical Automation Market Report

The Japan medical automation market size was valued at USD 3,353.33 Million in 2025.

The Japan medical automation market is expected to grow at a compound annual growth rate of 8.85% from 2026-2034 to reach USD 7,194.08 Million by 2034.

Laboratory and pharmacy automation dominated the market with a share of 38.6%, driven by rising demand for high-throughput diagnostic testing, precision dispensing capabilities, and workflow optimization across clinical and pharmaceutical environments in Japan.

Key factors driving the Japan medical automation market include the rapidly aging population intensifying healthcare demand, acute workforce shortages compelling automation adoption, and government-led digital transformation initiatives providing regulatory support and financial incentives.

Major challenges include high implementation and maintenance costs limiting broader adoption among smaller facilities, cybersecurity vulnerabilities in interconnected medical systems, interoperability challenges across diverse healthcare institutions, regulatory compliance complexities, and regional disparities in digital infrastructure readiness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)